CHAPTER 19 Job Order Costing

Prob. 19-2A

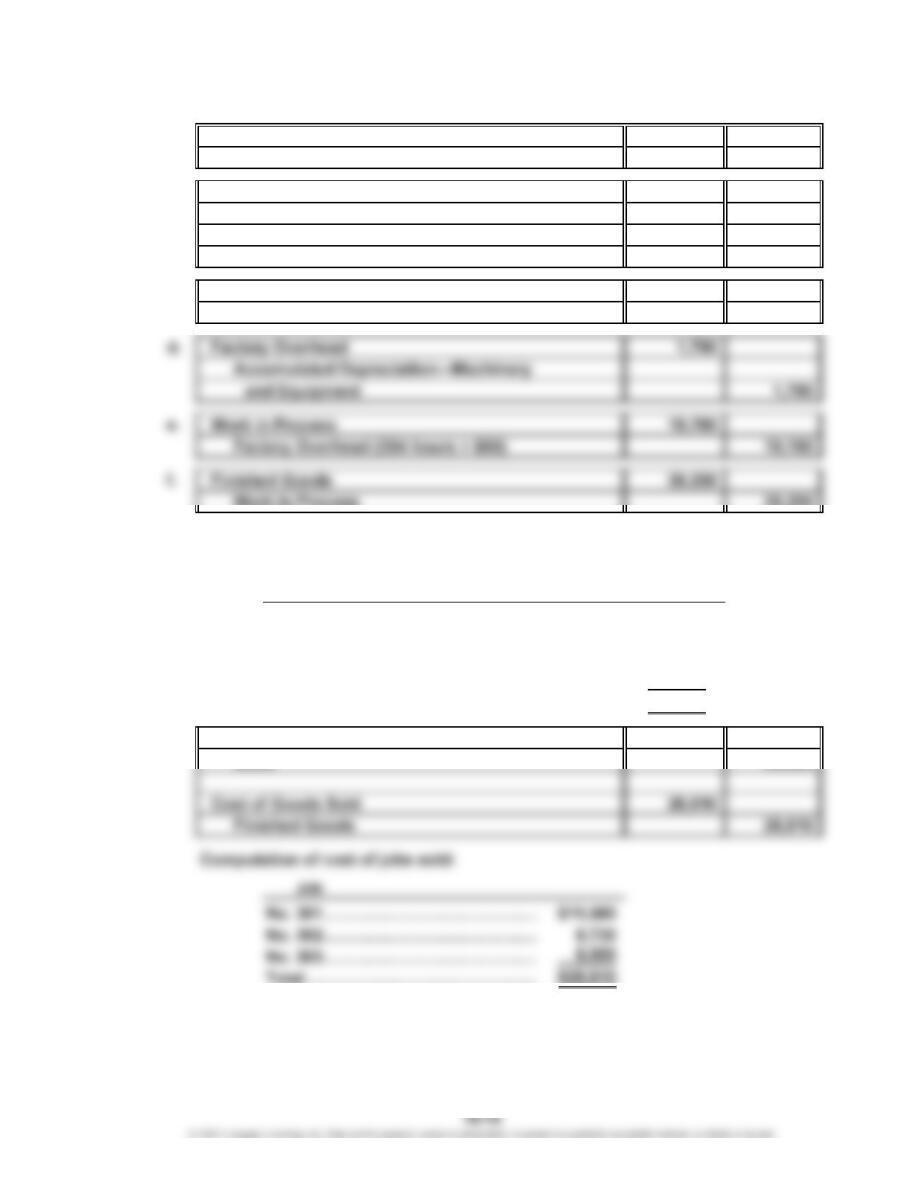

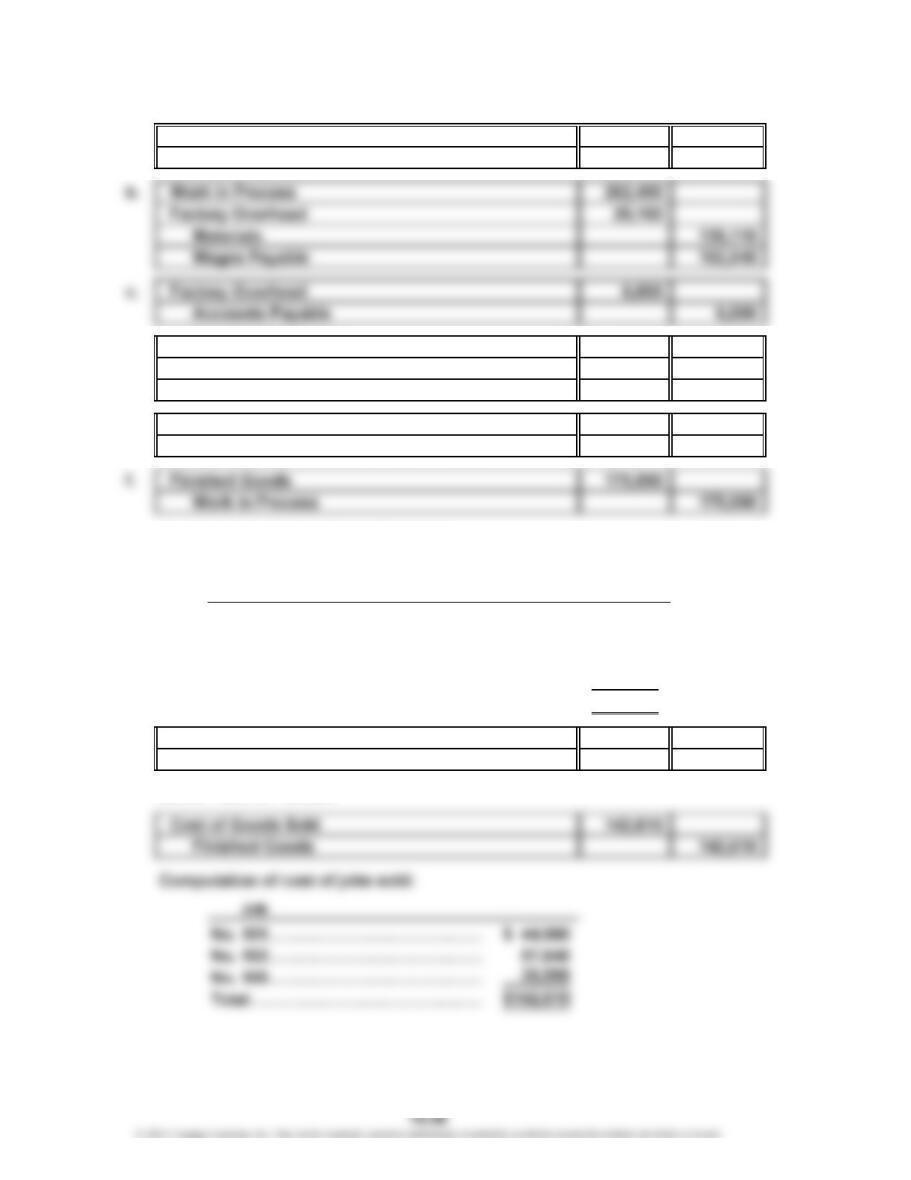

1. a. Materials 33,100

Accounts Payable

b. Work in Process 56,570

Factory Overhead 5,720

Materials

Wages Payable

c. Factory Overhead 6,470

Accounts Payable

Work in Process

Computation of cost of jobs finished:

Direct Direct Factory

Job Materials Labor Overhead Total

No. 301…… $2,740 $5,460 $3,380 $11,580

No. 302…… 3,980 2,930 1,820 8,730

No. 303…… 2,570 3,070 2,860 8,500

No. 305…… 6,210 1,840 2,340 10,390

Total…………………………………………………

…

$39,200

g. Accounts Receivable 60,020

Total……………………………………

…

$28,810

39,200

33,100

32,450

6,470

29,840

CHAPTER 19 Job Order Costing

Prob. 19-2A (Concluded)

2.

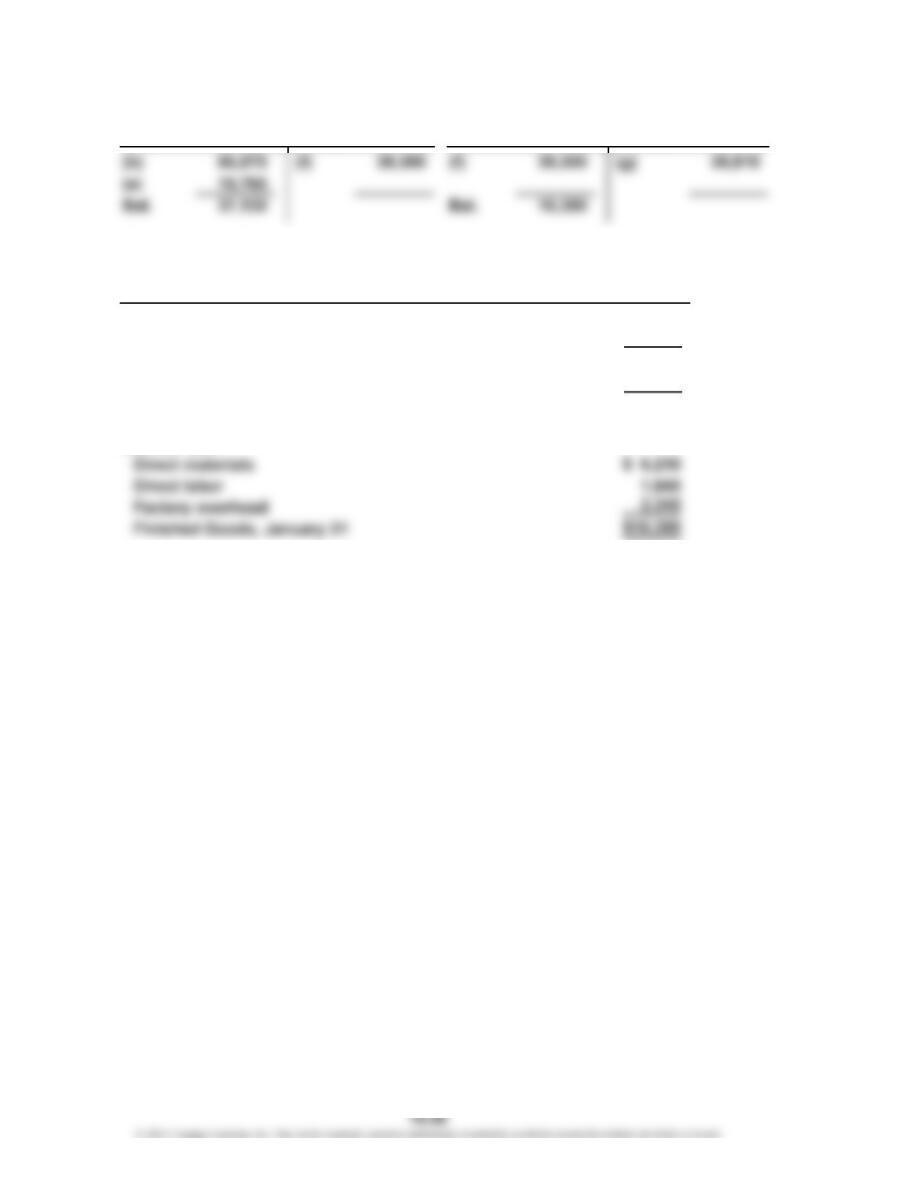

3. Schedule of unfinished jobs:

Direct Factory

Job Labor Overhead

No. 304…………………………

…

$8,520 $4,225

No. 306…………………………

…

6,110 5,135

Balance of Work in

Process, January 31…………………………………………………

4.

Job No. 305:

$8,850

4,290

$21,595

15,535

Work in Process Finished Goods

Direct

TotalMaterials

$37,130

Schedule of completed jobs:

1. and 2.

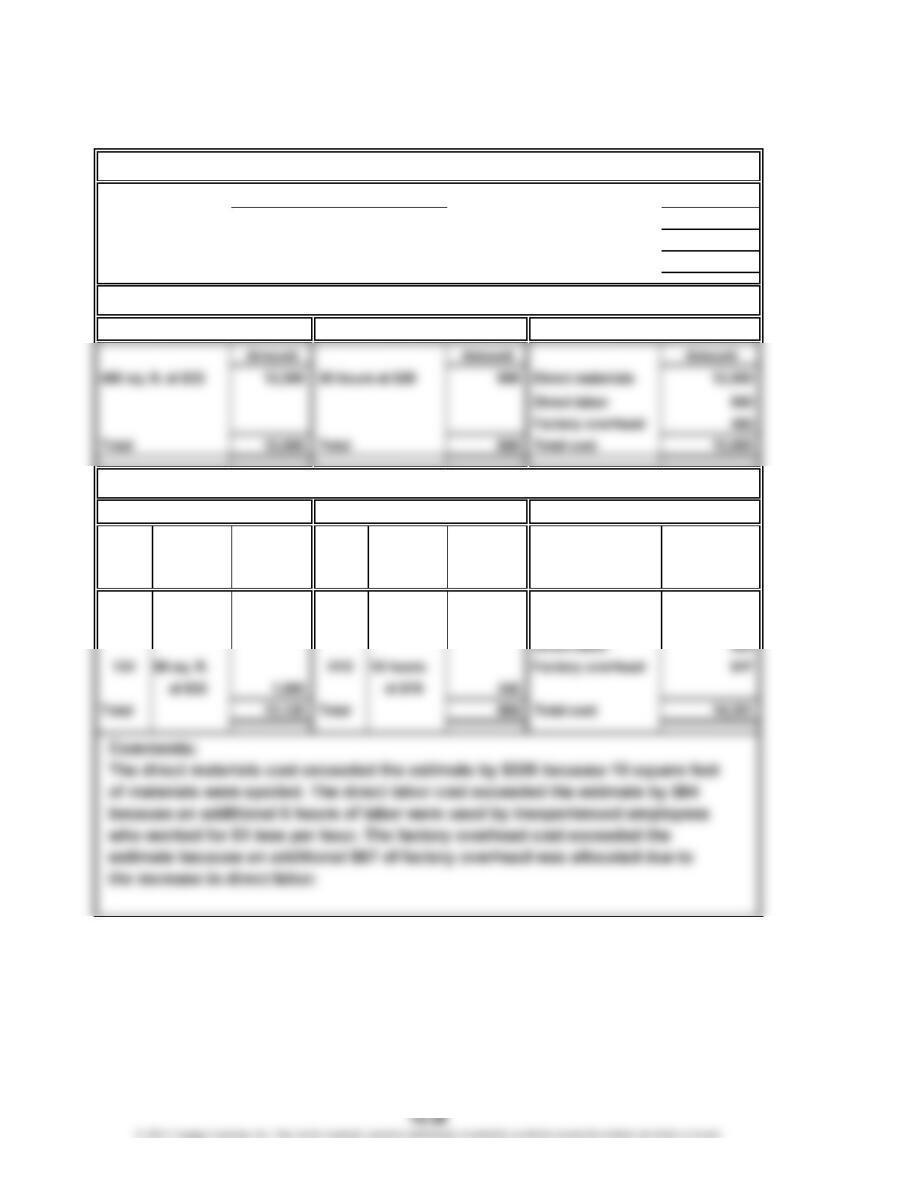

Jackson Consulting Date October 1

Date wanted October 10

Date completed October 10

Job. No.

Mat. Time

Req. Ticket

No. Description Amount No. Description Amount Item Amount

112 140 sq. ft. H10 10 hours

at $35 4,900 at $20 200 Direct materials 7,280

Direct labor 400

114 68 sq. ft. H11 10 hours Factory overhead 300

at $35 2,380 at $20 200

Total 7,280 Total 400 Total cost 7,980

Comments:

The direct materials cost exceeded the estimate by $280 because 8 square feet of

ESTIMATE

Direct Materials Direct Labor Summary

ACTUAL

Direct Materials Direct Labor Summary

JOB ORDER COST SHEET

Customer

CHAPTER 19 Job Order Costing

Prob. 19-4A

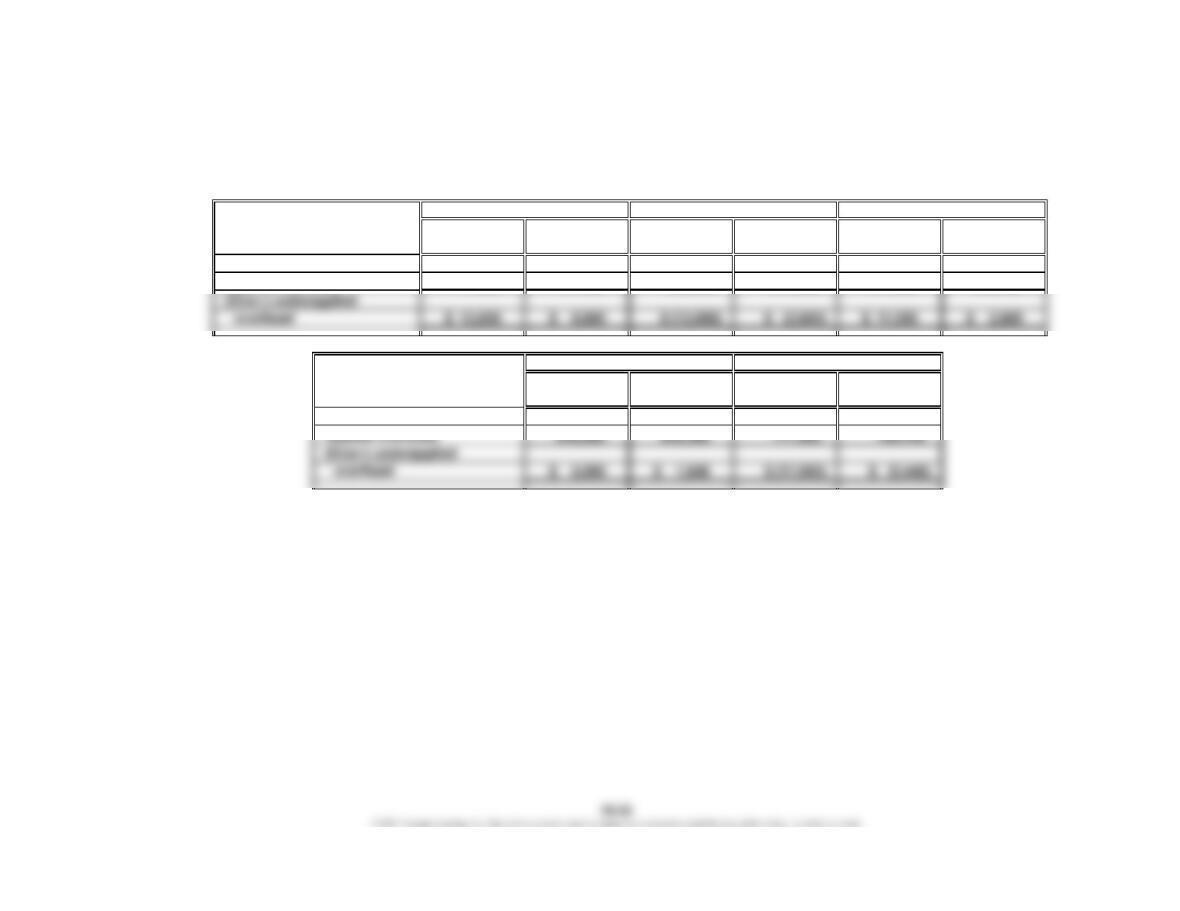

1. Supporting calculations:

June 1 Cost of

Work in Direct Direct Factory Total Unit Units Goods

Quantity Process Materials Labor Overhead Cost Cost Sold Sold

No. 201 550 $16,500 $ 55,000 $ 41,250 $ 57,750 $ 170,500 $310.00 440 $136,400

No. 202 1,100 44,000 93,500 71,500 100,100 309,100 281.00 880 247,280

a. $395,500. Materials applied to production in June + indirect materials.

($351,500 + $44,000)

b. $60,500. From table above and problem.

c. $351,500. From table above.

d. $264,450. From table above.

Job. No.

CHAPTER 19 Job Order Costing

Prob. 19-4A (Concluded)

2. June 30 balances:

Materials……………………

…

$ 17,000 ($82,500 + $330,000 – $395,500)

Work in Process*…………

…

143,060 ($91,300 + $51,760, Job 203 and Job 206)

Finished Goods**…………

…

151,750 ($903,620 – $751,870)

Factory Overhead…………

…

9,820 Dr. underapplied ($33,000 + $65,550

+ $44,000 + $237,500 – $370,230)

*$60,500 + $351,500 + $264,450 + $370,230 – $903,620 = $143,060

** Units in Unit Total

Inventory Cost Cost

110 $310.00 $ 34,100

201

Job. No.

CHAPTER 19 Job Order Costing

Prob. 19-5A

1.

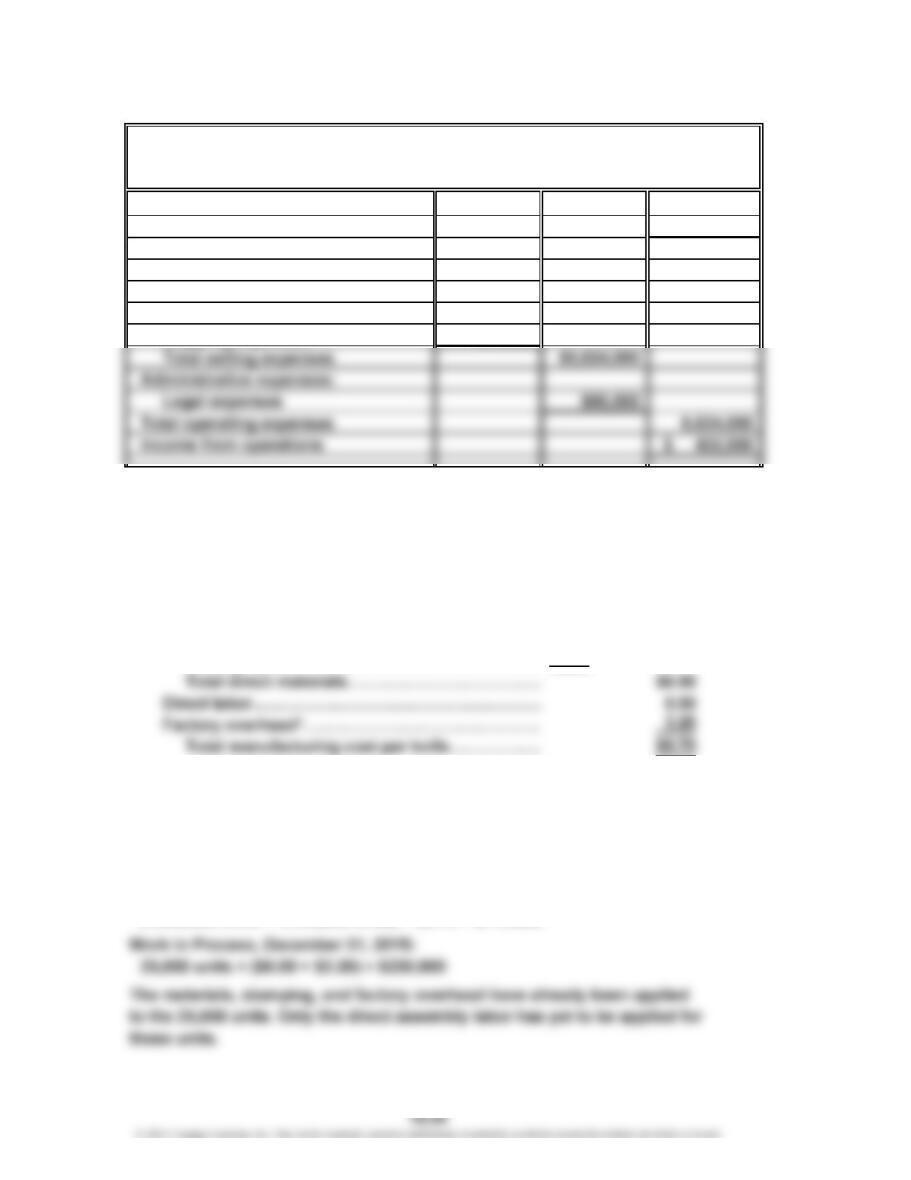

Sales $17,920,000

Cost of goods sold 10,864,000

Gross profit $ 7,056,000

Selling expenses:

Infomercial campaign $2,000,000

Promotional materials 3,600,000

Shipping expenses 224,000

Supporting calculations:

Sales: 1,120,000 units × $16 = $17,920,000

Cost of goods sold: 1,120,000 units × $9.70 = $10,864,000

Manufacturing cost per unit (knife):

Direct materials:

Hardened steel blanks……………………………

…

$4.00

Wood (for handle)…………………………………

…

1.50

Packaging……………………………………………

…

0.50

*$800 ÷ 250 knives per hour

Infomercial campaign: $600,000 + $1,400,000 = $2,000,000

Promotional materials: 60,000 stores × $60 = $3,600,000

Shipping expenses: 1,120,000 units × $0.20 = $224,000

2. Finished Goods balance, December 31, 20Y8:

Ginocera Inc.

Income Statement

For the Year Ended December 31, 20Y8

CHAPTER 19 Job Order Costing

Prob. 19-1B

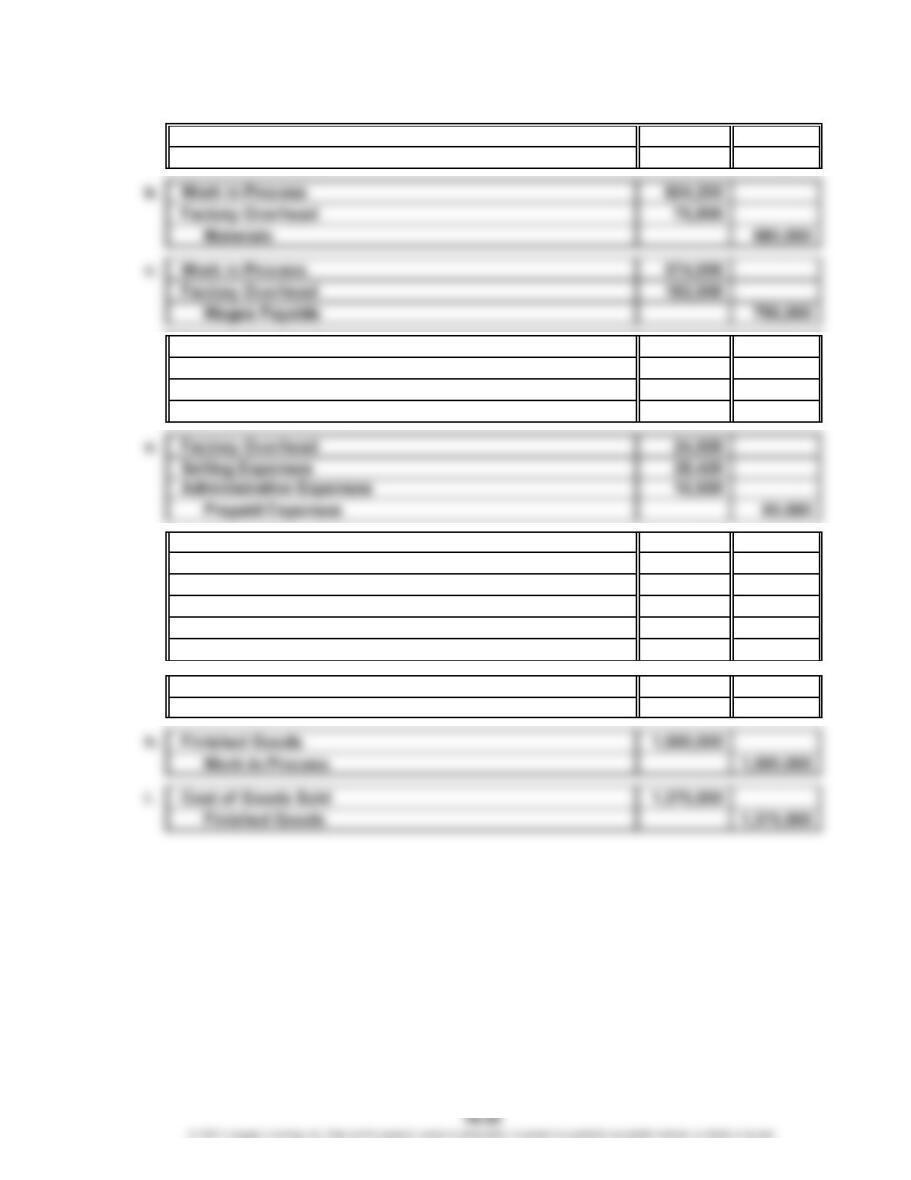

a. Materials 770,000

Accounts Payable 770,000

d. Factory Overhead 245,000

Selling Expenses 171,500

Administrative Expenses 110,600

Accounts Payable 527,100

f. Factory Overhead 49,500

Depreciation Expense—Office Equipment 61,800

Depreciation Expense—Office Building 14,900

Accumulated Depreciation—Factory Equipment 49,500

Accumulated Depreciation—Office Equipment 61,800

Accumulated Depreciation—Office Building 14,900

g. Work in Process 568,500

Factory Overhead 568,500

CHAPTER 19 Job Order Costing

Prob. 19-2B

1. a. Materials 147,000

Accounts Payable

d. Factory Overhead 4,100

Accumulated Depreciation—Machinery

and Equipment

e. Work in Process 40,480

Factory Overhead (1,012 hours × $40)

Computation of cost of jobs finished:

Direct Direct Factory

Job Materials Labor Overhead Total

No. 101…… $19,320 $19,500 $6,160 $ 44,980

No. 102…… 23,100 28,140 6,400 57,640

No. 103…… 13,440 14,000 5,040 32,480

No. 105…… 18,050 15,540 6,400 39,990

Total……………………………………………………

…

$175,090

g. Accounts Receivable 189,100

Sales*

*$62,900 + $80,700 + $45,500

40,480

4,100

189,100

147,000

CHAPTER 19 Job Order Costing

Prob. 19-2B (Concluded)

2.

(b) 262,490 (f) 175,090 (f) 175,090 (g) 142,610

3. Schedule of unfinished jobs:

Direct Factory

Job Labor Overhead

No. 104……………………

…

$36,500 $9,520

…

4. Schedule of completed jobs:

Job No. 103:

Direct materials

$13,440

$38,200

$ 84,220

Work in Process Finished Goods

Direct

TotalMaterials

CHAPTER 19 Job Order Costing

Prob. 19-3B

1. and 2.

Lunden Consulting Date May 9

Date wanted May 15

Date completed May 15

Job. No.

Mat. Time

Req. Ticket

No. Description Amount No. Description Amount Item Amount

132 360 sq. ft. H9 18 hours

at $32 11,520 at $19 342 Direct materials 13,120

ESTIMATE

Direct Materials Direct Labor Summary

ACTUAL

Direct Materials Direct Labor Summary

JOB ORDER COST SHEET

Customer

CHAPTER 19 Job Order Costing

Prob. 19-4B

1. Supporting calculations:

May 1 Cost of

Work in Direct Direct Factory Total Unit Units Goods

Quantity Process Materials Labor Overhead Cost Cost Sold Sold

No. 101 330 $26,400 $ 82,500 $ 59,400 $ 29,700 $ 198,000 $600.00 264 $158,400

No. 102 380 46,000 105,400 72,600 36,300 260,300 685.00 360 246,600

No. 103 500 132,000 110,000 55,000 297,000

No. 104 400 66,000 39,600 19,800 125,400 313.50 384 120,384

a. $586,100. Materials applied to production in May + indirect materials.

($570,700 + $15,400)

b. $72,400. From table above and problem.

c. $570,700. From table above.

d. $378,400. From table above.

Job. No.

CHAPTER 19 Job Order Costing

Prob. 19-4B (Concluded)

2. May 31 balances:

Materials……………………

…

$ 19,500 ($105,600 + $500,000 – $586,100)

*$72,400 + $570,700 + $378,400 + $189,200 – $801,500 = $409,200

** Units in Unit Total

Inventory Cost Cost

66 $600.00 $ 39,600

Job. No.

101

…

CHAPTER 19 Job Order Costing

Prob. 19-5B

1.

Sales $18,400,000

Cost of goods sold 11,914,000

Gross profit $ 6,486,000

Selling expenses:

Salespersons commissions $3,680,000

Supporting calculations:

Sales: 460,000 units × $40 = $18,400,000

Cost of goods sold: 460,000 units × $25.90 = $11,914,000

Manufacturing cost per unit:

Direct materials:

Leather………………………………………………

…

$10.00

V

elvet (for interior)…………………………………

…

5.00

Packaging……………………………………………

…

0.40

*$1,250 ÷ 125 units per hour

Salespersons commissions: $18,400,000 × 20% = $3,680,000

2. Finished Goods balance, December 31, 20Y3:

(500,000 units – 460,000 units) × $25.90 = $1,036,000

Work in Process, December 31, 20Y3:

22,000 units × ($15.40 + $10.00) = $558,800

Technology Accessories Inc.

Income Statement

For the Year Ended December 31, 20Y3

CHAPTER 19 Job Order Costing

CP 19-1

No. Tandy’s plan is not ethical. A job order cost accounting system accumulates and

records product costs by jobs. The resulting total and unit product costs can be

compared to similar jobs, compared over time, or compared to expected costs. In this

way, a job order cost system can be used by managers for cost evaluation and control.

CP 19-2

1. Direct labor cost:

Total actual (applied) overhead, Year 1–Year 5……

…

$ 4,200,000

Total direct labor cost, Year 1–Year 5………………

…

21,000,000

Predetermined overhead rate

($4,200,000 ÷ $21,000,000)………………………

…

20% of direct labor cost

Machine hours:

…

…

…

CASES & PROJECTS

CHAPTER 19 Job Order Costing

CP 19-2 (Continued)

2.

Direct Labor Machine Direct Labor Machine Direct Labor Machine

Cost Hours Cost Hours Cost Hours

Actual overhead $790,000 $790,000 $870,000 $870,000 $935,000 $935,000

Applied overhead 777,000 781,200 882,000 873,600 924,000 932,400

Direct Labor Machine Direct Labor Machine

Cost Hours Cost Hours

$845,000 $845,000 $760,000 $760,000

Year 5 Year 4

Year 1

Year 3

Year 2

Actual overhead

CHAPTER 19 Job Order Costing

CP 19-2 (Concluded)

3. The best predetermined overhead rate is machine hours. Although the total

overhead applied for each rate developed in part (1) is the same over the entire

five-year period (as a result of the method by which the predetermined overhead

rates were developed), the predetermined overhead rate based on machine hours

CP 19-3

To: Carol Creedence

From: A+ Student

Re: Product CCR Job Cost

The graph of job costs for Product CCR indicates two significant trends in job cost.

First, there appears to be a strong and consistent “Friday effect.” Unit cost increases

significantly on Fridays, then falls on Monday. Each Friday effect is larger than the

previous week. There also appears to be a steady increase in the unit cost over time, with

unit cost increasing significantly over the time period.

The “Friday effect” could be caused by a reduction in the efficiency of the workforce on

Fridays, as it is the last day of the workweek. If this is the case and the trend is not

product-related, then it should also appear throughout the plant. To test this explanation,

management should collect job cost data for other products in the plant. If the trend

CHAPTER 19 Job Order Costing

CP 19-4

1. The unit costs are influenced by both the price and quantity of inputs. On the

price side, the cost of steel has dropped from $1,200 to $1,100 per ton. This is

apparently the result of the purchasing manager’s decision to reduce the cost

of raw materials by going to a new vendor. No other input prices change.

Some of the input quantities changed for the worse. Specifically, the following:

Steel input…………………………………………

…

2.10 tons12.60 tons2

Foundry labor……………………………………

…

8.00 hours

3

10.00 hours

4

Welding labor……………………………………… 11.00 hours

5

14.00 hours

6

1105 tons ÷ 50 units

2195 tons ÷ 75 units

2. A possible reason for this deterioration in performance is related to the

purchasing manager’s decision to change vendors in order to secure a lower

price per ton. The new vendor is apparently delivering a lower-quality steel

product to the company. As a result, the foundry operation is spending

more time forming the steel parts. Moreover, the increased steel tons per unit

Job 206 Job 228

Input Quantity per Unit

CHAPTER 19 Job Order Costing

CP 19-5

1. Todd should record the debits for factory wages as a debit to Work in Process.

The factory wages are product costs that must be accumulated in the cost of

producing the product. Eventually, these wage costs will become part of the

finished goods inventory and the cost of goods sold when the gift items are sold.

Likewise, the depreciation should be recorded as a debit to Factory Overhead.

The overhead is then applied to production work in process. Like the wages, the

depreciation will also eventually become part of the finished goods inventory and

2. Jeff would not be concerned about expensing administrative wages and