Ex. 18.9 (concluded)

e. 161,000

Work in Process: Baking Department 161,000

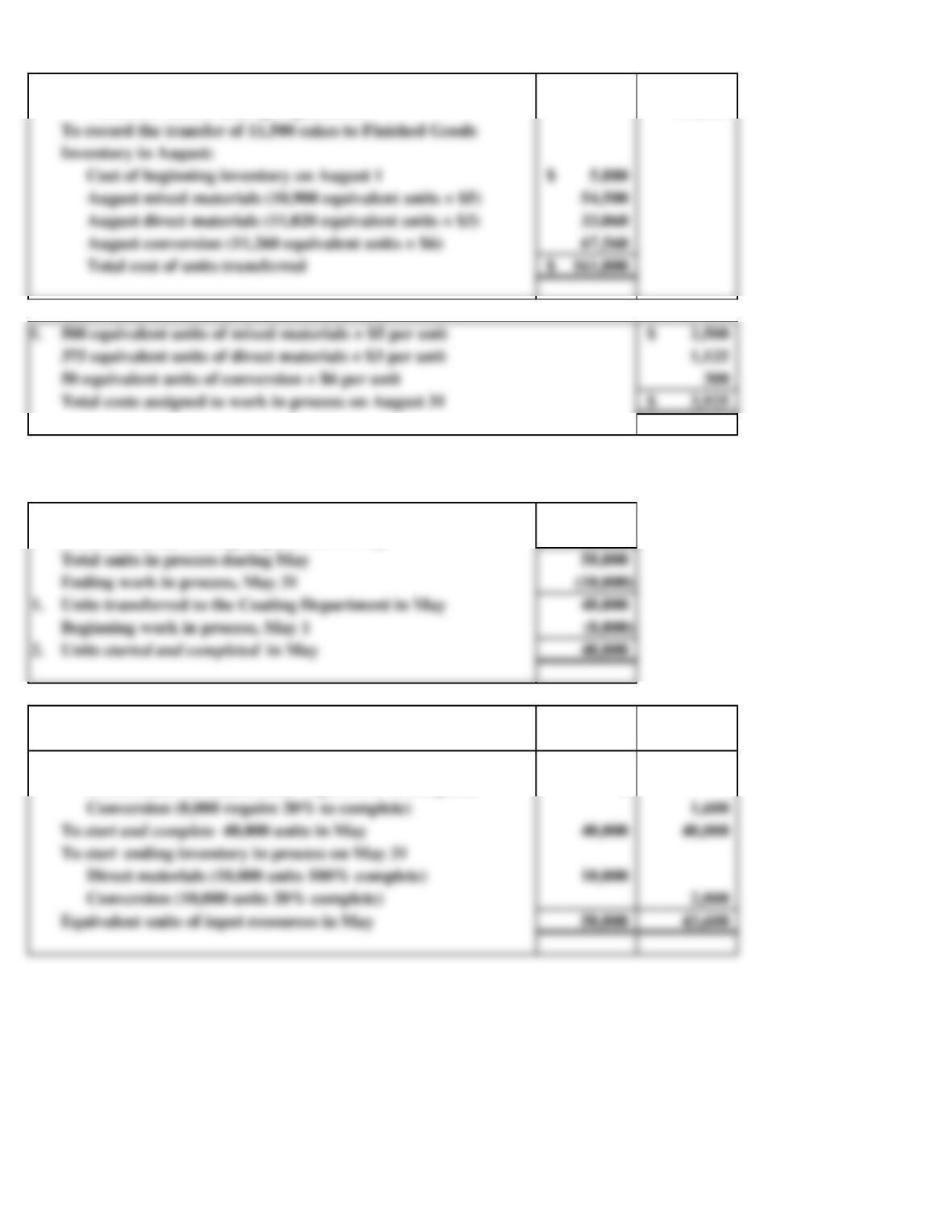

500 equivalent units of mixed materials × $5 per unit

Total costs assigned to work in process on August 31

375 equivalent units of direct materials × $3 per unit

50 equivalent units of conversion × $6 per unit

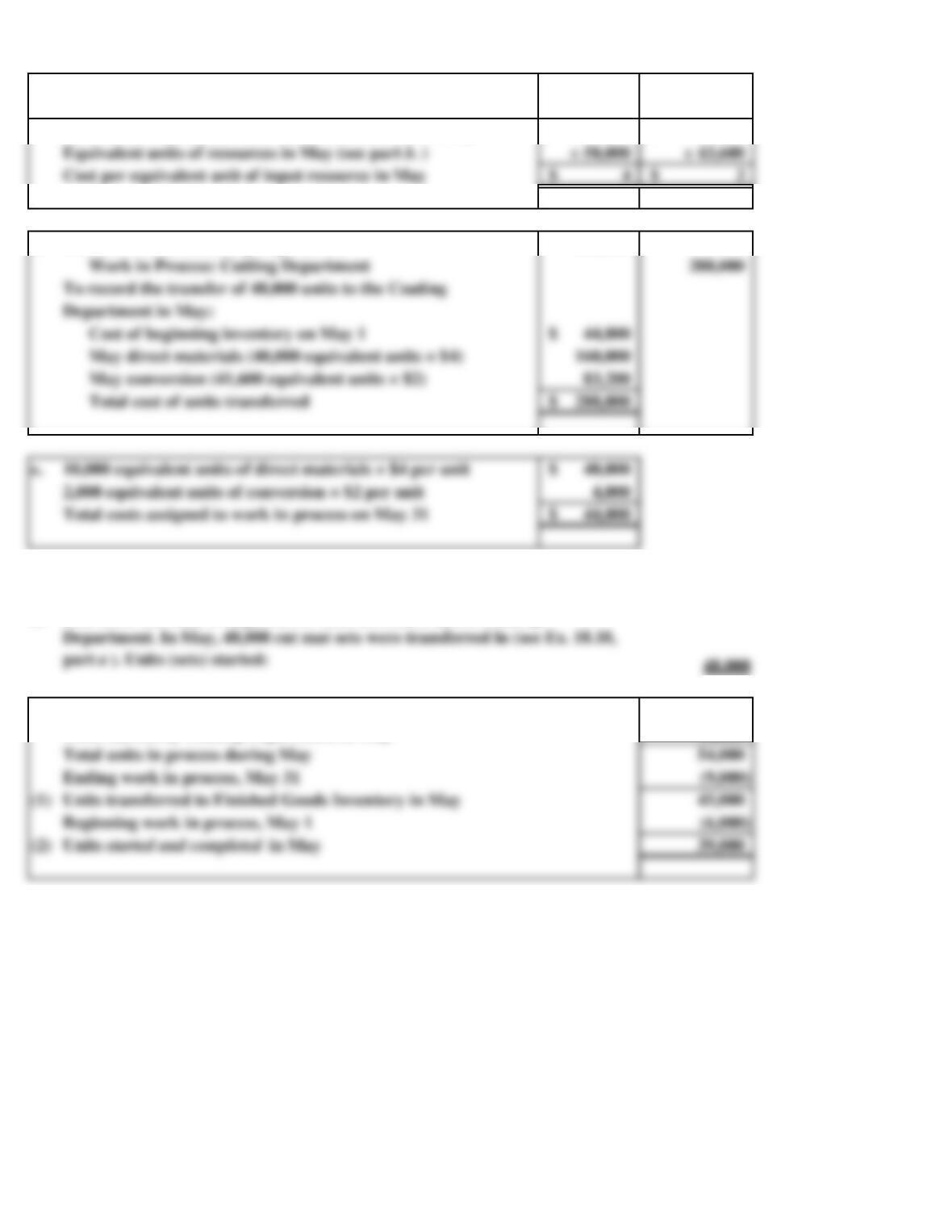

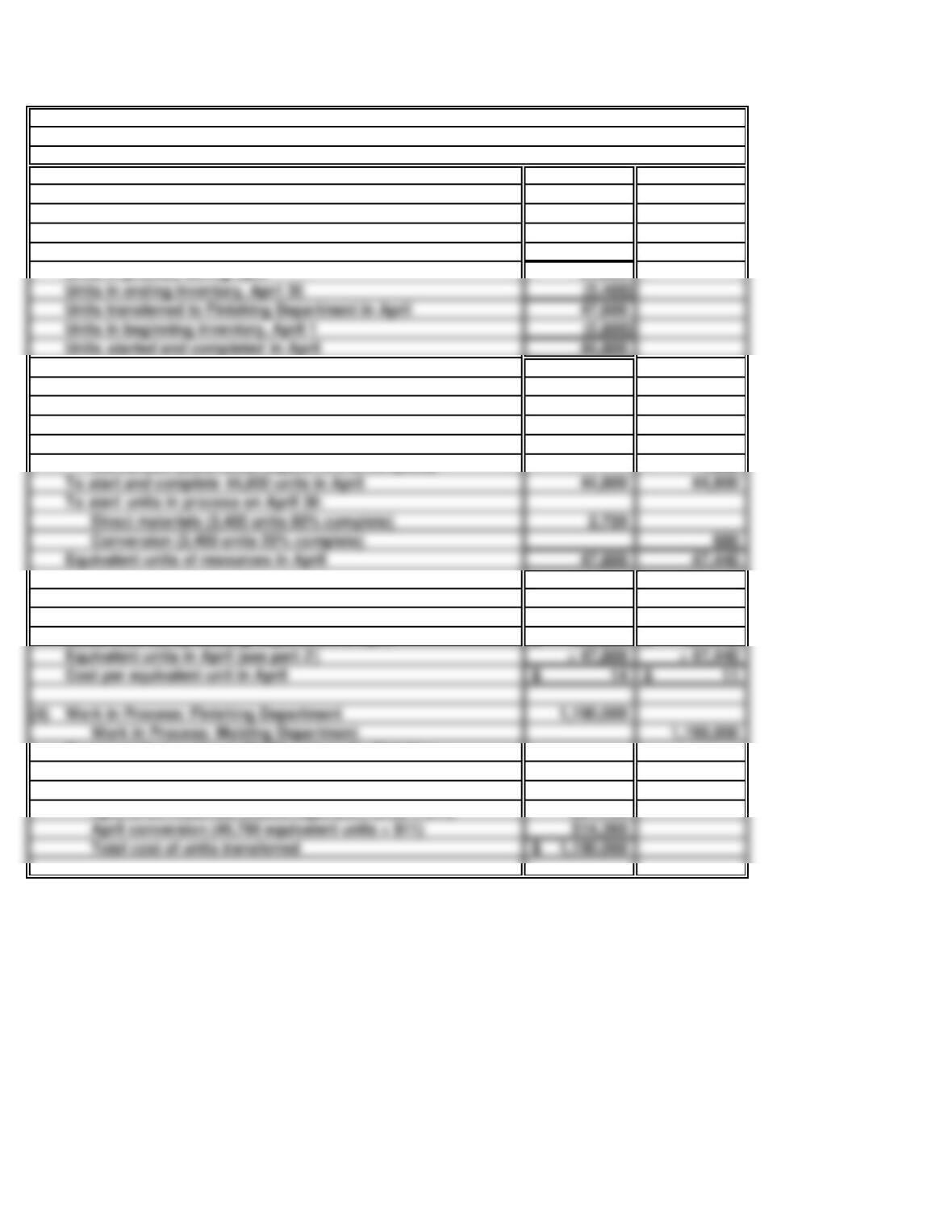

Units started and completed in May 40,000

Ex. 18.10

a. Beginning work in process, May 1 8,000

Units started by Cutting Department in May 50,000

b. Direct

Input resources required Materials Conversion

To finish beginning inventory in process on May 1:

To start and complete 40,000 units in May 40,000 40,000

To start ending inventory in process on May 31

Direct materials (8,000 units require 0% to complete) 0

Finished Goods Inventory

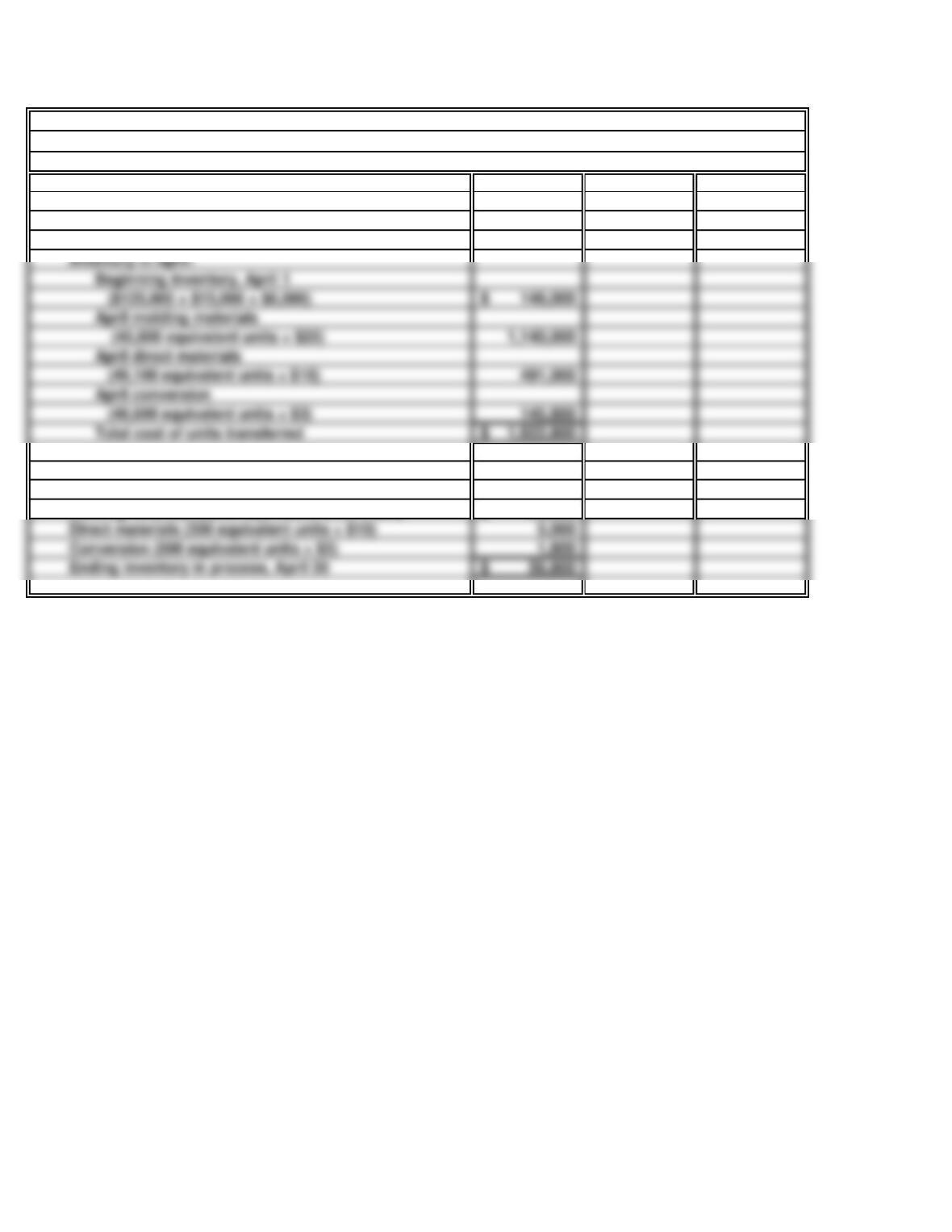

Cost of beginning inventory on August 1 5,880$

Total cost of units transferred 161,000$

To record the transfer of 11,500 cakes to Finished Goods

Inventory in August:

August mixed materials (10,900 equivalent units × $5)

August direct materials (11,020 equivalent units × $3)

August conversion (11,260 equivalent units × $6)

Ex. 18.10 (concluded)

c. Direct Conversion

Materials Costs

200,000$ 87,200$

d. 288,000

To record the transfer of 48,000 units to the Coating

May conversion (41,600 equivalent units × $2)

Department in May:

Cost of beginning inventory on May 1

May direct materials (40,000 equivalent units × $4)

Total cost of units transferred

Total costs assigned to work in process on May 31

10,000 equivalent units of direct materials × $4 per unit

2,000 equivalent units of conversion × $2 per unit

a.

b. 6,000

Units started and completed in May

Total units in process during May

Beginning work in process, May 1

Ending work in process, May 31

Units transferred to Finished Goods Inventory in May

48,000

One set of cut mats is required for each set coated by the Coating

Beginning work in process, May 1

Units started by Coating Department in May

Cost of direct materials and conversion incurred in May

Work in Process: Coating Department

Ex. 18.11

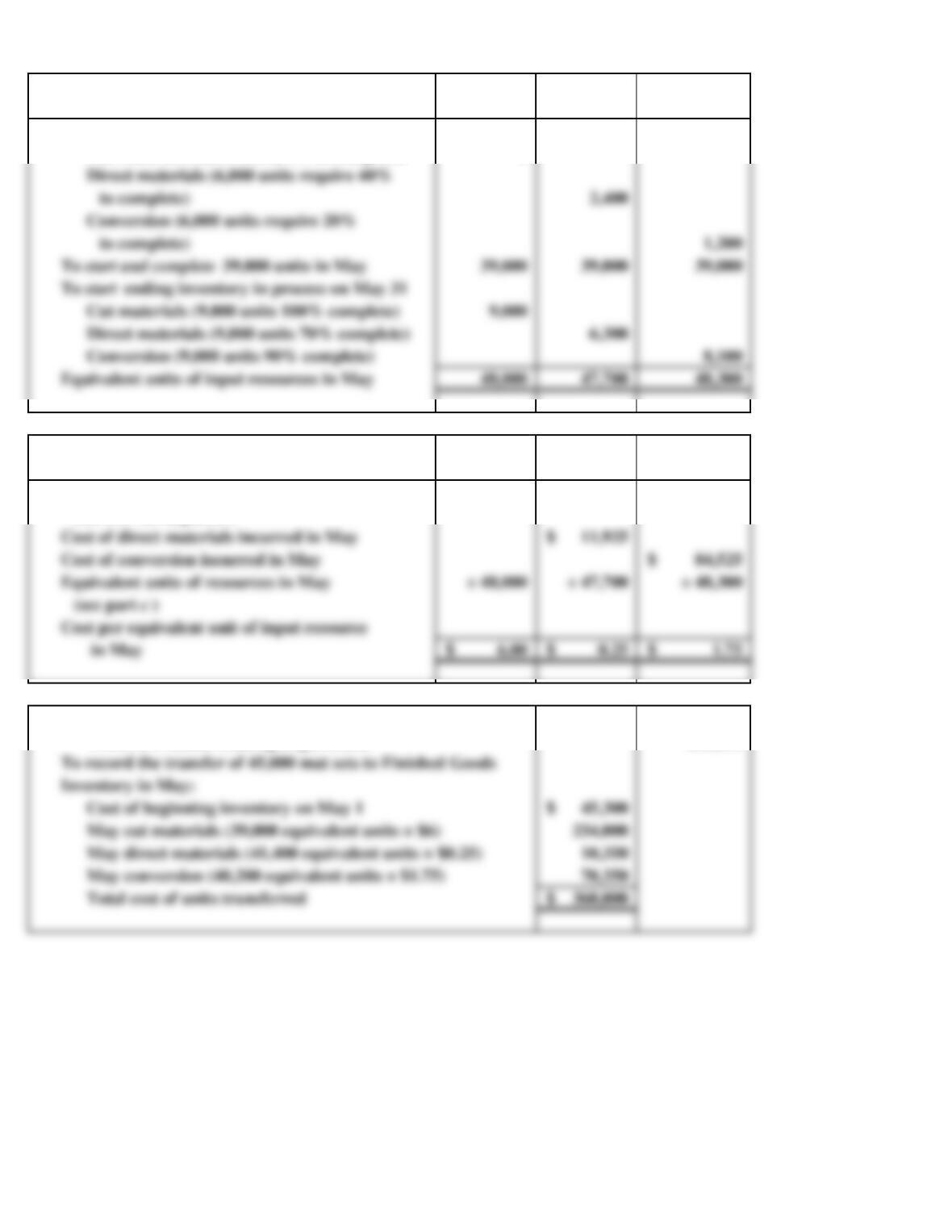

Equivalent units of resources in May (see part b. )

Cost per equivalent unit of input resource in May

Ex. 18.11 (continued)

c. Cut Direct

Materials Materials Conversion

Cut materials (6,000 units, 0% to complete) 0

d. Cut Direct Conversion

Materials Materials Costs

in May 6.00$ 0.25$ 1.75$

Cost per equivalent unit of input resource

(see part c)

Cost of direct materials incurred in May

Cost of conversion incurred in May

Equivalent units of resources in May

288,000$

e. 360,000

Work in Process: Coating Department 360,000

Cost of beginning inventory on May 1 45,300$

May conversion (40,200 equivalent units × $1.75)

May cut materials (39,000 equivalent units × $6)

May direct materials (41,400 equivalent units × $0.25)

Inventory in May:

To record the transfer of 45,000 mat sets to Finished Goods

Finished Goods Inventory

Input resources required

To finish beginning inventory in process on May

Cost of cut mats transferred in

(see Ex. 18.10, part d)

Direct materials (6,000 units require 40%

Conversion (6,000 units require 20%

Cut materials (9,000 units 100% complete) 9,000

Direct materials (9,000 units 70% complete) 6,300

Conversion (9,000 units 90% complete) 8,100

To start and complete 39,000 units in May

To start ending inventory in process on May 31

Equivalent units of input resources in May

Ex. 18.11 (concluded)

f. 54,000$

1,575

a. 1,500

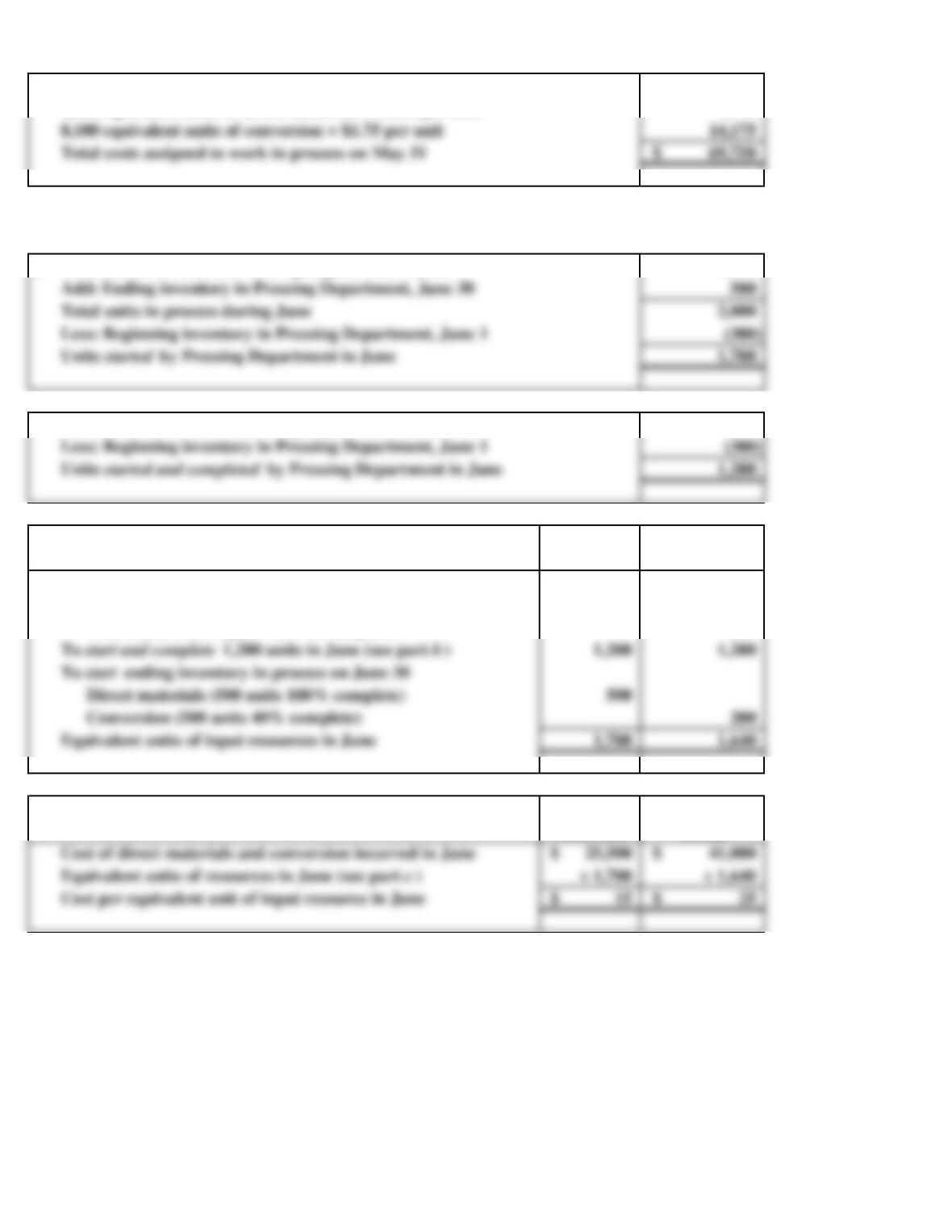

Add: Ending inventory in Pressing Department, June 30

Total units in process during June

Less: Beginning inventory in Pressing Department, June 1

Units started by Pressing Department in June

b. 1,500

Less: Beginning inventory in Pressing Department, June 1

Units started and completed by Pressing Department in June

c. Direct

Materials Conversion

0

Conversion (300 require 80% to complete) 240

Direct materials (500 units 100% complete) 500

Conversion (500 units 40% complete) 200

Equivalent units of input resources in June

To start and complete 1,200 units in June (see part b)

To start ending inventory in process on June 30

d. Direct Conversion

Materials Costs

Cost of direct materials and conversion incurred in June

Equivalent units of resources in June (see part c )

Cost per equivalent unit of input resource in June

Units transferred to the Painting Department in June

Input resources required

To finish beginning inventory in process on June 1:

Direct materials (300 units require 0% to complete)

Units transferred to the Painting Department in June

9,000 equivalent units of cut materials × $6 per unit

6,300 equivalent units of direct materials × $0.25 per unit

Ex. 18.12

8,100 equivalent units of conversion × $1.75 per unit

Total costs assigned to work in process on May 31

Ex. 18.12 (concluded)

e. 60,000

Work in Process: Painting Department 60,000

200 equivalent units of conversion × $25 per unit

500 equivalent units of direct materials × $15 per unit

Total costs assigned to Pressing Department on June 30

a. Direct Conversion

Materials Costs

50,400$ 36,000$

Direct materials (300 equivalent units × 40%) ÷ 120

Cost per equivalent unit carried forward from August

Costs in beginning inventory, September 1

Work in Process: Pressing Department

Ex. 18.14

Equivalent units in process, September 1:

The recommendation to eliminate the company’s current work in process accounts and charge all

manufacturing costs directly to Finished Goods Inventory makes sense for this company. If we assume

that the company operates 300 days per year, daily production is 100,000 pencils (30,000,000 pencils per

Ex. 18.13

June conversion (1,440 equivalent units × $25) 36,000

Total cost of units transferred 60,000$

To record the transfer of 1,500 units to the Painting

Department in June:

Cost of beginning inventory on June 1

June direct materials (1,200 equivalent units × $15)

Ex. 18.14 (concluded)

b.

Direct

Materials Conversion

180

Direct Conversion

Materials Costs

Equivalent units in September (see step 1 )

Cost per equivalent unit in September

789,750$ 787,500$

c.

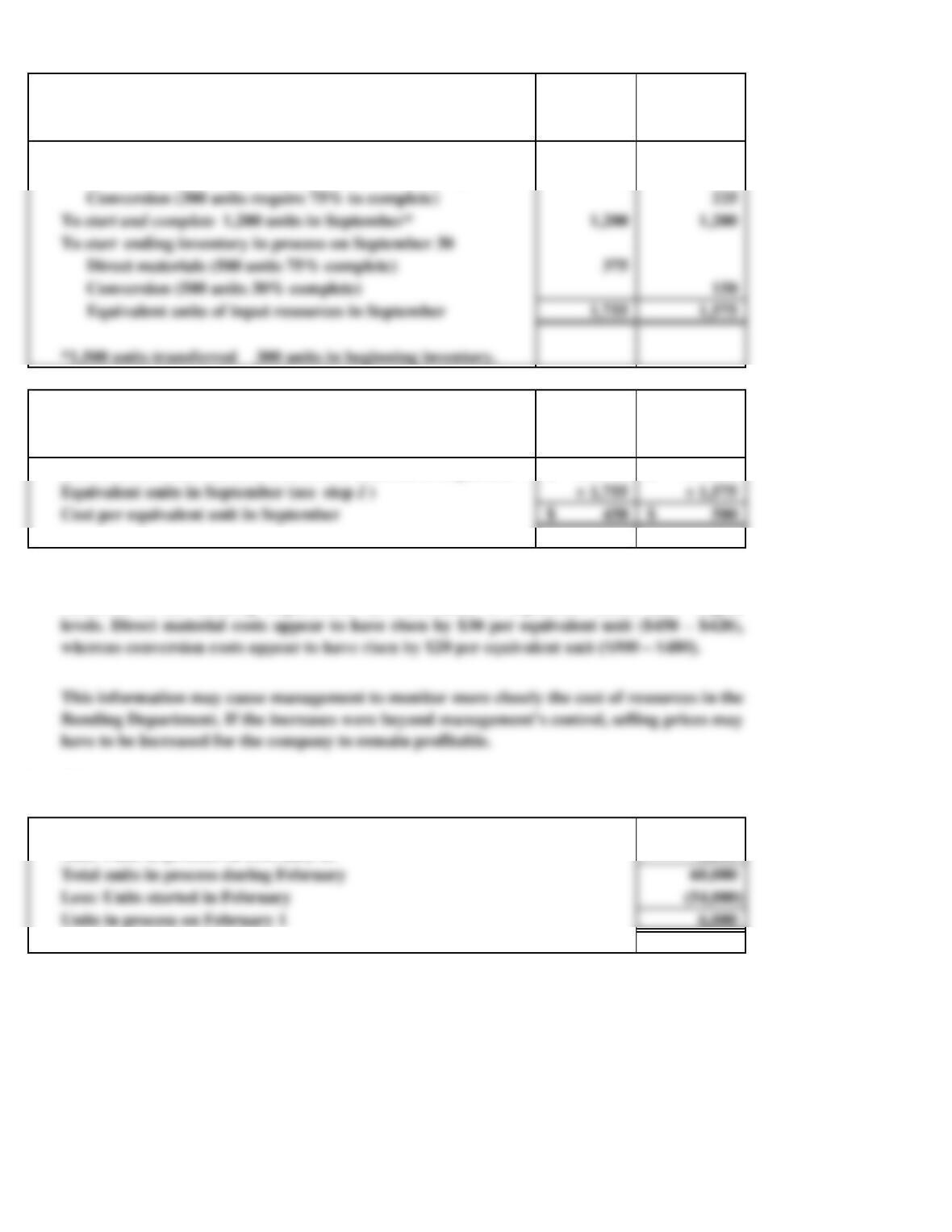

a. 58,000

Units in process on February 1

Total units in process during February

Less: Units started in February

2,000

Ex. 18.15

The cost figures computed in parts aand bconvey to management that the cost of input

resources in the Bonding Department have increased in September above their August

Add: Units in process on February 28

Units transferred out of the Blending Department in February

Step 1: Compute input resources required in September

Input resources required

Step 2: Compute equivalent costs per unit in September

Cost of direct materials and conversion incurred in September

To finish beginning inventory in process on September 1:

Direct materials (300 units require 60% to complete)

Conversion (300 units require 75% to complete)

Equivalent units of input resources in September

To start and complete 1,200 units in September*

To start ending inventory in process on September 30

Ex. 18.15 (continued)

b. 58,000

c. 12,000$

÷ 6,000

2$

6$

6$

Start inventory in process on February 28 (2,000 units × 20%)

Conversion costs incurred in February

Cost per equivalent unit of conversion from January

6,000 units in process × 70% complete

Conversion costs carried forward from January

Equivalent units of conversion carried forward from January

Equivalent units of conversion in February

Less: Units of conversion used in February to

Start and complete 52,000 units (see part b)

Percentage required to complete February 1 inventory

Units in inventory on February 1

Equivalent units of conversion carried forward from January:

Cost per equivalent unit of conversion in February

Equivalent units required to complete inventory on February 1

Units transferred out of the Blending Department in February

Direct material costs in beginning inventory, February 1

Units of inventory on February 1 (materials 100% complete)

Cost per equivalent unit of direct material from January

Cost per equivalent unit of conversion from January*

Less: Units in process on February 1 (see part a)

Units started and completed in February

Ex. 18.15 (concluded)

d. February cost per equivalent unit of direct material* 3$

*Computations:

Step 1: Compute equivalent units of direct material

Step 2: Compute cost per equivalent unit

SOLUTIONS TO PROBLEMS SET A

20 Minutes, Easy

PROBLEM 18.1A

BRITE IDEAS

a.

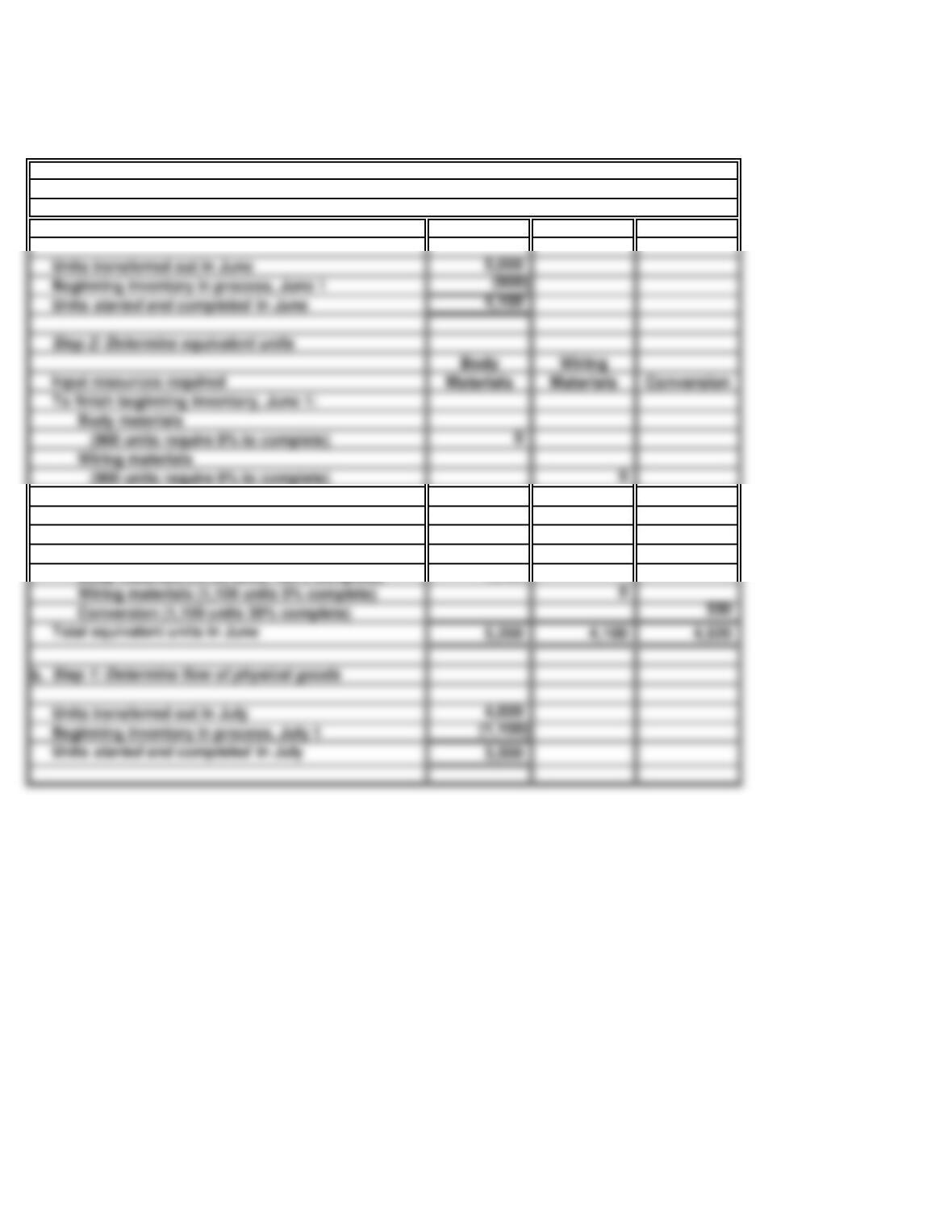

Conversion

(900 units require 10% to complete) 90

4,100 4,100 4,100

Body materials (1,100 units 100% complete) 1,100

Wiring materials (1,100 units 0% complete) 0

4,600

Beginning inventory in process, July 1

Units transferred out in July

Step 1: Determine flow of physical goods

Step 1: Determine flow of physical goods

To start and complete 4,100 units in June

To start ending inventory in process on June 30:

5,000

(900 units require 0% to complete) 0

(900 units require 0% to complete) 0

Units transferred out in June

Beginning inventory in process, June 1

Units started and completed in June

Step 2: Determine equivalent units

To finish beginning inventory, June 1:

PROBLEM 18.1A

BRITE IDEAS (concluded)

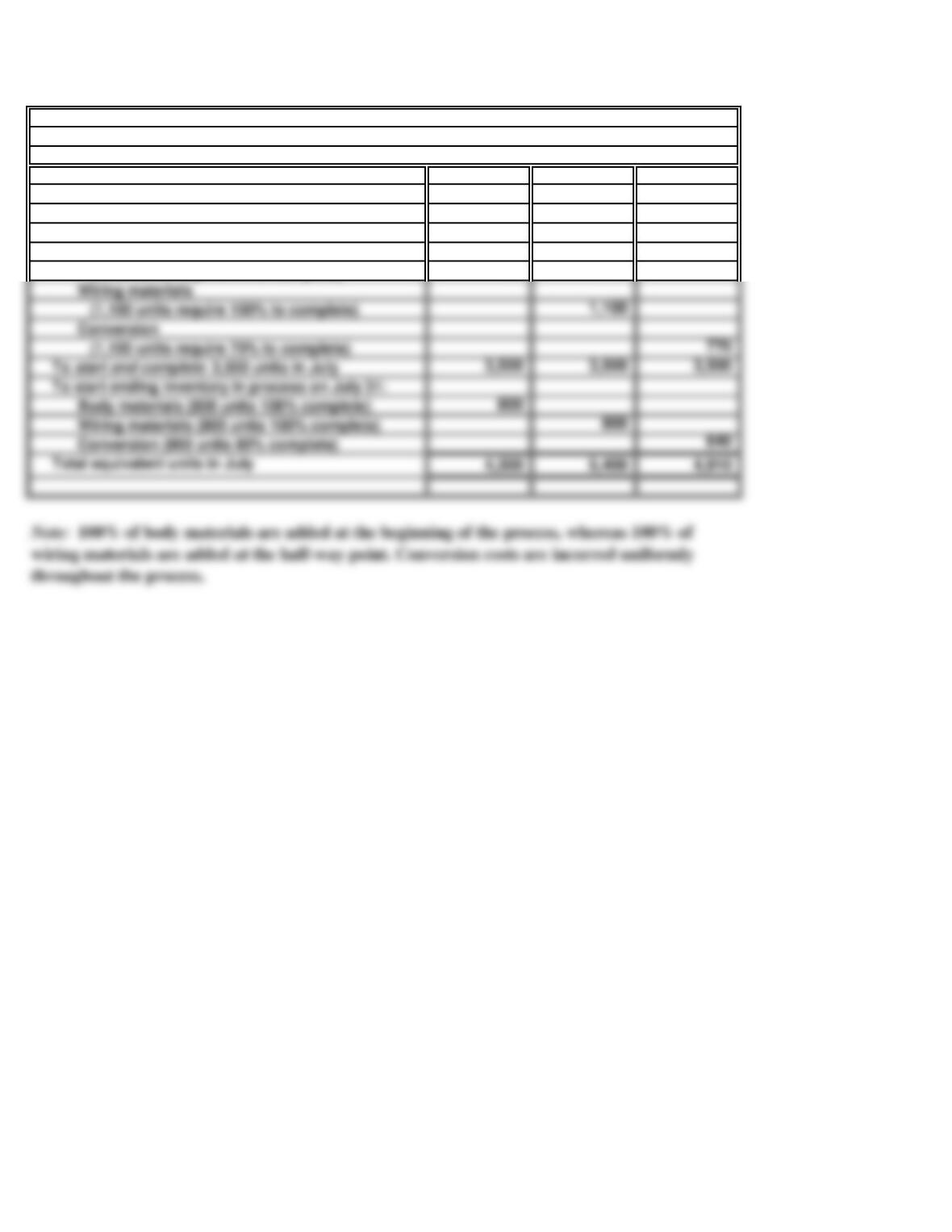

Body Wiring

Materials Materials Conversion

Body materials

(1,100 units require 0% to complete) 0

Step 2: Determine equivalent units

Input resources required

To finish beginning inventory, July 1:

Wiring materials

Conversion

To start and complete 3,500 units in July

To start ending inventory in process on July 31:

30 Minutes, Easy

PROBLEM 18.2A

SUN APPLIANCE

a. (1) $50 [($160,000 + $15,000 + $25,000) ÷ 4,000 units]

b.

In evaluating the overall efficiency of the Motor Department, management would look at

30 Minutes, Medium PROBLEM 18.3A

SUN APPLIANCE

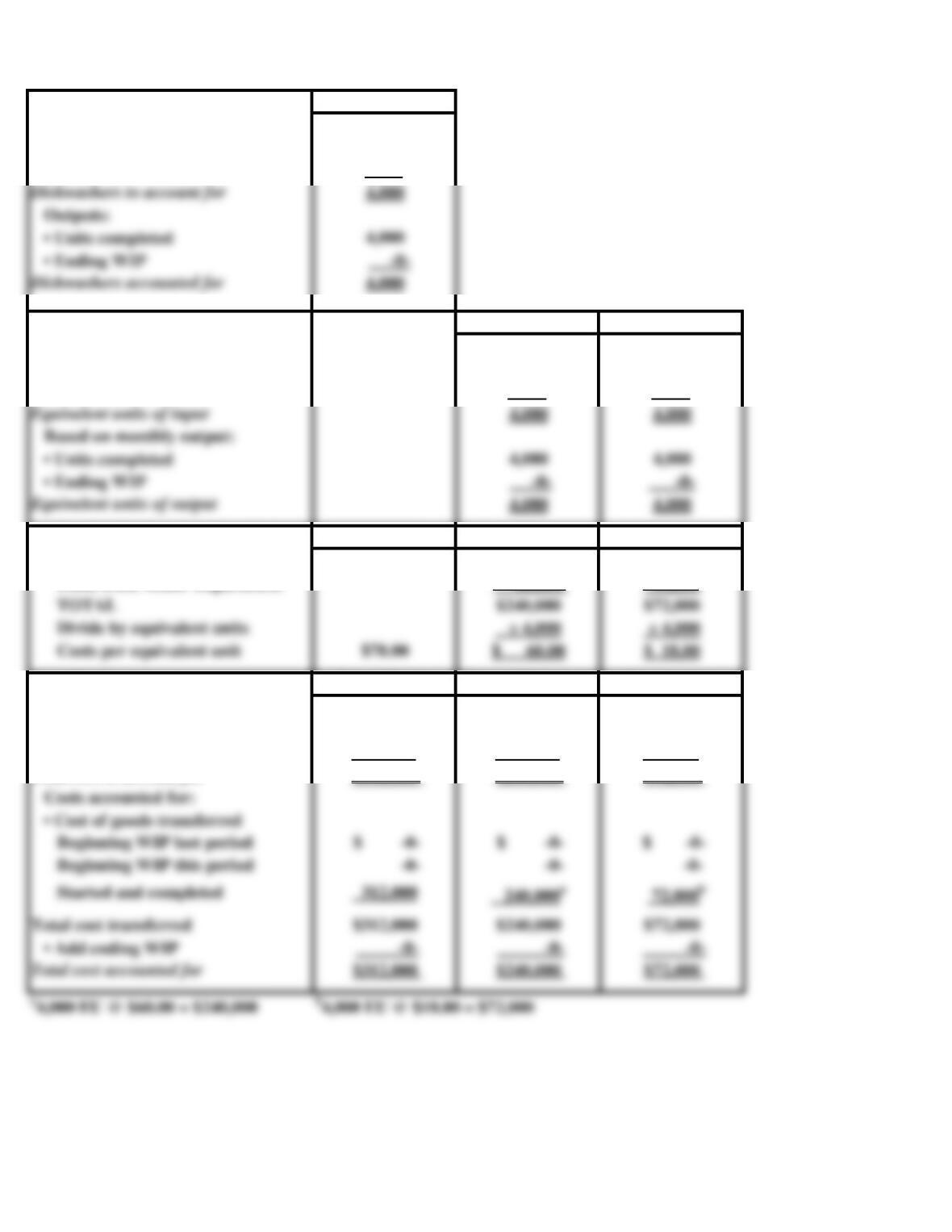

Part I. Physical Flow Total Units

Inputs:

• Beginning WIP -0-

• Started 4,000

Part II. Equivalent Units Direct Materials Conversion

Based on monthly input:

• Beginning WIP -0- -0-

• Units started 4,000 4,000

Based on monthly output:

• Units completed 4,000 4,000

• Ending WIP -0- -0-

Part III. Cost Per Equivalent Unit Total Unit Cost Direct Materials

Conversion

Costs from Tub Department $160,000 $40,000

Costs from Motor Department 80,000 32,000

TOTAL $240,000 $72,000

Divide by equivalent units ÷ 4,000 ÷ 4,000

Costs per equivalent unit $78.00 $ 60.00 $ 18.00

Part IV. Total Cost Assignment Total Costs Direct Materials

Conversion

Costs to account for:

• Cost of beginning WIP $ -0-

• Cost added during the period 312,000 240,000 72,000

Total cost to account for $312,000 $240,000 $72,000

Costs accounted for:

• Cost of goods transferred

Beginning WIP last period $ -0- $ -0- $ -0-

Total cost transferred $312,000 $240,000 $72,000

• Add ending WIP -0- -0- -0-

Total cost accounted for $312,000 $240,000 $72,000

Outputs:

• Units completed 4,000

• Ending WIP -0-

PROBLEM 18.4A

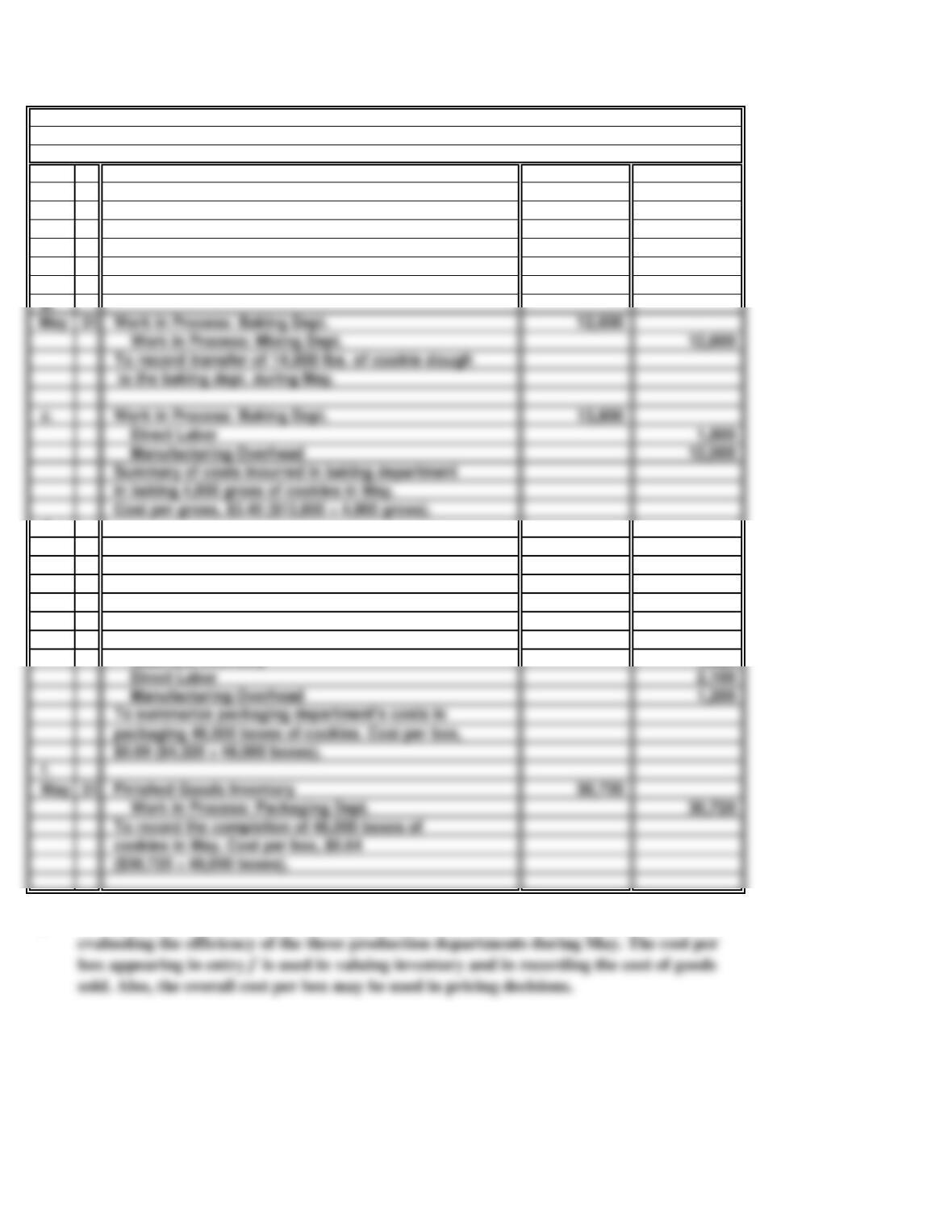

TOLL HOUSE

a. Work in Process: Mixing Dept. 12,600

Materials Inventory 3,600

Direct Labor 3,000

Manufacturing Overhead 6,000

Summary of costs incurred in mixing 14,000 lbs.

of cookie dough in May. Cost per lb., $0.90

($12,600 ÷ 14,000 lbs.).

d.

May 31 Work in Process: Packaging Dept. 26,400

Work in Process: Baking Dept. 26,400

To record transfer cost of 4,000 gross of cookies sent

to the packaging department in May.

e. Work in Process: Packaging Dept. 4,320

Materials Inventory 1,020

Direct Labor 2,100

Manufacturing Overhead 1,200

packaging 48,000 boxes of cookies. Cost per box,

f.

Work in Process: Packaging Dept. 30,720

To record the completion of 48,000 boxes of

cookies in May. Cost per box, $0.64

($30,720 ÷ 48,000 boxes).

g.

Management will use the unit costs appearing in entries a, c, and e, in separately

30 Minutes, Medium

b.

Work in Process: Mixing Dept. 12,600

to the baking dept. during May.

c. Work in Process: Baking Dept. 13,800

Direct Labor 1,800

Manufacturing Overhead 12,000

Summary of costs incurred in baking department

in baking 4,000 gross of cookies in May.

Cost per gross, $3.45 ($13,800 ÷ 4,000 gross).

35 Minutes, Medium

PROBLEM 18.5A

BADGERSIZE COMPANY

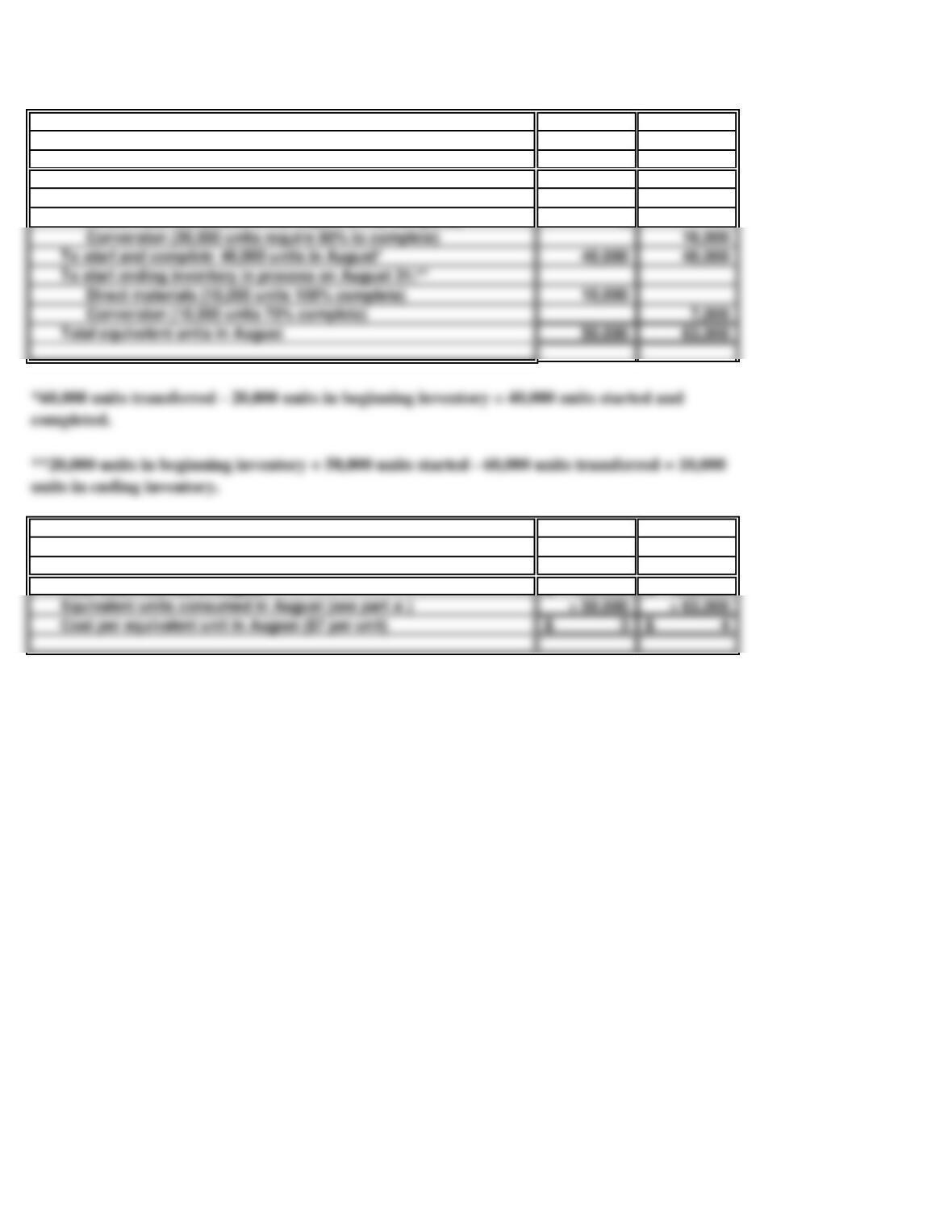

a.

Direct

Materials Conversion

0

b.

Direct Conversion

Materials Costs

150,000$ 252,000$

Cost per equivalent unit in August ($7 per unit)

Equivalent units consumed in August (see part a. )

Total cost incurred in August

Input resources required

To finish beginning inventory, August 1:

Direct materials (20,000 units require 0% to complete)

Conversion (20,000 units require 80% to complete)

Total equivalent units in August

Direct materials (10,000 units 100% complete)

30 Minutes, Medium PROBLEM 18.6A

BADGERSIZE COMPANY

a. Production Cost Report

Part I. Physical Flow Total Units

Inputs:

• Beginning WIP 20,000

• Started 50,000

Units to account for 70,000

Part II. Equivalent Units Direct Materials Conversion

Consumed

Based on monthly input:

• Finish BWIP -0- 16,000

• Start new units 50,000 47,000

Equivalent units of input 50,000 63,000

Based on monthly output:

• T ransferred units 40,000 56,000

• EWIP units 10,000 7,000

Equivalent units of output 50,000 63,000

Part III. Cost Per Equivalent Unit Total Unit Cost Direct Materials

Conversion

Input costs in August $150,000 $252,000

Equivalent units, August ÷50,000 ÷63,000

Costs per equivalent unit, Aug. $7.00 $ 3.00 $ 4.00

Forming Department, Month of August

Outputs:

• Units completed 60,000

• Ending WIP 10,000

Units accounted for 70,000

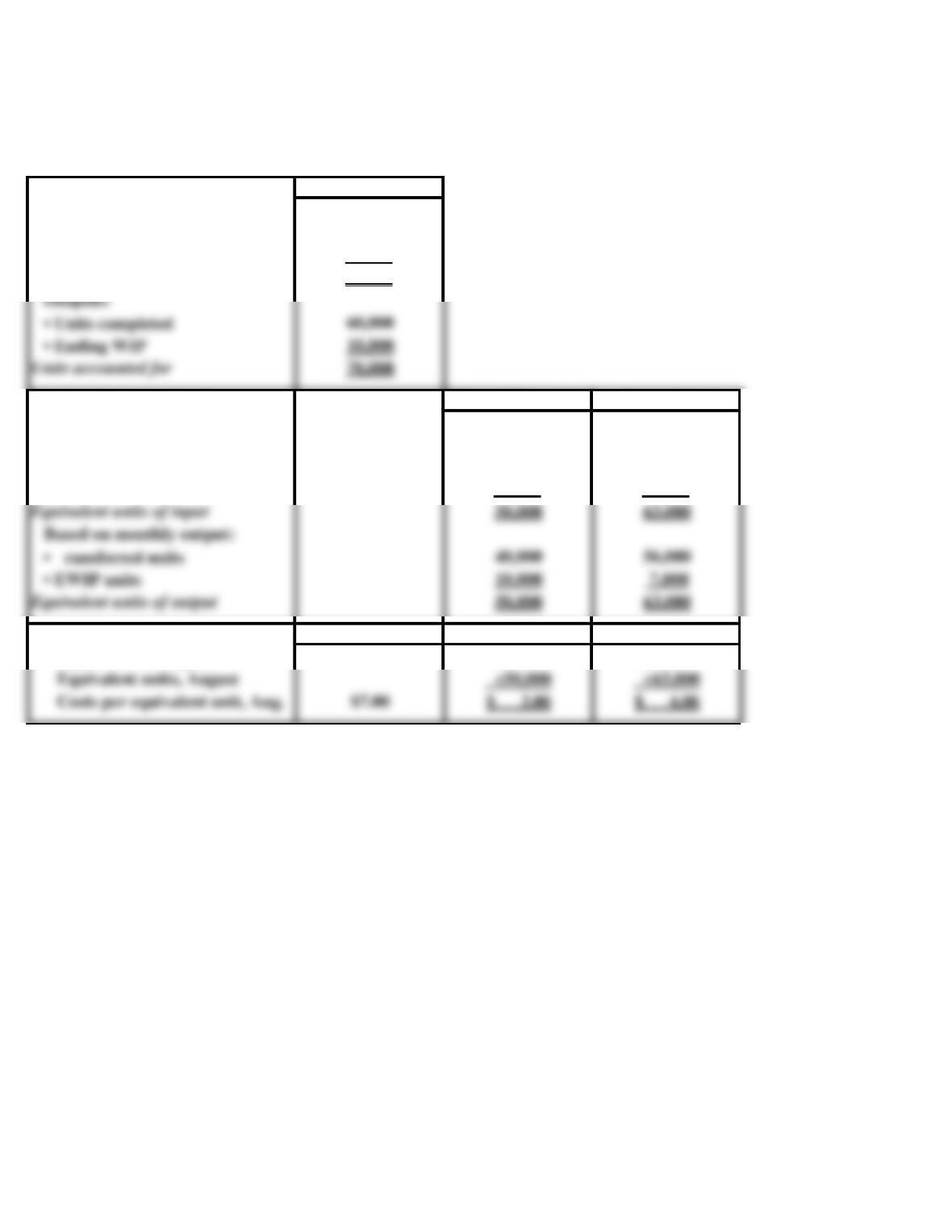

PROBLEM 18.6A

BADGERSIZE COMPANY (concluded)

Total Costs Direct Materials

Conversion

$104,000

402,000

$506,000

b.

Costs accounted for:

• Cost of goods transferred

Total cost to account for

Part IV. Total Cost Assignment

Costs to account for

• Cost of beginning WIP

• Cost added during the period

Management can compare production cost reports from month to month to help control

costs and assess efficiency of their processes. For example, the equivalent units can be

$104,000 $ 80,000 $ 24,000

$448,000 $200,000 248,000

$506,000 $230,000 $276,000

Total cost transferred

Total cost accounted for

50 Minutes, Strong

PROBLEM 18.7A

HOUND HAVENS

a.

(1)

2,800

48,200

51,000

(2) Direct

Materials Conversion

280

1,960

44,800 44,800

2,720

47,800 47,440

To start units in process on April 30:

Equivalent units of resources in April

Direct materials (3,400 units 80% complete)

To start and complete 44,800 units in April

(3) Direct Conversion

Materials Costs

669,200$ 521,840$

Equivalent units in April (see part 2 )

Work in Process: Finishing Department

Cost per equivalent unit in April

44,520$

631,120

514,360

April conversion (46,760 equivalent units × $11)

To finish units in process on April 1:

Conversion (2,800 units require 70% to complete)

Units started in April

Units in process during April

Requirements for the Molding Department in April

Flow of physical units: Molding Department

Units in beginning inventory, April 1

Input resources

Direct materials (2,800 units require 10% to complete)

Cost per equivalent unit in April

Costs incurred by Molding Department in April

April direct materials (45,080 equivalent units × $14)

Cost of beginning inventory, April 1 ($33,340 + $11,180)

Department in April:

To record the transfer of 47,600 units to the Finishing

47,600

44,800

Units in beginning inventory, April 1

Units started and completed in April

Units in ending inventory, April 30

Units transferred to Finishing Department in April

PROBLEM 18.7A

HOUND HAVENS (continued)

(5)

38,080$

b.

(1)

5,000

47,600

52,600

50,600

45,600

Units transferred to Finishing Dept. in April

Units in process during April

Units in beginning inventory, April 1

Units started and completed in April

(2) Molding Direct

Materials Materials Conversion

Molding materials

(5,000 units require 0% to complete) 0

Direct materials

(5,000 units require 70% to complete) 3,500

Conversion

(5,000 units require 60% to complete) 3,000

45,600 45,600 45,600

To start and complete 45,600 units in April

To start units in process on April 30:

47,600 49,600 49,200

(3) Molding Direct Conversion

Materials Materials Costs

Costs charged to Finishing Department

in April* 1,190,000$ 496,000$ 147,600$

Equivalent units in April [see part (2) ]

Cost per equivalent unit in April

Equivalent units of resources in April

To finish units in process on April 1:

Units in beginning inventory, April 1

Units started in April (see part a (1) )

Cost per equivalent unit in April

Input resources

Work in Process: Molding Department, April 30

Direct materials (2,720 equivalent units × $14)

Requirements for the Finishing Dept. in April

Flow of physical units: Finishing Department

7,480

45,560$

Conversion (680 equivalent units × $11)

Ending inventory in process, April 30

PROBLEM 18.7A

HOUND HAVENS (concluded)

(4) 1,922,800

Work in Process: Finishing Department 1,922,800

(5)

50,000$

56,800$

Conversion (600 equivalent units × $3)

Ending inventory in process, April 30

Direct materials (500 equivalent units × $10)

Finished Goods Inventory

To record the transfer of 50,600 units

Work in Process: Finishing Department,

Molding materials (2,000 equivalent units × $25)

to the Finished Goods

April 30

Total cost of units transferred 1,922,800$

Inventory in April:

50 Minutes, Strong

PROBLEM 18.8A

WILSON DYNAMICS

a.

1.

5,000

75,000

2. Direct

Materials Conversion

0

3,000

67,000 67,000

8,000

6,000

75,000 76,000

Direct materials (8,000 units 100% complete)

Conversion (8,000 units 75% complete)

Equivalent units of resources in July

3. Direct Conversion

Materials Costs

675,000$ 608,000$

Cost per equivalent unit in July

Equivalent units in July [see part (2) ]

4. 1,224,000

Work in Process: Forging Department 1,224,000

61,000$

Total cost of units transferred

July conversion (70,000 equivalent units × $8)

July direct materials (67,000 equivalent units × $9)

5. Work in Process: Forging Department, July 31

Requirements for the Forging Department in July

Flow of physical units: Forging Department

Units in beginning inventory, July 1

Units started in July

To finish units in process on July 1:

Input resources

To start and complete 67,000 units in July

To start units in process on July 31:

Conversion (5,000 units require 60% to complete)

Direct materials (5,000 units require 0% to complete)

Work in Process: Assembly Department

To record the transfer of 72,000 units to the Assembly

Department in July:

Cost of beginning inventory, July 1 ($45,000 + $16,000)

Costs incurred by Forging Department in July

Cost per equivalent unit in July

80,000

72,000

67,000

Units transferred to Assembly Department in July

Units in process during July

Units in ending inventory, July 31

Units in beginning inventory, July 1

Units started and completed in July