18-38

18-39

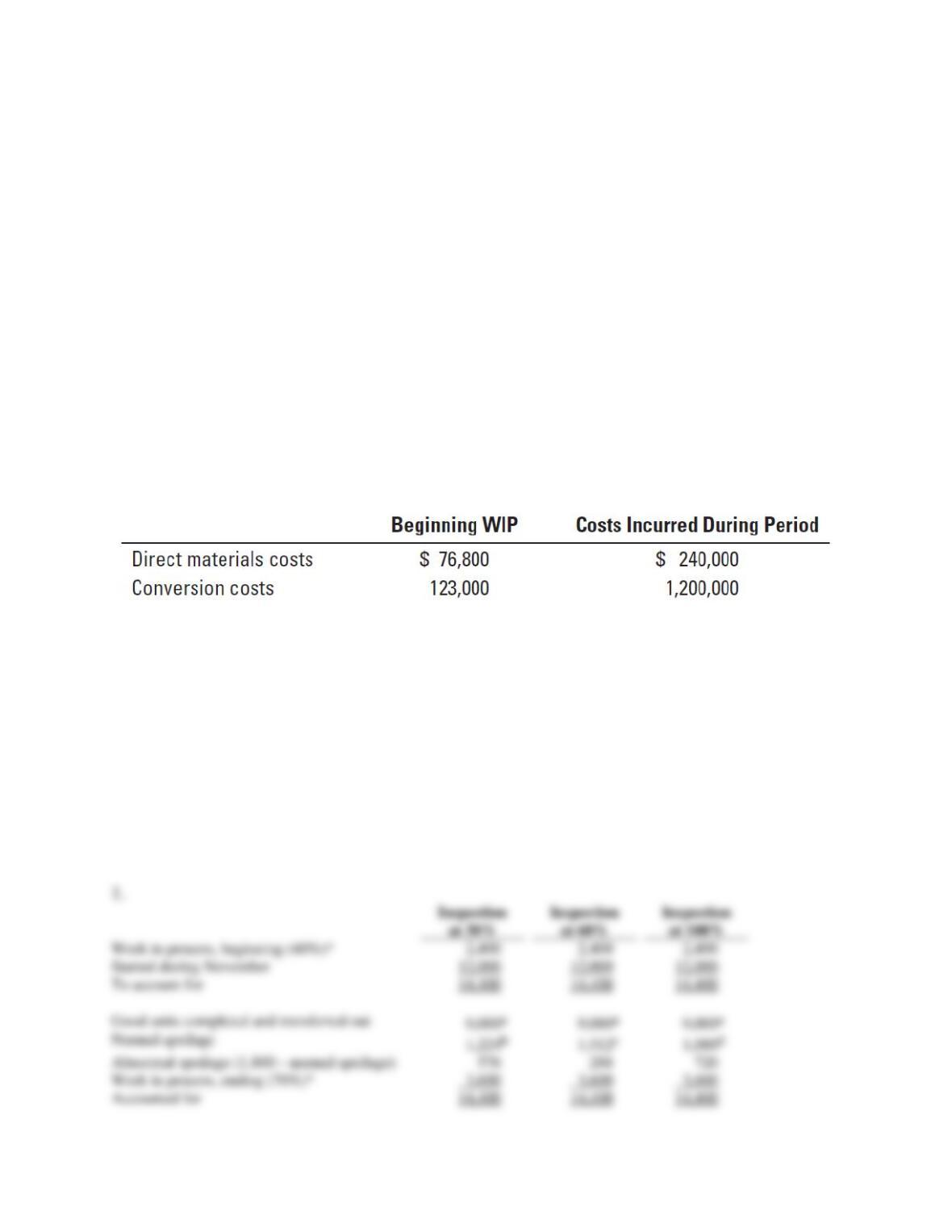

18-35 (30 min.) Physical units, inspection at various levels of completion, weighted–

average process costing.

SunEnergy produces solar panels. A key step in the conversion of raw silicon to a completed

solar panel occurs in the assembly department, where lightweight photovoltaic cells are

assembled into modules and connected on a frame. In this department, materials are added at the

beginning of the process and conversion takes place uniformly.

At the start of November 2014, SunEnergy’s assembly department had 2,400 panels in

beginning work in process, which were 100% complete for materials and 40% complete for

conversion costs. An additional 12,000 units were started in the department in November, and

3,600 units remain in work in process at the end of the month. These unfinished units are 100%

complete for materials and 70% complete for conversion costs.

The assembly department had 1,800 spoiled units in November. Because of the difficulty of

keeping moisture out of the modules and sealing the photovoltaic cells between layers of glass,

normal spoilage is approximately 12% of good units. The department’s costs for the month of

November are as follows:

Required:

1. Using the format on page 715, compute the normal and abnormal spoilage in units for

November, assuming the inspection point is at (a) the 30% stage of completion, (b) the 60%

stage of completion, and (c) the 100% stage of completion.

2. Refer to your answer in requirement 1. Why are there different amounts of normal and

abnormal spoilage at different inspection points?

3. Now assume that the assembly department inspects at the 60% stage of completion. Using

the weighted-average method, calculate the cost of units transferred out, the cost of abnormal

spoilage, and the cost of ending inventory for the assembly department in November.

SOLUTION

18-40

18-41

SOLUTION EXHIBIT 18-35

18-42

18-43

18-36 (15 min.) Spoilage in job costing.

Jellyfish Machine Shop is a manufacturer of motorized carts for vacation resorts.

Patrick Cullin, the plant manager of Jellyfish, obtains the following information for Job #10

in August 2014. A total of 46 units were started, and 6 spoiled units were detected and rejected at

final inspection, yielding 40 good units. The spoiled units were considered to be normal spoilage.

Costs assigned prior to the inspection point are $1,100 per unit. The current disposal price of the

spoiled units is $235 per unit. When the spoilage is detected, the spoiled goods are inventoried at

$235 per unit.

Required:

1. What is the normal spoilage rate?

2. Prepare the journal entries to record the normal spoilage, assuming the following:

a. The spoilage is related to a specific job.

b. The spoilage is common to all jobs.

c. The spoilage is considered to be abnormal spoilage.

SOLUTION

18-44

18-37 (10 min.) Rework in job costing, journal entry (continuation of 18-36).

Assume that the 6 spoiled units of Jellyfish Machine Shop’s Job #10 can be reworked for a total

cost of $1,800. A total cost of $6,600 associated with these units has already been assigned to

Job #10 before the rework.

Required:

Prepare the journal entries for the rework, assuming the following:

a. The rework is related to a specific job.

b. The rework is common to all jobs.

c. The rework is considered to be abnormal.

SOLUTION

18-45

18-38 (10 min.) Scrap at time of sale or at time of production, journal entries

(continuation of 18-36).

Assume that Job #10 of Jellyfish Machine Shop generates normal scrap with a total sales value

of $700 (it is assumed that the scrap returned to the storeroom is sold quickly).

Required:

Prepare the journal entries for the recognition of scrap, assuming the following:

a. The value of scrap is immaterial and scrap is recognized at the time of sale.

b. The value of scrap is material, is related to a specific job, and is recognized at the time of

sale.

c. The value of scrap is material, is common to all jobs, and is recognized at the time of sale.

d. The value of scrap is material, and scrap is recognized as inventory at the time of production

and is recorded at its net realizable value.

SOLUTION

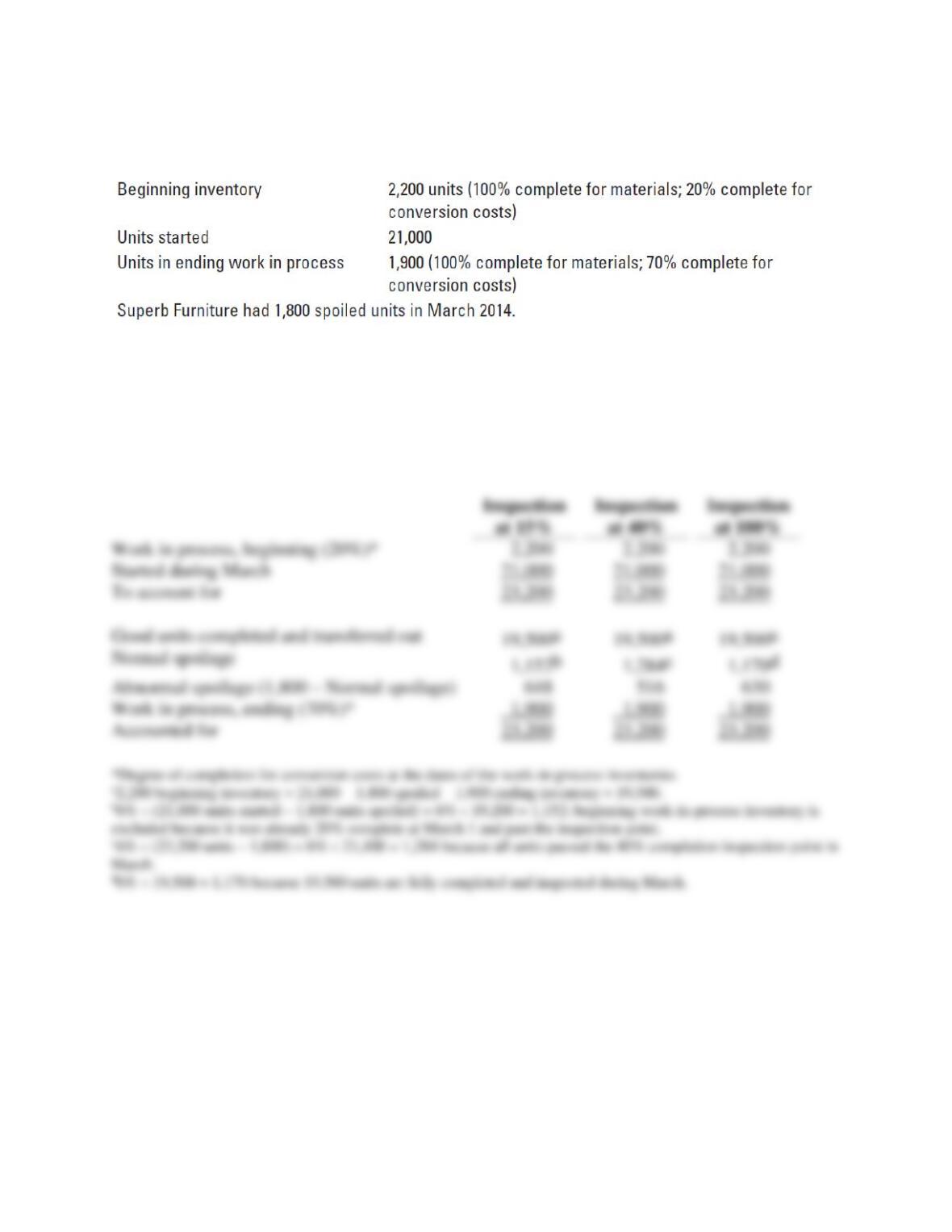

18-39 (20−25 min.) Physical units, inspection at various stages of completion (chapter

appendix).

Superb Furniture manufactures plastic lawn furniture in a continuous process. The company

pours molten plastic into molds and then cools the plastic. Materials are added at the beginning

of the process, and conversion is considered uniform through the period. Occasionally, the

plastic does not completely fill a mold because of air pockets, and the chair is then considered

18-46

spoiled. Normal spoilage is 6% of the good units that pass inspection. The following information

pertains to March 2014:

Required:

Using the format on page 715, compute the normal and abnormal spoilage in units, assuming the

inspection point is at (a) the 15% stage of completion, (b) the 40% stage of completion, and (c)

the 100% stage of completion.

SOLUTION

18-47

18-40 (20 min.) Job costing, rework.

Avid Corporation manufactures a sophisticated controller that is compatible with a variety of

gaming consoles. Excluding rework costs, the cost of manufacturing one controller is $220. This

consists of $120 in direct materials, $24 in direct manufacturing labor, and $76 in manufacturing

overhead. Maintaining a reputation for quality is critical to Avid. Any defective units identified

at the inspection point are sent back for rework. It costs Avid $72 to rework each defective

controller, including $24 in direct materials, $18 in direct manufacturing labor, and $30 in

manufacturing overhead.

In August 2014, Avid manufactured 1,000 controllers, 80 of which required rework. Of these

80 controllers, 50 were considered normal rework common to all jobs and the other 30 were

considered abnormal rework.

Required:

1. Prepare journal entries to record the accounting for both the normal and abnormal rework.

2. What were the total rework costs of controllers in August 2014?

3. Suppose instead that the normal rework is attributable entirely to Job #9, for 200 controllers

intended for Australia. In this case, what are the total and unit costs of the good units

produced for that job in August 2014? Prepare journal entries for the manufacture of the 200

controllers, as well as the normal rework costs.

SOLUTION

18-48

18-49

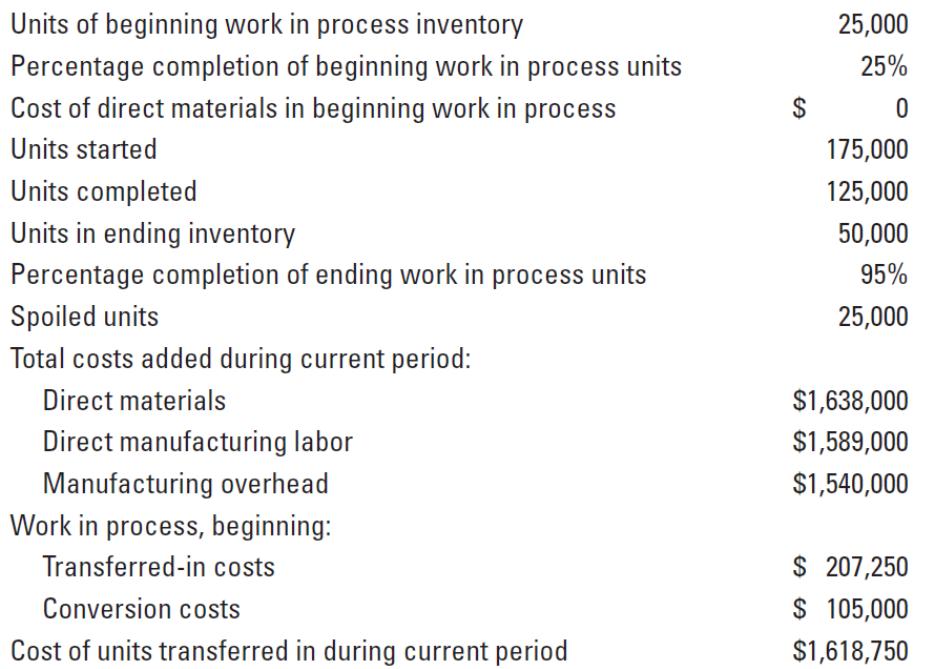

18-41 (45 min.) Weighted-average method, inspection at 80% completion.

(A. Atkinson) The Horsheim Company is a furniture manufacturer with two departments:

molding and finishing. The company uses the weighted-average method of process costing. In

August, the following data were recorded for the finishing department:

Conversion costs are added evenly during the process. Direct material costs are added when

production is 90% complete. The inspection point is at the 80% stage of production. Normal

spoilage is 10% of all good units that pass inspection. Spoiled units are disposed of at zero net

disposal value.

Required:

1. For August, summarize total costs to account for and assign these costs to units completed

and transferred out (including normal spoilage), to abnormal spoilage, and to units in ending

work in process.

2. What are the managerial issues involved in determining the percentage of spoilage

considered normal? How would your answer to requirement 1 differ if all spoilage were

treated as normal?

18-50

SOLUTION

18-51

SOLUTION EXHIBIT 18-41

18-52

18-53