18–1

CHAPTER 18

UNDERSTANDING THE ISSUES

1. Separating the accounting for current activ-

ities into restricted and unrestricted funds

allows for detailed reporting of resources

and spending. This is often done to satisfy

2. Users of not-for-profit financial information

are interested in the fair value of invest-

ments regardless of their trading status.

Not-for-profits, particularly foundations and

3. Public support captures all forms of dona-

tions to a not-for-profit organization, includ-

ing direct contributions of all types (cash,

assets, services, reduced liabilities, free

of goods or services, and realized and un-

realized earnings from investments.

4. A contribution is a nonreciprocal transac-

tion where one part gives something of

contribution. In the second example, a lia-

bility to the ultimate recipient is recorded.

5. A VHWO must include a statement of func-

tional expense as part of its financial

detailed expense patterns by program.

6. (Appendix) A VHWO may wish to present

its financial information on a fund basis ra-

Ch. 18—Exercises 18–2

EXERCISES

EXERCISE 18-1

EXERCISE 18-2

(1) C There is a permanent restriction on this donation.

(3) A If there is no law regarding recognition of unrealized gains/losses, an organization may

(4) B Investment income from donor-restricted permanent endowments is recognized as

temporarily restricted if the donor restricts the income as to use or specific time period.

(5) B The gain is not permanently restricted unless there is a donor stipulation or legal re-

EXERCISE 18-3

(1) The measurement focus of state and local government’s government-type activities is flows

of financial resources, whereas the measurement focus of voluntary health and welfare

organizations (VHWOs) is flows of economic resources. Some financial activities of a gov-

ernment, such as those of operating a utility, may be better reported (i.e., the financial

18–3 Ch. 18—Exercises

Exercise 18-3, Concluded

(2) State and local governments present revenues and expenditures for the governmental funds

separate from the proprietary funds. In addition, government-wide financial statements are

(3) Depreciation expense is reported in the statement of activities of a government. Accumu-

(4) A voluntary health and welfare organization may use a separate fund to account for fixed

assets called the Plant Fund or Land, Building, and Equipment Fund.

If capital assets are purchased by the Plant Fund, the usual entry is made as follows:

Land, Building, and Equipment …………………………………………. xxx

Cash or Some Payable ………………………………………………. xxx

The purpose of a voluntary health and welfare organization is to provide a service to the

community. Because there are usually numerous voluntary health and welfare organizations

competing for donations, it is only proper that donors be able to evaluate the cost of the ser-

vices provided in an effort to see which organizations use donations most efficiently. The

use of fixed assets in an organization represents a cost of providing a service, and so it is

appropriate for a voluntary health and welfare organization to show depreciation as a cost of

providing its service to the community.

The Land, Building, and Equipment Fund records any gain or loss on the sale of fixed

assets as revenue of the fund. If the proceeds of the sale are not legally required to be rein-

vested in fixed assets, the funds should be transferred to the unrestricted fund by entries re-

flected as direct additions and reductions to the respective fund balances.

EXERCISE 18-4

(1) d Donated works of art, historical treasures, or similar objects that are not held for public

(3) b Contributed services must be provided by persons possessing specialized skills that

would need to be purchased if not donated. There is no licensing requirement.

(5) b Rather than requiring restricted contributions to first be classified as restricted and then

EXERCISE 18-5

Supporting schedule

Drug Alcohol Weight Fund General and Total

Rehabilitation Recovery Control Raising Administrative Amount

Secretarial salary …… $ 0 $ 0 $ 0 $ 0 $ 2,000 $ 2,000

Office supplies ………. 600 300 300 300 1,500 3,000

18–5 Ch. 18—Exercises

Exercise 18-5, Concluded

Whole Life Clinic

Statement of Activities

For Year Ended December 31, 2019

Temporarily Total All

Unrestricted Restricted Funds

Public support and revenue:

Public support ……………………………………………………. $ 35,000 $ 35,000

Revenue ……………………………………………………………. 12,000 12,000

Net assets released from restriction:

Expenses:

Program services:

Drug rehabilitation …………………………………………. $ 11,700 $ 11,700

Alcohol recovery ……………………………………………. 8,950 8,950

Weight control ………………………………………………. 11,850 11,850

EXERCISE 18-6

(1) Cash ………………………………………………………………………………….. 9,000

(2) Cash ………………………………………………………………………………….. 22,000

(3) Provision for Uncollectible Pledges ………………………………………… 3,200

Exercise 18-6, Concluded

(4) Cash ………………………………………………………………………………….. 12,000

Special Events Support …………………………………………………… 12,000

(5) Car for Resale …………………………………………………………………….. 75,000

(6) Cash ($70,000 – $20,000) …………………………………………………….. 50,000

Pledges Receivable ……………………………………………………………… 30,000

Fund-Raising Expense …………………………………………………………. 20,000

EXERCISE 18-7

(1) Cash ………………………………………………………………………………….. 20,000

(2) Cash ………………………………………………………………………………….. 10,000

Accumulated Depreciation …………………………………………………….. 9,000

(3) Depreciation Expense ………………………………………………………….. 9,000

18–7 Ch. 18—Exercises

Exercise 18-7, Concluded

(4) Land, Building, and Equipment ………………………………………………. 18,000

Accounts Payable (or Vouchers Payable) ………………………….. 18,000

(5) Accounts Payable (or Vouchers Payable) ……………………………….. 18,000

EXERCISE 18-8

(1) Cash ………………………………………………………………………………….. 400,000

Legacies and Bequests—Permanently Restricted ………………. 400,000

(2) Cash ………………………………………………………………………………….. 207,000

Investments …………………………………………………………………… 200,000

(3) Cash ………………………………………………………………………………….. 15,000

(4) Increase in Carrying Value ……………………………………………………. 7,000

Ch. 18—Problems 18–8

PROBLEMS

PROBLEM 18-1

(1) a Fund raising and administrative and general expenses are classified as supporting

services.

(2) b Amounts received (or promised) and restricted for future periods are recorded as public

(3) d Amounts not available to spend until 2018 are classified as temporarily restricted.

(5) a Contributions are $400,000 shown in the statement of activities as follows:

(6) c Printing an annual report is an administrative function.

PROBLEM 18-2

(1) b To be recognized as donated services, the service must be of a skilled nature and pur-

(2) d Net Assets are reported in three categories: unrestricted net assets, temporarily

restricted net assets, and permanently restricted net assets.

(4) b Gains and losses should be reported in the statement of activities as increases or de-

creases in unrestricted net assets unless otherwise stipulated by donor or by law.

18–9 Ch. 18—Problems

PROBLEM 18-3

(1) e Both are recorded as a contribution increasing public support in the period received.

(2) b The contributions have not yet been expended. They are part of resources and tempo-

(3) a The entry given is the typical journal entry to record board-designated intentions for

(4) d Not-for-profit organizations may choose to record unrealized gains/losses on marketa-

(5) d When investments are carried at fair value, changes in total fair value are recorded

PROBLEM 18-4

(1) Event

(a) Accounts Receivable ……………………………………………………… 2,200,000

Patient Service Revenue …………………………………………… 2,200,000

Provision for Uncollectible Accounts Receivable ……………….. 92,000

Allowance for Uncollectibles and Contractual

Problem 18-4, Continued

(e) Assets Whose Use Is Limited—Cash ……………………………….. 50,000

Cash ………………………………………………………………………. 50,000

Note: No outside restriction exists. An additional entry

to designate the unrestricted net assets may

Reclassification In—Unrestricted—Expiration

of Time Restrictions ………………………………………… 10,000

(g) Plant and Equipment ……………………………………………………… 250,000

Accounts Payable …………………………………………………….. 250,000

(h) Nursing Services Expenses ……………………………………………. 1,120,000

Problem 18-4, Concluded

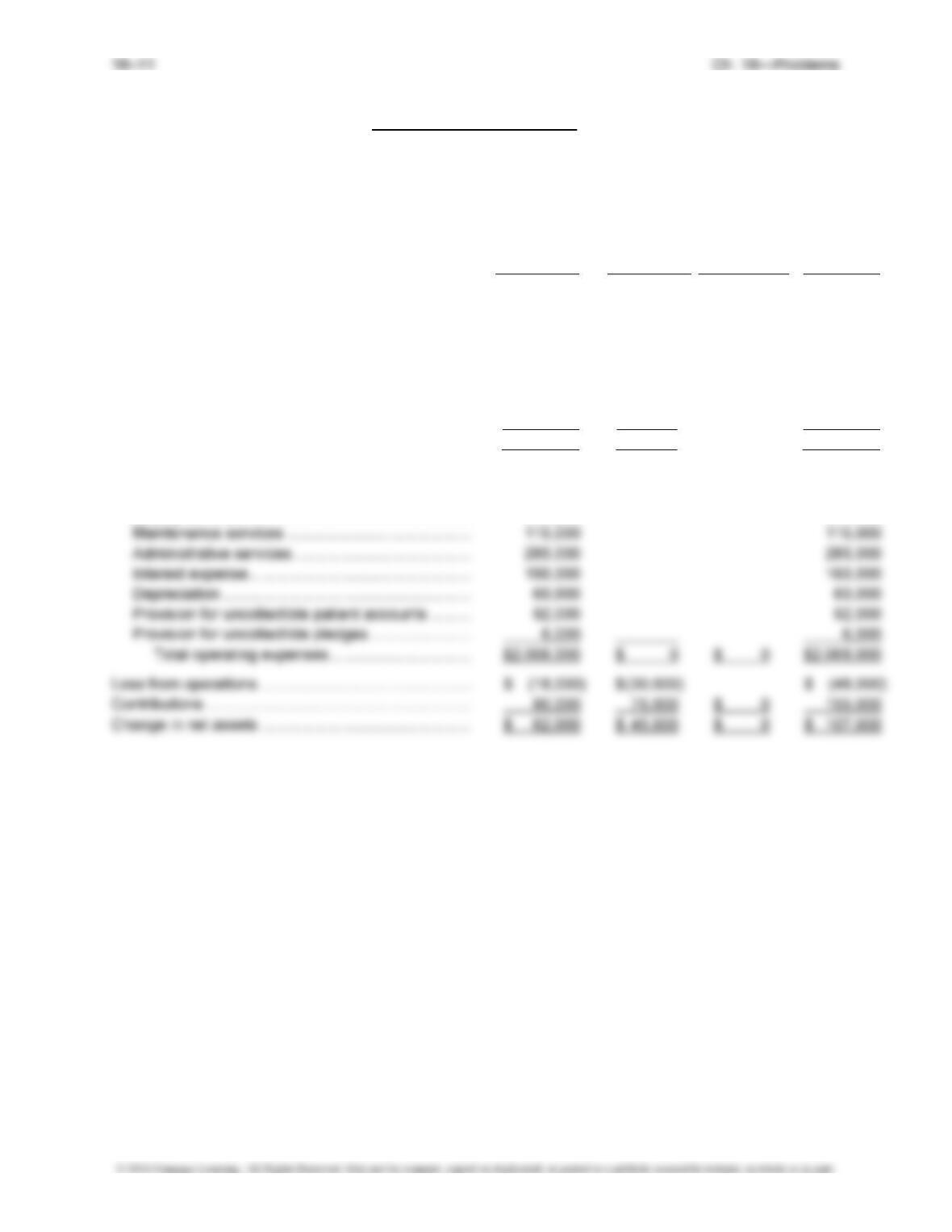

(2) Fall Nursing Home, Inc.

Statement of Activities

For Year Ended December 31, 2019

Temporarily Permanently

Unrestricted Restricted Restricted Total

Patient service revenue (net of $120,000 contractual

adjustments) …………………………………………………. $2,020,000 $2,020,000

Net assets released from restrictions:

Satisfaction of equipment acquisition restrictions

(depreciation) …………………………………………… 20,000 $(20,000) 0

Expiration of time restrictions

(term endowment expired) …………………………. 10,000 (10,000) 0

Total revenue and other support ……………………… $2,050,000 $(30,000) $2,020,000

Operating expenses:

Nursing services ……………………………………………. $1,120,000 $1,120,000

Dietary services …………………………………………….. 230,000 230,000

PROBLEM 18-5

(1) Land, Building, and Equipment ……………………………………………… 200,000

(2) Land, Building, and Equipment ………………………………………………. 9,000

(3) Land, Building, and Equipment ………………………………………………. 14,000

(4) Mortgage Payable ………………………………………………………………. 10,000

Interest Expense (14% × $160,000) ……………………………………….. 22,400

(5) Cash ………………………………………………………………………………….. 1,800

Accumulated Depreciation …………………………………………………….. 2,000

(6) Accumulated Depreciation …………………………………………………….. 7,000

(7) Depreciation Expense ………………………………………………………….. 46,000

Accumulated Depreciation ……………………………………………….. 46,000

To record annual depreciation.

(8) Land, Building, and Equipment ………………………………………………. 75,000

Cash …………………………………………………………………………….. 75,000

(9) Accounts Payable ………………………………………………………………… 9,000

18–13 Ch. 18—Problems

PROBLEM 18-6

(1) Pledges Receivable ……………………………………………………………… 800,000

Contributions—Unrestricted ……………………………………………… 800,000

(2) Cash ………………………………………………………………………………….. 470,000

Pledges Receivable ………………………………………………………… 470,000

(3) Cash ………………………………………………………………………………….. 35,000

Special Events Support—Unrestricted ………………………………. 12,000

(4) Medical Services Program ……………………………………………………. 60,000

(5) Management and General Services ……………………………………….. 150,000

(6) Buildings and Equipment ………………………………………………………. 18,000

Cash …………………………………………………………………………….. 18,000

(7) Depreciation Expense ………………………………………………………….. 15,000

Accumulated Depreciation ……………………………………………….. 15,000

(8) Vouchers Payable ……………………………………………………………….. 330,000

PROBLEM 18-7

(1) Event Journal Entry Debit Credit

(a) Cash ……………………………………………………………………………. 20,000

Revenue—Annual Dues ……………………………………………. 20,000

(b) Cash ……………………………………………………………………………. 31,000

Revenue—Snack Bar and Soda Fountain …………………… 31,000

(g) Cash ……………………………………………………………………………. 5,000

Public Support—Unrestricted Bequests ………………………. 5,000

(h) Investments ………………………………………………………………….. 7,000

Unrealized Gain on Investments—Unrestricted ……………. 7,000

(i) Depreciation Expense—House ……………………………………….. 9,000

18–15 Ch. 18—Problems

Problem 18-7, Concluded

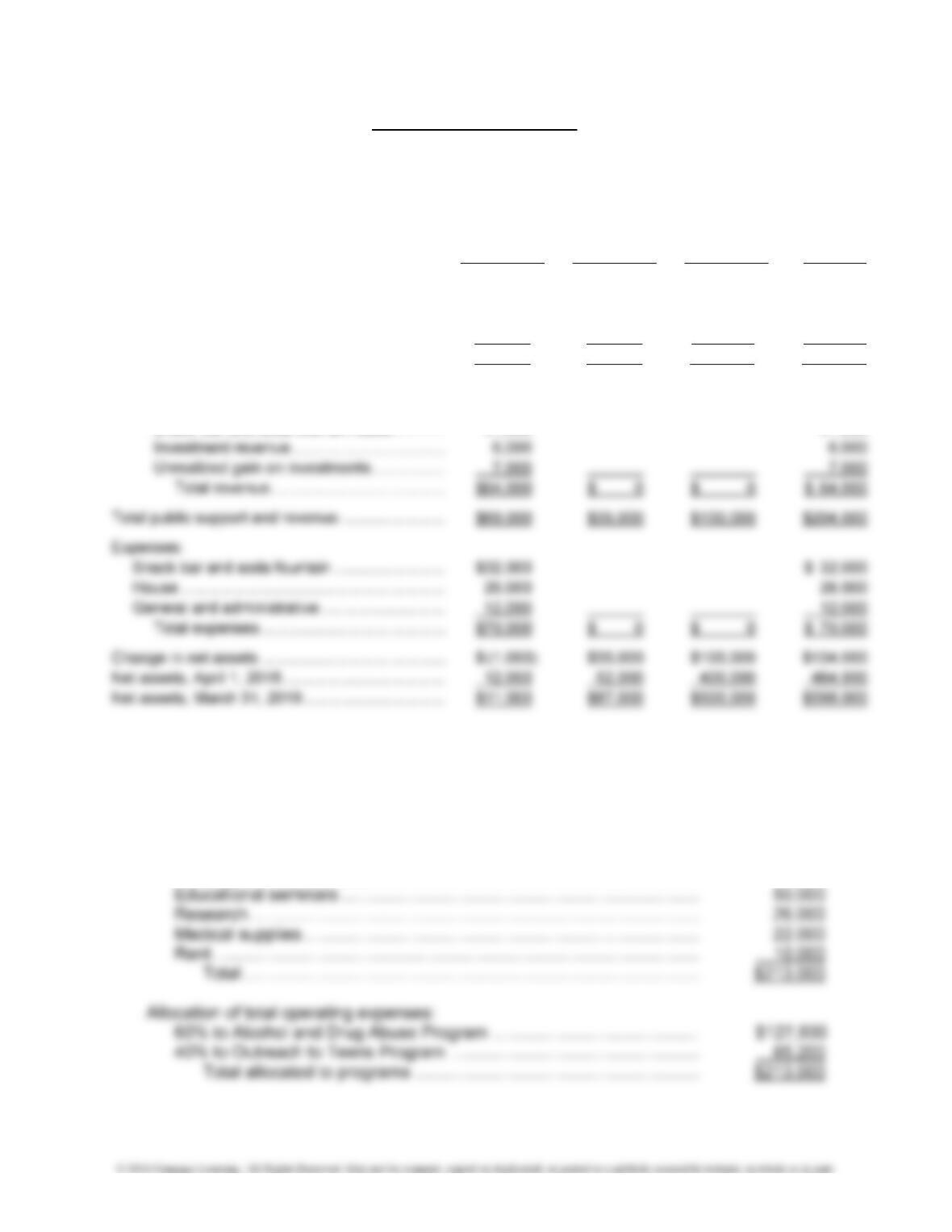

(2) Mayfair Sports Club

Statement of Activities

For Year Ended March 31, 2019

Temporarily Permanently

Unrestricted Restricted Restricted Total

Public support and revenue:

Public support:

Contributions ………………………………………. $35,000 $100,000 $135,000

Unrestricted bequests ………………………….. $ 5,000 5,000

Total public support …………………………. $ 5,000 $35,000 $100,000 $140,000

Revenue:

Annual dues ……………………………………….. $20,000 $ 20,000

Snack bar and soda fountain sales ………… 31,000 31,000

PROBLEM 18-8

(1) Total of allocable operating expenses financed by donor-restricted contributions:

Salaries and payroll taxes …………………………………………………………… $ 33,000

Telephone and miscellaneous …………………………………………………….. 2,000

Nursing and medical fees …………………………………………………………… 70,000

Problem 18-8, Continued

Journal entry:

Alcohol and Drug Abuse Program …………………………………….. 127,800

Outreach to Teens Program …………………………………………….. 85,200

(2) Outreach Clinic

Allocation of Expenses Financed by Unrestricted Resources

For Year Ended December 31, 2019

Programs

Supporting Services

Total Alcohol and Outreach Manage- Fund

Expense Allocated Amount Drug Abuse to Teens ment Raising

Salaries and payroll taxes …………………… $ 73,000 $ 21,900 $ 14,600 $21,900 $14,600

Telephone and miscellaneous …………….. 20,000 4,000 4,000 3,000 9,000

(3) Alcohol and Drug Abuse Program ………………………………………….. 225,200

Outreach to Teens Program ………………………………………………….. 125,700

Management and General Services ……………………………………….. 24,900

Fund-Raising Services ………………………………………………………… 54,200

Problem 18-8, Concluded

(4) Alcohol and Drug Abuse Program ………………………………………….. 24,000

Outreach to Teens Program ………………………………………………….. 4,800

Management and General Services ………………………………………. 14,400

PROBLEM 18-9

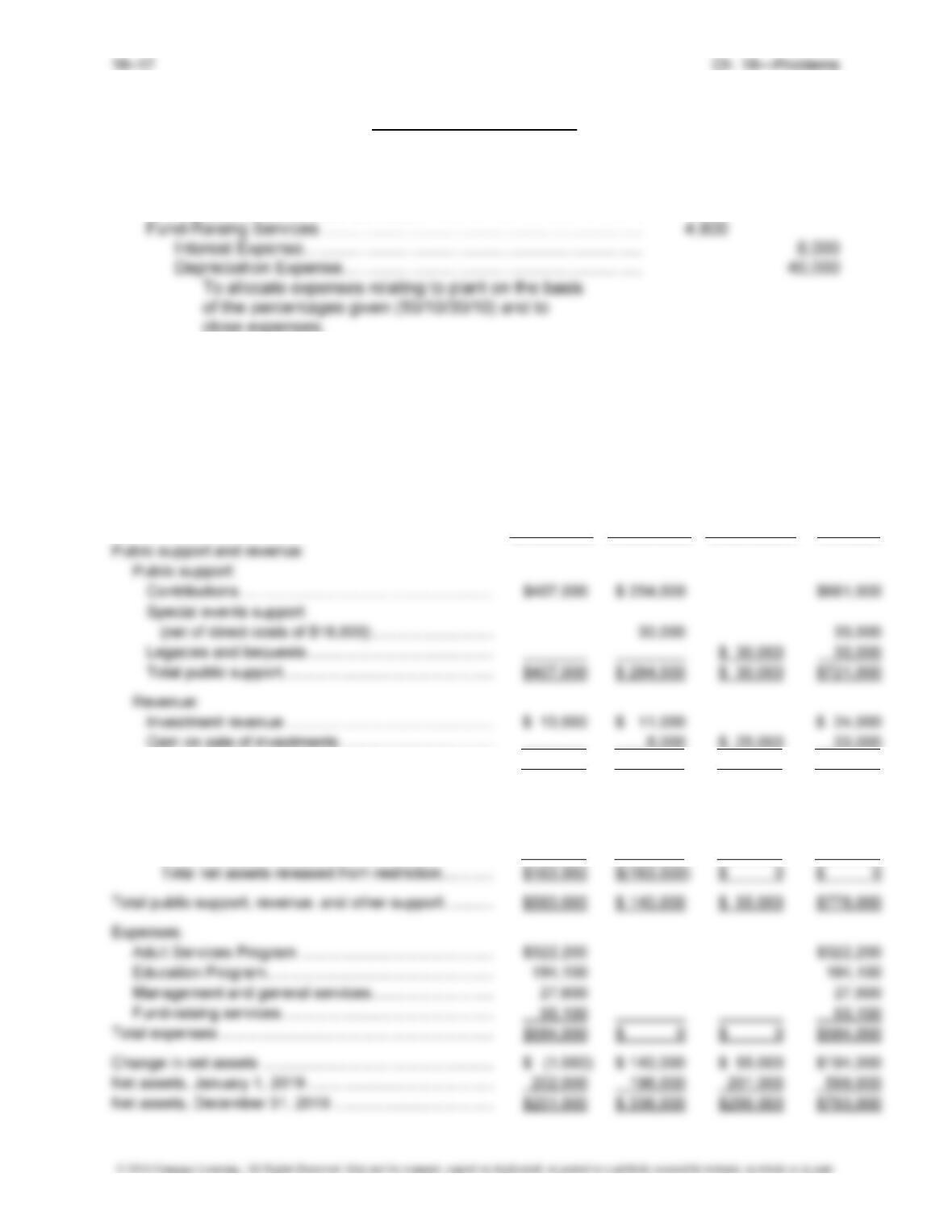

(1) We Care

Statement of Activities

For Year Ended December 31, 2019

Temporarily Permanently

Unrestricted Restricted Restricted Total

Total revenue ………………………………………………. $ 13,000 $ 19,000 $ 25,000 $ 57,000

Net assets released from restriction:

Satisfaction of program restrictions ………………… $143,000 $(143,000) $ 0

Satisfaction of equipment acquisition

restrictions ……………………………………………….. 20,000 (20,000) 0

Problem 18-9, Concluded

(2) Closing entries:

Contributions—Unrestricted ……………………………………………… 407,000

Investment Revenue—Unrestricted …………………………………… 13,000

Adult Services Program ……………………………………………… 322,200

Education Program ……………………………………………………. 184,100

Management and General Services …………………………….. 27,600

Fund-Raising Services ……………………………………………….. 50,100

PROBLEM 18-10

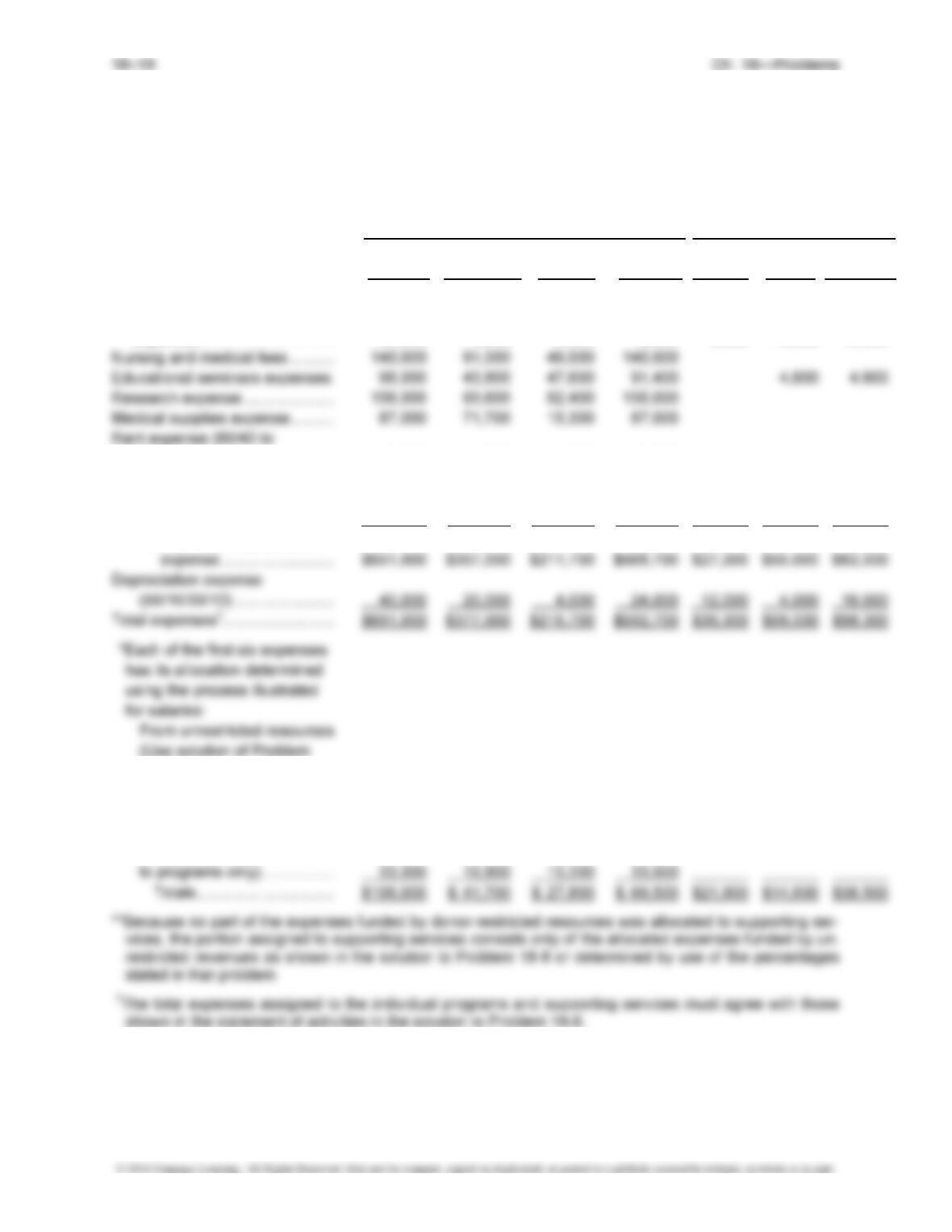

We Care

Statement of Functional Expenses

For Year Ended December 31, 2019

Program Services Supporting Services**

Total Alcohol and Outreach Total Manage- Fund Total

All Funds Drug Abuse to Teens Programs ment Raising Supporting

Salaries and payroll taxes* ……… $ 106,000 $ 41,700 $ 27,800 $ 69,500 $21,900 $14,600 $36,500

Telephone and miscellaneous

expenses …………………………. 22,000 5,200 4,800 10,000 3,000 9,000 12,000

programs) ………………………. 10,000 6,000 4,000 10,000

Interest expense (50/10/30/10) .. 8,000 4,000 800 4,800 2,400 800 3,200

Provision for uncollectible

pledges ……………………………. 26,000 26,000 26,000

Total before depreciation

18-8 or percentage

allocations in Problem

18-8.) …………………………….. $ 73,000 $ 21,900 $ 14,600 $ 36,500 $21,900 $14,600 $36,500

From donor-restricted

contributions (split 60/40