SOLUTIONS TO PROBLEMS SET B

20 Minutes, Easy

PROBLEM 17.1B

WINONA ENTERPRISES

a.

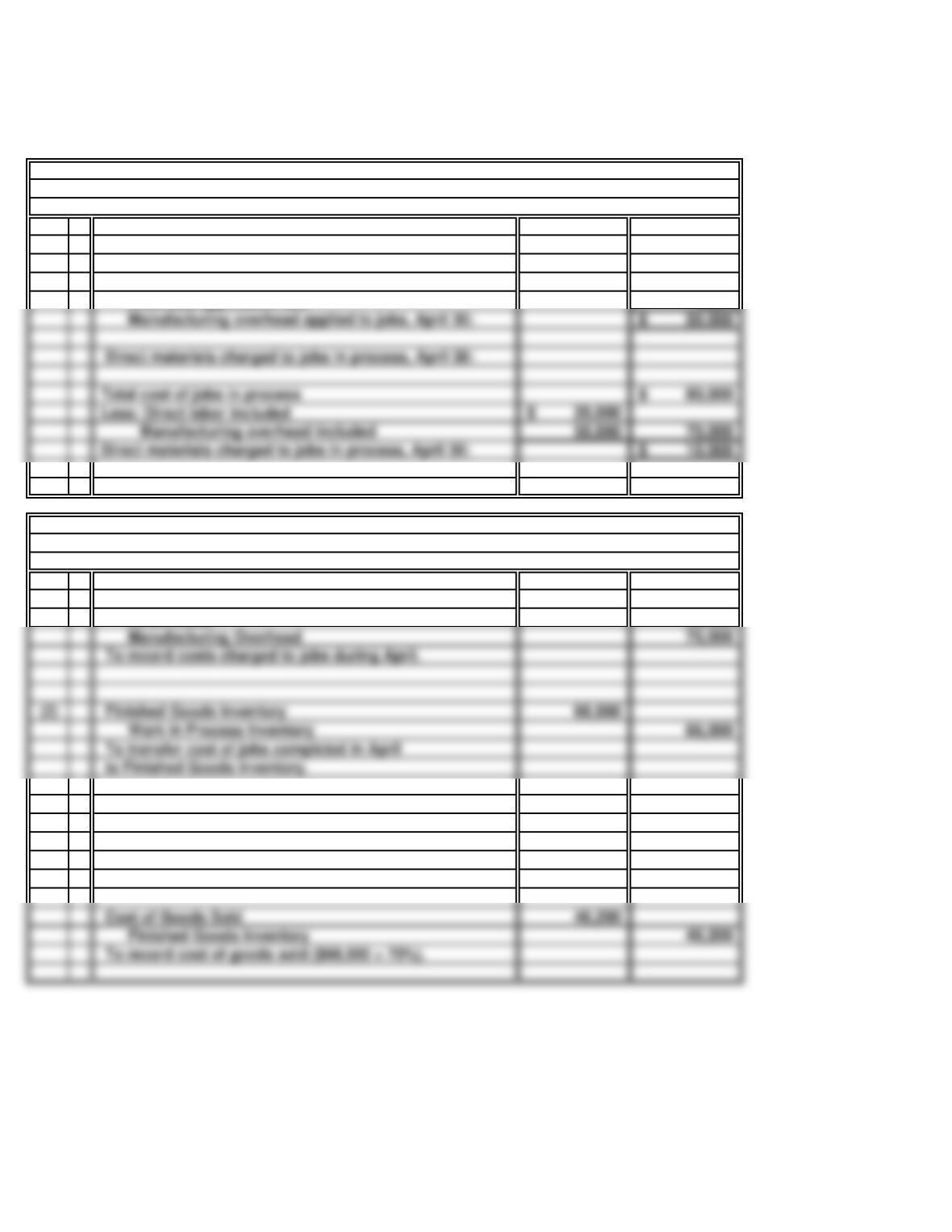

Manufacturing overhead charged to jobs in process,

April 30:

Direct labor charged to jobs in process, April 30: 20,000$

Overhead application rate 250%

b.

(1) Work in Process Inventory 130,000

Materials Inventory 25,000

Direct Labor 30,000

Manufacturing Overhead 75,000

To record costs charged to jobs during April.

(2) Finished Goods Inventory 66,000

Work in Process Inventory 66,000

To transfer cost of jobs completed in April

to Finished Goods Inventory.

(3) Cash 98,000

Sales 98,000

To record cash sale of 70% of goods completed

in April.

Finished Goods Inventory 46,200

To record cost of goods sold ($66,000 × 70%).

General Journal

Manufacturing overhead applied to jobs, April 30: 50,000$

Direct materials charged to jobs in process, April 30:

Manufacturing overhead included 50,000 70,000

15 Minutes, Easy

PROBLEM 17.2B

FARGO DEVELOPMENT CO.

General Journal

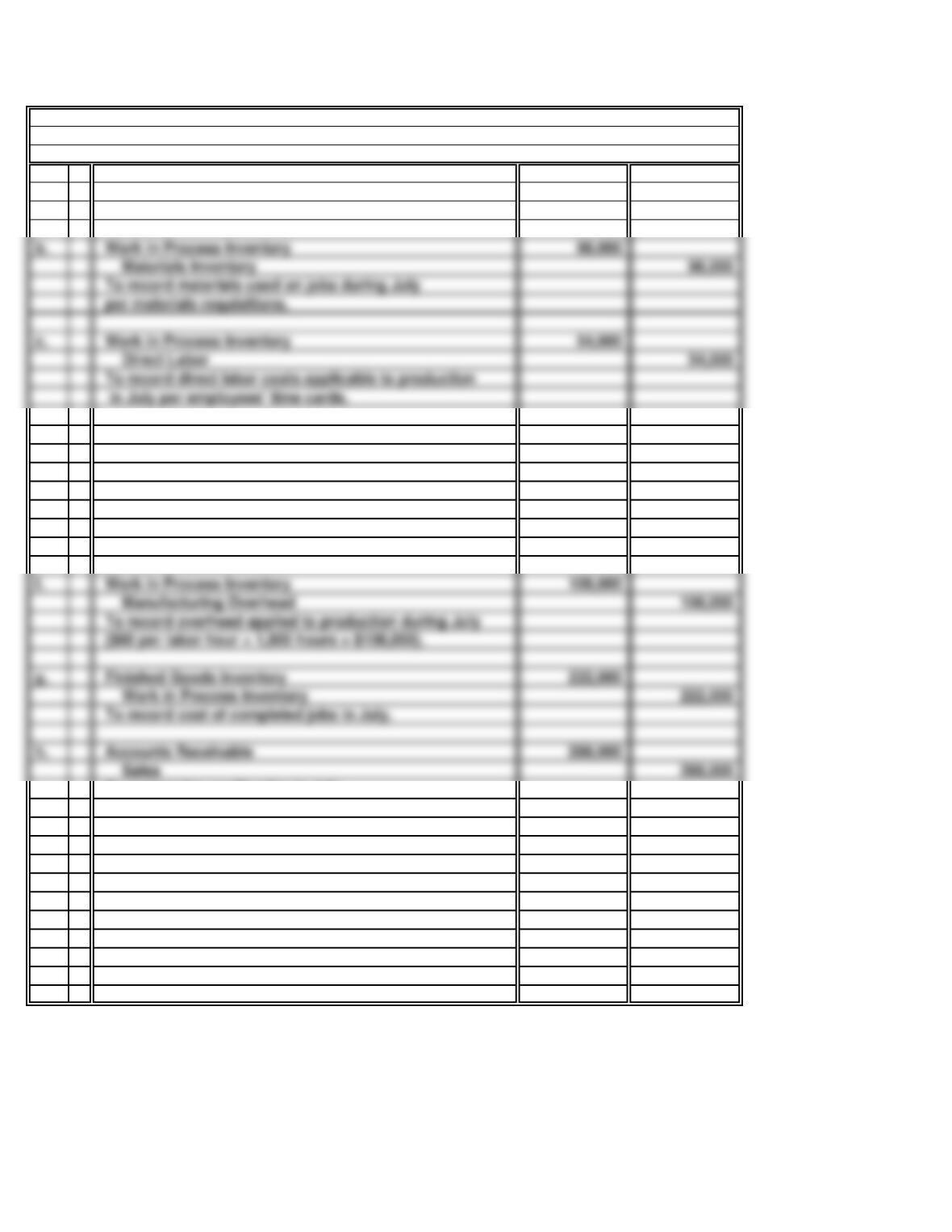

a. Materials Inventory 100,000

Accounts Payable 100,000

To record purchases of direct materials during July.

d. Direct Labor 50,000

Cash 50,000

To record direct labor payrolls paid in July.

e. Manufacturing Overhead 110,000

Accounts Payable 110,000

To record actual overhead costs in July.

f. Work in Process Inventory 108,000

Manufacturing Overhead 108,000

To record overhead applied to production during July

($60 per labor hour × 1,800 hours = $108,000).

g. Finished Goods Inventory 222,000

Work in Process Inventory 222,000

To record cost of completed jobs in July.

h. Accounts Receivable 288,000

To summarize credit sales in July.

Cost of Goods Sold 180,000

Finished Goods Inventory 180,000

To record cost of units sold during July.

b. Work in Process Inventory 98,000

Materials Inventory 98,000

To record materials used on jobs during July

per materials requisitions.

c. Work in Process Inventory 54,000

Direct Labor 54,000

To record direct labor costs applicable to production

30 Minutes, Medium

PROBLEM 17.3B

LINCOLN ESTATES

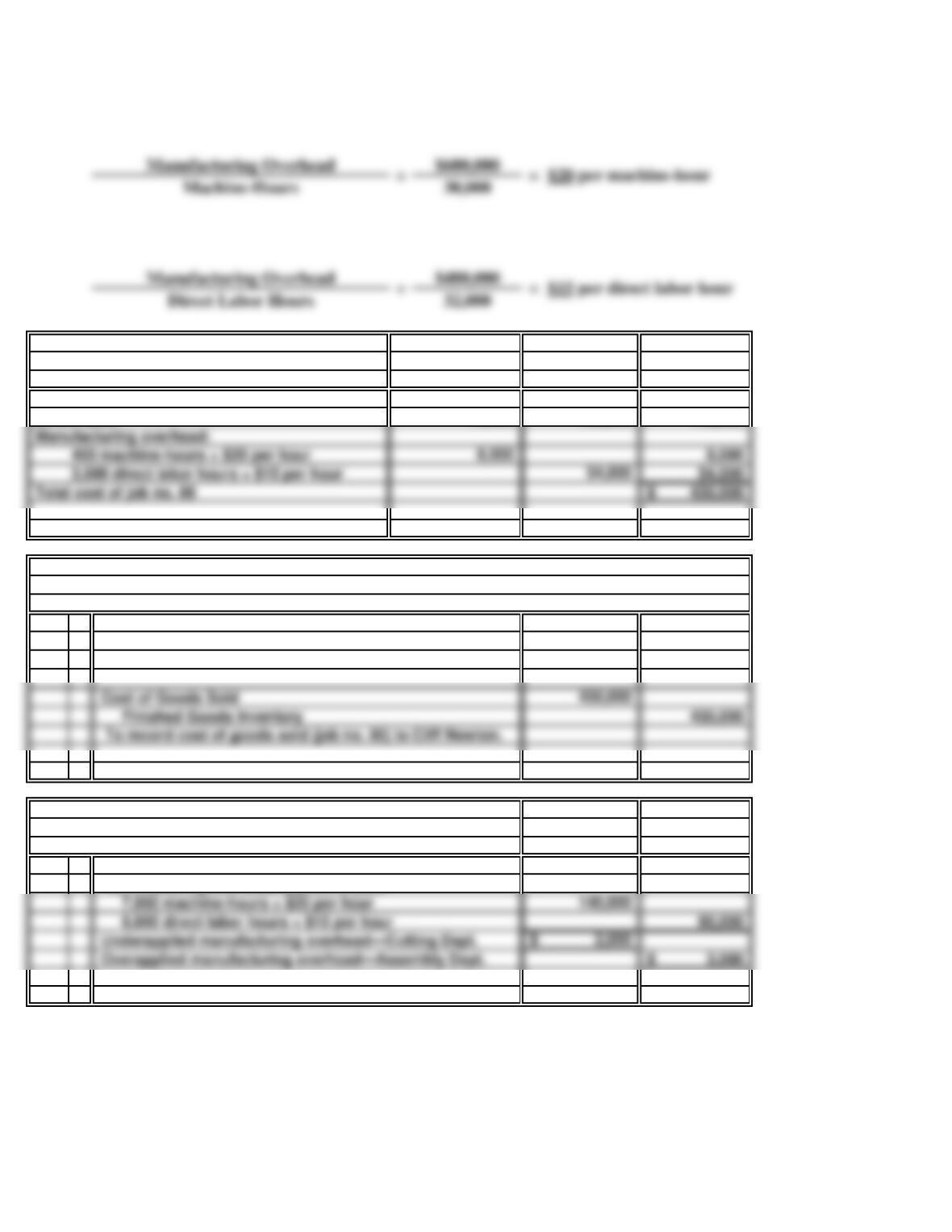

a. Cutting Department overhead application rate based on machine-hours:

Assembly Department overhead application rate based on direct labor hours:

b. Job no. 80

Total

Direct materials 250,000$

Direct labor

118,000

Manufacturing overhead:

Total cost of job no. 80 430,000$

c.

General Journal

Accounts Receivable (Cliff Newton)

Sales 602,000

To record revenue from sale to Cliff Newton.

Cost of Goods Sold

To record cost of goods sold (job no. 80) to Cliff Newton.

430,000

d.

Assembly

Department

Actual manufacturing overhead for first quarter 87,000$

Manufacturing overhead applied to jobs:

Cutting

Department

142,000$

Assembly

108,000

602,000

150,000$

Department

Department

100,000$

10,000

Cutting

30 Minutes, Medium

PROBLEM 17.4B

MONARK ELECTRONICS

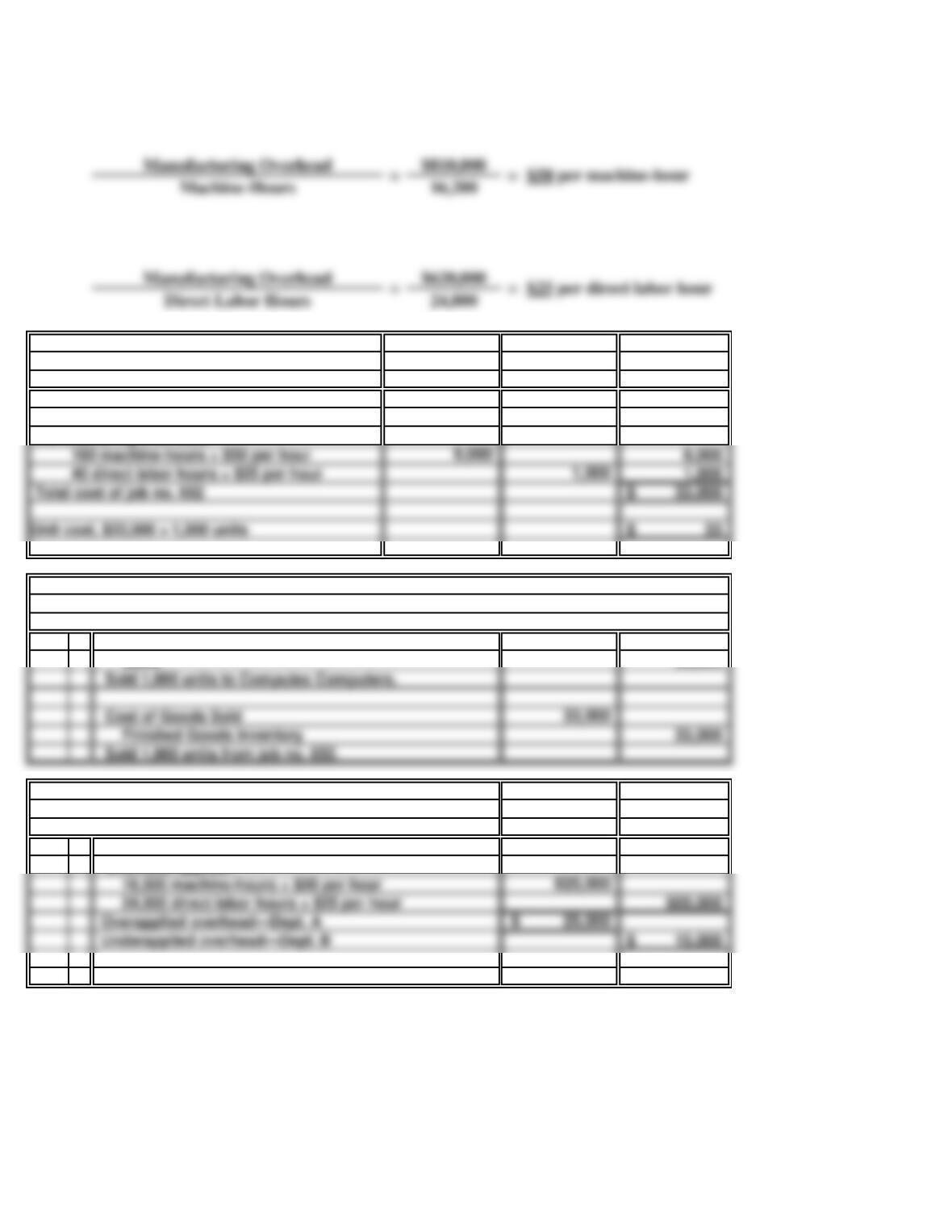

a. Department A overhead application rate:

Department B overhead application rate:

b. Job no. 652

Total

Direct materials 20,750$

Direct labor

2,250

Manufacturing overhead:

Total cost of job no. 652 33,000$

Unit cost, $33,000 ÷ 1,000 units 33$

1,000

9,000

c.

General Journal

Accounts Receivable (Computex Computers)

Sales 50,000

Sold 1,000 units to Computex Computers.

Cost of Goods Sold

Sold 1,000 units from job no. 652.

d.

Dept. B

Actual overhead for the year 615,000$

Overhead applied:

25,000$

50,000

800,000$

Dept. A

750

Dept. B

19,000$

1,750$

1,500

Dept. A

35 Minutes, Medium

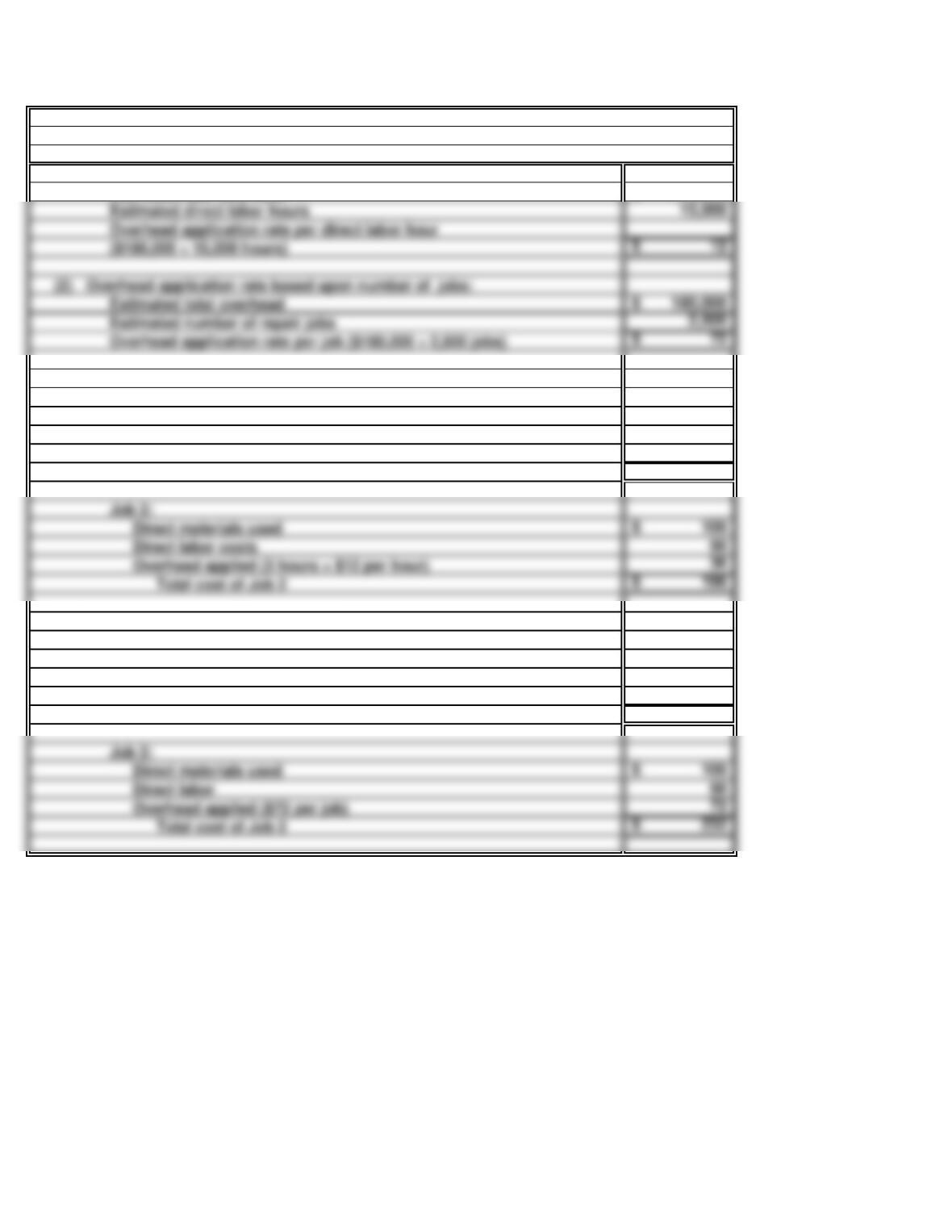

PROBLEM 17.5B

BIG BOOMERS

a. (1)

180,000$

b. (1)

300$

276

144

Total cost of Job 1 720$

100$

36

Total cost of Job 2 196$

Job 2:

Direct labor costs

Direct materials used

Overhead applied (3 hours × $12 per hour)

(2)

300$

276

72

Total cost of Job 1 648$

100$

72

Total cost of Job 2 232$

Overhead applied ($72 per job)

Job 2:

Direct materials used

Direct labor

Overhead application rate based on direct labor hours:

Estimated total overhead

Direct labor costs

Overhead applied on a per-job basis:

Job 1:

Direct materials used

Direct labor costs

Overhead applied (12 hours × $12 per hour)

Overhead applied using direct labor hours:

Job 1:

Direct materials used

Overhead applied ($72 per job)

(2)

180,000$

Overhead application rate based upon number of jobs:

Estimated total overhead

Estimated number of repair jobs

Estimated direct labor hours

($180,000 ÷ 15,000 hours)

Overhead application rate per direct labor hour

Overhead application rate per job ($180,000 ÷ 2,500 jobs)

PROBLEM 17.5B

BIG BOOMERS (concluded)

c.

Allocating overhead based upon the number of jobs assumes that each job should be

charged with an equal amount ($72) of overhead. This allocation method ignores the fact

Comments on the alternative overhead applications:

30 Minutes, Medium

PROBLEM 17.6B

LOGAN PHARMACEUTICAL

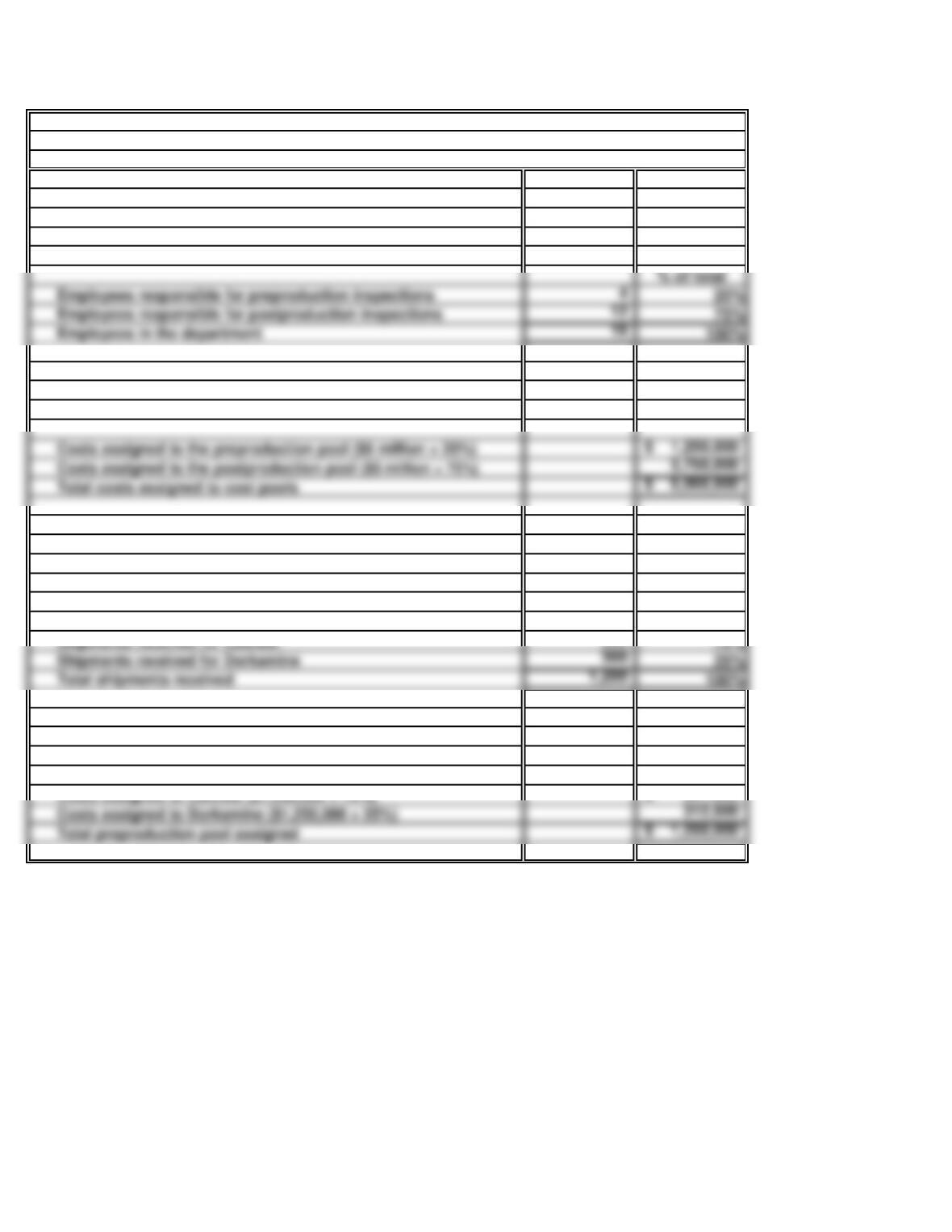

a.

Costs assigned to the postproduction pool ($5 million × 75%)

Costs assigned to the preproduction pool ($5 million × 25%)

Total costs assigned to cost pools

b.

% of total

900 75%

Shipments received for Caltrate

Shipments received for Dorkamine

Total shipments received

937,500$

Costs assigned to Caltrate ($1,250,000 × 75%)

Costs assigned to Dorkamine ($1,250,000 × 25%)

Total preproduction pool assigned

Assigning quality control department costs to activity pools:

Step 1:

Establish the percent of the department’s costs

to be assigned to each activity cost pool using the

number of employees as an activity base.

Step 2:

Assign the department’s total costs of $5 million

percentages computed in step 1.

to each product line using the number of

to each activity cost pool based on the

materials shipments received as an activity base.

Step 1:

Allocation of preproduction cost pool:

Establish the percent of the pool to be allocated

Step 2:

Allocate the preproduction pool to each product

line based on the percentages computed in step 1.

Employees responsible for preproduction inspections

Employees responsible for postproduction inspections

Employees in the department

PROBLEM 17.6B

LOGAN PHARMACEUTICAL (concluded)

c.

% of total

d.

Allocation of postproduction cost pool:

Step 1:

Establish the percent of the pool to be allocated

to each product line using the number of batches

produced as an activity base.

The company should consider reassigning its inspectors so that more time and effort is

spent inspecting shipments of Dorkamine materials. If relatively few problems are

associated with the material used to make Caltrate, time currently spent inspecting Caltrate

Batches of Dorkamine

Total batches produced

Costs assigned to Caltrate ($3,750,000 × 20%)

Batches of Caltrate

Step 2:

Costs assigned to Dorkamine ($3,750,000 × 80%)

Allocate the postproduction pool to each product

line based on the percentages computed in step 1.

45 Minutes, Strong

PROBLEM 17.7B

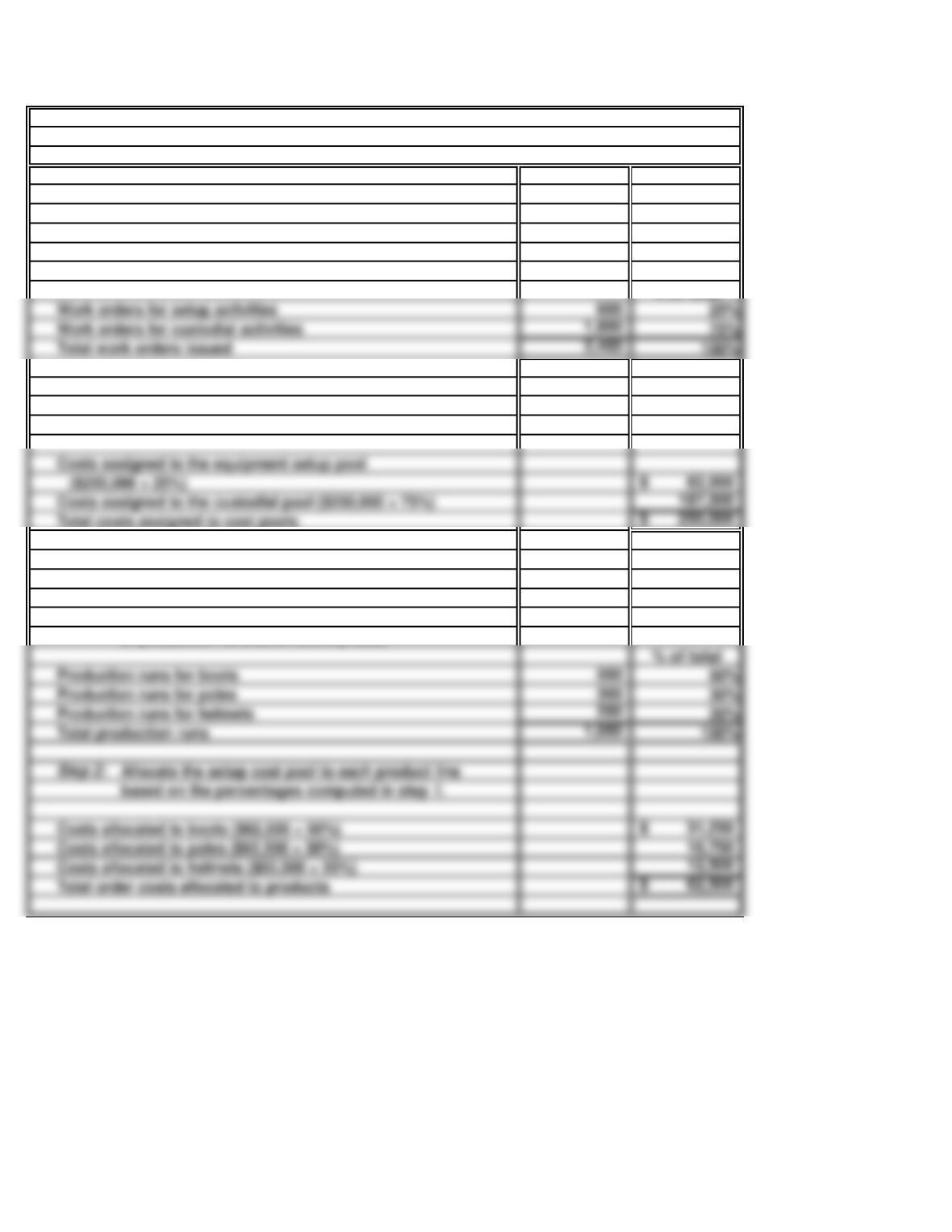

DOWNHILL FAST

a.

5,000 MH

10,000 MH

35,000 MH

50,000 MH

Compute the overhead application rate per MH:

Maintenance department costs allocated to each product line on a

per-unit basis using machine hours (MH):

Compute total MH at “normal” production levels:

Poles

Helmets

Step 2:

Step 1:

Boots

Total MH at normal production levels

Overhead application rate ($250,000 ÷ 50,000 MH)

Step 3:

Helmets (1.75 MH × $5 per MH)

Compute maintenance costs allocated to each product

Step 4:

Boots (5,000 MH ÷ 50,000 units)

Poles (10,000 MH ÷ 200,000 units)

Helmets (35,000 MH ÷ 20,000 units)

Boots (0.10 MH × $5 per MH)

Poles (0.05 MH × $5 per MH)

on a per-unit basis:

PROBLEM 17.7B

DOWNHILL FAST (continued)

b.

% of total

Costs assigned to the custodial pool ($250,000 × 75%)

Total costs assigned to cost pools

Costs assigned to the equipment setup pool

% of total

Costs allocated to helmets ($62,500 × 20%)

Total order costs allocated to products

Costs allocated to poles ($62,500 × 30%)

Total production runs

Step 2:

based on the percentages computed in step 1.

Production runs for helmets

Costs allocated to boots ($62,500 × 50%)

Allocate the setup cost pool to each product line

Production runs for poles

Production runs for boots

Assigning maintenance department costs to activity pools:

each activity cost pool based on the percentages

using the number of work orders as an

activity base.

Step 2:

Step 1:

Assign total maintenance department costs to

Establish the percent of maintenance department

costs to be assigned to each activity cost pool

Establish the percent of setup cost pool to be

allocated to each product line using the number

Allocating equipment setup pool to products:

Step 1:

computed in step 1.

of production runs as an activity base.

Work orders for setup activities

Work orders for custodial activities

Total work orders issued

PROBLEM 17.7B

DOWNHILL FAST (concluded)

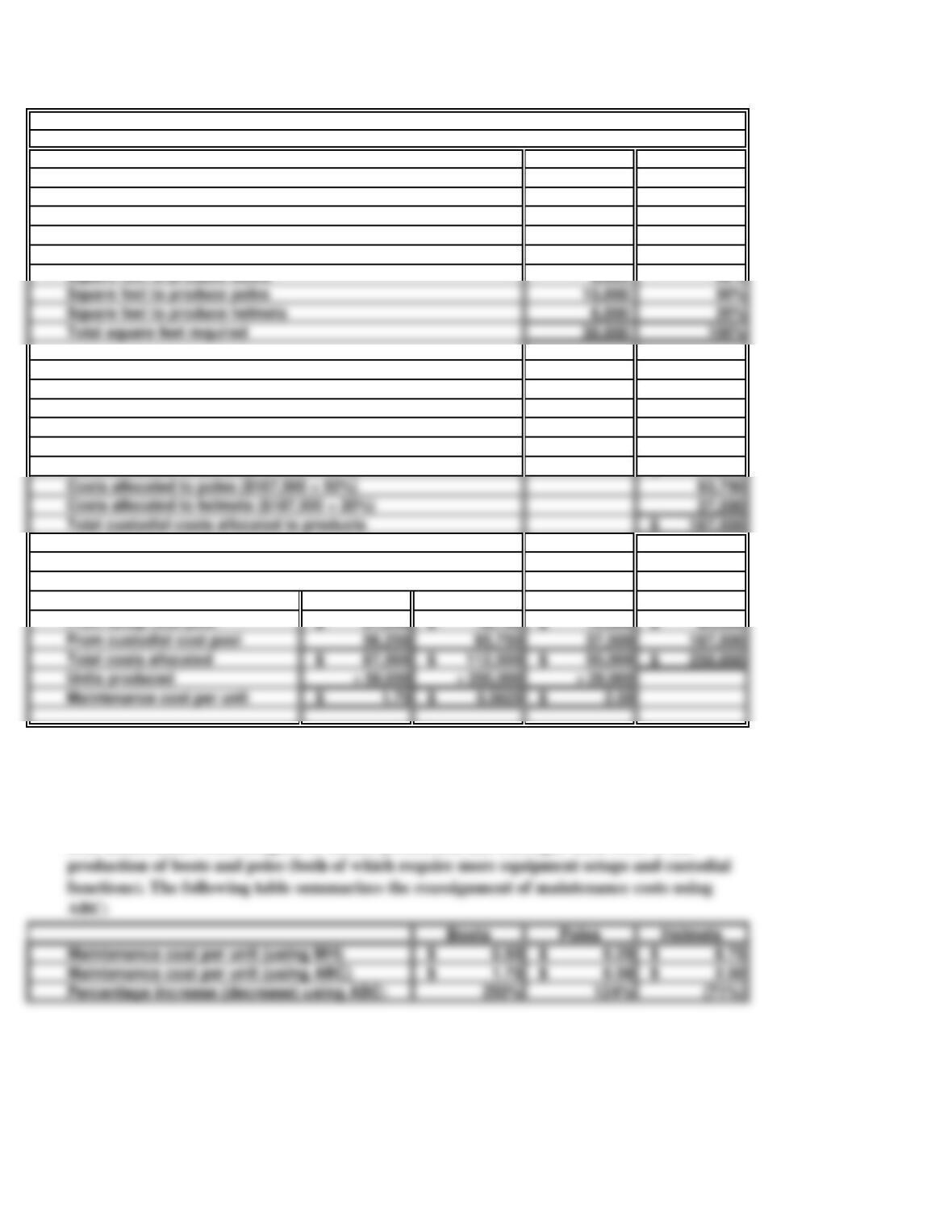

% of total

$ 56,250

93,750

37,500

$ 187,500

Costs allocated to helmets ($187,500 × 20%)

Costs allocated to poles ($187,500 × 50%)

Total custodial costs allocated to products

Boots Poles Helmets Total

Units produced

Maintenance cost per unit

Total costs allocated

From custodial cost pool

c.

Using machine hours as a single activity base is likely to result in significant cost distortions

for this company. While helmet production consumes the most machine hours, only 20% of

the company’s total maintenance cost is attributed to helmet production when activity-base

costing (ABC) is used ($50,000 out of a $250,000 total). Using ABC decreases the amount of

total maintenance costs assigned to helmet production and reassigns these costs to the

Square feet to produce boots

Allocating custodial cost pool to product lines:

Establish the percent of custodial cost pool to be

allocated to each product line using square

footage occupied as an activity base.

Step 1:

Step 2:

Allocate the custodial cost pool to each product

line based on the percentages computed

From setup cost pool

Determining maintenance costs per unit using ABC:

in step 1.

Costs allocated to boots ($187,500 × 30%)

Square feet to produce helmets

Total square feet required

Square feet to produce poles

45 Minutes, Strong

PROBLEM 17.8B

HAPPY CAT, INC.

a. Budgeted manufacturing overhead 60,000$

Budgeted direct labor hours (DLH) ÷ 15,000

Manufacturing overhead application rate $4 per DLH

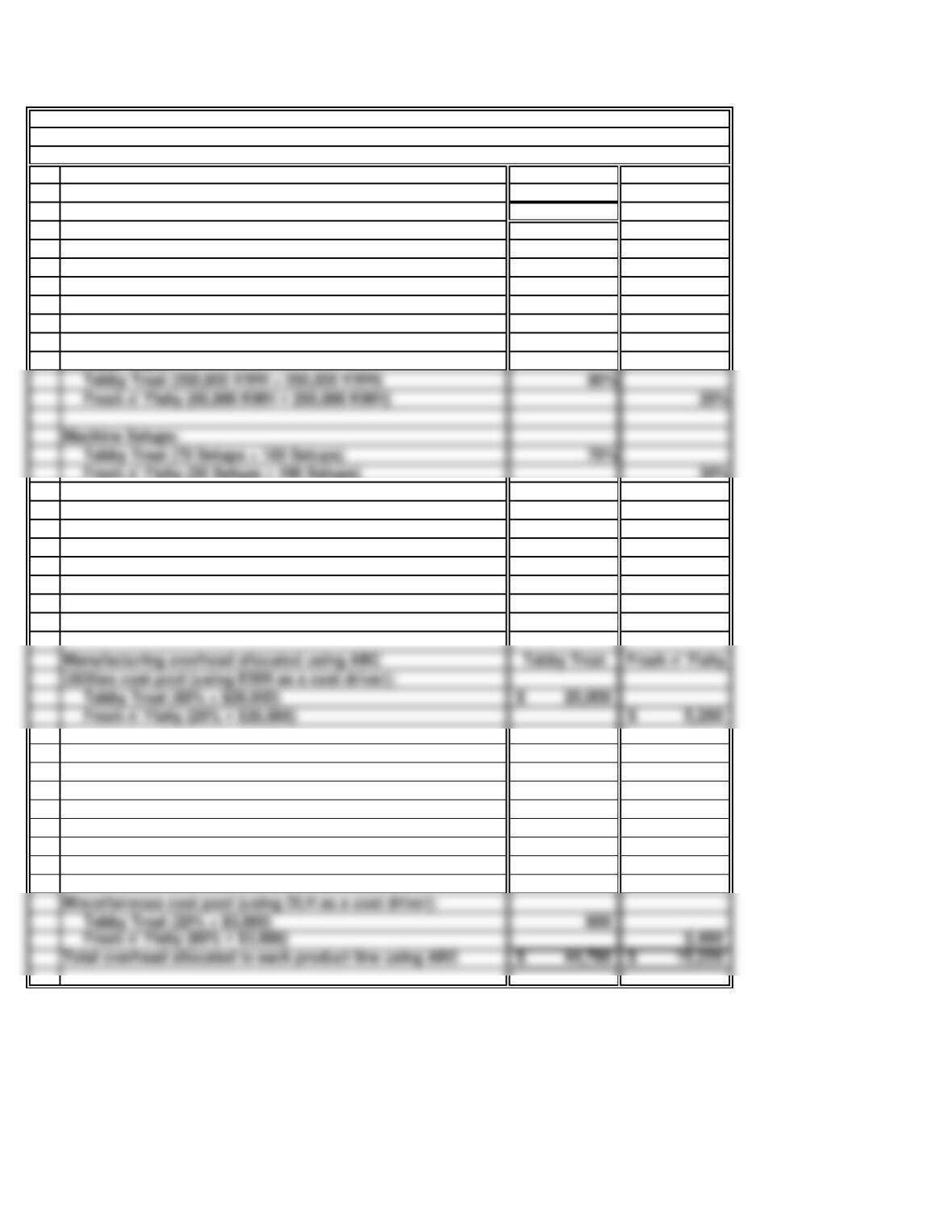

Manufacturing overhead allocated using DLH Tabby Treat Fresh n’ Fishy

75,000 bags × 0.04 DLH per bag × $4 per DLH 12,000$

48,000 cases × 0.25 DLH per case × $4 per DLH 48,000$

b. Percent of cost driver assigned to each product line Tabby Treat Fresh n’ Fishy

Kilowatt hours:

Fresh n’ Fishy (30 Setups ÷ 100 Setups) 30%

Square feet occupied:

Tabby Treat (42,000 Sq. Ft. ÷ 50,000 Sq. Ft.) 84%

Fresh n’ Fishy (8,000 Sq. Ft. ÷ 50,000 Sq. Ft.) 16%

Direct labor hours:

Tabby Treat (3,000 DLH ÷ 15,000 DLH) 20%

Fresh n’ Fishy (12,000 DLH ÷ 15,000 DLH) 80%

Manufacturing overhead allocated using ABC Tabby Treat Fresh n’ Fishy

Utilities cost pool (using KWH as a cost driver):

Tabby Treat (80% × $26,000) 20,800$

Fresh n’ Fishy (20% × $26,000) 5,200$

Maintenance cost pool (using setups as a cost driver):

Tabby Treat (70% × $19,000) 13,300

Fresh n’ Fishy (30% × $19,000) 5,700

Depreciation cost pool (using Sq. Ft. as a cost driver):

Tabby Treat (84% × $12,000) 10,080

Fresh n’ Fishy (16% × $12,000) 1,920

Tabby Treat (20% × $3,000) 600

Total overhead allocated to each product line using ABC 44,780$ 15,220$

Tabby Treat (200,000 KWH ÷ 250,000 KWH) 80%

Fresh n’ Fishy (50,000 KWH ÷ 250,000 KWH) 20%

Machine Setups:

Tabby Treat (70 Setups ÷ 100 Setups) 70%

PROBLEM 17.8B

HAPPY CAT, INC. (concluded)

c. Total manufacturing costs allocated to each product line

Tabby Treat Fresh n’ Fishy

Direct Labor:

d.

e.

The Fresh n’ Fishy product line is very labor intensive in comparison to the Tabby Treat

The benefits the company would achieve by implementing an activity-based costing system

Direct Materials:

Manufacturing Overhead (allocate using ABC):

SOLUTIONS TO CRITICAL THINKING CASES

CASE 17.1

CLASSIC CABINETS

a.

b.

c.

From Mary’s point of view, her per unit costs will decrease if the machine is purchased.

Since she is evaluated on per unit costs, the decision to purchase seems justified. However,

The information needed to evaluate the purchase is whether the direct labor costs saved

per unit is more than the additional per unit cost of using the machine. Since the machine

35 Minutes, Medium

If the machine is purchased, yearly depreciation will increase by $50,000 ($500,000/10

CASE 17.1

CLASSIC CABINETS (concluded)

d.

If each manager’s performance evaluation is based on the unit costs calculated in part a,

10 Minutes, Easy CASE 17.2

MICA CORPORATION

Under the current bonus system, unethical production managers could increase their bonuses

by purposely understating the square footage occupied by their respective product lines. To

25 Minutes, Medium CASE 17.3

THE BIDDING WARS

ETHICS, FRAUD & CORPORATE GOVERNANCE

It is tempting to say that underbidding is an unethical practice. But on the other hand, if it is

the standard and accepted practice, a company that does not “play the game” will win no

CASE 17.4

C. ERICKSON AND SONS, INC.

INTERNET

a.

c.

It is likely that job order costing is used for construction projects since each building is

Examples from the Web site of projects include: restaurants, building conversions, building

renovations, law offices, corporate headquarters, and a hospital, community center.

10 Minutes, Easy