CHAPTER 19

COSTING AND THE VALUE CHAIN

Brief Learning

Exercises Topic Objectives Skills

B. Ex. 19.1 Value chain components 19-1

Analysis

B. Ex. 19.2 Capturing market share with target prices 19-4

Analysis

B. Ex. 19.3 Cost of quality 19-7

Analysis, judgment

B. Ex. 19.4 Cost reduction non-value-added activities 19-2

Analysis, judgment

B. Ex. 19.5 Manufacturing efficiency in a JIT system 19-6

Analysis

B. Ex. 19.6 Activity-based management cost savings

19-2, 19-3,

19-7

Analysis, judgment

B. Ex. 19.7 Target costing 19-4

Analysis

B. Ex. 19.8 Cost of quality 19-7

Analysis

B. Ex. 19.9 Characteristics of quality 19-8

Analysis

B. Ex. 19.10 Target costing and cash flows 19-5

Analysis

Learning

Exercises Topic Objectives Skills

19.1 Accounting terminology

19-2–19–6 Analysis

19.2 Value chain activities 19-1

Analysis, communication,

judgment

19.3 Value-added vs. non-value-added activities 19-2, 19-3

Analysis

19.4 Activity-based management 19-3

Analysis

19.5 Target costing 19-4, 19-5

Analysis

19.6 Just-in-time manufacturing 19-6

Analysis, judgment

19.7 Cost of quality 19-7, 19-8

Analysis

19.8

Value-added and non-value-added activity

costs

19-2, 19-7

Analysis, judgment

19.9 Activity-based management at First Bank 19-3

Analysis

19.10 Quality costs and value chain decisions

19-1, 19-2,

19-7

Analysis, communication,

judgment

19.11 Just-in-time efficiency measures 19-6

Analysis, judgment

19.12 Target costing at Pizza Pies Limited 19-4, 19-5

Analysis, judgment

19.13 Classifying activities 19-2, 19-7

Analysis

19.14 Quality cost tradeoffs 19-7

Analysis, judgment

19.15 Real World: Home Depot 19-3

Analysis, research

Non-value-added costs

OVERVIEW OF BRIEF EXERCISES, EXERCISES, PROBLEMS, AND CRITICAL

THINKING CASES

Topic Skills

19.1 A,B

Identifying value-added and non-value-

19-2, 19-6

Analysis, communication,

activities judgment

19.2 A,B

Activity-based management and target

costing

19-2–19-5 Analysis

19.3 A,B

Target costing 19-4, 19-5 Analysis

19.4 A,B

Cost of quality 19-7, 19-8 Analysis, judgment

19.5 A

Real World: Home Depot 19-1–19-7 Analysis, communication,

Value chain judgment, research

19.6 A

Kare Company’s quality improvement

19-7, 19-8

Analysis, communication,

judgment

19.7 A

Activity-based management at

BookWeb, Inc.

19-2, 19-3

Analysis, judgment

19.8 A

Real World: Kimberly-Clark 19-1–19-8 Analysis,

Value chain, quality, and efficiency communication, judgment

Critical Thinking Cases

19.1 Activity-based management and target 19-2–19-7 Analysis, communication,

costing judgment

19.2 Just-in-time frozen dinners Analysis, communication,

judgment

19.3 Real World: Manufacturing 19-1–19–7

Analysis, research,

Engineering, Inc. (Internet) technology

19. 4

Sarbanes-Oxley and non-value-added

activities (Ethics, fraud & corporate

governance)

19-1–19-3

Analysis, research,

communication

Problems

Sets A, B

Learning

Objectives

19-1, 19-2,

19-6

DESCRIPTIONS OF PROBLEMS AND CRITICAL THINKING CASES

Problems (Sets A and B)

19.1 A,B

Castner Corporation/Quartex Corporation 30 Medium

Identifying how value-adding activities can improve efficiency. The

problem also has an ethical component that requires students to decide

if a company should attempt to improve efficiency by downsizing. This

is a good group discussion problem.

19.2 A,B

The Kallapur Company/Bitmore Company 60 Strong

Comprehensive target costing problem that illustrates how the method

used to allocate fixed overhead affects the manufacturing cost per unit

assigned to different products. Activity-based management is also used

in making decisions on how to reach a target cost.

19.3 A,B

Meiger Mining/Oro Mining 30 Medium

A target costing problem that requires the student to analyze an

alternative offered for reaching the desired target cost.

19.4 A,B Arusetta, Inc./Nazu, Inc. 40 Medium

A cost of quality problem that requires the construction of a categorical

cost of quality report. The student is also asked to analyze changes in

specific quality costs in light of the implementation of a total quality

management program.

19.5 A Home Depot 30 Medium

Students read Note 1 from Home Depot’s annual report to find

references to Home Depot’s value chain.

19.6 A Kare Company 40 Medium

Students identify quality costs and calculate quality costs as a percent of

sales over two years. Students prepare a graph illustrating the trade-off

between prevention and failure costs.

19.7 A BookWeb, Inc. 50 Strong

Students use activity-based management tools to manage the value

chain of a book warehousing operation. Students must identify activities

that give rise to non-value-added costs at the company.

Below are brief descriptions of each problem, case, and the Internet assignments. These descriptions

are accompanied by the estimated time (in minutes) required for completion and by a difficulty rating.

The time estimates assume use of the partially filled-in working papers.

19.8 A Kimberly-Clark Corporation 30 Medium

Recent areas of focus for Kimberly-Clark as identified in their

annual report are matched with the concepts introduced in the

chapter. Students consider how the concepts will help Kimberly-

Clark achieve their goals.

Critical Thinking Cases

19.1 Mays Electronics 50

Medium

A target costing and activity-based management problem that requires

students to analyze the effects of several actions. Also illustrates how

suggestions for cost reductions can be elicited from numerous sources,

such as suppliers, customers, and employees.

19.2 Healthy Times Frozen Dinners 40 Strong

Determining inefficiencies of a company by isolating value-added and

non–value-added activities.

Manufacturing Engineering, Inc.

19.3 Internet 30 Medium

Students are asked to access a sample reengineering project and assess the

usefulness of cost information.

Sarbanes-Oxley and Non-Value-Added Activities

19.4 Ethics, Fraud, and Corporate Governance 25 Medium

Students are asked to identify the costs and benefits of SOX and, in

particular, economy-wide benefits.

SUGGESTED ANSWERS TO DISCUSSION QUESTIONS

2.

The R&D and design component of the value chain would include all activities pertaining to the

type, location, menu, and service characteristics of the new restaurant. Examples include (but

3.

The marketing component of a fire department’s value chain would include all activities

designed to educate citizens on how to reach the department and for which types of emergencies

4.

Value-added activities add to the product’s or service’s desirability in the eyes of the consumer.

Customers would conceivably be willing to pay more for a product where such activities have

5.

The storage of the stereos results in explicit costs such as the cost of renting/owning the

6.

Target costing is better applied at the earliest stages of the value chain because it is estimated

7.

The objective of activity-based management is to use activity-based information, including

8.

In a JIT system, goods are produced only in sufficient quantity to meet customer demand.

Therefore, the goods must be “defect-free,” or the company will be unable to meet demand.

9.

The idea behind JIT is to minimize not only inventory but also all non-value-added activities.

Also, with minimal inventories to serve as a reserve, a JIT system requires a high degree of

10.

Prevention costs consist of the costs incurred by an organization to prevent defects from

occurring. Examples of prevention costs include employee training, efforts to design quality

into the product or production process, process quality audits, and the costs of evaluating

supplier quality. Appraisal costs are incurred to ensure that products conform to quality

standards. The most common appraisal costs are associated with product or raw materials

11.

Life-cycle costing consists of estimating the total costs incurred by a customer from the time

12.

Until management has a clear understanding of the activities that drive costs, they will not be

13.

Agree:

•A break down of machines in a JIT environment has the potential to halt production.

•

Disruptions in production are more serious in a JIT environment because it is

demand driven.

•

Any break down in the flow of operations, whether machine related or non-machine

related is likely to cause a serious disruption in a JIT environment.

15.

The four target costing components are 1) planning and market analysis, 2) concept

development, 3) production design and value engineering, and 4) production and continuous

improvement. Planning and market analysis would be critical to determine competitors prices

and the value they deliver customers at that price. Also, determining customer views of value-

Student answers may vary, but the arguments on both sides should include the following:

•

The cost of carrying inventory for non JIT firms may be equal to the opportunity

cost associated with disrupted sales in the JIT firm.

SOLUTIONS TO BRIEF EXERCISES

B. Ex. 19.1

B. Ex. 19.3

B. Ex. 19.4

B. Ex. 19.5

B. Ex. 19.6

Time savings with new mix and knead time = 50% × 50% =25%.

Cost savings with new mix and knead time = .25 × $850,000 = $212,500.

Design Phase—activities include designing new sailboats, market analysis of

Old mix and knead time = 50%.

Student answers will vary.

Student answers will vary.

B. Ex. 19.9

B. Ex. 19.10

The consulting firm should be focusing on customers perceptions of quality.

Current year cash flow implication of the proposed purchase of new

SOLUTIONS TO EXERCISES

Ex. 19.1 a. Non-value-added activity

Ex. 19.2 a.

Research and development activities of a management accountant might

include asking managers what types of information they need to make decisions

Ex. 19.3 1. Value-added.

2.

Non-value-added. Although the materials must be unloaded, it would be more

efficient if they were delivered straight to the Cutting Department as they were

needed.

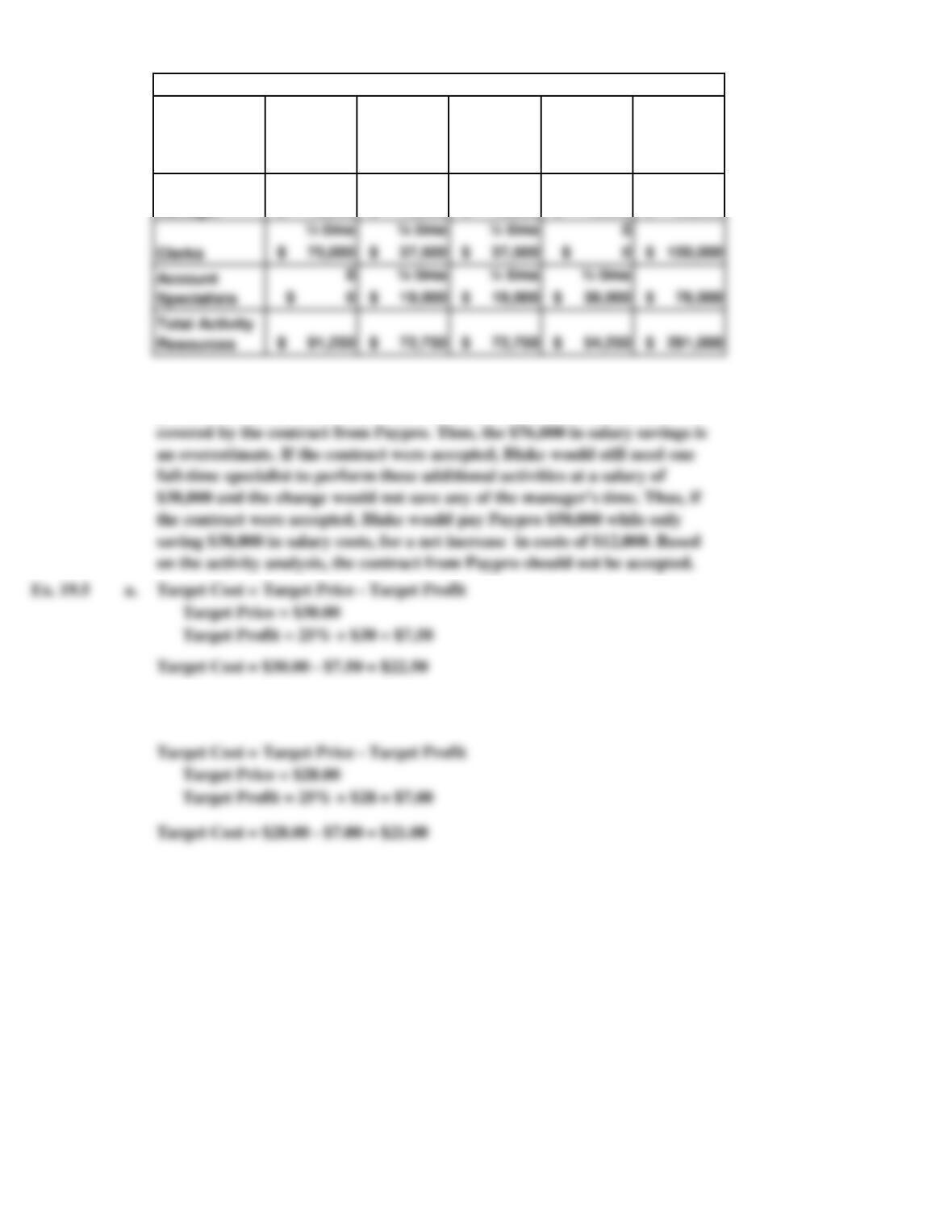

Ex. 19.4 a.

Labor

Category

Billing and

Recording

Payments

Customer

Service

Financial

Reporting

& Analysis

Delinquent

Accounts

Total Labor

Resources

¼ time ¼ time ¼ time ¼ time

$ 16,250 $ 16,250 $ 16,250 $ 16,250 $ 65,000

b.

Ex. 19.5 a.

b.

Since the competitor is selling essentially the same product for $28.00, On

Point should set its target price at that level to remain competitive.

BLAKE FURNITURE, INC.

Accounts Receivable Department

Manager

Activity Category

In addition to handling delinquent account activities, the account specialists

perform customer service activities and analysis activities that are not

½ time ¼ time ¼ time 0

$ 75,000 $ 37,500 $ 37,500 $ 0 $ 150,000

$ 91,250 $ 72,750 $ 72,750 $ 54,250 $ 291,000

Clerks

Ex. 19.5

(continued)

c.

d.

JIT and TQM implementation would allow for the elimination of inspection

and storage time, which would reduce cycle time to 11 days (18 – 4 – 3). Cart’s

The original estimated selling price of $30 would yield a profit of $7.50 per

unit once the target cost had been achieved. Total yearly profits would be:

Ex. 19.7 a.

11,000$

13.2%

Internal and External

Failure Costs as a

=

=

=

b. ($11,000 + $15,000) $26,000

$500,000 $500,000

Ex. 19.8

a.

b.

c.

Purchasing large quantities of materials to obtain a discount can be a value-

Low quality materials entering the production process can create downtime for

=

Transferring employees out of inspection to help with production can lower

NOGAIN MANUFACTURING

Quality Cost Report

For the Current Year Ended December 31

=

5.2%

Prevention and

Appraisal Costs as a

=

Foundry & Bellows, Inc. value-added and non-value-added activities are:

Prevention costs:

Machine maintenance ……………………………………………………………..

Total quality costs ………………………………………………………………….

External failure costs:

Inspections …………………………………………………………………………

Internal failure costs:

Lost sales …………………………………………………………….

Machine breakdown ……………………………………………………

Appraisal costs:

Scrap and rework …………………………………………………

Warranties …………………………………………………………

Defect returns ………………………………………………………….

Ex. 19.9

Ex. 19.10

Heavy Duty as

a Percentage of

Total

Regular as a

Percentage of

Total

Total

Activity

Costs

Activity

Cost to

Heavy Duty

Activity

Cost to

Regular

33% 67%

60% 40% $ 130,000 $ 78,000 $ 52,000

If each cashier spends five percent of his/her time on helping customers organize

their purchases, then a total of 5 cashiers × 5% = 25% of total cashier time per store

is consumed with organizing customer’s purchases. The clerks have enough capacity

to undertake assisting the customer because 10% idle time per clerk × 6 clerks =

Activities:

Production

Warranty

80% 20% 120,000 96,000 24,000

75% 25% 70,000 52,500 17,500

55% 45% 32,000 17,600 14,400

90% 10% 50,000 45,000 5,000

Recalls

Rework

Ex. 19.10

(continued)

Ex. 19.11

Ex. 19.12 a. Target cost = $6.50/1.10 = $5.91.

Ex. 19.13 a. Internal failure, non-valued added.

Internal failure, non-value-added (Kimberly-Clark would prefer no waste

Clearly, the Heavy Duty vacuum has the highest quality cost per unit (five times

the quality cost per unit of Regular). The manager might want to consider the

Items a., b., c., e., and f. might be considered non-value-added activities in a JIT

system. If that is the case, then:

c.

d.

Home Depot measures shrink by undertaking regular physical inventories

and comparing those inventories to its records. Between physical

Home Depot accrues estimated losses for shrink until a physical inventory

SOLUTIONS TO PROBLEMS SET A

PROBLEM 19.1A

CASTNER CORPORATION

a.

b.

c.

Production Activity

2

30 Minutes, Medium

Total cycle time:

Inspecting materials

Storing materials

Moving materials into production

Setting up production equipment

Assembling finished products

Painting finished products

Bending materials

Value-added production activities:

Inspecting materials ………………………………………………………………

Number of Days

Non-value-added production activities:

Cutting materials

2

3

Setting up production equipment ……………………………………………….

Moving materials into production …………………………………………………

PROBLEM 19.1A

CASTNER CORPORATION (concluded)

d.

e.

f.

There is no simple answer to this question. It may be argued that Castner does indeed

have a responsibility to those employees who have devoted their careers to the company.

Castner’s total cycle time was computed in part c above. Its value-added time is shown

below:

The following activities might be reduced or eliminated if Castner implements a JIT

system:

Manufacturing efficiency ratio: Value-Added Time ÷ Total Cycle Time

PROBLEM 19.2A

THE KALLAPUR COMPANY

a.

b.

Target Cost = $220 – $33 = $187

Target Cost = $120 – $18 = $102

Target Cost: QUIN

Target Cost = Target Price – Target Profit

Target Cost = Target Price – Target Profit

If fixed overhead is allocated based on units of production, the fixed overhead cost per unit

is equal to $50 calculated as follows:

60 Minutes, Strong

Target Cost: KAP1

Total manufacturing cost per unit: