CHAPTER 18

PROCESS COSTING

Brief Learning

Exercises Topic Objectives Skills

B. Ex. 18.1 Selecting a cost accounting system 18-1 Analysis, judgment

B. Ex. 18.2 Real World: Walmart and J & J 18-1 Analysis, judgment

Selecting a cost accounting system

B. Ex. 18.3 Understanding cost flows 18-2 Analysis

B. Ex. 18.4 Process costing journal entries 18-2 Analysis

B. Ex. 18.5 Computing equivalent units 18-3 Analysis

B. Ex. 18.6 Computing cost per equivalent unit 18-3, 18-4 Analysis

B. Ex. 18.7 Solving for missing information 18-3, 18-4 Analysis

B. Ex. 18.8 Determining departmental unit costs 18-5 Analysis

B. Ex. 18.9 Interpreting a production cost report 18-6 Analysis

B. Ex. 18.10 Interpreting a production cost report 18-6 Analysis

Learning

Exercises Topic Objectives Skills

18.1 Accounting terminology

18-1–18-3,

18-6

Analysis

18.2 Calculating equivalent units 18-2, 18-3 Analysis

18.3 Process costing in a single department 18-2–18-5 Analysis

18.4 Preparing a production cost report 18-6 Analysis

18.5 Computing equivalent units 18-2–18-5 Analysis

18.6 Process costing with no beginning inventories, 18-2–18-5 Analysis,

Part I 18-2–18-5 communication

18.7 Process costing with no beginning inventories, 18-2–18-5 Analysis

Part II 18-2–18-5

18.8 Process costing with beginning inventories, 18-2–18-5 Analysis

Part I 18-2–18-5

18.9 Process costing with beginning inventories, 18-2–18-5 Analysis

Part II 18-2–18-5

18.10 Process costing through two departments, Part I 18-2–18-5 Analysis

18.11 Process costing through two departments, 18-2–18-5 Analysis

Part II 18-2–18-5

18.12 Solving for missing information 18-2–18-5 Analysis

18.13 Assessing the need for process costing 18-1–18-6

Communication,

judgment, analysis

18.14 Interpreting a production cost report 18-2–18-6 Analysis

18.15 Solving for missing information 18-2–18-6 Analysis

OVERVIEW OF BRIEF EXERCISES, EXERCISES, PROBLEMS, AND CRITICAL

THINKING CASES

Learning

Topic Objectives Skills

18.1 A,B Calculating equivalent units 18-2, 18-3 Analysis

18.2 A,B Computing and using unit costs 18-2–18-5 Analysis, communication

18.3 A,B Preparing a production cost report 18-6 Analysis

18.4 A,B

Process costing with no beginning or ending

inventories

18-2–18-5 Analysis, communication

18.5 A,B Computing equivalent units and unit costs 18-2–18-4 Analysis

18.6 A,B Preparing a production cost report 18-5, 18-6 Analysis, communication

18.7 A,B Comprehensive process costing 18-2–18-5 Analysis

problem with two departments

18.8 A,B

Comprehensive process costing problem with

two departments

18-2–18-5 Analysis

Critical Thinking Cases

18.1 Evaluating a process costing system 18-1–18-3

Judgment,

communication

18.2

Interpreting and using process costing

information

18-2–18-6 Communication, analysis

18.3

Processes & Product Costs in Soft Drink

Manufacturing (Internet)

18-1, 18-2

Analysis, judgment,

communication

18.4

Real World: Wrigley Company

Manufacturing processes

18-1, 18-2

Communication,

technology, research

Ethics, Fraud & Corporate Governance

Problems

Sets A, B

DESCRIPTIONS OF PROBLEMS AND CRITICAL THINKING CASES

Problems (Sets A and B)

18.1 A,B Brite Ideas/Street Smarts 20 Easy

Compute equivalent units for two consecutive months with three

categories of inputs and beginning and ending work in process.

18.2 A,B Sun Appliance/MowTown Manufacturing 20 Easy

Compute per-unit costs of products and processes. Assess the usefulness

of these costs for managers.

18.3 A,B Sun Appliance/MowTown Manufacturing 30 Medium

Produce a cost of production report based on information in P18-2.

18.4 A,B Toll House/Snack Happy 30 Medium

A process cost problem involving three processes and an explanation of

the usefulness of different unit costs. Does not include equivalent unit

calculations.

18.5 A,B Badgersize Company/Balfanz Company 35 Medium

Determine the cost per equivalent unit with partially complete beginning

and ending work in process.

18.6 A,B Badgersize Company/Balfanz Company 35 Medium

Prepare a cost of production report based on information in P18.5.

18.7 A,B Hound Havens/Delray Industries 50 Strong

A comprehensive process costing problem with two production

departments.

18.8 A,B Wilson Dynamics/Thompson Tools 50 Strong

A comprehensive process costing problem with two production

departments.

Below are brief descriptions of each problem, case, and the first Internet assignment. These

descriptions are accompanied by the estimated time (in minutes) required for completion and by a

difficulty rating. The time estimates assume use of the partially filled-in working papers.

Critical Thinking Cases

Shouldn’t We Do Things Differently? 30 Strong

Students are to evaluate recommendations for changing a company’s cost

accounting methods. Requires judgment and perspective. Very

challenging—best as a group assignment to be discussed in class.

18.2 Metal Products, Inc. 20 Medium

Students are asked to analyze changes in unit costs from one month to

the next and speculate why these changes may have occurred.

18.3 Processes & Product Costs in Soft Drink Manufacturing 25 Easy

Internet

Students are asked to review the processes and product costs associated

with the production of soft drinks. They also must argue whether direct

labor or manufacturing overhead constitutes a larger portion of a soft

drink manufacturer’s total product costs.

Wrigley Company 30 Medium

Ethics, Fraud and Corporate Governance

Students are asked to read a description of a simple production process

and prepare a flowchart of activities. They must then determine how

various departments might be set up under a process costing system.

Finally, possible overhead sources and activity bases are to be

considered. They are also required to decide whether it is ethical for the

company to report only its good works throughout the world.

18.4

18.1

SUGGESTED ANSWERS TO DISCUSSION QUESTIONS

2.

4.

6.

Job order concepts are more appropriate than process cost concepts to the operations of a law firm.

Several answers are possible. Some suggestions include automobiles, furniture, stereo equipment,

Whether a manufacturing company should use job order costing or process costing depends upon

the nature of the company’s manufacturing operations. Job order costing is used when each unit

of product (or batch of products) has unique characteristics that may affect its manufacturing cost.

7.

8.

9.

10.

11.

In process costing, the costs of performing each manufacturing process are accumulated separately

for the accounting period. The cost per unit of product is then determined by dividing the total cost

of performing the manufacturing process by the number of units processed during the accounting

In many situations, assigning the entire cost of production to units completed and transferred

Managers use information obtained from process costing to value inventories, determine the cost

Equivalent units are a measure of work done during the period, including work performed on units

that were partially complete at the beginning or end of the period. The idea is that performing, say,

40% of the work on 100 units is “equivalent” to fully processing 40 units.

In a fast-paced assembly line, units are processed very quickly. Only those units actually on the

usually is insignificant in relation to the total number of units completed during the period. When

Units of production in a process costing system are often manufactured in high volume through

14.

15.

Beginning units in process ……………………………………………………………..

XXX

Plus: Units started ……………………………………………………………………….

XXX

Total units in production …………………………………………………………………

Less: Ending units in process ………………………………………………………….

Units started and completed during the current period may be computed using several

approaches:

The cost of units started and completed during the current period contain only the cost of input

SOLUTIONS TO BRIEF EXERCISES

b.

d.

e.

3: Retail establishments do not make their own products and thus, do not use

1: Handyman Special, Inc. probably does odd jobs for home owners and

1, 2 and 3: Carpet Makers manufactures large amounts of carpeting, in

B. Ex. 18.3 a. (1) XXX

Accounts Payable ………………………….

XXX

c. (1) XXX

Cash (or Accounts Payable) ………………

XXX

XXX

XXX

XXX

Cost of Goods Sold ………………………………

Finished Goods Inventory ………………………

Work in Process Inventory ……………………….

To record factory overhead costs applied to

To record transfer of cost of completed goods to the

To record factory overhead cost (such as payroll for

Materials Inventory ……………………………….

Manufacturing Overhead ………………………..

XXX

XXX

XXX

Work in Process Inventory ……………………….

Direct Labor ……………………………………….

Work in Process Inventory ……………………….

To record cost of direct labor assigned to production.

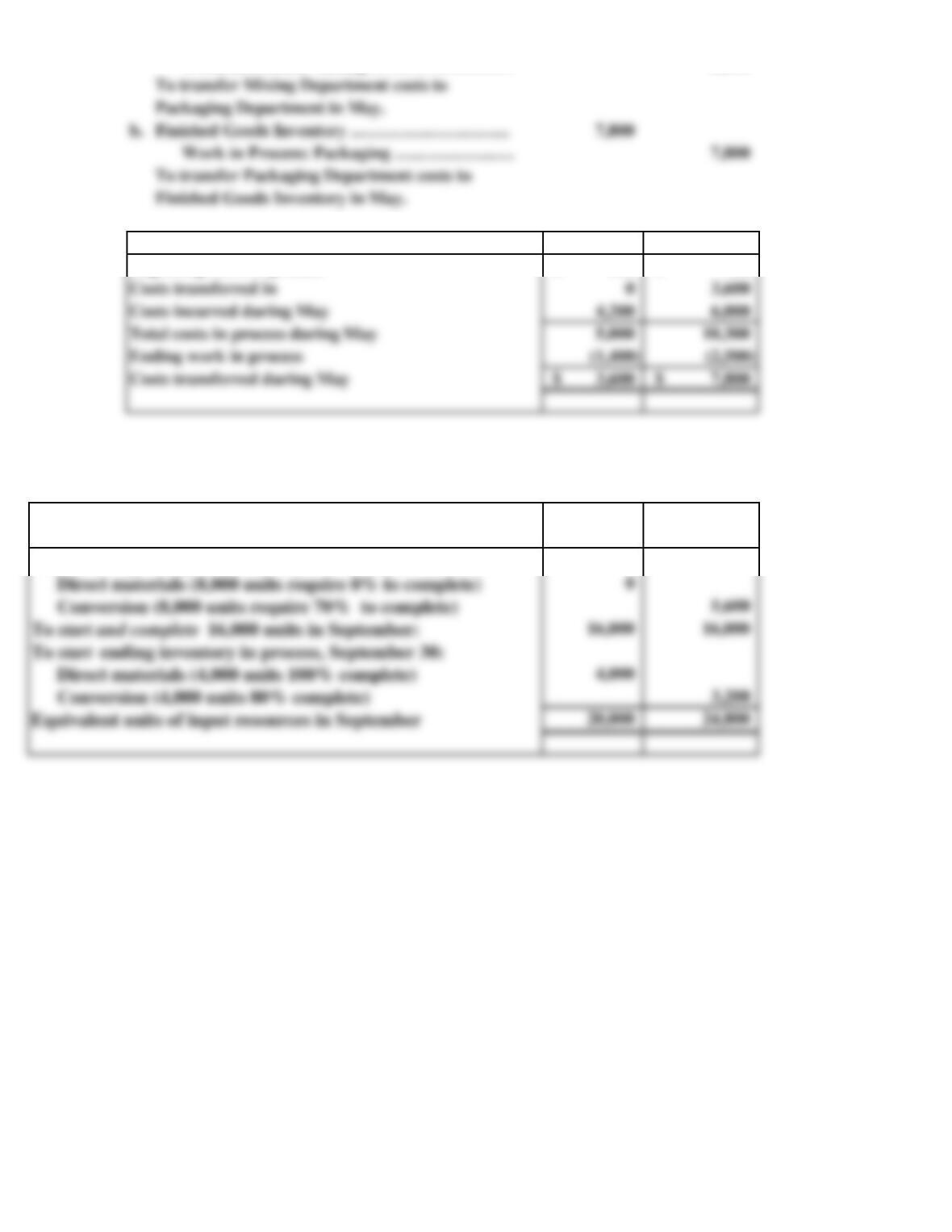

B. Ex. 18.4 a. 3,600

Work in Process: Mixing ……………………. 3,600

Computations: Mixing Packaging

Beginning work in process 800$ 700$

B. Ex. 18.5

Input resources required

Direct

Materials

Conversion

Work in Process: Packaging ……………………..

To finish beginning inventory in process, September 1:

Work in Process: Packaging ………………… 7,800

Finished Goods Inventory ……………………….

B. Ex. 18.6 a.

b.

Direct

Materials

Conversion

2,000

B. Ex. 18.7

Direct

Materials

Conversion

Units started and completed in July

Total equivalent units of input resources in July

Equivalent units to finish beginning inventory:

Conversion (12,000 units require 60% to complete)

Direct materials (12,000 units require 0% to complete)

Equivalent units to start ending inventory:

Direct materials (9,000 units 100% complete)

Conversion (9,000 units 70% complete)

500,000$ 352,000$

÷ $25 ÷ $16

Cost per equivalent unit of input resource in July

To finish beginning inventory in process, March 1:

$14 per equivalent unit of direct material

$16 per equivalent unit of conversion

Computations:

Input resources required

Cost of direct materials and conversion incurred in July

Direct materials (5,000 units require 40% to complete)

Direct materials (2,000 units 90% complete)

Conversion (2,000 units 30% complete)

Cost per equivalent unit of input resource in March

Conversion (5,000 units require 60% to complete)

To start ending inventory in process, March 31:

Equivalent units of input resources in March

Cost of direct materials and conversion incurred in March

To start and complete 30,000 units in March:

Equivalent units of resources in March

B. Ex. 18.8 $ 50,000

39,000

B. Ex. 18.9

a.

Direct

b.

Materials Conversion

Equivalent units to start ending inventory:

Units started and completed in December

B. Ex. 18.10

Beginning work in process, September 1

Costs incurred to complete beginning work in

process

The cost per equivalent unit transferred out of the department includes the costs

of beginning inventory carried forward from October. The $162 average cost

Given that no equivalent units of material were required to finish beginning

inventory, all direct materials must be added at the beginning of the production

process in the Distillation Department.

Equivalent units consumed to start new units

Cost of units started in September

September costs assigned to work in process,

Costs transferred out of Blending Department

SOLUTIONS TO EXERCISES

Ex. 18.2 a.

Direct Materials

b.

Direct Materials

Jan. Feb.

Labor and

Overhead

Equivalent Units Produced in February

1Number of units started and completed:

Labor and

Overhead

Equivalent Units Produced in January

Ex. 18.1 a.

b.

d.

Process costing

Job order costing

Conversion costs

Equivalent units

Production cost report

Ex. 18.3 a. 160,000

90,000

b. 160,000

Work in Process Inventory …………………..

c. 320,000

Cost of Goods Sold ………………………………….

Sales ……………………………………………

Finished Goods Inventory ……………………

Finish Goods Inventory …………………………….

Work in Process Inventory ………………………..

Direct Materials ………………………………

Accounts Receivable ………………………………..

Direct Labor …………………………………..

Manufacturing Overhead …………………….

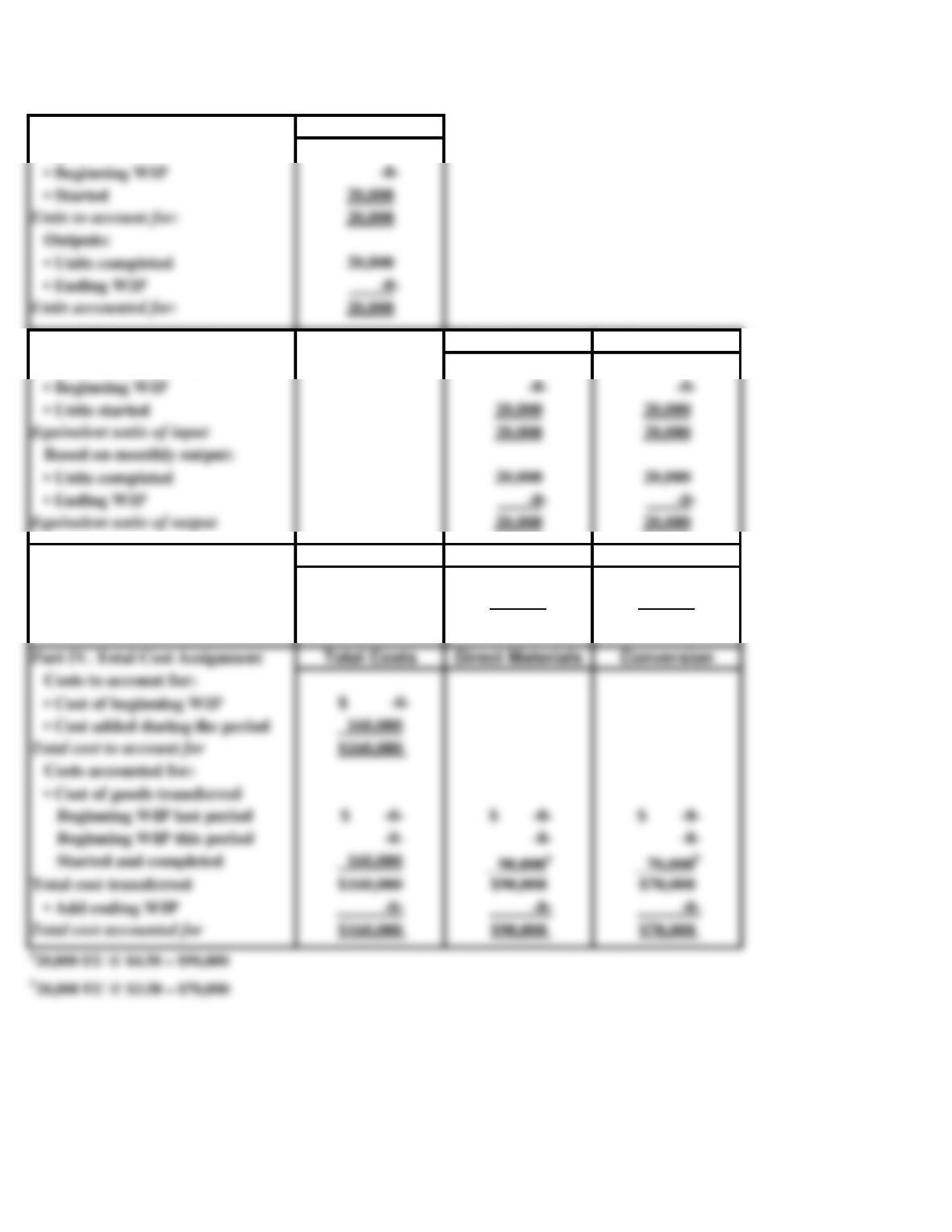

Part I. Physical Flow Total Units

Inputs:

Part II. Equivalent Units Direct Materials

Conversion

Based on monthly input:

Based on monthly output:

Part III. Cost Per Equivalent Unit Total Unit Cost Direct Materials

Conversion

Input costs $90,000 $70,000

Divide by equivalent units ÷20,000 ÷20,000

Costs per equivalent unit $8.00 $4.50 $3.50

Part IV. Total Cost Assignment Total Costs Direct Materials

Conversion

Costs to account for:

Costs accounted for:

Total cost transferred $160,000 $90,000 $70,000

Ex. 18.4

Shamrock Industries

Production Cost Report

For the Month of June

Outputs:

Ex. 18.5

a.

March

Beg. WIP 4,900 (7,000 × .7)

b. March April

$ 6,979,360 $ 7,781,280

c. March April

$ 978,460 $ 1,168,310

April

1,920 (4,800 × .4)

Equivalent full units of production:

Total manufacturing costs …………………………………

Direct Materials costs ………………………………………

End. WIP 2,880 (4,800 × .6)

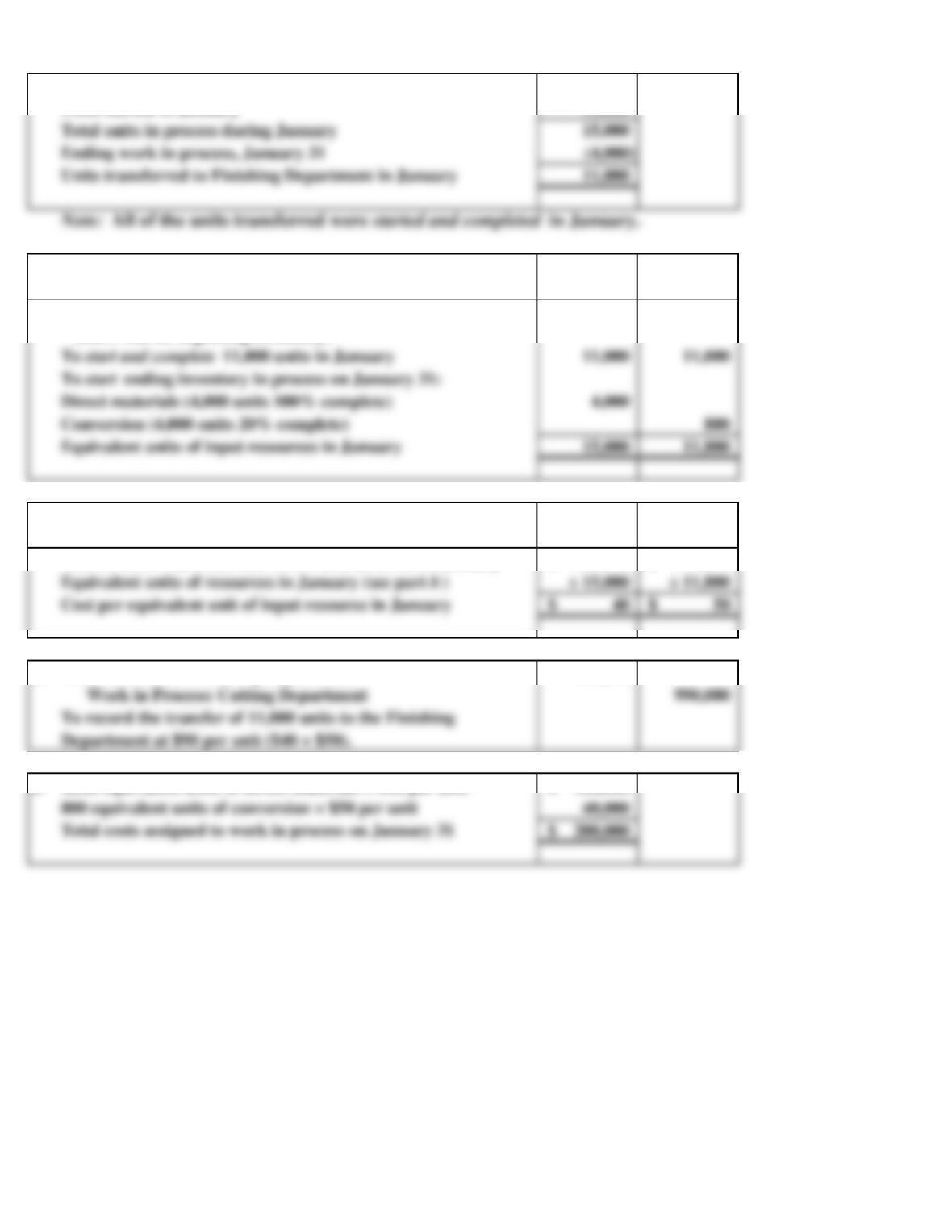

Units transferred to Finishing Department in January

Total units in process during January

Ending work in process, January 31

Ex. 18.6

a. 0

15,000

b. Direct

Materials Conversion

0 0

Equivalent units of resources in January (see part b)

Cost per equivalent unit of input resource in January

To record the transfer of 11,000 units to the Finishing

Department at $90 per unit ($40 + $50).

Work in Process: Cutting Department

800 equivalent units of conversion × $50 per unit

c. Direct Conversion

Materials Costs

600,000$ 590,000$

d. 990,000

e. 160,000$

To finish beginning inventory

Input resources required

Beginning work in process, January 1

Units started in January

(there was no beginning inventory)

Work in Process: Finishing Department

Cost of direct materials and conversion incurred in January

4,000 equivalent units of direct materials × $40 per unit

To start and complete 11,000 units in January

To start ending inventory in process on January 31:

Equivalent units of input resources in January

Conversion (4,000 units 20% complete)

Direct materials (4,000 units 100% complete)

a.

b. 0

c. Cut Direct Trim

Materials Materials Conversion

Equivalent units of input resources in January

To start ending inventory in process on January 31:

0 0 0

8,000 8,000 8,000

d. Cut Direct Trim Conversion

Materials Materials Costs

Cost per equivalent unit in January

Equivalent units in January (see part c)

990,000$ 142,400$ 235,200$

e. 1,040,000

To record the transfer of 8,000 units to Finished Goods

Inventory at $130 per unit ($90 + $16 + $24).

f. 270,000$

1,800 equivalent units of conversion x $24

Total costs assigned to work in process on January 31

900 equivalent units of direct trim materials x $16

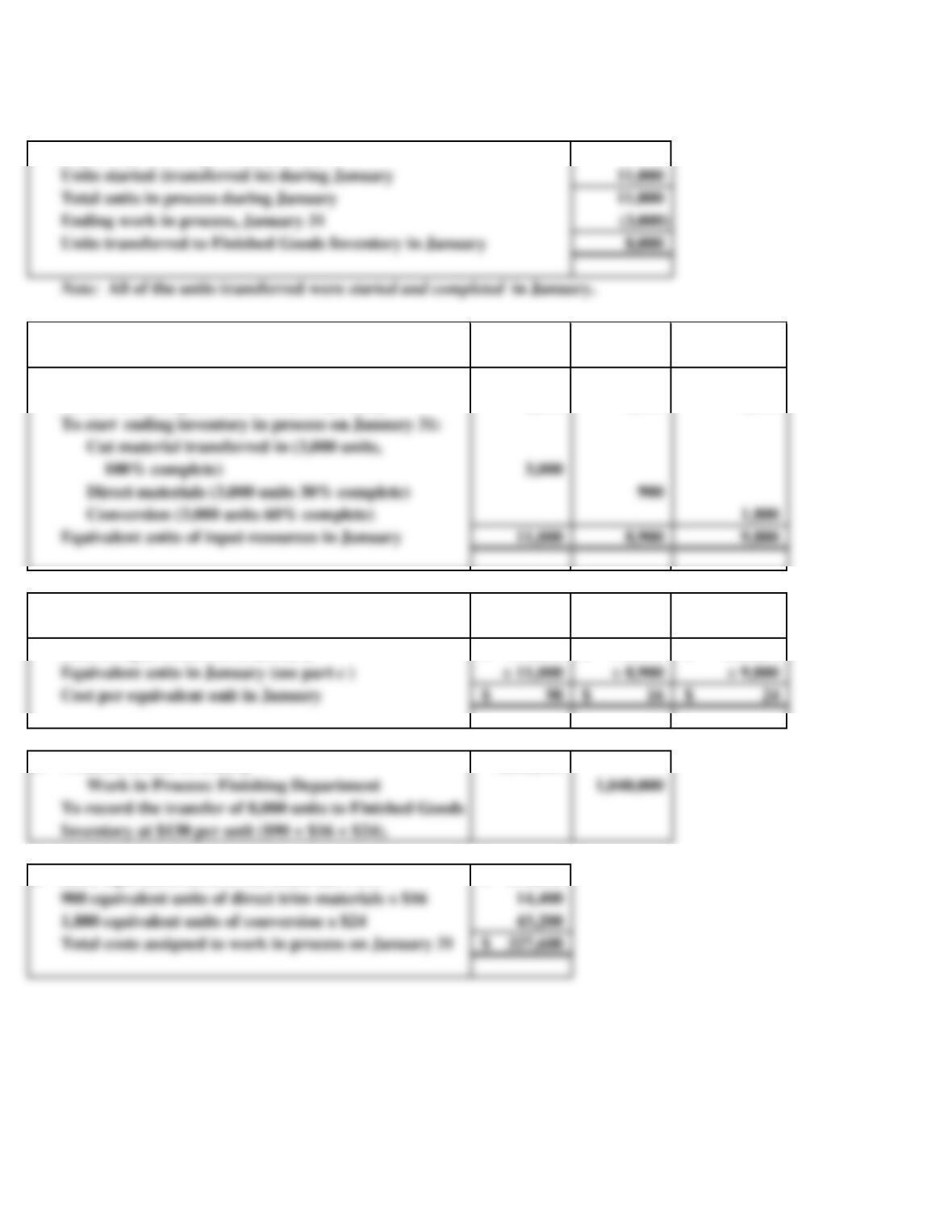

Ex. 18.7

Input resources required

To finish beginning inventory (there was none)

The number of units started by the Finishing Department equals the number of units transferred

in January from the Cutting Department, or 11,000 (see Exercise 18.6, part a).

Beginning work in process, January 1

To start and complete 8,000 units in January

Finished Goods Inventory

Cost of input resources in January

3,000 equivalent units of cut materials x $90

Units transferred to Finished Goods Inventory in January

Units started (transferred in) during January

Total units in process during January

Ending work in process, January 31

a. 500

11,500

b. Direct

Materials Conversion

Conversion (600 units 25% complete) 150

To start and complete 10,900 units in August

Direct materials (600 units 100% complete)

Equivalent units of input resources in August

To start ending inventory in process on August 31

0

350

c. Direct Conversion

Materials Costs

Equivalent units of resources in August (see part b )

Cost per equivalent unit of input resource in August

34,500$ 22,800$

d. 57,000

Work in Process: Mixing Department 57,000

Total cost of units transferred in August

August direct materials (10,900 equivalent units × $3)

August conversion (11,250 equivalent units × $2)

Cost of beginning inventory on August 1

600 equivalent units of direct materials × $3 per unit

150 equivalent units of conversion × $2 per unit

Total costs assigned to work in process on August 31

To finish beginning inventory in process on August 1:

Direct materials (500 gallons require 0% to complete)

To record the transfer of 11,400 gallons of mix to the Finishing

Conversion (500 gallons require 70% to complete)

Department in August:

Cost of direct materials and conversion incurred in August

Work in Process: Baking Department

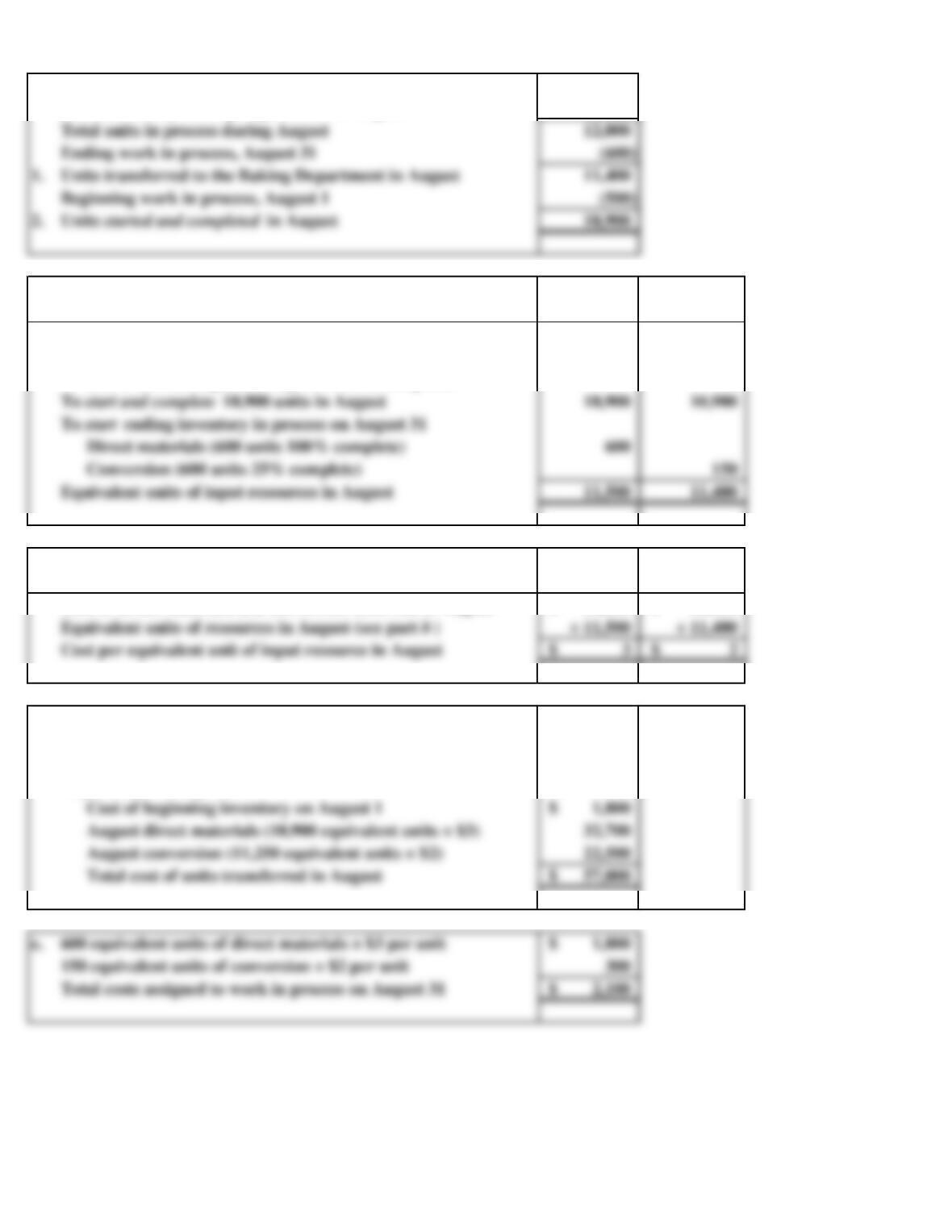

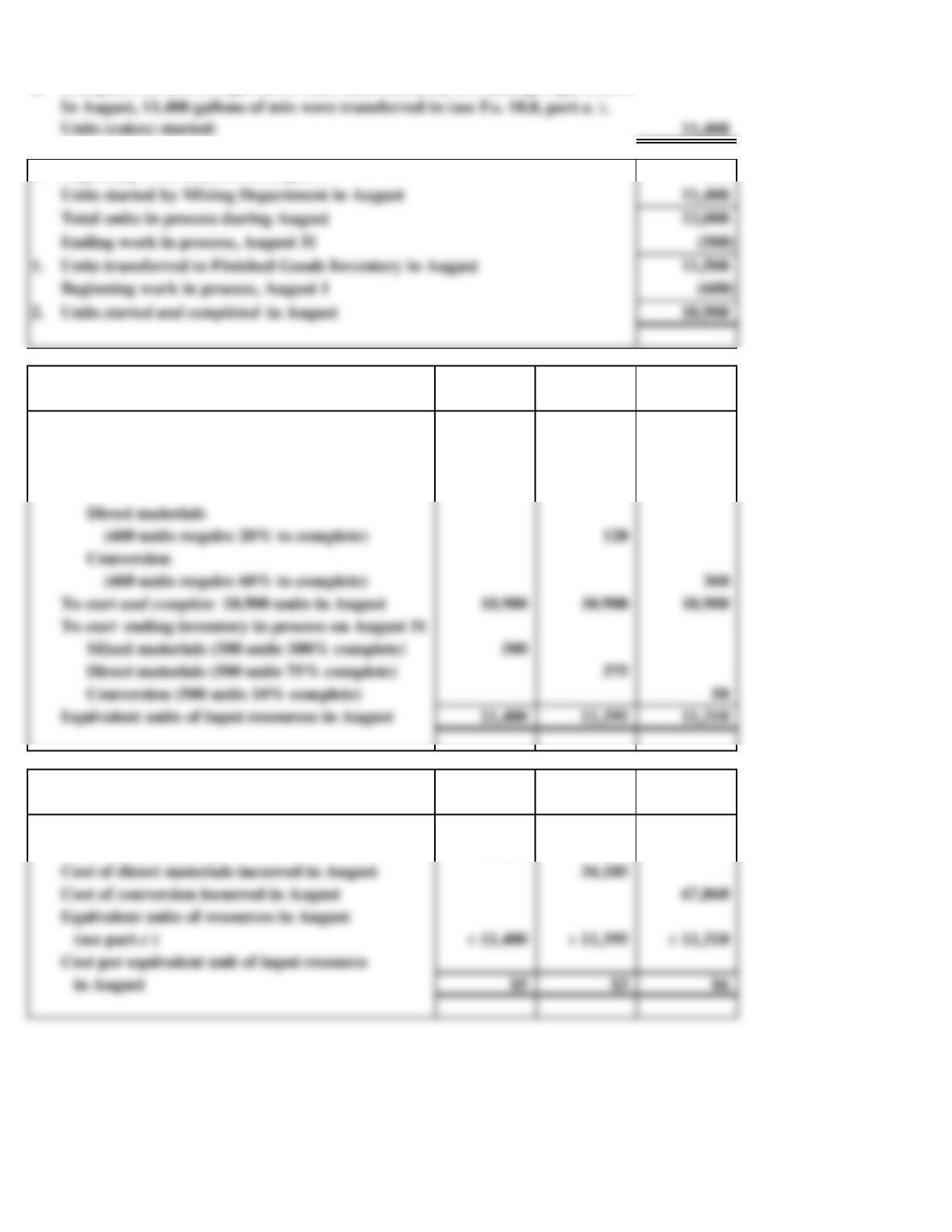

Ex. 18.8

Beginning work in process, August 1

Units started by Mixing Department in August

Input resources required

1. 11,400

2. 10,900

Total units in process during August

Ending work in process, August 31

Units transferred to the Baking Department in August

Beginning work in process, August 1

Units started and completed in August

a.

b. 600

Units started and completed in August

Beginning work in process, August 1

Units transferred to Finished Goods Inventory in August

Units started by Mixing Department in August

Total units in process during August

Ending work in process, August 31

c. Mixed Direct

Materials Materials Conversion

Mixed materials (600 units, 0% to complete) 0

To start ending inventory in process on August 31

Equivalent units of input resources in August

To start and complete 10,900 units in August

d. Mixed Direct Conversion

Materials Materials Costs

Equivalent units of resources in August

Cost of direct materials incurred in August

Cost of conversion incurred in August

in August

Cost per equivalent unit of input resource

(see part c)

57,000

(see Ex. 18.8, part d)

Cost of batter mix transferred in

August 1:

Input resources required

To finish beginning inventory in process on

Ex. 18.9

One gallon of mix is required for each cake Baked by the Baking Department.

Beginning work in process, August 1