CHAPTER 17 Job Order Costing

Prob. 17–2A (FIN MAN); Prob. 2–1A (MAN)

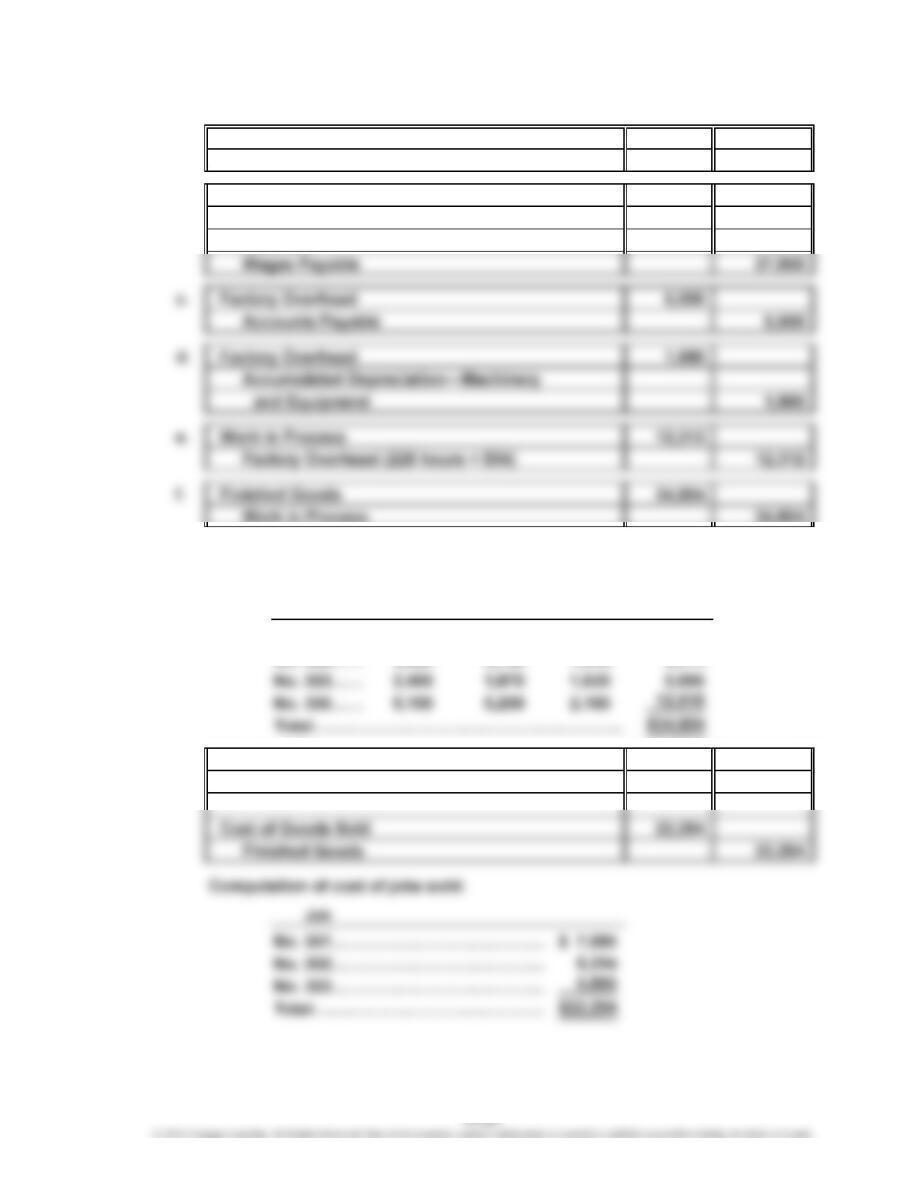

1. a. Materials 29,800

Accounts Payable

b. Work in Process 49,780

Factory Overhead 5,180

Materials

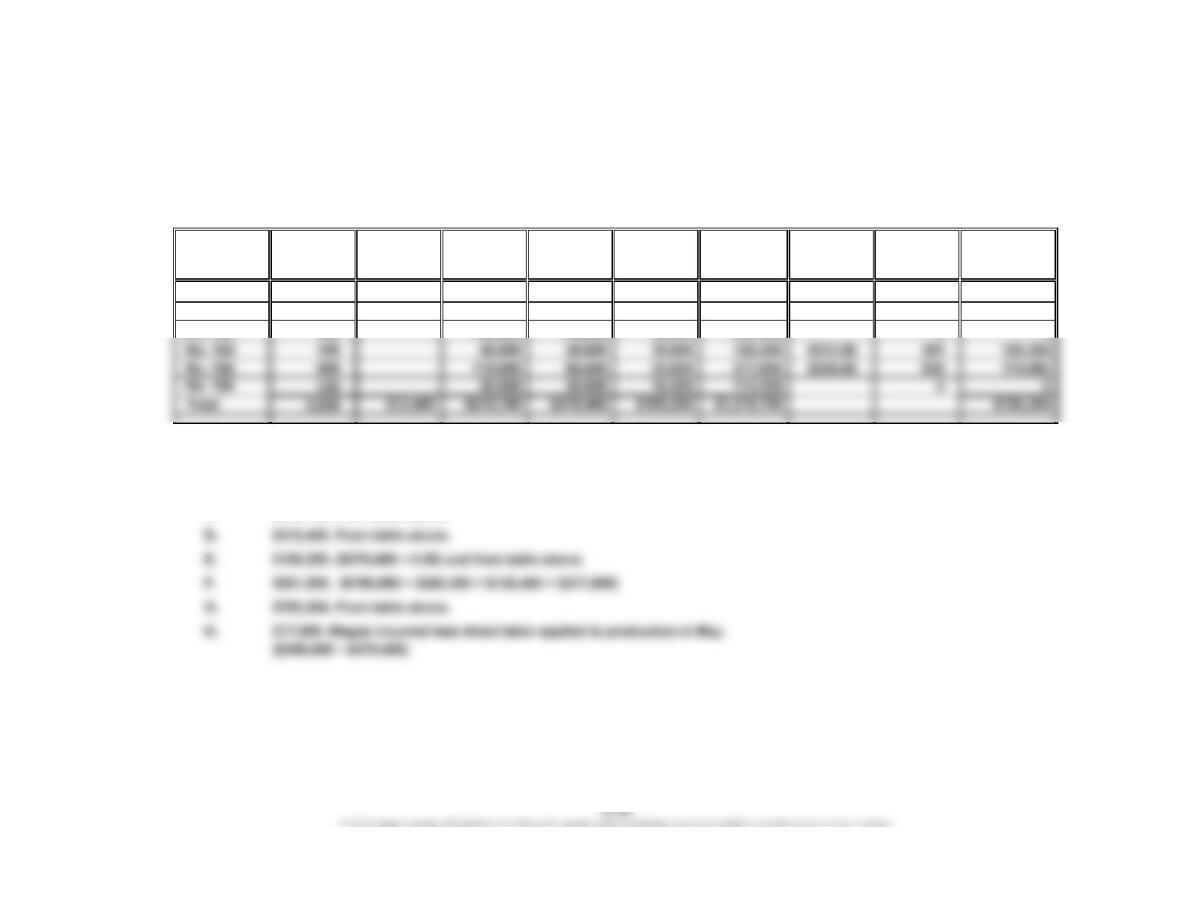

Computation of cost of jobs finished:

Direct Direct Factory

Job Materials Labor Overhead Total

No. 301…

…

$2,960 $2,775 $1,350 $ 7,085

No. 302…

…

3,620 3,750 1,944 9,314

…

…

g. Accounts Receivable 34,450

Sales

29,800

27,010

34,450

CHAPTER 17 Job Order Costing

Prob. 17–2A (FIN MAN); Prob. 2–2A (MAN) (Concluded)

2.

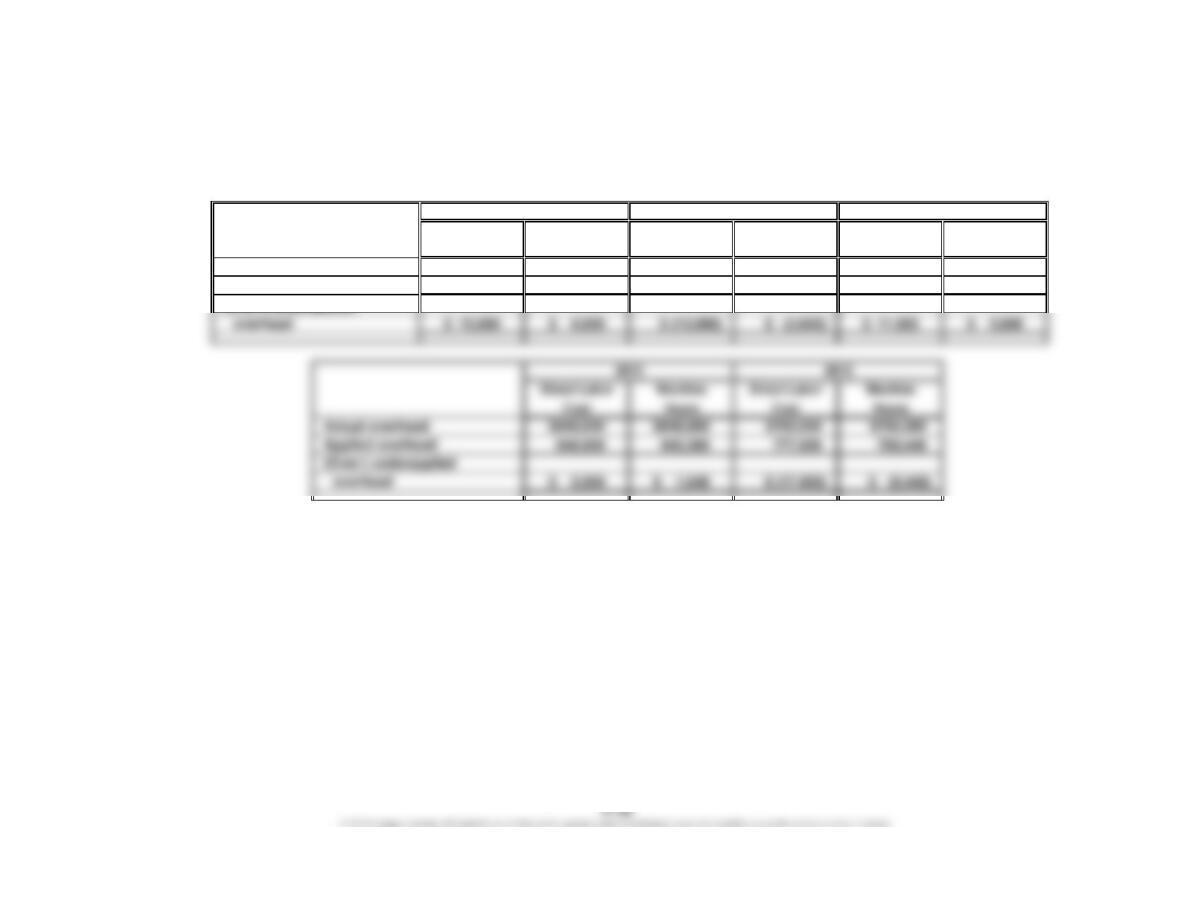

3. Schedule of unfinished jobs:

Direct Factory

Job Labor Overhead

No. 304…………………………… $6,860 $3,888

4. Schedule of completed jobs:

Direct Factory

Direct

Work in Process Finished Goods

Direct

TotalMaterials

$8,100

$18,848

CHAPTER 17 Job Order Costing

Prob. 17–3A (FIN MAN); Prob. 2–3A (MAN)

1. and 2.

Jackson Consulting Date October 1, 2016

Date wanted October 10, 2016

Date completed October 10, 2016

Job. No.

Amount Amount Amount

Mat. Time

Req. Descrip- Ticket Descrip-

No. tion Amount No. tion Amount Item Amount

112 140 meters H10 10 hours

at $35 4,900 at $20 200 Direct materials 7,280

Direct labor 400

JOB ORDER COST SHEET

Customer

ESTIMATE

Direct Materials Direct Labor Summary

ACTUAL

Direct Materials Direct Labor Summary

CHAPTER 17 Job Order Costing

Prob. 17–4A (FIN MAN); Prob. 2–4A (MAN)

1. Supporting calculations:

June 1 Cost of

Work in Direct Direct Factory Total Unit Units Goods

Quantity Process Materials Labor Overhead Cost Cost Sold Sold

No. 201 550 $16,500 $ 55,000 $ 41,250 $ 57,750 $ 170,500 $310.00 440 $136,400

No. 202 1,100 44,000 93,500 71,500 100,100 309,100 281.00 880 247,280

($330,000 – $264,450)

Job. No.

CHAPTER 17 Job Order Costing

Prob. 17–4A (FIN MAN); Prob. 2–4A (MAN) (Concluded)

2. June 30 balances:

Materials……………………

…

$ 17,000 ($82,500 + $330,000 – $395,500)

Work in Process*…………

…

$143,060 ($91,300 + $51,760, Job 203 & Job 206)

Finished Goods**…………

…

$151,750 ($903,620 – $751,870)

CHAPTER 17 Job Order Costing

Prob. 17–5A (FIN MAN); Prob. 2–5A (MAN)

1.

Sales $17,920,000

Cost of goods sold 10,864,000

Supporting calculations:

Sales: 1,120,000 units × $16 = $17,920,000

Cost of goods sold: 1,120,000 units × $9.70 = $10,864,000

Manufacturing cost per unit (Knife):

Direct materials:

Hardened Steel Blanks……………………………

…

$4.00

2. Finished Goods balance, December 31, 2016:

(1,200,000 units – 1,120,000 units) × $9.70 = $776,000

GINOCERA INC.

Income Statement

For the Year Ended December 31, 2016

CHAPTER 17 Job Order Costing

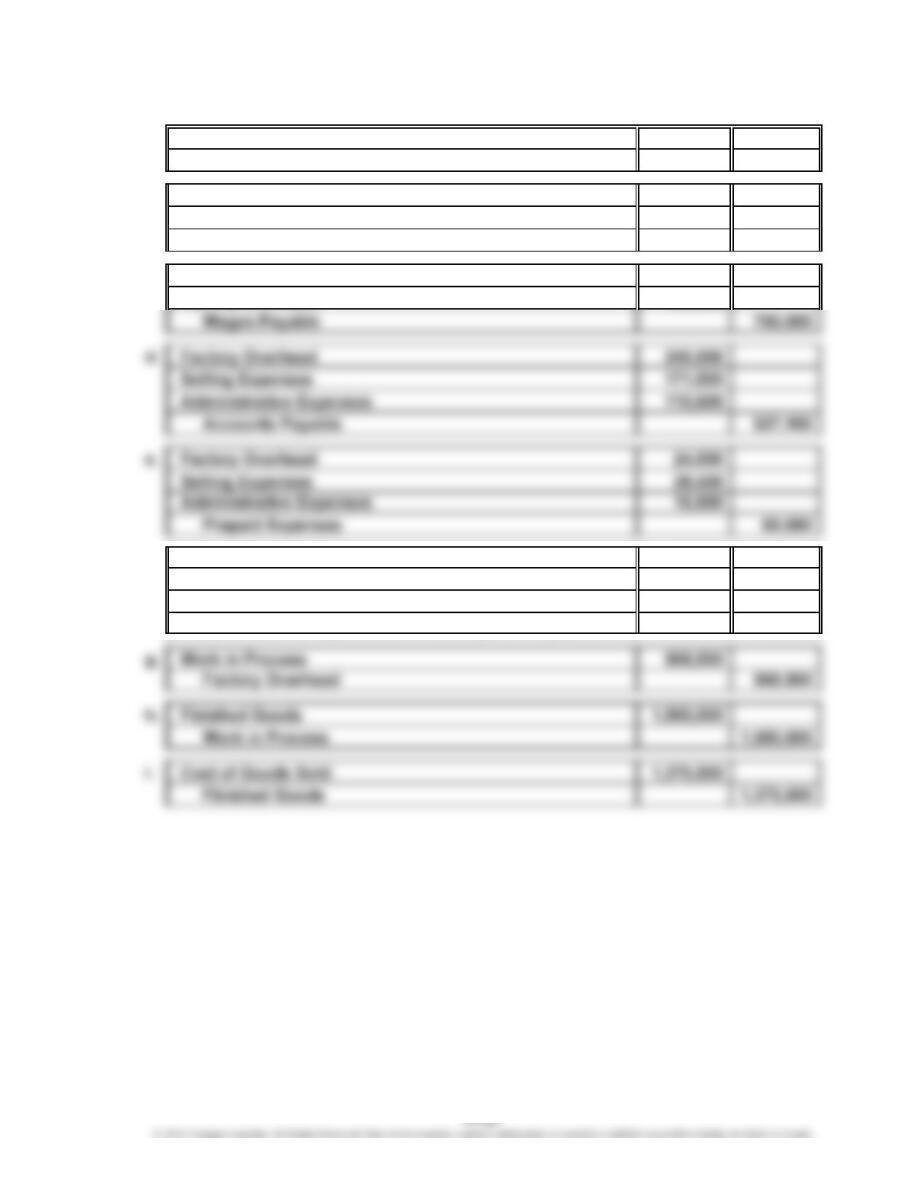

Prob. 17–1B (FIN MAN); Prob. 2–1B (MAN)

a. Materials 770,000

Accounts Payable 770,000

b. Work in Process 604,200

Factory Overhead 75,800

Materials 680,000

c. Work in Process 574,000

Factory Overhead 182,000

f. Factory Overhead 49,500

Depreciation Expense—Office Equipment 61,800

Depreciation Expense—Office Building 14,900

Accumulated Depreciation—Buildings and Equipment 126,200

CHAPTER 17 Job Order Costing

Prob. 17–2B (FIN MAN); Prob. 2–2B (MAN)

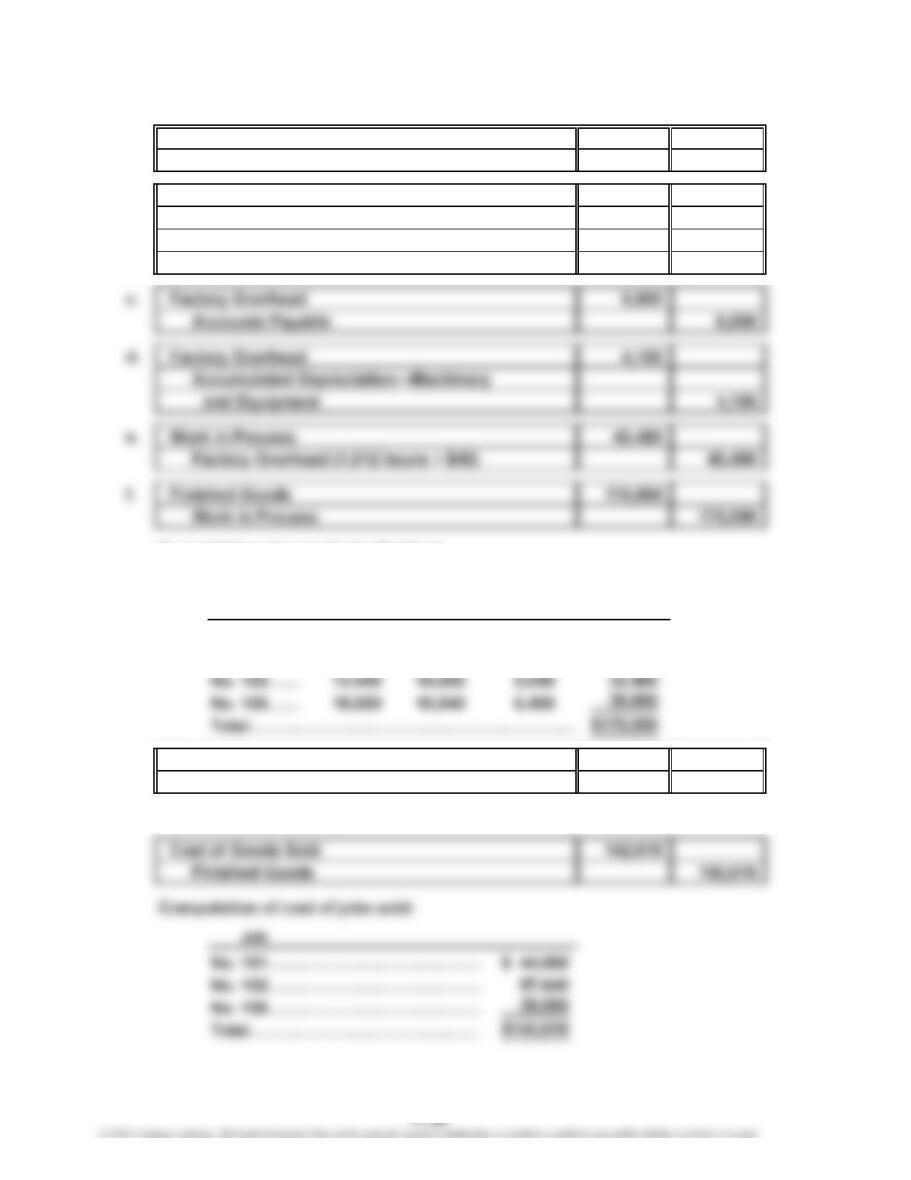

1. a. Materials 147,000

Accounts Payable

b. Work in Process 262,490

Factory Overhead 29,160

Materials

Wages Payable

Computation of cost of jobs finished:

Direct Direct Factory

Job Materials Labor Overhead Total

No. 101…

…

$19,320 $19,500 $6,160 $ 44,980

No. 102…

…

23,100 28,140 6,400 57,640

…

…

g. Accounts Receivable 189,100

Sales*

*$62,900 + $80,700 + $45,500

147,000

152,540

189,100

139,110

CHAPTER 17 Job Order Costing

Prob. 17–2B (FIN MAN); Prob. 2–2B (MAN) (Concluded)

2.

3. Schedule of unfinished jobs:

Direct Factory

Job Materials Labor Overhead

No. 104……………………

…

$36,500 $9,520

…

4. Schedule of completed jobs:

Direct Factory

Job Labor Overhead

$ 84,220

Work in Process Finished Goods

Direct

TotalMaterials

$38,200

Direct

Materials Total

CHAPTER 17 Job Order Costing

Prob. 17–3B (FIN MAN); Prob. 2–3B (MAN)

1. and 2.

Lunden Consulting Date May 9, 2016

Date wanted May 15, 2016

Date completed May 15, 2016

Job. No.

Amount Amount Amount

400 meters at $32 12,800 30 hours at $20 600 Direct materials 12,800

Mat. Time

Req. Descrip- Ticket Descrip-

No. tion Amount No. tion Amount Item Amount

132 360 meters H9 18 hours

at $32 11,520 at $19 342 Direct materials 13,120

Direct labor 684

JOB ORDER COST SHEET

Customer

ESTIMATE

Direct Materials Direct Labor Summary

ACTUAL

Direct Materials Direct Labor Summary

CHAPTER 17 Job Order Costing

Prob. 17–4B (FIN MAN); Prob. 2–4B (MAN)

1. Supporting calculations:

May 1 Cost of

Work in Direct Direct Factory Total Unit Units Goods

Quantity Process Materials Labor Overhead Cost Cost Sold Sold

No. 101 330 $26,400 $ 82,500 $ 59,400 $ 29,700 $ 198,000 $600.00 264 $158,400

No. 102 380 46,000 105,400 72,600 36,300 260,300 $685.00 360 246,600

No. 103 500 132,000 110,000 55,000 297,000 00

A. $586,100. Materials applied to production in May + indirect materials.

($570,700 + $15,400)

B. $72,400. From table above and problem.

C. $570,700. From table above.

Job. No.

CHAPTER 17 Job Order Costing

Prob. 17–4B (FIN MAN); Prob. 2–4B (MAN) (Concluded)

2. May 31 balances:

Materials……………………

…

$ 19,500 ($105,600 + $500,000 – $586,100)

Work in Process*…………

…

$409,200 ($297,000 + $112,200, Job 103 & Job 106)

Finished Goods**…………

…

$101,216 ($801,500 – $700,284)

CHAPTER 17 Job Order Costing

Prob. 17–5B (FIN MAN); Prob. 2–5B (MAN)

1.

Sales $18,400,000

Cost of goods sold 11,914,000

Gross profit $ 6,486,000

Selling expenses:

Supporting calculations:

Sales: 460,000 units × $40 = $18,400,000

Cost of goods sold: 460,000 units × $25.90 = $11,914,000

Manufacturing cost per unit:

Direct materials:

Leather………………………………………………

…

$10.00

V

elvet (for interior)…………………………………

…

5.00

2. Finished Goods balance, December 31, 2016:

(500,000 units – 460,000 units) × $25.90 = $1,036,000

TECHNOLOGY ACCESSORIES INC.

Income Statement

For the Year Ended December 31, 2016

CHAPTER 17 Job Order Costing

CP 17–1 (FIN MAN); CP 2–1 (MAN)

Two or three trends seem apparent. Starting with the most obvious:

a. There appears to be a strong “Friday effect.” The unit cost on Friday increases

dramatically, then falls on Monday. Apparently, the workforce is preparing early

for the weekend.

b. There also appears to be a general increasing trend in the unit cost. Every

Friday effect is larger than the previous Friday. Much the same can be said

A number of further pieces of information should be requested.

a. First, it would be good to verify these trends with some other products. This

trend is probably not product-related but related generally to the day of the

week. This would mean that the trend should be apparent in the other products.

b. The data should be sorted by shift and by employee. It’s possible that the effect

is stronger on one shift than on another or that just a few employees are

responsible for the effect. It may not be prevalent in the general population of

workers.

CASES & PROJECTS

CHAPTER 17 Job Order Costing

CP 17–2 (FIN MAN); CP 2–2 (MAN)

1. The unit costs are influenced by both the price and quantity of inputs. On the

price side, the cost of steel has dropped from $1,200 to $1,100 per ton. This is

apparently the result of the purchasing manager’s decision to reduce the cost

of raw materials by going to a new vendor. No other input prices change.

Some of the input quantities changed for the worse. Specifically:

2. A possible reason for this deterioration in performance is related to the

purchasing manager’s decision to change vendors in order to secure a lower

price per ton. The new vendor is apparently delivering a lower-quality steel

product to the company. As a result, the foundry operation is having to spend

more time forming the steel parts. Moreover, the increased steel tons per unit

Job 206 Job 228

Input Quantity per Unit

CHAPTER 17 Job Order Costing

CP 17–3 (FIN MAN); CP 2–3 (MAN)

1. The engineer is concerned that direct labor is not related to overhead

consumption because direct labor is a small part of the cost structure.

Apparently, the company has replaced labor with expensive machine

2. Because each direct labor hour now has $1,500 of factory overhead, small

mistakes in the direct labor time estimates can have a large impact on the

estimated cost of a product. This is very critical because the company sets selling

3. The engineer’s concern is valid. The company should consider replacing its

CHAPTER 17 Job Order Costing

CP 17–4 (FIN MAN); CP 2–4 (MAN)

1. Todd should record the debits for factory wages as a debit to Work in Process.

The factory wages are product costs that must be accumulated in the cost of

producing the product. Eventually, these wage costs will become part of the

finished goods inventory and the cost of goods sold when the gift items are sold.

2. Jeff would not be concerned about immediately expensing administrative wages

CHAPTER 17 Job Order Costing

CP 17–5 (FIN MAN); CP 2–5 (MAN)

1. Direct labor cost:

Total actual (applied) overhead, 2012–2016…… $ 4,200,000

CHAPTER 17 Job Order Costing

CP 17–5 (FIN MAN); CP 2–5 (MAN) (Continued)

2.

Direct Labor Machine Direct Labor Machine Direct Labor Machine

Cost Hours Cost Hours Cost Hours

Actual overhead $790,000 $790,000 $870,000 $870,000 $935,000 $935,000

Applied overhead 777,000 781,200 882,000 873,600 924,000 932,400

(Over-) underapplied

2016 2015

2014

CHAPTER 17 Job Order Costing

CP 17–5 (FIN MAN); CP 2–5 (MAN) (Concluded)

3. The best predetermined overhead rate is machine hours. Although the total

overhead applied for each rate developed in part (1) is the same over the entire

five-year period (as a result of the method by which the predetermined overhead