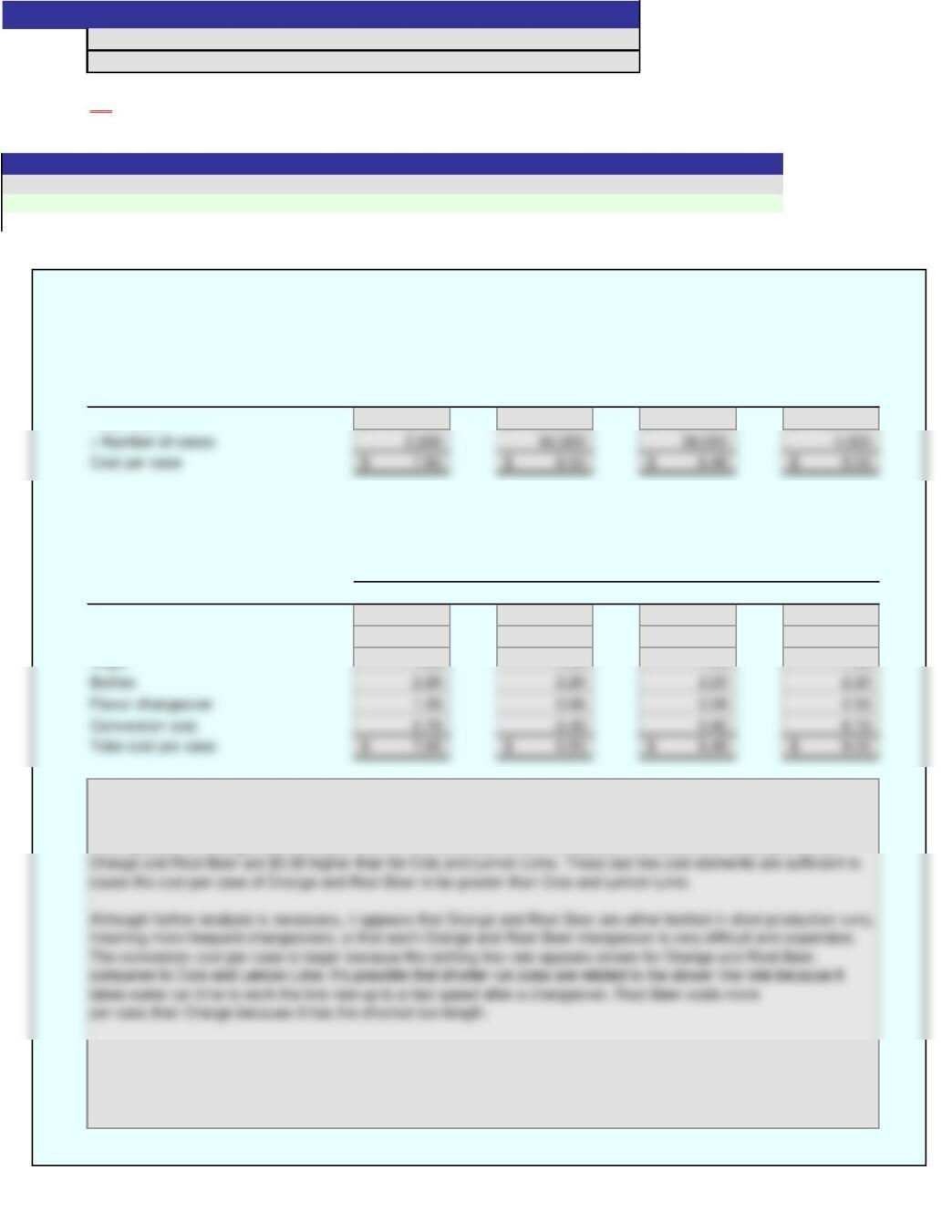

An asterisk (*) will appear to the right of an incorrect entry. The essay answer will not be graded.

Enter a zero in cells you would otherwise leave blank.

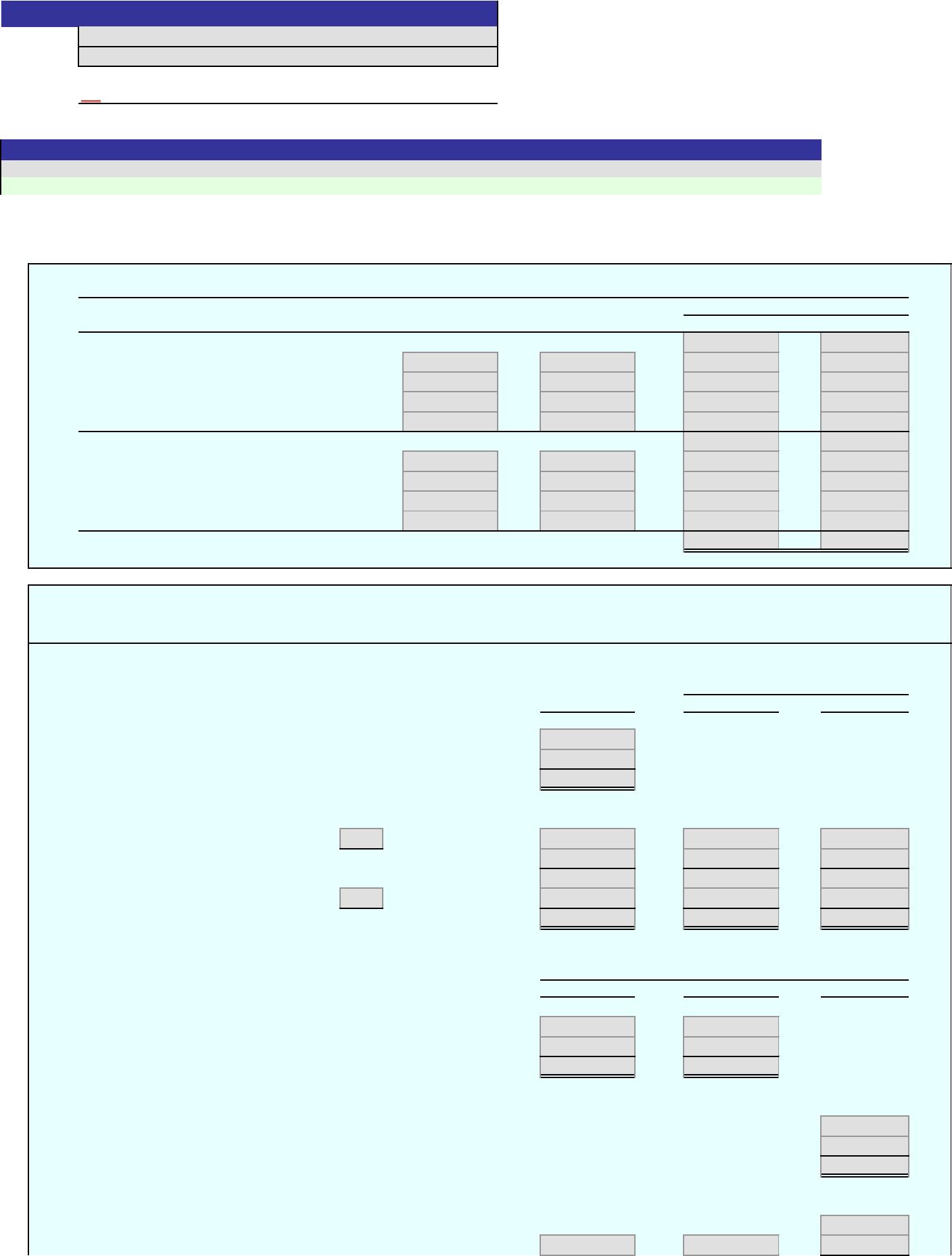

1. and 2.

Date

Debit Credit Debit Credit

Sept. 1 Bal., 2,600 units, 1/4 completed

30 Smelting Dept., 28,900 units, $16.00/unit

30 Direct labor

30 Factory overhead

30 Finished goods

Sept. 30 Bal., 2,900 units, 4/5 completed

Oct. 31 Smelting Dept., 31,000 units, $16.50/unit

31 Direct labor

31 Factory overhead

31 Finished goods

Oct. 31 Bal., 2,000 units, 2/5 completed

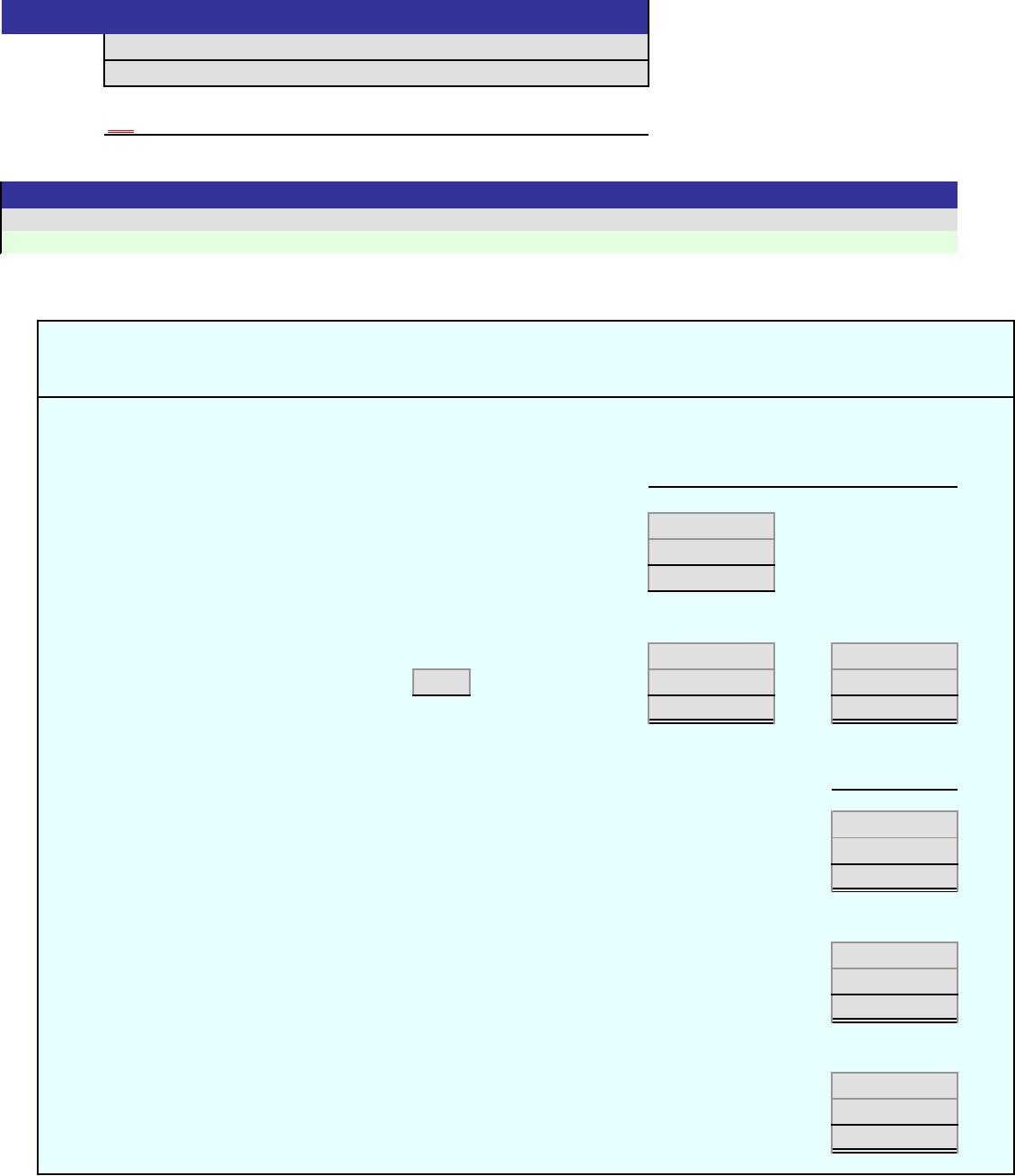

1.

UNITS

Whole Units Direct Materials Conversion

Units charged to production:

Inventory in process, Sept. 1

Received from Smelting Department

Total units accounted for by the Rolling Department

Units to be assigned cost:

Inventory in process, September 1 ( complete )

Started and completed in Sept.

Transferred to finished goods in September

Inventory in process, September 30 ( complete )

Total units to be assigned cost

COSTS

Direct Materials Conversion Total

Costs per equivalent unit:

Total costs for September in Rolling Department

Total equivalent units

Cost per equivalent unit (b)

Costs assigned to production:

Inventory in process, September 1

Costs incurred in September

Total costs accounted for by the Rolling Department

Costs allocated to completed and partially completed units:

Inventory in process, September 1 (c)

To complete inventory in process, September 1 (c)

Item

PITTSBURGH ALUMINUM COMPANY

Cost of Production Report – Rolling Department

For the Month Ended September 30, 2016

0%

[Key code here]

Answers are entered in the cells with gray backgrounds.

Score:

Key Code:

Instructions

Work in Process – Rolling Department

Balance

Equivalent Units (a)

Costs

Cells with non-gray backgrounds are protected and cannot be edited.

Problem 18(3)-4B

Name:

Section:

Cost of completed Sept. 1 work in process

Started and completed in September (c)

Transferred to finished goods in September (c)

Inventory in process, September 30 (d)

Total costs assigned by the Rolling Department

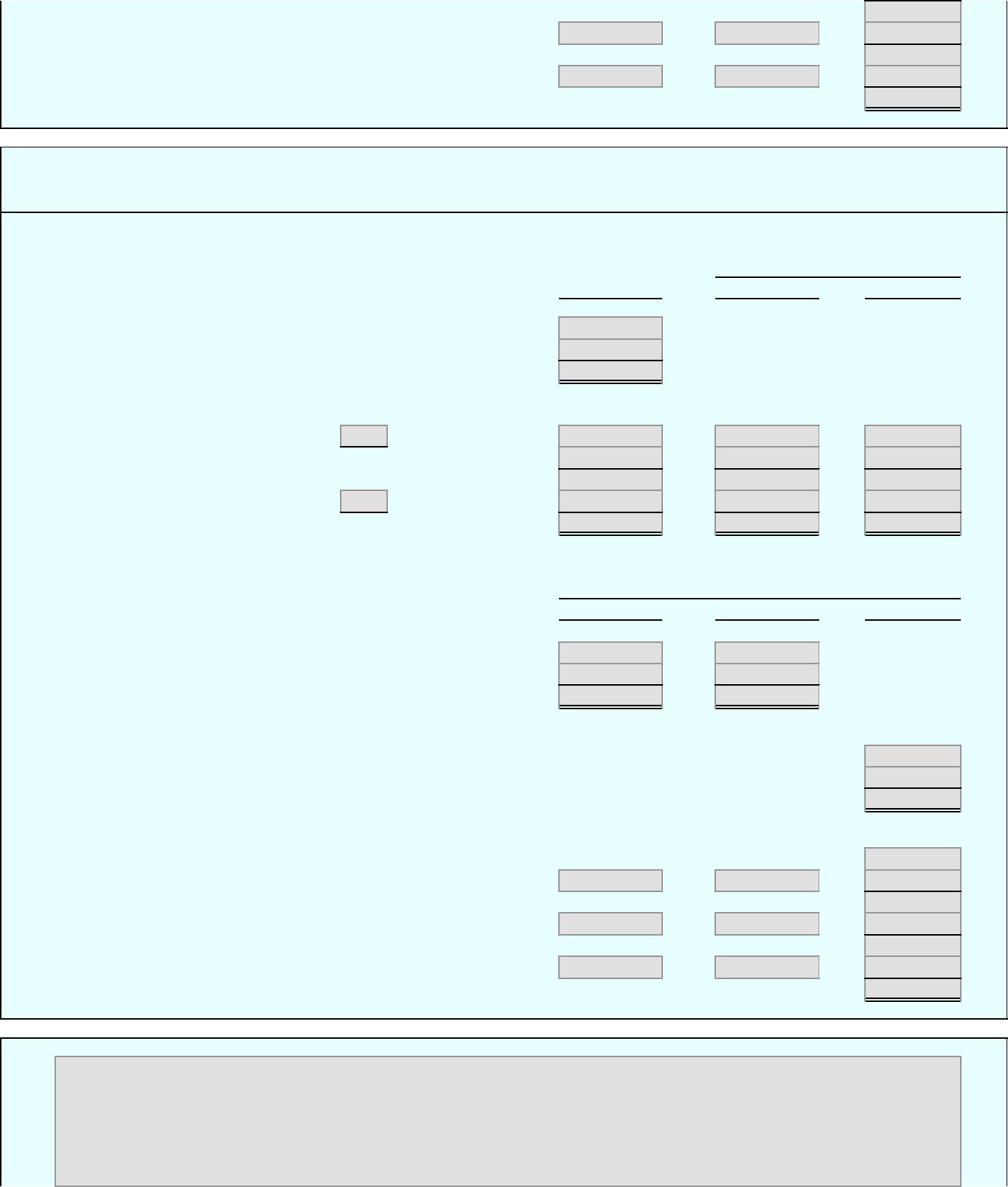

2.

UNITS

Whole Units Direct Materials Conversion

Units charged to production:

Inventory in process, October 1

Received from Smelting Department

Total units accounted for by the Rolling Department

Units to be assigned cost:

Inventory in process, October 1 ( complete )

Started and completed in October

Transferred to finished goods in October

Inventory in process, October 31 ( complete )

Total units to be assigned cost

COSTS

Direct Materials Conversion Total

Costs per equivalent unit:

Total costs for October in Rolling Department

Total equivalent units

Cost per equivalent unit (b)

Costs assigned to production:

Inventory in process, October 1

Costs incurred in October

Total costs accounted for by the Rolling Department

Costs allocated to completed and partially completed units:

Inventory in process, October 1 (c)

To complete inventory in process, October 1 (c)

Cost of completed October 1 work in process

Started and completed in October (c)

Transferred to finished goods in October (c)

Inventory in process, October 31 (d)

Total costs assigned by the Rolling Department

3.

[Key essay answer here]

PITTSBURGH ALUMINUM COMPANY

Cost of Production Report – Rolling Department

For the Month Ended October 31, 2016

Equivalent Units (a)

Costs

An asterisk (*) will appear to the right of an incorrect entry. The essay answer will not be graded.

Enter a zero in cells you would otherwise leave blank.

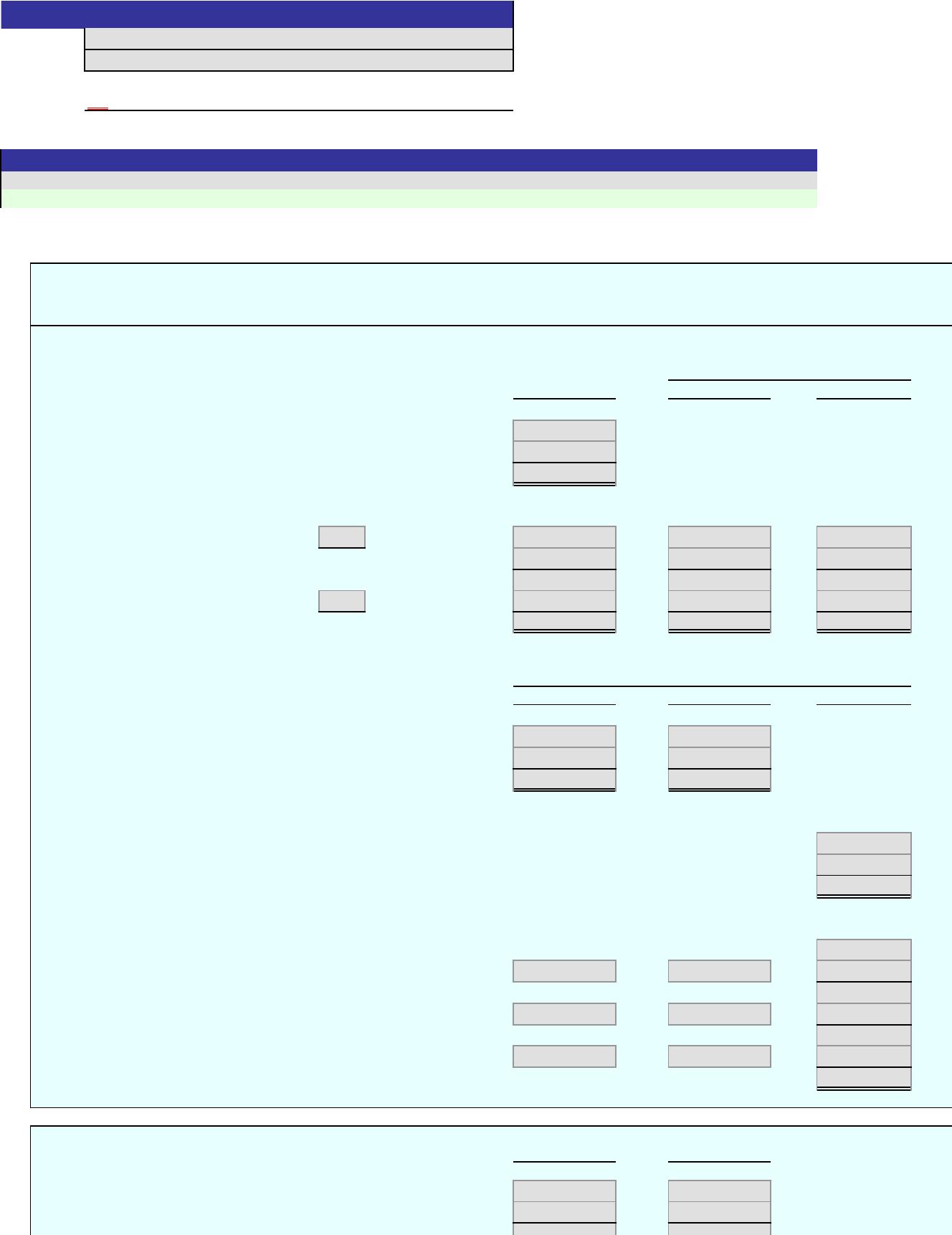

1. and 2.

Date

Debit Credit Debit Credit

Sept. 1 Bal., 2,600 units, 1/4 completed 45,825 –

30 Smelting Dept., 28,900 units, $16.00/unit

462,400 – 508,225 –

30 Direct labor 158,920 – 667,145 –

30 Factory overhead 101,402 – 768,547 –

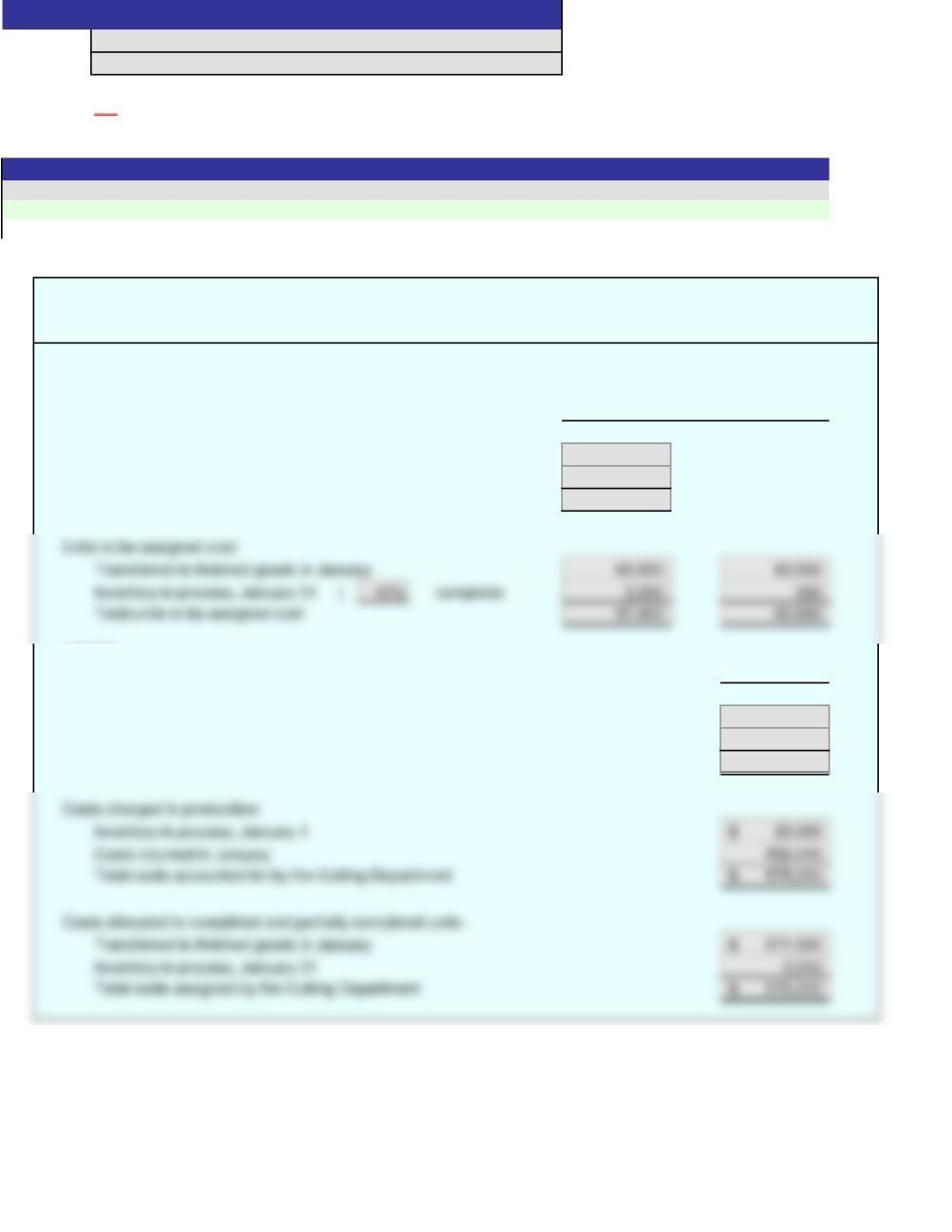

1.

UNITS

Whole Units Direct Materials Conversion

Units charged to production:

Inventory in process, Sept. 1 2,600

Received from Smelting Department 28,900

Total units accounted for by the Rolling Department 31,500

Units to be assigned cost:

COSTS

Direct Materials Conversion Total

Costs per equivalent unit:

Total costs for September in Rolling Department 462,400$ 260,322$

Costs assigned to production:

Inventory in process, September 1 45,825$

Costs incurred in September 722,722

ON

Balance

Work in Process – Rolling Department

Score:

Instructions

Cells with non-gray backgrounds are protected and cannot be edited.

Answers are entered in the cells with gray backgrounds.

Cost of Production Report – Rolling Department

For the Month Ended September 30, 2016

Item

Equivalent Units (a)

Costs

Problem 18(3)-4B

Name:

Solution

Section:

PITTSBURGH ALUMINUM COMPANY

Started and completed in September (c) 416,000 223,600 639,600

Transferred to finished goods in September (c) 702,195$

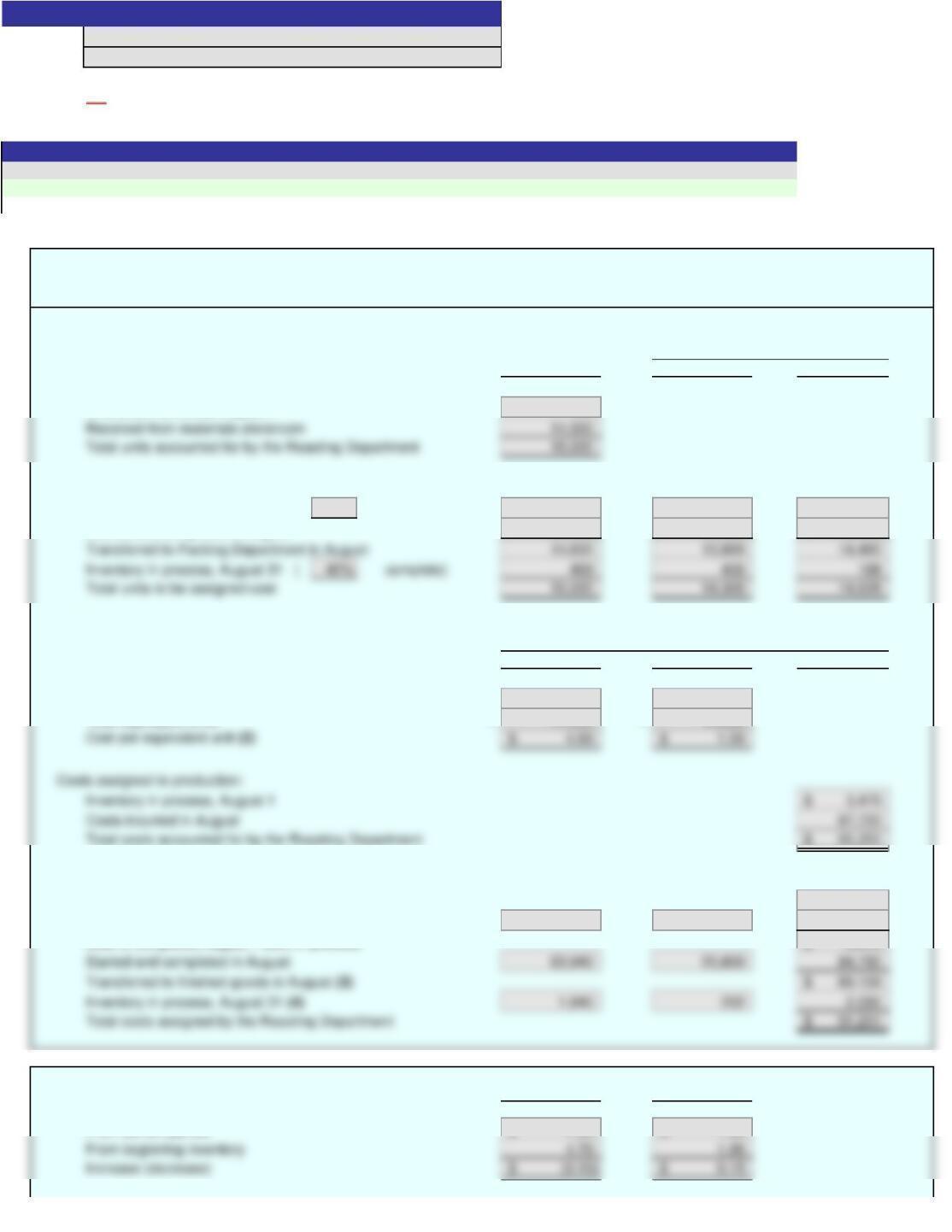

2.

UNITS

Whole Units Direct Materials Conversion

Units charged to production:

Inventory in process, October 1 2,900

Received from Smelting Department 31,000

Units to be assigned cost:

Inventory in process, October 1 ( 80% complete ) 2,900 – 580

Started and completed in October 29,000 29,000 29,000

COSTS

Direct Materials Conversion Total

Costs per equivalent unit:

Total costs for October in Rolling Department 511,500$ 267,344$

Costs assigned to production:

Inventory in process, October 1 66,352$

Costs incurred in October 778,844

Costs allocated to completed and partially completed units:

Inventory in process, October 1 (c) 66,352$

To complete inventory in process, October 1 (c) –$ 5,104$ 5,104

Cost of completed October 1 work in process 71,456$

3.

Equivalent Units (a)

The cost per equivalent unit for direct materials increased from $15.50 in August to $16.00 in September to $16.50 in October. The cost

Costs

PITTSBURGH ALUMINUM COMPANY

Cost of Production Report – Rolling Department

For the Month Ended October 31, 2016

An asterisk (*) will appear to the right of an incorrect entry.

UNITS

Equivalent Units

Whole Units of Production

Units to account for during production:

Inventory in process, December 1

Received from materials storeroom

Total units account for by the Roasting Department

Units to be assigned cost:

Transferred to Packing Department in December

Inventory in process, December 31 ( complete)

Total units to be assigned cost

COSTS

Costs

Unit costs:

Total costs for December in Roasting Department

Total equivalent units

Cost per equivalent unit

Costs charged to production:

Inventory in process, December 1

Costs incurred in December

Total costs accounted for by the Roasting Department

Costs allocated to completed and partially completed units:

Transferred to Packing Department in December

Inventory in process, December 31

Total costs assigned by the Roasting Department

Instructions

Cells with non-gray backgrounds are protected and cannot be edited.

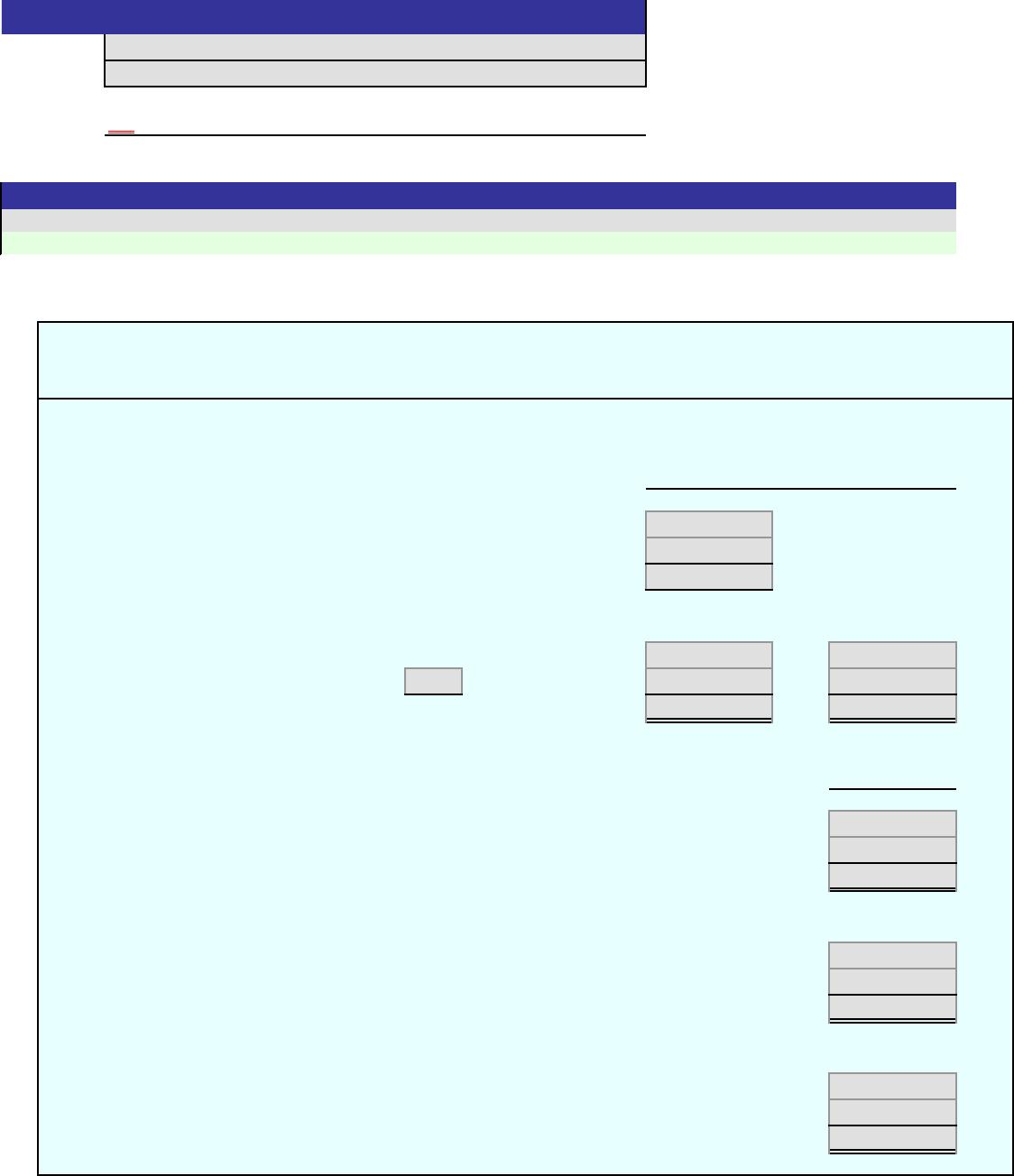

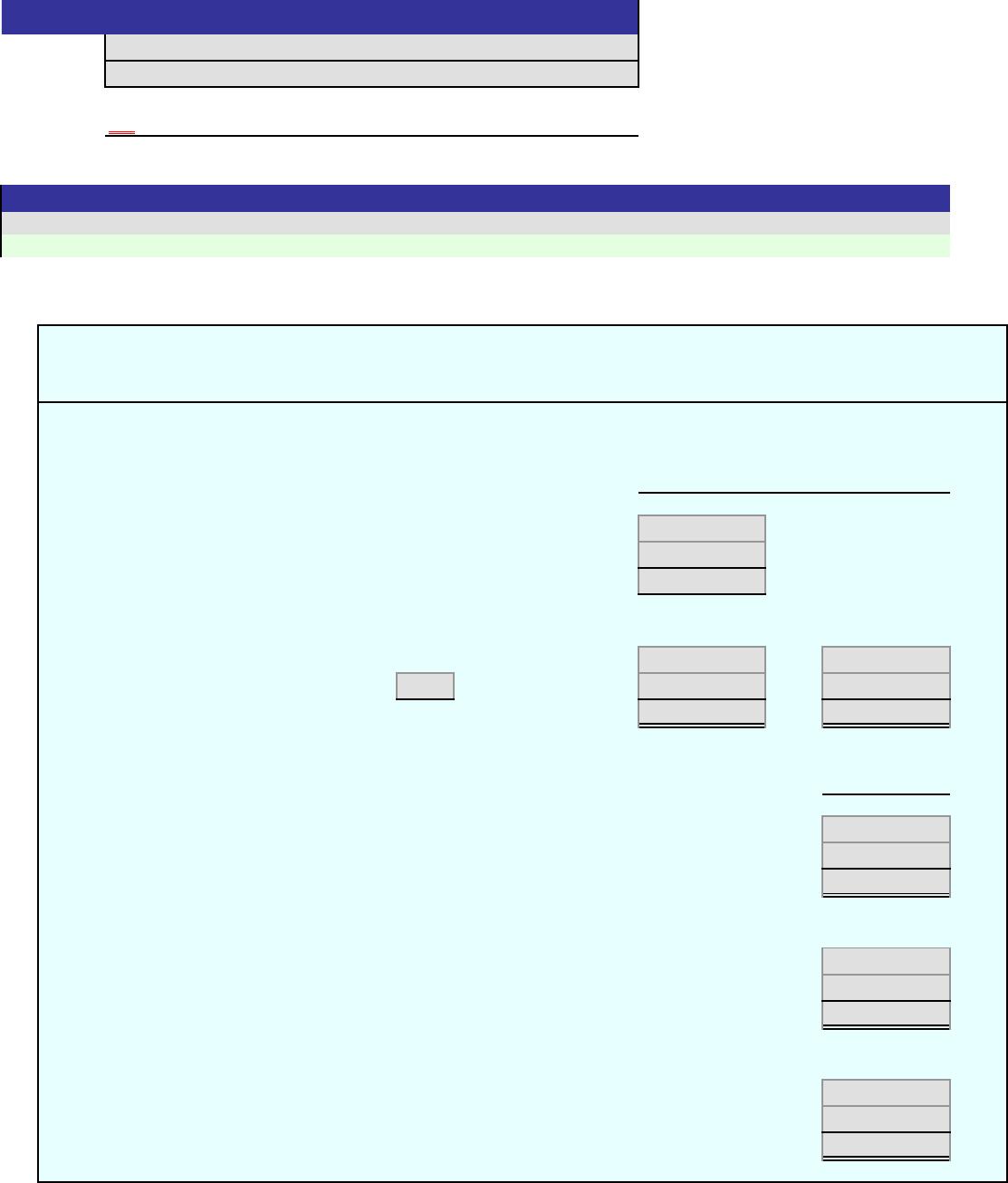

SUNRISE COFFEE COMPANY

For the Month Ended December 31, 2016

Cost of Production Report – Roasting Department

Answers are entered in the cells with gray backgrounds.

0%

[Key code here]

Problem 18(3)-5A

Name:

Section:

Score:

Key Code:

An asterisk (*) will appear to the right of an incorrect entry.

UNITS

Equivalent Units

Whole Units of Production

Units to account for during production:

Inventory in process, December 1 10,500

COSTS

Costs

Unit costs:

Total costs for December in Roasting Department 572,130$

Total equivalent units

211,900

Costs allocated to completed and partially completed units:

Transferred to Packing Department in December 564,030$

Answers are entered in the cells with gray backgrounds.

ON

Cost of Production Report – Roasting Department

For the Month Ended December 31, 2016

SUNRISE COFFEE COMPANY

Problem 18(3)-5A

Name:

Solution

Section:

Score:

Instructions

Cells with non-gray backgrounds are protected and cannot be edited.

Units to be assigned cost:

An asterisk (*) will appear to the right of an incorrect entry.

UNITS

Equivalent Units

Whole Units of Production

Units to account for during production:

Inventory in process, May 1

Received from Milling Department

Total units account for by the Sifting Department

Units to be assigned cost:

Transferred to Packaging Department in May

Inventory in process, May 31 ( complete)

Total units to be assigned cost

COSTS

Costs

Unit costs:

Total costs for May in Sifting Department

Total equivalent units

Cost per equivalent unit

Costs charged to production:

Inventory in process, May 1

Costs incurred in May

Total costs accounted for by the Sifting Department

Costs allocated to completed and partially completed units:

Transferred to Packaging Department in May

Inventory in process, May 31

Total costs assigned by the Sifting Department

Instructions

Cells with non-gray backgrounds are protected and cannot be edited.

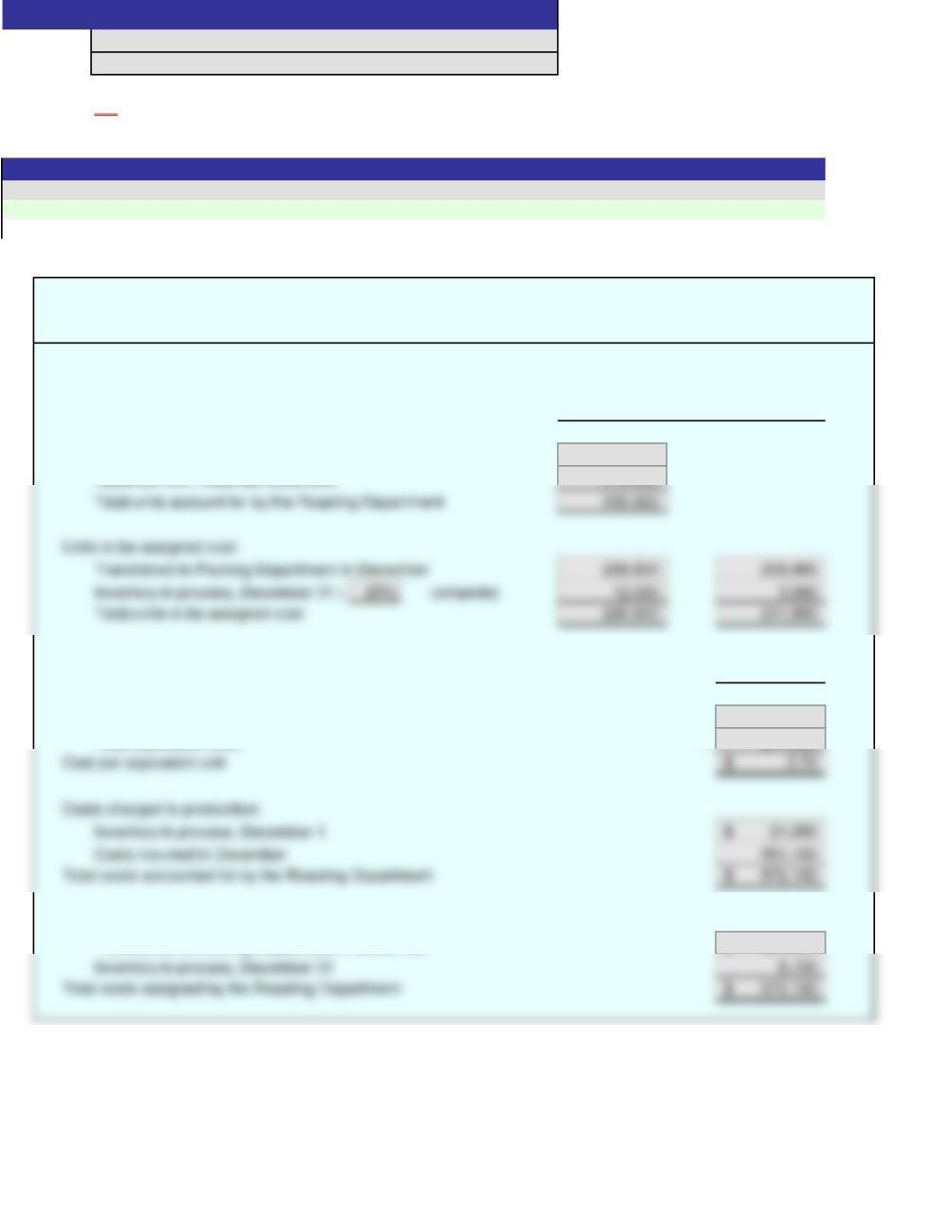

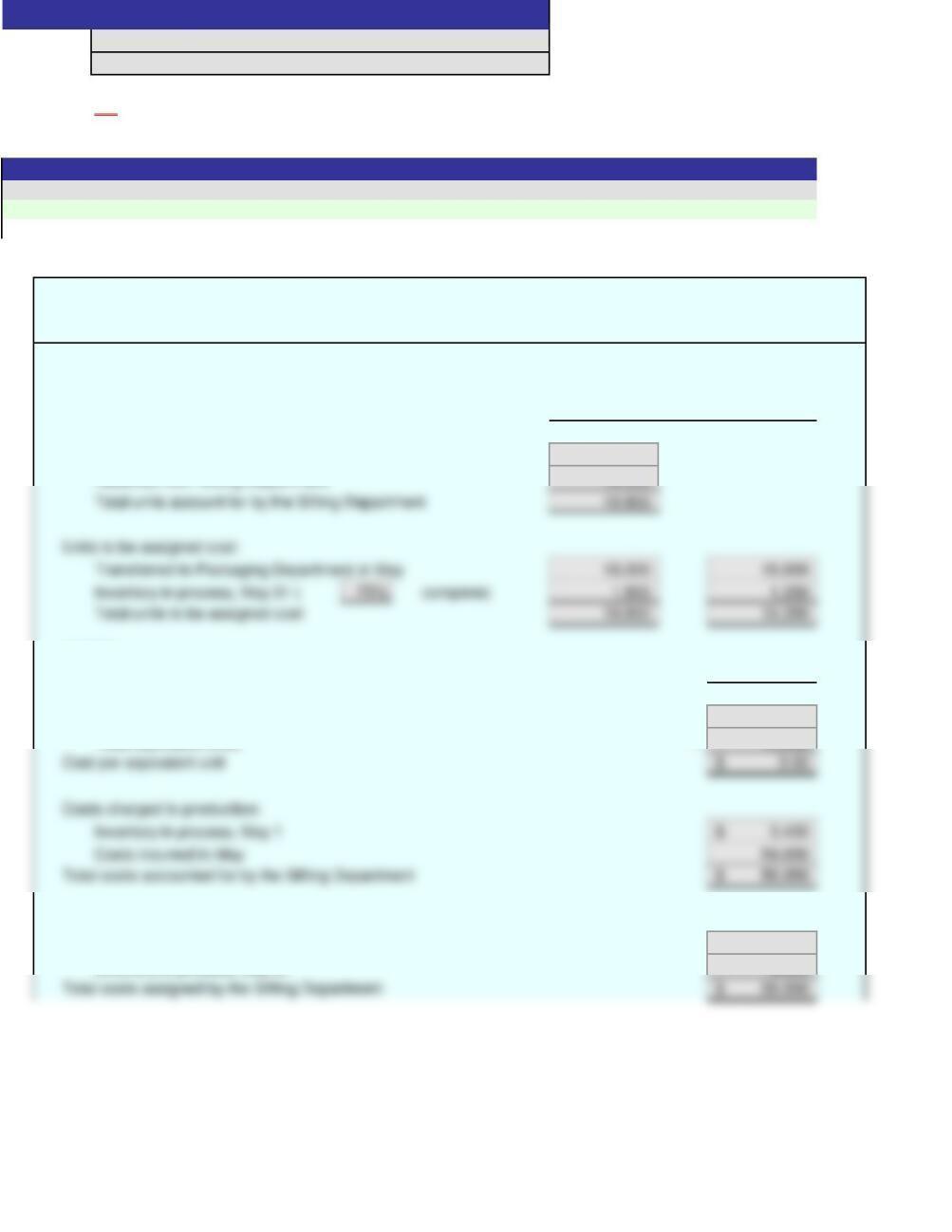

BLUE RIBBON FLOUR COMPANY

For the Month Ended May 31, 2016

Cost of Production Report – Sifting Department

Answers are entered in the cells with gray backgrounds.

0%

[Key code here]

Problem 18(3)-5B

Name:

Section:

Score:

Key Code:

An asterisk (*) will appear to the right of an incorrect entry.

UNITS

Equivalent Units

Whole Units of Production

Units to account for during production:

Inventory in process, May 1 1,500

Received from Milling Department 18,300

COSTS

Costs

Unit costs:

Total costs for May in Sifting Department 58,050$

Total equivalent units

19,350

Costs allocated to completed and partially completed units:

Transferred to Packaging Department in May 54,000$

Inventory in process, May 31 4,050

Answers are entered in the cells with gray backgrounds.

ON

Cost of Production Report – Sifting Department

For the Month Ended May 31, 2016

BLUE RIBBON FLOUR COMPANY

Problem 18(3)-5B

Name:

Solution

Section:

Score:

Instructions

Cells with non-gray backgrounds are protected and cannot be edited.

Units to be assigned cost:

An asterisk (*) will appear to the right of an incorrect entry.

Enter a zero in cells you would otherwise leave blank.

a.

Units in process at beginning of period

Units placed in production during period

Less units finished during period

Units in process at beginning of period

b. Percent

Completed

This Period Whole Units Direct Materials Conversion

Inventory in process, beginning

Started and completed

Transferred to finished goods

Inventory in process, ending

Total units

c.

Direct Materials Conversion

Total costs for period in Assembly Department

Divided by total equivalent units (from above)

Cost per equivalent unit

d.

Cost of the units started and completed during the period:

Direct materials unit cost

Conversion unit cost

Total unit cost

x Units started and completed

Cost of units started and completed

Cells with non-gray backgrounds are protected and cannot be edited.

[Key code here]

Answers are entered in the cells with gray backgrounds.

Score:

Key Code:

Costs

Instructions

Equivalent Units

Exercise 18(3)-11

Name:

Section:

0%

An asterisk (*) will appear to the right of an incorrect entry.

Enter a zero in cells you would otherwise leave blank.

a.

Units in process at beginning of period 1,600

Units placed in production during period 29,000

b. Percent

Completed

This Period Whole Units Direct Materials Conversion

Inventory in process, beginning 65% 1,600 01,040

Started and completed 28,000 28,000 28,000

c.

Direct Materials Conversion

Total costs for period in Assembly Department 275,500$ 123,858$

d.

Cost of the units started and completed during the period:

Direct materials unit cost 9.50$

Conversion unit cost 4.20

Score:

Instructions

Answers are entered in the cells with gray backgrounds.

Equivalent Units

Costs

ON

Exercise 18(3)-11

Name:

Solution

Section:

Cells with non-gray backgrounds are protected and cannot be edited.

An asterisk (*) will appear to the right of an incorrect entry. The essay answer will not be graded.

Enter a zero in cells you would otherwise leave blank.

(a)

UNITS

Whole Units Direct Materials Conversion

Units charged to production:

Inventory in process, August 1

Received from materials storeroom

Total units accounted for by the Roasting Department

Units to be assigned cost:

Inventory in process, August 1 ( complete)

Started and completed in August

Transferred to Packing Department in August

Inventory in process, August 31 ( complete)

Total units to be assigned cost

COSTS

Direct Materials Conversion Total

Costs per equivalent unit:

Total costs for August in Roasting Department

Total equivalent units

Cost per equivalent unit (2)

Costs assigned to production:

Inventory in process, August 1

Costs incurred in August

Total costs accounted for by the Roasting Department

Costs allocated to completed and partially completed units:

Inventory in process, August 1

To complete inventory in process, August 1

Cost of completed August 1 work in process

Started and completed in August

Transferred to finished goods in August (3)

Inventory in process, August 31 (4)

Total costs assigned by the Roasting Department

(b)

Direct Materials Conversion

Cost per equivalent unit:

From current period

From beginning inventory

Increase (decrease)

MORNING BREW COFFEE COMPANY

Cost of Production Report – Roasting Department

For the Month Ended August 31, 2016

[Key code here]

Answers are entered in the cells with gray backgrounds.

Score:

Key Code:

Instructions

Cells with non-gray backgrounds are protected and cannot be edited.

Exercise 18(3)-16

Name:

Section:

(1) Equivalent Units

Costs

0%

Evaluation comments:

[Key essay answer here]

An asterisk (*) will appear to the right of an incorrect entry. The essay answer will not be graded.

Enter a zero in cells you would otherwise leave blank.

(a)

UNITS

Whole Units Direct Materials Conversion

Units charged to production:

Inventory in process, August 1 700

Units to be assigned cost:

Inventory in process, August 1 ( 20% complete) 700 – 560

Started and completed in August 13,900 13,900 13,900

COSTS

Direct Materials Conversion Total

Costs per equivalent unit:

Total costs for August in Roasting Department 65,780$ 21,942$

Total equivalent units

14,300 14,628

Costs allocated to completed and partially completed units:

Inventory in process, August 1 3,479$

To complete inventory in process, August 1 –$ 840$ 840

Cost of completed August 1 work in process 4,319$

(b)

Direct Materials Conversion

Cost per equivalent unit:

From current period 4.60$ 1.50$

For the Month Ended August 31, 2016

Exercise 18(3)-16

Name:

Solution

Section:

(1) Equivalent Units

Costs

MORNING BREW COFFEE COMPANY

Cost of Production Report – Roasting Department

Instructions

Cells with non-gray backgrounds are protected and cannot be edited.

Answers are entered in the cells with gray backgrounds.

ON

Score:

Evaluation comments:

An asterisk (*) will appear to the right of an incorrect entry. The essay portion will not be graded.

MEMO

To: Production Manager

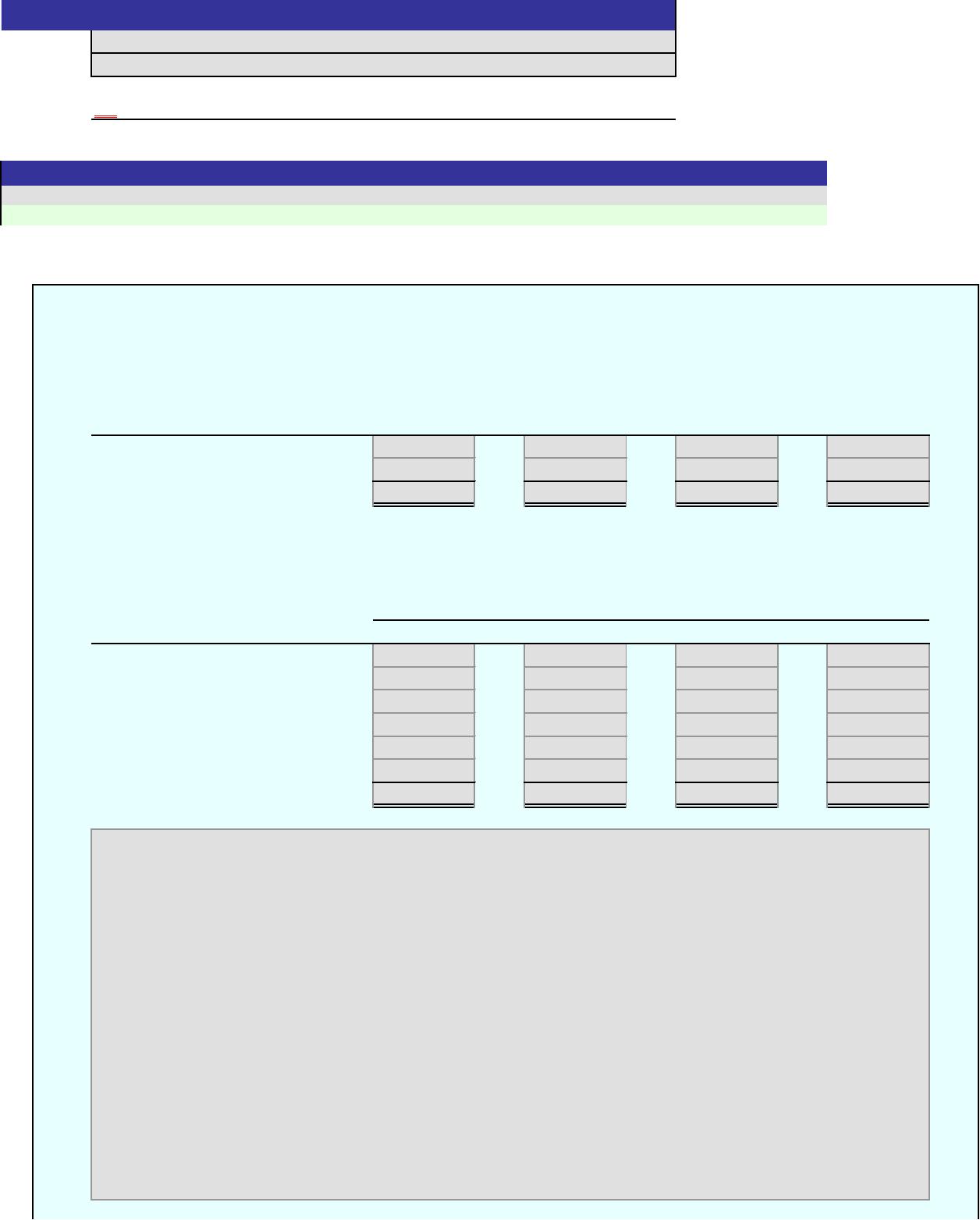

The cost of production report was used to identify the cost per case for each of the four flavors as shown below.

Orange Cola Lemon-Lime Root Beer

Total cases

Number of cases

Cost per case

Orange Cola Lemon-Lime Root Beer

Concentrate

Water

Sugar

Bottles

Flavor changeover

Conversion cost

Total cost per case

Score:

Key Code:

As can be seen, the cost per case of Root Beer is significantly above the cost per case of the other three flavors. A

more detailed analysis is necessary to understand the causes of this difference. The individual cost elements that

determine the total cost can be divided by the number of cases. This analysis is provided below.

Cells with non-gray backgrounds are protected and cannot be edited.

[Key code here]

Answers are entered in the cells with gray backgrounds.

Cost per Case by Cost Element

[Key conclusion of memo here]

Instructions

Exercise 18(3)-21

Name:

Section:

0%

An asterisk (*) will appear to the right of an incorrect entry. The essay portion will not be graded.

MEMO

To: Production Manager

The cost of production report was used to identify the cost per case for each of the four flavors as shown below.

Orange Cola Lemon-Lime Root Beer

Total cases 19,125$ 391,800$ 324,000$ 36,000$

Orange Cola Lemon-Lime Root Beer

Concentrate 1.85$ 2.15$ 2.10$ 1.90$

Water 0.50 0.50 0.50 0.50

Sugar 1.20 1.20 1.20 1.20

Cost per Case by Cost Element

Answers are entered in the cells with gray backgrounds.

ON

As can be seen, the cost per case of Root Beer is significantly above the cost per case of the other three flavors. A

more detailed analysis is necessary to understand the causes of this difference. The individual cost elements that

determine the total cost can be divided by the number of cases. This analysis is provided below.

Exercise 18(3)-21

Name:

Solution

Section:

The table above indicates that the concentrate per case is actually less for Orange and Root Beer than for Cola and

Lemon-Lime. This is because the concentrate supplier charges a higher price for the more popular flavors. The costs

per case for water, sugar, and bottles are the same for each flavor. However, the costs per case for changeover are

much greater for Orange and Root Beer than for the other two flavors. In addition, the conversion costs per unit for

Cells with non-gray backgrounds are protected and cannot be edited.

Instructions

Score:

An asterisk (*) will appear to the right of an incorrect entry.

a. and b.

Equivalent

Percent Units of

Complete Whole Units Production

Units to be accounted for:

Beginning work in process

Units started during the period

Total

Units to be assigned costs:

Transferred to finished goods

Inventory in process, ending

Total units

c.

Cost per equivalent unit:

Total production costs

Divided by total equivalent units (from above)

Cost per equivalent unit

d.

Cost of units transferred to Finished Goods:

Units transferred

x Cost per equivalent unit

Cost of units transferred

e.

Cost of units in ending Work in Process:

Equivalent units in process, ending (from above)

x Cost per equivalent unit

Cost of units remaining in process

0%

Exercise 18(3)-27

Name:

Section:

Cells with non-gray backgrounds are protected and cannot be edited.

[Key code here]

Answers are entered in the cells with gray backgrounds.

Score:

Key Code:

Instructions

An asterisk (*) will appear to the right of an incorrect entry.

Enter a zero in cells you would otherwise leave blank.

a. and b.

Equivalent

Percent Units of

Complete Whole Units Production

Units to be accounted for:

Beginning work in process 900

Units started during the period 8,400

c.

Cost per equivalent unit:

Total production costs 61,740$

Divided by total equivalent units (from above) 8,820

Exercise 18(3)-27

Name:

Solution

Section:

Cells with non-gray backgrounds are protected and cannot be edited.

Score:

Instructions

Answers are entered in the cells with gray backgrounds.

ON

An asterisk (*) will appear to the right of an incorrect entry.

UNITS

Equivalent Units

Whole Units of Production

Units charged to production:

Inventory in process, January 1

Received from Weaving Department

Total units account for by the Cutting Department

Units to be assigned cost:

Transferred to finished goods in January

Inventory in process, January 31 ( complete)

Total units to be assigned cost

COSTS

Costs

Unit costs:

Total costs for January in Cutting Department

Total equivalent units

Cost per equivalent unit

Costs charged to production:

Inventory in process, January 1

Costs incurred in January

Total costs accounted for by the Cutting Department

Costs allocated to completed and partially completed units:

Transferred to finished goods in January

Inventory in process, January 31

Total costs assigned by the Cutting Department

Instructions

Cells with non-gray backgrounds are protected and cannot be edited.

DALTON CARPET COMPANY

For the Month Ended January 31, 2016

Cost of Production Report – Cutting Department

Answers are entered in the cells with gray backgrounds.

0%

[Key code here]

Exercise 18(3)-30

Name:

Section:

Score:

Key Code:

An asterisk (*) will appear to the right of an incorrect entry.

UNITS

Equivalent Units

Whole Units of Production

Units charged to production:

Inventory in process, January 1 3,400

Received from Weaving Department 64,000

Total units account for by the Cutting Department 67,400

COSTS

Costs

Unit costs:

Total costs for January in Cutting Department

575,010$

Total equivalent units 63,890

Cost per equivalent unit 9.00$

Answers are entered in the cells with gray backgrounds.

ON

Cost of Production Report – Cutting Department

For the Month Ended January 31, 2016

DALTON CARPET COMPANY

Exercise 18(3)-30

Name:

Solution

Section:

Score:

Instructions

Cells with non-gray backgrounds are protected and cannot be edited.