CHAPTER 17 Financial Statement Analysis

Ex. 17-14

c. Hasbro carries a smaller proportion of debt to the stockholders’ equity than

a. Ratio of Liabilities to Stockholders’ Equity =

Total Liabilities

$270,402 + $90,826 =

Times Interest Earned Income Before Income Tax + Interest Expense

Interest Expense

b. =

Mattel:

Hasbro: 4.0

$90,826

$(419,261) + $181,886 =

$181,886 (1.3)

CHAPTER 17 Financial Statement Analysis

Ex. 17-15

c. Hershey uses more debt than Mondelez does. As a result, Hershey’s total liabilities

to stockholders’ equity ratio is higher than Mondelez’s (4.5 vs. 1.4). Mondelez has

a lower ratio of fixed assets to long-term liabilities than Hershey does. This ratio

divides the property, plant, and equipment (net) by the long-term debt. The ratio for

$2,130,294

$3,877,188

$12,532,000 + $7,747,000 =

=

$2,130,294

$3,254,280 + $622,908

Hershey:

=

=Mondelez:

0.5

$8,482,000

=Total Liabilities

Total Stockholders’ Equity

Ratio of Liabilities to Stockholders’ Equity

b. =

Ratio of Fixed Assets to Long-Term Liabilities Fixed Assets (net)

Long-Term Liabilities

a.

0.4

$8,482,000

$20,279,000

CHAPTER 17 Financial Statement Analysis

Ex. 17-16

b. The asset turnover ratio measures the number of sales dollars earned for

each dollar of assets. The greater the number of sales dollars earned for every

dollar of assets, the more efficient a firm is in using assets. Thus, the ratio is a

measure of each company’s asset efficiency. Union Pacific earns only 40 cents

for every dollar of assets. This is because railroads are very asset-intensive.

The company must invest in locomotives, railcars, terminals, tracks, right-of-way,

and information systems in order to earn revenues. These investments are

significant. YRC has a higher asset turnover ratio and is able to earn $3.20 for every

Note to Instructors: Students may wonder how asset-intensive companies

overcome their asset efficiency disadvantages to competitors with better asset

efficiencies, as in the case between railroads and motor carriers. Asset efficiency

is part of the financial equation; the other part is the profit margin made on each

dollar of sales. Thus, companies with high asset efficiency often operate on

thinner margins than do companies with lower asset efficiency. For example, the

=

a. =Asset Turnover Sales

Average Total Assets

3.2

$5,092,000

$1,601,300

YRC:

CHAPTER 17 Financial Statement Analysis

Ex. 17-17

1

Interest expense = $2,500,000 × 6%

2

Average total assets = ($5,200,000 + $5,000,000) ÷ 2

3

Interest expense = $2,500,000 × 6%

4

Average total assets = ($5,000,000 + $4,800,000) ÷ 2

*

Average total stockholders’ equity = ($2,324,000 + $1,972,000) ÷ 2

**

Average total stockholders’ equity = ($1,972,000 + $1,500,000) ÷ 2

1

Preferred dividends = $500,000 × 2.5%

2

Average common stockholders’ equity = ($1,824,000 + $1,472,000) ÷ 2

3

Preferred dividends = $500,000 × 2.5%

4

Average common stockholders’ equity = ($1,472,000 + $1,000,000) ÷ 2

b. The profitability ratios indicate that the company’s profitability has deteriorated.

Most of this change is from net income falling from $462,500 in 20Y6 to $411,000

Return on Common

Stockholders’ Equity

Net Income – Preferred Dividends

Average Common Stockholders’ Equity

20Y7:

Return on Total Assets Net Income + Interest Expense

Average Total Assets

a. =

$411,000 – $12,500

11.0%

=

=

$411,000 + $150,000

$5,100,000

20Y7:

$462,500 – $12,500 = 36.4%

$1,236,000

20Y6:

= 24.2%

$1,648,000

1

2

1

2

3

4

CHAPTER 17 Financial Statement Analysis

Ex. 17-18

($3,299,600 + $3,743,500) ÷ 2

c. Both the return on total assets and the return on stockholders’ equity have

Return on Total Assets Net Income + Interest Expense

Return on Stockholders’ Equity Net Income

Average Total Stockholders’ Equity

a. =

b.

=

Fiscal Year 2:

Fiscal Year 3:

=

= 4.8%

(2.8)%

$162,800

($3,457,400 + $3,299,600) ÷ 2

$(99,300)

CHAPTER 17 Financial Statement Analysis

Ex. 17-19

a.

*

Interest expense = $1,600,000 × 6%

**

Average total assets = ($6,000,000 + $6,800,000***) ÷ 2

***

The total assets at the end of the year is the sum of the total liabilities ($2,800,000) and total

stockholders’ equity ($4,000,000) at the end of the year. Total assets ($6,800,000) = Total

liabilities ($2,800,000) + Total stockholders’ equity ($4,000,000).

e.

*

Average total stockholders’ equity = [($1,072,000 + $1,600,000 + $800,000) + $4,000,000] ÷ 2

Ratio of Fixed Assets to

Long-Term Liabilities

Fixed Assets (net)

Long-Term Liabilities

=

=

=

Average Total Assets

Sales

2.8

=

Stockholders’ Equity

Asset Turnover

=

c.

$6,400,000

$17,920,000

Return on Net Income

=

Average Total Stockholders’ Equity

$3,736,000 = 24.8%

1.9=$3,040,000

$1,600,000

=$928,000

*

**

CHAPTER 17 Financial Statement Analysis

Ex. 17-20

*

Interest expense = $7,500,000 bonds payable × 8%

d.

c. =Price-Earnings Ratio

Earnings per Share

=

=

a. =

=

Times Interest Earned

9.8 times

$5,280,000 + $600,000*

$600,000

=

$53.90

$4.90

Dividends per Share

Income Before Income Tax + Interest Expense

Interest Expense

Market Price per Share of Common Stock

=

11.0

Dividends on Common Stock

CHAPTER 17 Financial Statement Analysis

Ex. 17-21

*

Preferred dividends = ($1,500,000 ÷ $50) × $3

**

Shares of common stock outstanding = $8,000,000 ÷ $20

=

=

a. =

$4.80

$2,010,000 – $90,000*

400,000 shares**

Earnings per Share

=

Net Income – Preferred Dividends

Shares of Common Stock Outstanding

$4.32

Dividends per Share Common Dividends

Shares of Common Stock Outstanding

==

c.

$1,728,000

400,000 shares

CHAPTER 17 Financial Statement Analysis

Ex. 17-22

b. Coca-Cola has a large dividend yield and a high price-earnings ratio. Stock market

participants value Coca-Cola common stock on the basis of its dividend and its

potential share price appreciation. Alphabet pays no dividend and, thus, has no

a. =

Price-Earnings Ratio Earnings per Share

Market Price per Share of Common Stock

$1.56

=

=

1.9%

$47.35

=

$2.58

$135.44

Dividend Yield =Dividends per Share of Common Stock

Market Price per Share of Common Stock

Deere & Company:

Alphabet:

The Coca-Cola Company:

0.0%

$0.00

$1,035.61

3.3%

CHAPTER 17 Financial Statement Analysis

Appendix Ex. 17-23

a. Earnings per share on income before discontinued operations:

Net income………………………………………………………………………

…

$4,000,000

Less gain on discontinued operations……………………………………

…

400,000

Income before discontinued operations…………………………………… $3,600,000

b.

= $7.60 per share

500,000 shares

=

Earnings per Share on

Common Stock =Net Income – Preferred Dividends

Shares of Common Stock Outstanding

$4,000,000 – $200,000

CHAPTER 17 Financial Statement Analysis

Appendix Ex. 17-24

a.

Income from continuing operations before income tax expense $1,000,000

* Income tax expense = $1,000,000 × 40%

b.

Earnings per share:

Income from continuing operations $ 30.00

Loss from discontinued operations (12.00)

Net income $ 18.00

1

EPS on Income from continuing operations = $30.00 = $600,000 ÷ 20,000

2

EPS on Loss from discontinued operations = –$12.00 = $(240,000) ÷ 20,000

Appendix Ex. 17-25

a. Colston Company reported this item correctly in the financial statements. This

Partial Income Statement

For the Year Ended December 31

Apex Inc.

Partial Income Statement

For the Year Ended December 31

Apex Inc.

1

2

CHAPTER 17 Financial Statement Analysis

Prob. 17-1A

1.

20Y2 20Y1 Amount Percent

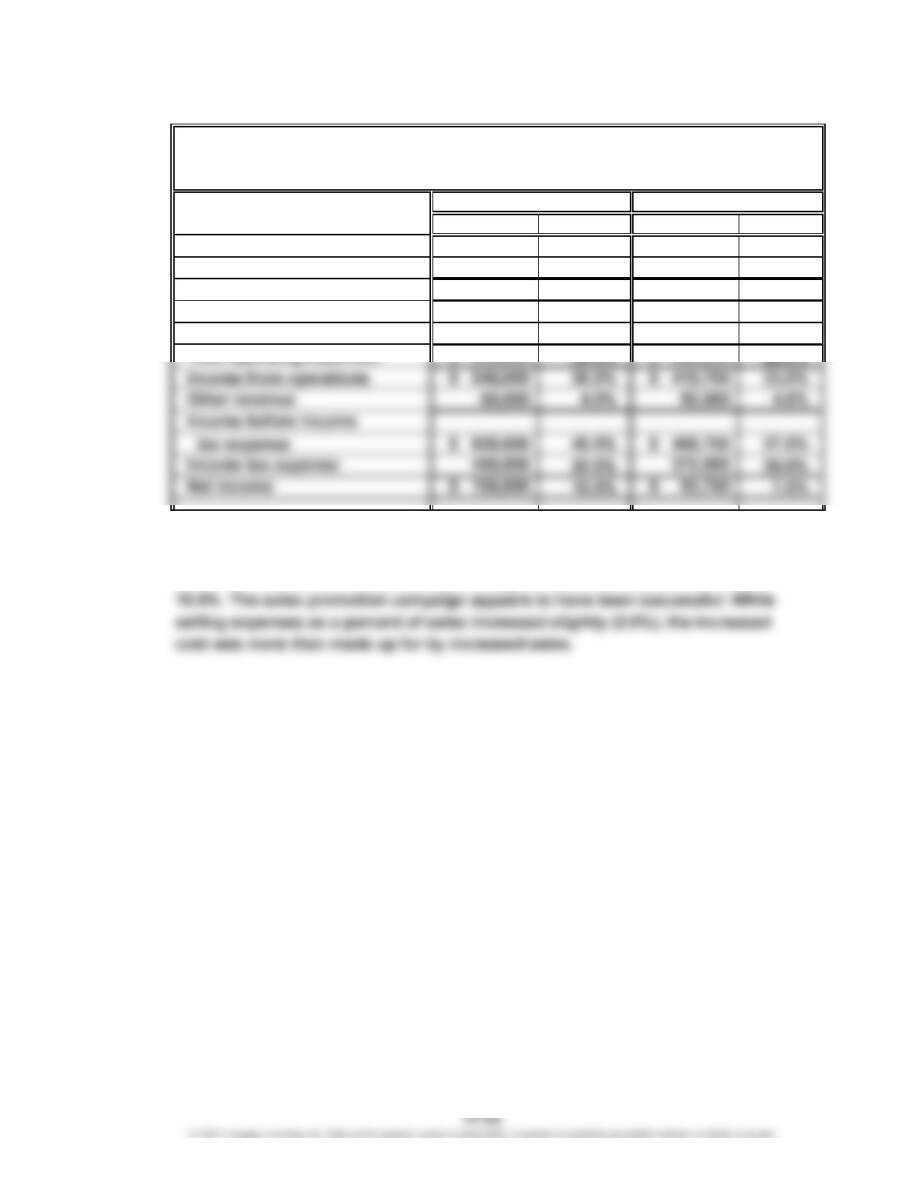

Sales $16,800,000 $15,000,000 $1,800,000 12.0%

Cost of merchandise sold 11,500,000 10,000,000 1,500,000 15.0%

Gross profit $ 5,300,000 $ 5,000,000 $ 300,000 6.0%

Selling expenses $ 1,770,000 $ 1,500,000 $ 270,000 18.0%

Administrative expenses 1,220,000 1,000,000 220,000 22.0%

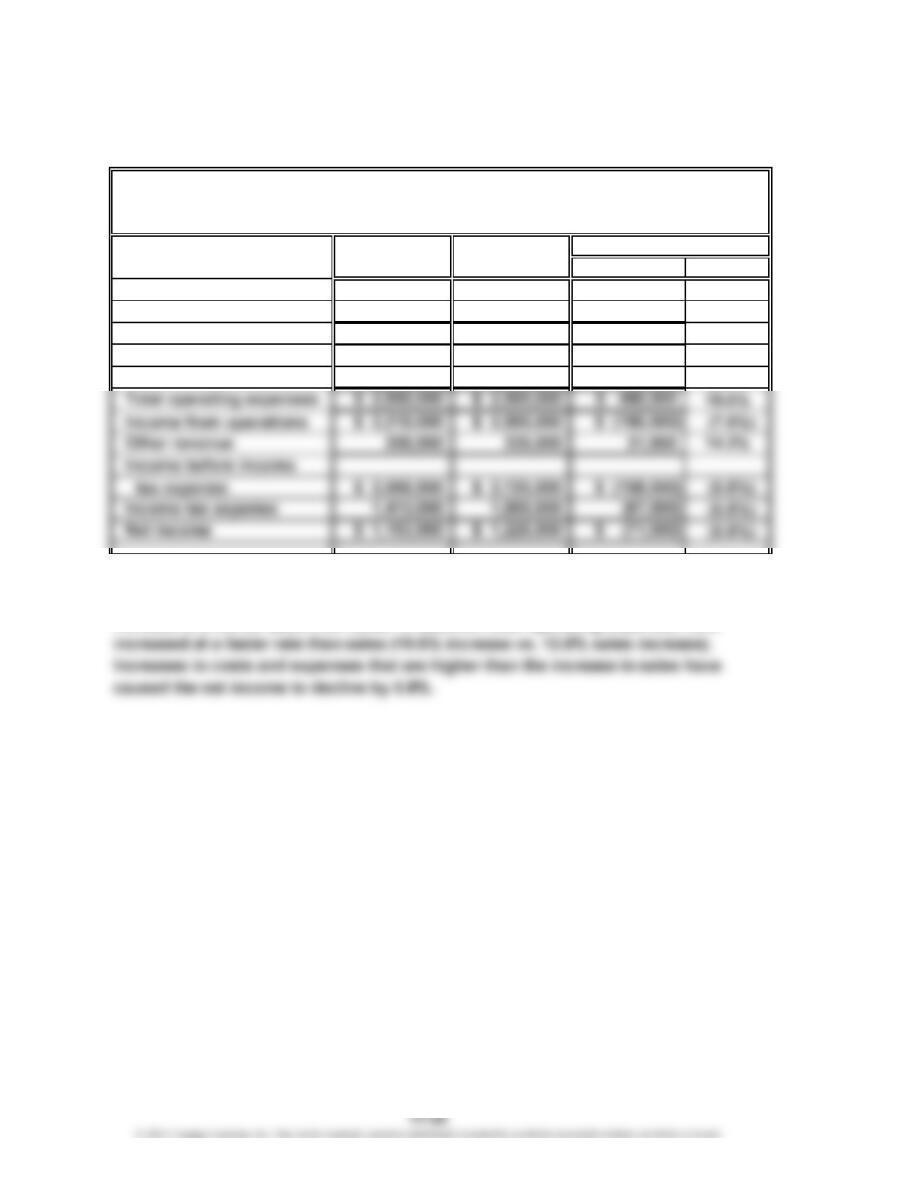

2. Net income has declined from 20Y1 to 20Y2. Sales have increased by 12.0%; however,

the cost of merchandise sold has increased by 15.0%, causing the gross profit to

PROBLEMS

Increase (Decrease)

McDade Company

Comparative Income Statement

For the Years Ended December 31, 20Y2 and 20Y1

CHAPTER 17 Financial Statement Analysis

Prob. 17-2A

1.

Amount Percent Amount Percent

Sales $1,500,000 100.0% $1,250,000 100.0%

Cost of merchandise sold 510,000 34.0% 475,000 38.0%

Gross profit $ 990,000 66.0% $ 775,000 62.0%

Selling expenses $ 270,000 18.0% $ 200,000 16.0%

Administrative expenses 180,000 12.0% 156,250 12.5%

2. The vertical analysis indicates that the costs other than selling expenses (cost of

merchandise sold and administrative expenses) improved as a percentage of

sales. As a result, net income as a percentage of sales increased from 7.5% to

20Y2 20Y1

Tri-Comic Company

Comparative Income Statement

For the Years Ended December 31, 20Y2 and 20Y1

CHAPTER 17 Financial Statement Analysis

Prob. 17-3A

1. a. = Current Assets – Current Liabilities

$900,000 = $1,650,000 – $750,000

2.

Working Quick

Capital Assets

$ 900,000 $ 900,000

900,000 775,000

900,000 900,000

900,000 800,000

Supporting Data

2.4 1.2 1,550,000

c.

d.

1.2 1,525,000

2.0 1.0 1,760,000

b.

= 2.2

Current Ratio = Current Assets

Current Liabilities

$1,650,000

=

Working Capital

Transaction

a.

b.

Assets

Current

Ratio

Quick

Ratio

Current

2.2 1.2 $1,650,000

2.4

$750,000

Current

Liabilities

$750,000

625,000

860,000

650,000

CHAPTER 17 Financial Statement Analysis

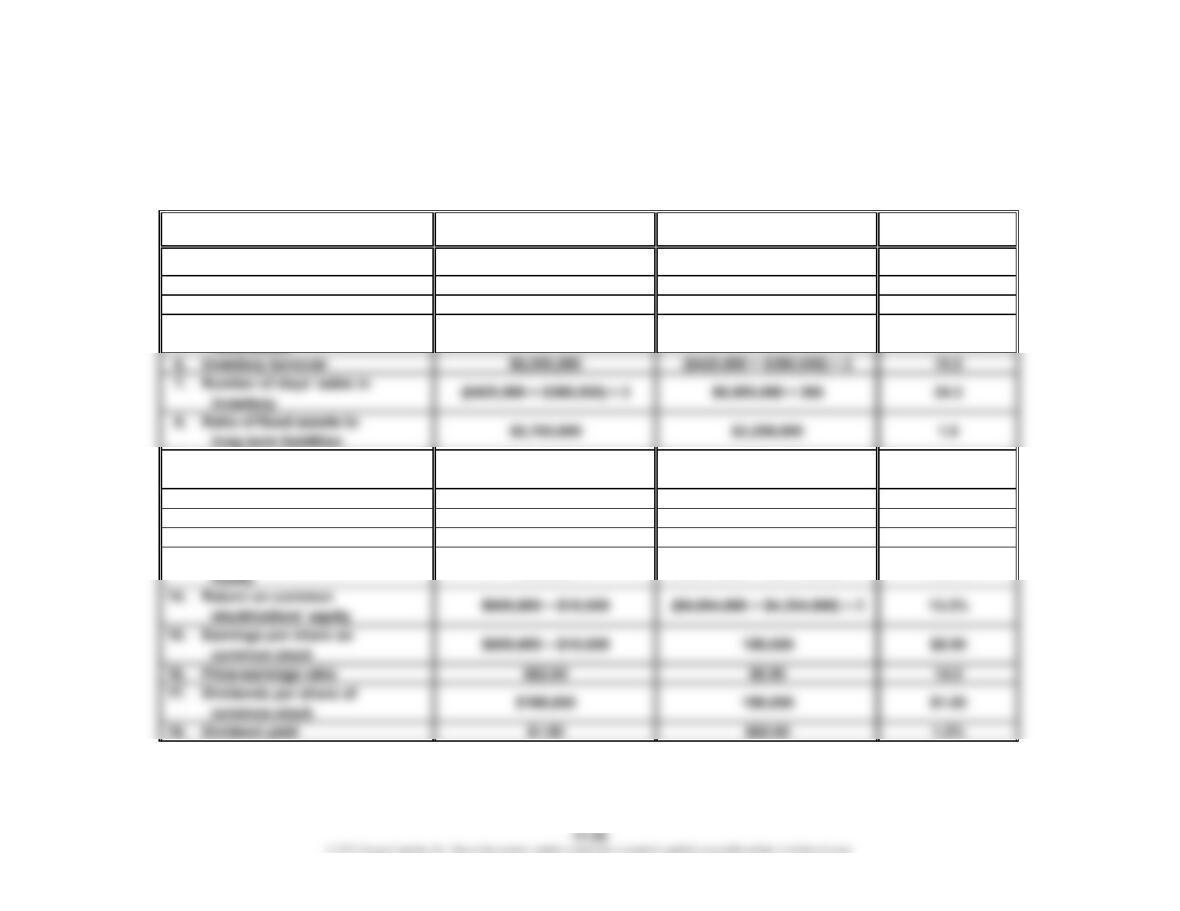

Prob. 17-4A

1. Working Capital: $2,464,000 – $880,000 = $1,584,000

Calculated

Numerator Denominator Value

2. Current ratio $2,464,000 $880,000 2.8

3. Quick ratio $1,936,000 $880,000 2.2

4. Accounts receivable turnover $10,850,000 ($585,000 + $500,000) ÷ 2 20.0

5. Number of days’ sales in

9. Ratio of liabilities to

stockholders’ equity

10. Times interest earned $1,020,000 + $132,000 $132,000 8.7

11. Asset turnover $10,850,000 ($9,024,000 + $8,254,000) ÷ 2 1.3

12. Return on total assets $600,000 + $132,000 ($9,024,000 + $8,254,000) ÷ 2 8.5%

13. Return on stockholders’

12.8%

($4,944,000 + $4,454,000) ÷ 2

$4,944,000

$600,000

0.8$4,080,000

18.3

($585,000 + $500,000) ÷ 2 $10,850,000 ÷ 365

Ratio

CHAPTER 17 Financial Statement Analysis

Prob. 17-5A

1. a.

$889,453

$4,270,764

Return on Total Assets =

$3,044,250

Net Income + Interest Expense

Average Total Assets

20.8%20Y8: =

20Y5: $1,379,000

45.3%

=

40.0%

50.0%

60.0%

CHAPTER 17 Financial Statement Analysis

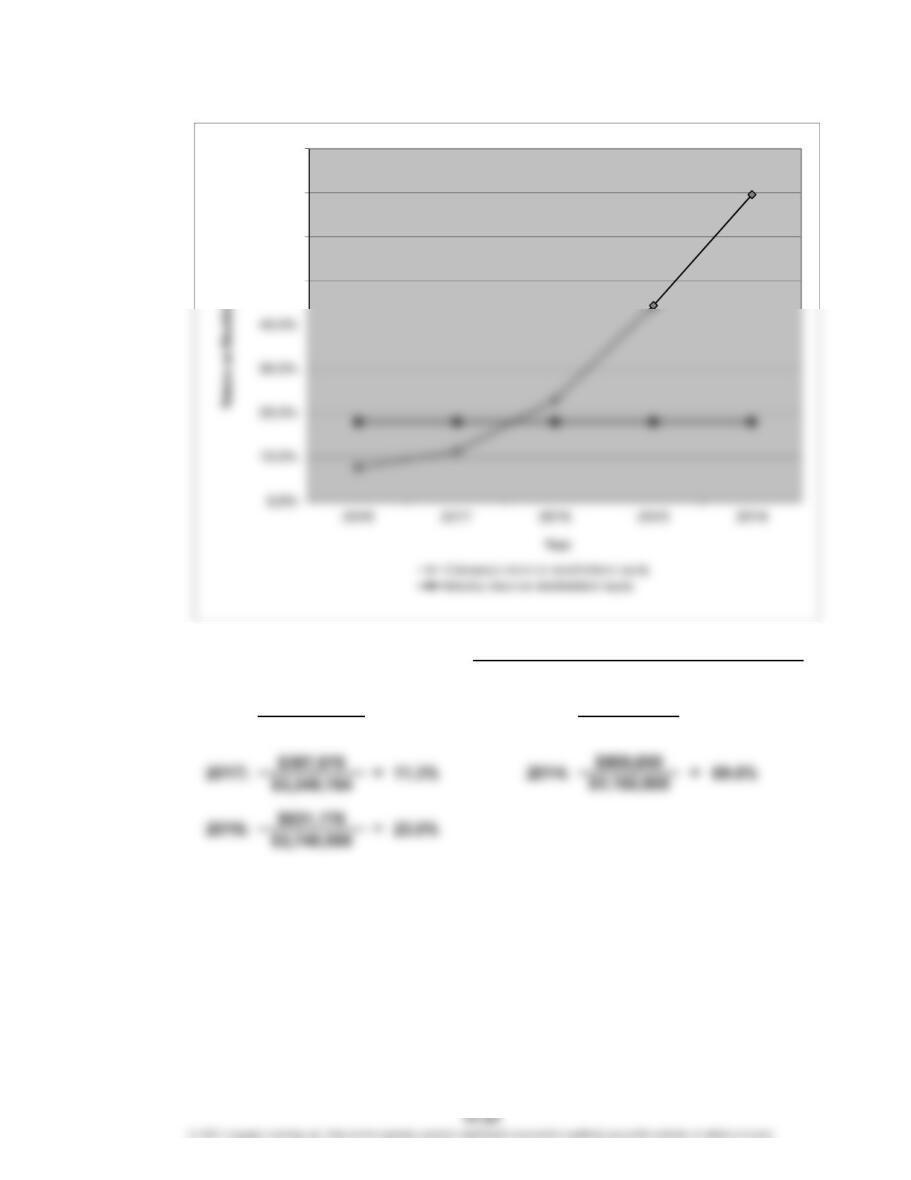

Prob. 17-5A (Continued)

1. b.

$273,406

$3,569,855

20Y8:

=

44.4%=

Average Total Stockholders’ Equity

Net Income

20Y5: $884,000

$1,992,000

7.7%

=Return on Stockholders’ Equity

50.0%

60.0%

70.0%

80.0%

CHAPTER 17 Financial Statement Analysis

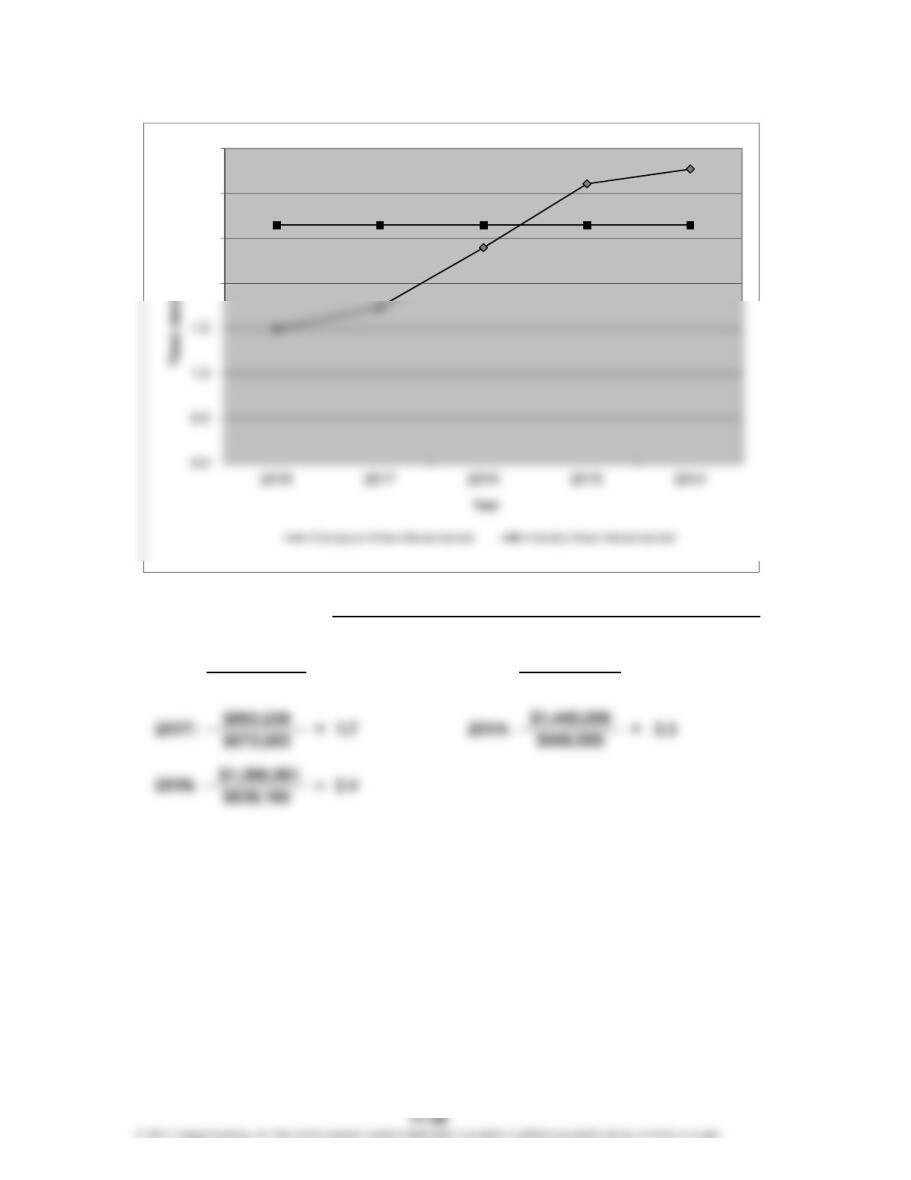

Prob. 17-5A (Continued)

1. c.

$921,202

$616,047

=

20Y8: =

Net Income + Income Tax Expense + Interest Expense

Interest Expense

Times Interest Earned

$1,539,000

$495,000 =20Y5:

3.1

1.5

2.0

2.5

3.0

3.5

CHAPTER 17 Financial Statement Analysis

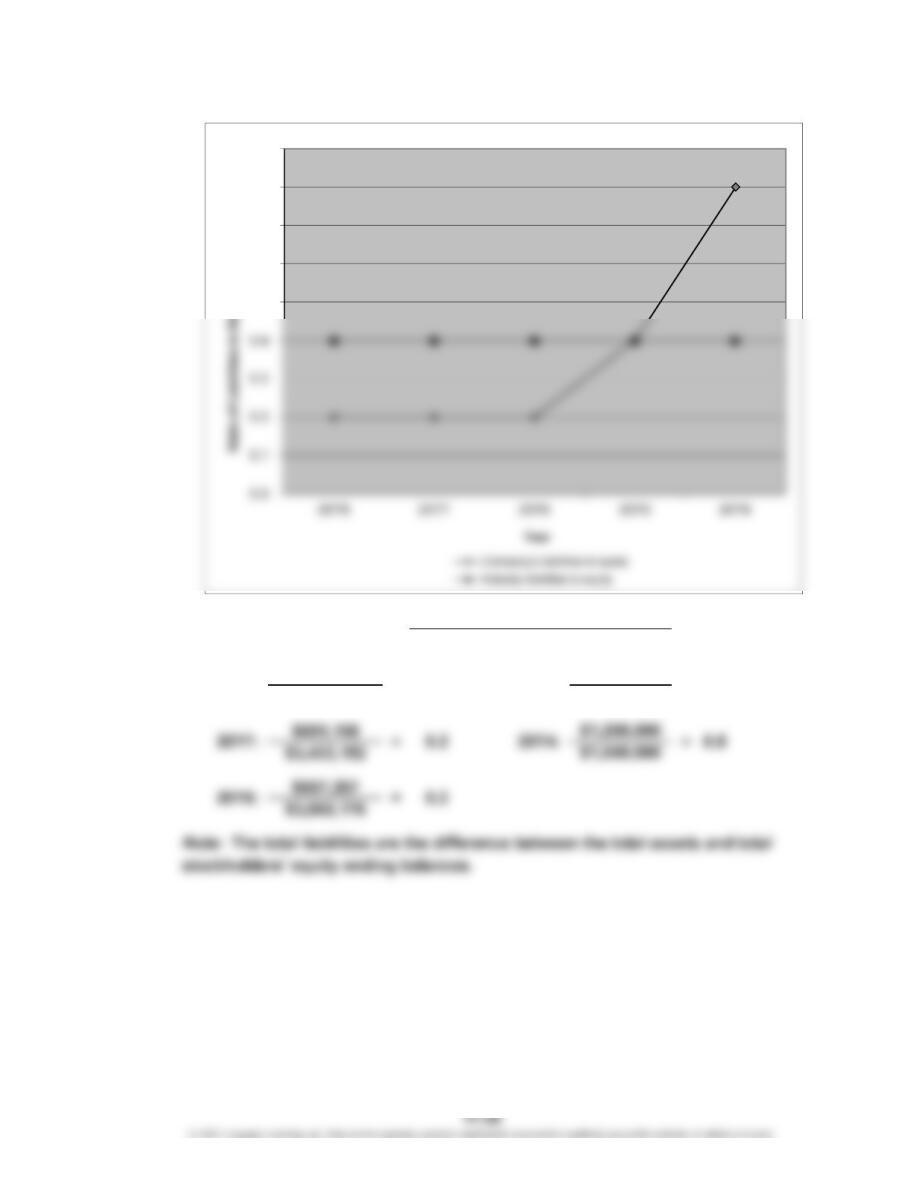

Prob. 17-5A (Continued)

1. d.

$710,621

$3,706,557

0.4

Total Liabilities

Total Stockholders’ Equity

$904,500

$2,434,000

=

20Y5:

Ratio of Liabilities to

Stockholders’ Equity =

=

20Y8: 0.2

0.5

0.6

0.7

0.8

0.9

CHAPTER 17 Financial Statement Analysis

Prob. 17-5A (Concluded)

2. Both the return on total assets and the return on stockholders’ equity have been

moving in a negative direction in the last five years. Both measures have moved

below the industry average over the last two years. The cause of this decline is

driven by a rapid decline in earnings. The use of debt can be seen from the ratio

Prob. 17-1B

1.

20Y2 20Y1 Amount Percent

Sales $805,200 $610,000 $195,200 32.0%

Cost of merchandise sold 365,400 280,000 85,400 30.5%

Gross profit $439,800 $330,000 $109,800 33.3%

Selling expenses $117,200 $ 92,000 $ 25,200 27.4%

2. The profitability has improved significantly from 20Y1 to 20Y2. Sales have

increased by 32.0% over the 20Y1 base year, while the cost of merchandise sold,

selling expenses, and administrative expenses grew at a slower rate. Increasing

sales combined with costs that increase at a slower rate results in strong earnings

growth. In this case, net income grew 32.0% over the base year.

Increase (Decrease)

Gerhardt Inc.

Comparative Income Statement

For the Years Ended December 31, 20Y2 and 20Y1