1. a. Job order cost system and process cost system.

b. The job order cost system provides a separate record of each quantity of product that

p

asses through the factory.

c. Process cost systems accumulate costs for each department or process within a factory.

5. A job cost sheet is the subsidiary ledger to the work in process control account. The cost of

materials, labor, and overhead are listed on each separate job cost sheet for each job. A summary

of all the job cost sheets during an accounting period is the basis for journal entries to the control

accounts.

6. The clock card is a means of recording the hours spent by employees in the factory. The

time ticket is a means of recording the time the employee spends on a specific job.

p

8. a. The predetermined factory overhead rate is determined by dividing the estimated total factory

overhead costs for the forthcoming year by an estimated activity base, one that reflects the

consumption or use of factory overhead costs.

b. Direct labor cost, direct labor hours, and machine hours.

CHAPTER 19

JOB ORDER COSTING

DISCUSSION QUESTIONS

CHAPTER 19 Job Order Costing

DISCUSSION QUESTIONS (Continued)

10. Job order cost accumulation would be most appropriate for professional service firms that

p

rovide extended, project-type services for clients. Examples would be architectural,

consulting, advertising, and legal services. Job cost sheets would accumulate all direct costs of

servicing the client. Such costs would include labor, materials, travel, and subcontracted

CHAPTER 19 Job Order Costing

PE 19-1A

7 Materials (12,000 units × $6) 72,000

Accounts Payable 72,000

PE 19-1B

4 Materials (31,000 units × $16) 496,000

Accounts Payable 496,000

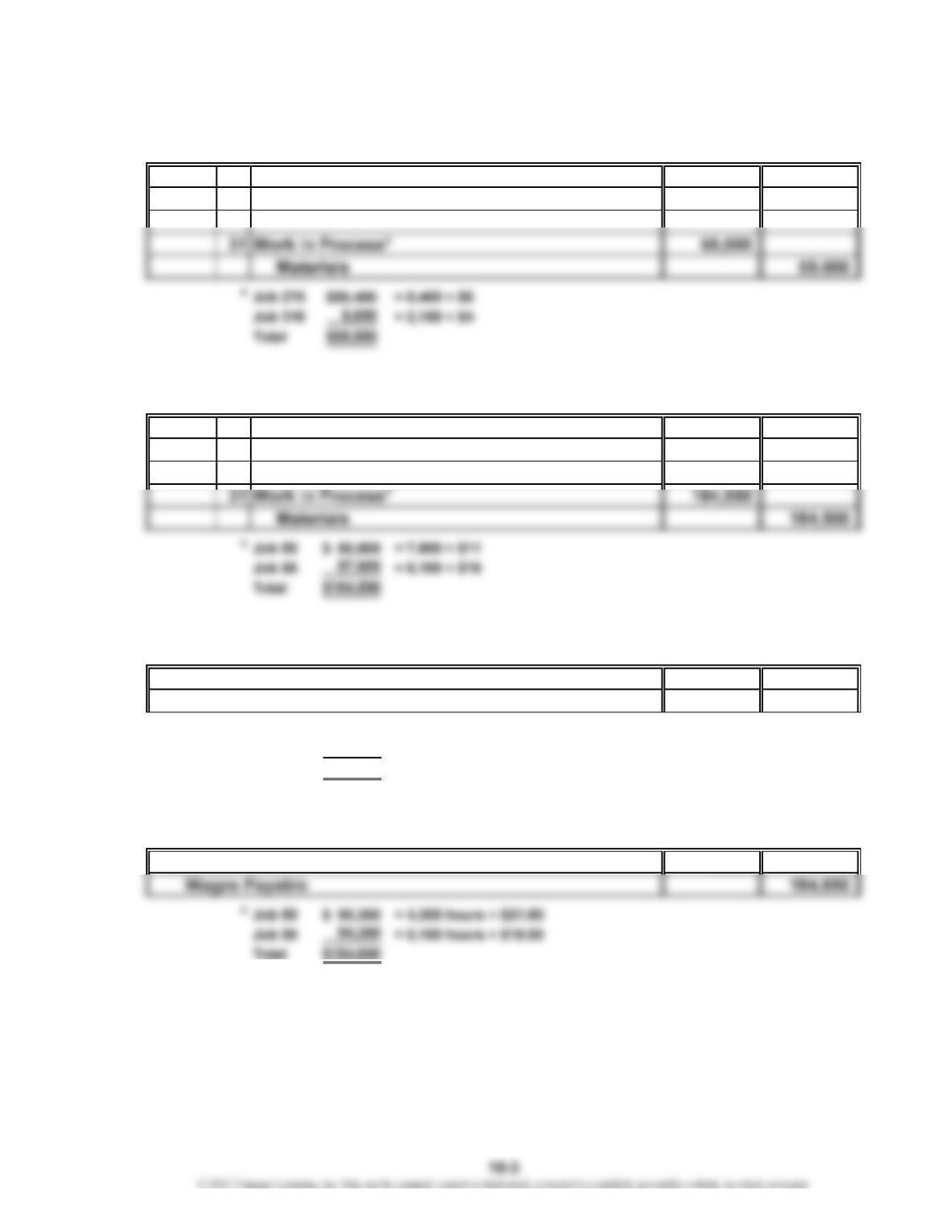

PE 19-2A

Work in Process* 132,200

Wages Payable 132,200

*Job 275 $ 64,600 = 1,900 hours × $34

Job 310 67,600 = 2,600 hours × $26

Total $132,200

PE 19-2B

Work in Process* 184,650

Aug.

PRACTICE EXERCISES

May

PE 19-3A

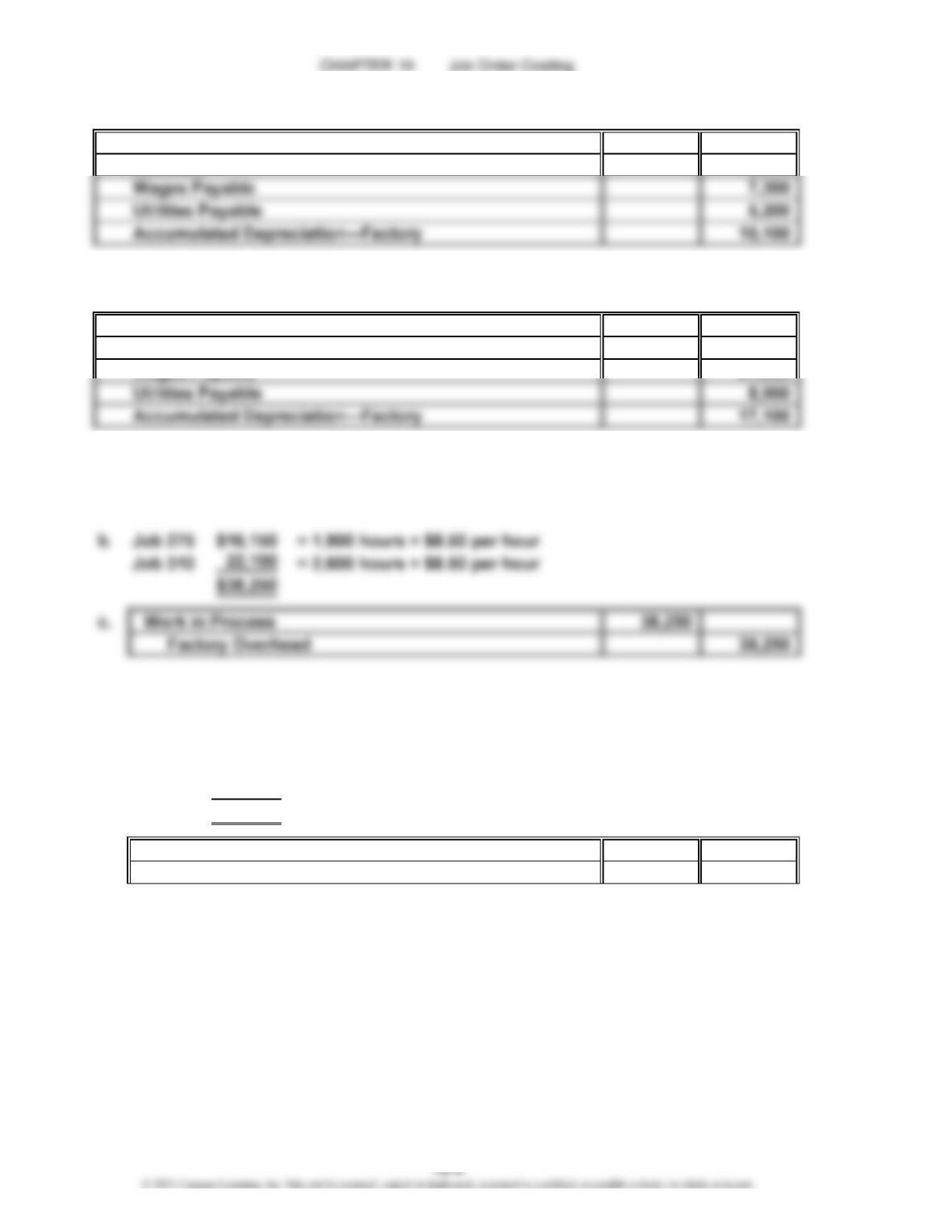

Factory Overhead 32,300

Materials 9,700

PE 19-3B

Factory Overhead 63,700

Materials 16,400

PE 19-4A

a. $8.50 per direct labor hour = $867,000 ÷ 102,000 direct labor hours

PE 19-4B

a. $12.00 per direct labor hour = $960,000 ÷ 80,000 direct labor hours

b. $ 51,600 = 4,300 hours × $12.00 per hour

61,200 = 5,100 hours × $12.00 per hour

$112,800

c. Work in Process 112,800

Factory Overhead 112,800

Job 50

Job 56

CHAPTER 19 Job Order Costing

PE 19-5A

a. Job 275 Job 310

Direct materials…………………………………………………

…

$ 50,400 $ 8,600

Direct labor………………………………………………………

…

64,600 67,600

Factory overhead………………………………………………

…

16,150 22,100

Total costs…………………………………………………… $131,150 $98,300

b. = $131,150 ÷ 5,000 units

= $98,300 ÷ 2,000 units

$26.23

$49.15

Job 275

Job 310

…

…

…

CHAPTER 19 Job Order Costing

Ex. 19-1

a. Materials requisitioned for use (both direct and indirect)

b. Factory labor used (both direct and indirect)

Ex. 19-2

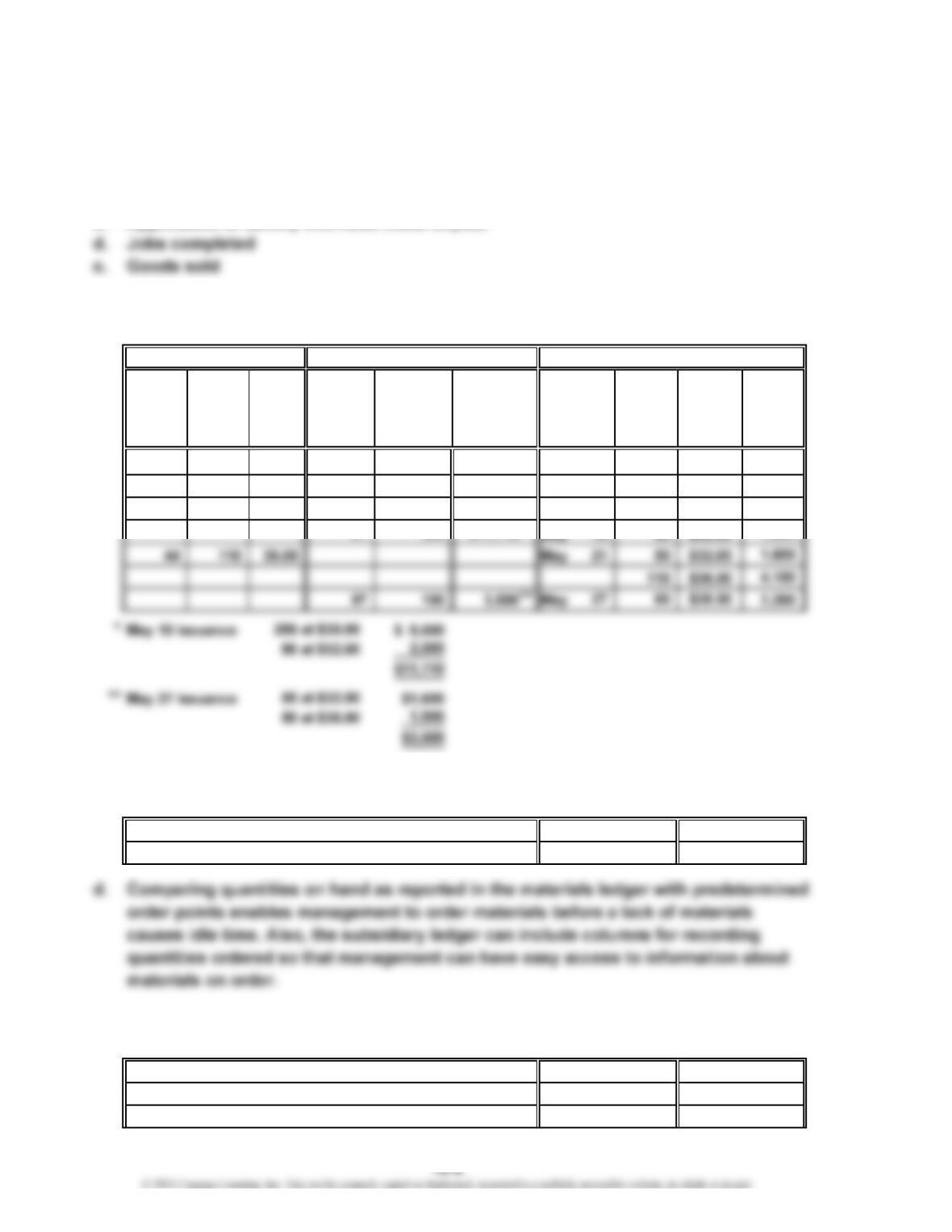

a.

Materials

Receiving Requi-

Report Unit sition Unit

Number Quantity Price Number Quantity Amount Quantity Price Amount

May 1 285 $30.00 $8,550

40 130 $32.00 May 4 285 $30.00 8,550

130 $32.00 4,160

b. Ending inventory balance:

60 at $38.00……………………………………………………………………

…

c. Work in Process ($11,110 + $3,500)

Materials

Ex. 19-3

Work in Process

Factory Overhead

Materials

EXERCISES

RECEIVED ISSUED

61,600

1,620

63,220

14,610

$2,280

14,610

BALANCE

Date

CHAPTER 19 Job Order Costing

Ex. 19-4

a. Materials* 918,000

Accounts Payable 918,000

*$396,000 + $162,000 + $324,000 + $36,000

c.

Lumber Glue

Balance, June 1…………… $ 56,200 $ 5,900

June purchases…………… 324,000 36,000

Less June requisitions…

…

(300,000) (31,300)

Balance, June 30…………

…

$ 80,200 $ 10,600

Ex. 19-5

Work in Process 88,800

Factory Overhead 8,500

Wages Payable 97,300

Supporting calculations:

Direct

Labor

Hourly Job Job (sum of Indirect

Rate 301 303 job costs) Labor

Landon Vincent…

…

$35 $315 $385 $1,330 $ 70

Fahad Hamad……

…

36 396 468 1,404 36

Ivory Argo………

…

28 224 252 1,036 84

$3,770 $190

$630

540

560

Polyester

Labor Costs (Hourly Rate × Hours)

Fabric

$ 36,500

396,000

(401,000)

$ 31,500

Filling

$ 25,700

162,000

(150,000)

$ 37,700

Job

302

CHAPTER 19 Job Order Costing

Ex. 19-7

a. Work in Process 25,200

Factory Overhead 4,000

Wages Payable 29,200

Ex. 19-8

a. Factory 1: $37.50 per machine hour ($12,000,000 ÷ 320,000 machine hours)

c. Factory 1:

Work in Process 1,031,250

Factory Overhead 1,031,250

($37.50 × 27,500).

Factory 2:

Ex. 19-9

The estimated shop overhead is determined as follows:

Shop and repair equipment depreciation………………………………………

…

$ 64,000

Shop supervisor salaries…………………………………………………………

…

212,000

Shop property taxes………………………………………………………………… 35,000

Shop supplies………………………………………………………………………

…

18,000

Total shop overhead……………………………………………………………

…

$329,000

CHAPTER 19 Job Order Costing

Ex. 19-9 (Concluded)

35,000 hours

Ex. 19-10

a. Estimated number of operating room hours:

Hours per day…………………………………………………

…

8

Days per week…………………………………………………

…

7

Hours per week………………………………………………

…

56

Weeks per year (net of two maintenance weeks)………

…

50

Estimated annual operating room hours…………………

…

2,800

c. Conrad Goldsmith’s procedure:

Number of surgical room hours……………………………

…

6

Predetermined surgical room overhead rate……………

…

$340

Procedure overhead…………………………………………

…

$2,040

×

×

×

CHAPTER 19 Job Order Costing

Ex. 19-11

a. Finished Goods* 1,149,800

Work in Process 1,149,800

*$200,000 + $288,000 + $225,000 + $436,800

b. Cost of unfinished jobs at January 31:

Balance in Work in Process at January 1…………

…

$ 72,000

Add: Direct materials………………………………

…

390,000

Ex. 19-12

a. Work in Process 93,500

Factory Overhead 7,600

Materials 101,100

b. Work in Process 102,000

Factory Overhead 15,100

Wages Payable 117,100

c. Predetermined overhead rate based upon direct labor cost is 65%, computed

as follows:

Job 301: $6,500 ÷ $10,000 = 65%

d. Work in Process* 66,300

Factory Overhead 66,300

*Job 301 $ 6,500

Job 302 15,600

Job 303 23,400

Job 304 20,800

e. Finished Goods* 97,300

Work in Process 97,300

*$30,800 + $66,500

CHAPTER 19 Job Order Costing

Ex. 19-12 (Concluded)

f. Work in process on January 31:

Job 303 $ 76,500 ($17,100 + $36,000 + $23,400)

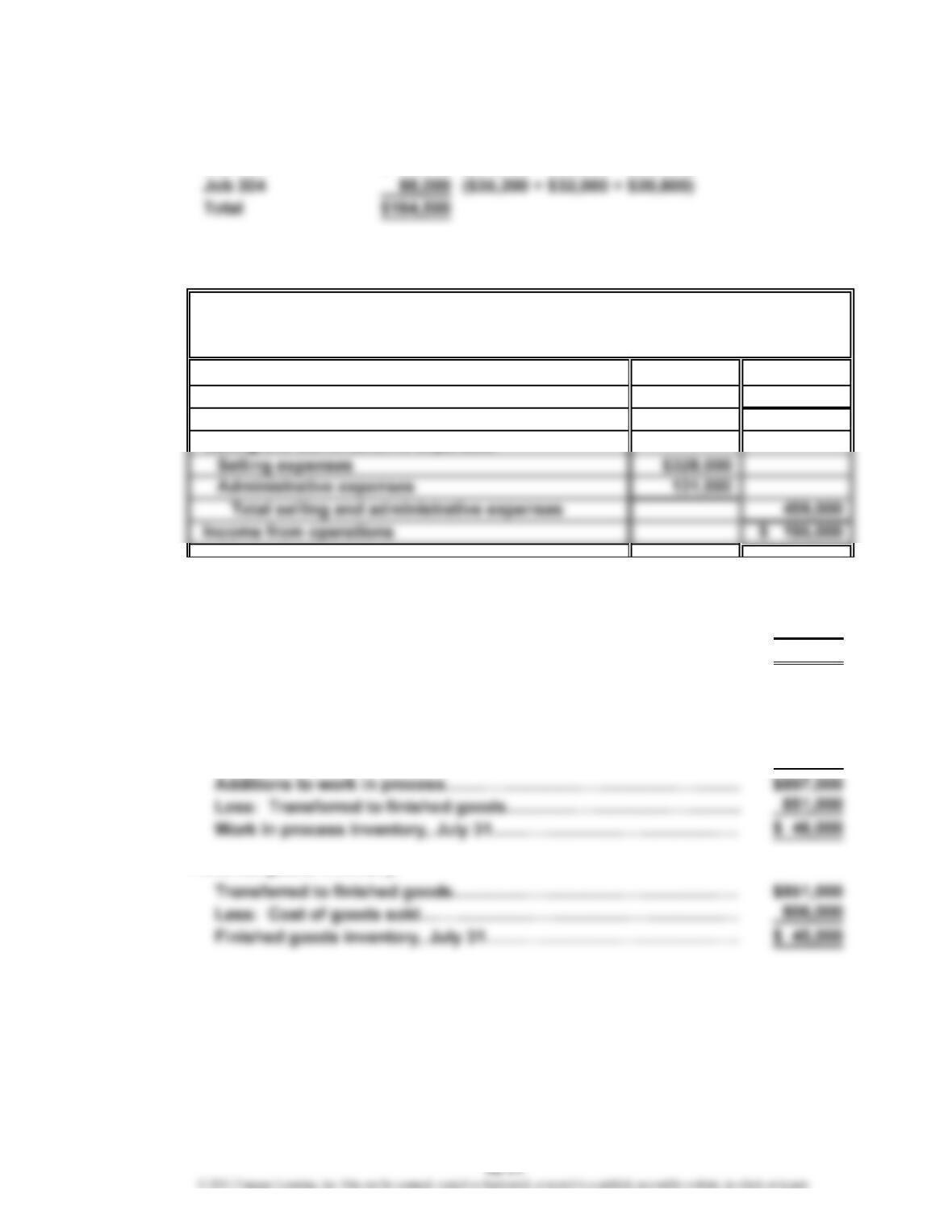

Ex. 19-13

a.

Revenues $1,460,000

Cost of goods sold 806,000

Gross profit $ 654,000

b. Materials inventory:

Purchased materials………………………………………………………

…

$416,000

Less: Materials used in production……………………………………

…

358,000

Materials inventory, July 31………………………………………………

…

$ 58,000

Work in process inventory:

Materials used in production……………………………………………

…

$358,000

Direct labor…………………………………………………………………

…

308,000

Factory overhead (75% × $308,000)……………………………………

…

231,000

Finished goods inventory:

Migliozzi Inc.

Income Statement

For the Month Ended July 31

CHAPTER 19 Job Order Costing

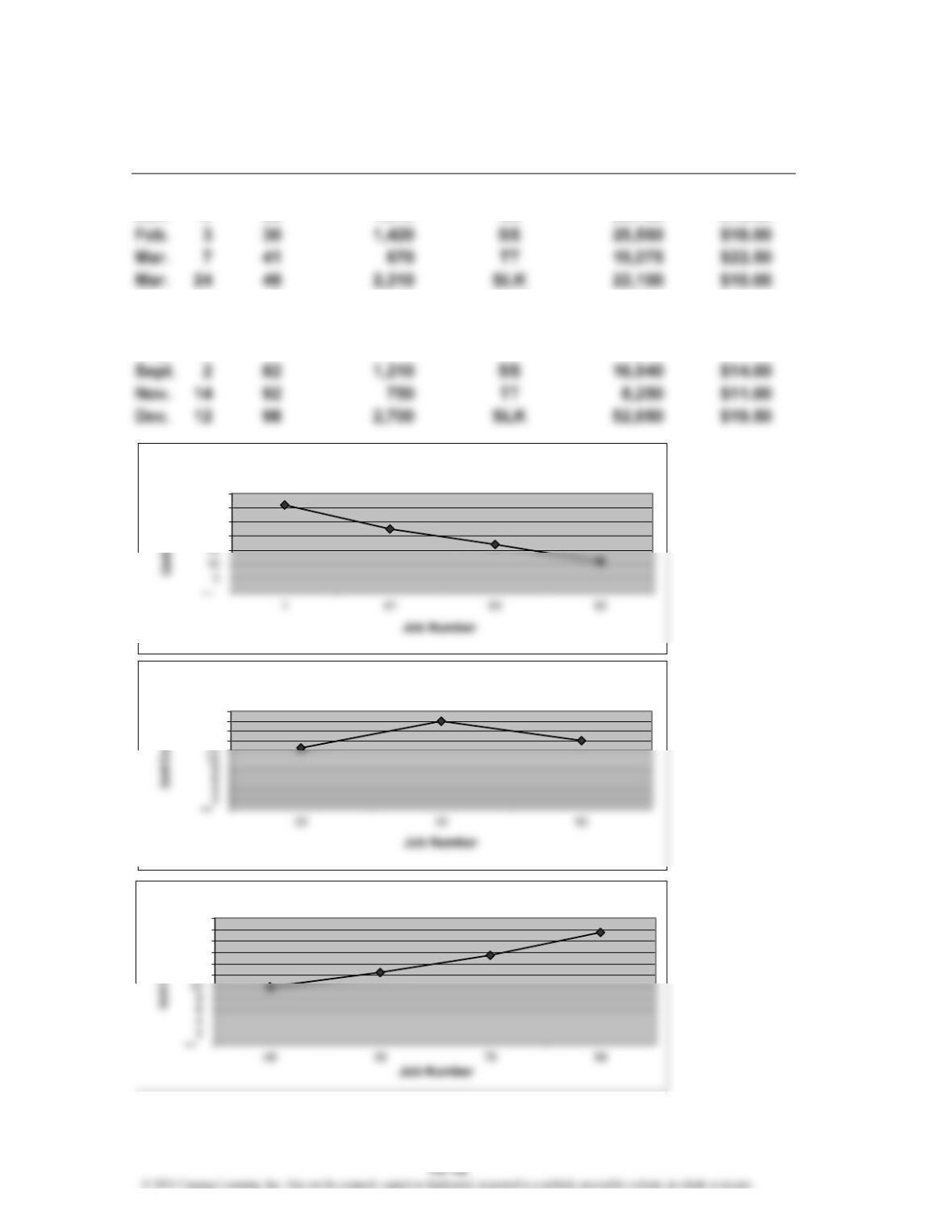

Ex. 19-14

a.

Unit

Date Job. No. Quantity Product Amount Cost

Jan. 2 1 520 TT $16,120 $31.00

May 19 58 2,550 SLK 31,875 $12.50

June 12 65 620 TT 10,540 $17.00

Aug. 18 78 3,110 SLK 48,205 $15.50

20

25

30

35

Unit Costs for TT

14

16

18

20

Unit Costs for SS

12

14

16

18

20

22

Unit Costs for SLK

CHAPTER 19 Job Order Costing

Ex. 19-14 (Concluded)

As can be seen, the unit costs behave differently for each product. SLK has

increasing unit costs during the year, SS is steady, and TT has decreasing

unit costs during the year.

b. Management should determine why SLK costs are increasing and why TT costs

CHAPTER 19 Job Order Costing

Ex. 19-15

a. The first item to note is that the cost did not go up due to any increases in the

cost of labor or materials. Rather, the cost of the plaques increased because

Job 105 used more labor and materials per unit than did Job 101. Specifically,

Job 101 required the same number of backboards and brass plates as

the number of actual plaques shipped. However, Job 105 required four more

backboards and brass plates than the number actually shipped (34 versus 30).

This is illustrated as follows:

Job 101:

Materials

Walnut plaques:

Actual units used………………………………………………………

…

40 units

Expected units needed to produce 40 plaques……………………

…

40 units

Difference………………………………………………………………………

…

0 units

Labor

Engraving:

Actual labor hours used………………………………………………

…

20 hours

Expected labor hours to produce 40 plaques

(40 units × 30 min. per unit) ÷ 60 min. per hour…………………

…

20 hours

Difference……………………………………………………………

…

0 hours

Assembly:

…

…

…

…

…

…

CHAPTER 19 Job Order Costing

Ex. 19-15 (Concluded)

Job 105:

Materials

Walnut plaques:

Actual units used………………………………………………………

…

34 units

Expected units needed to produce 30 plaques…………………… 30 units

Difference………………………………………………………………………

…

4 units

Labor

Engraving:

Actual labor hours used………………………………………………

…

17 hours

Expected labor hours to produce 30 plaques

(30 units × 30 min. per unit) ÷ 60 min. per hour…………………

…

15 hours

Difference……………………………………………………………

…

2 hours

…

…

…

Job 105’s 25.5 labor hours are 3.0 more (25.5 hrs. – 22.5 hrs.) than should have

been expected for a job of 30 plaques [(30 × 45 min.) ÷ 60 min. = 22.5 hrs.]. As a

result, the additional hours of labor cost, applied factory overhead, and direct

materials cost cause the unit cost of Job 105 to increase.

b. Apparently, the engraving and assembly work is becoming sloppy. Job 105

required 34 engraved brass plates in order to get 30 with acceptable quality. It is

likely that the engraver is not being careful in spelling the names correctly. The

names should be supplied to the engraver, using large typewritten fonts, so that

it is easy to read the names. The engraver should be instructed to be careful in

…

…

CHAPTER 19 Job Order Costing

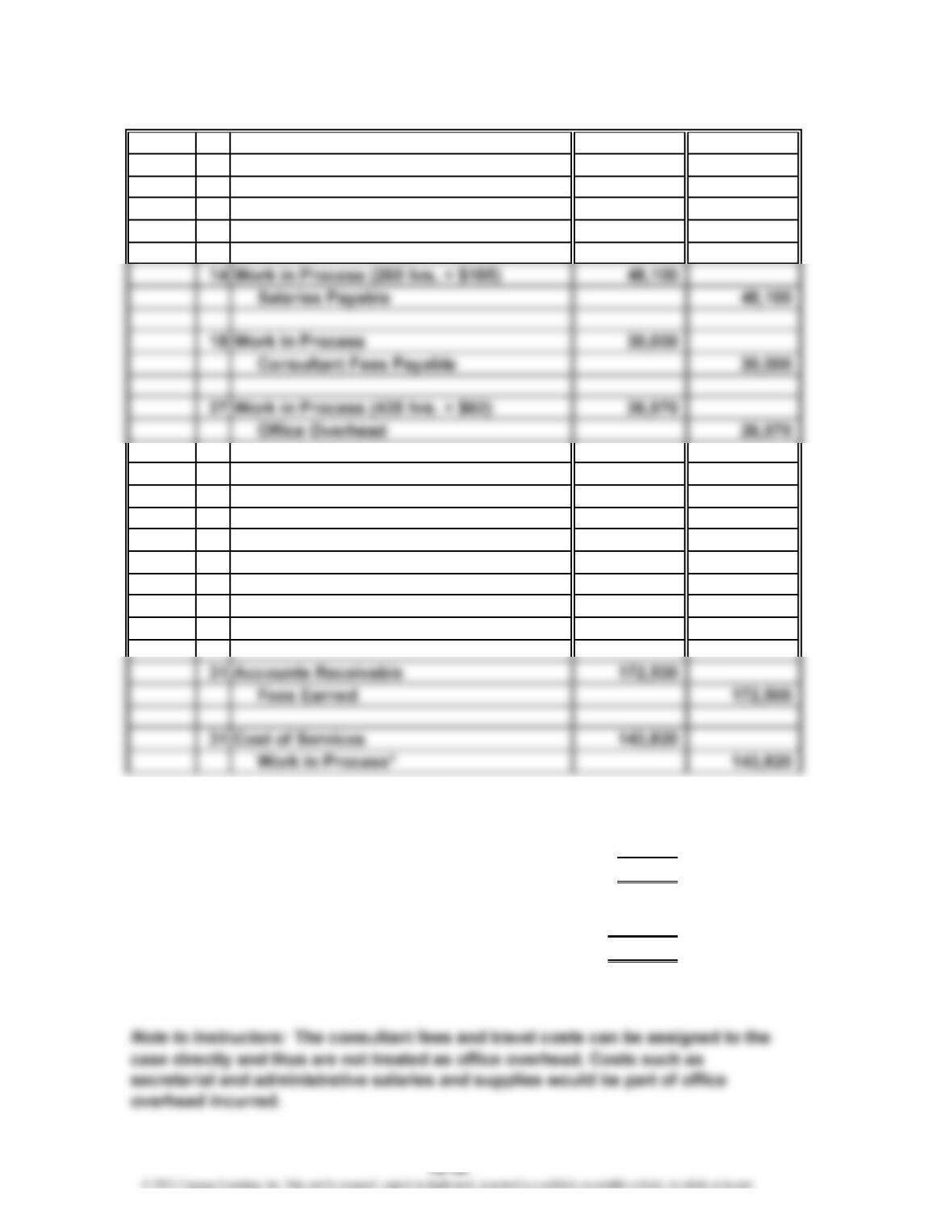

Ex. 19-16

a. July 3 Work in Process (175 hrs. × $150) 26,250

Salaries Payable 26,250

10 Work in Process 12,500

Cash 12,500

31 Office Overhead 28,500

Cash 28,500

31 Office Overhead 4,000

Supplies 4,000

31 Salaries Payable 74,350

Cash 74,350

*$26,250 + $12,500 + $48,100 + $30,000 + $26,970

b. Office overhead incurred ($28,500 + $4,000)……………

…

$32,500

Office overhead applied……………………………………… 26,970

Underapplied overhead………………………………………

…

$ 5,530

c. Fees earned……………………………………………………

…

$172,500

Cost of services*………………………………………………

…

149,350

Gross profit……………………………………………………

…

$ 23,150

*$143,820 + $5,530. Assumes the over- or underapplied office overhead is

closed to cost of services monthly.

CHAPTER 19 Job Order Costing

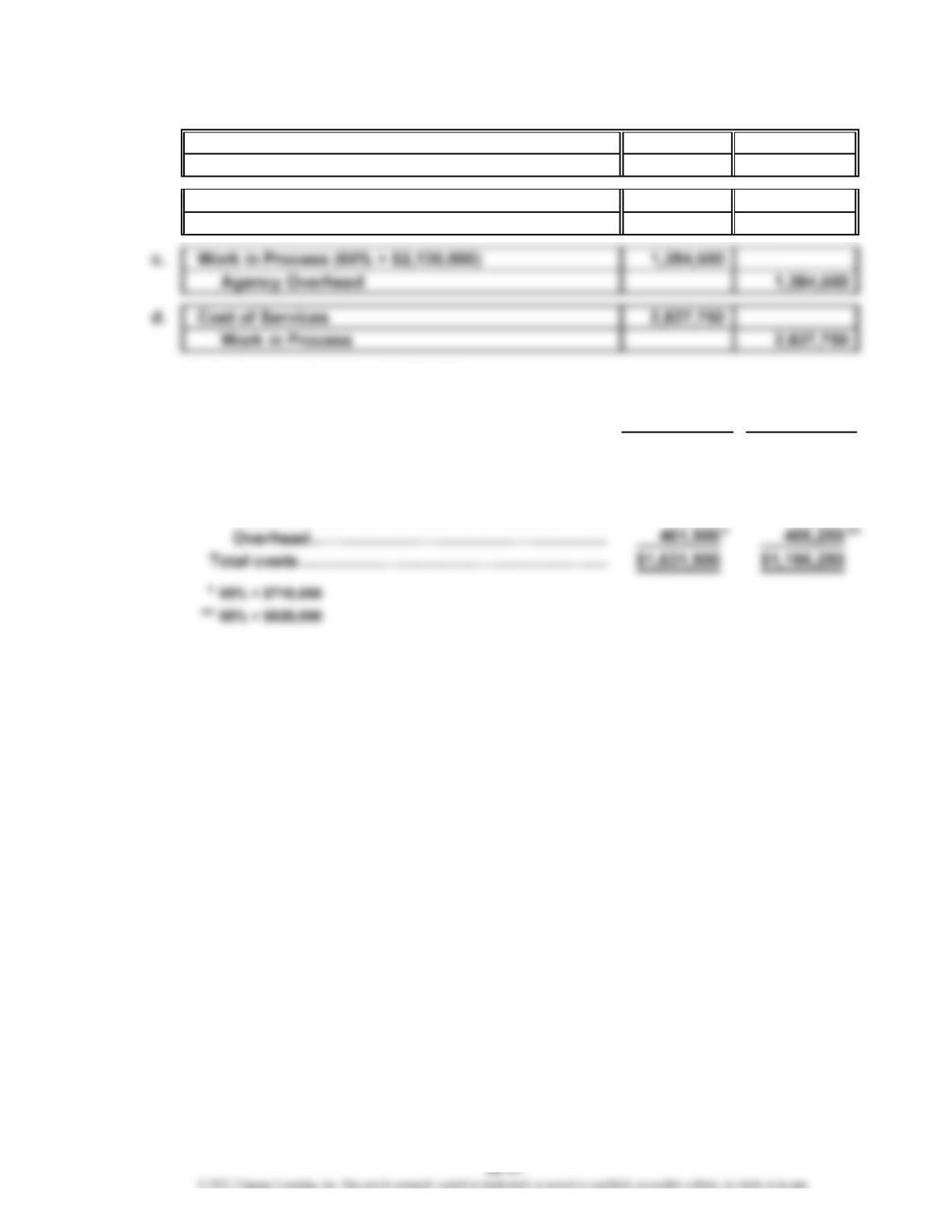

Ex. 19-17

a. Work in Process 1,068,000

Salaries Payable

b. Work in Process 2,130,000

Accounts Payable

Cost of completed jobs, $2,827,750:

Vault Take Off

Bank Airlines

August 1 balance………………………………………

…

$ 270,000 $ 80,000

August costs:

Direct labor…………………………………………

…

190,000 85,000

Media…………………………………………………

…

710,000 625,000

…

1,068,000

2,130,000

CHAPTER 19 Job Order Costing

Prob. 19-1A

a. Materials 203,940

Accounts Payable 203,940

c. Work in Process 534,780

Factory Overhead 63,620

Wages Payable 598,400

d. Factory Overhead 290,400

Selling Expenses 158,300

Administrative Expenses 110,900

Accounts Payable 559,600

f. Depreciation Expense—Office Building 40,100

Depreciation Expense—Office Equipment 13,500

Factory Overhead 51,200

Accumulated Depreciation—Office Building 40,100

Accumulated Depreciation—Office Equipment 13,500

Accumulated Depreciation—Factory Equipment 51,200

PROBLEMS