Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

19-1

CHAPTER 19

JOB ORDER COSTING

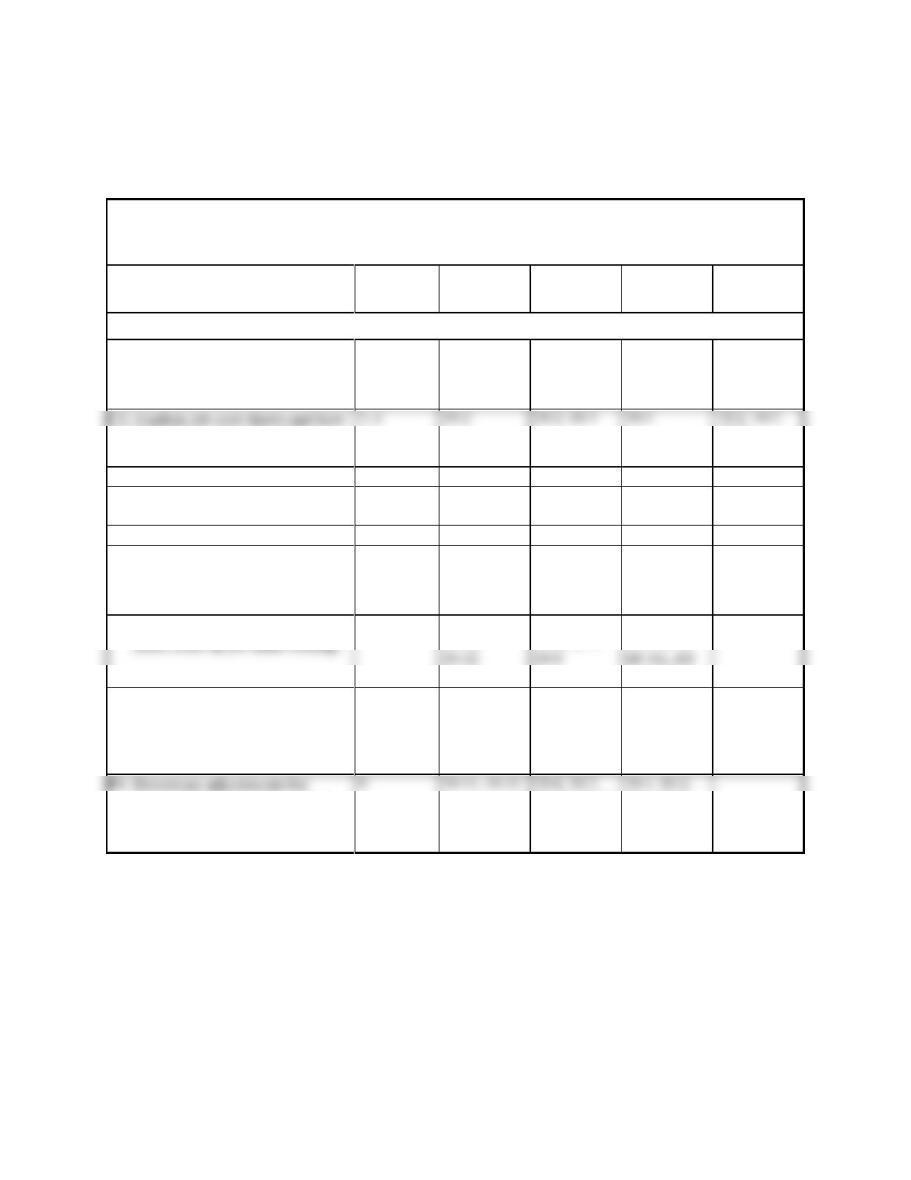

Related Assignment Materials

Student Learning Objectives

Questions

Quick

Studies*

Exercises*

Problems*

Beyond the

Numbers

Conceptual objectives:

C1. Describe important features of

job order production.

10, 11, 12,

13

19-1, 19-14

19-1

19-1, 19–2,

19-4, 19–5,

19-6, 19-7,

19-9

they are used in job order

costing.

19-8

Analytical objectives:

A1 Apply job order costing in

pricing services.

2, 14

19-13

19–18

Procedural objectives:

P1. Describe and record the flow of

materials costs in job order cost

accounting.

5, 6

19-3, 19-4,

19–10

19-4, 19-5,

19-6, 19–7,

19–8, 19-13,

19–19

19-1, 19–2,

19-3, 19-5, SP

GL, ES

19-8

P2. Describe and record the flow of

7

19-3, 19–5,

19–10

19-4, 19–5,

19-6, 19-7,

19-1, 19–2,

19-3, 19-5,

19-8

P3. Describe and record the flow of

overhead costs in job order

costing.

1, 2, 8, 11

19-3, 19-6,

19-7, 19–8,

19–9, 19–10,

19–4, 19-5,

19-6, 19-7,

19-10, 19–11,

19-12, 19-15,

19–16, 19–17

19-1, 19-2,

19-3, 19,-4,

19-5, SP, GL

19-3, 19-8

overapplied and underapplied

factory overhead.

19-13, 19–14,

19–15, 19-16

19-4, 19-5,

GL

*See additional information on next page that pertains to these quick studies, exercises and problems.

SP refers to the Serial Problem

GL refers to the General Ledger Problems

ES refers to Excel Simulations

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

19-2

Additional Information on Related Assignment Material

Connect

Available on the instructor’s course-specific website) repeats all numerical Quick Studies, all Exercises

and Problems Set A. Connect also provides algorithmic versions for Quick Study, Exercises and

Problems. It allows instructors to monitor, promote, and assess student learning. It can be used in

practice, homework, or exam mode.

Connect Insight

The first and only analytics tool of its kind, Connect Insight is a series of visual data displays that are each framed

The Serial Problem (SP) for Success Systems continues in this chapter.

General Ledger

Assignable within Connect, General Ledger (GL) problems offer students the ability to see how transactions post

from the general journal all the way through the financial statements. Critical thinking and analysis components are

added to each GL problem to ensure understanding of the entire process. GL problems are auto-graded and provide

instant feedback to the student.

Excel Simulations

Assignable within Connect, Excel Simulations allow students to practice their Excel skills—such as basic formulas

and formatting—within the context of accounting. These questions feature animated, narrated Help and Show Me

tutorials (when enabled). Excel Simulations are auto-graded and provide instant feedback to the student.

Synopsis of Chapter Revision

NEW opener—Neha Assar and entrepreneurial assignment.

Simplified discussion of cost accounting systems.

Simplified direct material and direct labor cost flows and entries.

Added time period information to graphic on 4-step overhead process.

Simplified discussion of recording overhead costs.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

19-3

Chapter Outline

Notes

I. Job Order Costing

A. Cost accounting system

1. Accumulates manufacturing costs and assigns them to

products and services.

2. Provides timely information about inventories and costs

3. Two basic types of cost accounting systems are job order cost

accounting and process cost accounting.

a.. Job Order Production—producing products or providing

services individually designed to meet the needs of a

specific customer (special orders).

i. The production activities for a customized product is

called a job

ii. A job lot involves producing more than one unit of a

unique product.

b. Process Operations

i. Mass production of products in a continuous flow of

steps.

ii. Designed to mass produce large quantities of identical

products. Covered in Chapter 20.

B. Production Activities in Job Order Costing

an overview of job order production activity and cost flows is

shown in Exhibit 19.2

1. Cost Flows:

a. Because they are product costs, manufacturing costs flow

through inventory accounts (Raw Materials Inventory,

Work in Process Inventory, Finished Goods Inventory)

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

19-4

Chapter Outline

Notes

2. Job Cost Sheet—separate record maintained for each job used

to record costs.

a. Classifies costs as direct materials, direct labor, or

overhead.

b. Used by managers to monitor costs incurred to date and to

predict and control costs to complete each job.

c. Accumulated job costs are kept in the Work in Process

Inventory while goods are being produced.

d. Job cost sheets filed for all of the jobs in process make up

a subsidiary ledger controlled by the Work in Process

II. Materials and Labor Cost Flows

1. Cost Flows and Documents—the three cost components and

documents used to account for them are:

Materials Cost Flows and Documents

a. Receiving report—Source document used to record the

quantity and cost of items received. Materials purchased

are used as a debit to Raw Materials Inventory and a credit

to Accounts Payable.

b. Materials ledger cards (or electronic files)—perpetual

2. Materials Purchases – includes direct and indirect materials.

Updates to individual materials ledger cards. Debit Raw

Materials Inventory to increase.

3. Materials Use (Requisition)

a. Materials Requisition⎯document identifying the type and

quantity of material needed in production. Job number is

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

19-5

Chapter Outline

Notes

4. Labor Cost Flows and Documents

a. Time tickets – used by employees to record hours worked.

Used to determine total labor costs for pay period. They

indicate how much time employees spent on each job and

b. Job Cost Sheets—accumulates the cost of direct labor

(from time tickets and related entry) as these costs are

incurred.

5. Overhead Cost Flows and Reports

a. Overhead costs can’t be traced to individual jobs. The

accounting for overhead follows a 4-step process shown in

Exhibit 19.11. Managers must first estimate total

overhead for the coming period. We can’t wait until the

b. Step 1: Set Predetermined Overhead Rate

i. Requires an estimated of total overhead cost and an

allocation factory such as total direct labor, total labor

hours, or total machine hours.

ii. Predetermined Overhead rate = Estimated overhead

costs divided by estimated activity based

iii. The allocation case should have a cause and effect

relation between the base and the overhead costs.

c. Step 2: Apply Estimated Overhead to Specific Jobs

i. Predetermined overhead rate times actual activity

where the activity is the allocation base such as direct

labor cost, direct labor hours, machine hours.

ii. The entry to record the applied overhead is a debit to

work in process inventory and a credit to factory

overhead.

iii. The overhead is allocated to each job based on the

resource the job used (rate x actual activity).

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

19-6

Chapter Outline

Notes

d. Step 3: Record Actual Overhead costs

i. Actual factory overhead costs include indirect

materials, indirect labor, supplies, utilities, adjusting

entries for depreciation on factory assets, etc.

ii. Indirect materials ledger cards in factory overhead

ledger—accumulates indirect material costs as they

are placed into production. This subsidiary ledger is

iii. Indirect labor card in Factory Overhead Ledger—

accumulates indirect labor costs (from time tickets and

related entry). Entry to record indirect labor costs

debits Factory Overhead and credits Factory Wages

Payable.

e. Step 4: Adjusting Factory Overhead—

i. Factory Overhead T-Account

a) The debit side shows the actual amount of factory

overhead incurred during the period based on bills

received.

b) The credit side shows the amount applied during

the period that was an estimate based on the

predetermined overhead rate.

d) A credit balance in the FOH account indicates

more was applied than incurred; an overapplied

FOH amount.

ii. Underapplied and Overapplied Overhead

a) Factory Overhead debit balance (underapplied

amount) is credited (closed) and debited (charged)

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

19-7

Chapter Outline

Notes

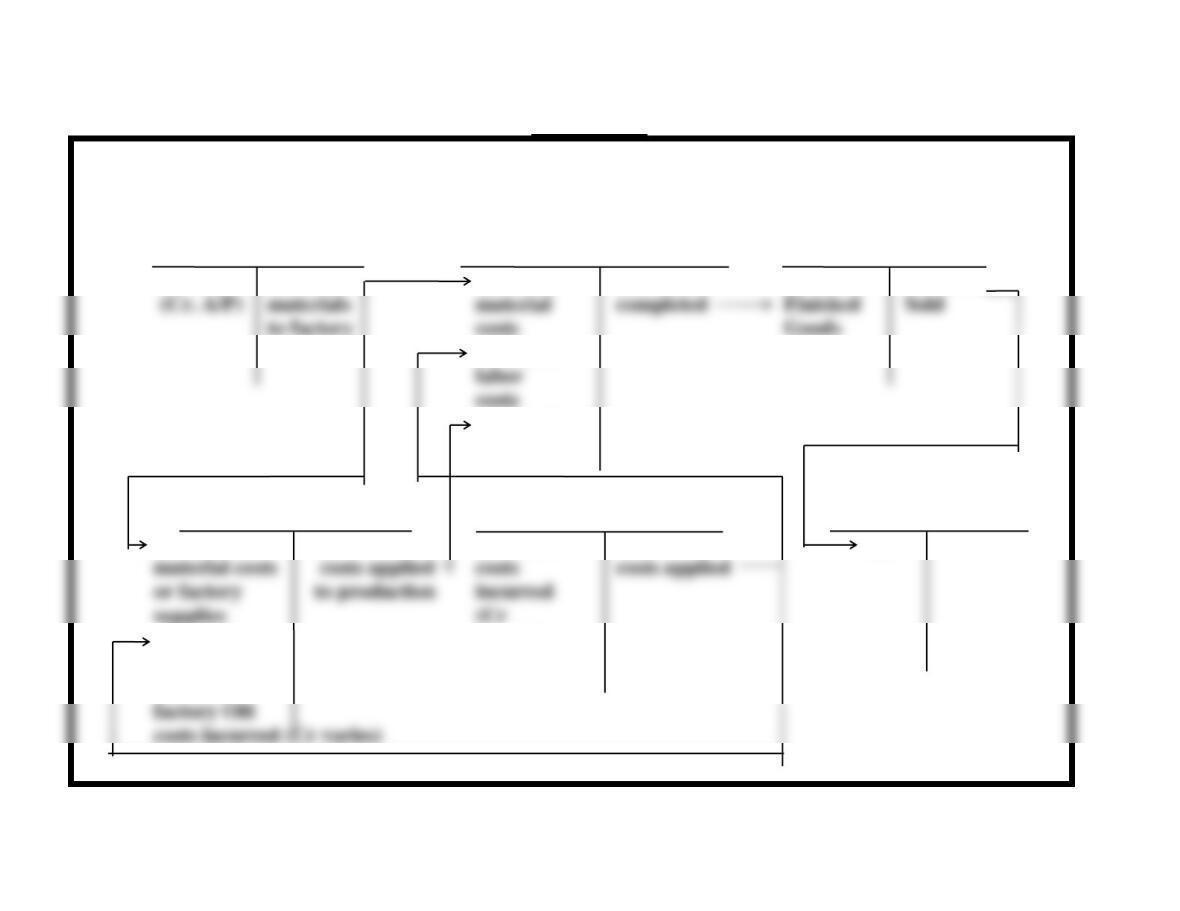

4. Summary of Cost Flows—Summary journal entries are used

to record cost flows as follows:

a. Into (debit) Raw Materials Inventory as acquired.

b. From (credit) Raw Materials Inventory to (debit) Work In

Process Inventory (direct materials) and (debit) Factory

Overhead (indirect materials) as good are requisitioned.

Direct material costs also accumulated on Job Cost Sheets.

f. From (credit) Factory Overhead and into (debit) Work In

Process as overhead costs are applied using overhead rate.

g. From (credit) Work In Process Inventory to (debit)

Finished Goods Inventory as jobs are completed. Full cost

from Job Cost Sheets.

h. From (credit) Finished Goods Inventory to (debit) Cost of

Goods Sold as goods are sold.

3. Combine labor and overhead to obtain cost of job.

III. Decision Analysis—Pricing for Services

A. Service providers also use job order costing.

B. Procedure to determine:

1. Determine direct labor costs

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

19-8

VISUAL #19-1

Tracing Product Costs

Through a Cost Accounting System

Work in Process Finished Goods

Materials Inventory Inventory Inventory

(1) Buy Send (2) (2) Direct (7) Goods (7) Cost of (8) Goods

(4) Direct

(6) Overhead

costs

Factory Overhead Factory Payroll Cost of Goods Sold

(2) Indirect (6) Overhead (3) Labor (4) Labor (8)

(4) Indirect payables)

labor costs

(5) Other

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

19-9

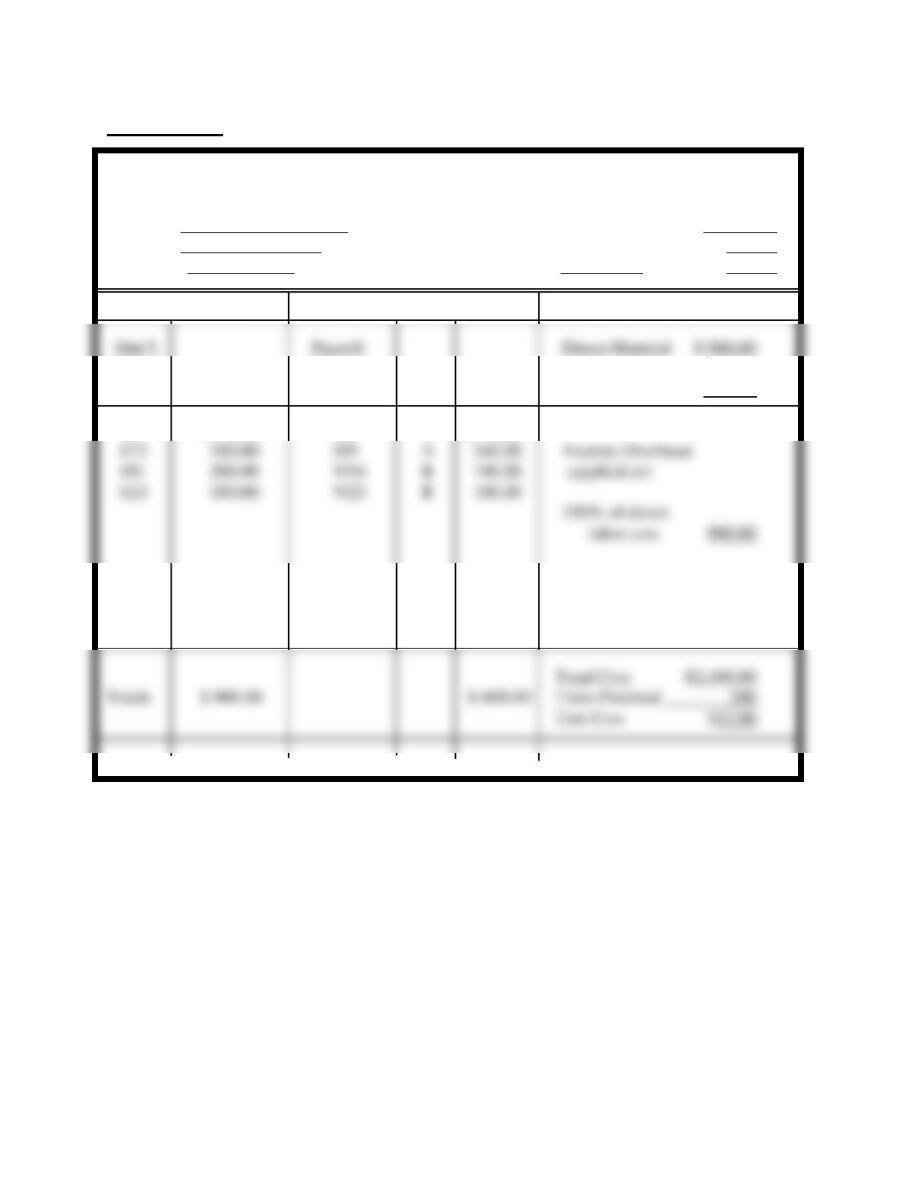

VISUAL #19-2

Job Cost Sheet

Customer Build We Must, Inc. Job No. 114

Product Bracket-H3 Date Promised 10/1

Quantity 200 Dates: Started 9/1 Completed 9/20

Direct Material Direct Labor Cost Summary

Req’n. Summary

No. Amount Dated Dept. Amount Direct Labor 600.00

667 $ 340.00 9/2 A $ 70.00

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

19-10

Chapter 19 Alternate Demo Problem

The following information is the Work in Process and Factory Overhead

Accounts for Superior Company:

Work in Process Inventory

Beg Inv. 302,000

Direct Materials 280,000

Factory Overhead

Required:

1. Prepare a manufacturing statement for Superior Company for 2017.

Finished Goods Inv. 548,000

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

19-11

Chapter 19 Solution: Alternate Demo Problem

SUPERIOR MANUFACTURING COMPANY

Manufacturing Statement

For Year Ended December 31, 2017

Direct materials used …………………………………….

$280,000

Adjusting entry for under or over-applied overhead

Factory Overhead

Actual Overhead 98,000

96,000 Applied Overhead

Under applied 2,000

Total manufacturing costs …………………………….

Work in Process Inventory 1/1/17……………….

Total goods in process during the year ………….