Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

PROBLEM 18-6 (Continued)

(i) Earnings per share =

$36,400

30,000 (1)

= $1.21.

(j) Price-earnings ratio =

$19.50

$1.21

= 16.1 times.

(l) Debt to assets =

$265,000

$638,000

= 41.5%.

PROBLEM 18-7

Accounts receivable turnover = 10 =

$11,000,000

Average accounts receivable

Averages accounts receivable =

$11,000,000

10

= $1,100,000

Net accounts receivables12/31/17 + $950,000

2

= $1,100,000

Profit margin = 14.5% = .145 =

Net income

$11,000,000

Net income = $11,000,000 X .145 = $1,595,000

Assets (12/31/17) = $7,500,000

Total current assets = $7,500,000 – $4,620,000 = $2,880,000

Inventory = $2,880,000 – $1,250,000 – $450,000 = $1,180,000

PROBLEM 18-7 (Continued)

Current ratio = 3.0 =

$2,880,000

Current liabilities

Inventory turnover = 4.8 =

Cost of goods sold

$1,720,000 + $1,180,000

2

PROBLEM 18-8

TERWILLIGER CORPORATION

Statement of Comprehensive Income

For the Year Ended December 31, 2017

Operating revenues

($12,850,000 – $1,500,000) ........................ $11,350,000

Operating expenses

($8,700,000 – $2,400,000) .......................... 6,300,000

Income from operations ............................... 5,050,000

Other revenues and gains ............................ 100,000

Discontinued operations

Loss from operations of discontinued division*,

net of $270,000 income

tax saving ........................................... $630,000

Gain from disposal of discontinued

division, net of $60,000 income tax .. 140,000 490,000

PROBLEM 18-9

JAIME CORPORATION

Statement of Comprehensive Income

For the Year Ended December 31, 2017

Net sales ............................................................. $1,700,000

Cost of goods sold ............................................ 1,100,000

Gross profit ........................................................ 600,000

Discontinued operations

Income from operations of discontinued

division, net of $5,000 income tax ........... 15,000

BYP 18-1 FINANCIAL REPORTING PROBLEM

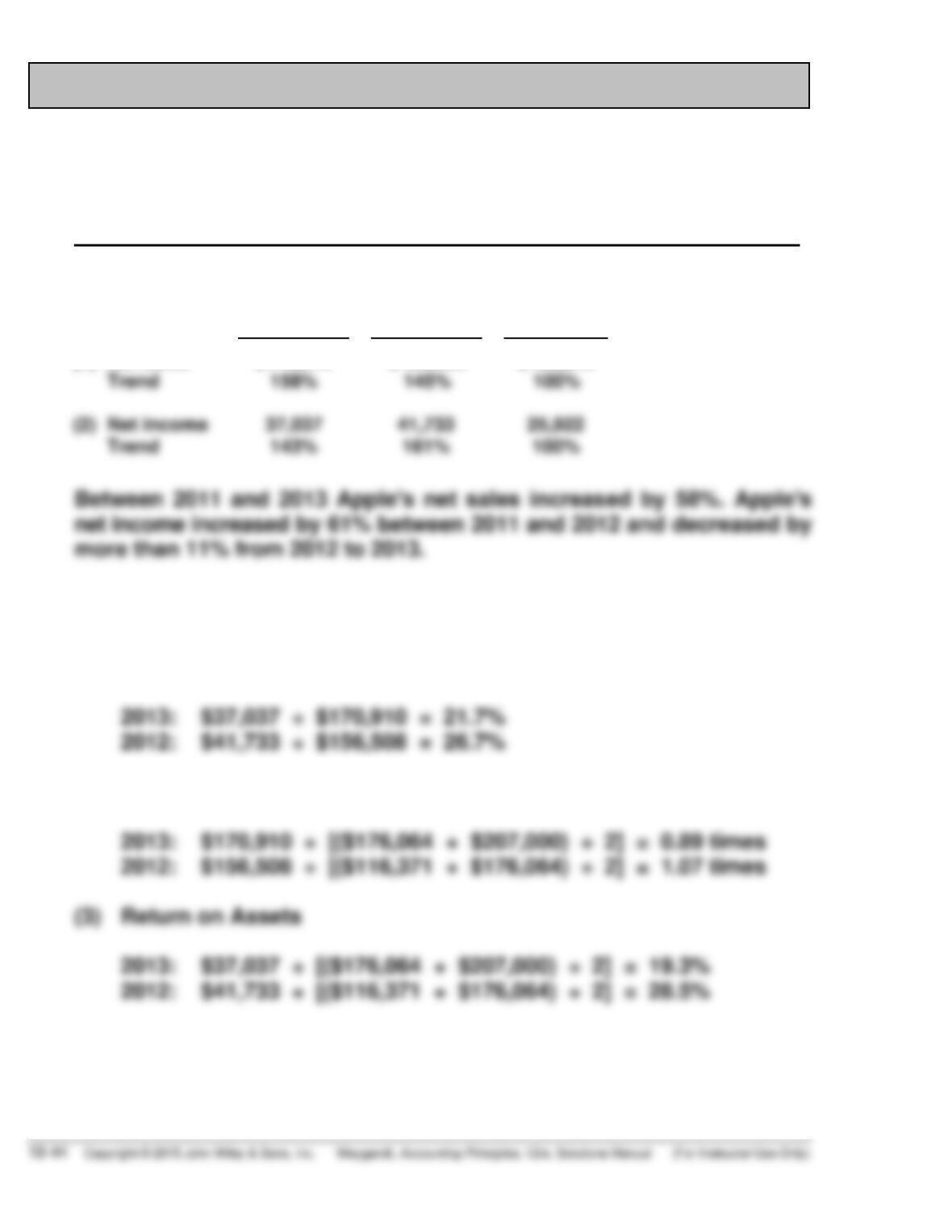

(a) APPLE, INC.

Trend Analysis of Net Sales and Net Income

For the Three Years Ended 2013

Base Period 2011—(in millions)

2013

2012

2011

(1)

Net sales

Trend

$170,910

158%

$156,508

145%

$108,249

100%

(b) (dollar amounts in millions)

(1) Profit Margin

2013: $37,037 ÷ $170,910 = 21.7%

2012: $41,733 ÷ $156,508 = 26.7%

(2) Asset Turnover

BYP 18-1 (Continued)

(4) Return on Common Stockholders’ Equity

(c) (dollar amounts in millions)

(1) Debt to Assets ratio

2013: $83,451 ÷ $207,000 = 40.3%

2012: $57,854 ÷ $176,064 = 32.9%

Since creditors are providing only 40% of Apple’s total assets, its long-

term solvency is not in jeopardy.

(2) Times Interest Earned

(d) Substantial amounts of important information about a company are not

in its financial statements. Events involving such things as industry

changes, management changes, competitors’ actions, technological

BYP 18-2 COMPARATIVE ANALYSIS PROBLEM

(a)

PepsiCo

Coca-Cola Company

(1)

(i)

Percentage increase

in net sales

$66,415 − $65,492

= 1.4%

$46,854 − $48,017

= –2.4%

$65,492

$48,017

(ii)

Percentage increase

(decrease) in net

income

$6,740 − $6,178

= 9.1%

$8,584 − $9,019

= −4.8%

$6,178

$9,019

(b) PepsiCo’s net sales increased 1.4% while Coca-Cola’s decreased over

2.4%. PepsiCo’s net income increased 9.1% while Coca-Cola’s net

income decreased 4.8% from 2012 to 2013. PepsiCo’s total assets

increased 3.8% while Coca-Cola increased its assets 4.5%.

BYP 18-3 COMPARATIVE ANALYSIS PROBLEM

(a)

Amazon

Wal-Mart

(1)

(i)

Percentage increase

in net sales

$60,903 − $51,733

= 17.7%

$473,076 − $465,604

= 1.6%

$51,733

$465,604

(ii)

Percentage increase

(decrease) in net

income

$274 − (39)

= 802.6%

$16,022 − $16,999

= (5.7)%

(39)

$16,999

(b) Amazon’s net sales increased 17.7% while Wal-Mart’s increased 1.6%.

Amazon’s net income increased 802.6% while Wal-Mart’s net income

decreased 5.7% from 2012 to 2013. Amazon’s total assets increased 23.4%

while Wal-Mart increased its assets 0.8%.

BYP 18-4 DECISION MAKING ACROSS THE ORGANIZATION

The current ratio increase is a favorable indication as to liquidity, but

alone tells little about the going-concern prospects of the client. From

this ratio change alone, it is impossible to know the amount and direction

of the changes in individual accounts, total current assets, and total

current liabilities. Also unknown are the reasons for the changes.

The acid-test ratio decrease is an unfavorable indication as to liquidity,

especially when the current-ratio increase is also considered. This decline

is also unfavorable as to the going-concern prospects of the client because

it reflects a declining cash position and raises questions as to reasons

for the increases in other current assets, such as inventories.

The increase in net income is a favorable indicator for both solvency

and going-concern prospects, although much depends on the quality of

receivables generated from sales and how quickly they can be converted

into cash. If there has been a decline in sales, a significant factor is that

management has been able to reduce costs to produce an increase in

earnings. Indirectly, the improved income picture may have a favorable

impact on solvency and going-concern potential by enabling the client

to borrow currently (if it needs to do so) to meet cash requirements.

BYP 18-4 (Continued)

The collective implications of these data alone are that the client entity

is about as solvent and as viable a going concern at the end of the current

year as it was at the beginning although there may be a need for short-term

operating cash.

BYP 18-5 REAL-WORLD FOCUS

(a) Optional elements include:

Financial highlights

Letter to stockholders

Corporate message

(b) SEC-required elements include:

Auditors’ report

Management discussion

Financial statements and notes

Selected financial data

(c) Management discussion. This series of short, detailed reports discusses and

the adequacy of liquid and capital resources to fund operations.

(d) Auditors’ report. This summary of the findings of an independent firm

of certified public accountants shows whether the financial statements

are complete, reasonable, and prepared consistent with generally accepted

accounting principles (GAAP) at a set time.

BYP 18-6 COMMUNICATION ACTIVITY

To: Abby Landis

From: Accounting Major

Subject: Financial Statement Analysis

The bases for comparison in analyzing financial statement are:

a. Intracompany—This basis compares an item or financial relationship

within a company in the current year with the same item or relation-

ship in one or more prior years.

BYP 18-7 ETHICS CASE

(a) The stakeholders in this case are:

Dave Schonhardt, president of Schonhardt Industries.

Steven Verlin, public relations director.

You, as controller of Schonhardt Industries.

(b) The president’s press release is deceptive and incomplete and to that

extent his actions are unethical.

(c) As controller you should at least inform Steven, the public relations

director, about the biased content of the release. He should be aware

BYP 18-8 ALL ABOUT YOU

Student responses will vary. We suggest that in class you ask for a few stu-

dents to share their responses in order to increase students understanding

of the various reasons why different people will choose different investment

vehicles.

BYP 18-9 FASB CODIFICATION ACTIVITY

(a) Discontinued Operations

205-20-45-1 The results of operations of a component of an entity that

either has been disposed of or is classified as held for sale under the

requirements of paragraph 360-10-45-9, shall be reported in discontinued

operations in accordance with paragraph 205-20-45-3 if both of the

following conditions are met:

a. The operations and cash flows of the component has been (or will be)

eliminated from the ongoing operations of the entity as a result of

(b) Comprehensive Income

The change in equity (net assets) of a business entity during a period

from transactions and other events and circumstances from nonowner

IFRS 18-1 INTERNATIONAL FINANCIAL REPORTING PROBLEM

(a) The company’s profit margin was 11.8% for 2013 (€3,436 €29,149).

Profit margin decreased from 13% in 2011 (€3,065 €23,659).

(b) Operating profit for 2013 was €5,894.