Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Exercise 19–6

Requirement 1

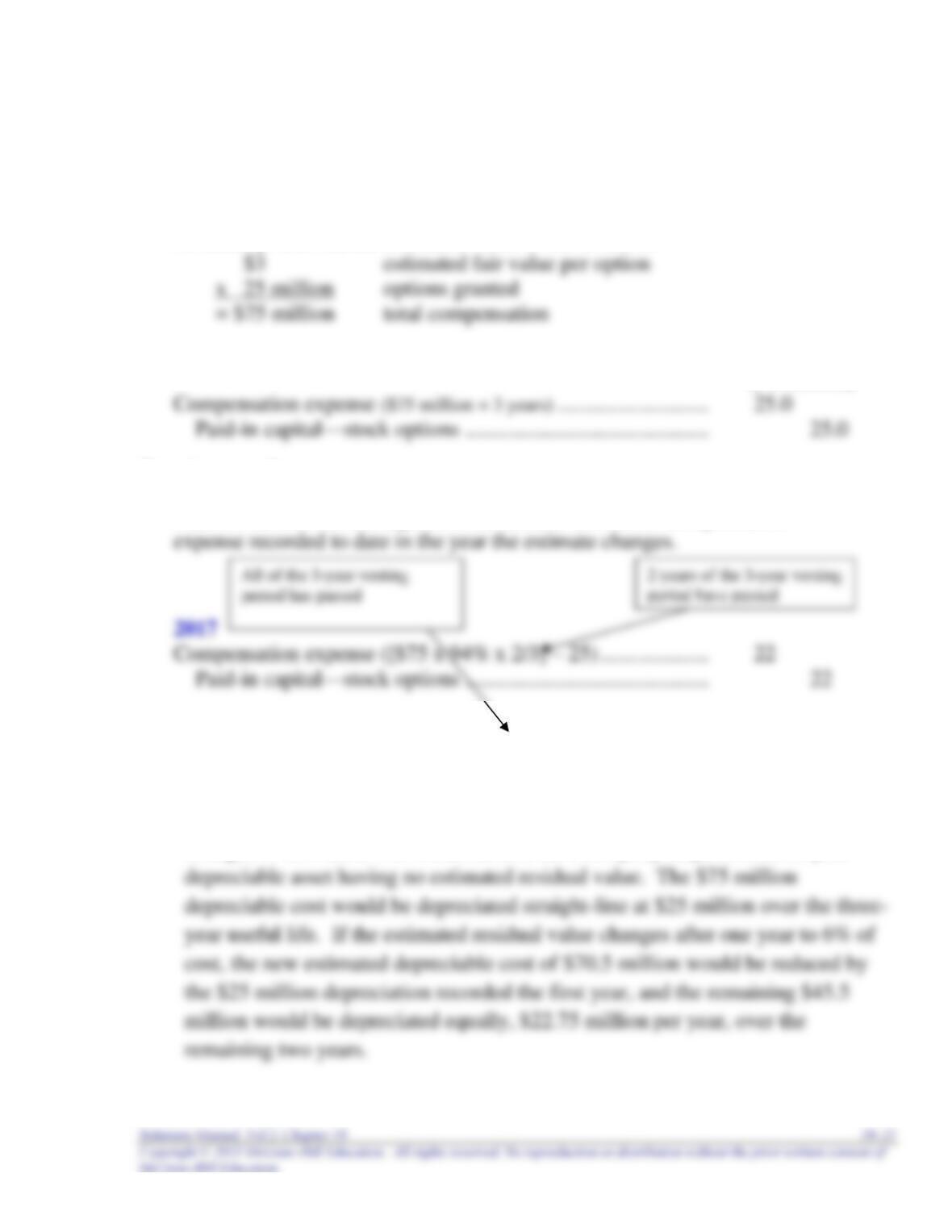

At January 1, 2016, the estimated value of the award is:

Requirement 2

($ in millions)

Requirement 3

Adams-Meneke should adjust the cumulative amount of compensation

2018

Compensation expense ([$75 x 94% x 3/3] – 25 – 22) ............ 23.5

Paid-in capital—stock options ............................................. 23.5

Note that this approach is contrary to the usual way companies account for

changes in estimates. For instance, assume a company acquires a three-year

19–22 Intermediate Accounting, 8/e

Exercise 19–7

Requirement 1

At January 1, 2016, the estimated value of the award is:

= $40 million fair value of award

Requirement 2

($ in millions)

Compensation expense ($40 million ÷ 2 years) ... 20

Requirement 3

Requirement 4

Cash ($8 exercise price x 30 million shares) ........................ 240

Paid-in capital—stock options

Requirement 5

Paid-in capital—stock options ($40 – 30 million) ........... 10

Paid-in capital—expiration of stock options .......... 10

Exercise 19–8

Requirement 1

At January 1, 2016, the total compensation is measured as:

Requirement 2

December 31, 2016, 2017, 2018

($ in millions)

Requirement 3

Cash ($11 exercise price x 12 million shares) ...................... 132

Paid-in capital—stock options ($12 million x 3 years) .... 36

Exercise 19–9

Cash ($12 x 50,000 x 85%) 510,000

Exercise 19–10

(amounts in thousands, except per share amount)

net Earnings

income Per Share

$655 $655

Exercise 19–11

1. EPS in 2016

(amounts in thousands, except per share amount)

net Earnings

2. EPS in 2017

(amounts in thousands, except per share amount)

net Earnings

3. 2016 EPS in the 2017 comparative financial statements

(amounts in thousands, except per share amount)

net Earnings

19–26 Intermediate Accounting, 8/e

Exercise 19–12

(amounts in thousands, except per share amount)

net preferred Earnings

Exercise 19–13

(amounts in thousands, except per share amount)

net preferred Net Loss

19.5% x $800* = $76

Exercise 19–14

(amounts in millions, except per share amount)

net preferred Earnings

income dividends Per Share

$150 – $27* $123

Exercise 19–15

(amounts in millions, except per share amount)

Basic EPS

net preferred

income dividends

$150 – $27* $123

Diluted EPS

net preferred

income dividends

$150 – $27 $123

**Purchase of treasury stock

30 million shares

Exercise 19–16

(amounts in millions, except per share amount)

Basic EPS

net preferred

income dividends

$150 – $27* $123

Diluted EPS

net preferred

income dividends

$150 – $27 $123

**Purchase of treasury stock

30 million shares

x $56 (exercise price)

$1,680 million

÷ $70 (average market price)

24 million shares

19–30 Intermediate Accounting, 8/e

Exercise 19–17

(amounts in millions, except per share amount)

Basic EPS

net preferred

income dividends

Diluted EPS

net preferred after-tax

income dividends interest savings

$150 – $27 + $5* – 40% ($5**) $126

———————————————————————————— = — = $.62

200 (1.05) – 24 (10/12) (1.05) + 4 (3/12) + (30 – 24***) + 6 202

shares treasury new assumed exercise conversion

Exercise 19–18

(amounts in thousands, except per share amount)

Basic EPS

Diluted EPS

net

income

$720 $720

————————————————————— = —— = $8.09

80 + 15 (4/12) + (24 – 20*) 89

shares new assumed exercise

at Jan. 1 shares of options

*Purchase of treasury shares

Exercise 19–19

(amounts in thousands, except per share amounts)

Basic EPS

Diluted EPS

net preferred preferred after-tax

income dividends dividends interest savings

Order of Entry:

Note that we included in our calculation, the convertible security with the lowest

“incremental effect” ($60 ÷ 32 = $1.87) before the one with the higher effect ($60 ÷

30 = $2.00).

After including the conversion of the preferred stock only, EPS is $500 ÷ 132 = $3.79.

Exercise 19–20

(amounts in thousands, except per share amounts)

Basic EPS

Diluted EPS

net Earnings

income Per Share

$120 $120

—————————— = ——— = $.14

800 + (54 – 18*) 836

shares shares

at Jan. 1 assumed vested

Proceeds:

$270,000 ($5 market price per share x 54,000 shares)

*Assumed purchase of treasury shares

$90,000 proceeds

÷ $5 (average market price)

18,000 shares

Note: The proceeds also must be increased (or decreased) by any tax benefits that

19–34 Intermediate Accounting, 8/e

Exercise 19–21

Requirement 1

$5 fair value per share

x 18 million shares granted

= $90 million fair value of award

The $90 million total compensation is expensed equally over the three-year vesting

period, reducing earnings by $30 million each year.

Requirement 2

The total compensation for the award is $90 million ($5 market price per share x 18

million shares). Because the stock award vests over three years, it is expensed as $30

million each year for three years. At the end of 2016, the second year, $60 million

Exercise 19–22

(amounts in millions, except per share amounts)

Basic EPS

Diluted EPS

net

income

$148 $148

Exercise 19–23

(amounts in thousands, except per share amounts)

Basic EPS

Diluted EPS

net

income

$2,000 $2,000

Exercise 19–24

List A List B

__e_ 1. Subtract preferred dividends. a. Options exercised.

__m_ 2. Time-weighted by 5/12. b. Simple capital structure.

__a_ 3. Time-weighted shares assumed issued c. Basic EPS.

Exercise 19–25

Requirement 1

The FASB Accounting Standards Codification represents the single source of

Requirement 2

Section 718–10–50–2c states that companies must disclose:

For the most recent year for which an income statement is provided, both of the

following:

1. The number and weighted-average exercise prices (or conversion ratios) for

each of the following groups of share options:

1. Those outstanding at the beginning of the year

Exercise 19–26

The FASB Accounting Standards Codification represents the single source of

authoritative U.S. generally accepted accounting principles. The specific citation for

each of the following items is:

1. Stock options:

2. The measurement date for share-based payments classified as liabilities:

3. The formula to calculate diluted earnings per share.

4. The way stock dividends or stock splits in the current year affect the

19–40 Intermediate Accounting, 8/e

Exercise 19–27

Requirement 1

The SARs are considered to be equity because IE will settle in shares of IE

stock at exercise.

January 1, 2016

No entry

Calculate total compensation expense:

Requirement 2

December 31, 2016, 2017, 2018, 2019 ($ in millions)

Compensation expense ($72 million ÷ 4 years) 18

Paid-in capital—SAR plan 18

Requirement 3

Requirement 4

June 6, 2021