CHAPTER 18

Financial Statement Analysis

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

Problems

1. Apply horizontal and vertical analysis

to financial statements.

1, 2, 3, 4, 5,

6, 23

1, 2, 3, 4, 5,

6, 7, 8

1

1, 2, 3, 4

1

3. Apply the concept of sustainable

20, 21, 22

14, 15

3

12, 13

8, 9

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1

Prepare vertical analysis and comment on profitability.

Simple

20–30

2

Compute ratios from balance sheet and income statement.

Simple

20–30

3

Perform ratio analysis, and evaluate financial position

and operating results.

Simple

20–30

4

Compute ratios, and comment on overall liquidity and

profitability.

Moderate

30–40

Compute numerous ratios.

7

Compute missing information given a set of ratios.

30–40

8

Prepare a statement of comprehensive income.

30–40

Prepare a statement of comprehensive income.

WEYGANDT ACCOUNTING PRINCIPLES 12E

CHAPTER 18

FINANCIAL STATEMENT ANALYSIS

Number

LO

BT

Difficulty

Time (min.)

BE1

1

C

Moderate

10–12

BE2

1, 2

K, AP

Simple

8–10

BE3

1

AP

Simple

6–8

BE4

1

AP

Simple

6–8

BE5

1

AP

Simple

4–6

BE6

1

AP

Simple

4–6

BE7

1

AP

Simple

4–6

BE8

1

AP

Simple

5–7

BE9

2

AP

Simple

4–6

BE10

2

AP

Simple

3–5

BE11

2

AN

Simple

6–8

BE12

2

AN

Moderate

6–8

BE13

2

AN

Moderate

6–8

BE14

3

AP

Simple

4–6

BE15

3

AP

Simple

3–5

DI1

1

AP

Simple

6–8

DI2

2

AP

Simple

10–12

DI3

3

AP

Simple

6–8

EX1

1

AP

Simple

10–12

EX2

1

AP

Simple

10–12

EX3

1

AP

Simple

12–15

EX4

1

AP

Simple

10–12

EX5

2

AN

Simple

8–10

EX6

2

AP

Simple

8–10

EX7

2

AP

Simple

6–8

EX8

2

AP

Simple

6–8

EX9

2

AP

Simple

6–8

EX10

2

AP

Moderate

8–10

FINANCIAL STATEMENT ANALYSIS (Continued)

Number

LO

BT

Difficulty

Time (min.)

EX11

2

AP

Simple

10–12

EX12

3

AP

Moderate

8–10

EX13

3

AP

Simple

6–8

P1

1, 2

AN

Simple

20–30

P2

2

Simple

20–30

P3

2

Simple

20–30

P4

2

AN

Moderate

30–40

P5

2

AP

Moderate

50–60

P6

2

AP

Simple

30–40

P7

2

AN

Complex

30–40

P8

3

AP

Moderate

30–40

P9

3

AP

Moderate

30–40

BYP1

1, 2

AN, E

Moderate

20–25

BYP2

1, 2

AN, E

Simple

15–20

BYP3

1, 2

AN, E

Simple

15–20

BYP4

—

AN

Simple

15–20

BYP5

2

Moderate

15–20

BYP6

1, 3

Simple

15–20

BYP7

2

Simple

10–15

BYP8

Simple

15–20

BYP9

3

AP

Simple

5–10

analysis.

BE18-2

Real-World Focus

Decision Making

Ethics Case

Q18-9

Q18-10

Q18-11

Q18-12

Q18-16

Q18-17

Q18-18

BE18-9

BE18-10

DI18-2

E18-6

E18-10

P18-2

P18-3

P18-5

BE18-13

E18-5

E18-11

P18-1

P18-4

P18-7

ANSWERS TO QUESTIONS

1. (a) Jose is not correct. There are three characteristics: liquidity, profitability, and solvency.

(b) The three parties are not primarily interested in the same characteristics of a company. Short-term

creditors are primarily interested in the liquidity of the enterprise. In contrast, long–term creditors

and stockholders are primarily interested in the profitability and solvency of the company.

2. (a) Comparison of financial information can be made on an intracompany basis, an intercompany

basis, and an industry average basis (or norms).

(1) An intracompany basis compares an item or financial relationship within a company in

3. Horizontal analysis (also called trend analysis) measures the dollar and percentage increase or

decrease of an item over a period of time. In this approach, the amount of the item on one statement

is compared with the amount of that same item on one or more earlier statements. Vertical analysis

(also called common-size analysis) expresses each item within a financial statement in terms of a

percent of a base amount.

5. A ratio expresses the mathematical relationship between one quantity and another. The relationship

is expressed in terms of either a percentage (200%), a rate (2 times), or a simple proportion (2:1).

Ratios can provide clues to underlying conditions that may not be apparent from individual financial

statement components. The ratio is more meaningful when compared to the same ratio in earlier

periods or to competitors’ ratios or to industry ratios.

6. (a) Liquidity ratios: Current ratio, acid-test ratio, accounts receivable turnover, and inventory

turnover.

Questions Chapter 18 (Continued)

9. The current ratio relates current assets to current liabilities. The acid-test ratio relates cash, short-term

investments, and net receivables to current liabilities. The current ratio includes inventory and

prepaid expenses while the acid-test ratio excludes these. The acid-test ratio provides additional

information about short-term liquidity and is an important complement to the current ratio.

12. The price earnings (P/E) ratio is a reflection of investors’ assessments of a company’s future

earnings. In this question, investors favor Microsoft because it has the higher P/E ratio. The investors

feel that Microsoft will be able to generate even higher future earnings and so the investors are

willing to pay more for the stock.

13. The payout ratio is cash dividends divided by net income. In a growth company, the payout ratio is

often low because the company is reinvesting earnings in the business.

14. (a) The increase in profit margin is good news because it means that a greater percentage of net

sales is going towards income.

(b) The decrease in inventory turnover signals bad news because it is taking the company longer

to sell the inventory and consequently there is a greater chance of inventory obsolescence.

(c) An increase in the current ratio signals good news because the company improved its ability

to meet maturing short-term obligations.

(d) The earnings per share ratio is a deceptive ratio. The decrease might be bad news to the

Questions Chapter 18 (Continued)

15.

Return on assets

(7.6%)

=

Net Income

Average Assets

16. (a) The times interest earned, which is an indication of the company’s ability to meet interest

payments, and the debt to assets ratio, which indicates the company’s ability to withstand losses

without impairing the interests of creditors.

(b) The current ratio and the acid-test ratio, which indicate a company’s liquidity and short-term

debt-paying ability.

17. Earnings per share means earnings per share of common stock. Preferred dividends are

subtracted from net income in computing EPS in order to obtain income available to common

stockholders.

18. (a) Trading on the equity means that the company has borrowed money at a lower rate of interest

than it is able to earn by using the borrowed money. Simply stated, it is using money supplied

by nonowners to increase the return to the owners.

(b) A comparison of the return on total assets with the rate of interest paid for borrowed money

indicates the profitability of trading on the equity.

19.

Net income – Preferred dividends

Weighted – average common shares outstanding

= Earnings per share

20. Discontinued operations refers to the disposal of a significant component of the business such as

the stopping of an entire activity or eliminating a major class of customers. It is important to report

discontinued operations separately from continuing operations because the discontinued component

will not affect future income statements.

Questions Chapter 18 (Continued)

22. When comparing EPS trends, discontinued operations should be omitted since they are not

reflective of normal operations. In this example, the trend is unfavorable because EPS, exclusive of

discontinued operations, has decreased from $3.20 to $2.99.

23. The following provide examples of horizontal and vertical analysis:

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 18-1

Dear Uncle Sammy,

It was so good to hear from you! I hope you and Aunt Jennie are still enjoying

your new house.

You asked some interesting questions. They relate very well to the material

that we are studying now in my financial accounting class. You said you

heard that different users of financial statements are interested in different

characteristics of companies. This is true. A short-term creditor, such as a bank,

is interested in the company’s liquidity, or ability to pay obligations as they

It is important to compare different financial statement elements to other

items. The amount of a financial statement element such as cash does not have

much meaning unless it is compared to something else. Comparisons can

be done on an intracompany basis. This basis compares an item or financial

relationship within a company for the current year to one or more previous

years. Intracompany comparisons are useful in detecting changes in financial

I hope this answers your questions. If it does not, or you have more questions,

please write me again or call. We could even meet for lunch sometime; it

would be great to see you!

Love,

Your niece (or nephew)

BRIEF EXERCISE 18-2

(a) The three tools of financial statement analysis are horizontal analysis,

vertical analysis, and ratio analysis. Horizontal analysis evaluates a series

of financial statement data over a period of time. Vertical analysis evalu-

(b) Horizontal Analysis

2016

2017

2018

Current assets

100%

105%

120%

Vertical Analysis

2016

2017

2018

Current assets*

40%

35%

39%

Ratio Analysis

2016

2017

2018

Current ratio

1.33:1

1.25:1

1.30:1

BRIEF EXERCISE 18-3

Horizontal analysis:

Increase

or (Decrease)

Dec. 31, 2017

Dec. 31, 2016

Amount

Percentage

Accounts receivable

Inventory

Total assets

$ 520,000

$ 840,000

$3,000,000

$ 400,000

$ 600,000

$2,500,000

$120,000

$240,000

$500,000

30%

40%

20%

BRIEF EXERCISE 18-4

Vertical analysis:

Dec. 31, 2017

Dec. 31, 2016

Amount

Percentage*

Amount

Percentage**

Accounts receivable

Inventory

Total assets

$ 520,000

$ 840,000

$3,000,000

17.3%

28.0%

100%

$ 400,000

$ 600,000

$2,500,000

16.0%

24.0%

100%

BRIEF EXERCISE 18-5

2018

2017

2016

Net income

$522,000

$450,000

$500,000

Increase or (Decrease)

Amount

BRIEF EXERCISE 18-6

2017

2016

Increase

Net income

$585,000

X

20%

BRIEF EXERCISE 18-6 (Continued)

1.20X = $585,000

X = $487,500

BRIEF EXERCISE 18-7

Comparing the percentages presented results in the following conclusions:

The net income for Dody increased in 2017 because of the combination of

BRIEF EXERCISE 18-8

2018

2017

2016

Sales

100.0%

100.0%

100.0%

BRIEF EXERCISE 18-9

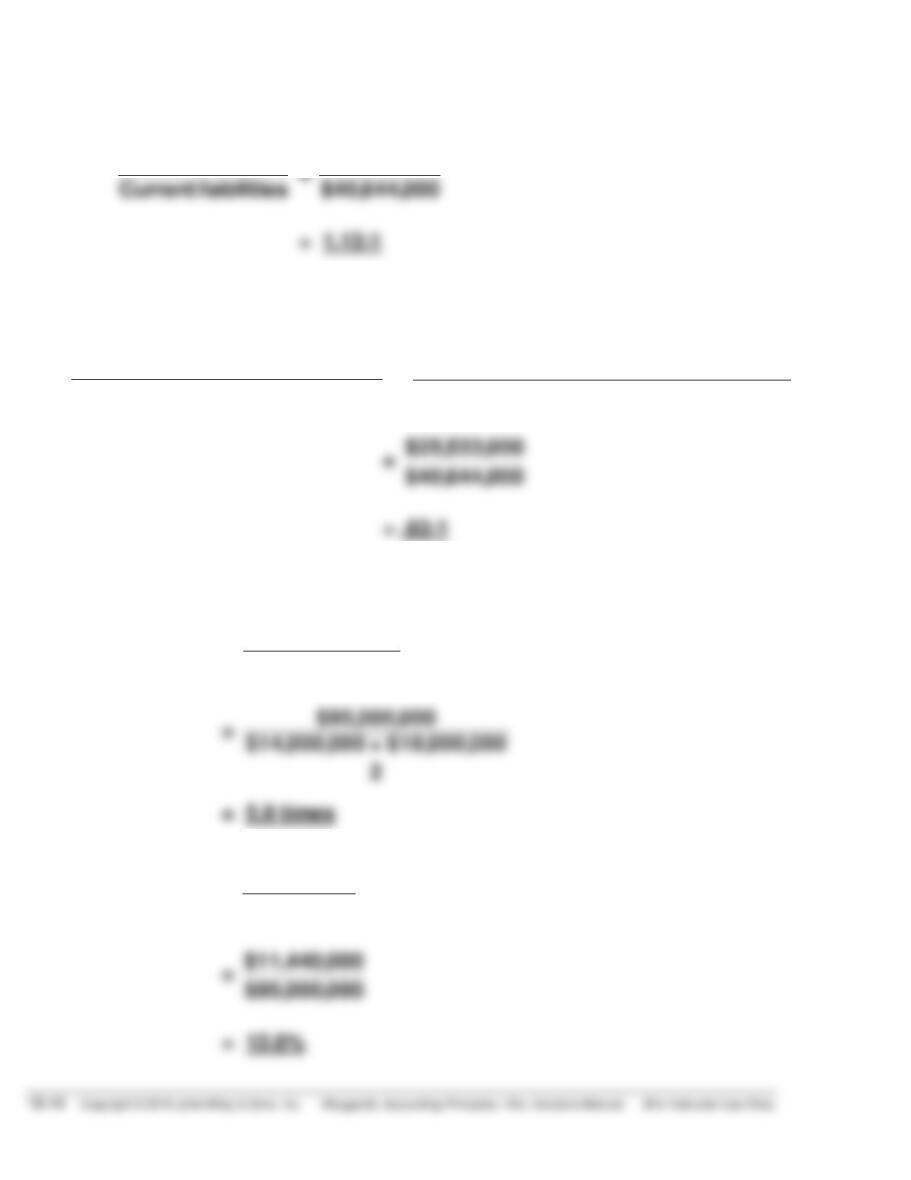

(a) Working capital = Current assets – Current liabilities

BRIEF EXERCISE 18-9 (Continued)

(b) Current ratio:

Current assets

$45,918,000

(c) Acid-test ratio:

Cash + Short–terminvestments

+ Receivables (net)

Current liabilities

=

$8,041,000 + $4,947,000 + $12,545,000

$40,644,000

BRIEF EXERCISE 18–10

(a) Asset turnover =

Net sales

Average assets

(b) Profit margin =

Net income

Net sales

BRIEF EXERCISE 18–11

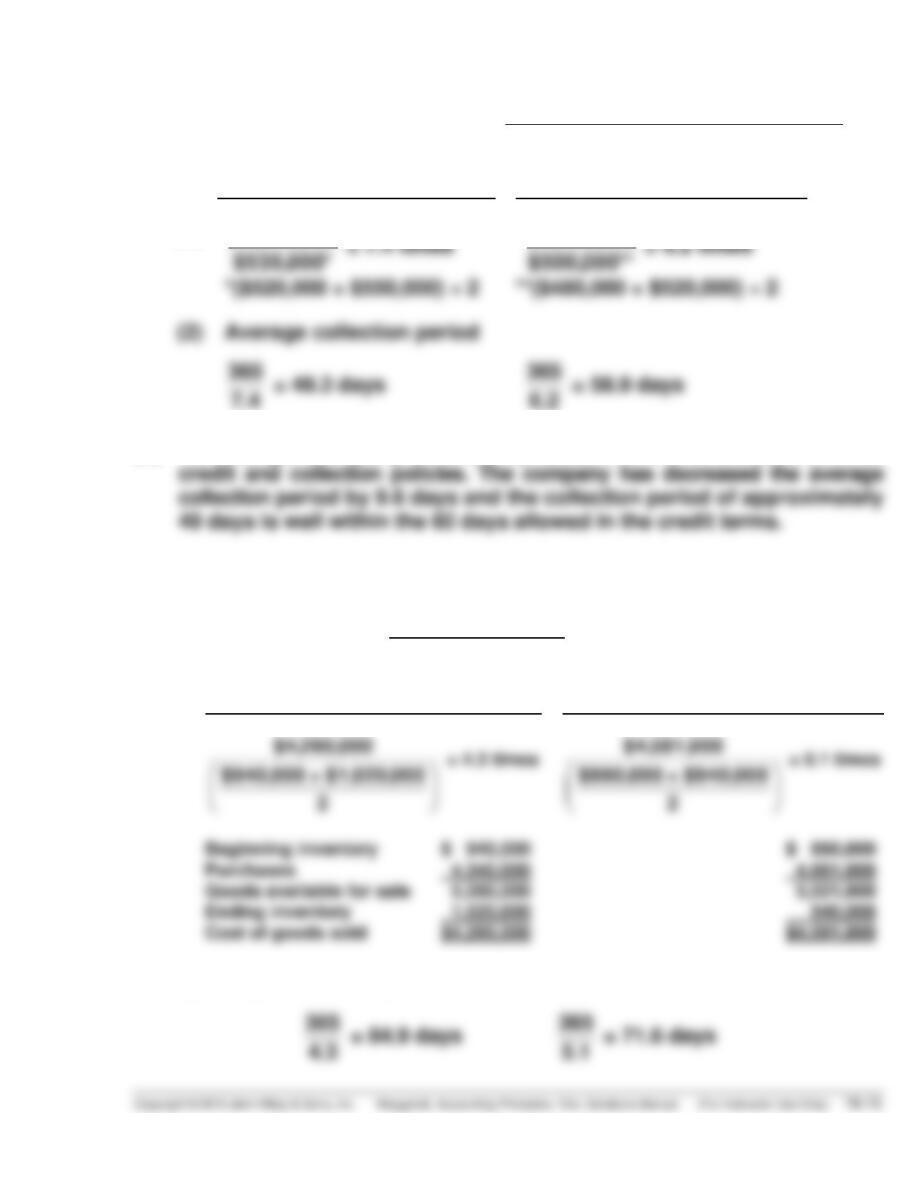

(a) Accounts Receivable turnover =

Net credit sales

Average net accounts receivable

2018

2017

(1)

*($520,000 + $550,000) ÷ 2

$3,960,000

= 7.4 times

$3,100,000

= 6.2 times

(b) Rainsberger Company should be pleased with the effectiveness of its

credit and collection policies. The company has decreased the average

BRIEF EXERCISE 18–12

(a) Inventory turnover =

Cost of goods sold

Average inventory

(1)

2017

2016

$4,260,000

$940,000 + $1,020,000

2

= 4.3 times

$4,581,000

$860,000 + $940,000

2

= 5.1 times

(2) Days in inventory

BRIEF EXERCISE 18-12 (Continued)

(b) Management should be concerned with the fact that inventory is moving

BRIEF EXERCISE 18–13

Payout ratio =

Cash dividends

Net income

Return on assets =

Net income

Average assets

BRIEF EXERCISE 18–14

SILVA CORPORATION

Partial Statement of Comprehensive Income

Income before income taxes ………………………………………………… $450,000

Income tax expense ($450,000 X 25%) …………………………………… 112,500

BRIEF EXERCISE 18–15

HOLLOWAY CORPORATION

Partial Income Statement

Loss from operations of discontinued division, net

of $60,000 income tax saving ($300,000 X 20%) ….. $240,000

SOLUTIONS FOR DO IT! REVIEW EXERCISES

DO IT! 18-1

Increase (Decrease) in 2017

Amount

Percent

Current assets $(21,000) (9.5)% [($199,000 – $220,000) ÷ $220,000]

DO IT! 18-2

2017 2016

(a) Current ratio:

$1,380 ÷ $900 = 1.53:1

$1,310 ÷ $790 = 1.66:1

(b) Inventory turnover:

$955/[($460 + $390) ÷ 2)] = 2.25 times

$890/[($390 + $340) ÷ 2)]= 2.44 times

(d) Return on assets:

$294/[($2,340 + $2,210) ÷ 2)] = 12.9%

$154/[($2,210 + $1,900) ÷ 2)] = 7.5%

(e) Return on common stockholders’ equity:

$294/[($1,030 + $1,040) ÷ 2)] = 28.4%

$154/[$1,040 + $900) ÷ 2)] = 15.9%

DO IT! 18-3

HRABIK CORPORATION

Statement of Comprehensive Income (Partial)

Income before income taxes …………………………………. $500,000

Income tax expense ……………………………………………… 100,000

Income from continuing operations ………………………. 400,000

SOLUTIONS TO EXERCISES

EXERCISE 18-1

KURZEN INC.

Condensed Balance Sheets

December 31

Increase or (Decrease)

2017

2016

Amount

Percentage

Assets

$430,000

Current assets

$125,000

$100,000

($25,000

(25.0%)

Liabilities

165,000

Current liabilities

$ 91,000

$ 70,000

($21,000)

(30.0%)

Stockholders’ Equity

Common stock, $1 par

Retained earnings

161,000

136,000

115,000

150,000

( 46,000

(14,000)

(40.0%)

(9.3%)