Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

18–1

Chapter 18

Performance Measurement to

Support Business Strategy

Learning Objectives

1. Explain why management accountants should know the business strategy of their

organization.

2. Explain why companies use nonfinancial performance measures.

3. Understand the reasons why performance measures differ across levels of the organization.

4. Understand how the balanced scorecard helps organizations recognize and deal with their

conflicting responsibilities.

5. Understand how to apply the methods involved in an effective performance measurement

system.

18–2

Chapter Overview

I. EXPLAIN WHY MANAGEMENT ACCOUNTANTS SHOULD KNOW THE

BUSINESS STRATEGY OF THEIR ORGANIZATION

III. BEYOND THE ACCOUNTING NUMBERS

IV. RESPONSIBILITIES ACCORDING TO LEVEL OF ORGANIZATION

V. BUSINESS MODEL

VI. MULTIPLE MEASURES OR A SINGLE MEASURE OF PERFORMANCE?

• Balanced Scorecard

• Continuous Improvement and Benchmarking

VII. PERFORMANCE MEASUREMENT FOR CONTROL

VIII. SOME COMMON NONFINANCIAL PERFORMANCE MEASURES

• Customer Satisfaction Performance Measures

o Quality Control

o Delivery Performance

o Bookings and Purchase Orders

o Market Share

• Functional Performance Measures

o Manufacturing Cycle Time

IX. EMPLOYEE INVOLVEMENT

X. DIFFICULTIES IN IMPLEMENTING NONFINANCIAL PERFORMANCE

MEASUREMENT SYSTEMS

• Fixation on Financial Measures

• Reliability of Nonfinancial Measures

• Lack of Correlation Between Nonfinancial Measures and Financial Results

18–3

Chapter Outline

LO 18-1 Explain why management accountants should know the business

strategy of their organization.

EXPLAIN WHY MANAGEMENT ACCOUNTANTS SHOULD KNOW THE BUSINESS

STRATEGY OF THEIR ORGANIZATION

• The performance measures that accountants develop must tie directly to concepts in strategy

and organizational behavior.

o We have to know what kind of performance adds value to the company.

▪ We define business strategy as a company’s specific approach for deploying the

organizational assets and capabilities required to meet its customers’ needs competi-

tively, while delivering the desired returns to stakeholders.

• Stakeholders are groups or individuals who have an interest in what the

organization does.

o The business strategy identifies the firm’s value proposition.

▪ The firm’s value proposition is how the organization will create value for all

stakeholders.

▪ This statement may also imply the firm’s mission.

THE FOUNDATION OF A SUCCESSFUL BUSINESS STRATEGY

• Managers start forming strategy by identifying the company’s core assets and capabilities.

18–4

O Core resources and capabilities are those things that, if used well, can make the company

very successful.

• Porter Framework

o Of many frameworks for thinking about strategy, we present one of the most popular by a

scholar named Michael E. Porter.

▪ Porter identified three types of companies that are successful. They are:

• Cost leaders

• Product differentiators

• Focused competitors

o Cost Leaders

▪ Cost leaders have a high-volume production of an undifferentiated product, called a

commodity.

o Product Differentiation

▪ The product differentiator earns a premium price for a product with unique features.

• While there may be fewer customers who value these features, those who do are

willing to pay more for them and are not easily tempted to buy a cheaper product.

• Companies that use this strategy obtain profits by earning large margins.

18–5

• Product differentiators must develop products that customers value.

To do so, they use measures of marketing performance and the balanced

scorecard, discussed later in this chapter.

o Focused Competitors

▪ The focus strategy (also called a niche strategy or segmentation strategy) requires a

company to select a narrow segment of customers or products and apply a

combination of the cost leader and product differentiation strategies.

LO 18-2 Explain why companies use nonfinancial performance measures.

BEYOND THE ACCOUNTING NUMBERS

• Financial performance measures, especially those that come from the company’s accounting

systems, are commonly used to evaluate employee performance.

o Financial performance measures are easily quantifiable and can motivate employees to

improve the company’s accounting profits.

▪ Financial measures are good at getting managers’ attention.

o Financial measures suffer from several flaws that reduce their value as an operational

control device.

▪ They are not useful in identifying operational problems.

18–6

o In recent years, more and more companies have begun using nonfinancial metrics

because:

▪ Nonfinancial performance measures direct employees’ attention to those things that

the employees can control.

LO 18-3 Understand the reasons why performance measures differ across

levels of the organization.

RESPONSIBILITIES ACCORDING TO LEVEL OF ORGANIZATION

• Effective performance measurement is based on two factors:

• Effective performance measurement systems use measures that emphasize different things at

different levels of the organization.

o In general, performance measures should relate to what people at different levels control.

▪ At the lower levels in the organization, nonfinancial performance measures focus on

factors these employees can control, such as:

• Customer satisfaction (for those dealing with customers directly).

• Product quality (for those in production).

18–7

• The following are some of the nonfinancial performance measures that

organizations use to evaluate middle managers’ performance:

Amount of unwanted employee turnover.

• At middle levels in organizations, coordination and improvement of ongoing

activities take place in addition to redesigning products and processes.

BUSINESS MODEL

• A business model is a description of how different levels and employees in the organization

must perform for the organization to achieve its goals.

o A business model is a framework that links the roles of various employees and levels in

the organization and that illustrates how the successful completion of these roles will

result in achievement of the organization’s goals.

o For a given strategy and environment, many possible business models could be

appropriate.

▪ Example 1: The business model for an investment firm describes how a profitable

branch operates in the retail investment business. The branch manager exercises

leadership to motivate and satisfy employees.

18–8

LO 18-4 Understand how the balanced scorecard helps organizations

recognize and deal with their conflicting responsibilities.

MULTIPLE MEASURES OR A SINGLE MEASURE OF PERFORMANCE?

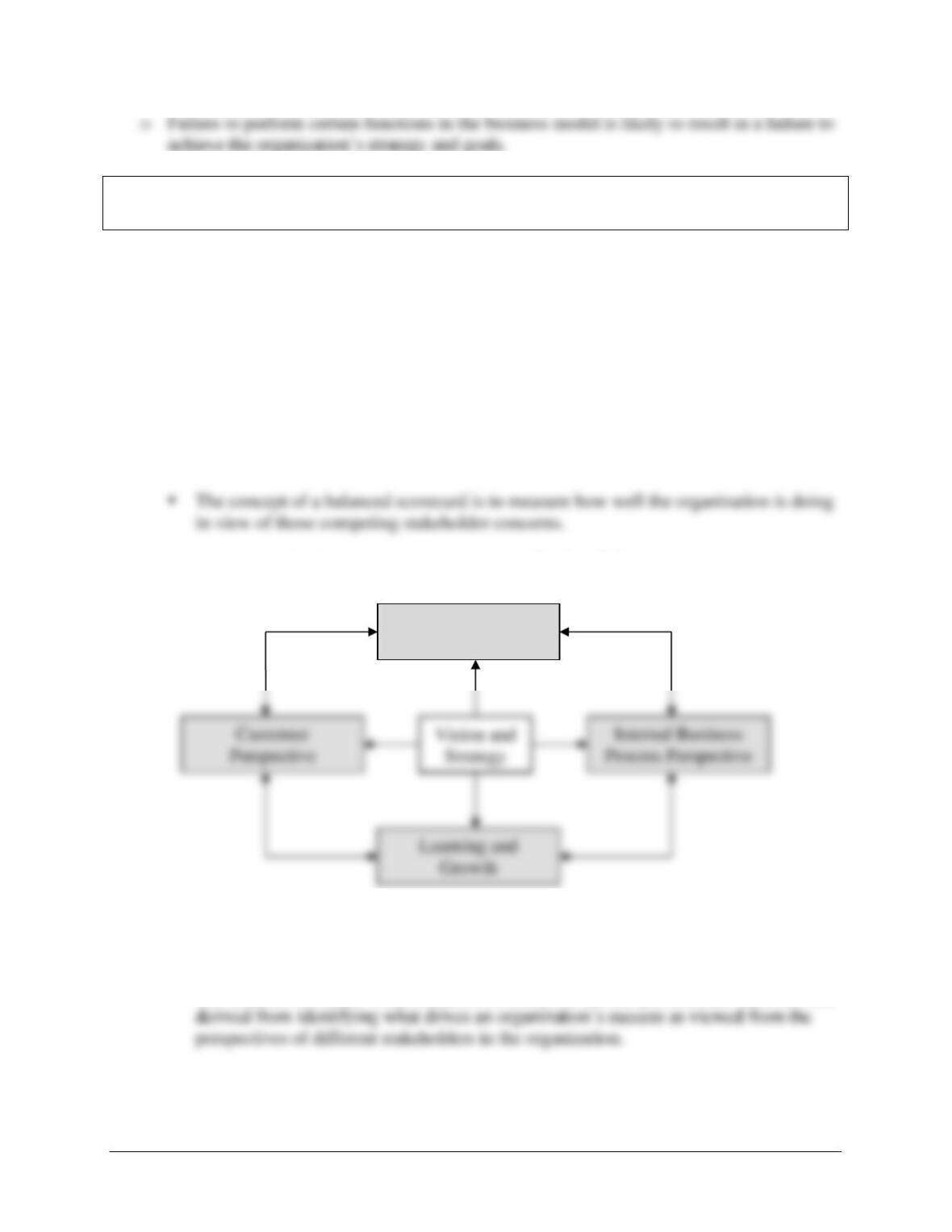

• Balanced Scorecard

o One structured approach to implementing a set of performance measures is the balanced

scorecard, which is a set of performance targets and results that show how well an

organization has performed in meeting its objectives relating to its stakeholders.

▪ A balanced scorecard is a management tool that recognizes organizational

responsibility to different stakeholder groups.

o An example of a balanced scorecard is shown in Exhibit 18.2.

o The focus of the balanced scorecard is to balance the efforts of the organization in

meeting its financial, customer, process, and innovative responsibilities.

▪ The distinctive feature of the balanced scorecard is that the performance measures are

Financial

Perspective

Perspective

18–9

o The balanced scorecard has four views or perspectives:

▪ Financial: To succeed financially, how should we appeal to our shareholders?

o A balanced scorecard for any particular organization could be based on any other

perspectives if they are important for the organization’s success.

▪ Within each perspective, the scorecard identifies the goals, or objectives, for the

organization as often shaped by the competitive environment.

• A select list of organizations using the balanced scorecard is in Exhibit 18.3.

o The balanced scorecard primarily has been used at the top management level to support

the organization’s development of strategies.

18–10

▪ A typical development of the balanced scorecard may involve the following:

Step1: A company’s top executives form a team to clarify the company’s strategy

and objectives to meet responsibilities.

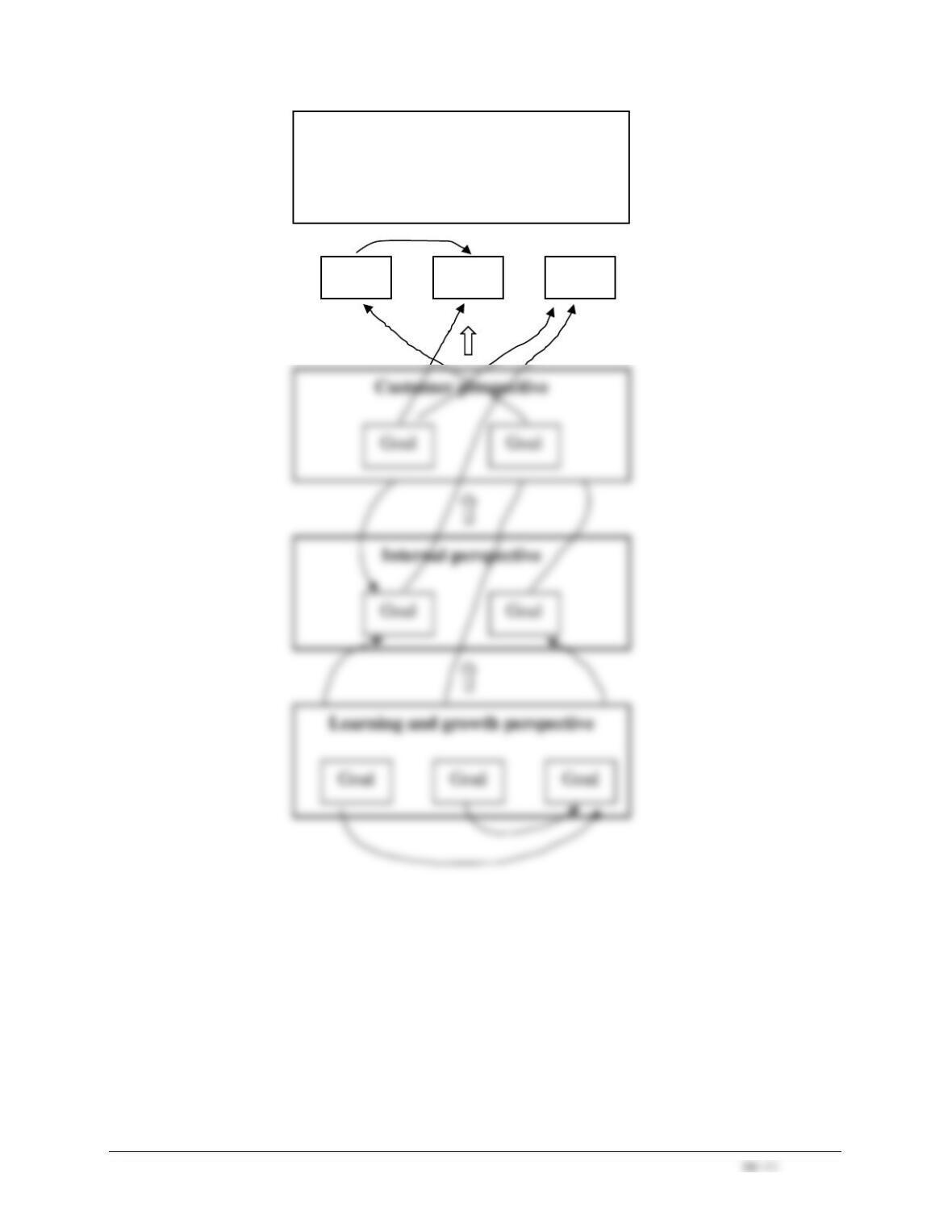

o A company’s strategy, as illustrated in the business model, can be linked to the balanced

scorecard through a strategy map, as shown in Exhibit 18.5. Specifically, the strategy

map links the objectives or goals in each of the perspectives.

▪ By drawing the strategy map, a company can determine if it is missing measures in

any of the perspectives or if it has goals that do not seem to be linked to other parts of

the map.

Financial perspective

Goal

Goal

Goal

18–12

LO 18-5 Understand how to apply the methods involved in an effective

performance measurement system.

• Continuous Improvement and Benchmarking

o Performance measurement is useful not only for evaluation, but also for control.

▪ Continuous improvement means the continuous reevaluation and improvement of

the efficiency of an organization’s activities.

• Continuous improvement is a philosophy that seeks to:

Improve the activities in which the organization engages through

documentation and understanding,

▪ Benchmarking involves continuously identifying an activity that needs to be

improved, finding an organization (sometimes in one’s own organization) that is the

most efficient in performing the activity, studying its process, and then utilizing that

process.

• Benchmarks are used to evaluate the performance of an activity, operation, or

organization relative to its performance by other companies.

• Important guidelines for benchmarking include:

18–13

PERFORMANCE MEASUREMENT FOR CONTROL

• Companies develop multiple performance measures as a way to evaluate the achievement of

its managers.

LO 18-6 Identify examples of nonfinancial performance measures and discuss

the potential for improved performance resulting from improved

activity management.

SOME COMMON NONFINANCIAL PERFORMANCE MEASURES

• Customer Satisfaction Performance Measures

o Quality Control

▪ Objective of quality control is to increase customer satisfaction with the product,

reduce the costs of dealing with customer complaints, and reduce the costs of

repairing products or providing a new service.

▪ Measures include:

o Delivery Performance

▪ The objective of delivery performance is to deliver goods and services when

promised.

18–14

o Bookings and Purchase Orders

▪ Bookings and purchase orders are a lead indicator of revenues.

o Market Share

▪ Market share must be measured relative to market size (i.e., its growth).

• Functional Performance Measures

o An organization must evaluate its internal functional process performance while serving

external customers. (See Business Application box “Loyal Customers Might Not Be

Profitable.”)

o Manufacturing Cycle Time

▪ Manufacturing cycle time represents the time involved in processing, moving,

storing, and inspecting products and materials. It is the total time taken to produce a

good or service.

18–15

o Manufacturing Cycle Efficiency

▪ Manufacturing cycle efficiency measures the efficiency of the total manufacturing

cycle.

• This formula calculates a percentage representing the time actually spent

processing the unit. The higher the percentage, the less the time (and costs) that

needs to be spent on nonvalue-added activities.

▪ Example 3: Tom operates a computer store that accepts custom orders for desktop

computers. Customers can choose from a variety of components such as

motherboards, CPUs, hard drives, DRAMs, graphics cards, sound cards, etc.

18–16

• Productivity

o Manufacturing cycle efficiency focuses on the effective use of time. Productivity focuses

on the efficient conversion of inputs into outputs.

o Partial productivity measures the relation between output and a single input, or

▪ Partial productivity measures are typically measured as:

• The efficiency variance is a good basis for assessing how a manufacturing plant is

doing as compared to engineering standards; if these standards do not change over

time, they are also a basis for assessing whether the plant is improving.

o One approach for comparing the productivity of business units that use a different mix of

inputs (or even different inputs) is to calculate total factor productivity.

▪ Total factor productivity is a ratio of the value of output to the value of all key

inputs.

18–17

o An Illustration of Various Productivity Measures

▪ Exhibit 18.8 provides selected operating data.

▪ Exhibit 18.9 provides the results. See Demonstration Problem

• Nonfinancial Performance and Activity-Based Management

o Organizations should manage by using activity data rather than cost data to identify

problems, to suggest an approach to solve problems, and to prioritize improvement

efforts.

▪ Organizations find value in knowing the amount of time it takes to complete a

sequence of activities.

▪ Companies often make four mistakes when trying to measure nonfinancial

performance.

• Not linking measures to strategy.

• Objective ad Subjective Performance Measures

o Objective performance measures are such that different people can look at them and

agree that the method used to calculate the measure is correct, even though the choice of

the measures is in dispute.

18–18

LO 18-7 Explain why employee involvement is important in an effective

performance measurement system.

EMPLOYEE INVOLVEMENT

• Nonfinancial measures have the advantage that they are more likely to be understandable by

employees directly involved in operations.

o The measures used to evaluate performance reflect each unit’s understanding of its

contribution to the organization.

o Worker involvement is important for three reasons:

▪ When workers take on real decision-making authority, their commitment to the

organization and its objectives increases.

▪ When decision-making responsibility lies with workers closer to the customer,

workers are more responsive to customer concerns and can make informed decisions.

o Companies need to evaluate their own performance in getting workers involved and

committed.

▪ Exhibit 18.10 lists performance measures that organizations can use to assess their

accomplishments in terms of worker involvement and commitment.

18–19

o Worker involvement and commitment measures include:

▪ Worker development (percentage of workers in mentor programs),

▪ Worker empowerment (percentage of workers authorized to issue credit),

o Increasing the percentages on these measures demonstrate the organization’s attempt to

increase worker involvement and commitment to it.

o Effective worker involvement presents three challenges for management.

▪ Management must create a system that conveys the organization’s objectives and

critical success factors to all members.

18–20

DIFFICULTIES IN IMPLEMENTING NONFINANCIAL PERFORMANCE

MEASUREMENT SYSTEMS

• Fixation on Financial Measures

o A strong fixation on financial measures works against effective use of nonfinancial

performance measures.

• Reliability of Nonfinancial Measures

18–21

Matching

A.

Balanced scorecard

I.

Mission statement

B.

Benchmarking

J.

Partial productivity

C.

Business model

K.

Productivity

D.

Business strategy

L.

Stakeholders

E.

Continuous improvement

M.

Strategy map

F.

Manufacturing cycle efficiency

N.

Total factor productivity

G.

Manufacturing cycle time

O.

Value proposition

H.

Mission

_____ 1. Description of how different levels and employees in the organization must perform

for the organization to achieve its goals.

_____ 2. Why an organization exists; its purpose and goals..

_____ 3. Description of an organization’s values, definition of its responsibilities to

stakeholders, and identification of its major strategies..

_____ 4. A company’s specific approach for deploying the organizational assets and

capabilities required to meet its customers’ needs competitively, while delivering the

desired returns to shareholders. .

_____ 5. Groups or individuals, such as employees, suppliers, customers, shareholders, and

communities, who have an interest in what the organization does.

_____ 6. Continuous reevaluation and improvement of the efficiency of an organization’s

activities.

_____ 7. Performance measurement system relying on multiple financial and nonfinancial

measures of performance.

_____ 8. The time involved in processing, moving, storing, and inspecting products and

materials.

_____ 9. Continuous process of measuring a company’s own products, services, or activities

against competitors’ performance.

_____ 10. Measures of the efficiency of the total manufacturing cycle; equals processing time

divided by the manufacturing cycle time.

_____ 11. Measure that expresses the relation between output and a single input.

_____ 12. How the organization will create value for all stakeholders.

_____ 13. Ratio of the value of output to the value of all key inputs.

_____ 14. A measure that expresses the conversion of inputs into output.

_____ 15. A visual device to communicate an organization’s strategy.

Matching Answers

18–23

Multiple Choice

1. Which of the following is a nonfinancial measure?

a. Number of customer complaints.

b. Return on investment.

c. Prevention cost.

d. Opportunity cost.

2. Which of the following statements is correct?

a. The business model can suggest ways to evaluate performance that makes sense to the

organization.

b. A single measure of performance typically evaluates the result.

c. Multiple measures emphasize how the result was achieved.

d. All of the above.

3. A balanced scorecard:

a. Emphasizes financial performance.

b. Caters to the needs of employees.

c. Tries to meet the organization’s responsibilities to stakeholders.

d. Is just a set of multiple performance measures.

4. Manufacturing cycle time is an example of a balanced-scorecard measure of:

a. Financial performance.

b. Customer perspective.

c. Internal business process.

d. Learning and growth.

5. Continuous improvement:

a. Is a philosophy of running the business.

b. Is independent of benchmarking.

c. Is looking to improve the efficiency of activities.

d. Both a and c.

6. Which of the following can be used to measure customer satisfaction?

a. Number of customer complaints

b. Number of service calls

c. Number or returns

d. All of the above

18–24

Use the following information to answer questions 7 and 8:

A manufacturing company has the following average times.

Product transportation

0.25 hour

Product manufacturing

3.5 hours

Inspection

0.25 hour

Inventory storage

10 hours

7. What is the average manufacturing cycle time (in hours)?

a. 14.00

b. 13.75

c. 13.50

d. 10.00

8. What is the manufacturing cycle efficiency?

a. 15%

b. 25%

c. 35%

d. 45%

9. Which of the following is an example of subjective measurement?

a. Economic conditions of the city where a branch is located

b. Employee turnover

c. Branch profits

d. Defect rates

10. Which of the statements regarding employee involvement is not correct?

a. When workers take on real decision-making authority, their commitment to the

organization increases.

b. When decision-making responsibility lies with workers farther away from the customer,

workers are more responsive and make informed decisions.

c. Management must create a system that conveys the organization’s objectives to all

members.

d. Management must ensure that the performance measures are applied consistently and

accurately.

11. Which of the statements is not correct?

a. People at different levels in the organization have different responsibilities.

b. At the lower levels, financial measures are critical.

c. At the middle levels, it is important to coordinate ongoing activities.

d. At the top levels, performance measures focus on meeting stakeholders’ needs.

18–25

12. Which of the following performance measures are appropriate for a regional manager?

a. Profitability

b. Employee turnover

c. Customer and employee satisfaction

d. All of the above

18–26

Multiple Choice Answers

18–27

Demonstration Problem

ChemUSA operates two highly automated chemical processing plants: East Plant and West Plant.

The same production process takes place in the two plants and turns material X into chemical

compound Y.

In order to evaluate their productivity measures, the managers of ChemUSA have the accounting

department gather comparative operating and financial data in the follow table.

East Plant

West Plant

This Year

Last Year

This Year

Last Year

Inputs:

X

30,000 lb @ $75

29,000 lb @ $73

50,000 lb @ $72

52,000 lb @ $71

Labor

4,000 h @ $15

3,740 h @$14

6,050 h @ $14

6,180 h @ $13

Overhead

$3,150,000

$2,878,000

$5,480,000

$5,672,500

Outputs:

Y

26,500 lb

24,650 lb

43,100 lb

44,200 lb

Value

$7,380,000

$6,763,500

$11,089,300

$11,428,300

Required:

Determine relevant partial productivity and total factor productivity measures for both plants and

compare the results.

Demonstration Problem – Solution

The accounting department recommends the calculation of two partial productivity measures

corresponding to the use of material input (X) and labor input (hours), respectively.

Material partial productivity = Output in pounds (lbs.) ÷ Input in pounds (lbs.)