chapter

19(4)

Cost Behavior and Cost–

Volume-Profit Analysis

______________________________________________

OPENING COMMENTS

In Chapter 19(4), students learn how to conduct cost-volume-profit analysis. In preparation for this

activity, the chapter discusses variable, fixed, and mixed costs.

Cost-volume-profit analysis is conducted using both a formula-based mathematical approach and a

graphic approach. It is applied to single-product and multiple-product companies. The chapter concludes

with an appendix that discusses variable costing.

After studying the chapter, your students should be able to:

2. Compute the contribution margin, the contribution margin ratio, and the unit contribution margin.

4. Using a cost-volume-profit chart and a profit-volume chart, determine the break-even point and sales

necessary to achieve a target profit.

5. Compute the break-even point for a company selling more than one product, the operating leverage,

and the margin of safety.

KEY TERMS

absorption costing

activity bases (drivers)

break-even point

contribution margin

contribution margin ratio

356 Chapter 19(4) Cost Behavior and Cost-Volume-Profit Analysis

cost behavior

cost-volume-profit analysis

cost-volume-profit chart

fixed costs

high-low method

margin of safety

mixed costs

STUDENT FAQS

• Why does variable cost per unit stay the same but total cost varies with the number of units you

produce?

• How do you choose what activity base to use?

• Why does fixed cost remain the same in total dollar amount but increase or decrease per unit as the

level of activity changes?

• What do increases in fixed cost do to break-even analysis?

• What do increases in variable cost do to break-even analysis?

OBJECTIVE 1

Classify costs as variable costs, fixed costs, or mixed costs.

SYNOPSIS

Cost behavior is the manner in which a cost changes as activity changes. Managers find this relationship

useful as it allows managers to predict profits as sales and production volume change. Activity bases are

the things that cause cost to change, and the range over which the changes are of interest is called the

relevant range. Costs are classified as variable, fixed, or mixed costs. Variable costs are those that change

directly in proportion to changes in production volume. Direct materials and direct labor are usually

variable costs. Variable costs have certain characteristics, such as the cost per unit remains the same and

Chapter 19(4) Cost Behavior and Cost-Volume-Profit Analysis 357

historical data, including units produced and total costs. Subtract the lowest levels of production from the

highest levels of production computed as: variable cost per unit = difference in total cost/difference in

units produced. The fixed cost is then estimated by subtracting the total variable costs from the total fixed

costs, as follows: fixed cost = total costs – (variable cost per unit × units produced). Mixed costs contain a

fixed component even if nothing is produced.

Key Terms and Definitions

• Activity Base (Driver) – A measure of activity that is related to changes in cost. Used in

analyzing and classifying cost behavior. Activity bases are also used in the denominator in

calculating the predetermined factory overhead rate to assign overhead costs to cost objects.

• Cost Behavior – The manner in which a cost changes in relation to its activity base (driver).

• Fixed Costs – Costs that tend to remain the same in amount, regardless of variations in the level

of activity.

Relevant Example Exercises and Exhibits

• Example Exercise 19(4)-1 High-Low Method

• Exhibit 1 – Variable Cost Graphs

• Exhibit 2 – Variable Costs and Their Activity Bases

• Exhibit 3 – Fixed Cost Graphs

• Exhibit 4 – Fixed Costs and Their Activity Bases

• Exhibit 5 – Mixed Costs

• Exhibit 6 – Variable and Fixed Cost Behavior

• Exhibit 7 – Variable, Fixed, and Mixed Cost

SUGGESTED APPROACH

Knowing how costs behave enables management to estimate costs when evaluating alternative operating

proposals. Begin your coverage of this objective by reviewing the definitions of variable, fixed, and

358 Chapter 19(4) Cost Behavior and Cost-Volume-Profit Analysis

Mixed costs have both a fixed and a variable component. An example of a mixed cost is the price paid to

rent a moving van if that price includes a fixed fee plus a charge per mile (i.e., $50 plus $0.30 per mile).

In addition to understanding how costs behave, managers need to know what activities create costs. These

activities are called activity bases (or activity drivers). Ask your students to identify the activity base that

drives their textbook expenditures. (Answer: the number of courses taken)

GROUP LEARNING ACTIVITY—Variable, Fixed, and Mixed Costs

Divide your class into small groups. Ask them to list examples of fixed, variable, and mixed costs

incurred by a McDonald’s restaurant. Encourage them to list as many examples as they can. Also instruct

DEMONSTRATION PROBLEM—High-Low Method

For most business analysis, mixed costs must be separated into their fixed and variable components. Use

the following problem to demonstrate the high-low method.

Once the high and low points have been identified, the variable portion of the cost is determined using the

following equation:

Difference in Total Cost

Variable Cost/Unit Difference in Machine Hours

=

Chapter 19(4) Cost Behavior and Cost-Volume-Profit Analysis 359

Using data from July:

$1,900 = ($0.05/unit 14,000) + Fixed Costs

$1,900 – $700 = Fixed Costs

$1,200 = Fixed Costs

OBJECTIVE 2

Compute the contribution margin, the contribution margin ratio, and the unit contribution

margin.

SYNOPSIS

Cost-volume-profit analysis is useful for managerial decision making. The analysis may be used to

analyze the following: the effects of changes in selling price on profits, the effects of changes in costs of

profits, the effects of changes in volume on profits, how to set prices, how to select the mix of products to

sell, and how to choose marketing strategy. The contribution margin provides insights in to the profit

Key Terms and Definitions

• Contribution Margin – Sales less variable costs and variable selling and administrative

expenses.

• Contribution Margin Ratio – The percentage of each sales dollar that is available to cover the

fixed costs and provide an operating income.

Relevant Example Exercises and Exhibits

• Example Exercise 19(4)-2 Contribution Margin

• Exhibit 8 – Contribution Margin Income Statement Format

SUGGESTED APPROACH

Give students the following formulas related to contribution margin (CM):

CM = Sales – Variable Costs

CM Ratio = CM/Sales

360 Chapter 19(4) Cost Behavior and Cost-Volume-Profit Analysis

Stress that contribution margin is the amount of funds left from a sale after the variable costs have been

paid. Contribution margin is used to pay the fixed costs of the business. Once all fixed costs have been

covered, any contribution margin left represents profit.

GROUP LEARNING ACTIVITY—Contribution Margin

Give your students the following sales and cost data for Van Buren Company. The total sales and cost

information is based on the sale of 20,000 units.

Total Per Unit

Sales $570,000 $28.50

Variable costs $387,600 $19.38

Fixed costs $140,000

Divide the class into small groups. Ask students to compute the total contribution margin, contribution

margin ratio, and unit contribution margin for this company. Also instruct them to compute the increase

in net income that will result from a $50,000 increase in sales and a 1,000-unit increase in sales.

The answers to this exercise are as follows:

2. Contribution margin ratio: 32 percent

4. Increase in net income from $50,000 increase in sales: $50,000 32% = $16,000

5. Increase in net income from 1,000-unit increase in sales: 1,000 $9.12 = $9,120

OBJECTIVE 3

Determine the break-even point and sales necessary to achieve a target profit.

SYNOPSIS

The cost-volume-profit analysis allows a business to determine the break-even point in sales and to

determine the sales needed to make a desired profit. The break-even point is the level of sales at which a

company’s revenues and expenses are equal. It is computed as follows: break-even sales units = fixed

costs/unit contribution margin. This number can also be computed using sales dollars as follows: break-

even sales (dollars) = fixed costs/contribution margin ratio. The break-even point is affected by changes

Chapter 19(4) Cost Behavior and Cost-Volume-Profit Analysis 361

opposite direction. If the sales price increases, the break-even point decreases, and if the sales price

decreases, the break-even point increases. A summary of the effects is shown in Exhibit 13. By modifying

the break-even equation, a business can determine what sales are necessary to achieve a target profit. The

equation is: sales (units) = (fixed costs + target profit)/unit contribution margin.

Key Terms and Definitions

• Break-Even Point – The level of business operations at which revenues and expired costs are

equal.

Relevant Example Exercises and Exhibits

• Example Exercise 19(4)-3 Break-Even Point

• Example Exercise 19(4)-4 Target Profit

• Exhibit 9 – Break-Even Point

SUGGESTED APPROACH

Under this objective, the text presents formulas to calculate the break-even point in units and the unit

sales necessary to achieve a target profit. Use the following lecture notes to explain these formulas.

LECTURE NOTES—Break-Even Point and Target Profit

Although students generally like to use a “formula” in solving accounting problems, they dislike

memorizing them. Remind students that they can use the following formula to solve both break-even and

target profit problems as long as they remember that profit is zero at the break-even point.

Fixed Costs + Target Profit

Sales (units) Unit Contribution Margin

=

Many students benefit from seeing formulas derived from equations they already understand. The text’s

formula can be derived as follows:

362 Chapter 19(4) Cost Behavior and Cost-Volume-Profit Analysis

. . . or (solving for X)

Sales Price (X) – Variable Cost (X) = Fixed Costs + Income from Operations

X (Sales Price – Variable Cost) = Fixed Costs + Income from Operations

X = (Fixed Costs + Income from Operations)/(Sales Price – Variable Cost)

GROUP LEARNING ACTIVITY—Break-Even and Target Profit

One of the true benefits of cost-volume-profit analysis is that a business can analyze a variety of “what-if”

scenarios. TM 19(4)-2 presents several what-ifs for your students to answer in small groups. Solutions are

presented on TM 19(4)-3.

WRITING EXERCISE—Break-Even Point

Ask your students to write an answer to the following questions [TM 19(4)-4]:

Would an increase in variable costs per unit cause a company’s break-even point to

increase or decrease? Why?

OBJECTIVE 4

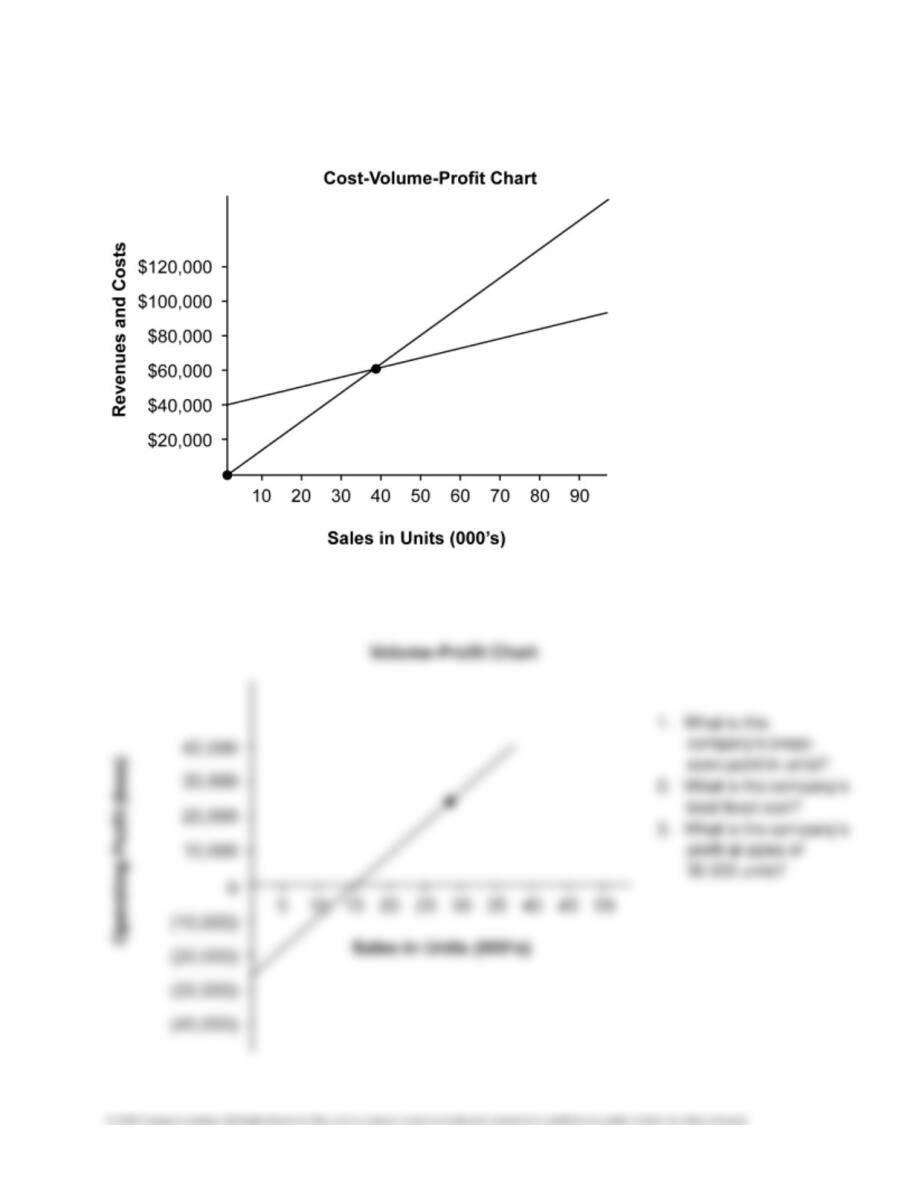

Using a cost-volume-profit chart and a profit-volume chart, determine the break-even point

and sales necessary to achieve a target profit.

SYNOPSIS

Managers often want to know a business’s profit at multiple sales, costs, and the related profits. To

achieve this, a cost-volume-profit chart is constructed over the relevant range. The horizontal axis of the

Chapter 19(4) Cost Behavior and Cost-Volume-Profit Analysis 363

chart is the sales volume expressed in units; the vertical axis displays the dollar amounts of total sales and

total costs. A total sales line is plotted by connecting the point at zero on the left corner of the graph to a

second point on the chart. A total cost line is plotted by beginning with total fixed costs on the vertical

axis. A second point is determined by multiplying the maximum number of units in the relevant range,

which is found on the far right of the horizontal axis by the unit variable costs and adding the total fixed

Key Terms and Definitions

• Cost-Volume-Profit Chart – A chart used to assist management in understanding the

relationships among costs, expenses, sales, and operating profit or loss.

• Profit-Volume Chart – A chart used to assist management in understanding the relationship

between profit and volume.

Relevant Example Exercises and Exhibits

• Exhibit 14 – Cost-Volume-Profit Chart

• Exhibit 15 – Revised Cost-Volume-Profit Chart

• Exhibit 16 – Profit-Volume Chart

• Exhibit 17 – Original Profit-Volume Chart and Revised Profit-Volume Chart

SUGGESTED APPROACH

The mathematical (formula-based) approach to calculating a break-even point is usually more accurate

than the graphic approach. Most students also find the mathematical approach to be a quicker and easier

way to solve problems. However, because it is important that students learn how to read business graphs,

the graphic approach to break-even analysis deserves attention.

364 Chapter 19(4) Cost Behavior and Cost-Volume-Profit Analysis

GROUP LEARNING ACTIVITY—CVP and PV Charts

Handout 19(4)-1 presents a CVP chart and a PV chart. It also poses several questions to test your

students’ ability to read and interpret these graphs. Distribute copies of the handout to your students and

ask them to work in small groups to answer the questions.

Handout 19(4)-1 solutions:

OBJECTIVE 5

Compute the break-even point for a company selling more than one product, the operating

leverage, and the margin of safety.

SYNOPSIS

The sales mix is the relative distribution of sales among the products sold by a company. For break-even

analysis, it is useful to think of the unit selling price as a constant. The constant is the sum of the unit

selling prices of each product multiplied by the sale mix percentage. The equation using E as the constant

is: break-even sales (units) for E = fixed costs/unit contribution margin. If the sales mix changes, the

Key Terms and Definitions

• Margin of Safety – Indicates the possible decrease in sales that may occur before an operating

loss results.

• Operating Leverage – A measure of the relative mix of a business’s variable costs and fixed

costs, computed as contribution margin divided by operating income.

• Sales Mix – The relative distribution of sales among the various products available for sale.

Relevant Example Exercises and Exhibits

• Example Exercise 19(4)-5 Sales Mix and Break-Even Analysis

Chapter 19(4) Cost Behavior and Cost-Volume-Profit Analysis 365

SUGGESTED APPROACH

Cost-volume-profit analysis can be applied to companies that sell more than one product, as long as their

sales mix is constant. Use the Demonstration Problem to illustrate this modification to basic break-even

analysis.

Ask your students to identify examples of sales mixes for various real-life businesses. An example would

be car dealerships that sell different makes of cars, such as Cadillacs and Buicks.

DEMONSTRATION PROBLEM—Sales Mix

To calculate the break-even point for a company that sells more than one product, a weighted average

contribution margin must be determined. The text illustrates this calculation by multiplying the sales price

and then the unit variable cost by the sales mix percentage and adding these two amounts. The calculation

can also be performed directly on the unit contribution margin.

A weighted average unit contribution margin would be as follows:

$1.50 50% = $0.75

To break even, the company would need to sell 18,000 gift boxes ($27,900/$1.55). Using the sales mix,

the number of each type of gift box can be calculated.

Candy: 18,000 50% = 9,000

Nuts: 18,000 30% = 5,400

366 Chapter 19(4) Cost Behavior and Cost-Volume-Profit Analysis

DEMONSTRATION PROBLEM—Operating Leverage

Operating leverage compares contribution margin to operating income. The formula is:

Ask your students to calculate the operating leverage of a company with $800,000 in sales, $200,000 in

variable costs, and $400,000 in fixed costs.

Operating Leverage = $600,000/$200,000 = 3

An operating leverage of 3 indicates that operating income will increase three times any percentage

increase in sales. For example, if sales increase 5 percent, operating income will increase 15 percent. You

may want to prove this by presenting the follow example.

Original Data + 5% in Sales

Sales $800,000 $840,000

GROUP LEARNING ACTIVITY—Margin of Safety

Explain that margin of safety measures the amount by which current sales exceed sales at the break-even

point. It may be expressed in dollars, in units, or as a percentage. When expressed as a percentage, margin

of safety shows the percentage that sales can drop without resulting in an operating loss. The formula to

calculate margin of safety as a percentage of current sales is as follows:

Chapter 19(4) Cost Behavior and Cost-Volume-Profit Analysis 367

INTERNET ACTIVITY—Review of Chapter Concepts

CCH Business Owner’s Toolkit is an excellent Web site for reviewing cost-volume-profit analysis and

related topics from the chapter. Direct your students to the following Web site:

http://www.toolkit.cch.com/text/P06_7500.asp

APPENDIX—VARIABLE COSTING

SYNOPSIS

GAAP accounting requires absorption costing for financial statements. The previous chapters have shown

absorption costing. Alternative reports may be prepared using variable or direct costing. These are for use

in internal decision making. In variable costing, fixed factory overhead costs do not become a part of the

Key Terms and Definitions

• Absorption Costing – The reporting of the costs of manufactured products, normally direct

materials, direct labor, and factory overhead, as product costs.

Relevant Example Exercises and Exhibits

• Exhibit 21 – Absorption Versus Variable Cost of Goods Manufactured

• Exhibit 22 – Variable Costing Income Statement

• Exhibit 23 – Absorption Costing Income Statement

• Exhibit 24 – Relationship Between Variable and Absorption Costing Income

• Exhibit 25 – Units Manufactured Exceed Units Sold

SUGGESTED APPROACH

368 Chapter 19(4) Cost Behavior and Cost-Volume-Profit Analysis

GROUP LEARNING ACTIVITY—Absorption and Variable Costing

To review absorption costing, ask your students to prepare an income statement for Laurens Incorporated,

using the data on TM 19(4)-7.

TM 19(4)-8 displays Laurens’ income statement under absorption costing. It also shows the company’s

income statement under variable costing. Point out the $30,000 difference in the two income statements.

Ask students to examine the income statements, silently on their own, and look for the reason the

LECTURE AID—Variable Costing

Although variable costing is not permitted for financial reporting, many managers find it useful for

management reporting. Variable costing tends to show costs in the same manner as they are incurred:

variable costs on a per-unit basis and fixed costs in total.

Another benefit of variable costing is the ability to isolate the impact of changes in sales or costs. TM

Handout 19(4)-1

1. Identify the sales

and cost lines.

2. What is the break–

even point in units?

3. What is the

company’s total

fixed cost?

4. What is the

company’s variable

cost per unit?

5. What is the

company’s profit at

sales of 80,000

units?

2. What is the company’s

Type Item Description LO(s) Difficulty Time Est BUSPROG AICPA ACBSP – APC Bloom’s EE Excel GL SMH FAI Service Real World Writing Ethics Internet Group

DQ 1 1 Easy 5 min. Analytic Measurement Variable and Fixed Costs Knowledge

DQ 2 1 Easy 5 min. Analytic Measurement Variable and Fixed Costs Knowledge

DQ 3 1 Easy 5 min. Analytic Measurement Variable and Fixed Costs Knowledge

DQ 4 1 Easy 5 min. Analytic Measurement Variable and Fixed Costs Knowledge

DQ 5 2 Easy 5 min. Analytic Measurement Variable and Fixed Costs Knowledge

DQ 6 2 Easy 5 min. Analytic Measurement Contribution Margin Knowledge

DQ 7 3 Easy 5 min. Analytic Measurement Break-even point Knowledge

DQ 8 3 Easy 5 min. Analytic Measurement Break-even point Knowledge

DQ 9 5 Easy 5 min. Analytic Measurement Break-even point Knowledge

DQ 10 5 Easy 5 min. Analytic Measurement Break-even point Knowledge

PE 1A High-low method 1 Easy 10 min. Analytic Measurement Variable and Fixed Costs Application x

PE 1B High-low method 1 Easy 10 min. Analytic Measurement Variable and Fixed Costs Application x

PE 2A Contribution margin 2 Easy 10 min. Analytic Measurement Contribution Margin Application x

PE 2B Contribution margin 2 Easy 10 min. Analytic Measurement Contribution Margin Application x

PE 3A Break-even point 3 Easy 10 min. Analytic Measurement Break-even point Application x

PE 3B Break-even point 3 Easy 10 min. Analytic Measurement Break-even point Application x

PE 4A Target profit 3 Easy 10 min. Analytic Measurement Margin of safety/sales target Application x

PE 4B Target profit 3 Easy 10 min. Analytic Measurement Margin of safety/sales target Application x

PE 5A Sales mix and break-even analysis 5 Easy 10 min. Analytic Measurement Margin of safety/sales target Application x

PE 5B Sales mix and break-even analysis 5 Easy 10 min. Analytic Measurement Margin of safety/sales target Application x

PE 6A Operating leverage 5 Easy 5 min. Analytic Measurement CVP Analysis Application x

PE 6B Operating leverage 5 Easy 5 min. Analytic Measurement CVP Analysis Application x

PE 7A Margin of safety 5 Easy 5 min. Analytic Measurement Margin of safety/sales target Application x

PE 7B Margin of safety 5 Easy 5 min. Analytic Measurement Margin of safety/sales target Application x

EX 1 Classify costs 1 Easy 15 min. Analytic Measurement Variable and Fixed Costs Knowledge

EX 2 Identify cost graphs 1 Easy 15 min. Analytic Measurement CVP Analysis Application

EX 3 Identify activity bases 1 Easy 15 min. Analytic Measurement Managerial Accounting Features/Costs Knowledge

EX 4 Identify activity bases 1 Easy 15 min. Analytic Measurement Managerial Accounting Features/Costs Knowledge

EX 5 Identify fixed and variable costs 1 Easy 15 min. Analytic Measurement Variable and Fixed Costs Knowledge

EX 6 Relevant range and fixed and variable costs 1 Moderate 20 min. Analytic Measurement Variable and Fixed Costs Application x

EX 7 High-low method 1 Easy 15 min. Analytic Measurement Variable and Fixed Costs Application x x

EX 8 High-low method for a service company 1 Moderate 20 min. Analytic Measurement Variable and Fixed Costs Application x x

EX 9 Contribution margin ratio 2 Easy 10 min. Analytic Measurement Contribution Margin Application x

EX 10 Contribution margin and contribution margin ratio 2 Moderate 15 min. Analytic Measurement Break-even point Application x x

EX 11 Break-even sales and sales to realize income from operations 3 Easy 10 min. Analytic Measurement Break-even point Application x

EX 12 Break-even sales 3 Moderate 15 min. Analytic Measurement Break-even point Application x

EX 13 Break-even sales 3 Easy 10 min. Analytic Measurement Break-even point Application x

EX 14 Break-even analysis 3 Easy 10 min. Analytic Measurement Break-even point Application

EX 15 Break-even analysis 3 Moderate 15 min. Analytic Measurement Break-even point Application x

EX 16 Break-even analysis for a service company 3 Moderate 15 min. Analytic Measurement Break-even point Application x x x

EX 17 Cost-volume-profit chart 4 Moderate 20 min. Analytic Measurement CVP Analysis Application x

EX 18 Profit-volume chart 4 Moderate 20 min. Analytic Measurement CVP Analysis Application

EX 19 Break-even chart 4 Moderate 15 min. Analytic Measurement Break-even point Application

EX 20 Break-even chart 4 Moderate 15 min. Analytic Measurement Break-even point Application

EX 21 Sales mix and break-even sales 5 Moderate 15 min. Analytic Measurement Break-even point Application x

EX 22 Break-even sales and sales mix for a service company 5 Moderate 20 min. Analytic Measurement Break-even point Application x

EX 23 Margin of safety 5 Moderate 15 min. Analytic Measurement Margin of safety/sales target Application x

EX 24 Break-even and margin of safety relationships 5 Moderate 10 min. Analytic Measurement Margin of safety/sales target Application x

EX 25 Operating leverage 5 Moderate 15 min. Analytic Measurement CVP Analysis Application x

EX 26 Items on variable costing income statement Appendix Easy 5 min. Analytic Measurement CVP Analysis Application

EX 27 Variable costing income statement Appendix Moderate 15 min. Analytic Measurement CVP Analysis Application x

EX 28 Absorption costing income statement Appendix Moderate 20 min. Analytic Measurement CVP Analysis Application x

PR 1A Classify costs 1 Moderate 45 min. Analytic Measurement Variable and Fixed Costs Application

PR 2A Break-even sales under present and proposed conditions 2,3 Challenging 2 hours Analytic Measurement Break-even point Application x x

PR 3A Break-even sales and cost-volume-profit chart 3,4 Moderate 1 hour Analytic Measurement Break-even point Application

PR 5A Sales mix and break-even sales 5 Easy 1.5 hours Analytic Measurement Break-even point Application x

PR 6A Contribution margin, break-even sales, cost-volume-profit chart, margin of safety, and operating leverage 2,3,4,5 Challenging 1.5 hours Analytic Measurement Contribution Margin Application x

PR 1B Classify costs 1 Moderate 45 min. Analytic Measurement Variable and Fixed Costs Application

PR 2B Break-even sales under present and proposed conditions 2,3 Challenging 2 hours Analytic Measurement Break-even point Application x x

PR 4B Break-even sales and cost-volume-profit chart 3,4 Challenging 1.5 hours Analytic Measurement Break-even point Application

PR 5B Sales mix and break-even sales 5 Easy 1.5 hours Analytic Measurement Break-even point Application x

PR 6B Contribution margin, break-even sales, cost-volume-profit chart, margin of safety, and operating leverage 2,3,4,5 Challenging 1.5 hours Analytic Measurement Contribution Margin Application x

CP 1 Ethics and professional conduct in business 3 Moderate 15 min. Ethics Measurement Break-even point Analysis x x

CP 2 Break-even sales, contribution margin 2,3 Moderate 15 min. Analytic Measurement Break-even point Comprehension x x

CP 3 Break-even analysis 3 Moderate 15 min. Analytic Measurement Break-even point Analysis x

CP 4 Variable costs and activity bases in decision making 3,4 Moderate 30 min. Analytic Measurement Variable and Fixed Costs Analysis x

CP 5 Variable costs and activity bases in decision making 3,4 Challenging 30 min. Analytic Measurement Variable and Fixed Costs Analysis x

CP 6 Break-even analysis 3 Moderate 1 hour Analytic Measurement Break-even point Application x

HOMEWORK CHART WITH LEARNING OUTCOMES TAGGING

TAGGING

RESOURCES

FOCUS