Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

PROBLEM 18.8A

WILSON DYNAMICS (continued)

b.

(1)

4,000

72,000

(2) Forging Direct

Materials Materials Conversion

Forging materials

(4,000 units require 0% to complete) 0

Direct materials

(4,000 units require 100% to complete) 4,000

Conversion

(4,000 units require 75% to complete) 3,000

(3) Forging Direct Conversion

Materials Materials Costs

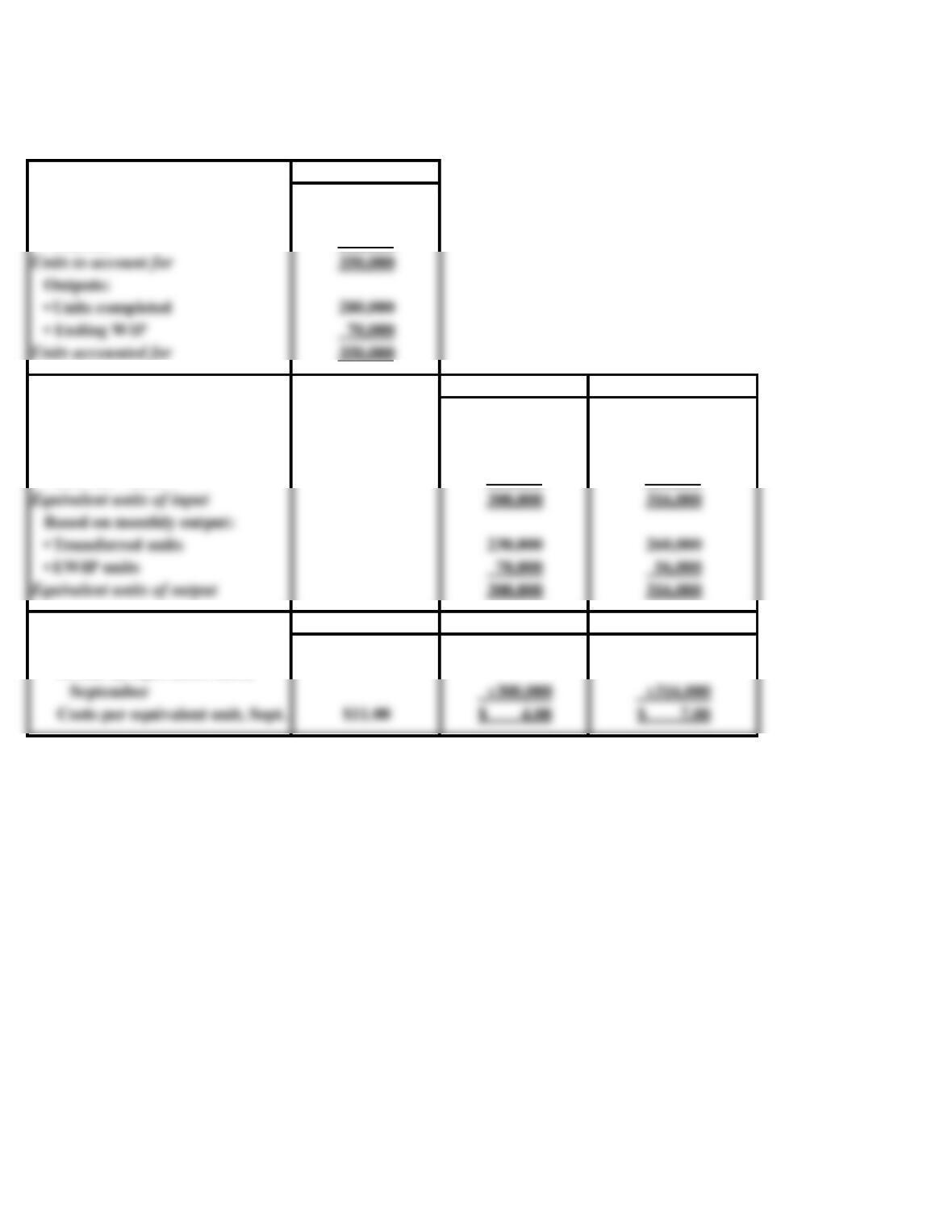

Costs charged to Assembly Department in July*

Cost per equivalent unit in July

Requirements for the Assembly Dept. in July

To finish units in process on July 1:

Input resources

Flow of physical units: Assembly Department

Units in beginning inventory, July 1

Units started in July [see part a (1 )]

PROBLEM 18.8A

WILSON DYNAMICS (concluded)

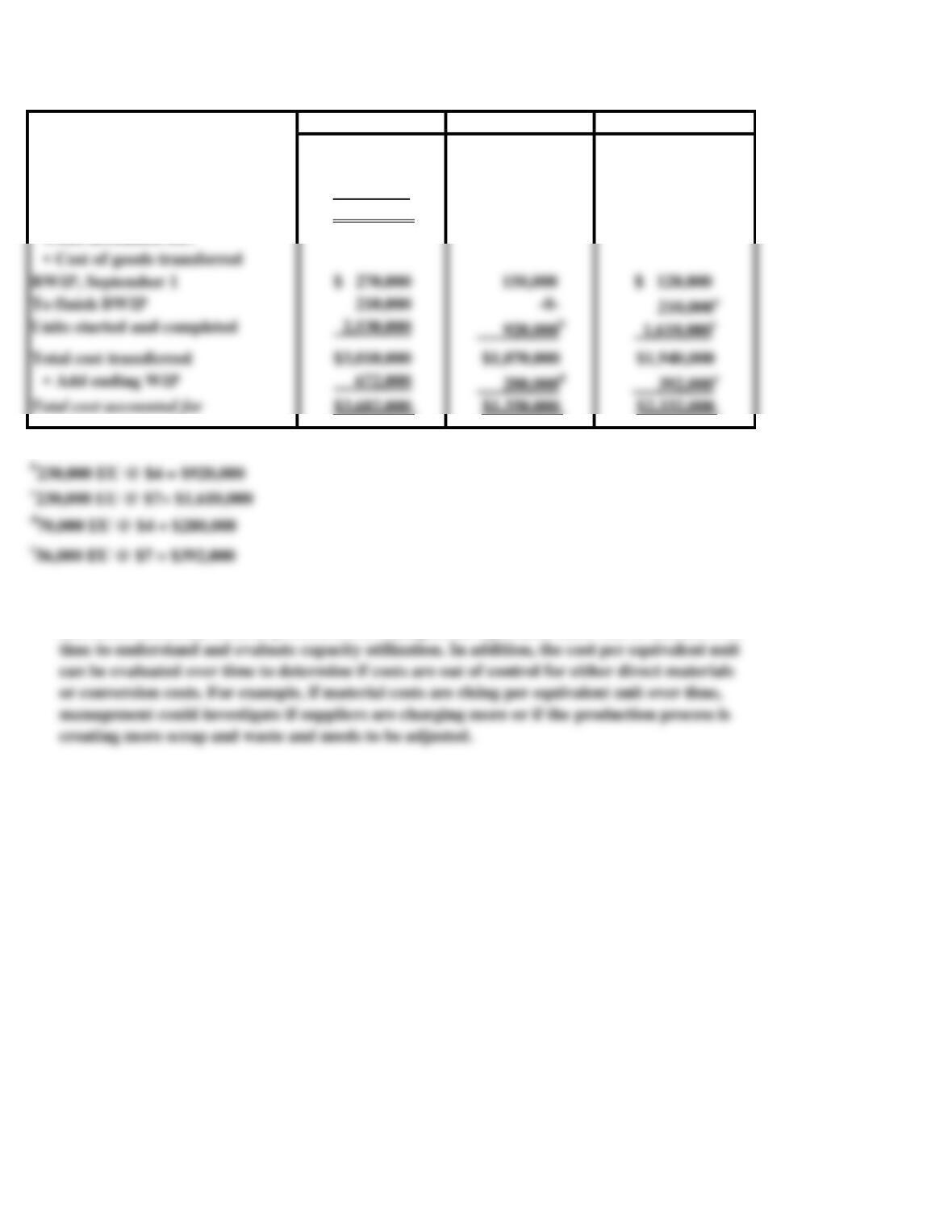

(4) 1,920,000

Work in Process: Assembly 1,920,000

71,000

(5)

272,000$

Finished Goods Inventory

To record the transfer of 60,000 units to the Finished Goods

Inventory in July:

Beginning inventory, July 1 ($68,000 + $3,000)

Work in Process: Finishing Department, July 31

Forging materials (16,000 equivalent units × $17)

SOLUTIONS TO PROBLEMS SET B

20 Minutes, Easy

PROBLEM 18.1B

STREET SMARTS

a.

5,000

(1,000)

4,000

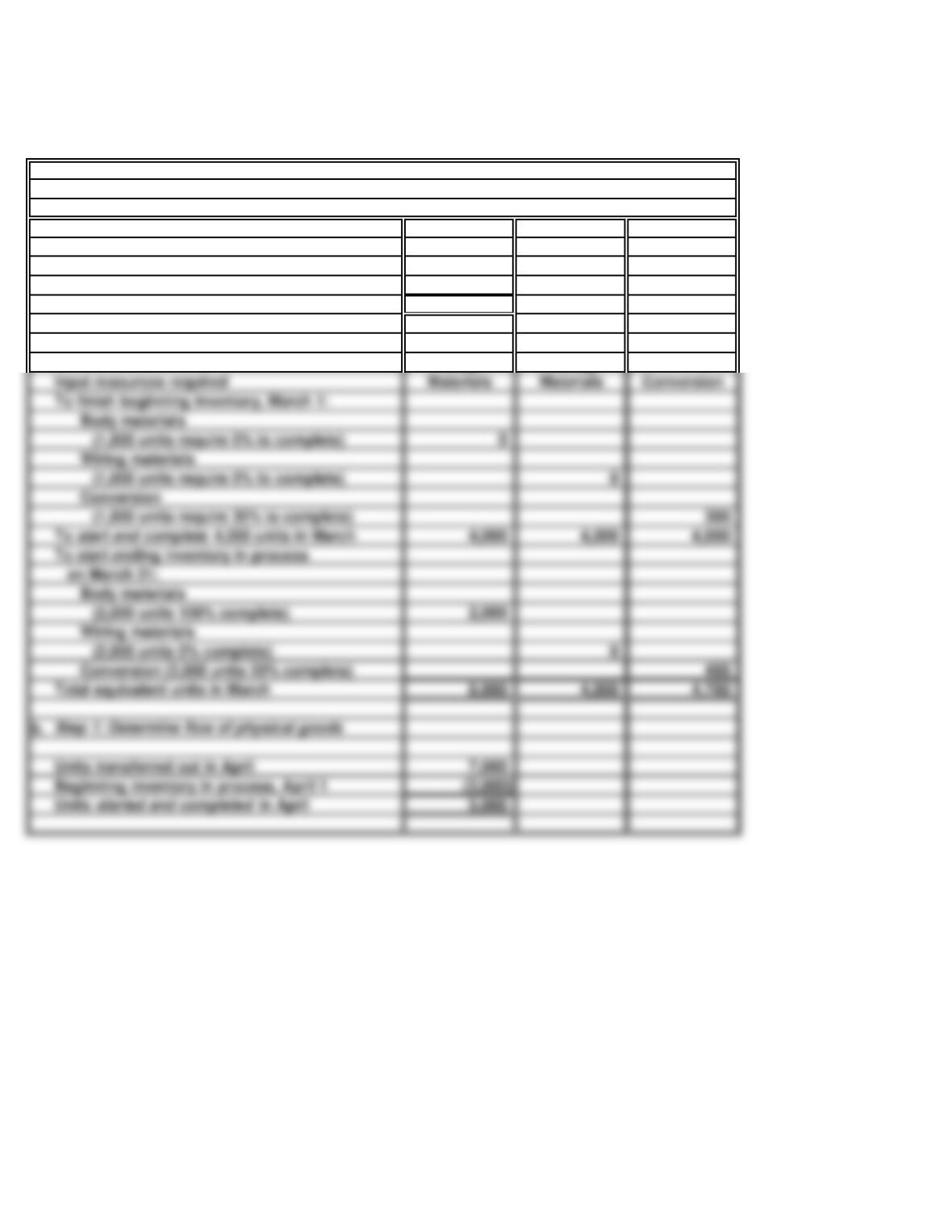

Body Wiring

Step 1: Determine flow of physical goods

Units transferred out in March

Beginning inventory in process, March 1

Units started and completed in March

Step 2: Determine equivalent units

PROBLEM 18.1B

STREET SMARTS (concluded)

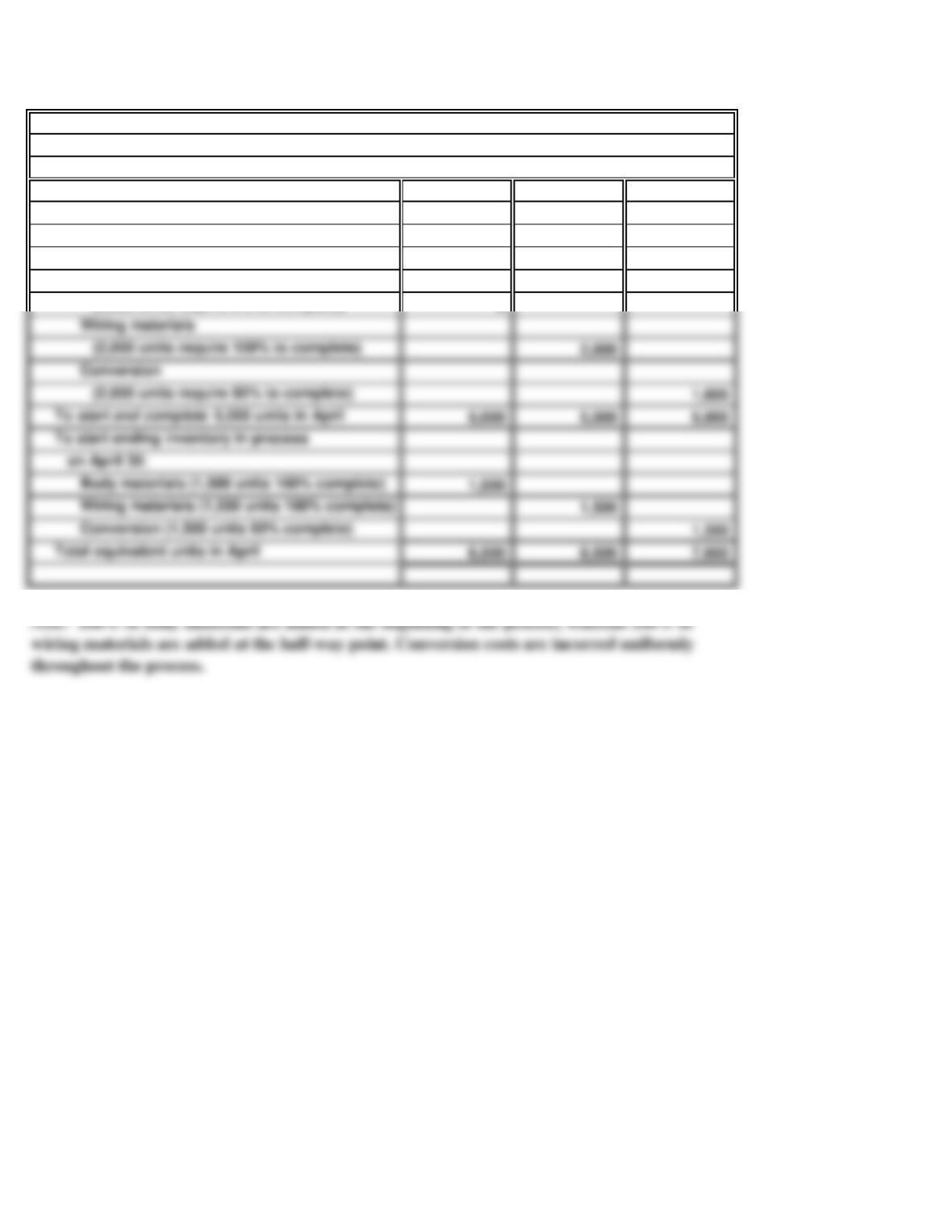

Body Wiring

Materials Materials Conversion

Body materials

(2,000 units require 0% to complete) 0

Step 2: Determine equivalent units consumed

Input resources required

To finish beginning inventory, April 1:

20 Minutes, Easy

PROBLEM 18.2B

MOWTOWN MANUFACTURING

a. (1)

b.

In evaluating the overall efficiency of the Engine Department, management would look at

$50 [($180,000 + $30,000 + $90,000) ÷ 6,000 units]

30 Minutes, Medium PROBLEM 18.3B

MOWTOWN MANUFACTURING

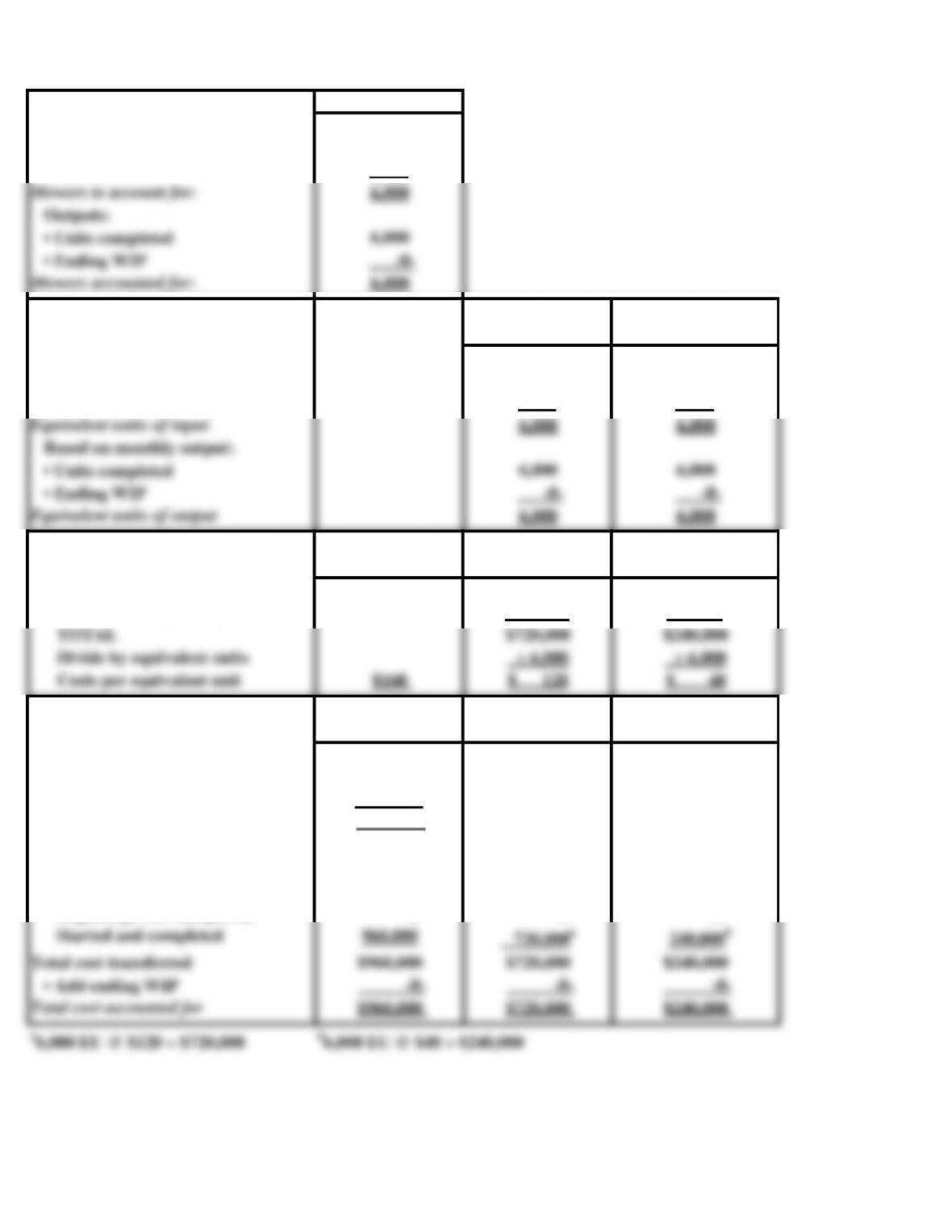

Part I. Physical Flow Total Units

Inputs:

• Beginning WIP -0-

• Started 6,000

Part II. Equivalent Units Direct Materials Conversion Costs

Based on monthly input:

• Beginning WIP -0- -0-

• Units started 6,000 6,000

Part III. Cost per Equivalent Unit Total Unit Cost Direct Materials Conversion Costs

Costs from Deck Department $180,000 $120,000

Costs from Engine Dept. 540,000 120,000

Part IV. Total Cost Assignment Total Costs Direct Materials Conversion Costs

Costs to account for:

• Cost of beginning WIP $ -0-

• Cost added during the period 960,000

Total cost to account for $960,000

Costs accounted for:

• Cost of goods transferred

Beginning WIP last period $ -0- $ -0- $ -0-

Beginning WIP this period -0- -0- -0-

PROBLEM 18.4B

SNACK HAPPY

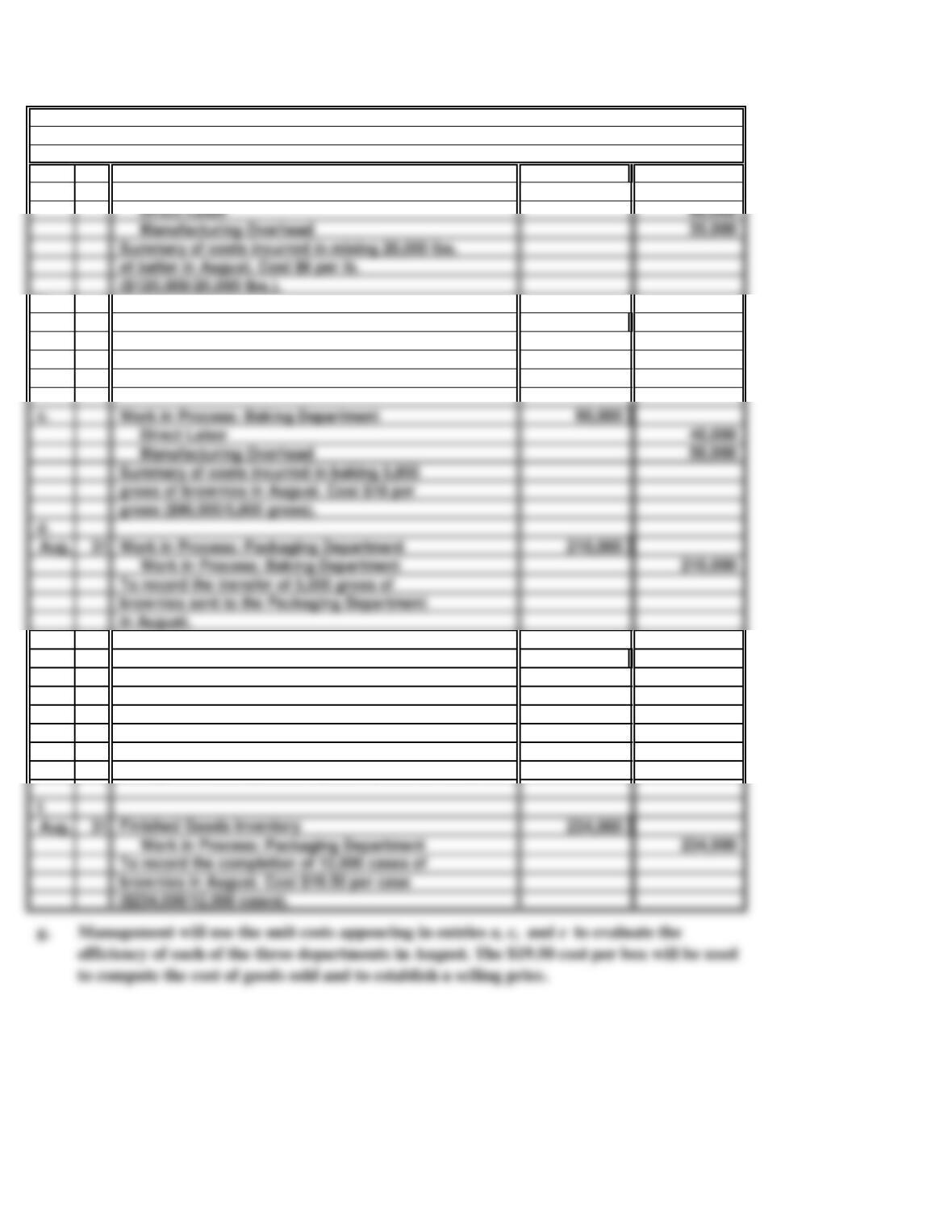

a. 120,000

Materials Inventory 25,000

b.

Aug. 31 120,000

Work in Process: Mixing Department 120,000

e. 24,000

Materials Inventory 3,000

Direct Labor 14,000

Manufacturing Overhead 7,000

30 Minutes, Medium

Work in Process: Mixing Department

Work in Process: Baking Department

To record the transfer of 20,000 pounds

of batter to the Baking Department in August.

To summarize the Packaging Department’s

costs in packaging 12,000 cases of brownies

in August. Cost $2 per case ($24,000/12,000 cases).

Work in Process: Packaging Department

35 Minutes, Medium

PROBLEM 18.5B

BALFANZ COMPANY

a.

Direct

Materials Conversion

b.

Direct Conversion

Materials Costs

Input resources required

*280,000 units transferred - 50,000 units in beginning inventory = 230,000 units started and

completed.

35 Minutes, Medium PROBLEM 18.6B

BALFANZ COMPANY

a. Production Cost Report

Part I. Physical Flow Total Units

Inputs:

• Beginning WIP 50,000

• Started 300,000

Part II. Equivalent Units Direct Materials Conversion

Consumed

Based on monthly input:

• Finish BWIP -0- 30,000

• Start new units 300,000 286,000

Part III. Cost Per Equivalent Unit Total Unit Cost Direct Materials Conversion Costs

Input costs in September $1,200,000 $2,212,000

Divide by equivalent units,

Finishing Department, Month of September

PROBLEM 18.6B

BALFANZ COMPANY (concluded)

Total Costs Direct Materials Conversion Costs

$ 270,000

3,412,000

$3,682,000

b.

Costs accounted for:

Total cost to account for

Part IV. Total Cost Assignment

Costs to account for:

• Cost of beginning WIP

• Cost added during the period

Management can compare production cost reports from month to month to help control costs

and assess efficiency of their processes. For example, the equivalent units can be tracked over

a30,000 EU @ $7 = $210,000

50 Minutes, Strong

PROBLEM 18.7B

DELRAY INDUSTRIES

a.

(1)

3,000

(2) Direct

Materials Conversion

900

1,800

(3) Direct Conversion

Materials Costs

912,600$ 612,000$

÷ 50,700 ÷ 51,000

18$ 12$

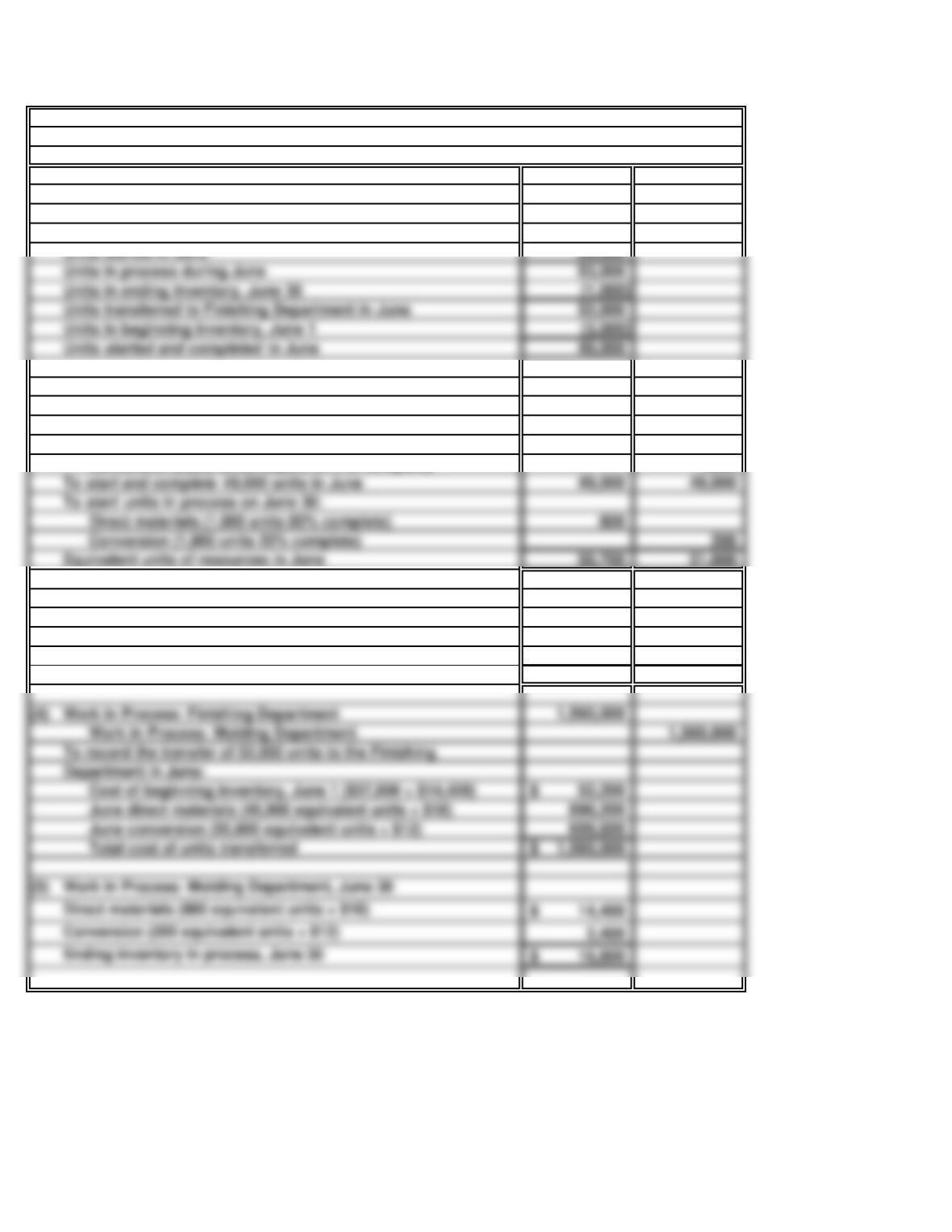

Requirements for the Molding Department in June

Flow of physical units: Molding Department

Units in beginning inventory, June 1

Cost per equivalent unit consumed in June

Input resources

To finish units in process on June 1:

Direct materials (3,000 units require 30% to complete)

Conversion (3,000 units require 60% to complete)

Cost per equivalent unit in June

Costs incurred by Molding Department in June

Equivalent units in June [see part (2) ]

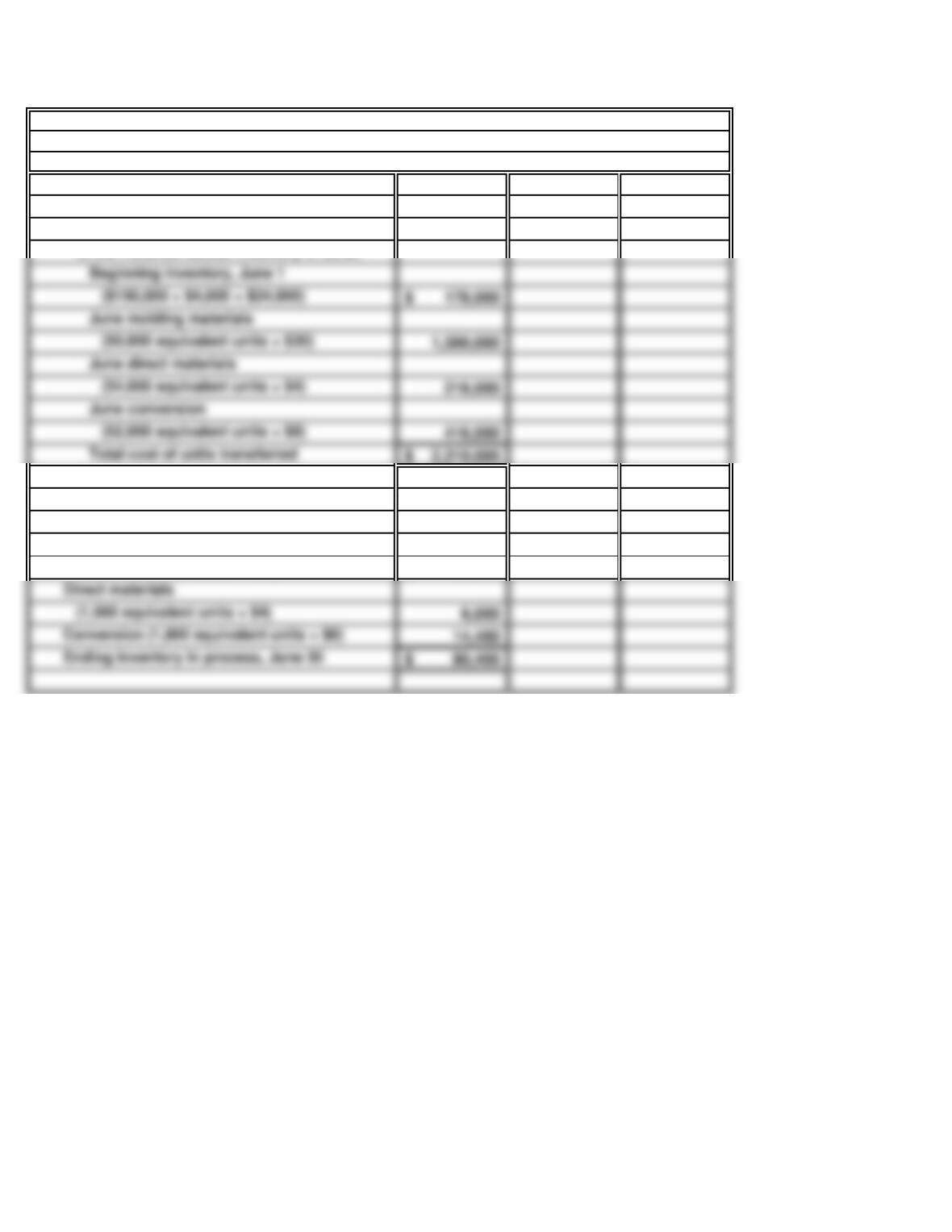

PROBLEM 18.7B

DELRAY INDUSTRIES (continued)

b.

(1)

5,000

52,000

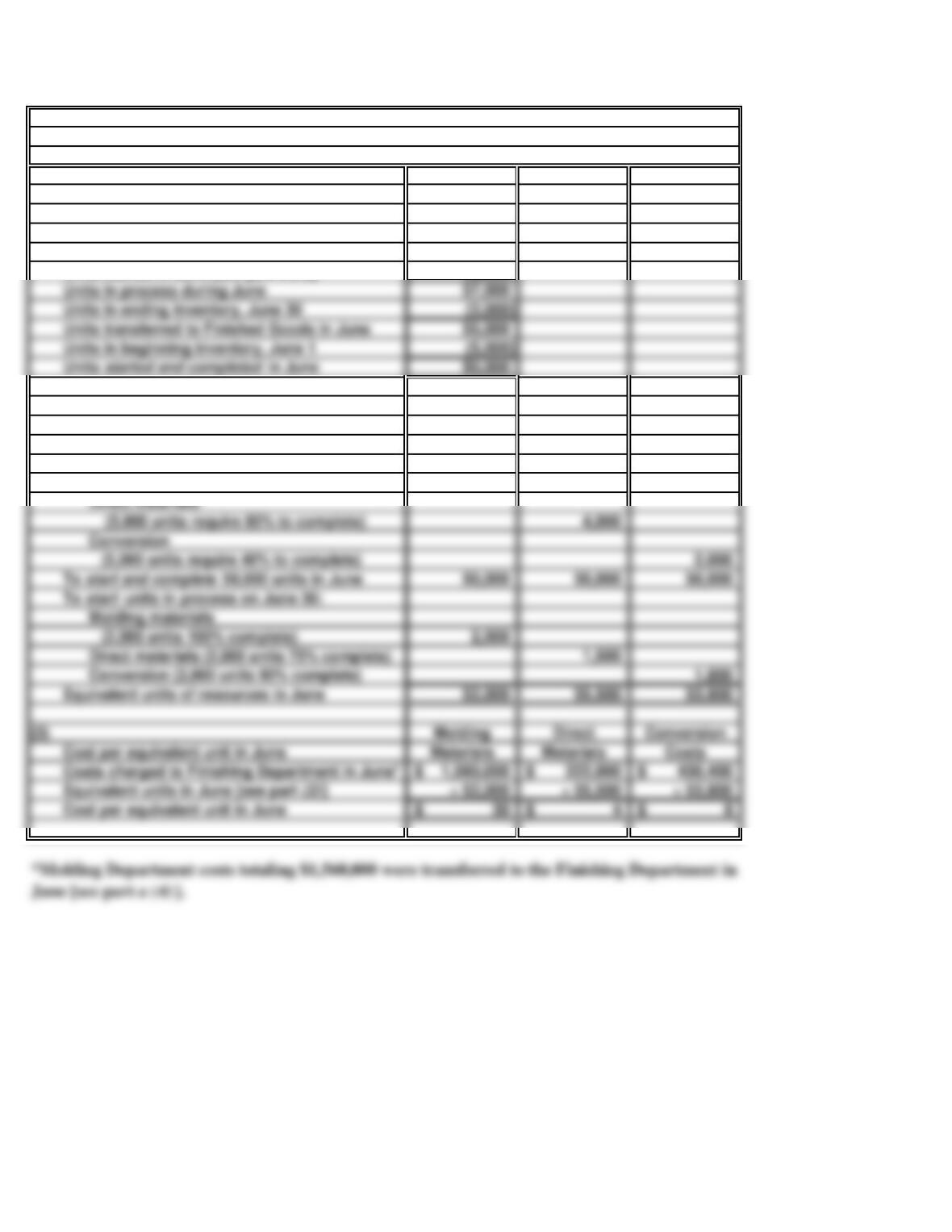

(2) Molding Direct

Materials Materials Conversion

Molding materials

(5,000 units require 0% to complete) 0

To finish units in process on June 1:

Input resources

Units in beginning inventory, June 1

Requirements for the Finishing Dept.

Flow of physical units: Finishing Dept.

in June

Units started in June [see part a (1) ]

PROBLEM 18.7B

DELRAY INDUSTRIES (concluded)

(4) 2,310,000

Work in Process: Finishing Department 2,310,000

(5)

60,000$

Finished Goods Inventory

To record the transfer of 55,000 units

Work in Process: Finishing Department,

Molding materials

to the Finished Goods Inventory in June:

June 30

(2,000 equivalent units × $30)

50 Minutes, Strong

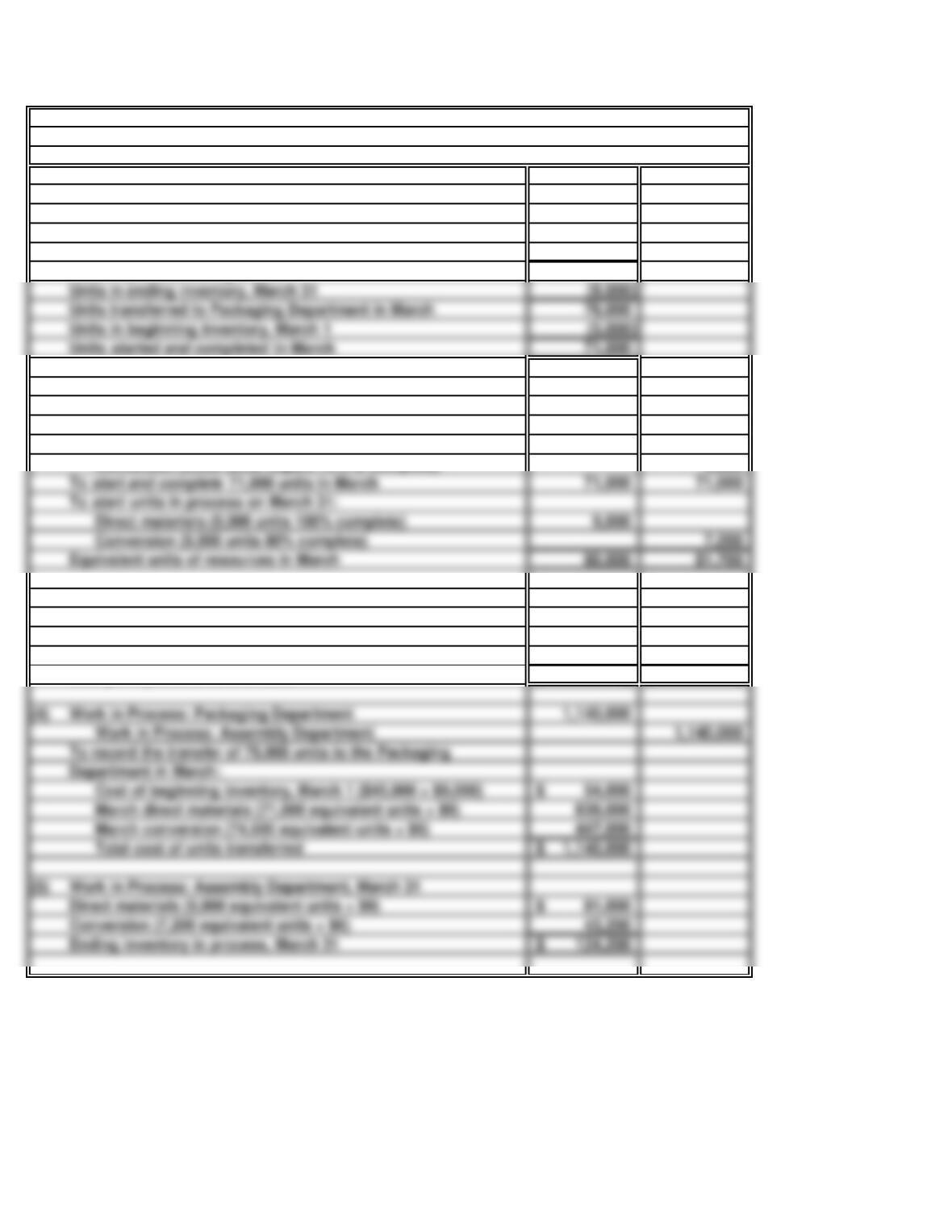

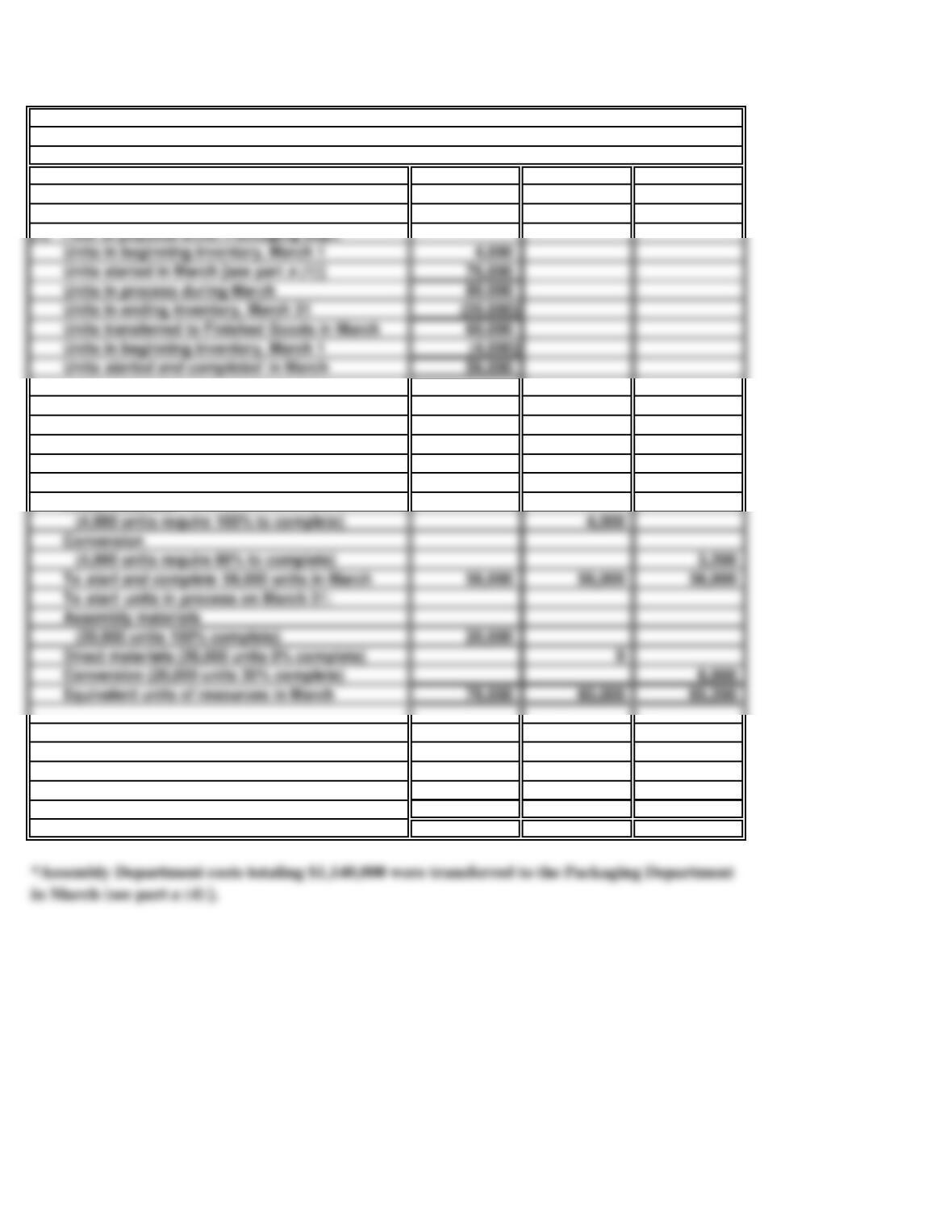

PROBLEM 18.8B

THOMPSON TOOLS

a.

(1)

5,000

80,000

85,000

(2) Direct

Materials Conversion

0

3,500

(3) Direct Conversion

Materials Costs

720,000$ 490,200$

÷ 80,000 ÷ 81,700

9$ 6$

Requirements for the Assembly Department in March

Cost per equivalent unit in March

Costs incurred by Assembly Department in March

Equivalent units in March [see part (2) ]

Cost per equivalent unit in March

Conversion (5,000 units require 70% to complete)

Units in beginning inventory, March 1

Units in process during March

Flow of physical units: Assembly Department

Input resources

To finish units in process on March 1:

Direct materials (5,000 units require 0% to complete)

Units started in March

PROBLEM 18.8B

THOMPSON TOOLS (continued)

b. Requirements for the Packaging

(2) Assembly Direct

Input resources Materials Materials Conversion

To finish units in process on March 1:

Assembly material

0

Direct materials

(3)

Assembly Direct Conversion

Cost per equivalent unit in March Materials Materials Costs

Costs charged to Packaging Dept. in March* 1,140,000$ 840,000$ 260,800$

Equivalent units in March [see part (2) ]÷ 76,000 ÷ 60,000 ÷ 65,200

Cost per equivalent unit in March 15$ 14$ 4$

Department in March

(4,000 units require 0% to complete)

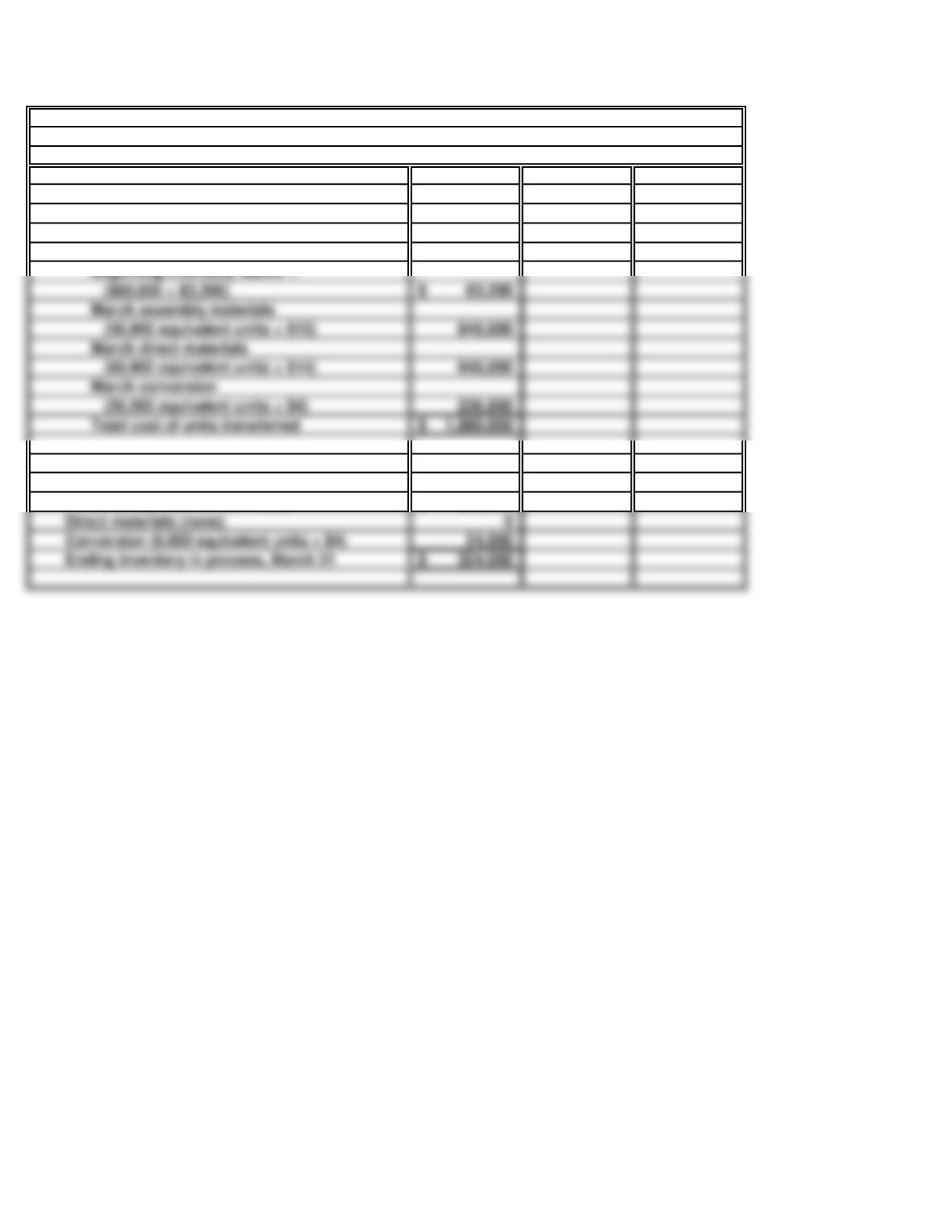

PROBLEM 18.8B

THOMPSON TOOLS (concluded)

(4) 1,980,000

Work in Process: Packaging Department 1,980,000

(5)

300,000$

Finished Goods Inventory

(20,000 equivalent units × $15)

To record the transfer of 60,000 units

Inventory in March:

Work in Process: Packaging Dept., March 31

Assembly materials

to the Finished Goods

SOLUTIONS TO CRITICAL THINKING CASES

CASE 18.1

SHOULDN'T WE DO THINGS DIFFERENTLY?

30 Minutes, Strong

Mr. Brown:

Thank you for your recent memo. I am glad to see that you have become familiar with our cost

accounting methods and have constructive suggestions. You are correct that we could use job

order costing and, also, that we could base our unit cost computations upon equivalent units,

rather than upon units completed. But let me explain briefly why we are currently doing what

we do.

Given that we have a substantial amount of work in process in our fermenting tanks, you may

ask, Why? The answer is that we always have the same quantity of beer in our fermenting

tanks. As the amount of our work in process does not change from month to month, our

productive effort is essentially equivalent to the amount of finished product coming off our

bottling line.

CASE 18.2

METAL PRODUCTS, INC.

a.

b.

c.

20 Minutes, Medium

The cost per equivalent unit of cut materials transferred into the Assembly Department in

February and reported as beginning inventory on March 1 was $25 per unit ($25,000 ÷ 1,000

The cost per equivalent unit of conversion for the Assembly Department in March was $25.

The cost of conversion added by the Assembly Department in February and reported as

There are many reasons why the cost of cut materials transferred in from the Cutting

Department and conversion costs incurred by the Assembly Department may have

decreased. Possible reasons include:

CASE 18.3

PROCESS COSTING

INTERNET

a.

d.

Responses to this question will vary. Some may argue that certain environmental and safety

25 Minutes, Easy

Carbonated water comprises over 90% of a soft drink's direct material. The second main

ingredient is sugar, which comprises another 7% - 12% of the direct materials. Much

smaller quantities of ingredients (that often are considered indirect materials) include

CASE 18.4

WRIGLEY COMPANY

ETHICS, FRAUD & CORPORATE GOVERNANCE

a.

Melting

Mixing

b.

c.

d.

One configuration of processing departments could include a “Production Department” and a

wrapping, and packing activities. Other configurations may also be acceptable.

Major overhead costs at Wrigley might include the cost of maintaining the various machines

30 Minutes, Medium

A sample flowchart of the activities involved in manufacturing chewing gum could be

constructed as follows:

Responses to this question will vary. Some may argue that certain environmental and charitable