PROBLEM 19.2B

THE BITMORE COMPANY

a.

b.

60 Minutes, Strong

Target Cost: BIT

Target Cost = Target Price – Target Profit

Target Cost = $120 – $14.40 = $105.60

Target Cost = Target Price – Target Profit

If fixed overhead is allocated based on units of production, the fixed overhead cost per unit is

equal to $62.50 calculated as follows:

Total manufacturing cost per unit:

PROBLEM 19.2B

THE BITMORE COMPANY (continued)

c.

BIT MORE

Fixed overhead cost ………………………………………………………..

Variable overhead cost …………………………………………………….

25.00$ 40.00$

20.00 50.00

Given that it takes 2 hours ($20 total labor cost per unit/$10 per hr. wage rate) to produce

each unit of BIT and 5 hours ($50 total labor cost per unit/$10 per hr. wage rate) to

produce each unit of MORE, the total expected labor hours needed for the year are:

Total manufacturing cost per unit:

Direct labor cost per unit …………………………………………………….

Direct materials cost per unit ……………………………………………..

30,000 units of BIT × 2 hours per unit

+ 10,000 units of MORE × 5 hours per unit

= 110,000 hours

= 60,000 hours + 50,000 hours

PROBLEM 19.2B

THE BITMORE COMPANY (continued)

d.

BIT MORE

Total fixed overhead allocated …………………………………………….

Shipping (400 × $400, 100 × $400) ………………………………………….

Inspection (40 × $5,000, 20 × $5,000) ………………………………………

Machining (3,000 × $71.43, 4,000 × $71.43) ……………………………..

87,500$ 262,500$

487,500 162,500

BIT MORE

Direct labor cost per unit …………………………………………………

Variable overhead cost …………………………………………………….

25.00$ 40.00$

The allocation rates of each overhead activity are calculated as follows:

Direct materials cost per unit …………………………………………..

Total fixed overhead allocated per unit:

Setup costs (100 × $875, 300 × $875) ………………………………..

Purchase orders (300 × $1,625, 100 × $1,625) ………………………..

Total manufacturing cost per unit:

PROBLEM 19.2B

THE BITMORE COMPANY (continued)

f.

BIT MORE

Purchase orders (300 × $1,625, 100 × $1,625) ………

Machining (3,000 × $71.43, 4,000 × $71.43) …………

Inspection (40 × $5,000, 20 × $5,000) ………………….

Shipping (400 × $400, 100 × $400) ……………………..

Total fixed overhead allocated …………………………..

÷ units produced ………………………………………….

200,000$ 150,000$

BIT MORE

Direct labor cost per unit …………………………….

Variable overhead cost ……………………………….

Fixed overhead cost ………………………………….

25.00$ 40.00$

Setup costs (100 × $2,000, 75 × $2,000) ………………

Total fixed overhead allocated per unit:

Since the cost per unit of BIT is below the target cost of $105.60, it is earning a return

greater than the desired rate. The cost per unit of MORE is above the target cost of $180, so

Reducing the number of setups required for one product while not reducing the related

overhead cost will change the allocation rate per setup and the total manufacturing cost per

unit for each product.

Total manufacturing cost per unit:

Direct materials cost per unit …………………………

($500,000 + 200,000)/$2,000,000 = 35%.

PROBLEM 19.2B

THE BITMORE COMPANY (concluded)

g.

BIT MORE

Total fixed overhead allocated …………………………………………..

Machining (3,000 × $71.43, 4,000 × $71.43) ……………………………..

Inspection (40 × $5,000, 20 × $5,000) ………………………………….

Shipping (400 × $400, 100 × $400) ……………………………………….

÷ units produced …………………………………………………………..

72,500$ 203,000$

487,500 162,500

BIT MORE

Direct labor cost per unit ………………………………………………….

Variable overhead cost ……………………………………………………….

Fixed overhead cost ………………………………………………………..

25.00$ 40.00$

With the new machine, the allocation rate per setup is calculated as follows:

Total fixed overhead allocated per unit:

Total manufacturing cost per unit:

Since the cost per unit of BIT is still below the target cost of $105.60, it is earning a return

more than the desired rate. The cost per unit of MORE is still above the target cost of

$158.40, so it is earning lower than the desired return.

Setup costs (50 × $1,450, 140 × $1,450) …………………………………

Purchase orders (300 × $1,625, 100 × $1,625) …………………………

Direct materials cost per unit ……………………………………………

30 Minutes, Medium PROBLEM 19.3B

ORO MINING

a.

b. Site A Site Z

c.

Target Cost = Target Price – Target Profit

If the conveyor is purchased, the total fixed costs associated with Site Z will increase by

Total cost per ton:

PROBLEM 19.4B

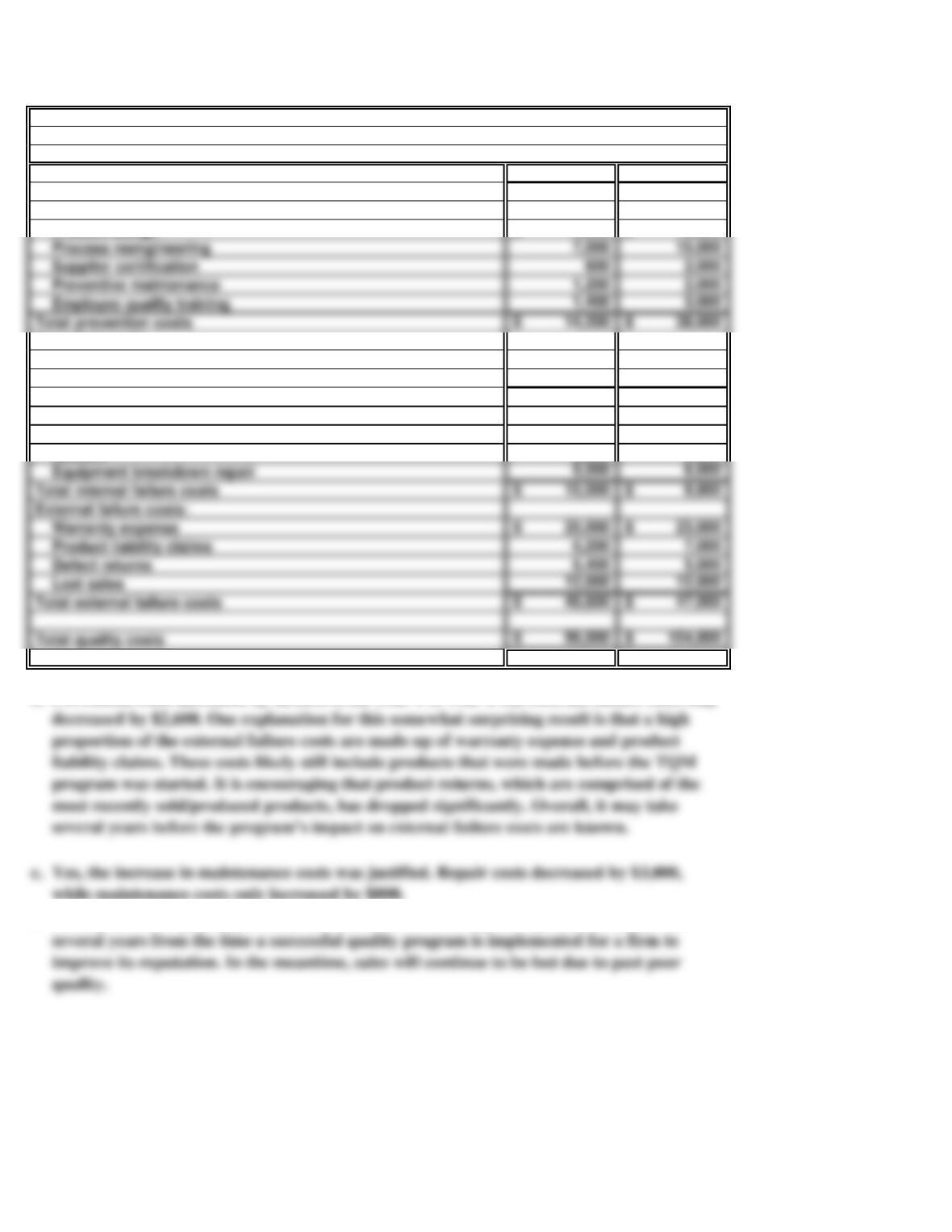

NAZU, INC.

a.

Year 1 Year 2

Prevention costs:

Product design 4,000$ 16,000$

Appraisal costs:

Raw materials inspections 5,200$ 2,000$

Final inspections 12,000 8,000

Total appraisal costs 17,200$ 10,000$

Internal failure costs:

Scrap 3,000$ 1,000$

Rework 3,000 2,800

Equipment breakdown repair 9,000 6,000

External failure costs:

Warranty expense 25,000$ 23,000$

Product liability claims 6,200 7,000

Defect returns 6,400 5,000

Lost sales 12,000 12,000

b.

d.

40 Minutes, Medium

Lost sales due to quality problems are often the result of a poor reputation. It may take

Quality Cost Report

Prevention costs increased by $23,800 from Year 1 to Year 2 but external failure costs only

while maintenance costs only increased by $800.

Process reengineering 7,000 15,000

Supplier certification 600 2,000

Preventive maintenance 1,200 2,000

Employee quality training 1,400 3,000

SOLUTIONS TO CRITICAL THINKING CASES

CASE 19.1

MAYS ELECTRONICS

a. Activity Classification

Setups Non-value-added

b.

Activity Cost

Setups 125,000$

Materials handling 180,000

Inspection 122,000

Customer complaints 100,000

Warranty expense 170,000

Storage 80,000

Rework 75,000

50 Minutes, Medium

Cost of non-value-added activities:

Customer support Value-added

Direct materials Value-added

Manual insertion labor Value-added

Other direct labor Value-added

CASE 19.1

MAYS ELECTRONICS (concluded)

c.

d.

e.

Total net cost reduction:

Automated insertion 100,000$ (from part d)

Factory redesign 90,000 ($100,000 + $10,000 – $20,000)

Net cost reduction

To maintain current market share, the selling price per CB must drop to $14. Given a

The net cost reduction of switching to automated insertion is $100,000 ($90,000 + $20,000 +

Leasing machine 65,000 ($80,000 – $15,000)

Just-in-time system 40,000 ($45,000 – $5,000)

Quality training and bonus 207,000 ($122,000 + 120,000 – $35,000)

CASE 19.2

HEALTHY TIMES FROZEN DINNERS

a.

b.

—

c.

40 Minutes, Strong

Description of a JIT system for Healthy Times:

The company operates from a single location—what is now the factory. Production and

receipt of direct materials are scheduled for each day of the week one week in advance. Each

A JIT manufacturing system is a “demand pull” system, in which materials are acquired

Non-value-added activities in Healthy Time’s operations and costs that might be eliminated:

Materials storage is a non-value-added activity. The company stores in its warehouse

enough direct materials for approximately two weeks’ production. Reduction or

CASE 19.2

HEALTHY TIMES FROZEN DINNERS (concluded)

d.

A JIT system should work at Healthy Times. Customer orders are received at least a week

in advance of delivery dates, which facilitates scheduling. Materials are available in

abundance from local suppliers. Therefore, it should be possible to arrange for reliable daily

deliveries of materials. Apparently all processing, including freezing and cutting, can be

MANUFACTURING ENGINEERING, INC.

INTERNET

a.

Quick Change: This includes training, implementation, operation, and sustainment.

b.

c.

Given that many of the innovations target existing products or processes, target costing and

The web site has a long list of different innovations. However, the majority of these

innovations result in changes in existing production processes or in characteristics of

existing products as illustrated by the categories below. Thus, the innovations are usually

targeted at the manufacturing phase of the value chain.

Benefits vary, but frequently involve increased productivity and reduce wait time and

30 Minutes, Medium CASE 19.3

CASE 19.4

SARBANES-OXLEY AND NON-VALUE-ADDED

ACTIVITIES ETHICS, FRAUD

& CORPORATE GOVERNANCE

a.

The costs of the Sarbanes-Oxley Act have been estimated to be enormous. Those costs

include the costs of documenting and auditing firm-wide internal control systems

processes and procedures. Besides the benefit of helping firms clarify their processes

and, as a result, identify non-value-added activities, the provisions of the Sarbanes-

25 Minutes, Medium