CHAPTER 19

Managerial Accounting

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

A

Problems

*1. Identify the features of

managerial accounting and

the functions of

management.

1, 2, 3, 4, 5,

6, 7, 8

1, 2

1

1

*2. Describe the classes of

manufacturing costs and the

differences between product

and period costs.

9, 11, 12, 13,

14

3, 4, 5, 6

2

2, 3, 4, 5, 6,

7, 13

1A, 2A

*3. Demonstrate how to compute

cost of goods manufactured

and prepare financial

statements for a

manufacturer.

10, 15, 16, 17,

18, 19, 20, 21

7, 8, 9, 10

3

8, 9, 10, 11,

12, 13, 14, 15,

16, 17

3A, 4A, 5A

*4. Discuss trends in managerial

accounting.

22, 23, 24, 25,

26

11

4

18

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A

Classify manufacturing costs into different categories and

compute the unit cost.

Simple

20–30

2A

Classify manufacturing costs into different categories and

compute the unit cost.

Simple

20–30

3A

Indicate the missing amount of different cost items, and

prepare a condensed cost of goods manufactured schedule,

an income statement, and a partial balance sheet.

Moderate

30–40

4A

Prepare a cost of goods manufactured schedule, a partial

income statement, and a partial balance sheet.

Moderate

30–40

5A

Prepare a cost of goods manufactured schedule and a

correct income statement.

Moderate

30–40

BLOOM’ S TAXONOMY TABLE

Correlation Chart between Bloom’s Taxonomy, Learning Objectives and End–of-Chapter Exercises and Problems

Learning Objective

Knowledge

Comprehension

Application

Analysis

Synthesis

Evaluation

* 1. Identify the features of managerial

accounting and the functions of

management.

Q19-1

Q19-2

Q19-3

Q19-4

Q19-5

Q19-6

Q19-7

Q19-8

BE19-1

BE19-2

DI19-1

E19-1

* 3. Demonstrate how to compute cost of

goods manufactured and prepare

financial statements for a

manufacturer.

Q19-19

Q19-10

Q19-20

Q19-21

E19-15

Q19-15

Q19-16

Q19-17

Q19-18

BE19-7

BE19-8

BE19-9

BE19-10

DI19-3

E19-8

E19-9

E19-12

E19-13

E19-14

E19-16

E19-17

P19-4A

E19-10

E19-11

P19-3A

P19-5A

ANSWERS TO QUESTIONS

1. (a) Disagree. Managerial accounting is a field of accounting that provides economic and financial

information for managers and other internal users.

(b) Joe is incorrect. Managerial accounting applies to all types of businesses—service, merchandising,

and manufacturing.

3. Differences in the content of the reports are as follows:

Financial

Managerial

• Pertains to business as a whole and is highly

aggregated.

• Limited to double-entry accounting and cost

• Pertains to subunits of the business and

may be very detailed.

• Extends beyond double-entry accounting

4. Linda should know that the management of an organization performs three broad functions:

(1) Planning requires management to look ahead and to establish objectives.

(2) Directing involves coordinating the diverse activities and human resources of a company to

produce a smooth-running operation.

Questions Chapter 19 (Continued)

7. The differences between income statements are in the computation of the cost of goods sold as

follows:

Manufacturing

Beginning finished goods inventory plus cost of goods manufactured minus

8. The difference in balance sheets pertains to the presentation of inventories in the current asset

section. In a merchandising company, only merchandise inventory is shown. In a manufacturing

company, three inventory accounts are shown: finished goods, work in process, and raw materials.

9. Manufacturing costs are classified as either direct materials, direct labor, or manufacturing overhead.

10. No, Mel is not correct. The distinction between direct and indirect materials is based on two criteria:

(1) physical association and (2) the convenience of making the physical association. Materials which

cannot be easily associated with the finished product are considered indirect materials.

13. (a) X = total cost of work in process.

(b) X = cost of goods manufactured.

14. Raw materials inventory, beginning …………………………………………………………….. 12,000 $

Raw materials purchases ………………………………………………………………………….. 170,000

16. (a) Total cost of work in process ($26,000 + $640,000) ……………………………….. $666,000

(b) Cost of goods manufactured ($666,000 – $32,000) ……………………………….. $634,000

17. The order of listing is finished goods inventory, work in process inventory, and raw materials inventory.

Questions Chapter 19 (Continued)

18. The products differ in how each are consumed by the customer. Services are consumed

immediately; the product is not put into inventory. Meals at a restaurant are the best example

where they are consumed immediately by the customer. There could be a long lead time before

the product is consumed in a manufacturing environment.

19. Yes, product costing techniques apply equally well to manufacturers and service companies. Each

needs to keep track of the cost of production or services in order to know whether it is generating

a profit. The techniques shown in this chapter, to accumulate manufacturing costs to determine

manufacturing inventory, are equally useful for determining the cost of services.

22. In a just-in-time inventory system, the company has no extra inventory stored. Consequently, if

some units that are produced are defective, the company will not have enough units to deliver to

customers.

23. The balanced scorecard is called “balanced” because it strives to not over emphasize any one

performance measure, but rather uses both financial and non-financial measures to evaluate all

aspects of a company’s operations in an integrated fashion.

26. Activity-based costing is an approach used to allocate overhead based on each product’s relative

use of activities in making the product. Activity-based costing is beneficial because it results in

more accurate product costing and in more careful scrutiny of all activities in the value chain.

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 19-1

Financial Accounting

Managerial Accounting

Primary users

External users

Internal users

Types of reports

Financial statements

Internal reports

Frequency of reports

Quarterly and annually

As frequently as needed

for specific decisions

accounting principles

public accountant

BRIEF EXERCISE 19-2

(a) 1. Planning.

BRIEF EXERCISE 19-3

(a) DM Frames and tires used in manufacturing bicycles.

BRIEF EXERCISE 19-4

(a) Direct materials.

(b) Direct materials.

(c) Direct labor.

(d) Manufacturing overhead.

BRIEF EXERCISE 19-5

(a) Product.

(b) Period.

BRIEF EXERCISE 19-6

Product Costs

Direct

Materials

Direct

Labor

Factory

Overhead

(a)

X

BRIEF EXERCISE 19-7

(a) Direct materials used …………………………………………………… $180,000

Direct labor …………………………………………………………………. 209,000

BRIEF EXERCISE 19-8

ROLAND COMPANY

Balance Sheet

December 31, 2017

Current assets

Cash …………………………..…………………………….. $ 62,000

Accounts receivable ………………………………….. 200,000

Inventories

BRIEF EXERCISE 19-9

Direct

Materials Used

Direct

Labor Used

Factory

Overhead

Total

Manufacturing

Costs

(1)

$151,000

BRIEF EXERCISE 19-10

Total

Manufacturing

Costs

Work in

Process

(January 1)

Work in

Process

(December 31)

Cost of Goods

Manufactured

(1)

$151,000*

$189,000

BRIEF EXERCISE 19–11

One implication of SOX was to clarify top management’s responsibility for

the company’s financial statements. CEOs and CFOs must now certify that

financial statements give a fair presentation of the company’s operating

results and its financial condition. In addition, top managers must certify

SOLUTIONS FOR DO IT! REVIEW EXERCISES

DO IT! 19-1

1. False

DO IT! 19-2

Period costs:

Product costs:

Blank CDs (DM)

Depreciation of CD image burner (MO)

Salary of factory manager (MO)

DO IT! 19-3

TOMLIN COMPANY

Cost of Goods Manufactured Schedule

For the Month Ended April 30

Work in process, April 1 ………………………….. $ 5,000

Direct materials ……………………………………….

Raw materials, April 1 …………………………. $ 10,000

Cost of goods manufactured …………………… $335,500

DO IT! 19-4

1. f

2. a

SOLUTIONS TO EXERCISES

EXERCISE 19-1

1. False. Financial accounting focuses on providing information to external

users.

2. False. Line positions are directly involved in the company’s primary

revenue-generating operating activities.

EXERCISE 19-2

1. (b) Direct labor.*

2. (c) Manufacturing overhead.

EXERCISE 19-3

(a)

Bicycle components …………… DM

Advertising expense ………….. Period

Depreciation on plant ………. MOH

Property taxes on plant ………… MOH

Salaries paid to sales clerks … Period

(b) Product costs are recorded as a part of the cost of inventory because

they are an integral part of the cost of producing the bicycles. Product

EXERCISE 19-4

(a) Factory utilities …………………………………………………………….. $ 15,500

Depreciation on factory equipment ……………………………….. 12,650

(b) Direct materials ……………………………………………………….…… $137,600

Direct labor ………………………………………………………………….. 69,100

EXERCISE 19-5

1.

(c)

3.

(a)

5.

(b)*

7.

(a)

9.

(c)

*or sometimes (c), depending on the circumstances.

EXERCISE 19-6

1. (b)

EXERCISE 19-7

(a) Delivery service (product) costs:

Indirect materials

$ 6,400

Depreciation on delivery equipment

11,200

Dispatcher’s salary

Gas and oil for delivery trucks

Drivers’ salaries

16,000

Total

$41,100

(b) Period costs:

Property taxes on office building

$ 870

CEO’s salary

12,000

Office supplies

Office utilities

Repairs on office equipment

180

Total

$19,290

EXERCISE 19-8

(a) Work-in-process, 1/1 …………………………. $ 12,000

Direct materials used ………………………… $120,000

Direct labor ………………………………………. 110,000

Manufacturing overhead

Depreciation on plant ………………….. $60,000

EXERCISE 19-9

Total raw materials available for use:

Direct materials used ………………………………………………. $180,000

Raw materials inventory (1/1):

Total raw materials available for use:

Direct materials used ………………………………………………. $180,000

Add: Raw materials inventory (12/31) ……………………… 22,500

Total cost of work in process:

EXERCISE 19-9 (Continued)

Total manufacturing costs:

Total cost of work in process …………………………... $621,000

Less: Work in process (1/1) ……………………………… 210,000

EXERCISE 19–10

A + $57,000 + $46,500 = $195,650 $252,500 – $11,000 = F

A = $92,150 F = $241,500

Additional explanation to EXERCISE 19-10 solution:

Case A

(a) Total manufacturing costs ……………………………….. $195,650

EXERCISE 19-10 (Continued)

(b) Total cost of work in process …………………………... $221,500

Less: Total manufacturing costs ………………………. 195,650

Work in process (1/1/17) …………………………………… $ 25,850

Case B

(d) Direct materials used ………………………………………. $ 68,400

Direct labor ……………………………………………………… 86,000

Manufacturing overhead ………………………………….. 81,600

Total manufacturing costs ……………………………….. $236,000

Cost of goods manufactured ……………………………. $241,500

Case C

(g) Total manufacturing costs ……………………………….. $253,700

Less: Manufacturing overhead ………………………… $102,000

Direct materials used …………………………….. 130,000 232,000

EXERCISE 19–11

(a) (a) $117,000 + $140,000 + $87,000 = $344,000

(b) $344,000 + $33,000 – $360,000 = $17,000

(b) HORIZON COMPANY

Cost of Goods Manufactured Schedule

For the Year Ended December 31, 2017

Work in process, January 1 …………………………. $ 33,000

Direct materials …………………………………………… $117,000

Direct labor …………………………………………………. 140,000

EXERCISE 19–12

(a) CEPEDA CORPORATION

Cost of Goods Manufactured Schedule

For the Month Ended June 30, 2017

Work in process, June 1……………………….. $ 3,000

Direct materials used …………………………... $20,000

Direct labor ………………………………………….. 40,000

Manufacturing overhead

Indirect labor ………………………………… $4,500

Factory manager’s salary ………………. 3,000

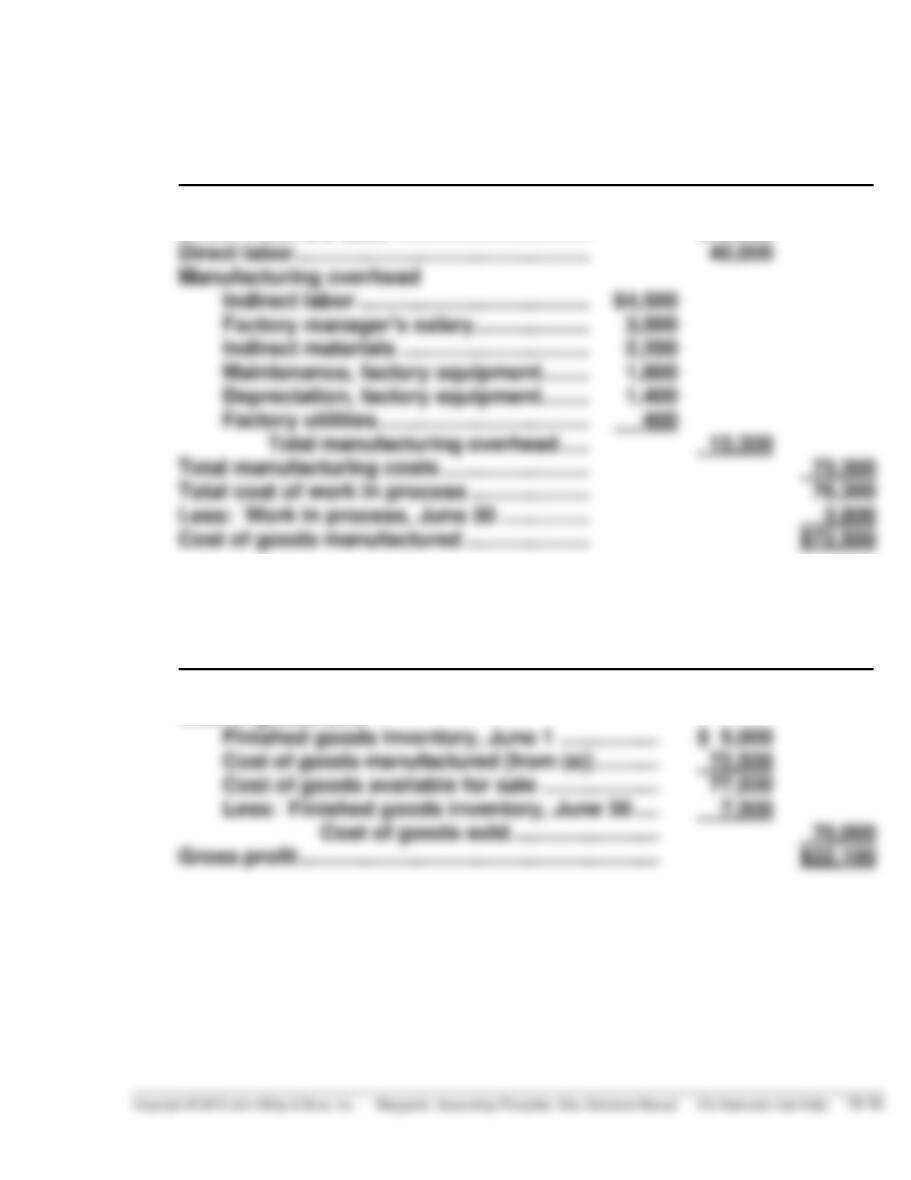

(b) CEPEDA CORPORATION

Income Statement (Partial)

For the Month Ended June 30, 2017

Sales revenue ………………………………………………… $92,100

Cost of goods sold

EXERCISE 19–13

(a)

WASHINGTON CONSULTING

Schedule of Cost of Contract Services Performed

For the Month Ended August 31, 2017

Supplies used (direct materials) ……………………………..

$ 1,700

Salaries of professionals (direct labor) ……………………

15,600

Service overhead:

Utilities for contract operations ………………………….

$1,400

Contract equipment depreciation ……………………….

Insurance on contract operations ………………………

Janitorial services for professional offices ………….

700

Total overhead …………………………………………….

EXERCISE 19–14

(a) Work-in-process, 1/1 ………………………… $ 13,500

Direct materials

Materials inventory, 1/1 ………………. $ 21,000

Materials purchased …………………… 150,000

Materials available for use ………….. 171,000