1. Financial accounting and managerial accounting are different in several ways. Financial

accounting information is reported in statements that are useful to persons or groups outside

a company. These statements objectively report the results of operations for fixed periods of

time and the financial condition of the business under generally accepted accounting principles.

Managerial accounting information uses both subjective and objective information to meet the

specific needs of management. This non-GAAP information can be reported periodically or as

needed by management and can be reported for the entire entity or for segments of the organization.

This information includes (1) historical data, which provide objective measures of past operations,

and (2) estimated data, which provide subjective estimates about future decisions.

3. Direct materials cos

t

4. Prime costs are the combination of direct materials and direct labor costs, while conversion

costs are the combination of direct labor costs and factory overhead costs.

6. The three inventory accounts for a manufacturing business are as follows:

a. Finished goods inventory consists of completed (or finished) products that have not been sold.

b. Work in process inventory consists of the direct materials, direct labor, and factory overhead

costs for products that have entered the manufacturing process but are not yet completed.

c. Materials inventory consists of the costs of the direct and indirect materials that have not

entered the manufacturing process.

7. Finished goods, work in process, and materials

8. The cost of finished goods and the cost of work in process included the following:

a. Direct materials—the costs of materials that enter directly into the finished product

b. Direct labor—the wages of factory workers who convert materials into a finished product

c. Factory overhead—the costs, other than direct materials and direct labor, that are incurred in

the manufacturing process

CHAPTER 18

INTRODUCTION TO MANAGERIAL ACCOUNTING

DISCUSSION QUESTIONS

CHAPTER 18 Introduction to Managerial Accounting

PE 18-1A

Controlling (a)

Planning (c)

Decision making (b)

PE 18-1B

PE 18-2A

a. DL

b. FO

c. DM

d. FO

PE 18-2B

a. DM (or FO if the cost is immaterially small)

PE 18-3A

a. B

b. C

c. P

d. C

PE 18-3B

a. P

PRACTICE EXERCISES

CHAPTER 18 Introduction to Managerial Accounting

PE 18-4A

a. Product cost

b. Product cost

c. Period cost

d. Period cost

PE 18-4B

a. Period cost

PE 18-5A

a. Work in process inventory, May 1………………………………

…

$ 72,100

Cost of direct materials used in production…………………

…

$17,300

Direct labor…………………………………………………………

…

44,700

Factory overhead…………………………………………………

…

28,800

Total manufacturing costs incurred during May……………

…

90,800

Total manufacturing costs………………………………………

…

$162,900

Less work in process inventory, May 31………………………

…

76,400

Cost of goods manufactured……………………………………

…

$ 86,500

…

…

PE 18-5B

a. Work in process inventory, November 1………………………

…

$ 59,600

Cost of direct materials used in production…………………

…

$230,700

Direct labor…………………………………………………………

…

267,000

Factory overhead…………………………………………………

…

155,800

Total manufacturing costs incurred during November……

…

653,500

Total manufacturing costs………………………………………

…

$713,100

Less work in process inventory, November 30………………

…

63,300

Cost of goods manufactured……………………………………

…

$649,800

CHAPTER 18 Introduction to Managerial Accounting

Ex. 18-1

a. Direct materials cost e. Factory overhead cost

b. Direct materials cost f. Direct materials cost

Ex. 18-2

a. Direct materials cost f. Factory overhead cost

b. Direct materials cost g. Direct materials cost

Ex. 18-3

a, b, d, f, g

Ex. 18-4

a. Period cost j. Period cost

b. Product cost k. Product cost

c. Product cost l. Product cost

Ex. 18-5

a. period e. work in process inventory

b. improve f. conversion

EXERCISES

CHAPTER 18 Introduction to Managerial Accounting

Ex. 18-6

a. improving e. strategic

b. conversion f. materials inventory

Ex. 18-7

a. direct g. indirect

b. indirect h. indirect

c. direct i. indirect

Ex. 18-8

1. c., 2. d., 3. b., 4. a.

Ex. 18-9

1. The maintenance salaries of $84,400 and indirect materials of $56,200 should be

included as factory overhead.

2. The factory overhead incorrectly includes the following items: sales salaries of

$348,750, promotional expenses of $315,000, corporate office insurance and

Cost of direct materials used in production $ 551,300

Direct labor 478,100

Factory overhead:

Maintenance salaries $ 84,400

Marching Ants Inc.

Manufacturing Costs

For the Quarter Ended June 30

CHAPTER 18 Introduction to Managerial Accounting

Ex. 18-10

a.

Revenues $742,000

Cost of goods sold 445,200

Gross profit $296,800

b. Inventory balances on January 31:

Materials ($142,900 – $126,600)………………………………………………… $16,300

Ex. 18-11

Current assets:

Cash $ 243,400

Accounts receivable 505,700

Inventories:

Upper Crust Company

Balance Sheet

August 31

Technology Treasures Manufacturing Company

Income Statement

For the Month Ended January 31

CHAPTER 18 Introduction to Managerial Accounting

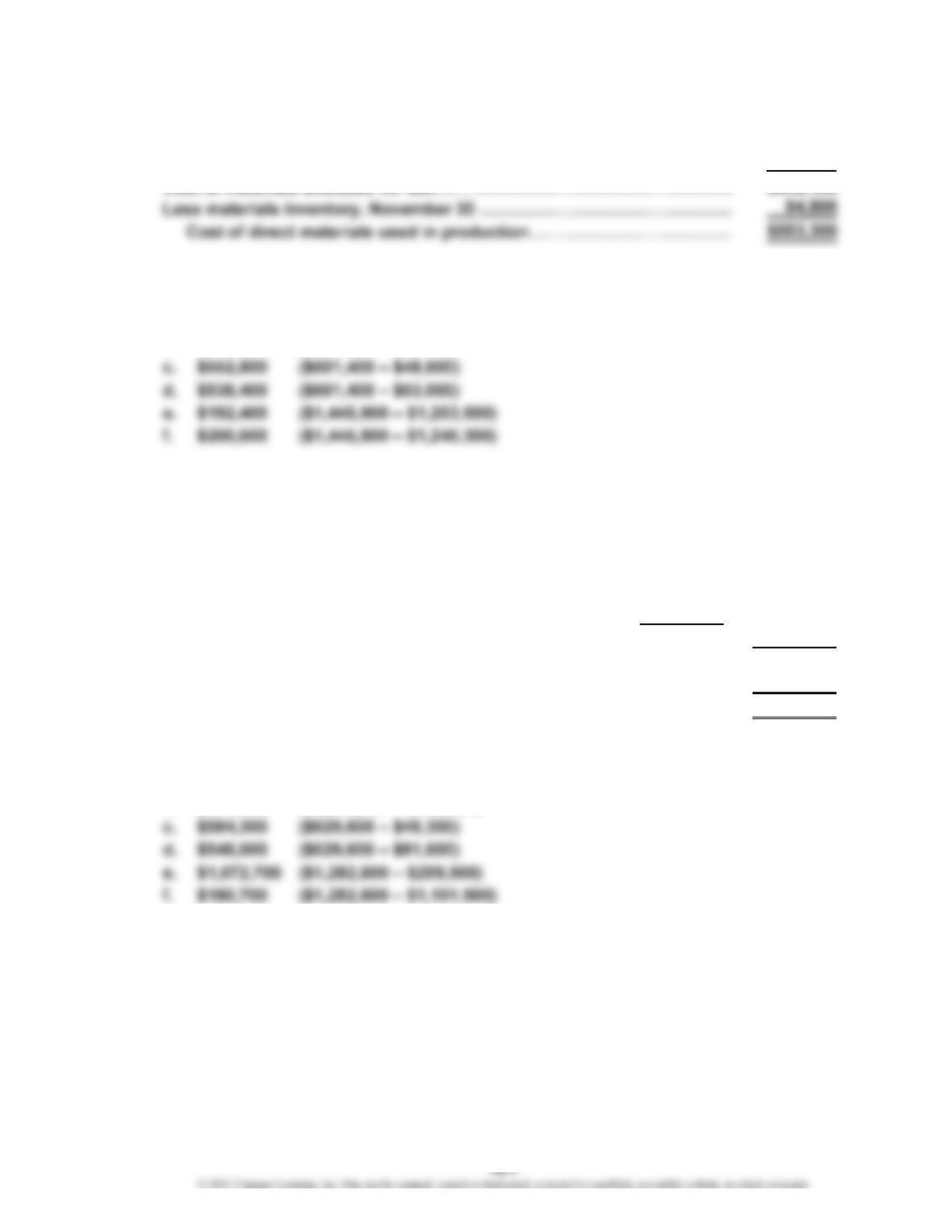

Ex. 18-12

Materials inventory, November 1………………………………………………

…

$ 75,700

Purchases…………………………………………………………………………

…

572,400

Ex. 18-13

a. $410,900 ($22,900 + $388,000)

b. $383,500 ($410,900 – $27,400)

Ex. 18-14

Work in process inventory, July 1……………………………

…

$ 316,400

Add manufacturing costs incurred during July:

Cost of direct materials used ……………………………

…

$1,150,000

Direct labor……………………………………………………

…

966,000

Factory overhead……………………………………………

…

490,500

Total manufacturing costs incurred……………………… 2,606,500

Total manufacturing costs……………………………………

…

$2,922,900

Less work in process inventory, July 31……………………

…

355,500

Cost of goods manufactured…………………………………

…

$2,567,400

Ex. 18-15

a. $1,099,000 ($136,000 + $963,000)

b. $947,400 ($1,099,000 – $151,600)

CHAPTER 18 Introduction to Managerial Accounting

Ex. 18-16

a.

Work in process inventory, January 1 $ 334,600

Direct materials:

Direct labor 2,260,000

Factory overhead:

Indirect labor $ 115,000

Machinery depreciation 90,000

Heat, light, and power 55,000

Supplies 18,500

Property taxes 10,000

Miscellaneous cost 33,100

Total factory overhead 321,600

Cost of goods manufactured $4,035,000

b. Finished goods inventory, January 1…………………………………………

…

$ 675,000

Cost of goods manufactured*……………………………………………………

…

4,035,000

*From part (a) above

Disksan Manufacturing Company

Statement of Cost of Goods Manufactured

For the Month Ended January 31

CHAPTER 18 Introduction to Managerial Accounting

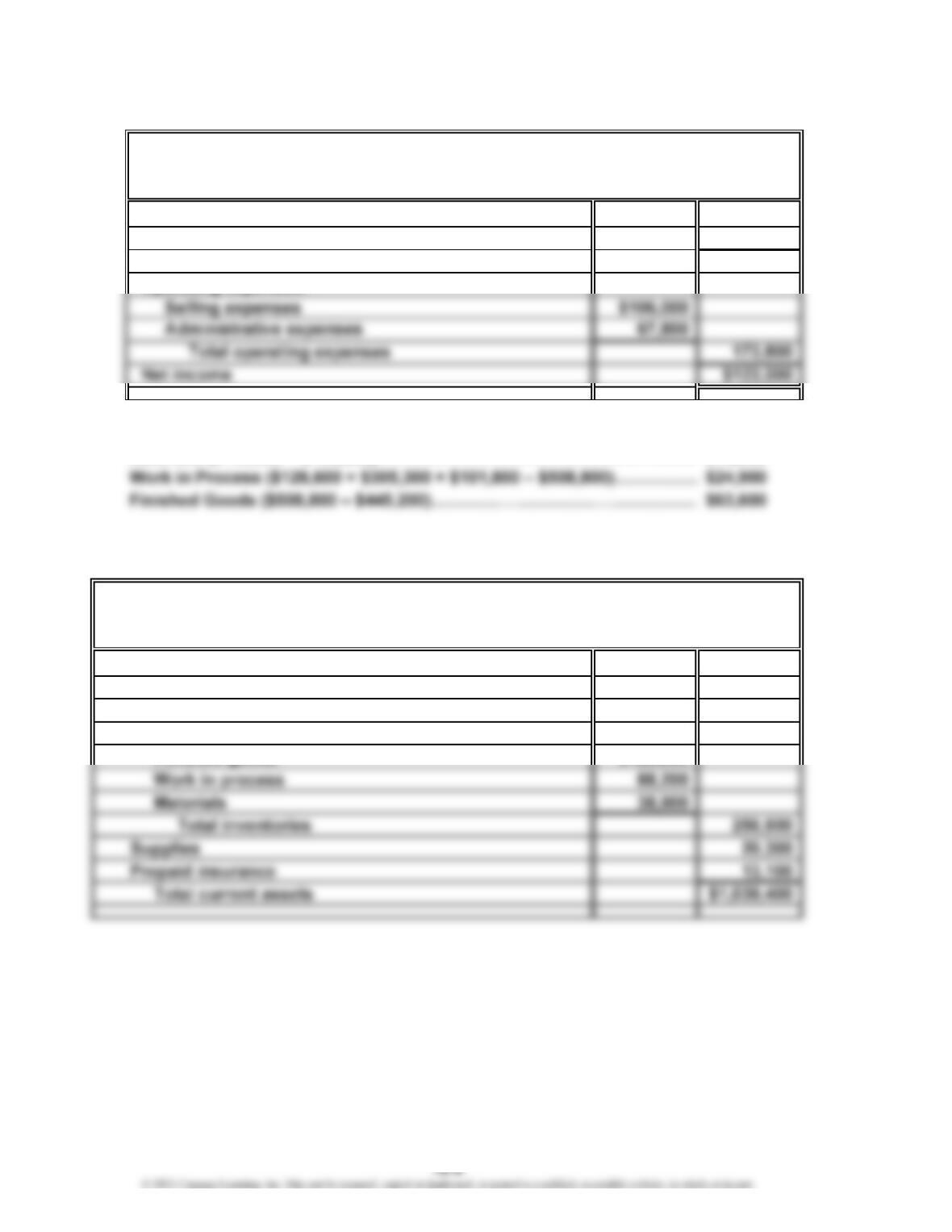

Ex. 18-17

a. Finished goods inventory, January 1………………………

…

$ 707,000

Cost of goods manufactured…………………………………

…

3,606,000

Cost of finished goods available for sale…………………

…

$4,313,000

Less finished goods inventory, January 31………………

…

622,000

Cost of goods sold……………………………………………

…

$3,691,000

c. Gross profit………………………………………………………

…

$1,609,000

Operating expenses:

Selling expenses……………………………………………

…

$426,000

…

Ex. 18-18

a. Sales………………………………………………………………

…

$792,000

Less gross profit………………………………………………

…

462,000

Cost of goods sold……………………………………………

…

$330,000

…

…

c. Purchased materials……………………………………………

…

$244,200

Less materials inventory………………………………………

…

33,000

Direct materials cost…………………………………………… $211,200

…

e. Total manufacturing costs……………………………………

…

$455,400

Less cost of goods manufactured…………………………… 396,000

Work in process inventory……………………………………

…

$ 59,400

…

…

…

CHAPTER 18 Introduction to Managerial Accounting

Ex. 18-19

The Hotel Monaco has excess capacity for this day, so it is willing to accept

additional customers. To determine whether or not to accept Natalie Mooney’s

bid, the Hotel Monaco could use managerial accounting information to determine

CHAPTER 18 Introduction to Managerial Accounting

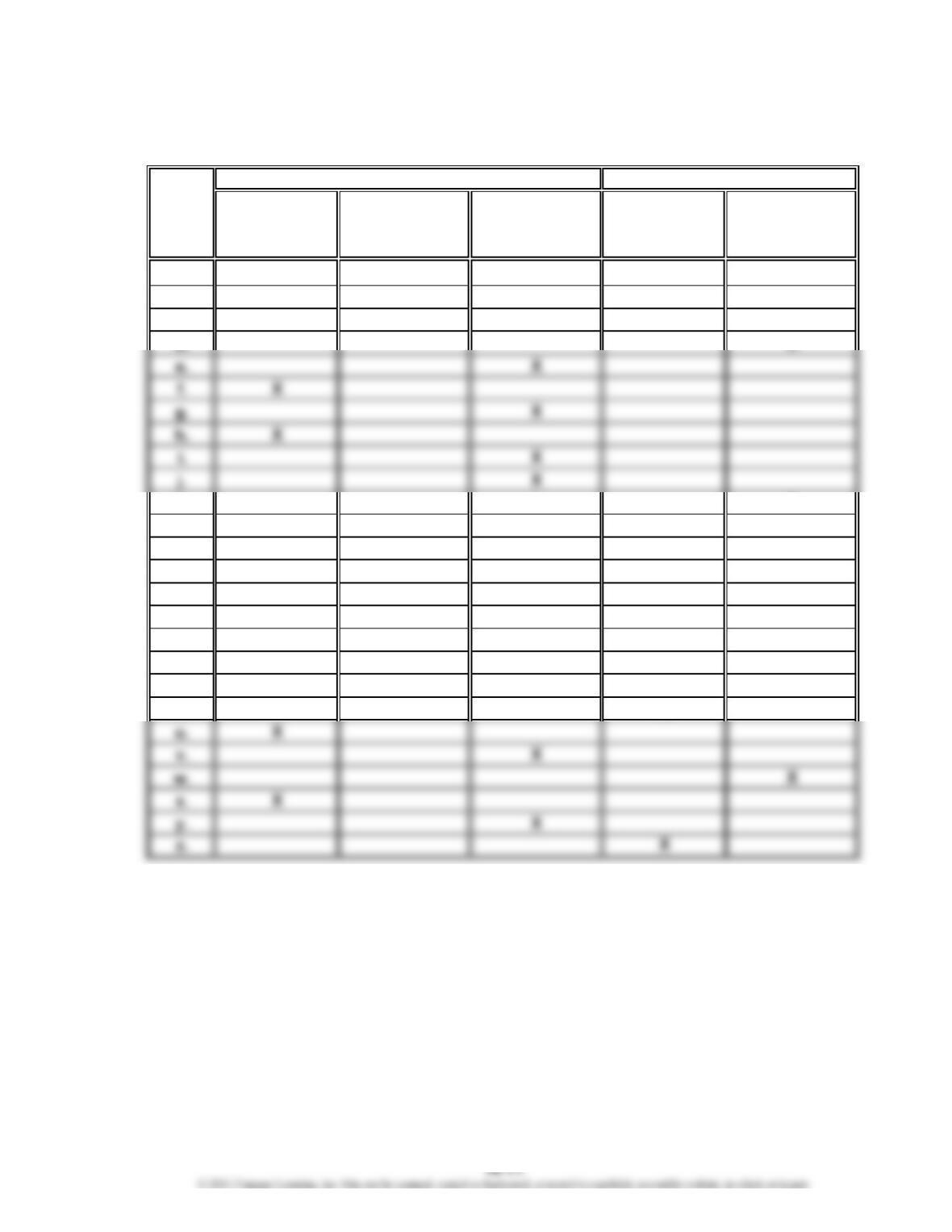

Prob. 18-1A

Direct Direct Factory

Materials Labor Overhead Selling Administrative

Cost Cost Cost Cost Expense Expense

a. X

b. X

c. X

k. X

l. X

m. X

n. X

o. X

p. X

q. X

r. X

s. X

t. X

PROBLEMS

Product Costs Period Costs

CHAPTER 18 Introduction to Managerial Accounting

Prob. 18-2A

Direct Direct Factory

Materials Labor Overhead Selling Administrative

Cost Cost Cost Cost Expense Expense

g. X

hX

i. X

j. X

k. X

l. X

m. X

n. X

Product Costs Period Costs

CHAPTER 18 Introduction to Managerial Accounting

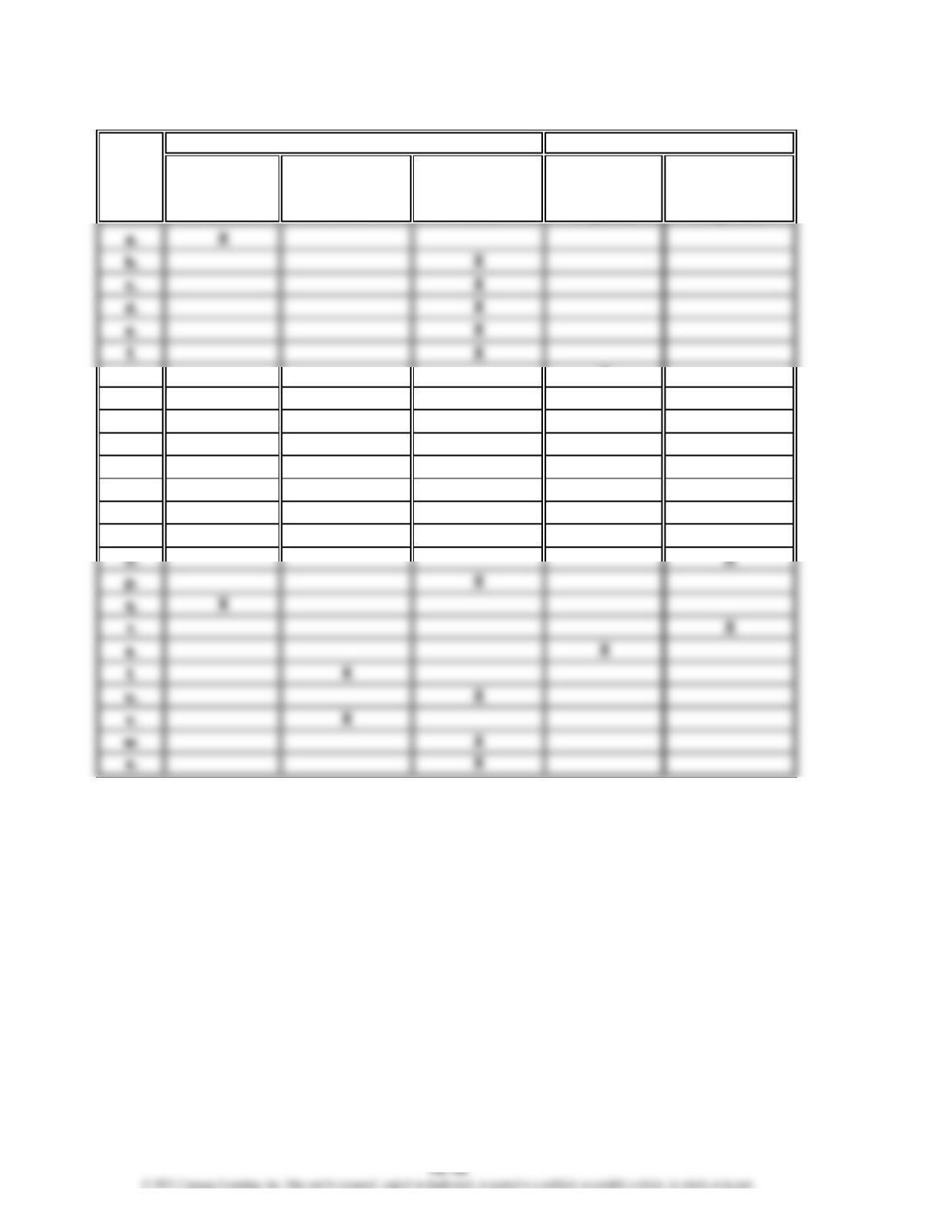

Prob. 18-3A

1. The most logical definition for the final cost object would be the patient. The

reason is that the cost can be accumulated at the patient level for billing and

insurance reimbursement.

2. Cost Direct Indirect

a. X

b. X

h. X

i. X

j. X

k. X

l. X

m. X

CHAPTER 18 Introduction to Managerial Accounting

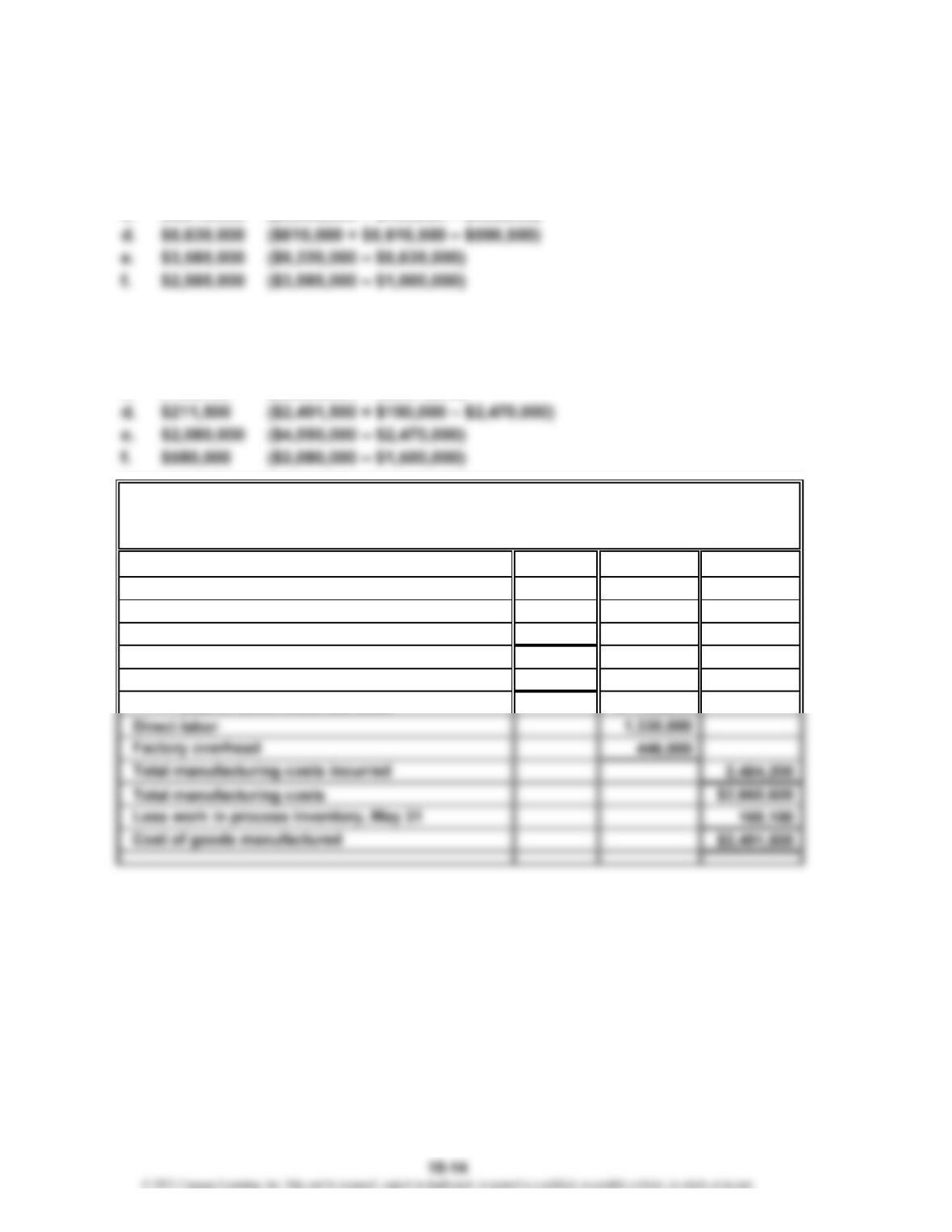

Prob. 18-4A

1. Rainier Company

a. $111,500 ($950,000 + $100,000 – $938,500)

b. $5,598,500 ($938,500 + $2,860,000 + $1,800,000)

Yakima Company

a. $708,200 ($48,200 + $710,000 – $50,000)

b. $1,330,000 ($2,484,200 – $708,200 – $446,000)

c. $169,100 ($2,660,600 – $2,491,500)

2.

Work in process inventory, May 1 $ 176,400

Direct materials:

Materials inventory, May 1 $ 48,200

Purchases 710,000

Cost of materials available for use $758,200

Less materials inventory, May 31 50,000

Cost of direct materials used $ 708,200

Yakima Company

Statement of Cost of Goods Manufactured

For the Month Ended May 31