CHAPTER 17

Statement of Cash Flows

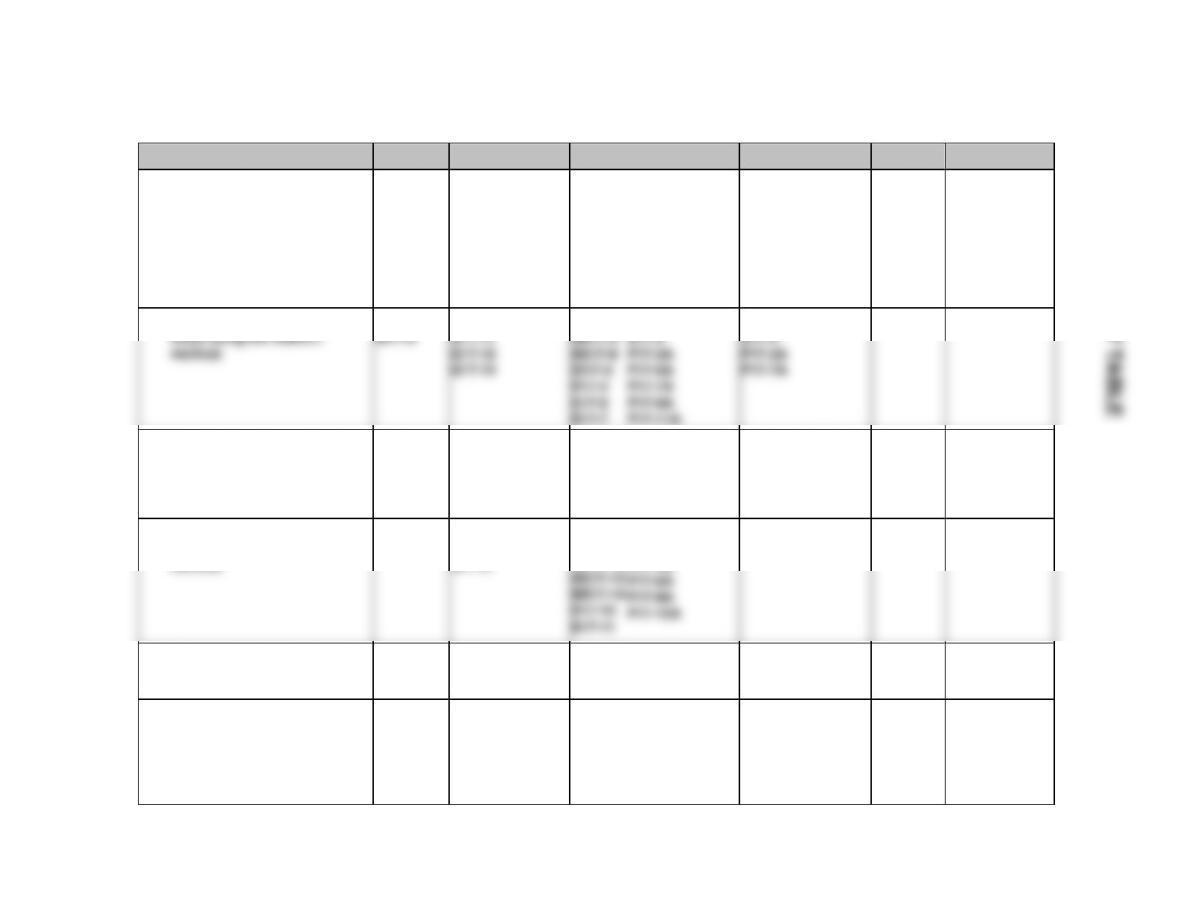

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

A

Problems

*1. Discuss the usefulness and

format of the statement of

cash flows.

1, 2, 3, 4, 5,

6, 7, 8, 9, 15,

16, 17

1, 2, 3

1

1, 2, 3

1A

*2. Prepare a statement of cash

flows using the indirect

method.

10, 11, 12,

13, 14

4, 5, 6, 7

2

4, 5, 6,

7, 8, 9

2A, 3A, 5A,

7A, 9A, 11A

*3. Analyze the statement of

8, 9, 10, 11

3

7, 9

7A, 8A

*4. Prepare a statement of cash

8, 18, 19, 20,

12, 13, 14

10, 11,

4A, 6A, 8A,

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A

Distinguish among operating, investing, and financing

activities.

Simple

10–15

2A

Determine cash flow effects of changes in equity accounts.

Simple

10–15

3A

Prepare the operating activities section—indirect method.

Simple

20–30

*4A

Prepare the operating activities section—direct method.

Simple

20–30

5A

Prepare the operating activities section—indirect method.

Simple

20–30

Prepare the operating activities section—direct method.

Simple

20–30

7A

Prepare a statement of cash flows—indirect method, and

compute free cash flow.

Moderate

40–50

*8A

Prepare a statement of cash flows—direct method, and

compute free cash flow.

Moderate

40–50

9A

Prepare a statement of cash flows—indirect method.

Moderate

40–50

*10A

Prepare a statement of cash flows—direct method.

Moderate

40–50

*12A

Prepare a worksheet—indirect method.

Moderate

40–50

WEYGANDT ACCOUNTING PRINCIPLES 12E

CHAPTER 17

STATEMENT OF CASH FLOWS

Number

LO

BT

Difficulty

Time (min.)

BE1

1

AP

Simple

3–5

BE2

1

C

Simple

2–4

BE3

1

AP

Simple

3–5

BE4

2

AP

4–6

BE5

2

AP

Simple

3–5

BE6

2

AP

Simple

4–6

BE7

2

AN

Moderate

3–5

BE8

3

AN

Simple

2–4

BE9

3

AN

Simple

2–3

BE10

3

AN

Simple

2–3

BE11

3

AN

Simple

4–6

*BE12

4

AP

Simple

2–4

*BE13

4

AP

Simple

3–5

*BE14

4

AP

Moderate

3–5

*BE15

5

AP

Simple

4–6

DI1

1

C

Simple

2–4

DI2

2

AP, C

Simple

4–6

DI3

3

AN, C

Simple

4–6

EX1

1

C

Simple

5–7

EX2

1

C

Simple

6–8

EX3

1

AP

Simple

8–10

EX4

2

AP

Simple

5–7

EX5

2

AP

Simple

6–8

EX6

2

AN

Moderate

10–12

EX7

2, 3

AP

Simple

12–14

EX8

2

AP

Simple

10–12

EX9

2, 3

AP

Simple

12–14

EX10

4

AP

Moderate

6–8

EX11

4

AP

Moderate

6–8

*EX12

4

AP

Simple

5–7

*EX13

4

AP

Moderate

6–8

STATEMENT OF CASH FLOWS (Continued)

Number

LO

BT

Difficulty

Time (min.)

*EX14

5

AP

Moderate

16–20

P1A

1

C

Simple

10–15

P2A

2

AN

Simple

10–15

P3A

2

AP

Simple

20–30

*P4A

4

AP

Simple

20–30

P5A

2

AP

Simple

20–30

*P6A

4

AP

Simple

20–30

P7A

Moderate

40–50

*P8A

Moderate

40–50

P9A

2

AP

Moderate

40–50

*P10A

4

AP

Moderate

40–50

P11A

2

AP

Moderate

40–50

*P12A

5

AP

Moderate

40–50

BYP1

1

AN

Simple

15–20

BYP2

3

AP, E

Simple

8–12

BYP3

3

AP, E

Simple

8–12

BYP4

2

C

Simple

15–20

BYP5

—

C

Simple

10–15

BYP6

—

AP

Moderate

25–30

BYP7

1

AP

Simple

10–15

BYP8

1

E

Simple

10–15

BYP9

—

E

Simple

15–20

BYP10

1

AP

Moderate

10–15

BLOOM’ S TAXONOMY TABLE

Correlation Chart between Bloom’s Taxonomy, Learning Objectives and End–of-Chapter Exercises and Problems

Learning Objective

Knowledge

Comprehension

Application

Analysis

Synthesis

Evaluation

1. Discuss the usefulness and

format of the statement of cash

flows.

Q17-4

Q17-6

Q17-1

Q17-2

Q17-3

Q17-5

Q17-7

Q17-8

Q17-9

Q17-15

Q17-16

Q17-17

BE17-2

DI17-1

E17-1

E17-2

P17-1A

BE17-1

BE17-3

E17-2

E17-3

2. Prepare a statement of cash

Q17-13

Q17-10

BE17-4

E17-8

BE17-7

3. Analyze the statement of

cash flows.

Dl17-3

E17-7

E17-9

P17-7A

P17-8A

BE17-8

BE17-9

BE17-10

BE17-11

DI17-3

P17-7A

P17-8A

*4. Prepare a statement of cash

flows using the direct

method.

Q17-8

Q17-18

Q17-21

Q17-19

Q17-20

BE17-12

E17-12

E17-13

P17-4A

P17-8A

*5 Use a worksheet to prepare the

statement of cash flows

using the indirect method.

Q17-22

BE17-15

E17-14

P17-12A

Broadening Your Perspective

Real-World Focus

Comparative Analysis

Decision Making Across

the Organization

Communication

FASB Codification

Financial Reporting

Comp. Analysis

Decision Making

Across the

Organization

Ethics Case

All About You

ANSWERS TO QUESTIONS

1. (a) The statement of cash flows reports the cash receipts, cash payments, and net change in cash

resulting from the operating, investing, and financing activities of a company during a

period.

(b) Disagree. The statement of cash flows is required. It is the fourth basic financial statement.

2. The statement of cash flows answers the following questions about cash: (a) Where did the cash

come from during the period? (b) What was the cash used for during the period? and (c) What was

the change in the cash balance during the period?

3. The three types of activities are:

Operating activities include the cash effects of transactions that create revenues and expenses

and thus enter into the determination of net income.

Investing activities include: (a) acquiring and disposing of investments and property, plant and

equipment and (b) lending money and collecting loans.

Financing activities include: (a) obtaining cash from issuing debt and repaying amounts borrowed

and (b) obtaining cash from stockholders, repurchasing shares, and paying dividends.

5. The statement of cash flows presents investing and financing activities so that even noncash

transactions of an investing and financing nature are disclosed in the financial statements. If they

affect financial conditions significantly, the FASB requires that they be disclosed in either a separate

schedule at the bottom of the statement of cash flows or in a separate note or supplementary

schedule to the financial statements.

6. Examples of significant noncash activities are: (1) issuance of stock for assets, (2) conversion of

bonds into common stock, (3) issuance of bonds or notes for assets, and (4) noncash exchanges

of property, plant, and equipment.

7. Comparative balance sheets, a current income statement, and certain transaction data all provide

information necessary for preparation of the statement of cash flows. Comparative balance sheets

indicate how assets, liabilities, and equities have changed during the period. A current income

statement provides information about the amount of cash provided or used by operations. Certain

transactions provide additional detailed information needed to determine how cash was provided

or used during the period.

Questions Chapter 17 (Continued)

9. When total cash inflows exceed total cash outflows, the excess is identified as a “net increase in cash”

near the bottom of the statement of cash flows.

10. The indirect method involves converting accrual net income to net cash provided by operating activities.

This is done by starting with accrual net income and adding or subtracting noncash items included

in net income. Examples of adjustments include depreciation and other noncash expenses, gains

and losses on the disposal of noncurrent assets, and changes in the balances of current asset

and current liability accounts from one period to the next.

12. A number of factors could have caused an increase in cash despite the net loss. These are (1) high

cash revenues relative to low cash expenses; (2) sales of property, plant, and equipment; (3) sales

of investments; (4) issuance of debt or capital stock, and (5) differences between cash and accrual

accounting, e.g. depreciation.

13. Depreciation expense.

Gain or loss on disposal of a noncurrent asset.

Increase/decrease in accounts receivable.

Increase/decrease in inventory.

Increase/decrease in accounts payable.

14. Under the indirect method, depreciation is added back to net income to reconcile net income to net

cash provided by operating activities because depreciation is an expense but not a cash payment.

15. The statement of cash flows is useful because it provides information to the investors, creditors,

and other users about: (1) the company’s ability to generate future cash flows, (2) the company’s ability

to pay dividends and meet obligations, (3) the reasons for the difference between net income and

net cash provided by operating activities, and (4) the cash investing and financing transactions

during the period.

16. This transaction is reported in the note or schedule entitled “Noncash investing and financing activities”

as follows: “Retirement of bonds payable through issuance of common stock, $1,700,000.”

Questions Chapter 17 (Continued)

+ Decrease in accounts receivable

*19.

(a)

Cash receipts from customers = Revenues from sales

– Increase in accounts receivable

+ Increase in inventory

(b)

Purchases = Cost of goods sold

– Decrease in inventory

+ Decrease in accounts payable

Cash payments to suppliers = Purchases

– Increase in accounts payable

*21. Depreciation expense is not listed in the direct method operating activities section because it is not

a cash flow item—it does not affect cash.

*22. A worksheet is desirable because it allows the accumulation and classification of data that will

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 17-1

(a) Cash inflow from financing activity, $200,000.

BRIEF EXERCISE 17-2

(a) Investing activity. (d) Operating activity.

(b) Investing activity. (e) Financing activity.

(c) Financing activity. (f) Financing activity.

BRIEF EXERCISE 17-3

BRIEF EXERCISE 17-4

Net income …………………………………………………. $2,800,000

Adjustments to reconcile net income

to net cash provided by operating activities

Depreciation expense …………………………... $160,000

BRIEF EXERCISE 17-5

Cash flows from operating activities

Net income ………………………………………………….. $280,000

Adjustments to reconcile net income

to net cash provided by operating activities

BRIEF EXERCISE 17-6

Net income …………………………………………………………. $300,000

Adjustments to reconcile net income to net

cash provided by operating activities

Decrease in accounts receivable …………………… $ 80,000)

BRIEF EXERCISE 17-7

Original cost of equipment sold …………………………... $22,000

Less: Accumulated depreciation …………………………. 5,500

Book value of equipment sold ……………………………… 16,500

BRIEF EXERCISE 17-8

Free cash flow = $155,793,000 – $132,280,000 – $5,000,000 = $18,513,000

BRIEF EXERCISE 17-9

BRIEF EXERCISE 17-11

Free cash flow is cash provided by operations less capital expenditures and cash

dividends paid. For Morrow Inc. this would be $384,000 ($734,000 – $280,000 –

$70,000). Since it has positive free cash flow that far exceeds its dividend, an

increase in the dividend might be possible. However, other factors should be

considered. For example, it must have adequate retained earnings, and it

should be convinced that a larger dividend can be sustained over future

years. It could also use the free cash flow to expand its operations or pay

down its debt.

*BRIEF EXERCISE 17-12

+ Decrease in accounts receivable

Receipts from

customers

=

Sales

revenues

– Increase in accounts receivable

$115,000,000 = $340,000,000 – $225,000,000*

*BRIEF EXERCISE 17-14

+ Increase in prepaid expenses

– Increase in accrued expenses payable

Cash

payments for

operating

=

Operating

expenses,

excluding

– Decrease in prepaid expenses

and

*BRIEF EXERCISE 17-15

Balance

1/1/17

Reconciling Items

Balance

12/31/17

Balance Sheet Accounts

Debit

Credit

Prepaid expenses

Accrued expenses payable

18,600

8,200

(a) 5,600

(b) 2,400

13,000

10,600

Statement of Cash Flow Effects

Operating activities

SOLUTIONS TO DO IT! REVIEW EXERCISES

DO IT! 17-1

1. Financing activity

2. Operating activity

DO IT! 17-2

Cash flows from operating activities

Net income ……………………………………………………. $130,000

Adjustments to reconcile net income to net

cash provided by operating activities:

Depreciation expense ……………………………… $6,000

DO IT! 17-3

(a) Free cash flow = $73,700 – $27,000 – $15,000 = $31,700

(b) Cash provided by operating activities fails to take into account that a

SOLUTIONS TO EXERCISES

EXERCISE 17-1

(a) Financing activities.

(b) Noncash investing and financing activities.

(c) Noncash investing and financing activities.

EXERCISE 17-2

(a)

(b)

Operating activity.

Noncash investing and

(i)

(j)

Operating activity.

Noncash investing and financing

EXERCISE 17-3

1. (a) Cash ………………………………………………….. 15,000

Land……………………………………………. 12,000

Gain on Disposal of Plant Assets ….. 3,000

2. (a) Cash ………………………………………………….. 20,000

Common Stock ……………………………. 20,000

EXERCISE 17-3 (Continued)

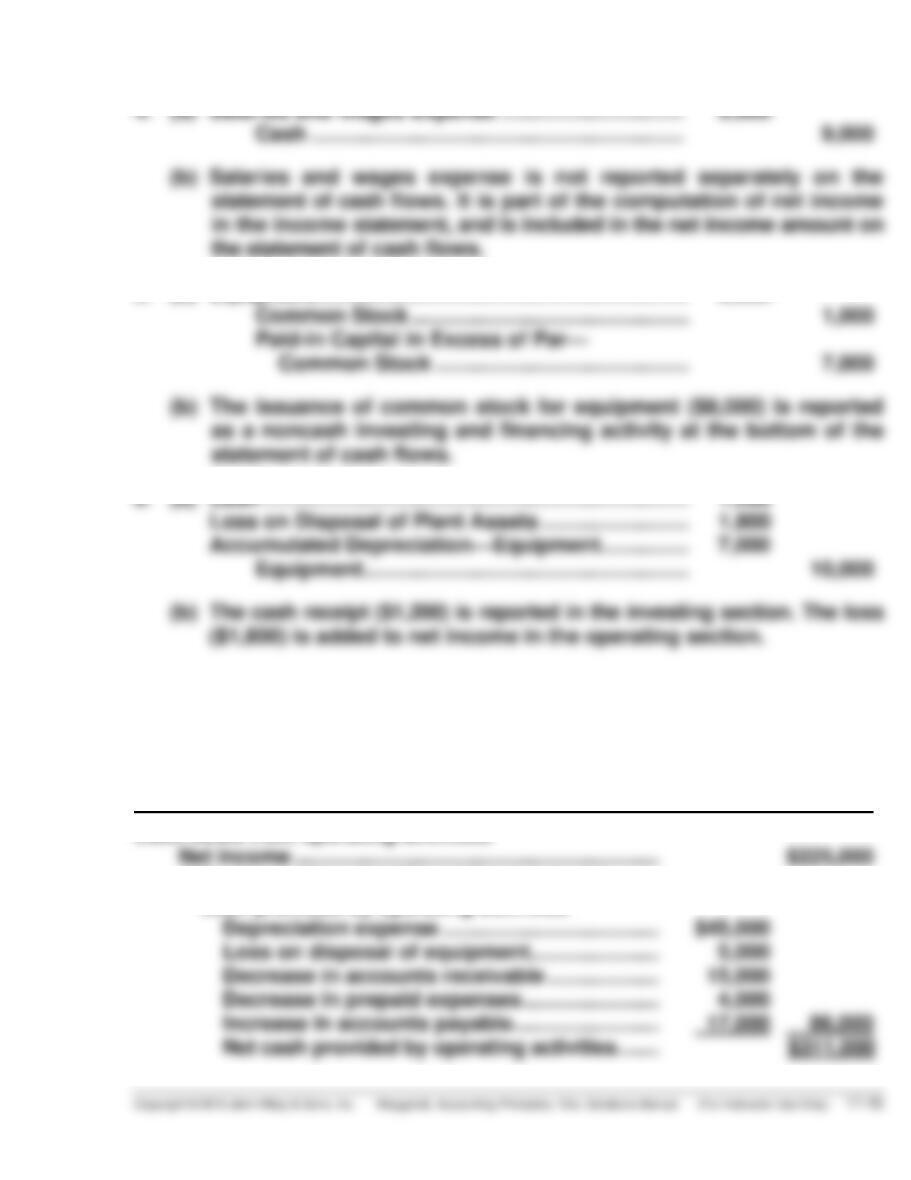

4. (a) Salaries and Wages Expense …………………………. 9,000

Cash ……………………………………………………… 9,000

5. (a) Equipment ……………………………………………………… 8,000

Common Stock ……………………………………….. 1,000

Paid-in Capital in Excess of Par—

Common Stock ……………………………………. 7,000

6. (a) Cash ……………………………………………………………… 1,200

Loss on Disposal of Plant Assets ……………………. 1,800

Accumulated Depreciation—Equipment …………… 7,000

Equipment ………………………………………………. 10,000

EXERCISE 17-4

GUTIERREZ COMPANY

Partial Statement of Cash Flows

For the Year Ended December 31, 2017

Cash flows from operating activities

Net income …………………………………………………….. $225,000

Adjustments to reconcile net income to net

cash provided by operating activities

Depreciation expense ………………………………. $45,000

EXERCISE 17-5

SCOGGIN INC.

Partial Statement of Cash Flows

For the Year Ended December 31, 2017

Cash flows from operating activities

Net income …………………………………………………. $153,000

Adjustments to reconcile net income to net

cash provided by operating activities

Depreciation expense …………………………... $24,000)

Increase in accounts receivable …………….. (21,000)

EXERCISE 17-6

HERRICK CORP

Partial Statement of Cash Flows

For the Year Ended December 31, 2017

Cash flows from operating activities

Net income ……………………………………………….. $ 77,000)

Cash flows from investing activities

Sale of equipment ……………………………………… 12,000*

Construction of equipment ………………………… (53,000)

Purchase of equipment ……………………………… (70,000)

Net cash used by investing activities …… (111,000)

Cash flows from financing activities

Payment of cash dividends ………………………… (14,000)

*Cost of equipment sold …………………………….. $ 49,000)

EXERCISE 17-7

(a) ROJAS CORPORATION

Statement of Cash Flows

For the Year Ended December 31, 2017

Cash flows from operating activities

Net income …………………………………………………. $ 22,630)

Adjustments to reconcile net income

to net cash provided by operating activities

Depreciation expense …………………………... $ 5,000

)

Cash flows from investing activities

Sale of land ………………………………………………… 4,900

Cash flows from financing activities

Issuance of common stock ………………………….. $ 6,000

EXERCISE 17-8

VELO COMPANY

Statement of Cash Flows

For the Year Ended December 31, 2017

Cash flows from operating activities

Net income …………………………………………… $93,000)

Adjustments to reconcile net income

to net cash provided by operating

activities

activities ……………………………………. 129,000)

Cash flows from investing activities

Sale of land ………………………………………….. 25,000)

Purchase of equipment …………………………. (70,000)

Net cash used by investing

activities ……………………………………. (45,000)

Cash flows from financing activities

Net increase in cash ……………………………………. 41,000)

Cash at beginning of period ………………………… 22,000)

Cash at end of period ………………………………….. $ 63,000)

EXERCISE 17-9

(a) RODRIQUEZ CORPORATION

Statement of Cash Flows

For the Year Ended December 31, 2017

Cash flows from operating activities

Net income …………………………..………………. $ 18,300)

Adjustments to reconcile net income

to net cash provided by operating

activities

Depreciation expense ……………………… $ 5,200* )

Cash flows from investing activities

Sale of equipment ………………………………… 3,300)

Purchase of investments ………………………. (4,000)

Net cash used by investing activities ……….. (700)

Cash flows from financing activities

Net increase in cash ……………………………………. (2,500))

Cash at beginning of period …………………………. 17,700

Cash at end of period ………………………………….. $ 15,200