1. Liquidity is the ability of a company to convert assets into cash. Short-term creditors such as banks

and financial institutions are most concerned with liquidity. Solvency is the ability of a company to

p

ay its debts. Long-term creditors such as bondholders are concerned primarily with a company’s

solvency. Profitability is the ability of a company to generate earnings. Investors such as

stockholders are concerned primarily with profitability because it determines whether the

company’s stock price will increase.

4. Generally, the two ratios would be very close because most service businesses sell services

and hold very little inventory.

5. a. A high inventory turnover minimizes the amount invested in inventories, thus freeing

funds for more advantageous use. Storage costs, administrative expenses, and losses

caused by obsolescence and adverse changes in prices are also kept to a minimum.

b. Yes. The inventory turnover relates to the “turnover” of inventory during the year, while

the number of days’ sales in inventory relates to the amount of inventory on hand at the

b

eginning and end of the year. Therefore, a business could have a high inventory turnover

during the year yet have a high number of days’ sales in inventory based on the

b

eginning and end-of-year inventory amounts.

6. The ratio of fixed assets to long-term liabilities increased from 3.4 ($1,360,000 ÷ $400,000) for

the preceding year to 4.2 ($1,260,000 ÷ $300,000) for the current year, indicating that the

company is in a stronger position now than in the preceding year to borrow additional funds

on a long-term basis.

CHAPTER 17

FINANCIAL STATEMENT ANALYSIS

DISCUSSION QUESTIONS

p

CHAPTER 17 Financial Statement Analysis

DISCUSSION QUESTIONS (Continued)

9. The dividend yield measures the rate of return common stockholders receive from a cash dividend.

The high dividend yield for Suburban Propane indicates that a significant portion of the return to

its shareholders comes in the form of a cash dividend. The lack of a dividend yield for Alphabet

indicates that the return to shareholders comes solely from stock appreciation.

CHAPTER 17 Financial Statement Analysis

PE 17-1A

or (4)% ($3,000 ÷ $75,000)

PE 17-1B

Accounts payable…………

…

$24,000 decrease ($176,000 – $200,000),

or (12)% ($24,000 ÷ $200,000)

Long-term debt……………… $13,950 increase ($168,950 – $155,000),

or 9% ($13,950 ÷ $155,000)

PE 17-2A

Amount Percentage

…

…

…

PE 17-2B

Amount Percentage

Sales…………………………

…

$1,400,000 100% ($1,400,000 ÷ $1,400,000)

Cost of merchandise sold…

…

812,000 58% ($812,000 ÷ $1,400,000)

Gross profit…………………

…

$ 588,000 42% ($588,000 ÷ $1,400,000)

PE 17-3A

= 2.0

= 1.4

PRACTICE EXERCISES

CHAPTER 17 Financial Statement Analysis

PE 17-3B

a. Current Ratio = Current Assets ÷ Current Liabilities

= ($320,000 + $170,000 + $140,000 + $450,000) ÷ $300,000

= 3.6

Average Accounts Receivable

Average Daily Sales

= $100,000 ÷ ($1,460,000 ÷ 365)

= $100,000 ÷ $4,000

= 25.0 days

PE 17-4B

a. =Sales ÷ Average Accounts Receivable

=$6,862,000 ÷ $365,000

=18.8

b. =Number of Days’ Sales in Receivables

Accounts Receivable Turnover

CHAPTER 17 Financial Statement Analysis

PE 17-5A

a. Inventory Turnover = Cost of Merchandise Sold ÷ Average Merchandise Inventory

= $558,000 ÷ $45,000

= 12.4

PE 17-5B

a. Inventory Turnover = Cost of Merchandise Sold ÷ Average Merchandise Inventory

= $680,400 ÷ $94,500

= 7.2

CHAPTER 17 Financial Statement Analysis

PE 17-6A

=

=

PE 17-6B

=

=

PE 17-7A

a.

=

a. =

Ratio of Fixed Assets to Long-Term Liabilities

=

$300,000

Fixed Assets

Long-Term Liabilities

$630,000 ÷ $140,000

Ratio of Fixed Assets to Long-Term Liabilities

=

Times Interest Earned

=

Income Before Income Tax +

Interest Expense

Interest Expense

$6,000,000 + $300,000

21.0

Fixed Assets

Long-Term Liabilities

$774,000 ÷ $430,000

1.8

4.5

CHAPTER 17 Financial Statement Analysis

PE 17-8A

Asset Turnover = Sales ÷ Average Total Assets

= $6,480,000 ÷ $2,400,000

= 2.7

PE 17-8B

PE 17-9A

$187,000

$1,700,000

= 11.0%

PE 17-9B

=

=

=

Return on Total Assets Net Income + Interest Expense

Average Total Assets

$110,000 + $77,000

$1,700,000

CHAPTER 17 Financial Statement Analysis

PE 17-10A

= $750,000 ÷ $5,000,000

= 15.0%

PE 17-10B

= $500,000 ÷ $3,125,000

= 16.0%

Net Income

Average Stockholders’ Equity

Return on Stockholders’ Equity Net Income

Average Stockholders’ Equity

a. =Return on Stockholders’ Equity

a. =

CHAPTER 17 Financial Statement Analysis

PE 17-11A

= ($460,000 – $40,000) ÷ 150,000

=

=

=

a. =

Earnings per Share

on Common Stock

Net Income – Preferred Dividends

Shares of Common Stock Outstanding

13.0

$2.80

b. Market Price per Share of Common Stock

Earnings per Share on Common Stock

$120.90 ÷ $9.30

Price-Earnings Ratio =

CHAPTER 17 Financial Statement Analysis

Ex. 17-1

a.

Amount Percent Amount Percent

Sales $4,000,000 100% $3,600,000 100%

Income tax expense 240,000 6% 216,000 6%

Net income $ 360,000 9% $ 504,000 14%

b. The vertical analysis indicates that the cost of merchandise sold as a percent of

Current Year Prior Year

EXERCISES

Innovation Quarter Inc.

Comparative Income Statement

For the Years Ended December 31

CHAPTER 17 Financial Statement Analysis

Ex. 17-2

a.

Amount Percent Amount Percent

Revenues:

Admissions $ 78,332 17.0% $ 86,949 19.0%

Event-related revenue 140,210 30.4% 133,632 29.2%

Total revenues $461,914 100.0% $458,358 100.0%

Expenses and other:

Direct expense of events $101,876 22.1% $ 98,973 21.6%

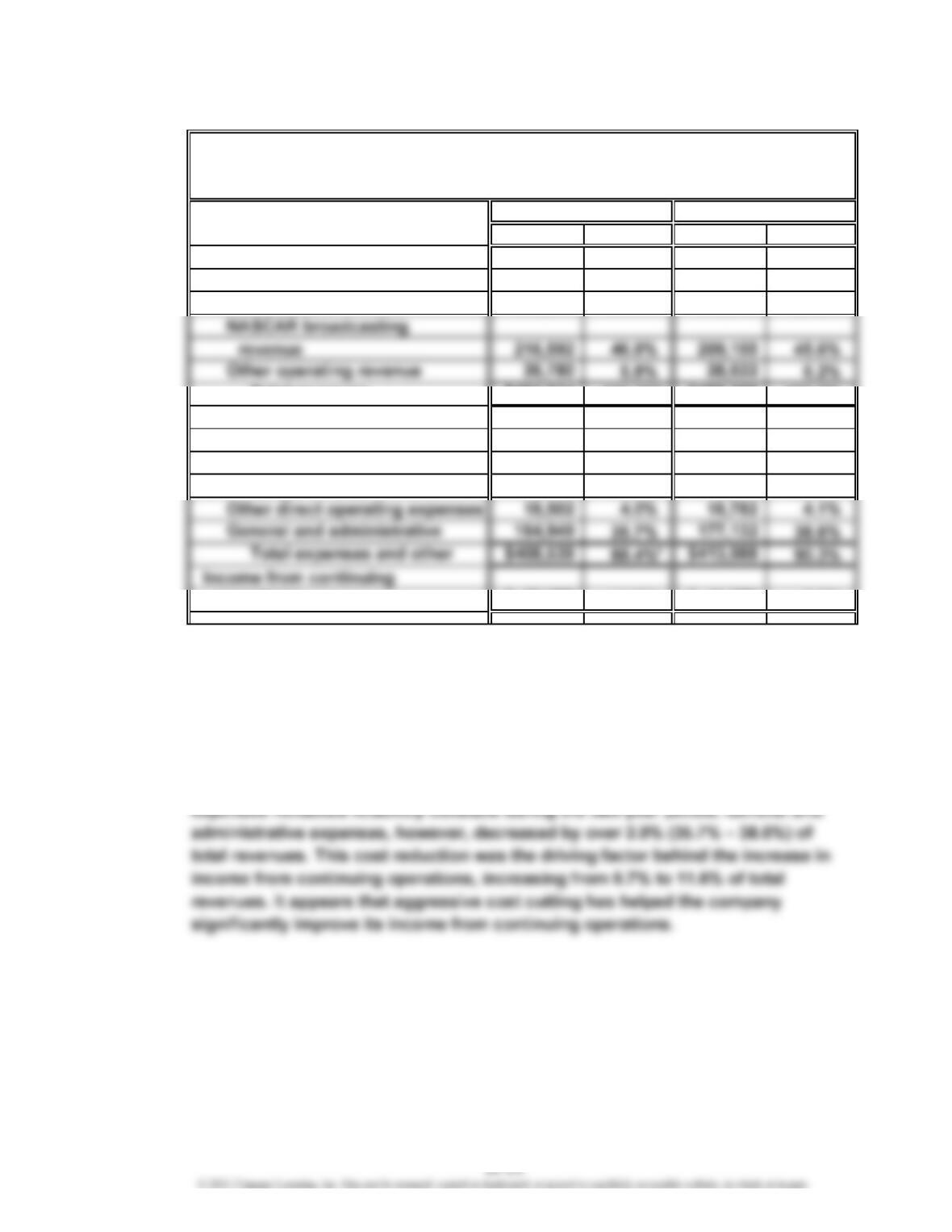

NASCAR event

management fees 123,212 26.7% 119,101 26.0%

operations $ 53,375 11.6% $ 44,370 9.7%

*

Totals may differ because of rounding.

b. Overall revenue increased some between the two years, accompanied by a slight

change in the overall mix of revenue sources. The NASCAR broadcasting revenue

increased by 1.3% (46.9% – 45.6%) of total revenues, and event-related revenue

increased by 1.2% (30.4% – 29.2%) of total revenues. One of the major expense

categories, NASCAR event management fees, increased by 0.7% (26.7% – 26.0%)

of total revenues. The direct expense of events and other direct operating

Current Year Prior Year

Speedway Motorsports, Inc.

Comparative Income Statement (in thousands of dollars)

For the Years Ended December 31

*

CHAPTER 17 Financial Statement Analysis

Ex. 17-3

a.

Amount Percent

Sales $4,000,000 100%

Cost of merchandise sold 2,120,000 53%

Total operating expenses $1,720,000 43%

Income from operations $ 160,000 4%

Other revenue and expense:

Other revenue 120,000 3%

b. The cost of merchandise sold is 7% (60% – 53%) lower than the industry average,

but the selling expenses and administrative expenses are 3% and 2% higher than

the industry average, respectively. The combined impact causes net income as a

percent of sales to be 2% better than the industry average. Apparently, the company

60%

Tannenhill Company

Common-Sized Income Statement

For the Year Ended December 31

38%

2%

3%

Tannenhill

Company

Industry

Average

Electronics

100%

CHAPTER 17 Financial Statement Analysis

Ex. 17-4

Amount Percent Amount Percent

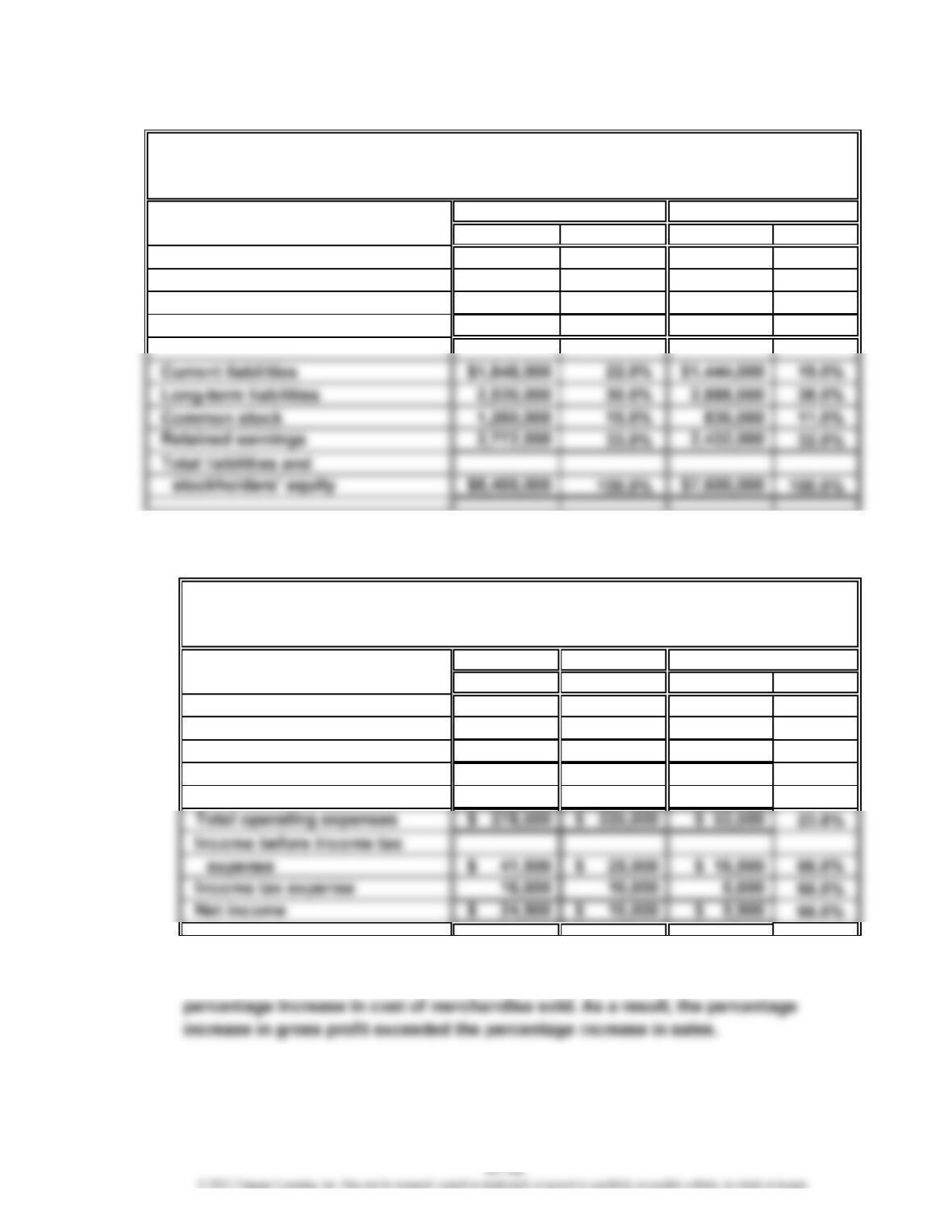

Current assets $2,352,000 28.0% $1,900,000 25.0%

Property, plant, and equipment 4,536,000 54.0% 4,712,000 62.0%

Intangible assets 1,512,000 18.0% 988,000 13.0%

Total assets $8,400,000 100.0% $7,600,000 100.0%

Ex. 17-5

a.

Current Year Prior Year

Amount Amount Amount Percent

Sales $2,280,000 $2,000,000 $280,000 14.0%

Cost of merchandise sold 1,960,000 1,750,000 210,000 12.0%

Gross profit $ 320,000 $ 250,000 $ 70,000 28.0%

Selling expenses $ 156,500 $ 125,000 $ 31,500 25.2%

Administrative expenses 122,000 100,000 22,000 22.0%

b. The net income for Winthrop Company increased by 66% between years. This

increase was the combined result of an increase in sales of 14% and a lower

Kwan Company

Comparative Balance Sheet

For the Years Ended December 31

Increase (Decrease)

Winthrop Company

Comparative Income Statement

For the Years Ended December 31

Current Year Prior Year

CHAPTER 17 Financial Statement Analysis

Ex. 17-6

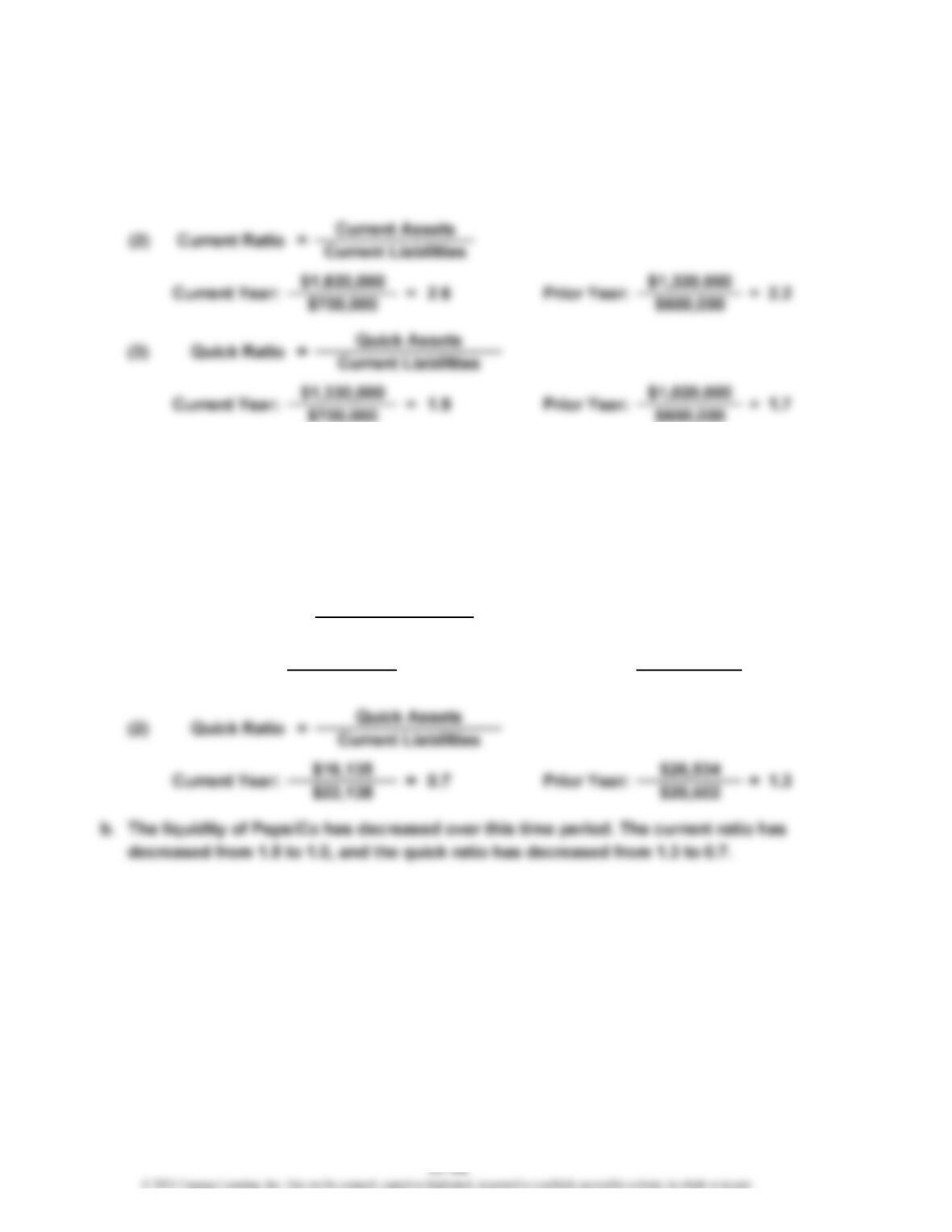

a. (1) Working Capital = Current Assets – Current Liabilities

Current year: $1,120,000 = $1,820,000 – $700,000

Prior year: $720,000 = $1,320,000 – $600,000

b. The liquidity of Albertini has improved from the preceding year to the current year.

The working capital, current ratio, and quick ratio have all increased. Most of

these changes are the result of an increase in current assets relative to current

liabilities.

Ex. 17-7

Current Year: $21,893 Prior Year:

Current Assets

Current Liabilities

$31,027

= 1.5

$22,138 $20,502

= 1.0

a.

=Current Ratio(1)

CHAPTER 17 Financial Statement Analysis

Ex. 17-8

a. The working capital, current ratio, and quick ratio are calculated incorrectly. The

working capital and current ratio incorrectly include intangible assets and property,

plant, and equipment as a part of current assets. Both are noncurrent. The quick

ratio has an incorrect numerator and denominator. The numerator of the quick

The correct calculations are as follows:

= Current Assets – Current Liabilities

= $330,000 – $300,000

b. Unfortunately, the working capital, current ratio, and quick ratio are below the

minimum threshold required by the bond indenture. This may require the company

to renegotiate the bond contract, including a possible unfavorable change in the

interest rate.

1.1

$330,000

Working Capital

$30,000

Current Assets

Current Liabilities

=

=

$300,000

=

Current Ratio

CHAPTER 17 Financial Statement Analysis

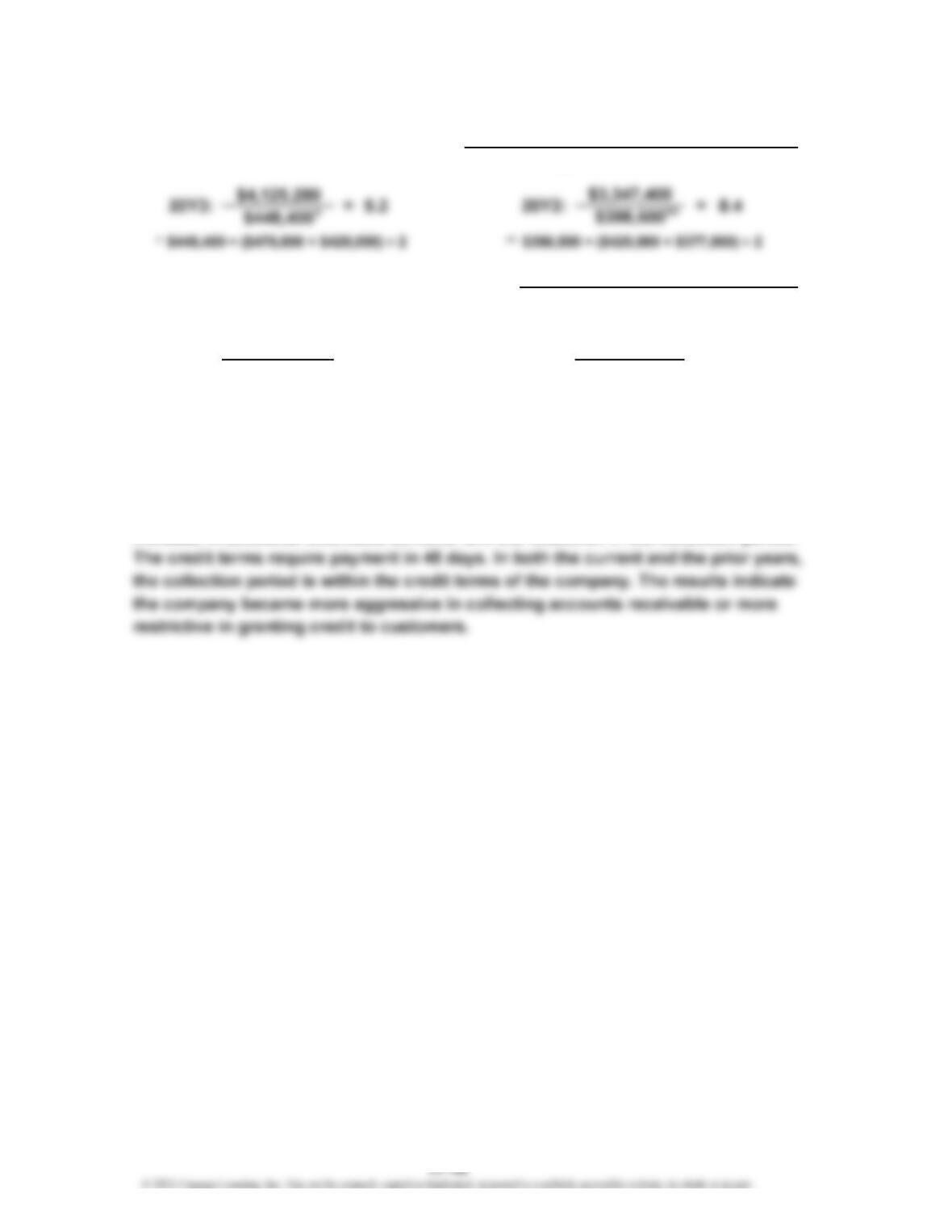

Ex. 17-9

$448,400

$11,302

1

2

Average daily sales = $11,302 = $4,125,280 ÷ 365 days

3

4

Average daily sales = $9,171 = $3,347,400 ÷ 365 days

b. The collection of accounts receivable has improved. This can be seen in both the

Average accounts receivable = $448,400 = ($476,800 + $420,000) ÷ 2

Average accounts receivable = $398,500 = ($420,000 + $377,000) ÷ 2

a. (1) =

Accounts Receivable Turnover

Average Accounts Receivable

Sales

43.5 days

$398,500 =

(2)

$9,171

20Y3: = 39.7 days 20Y2:

=Number of Days’ Sales in Receivables Average Accounts Receivable

Average Daily Sales

1

2

3

4

CHAPTER 17 Financial Statement Analysis

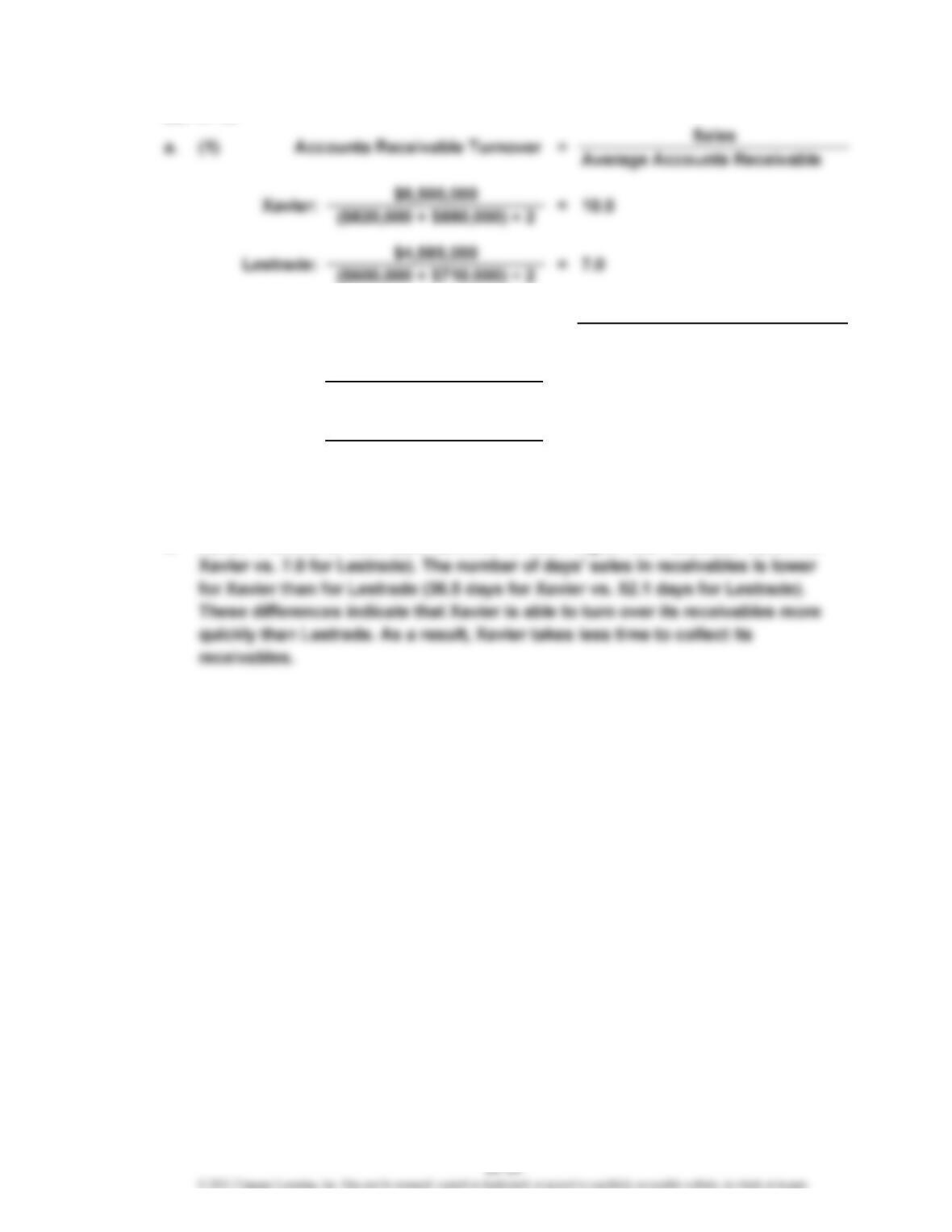

*

Average daily sales = $23,287.7 = $8,500,000 ÷ 365 days

**

Average daily sales = $12,561.6 = $4,585,000 ÷ 365 days

b. Xavier’s accounts receivable turnover is much higher than Lestrade’s (10.0 for

Xavier: =

($820,000 + $880,000) ÷ 2

$23,287.7

(2)

Number of Days’ Sales in Receivables

Average Accounts Receivable

Average Daily Sales

52.1 daysLestrade: ($600,000 + $710,000) ÷ 2

$12,561.6 =

36.5 days

=

*

**

CHAPTER 17 Financial Statement Analysis

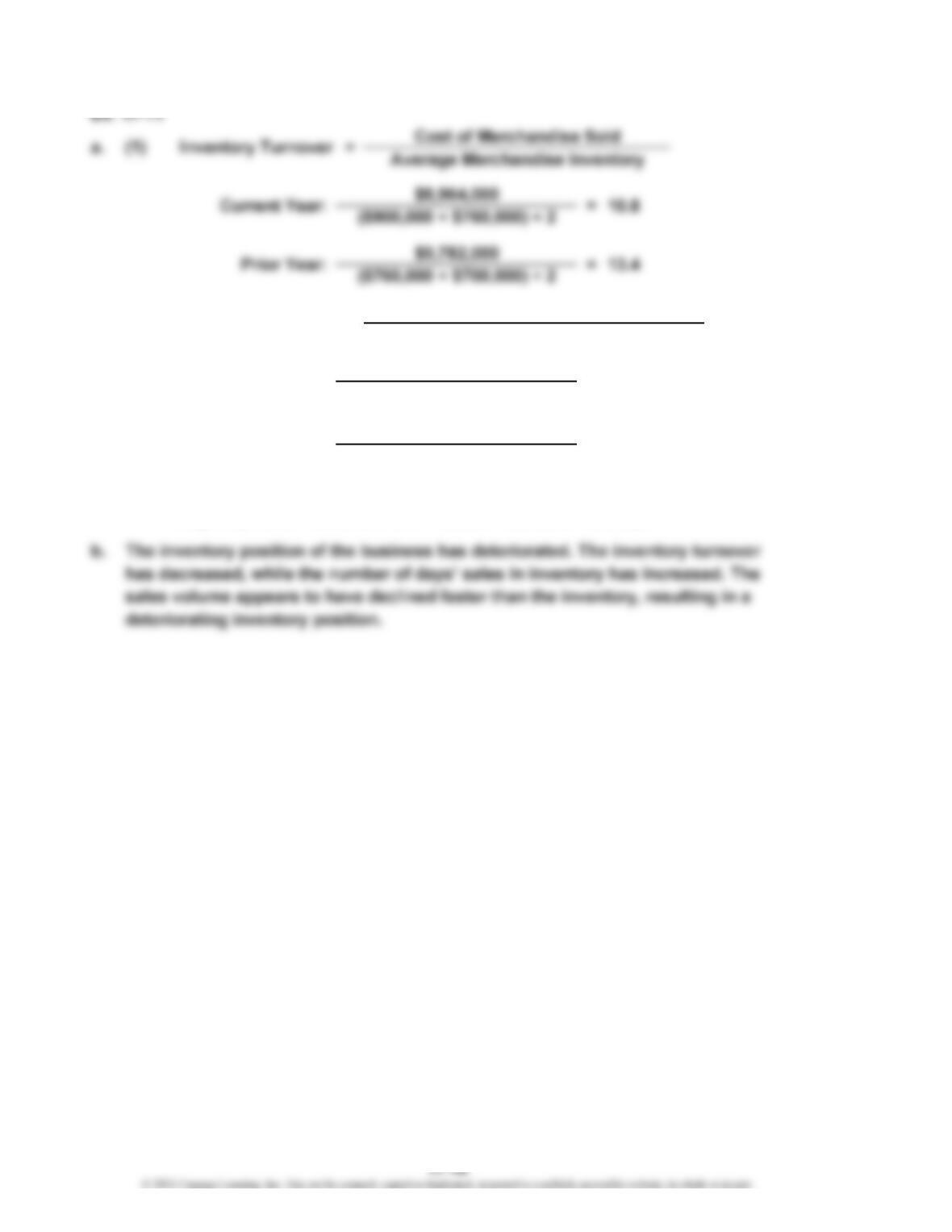

(2)

*

Average daily cost of merchandise sold = $24,559 = $8,964,000 ÷ 365 days

**

Average daily cost of merchandise sold = $26,800 = $9,782,000 ÷ 365 days

Number of Days’

Sales in Inventory Average Daily Cost of Merchandise Sold

Average Merchandise Inventory

=

33.8 days

27.2 days=

=

($900,000 + $760,000) ÷ 2

Current Year:

Prior Year:

$24,559

($760,000 + $700,000) ÷ 2

$26,800

**

*

CHAPTER 17 Financial Statement Analysis

Ex. 17-12

b. QT has a much higher inventory turnover ratio than does Elppa (32.1 vs. 13.4).

Likewise, QT has a much smaller number of days’ sales in inventory (11.4 days vs.

27.3 days). These significant differences are a result of QT’s make-to-order strateg

y

whereby QT has successfully developed a manufacturing process that fills a

=

Cost of Merchandise Sold

Average Merchandise Inventory

$44,754

($1,382 + $1,404) ÷ 2

32.1

13.4

$92,385

($6,317 + $7,490) ÷ 2

Elppa:

QT:

a. (1) Inventory Turnover =

=

CHAPTER 17 Financial Statement Analysis

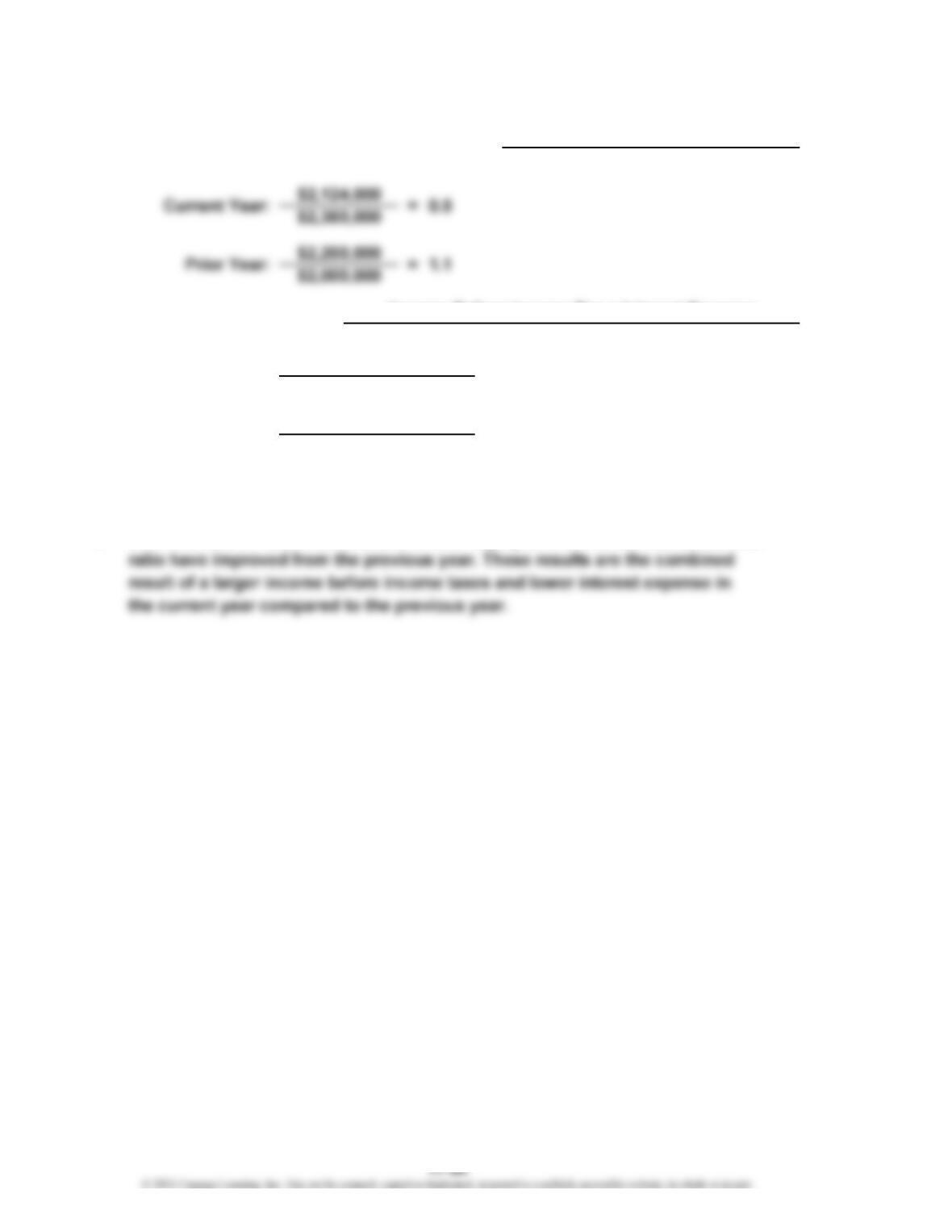

Ex. 17-13

*

Interest expense = ($1,000,000 + $200,000) × 10% = $120,000

**

Interest expense = ($1,200,000 + $200,000) × 10% = $140,000

c. Both the ratio of liabilities to stockholders’ equity and the times interest earned

Prior Year:

$480,000 + $120,000

$120,000

$420,000 + $140,000

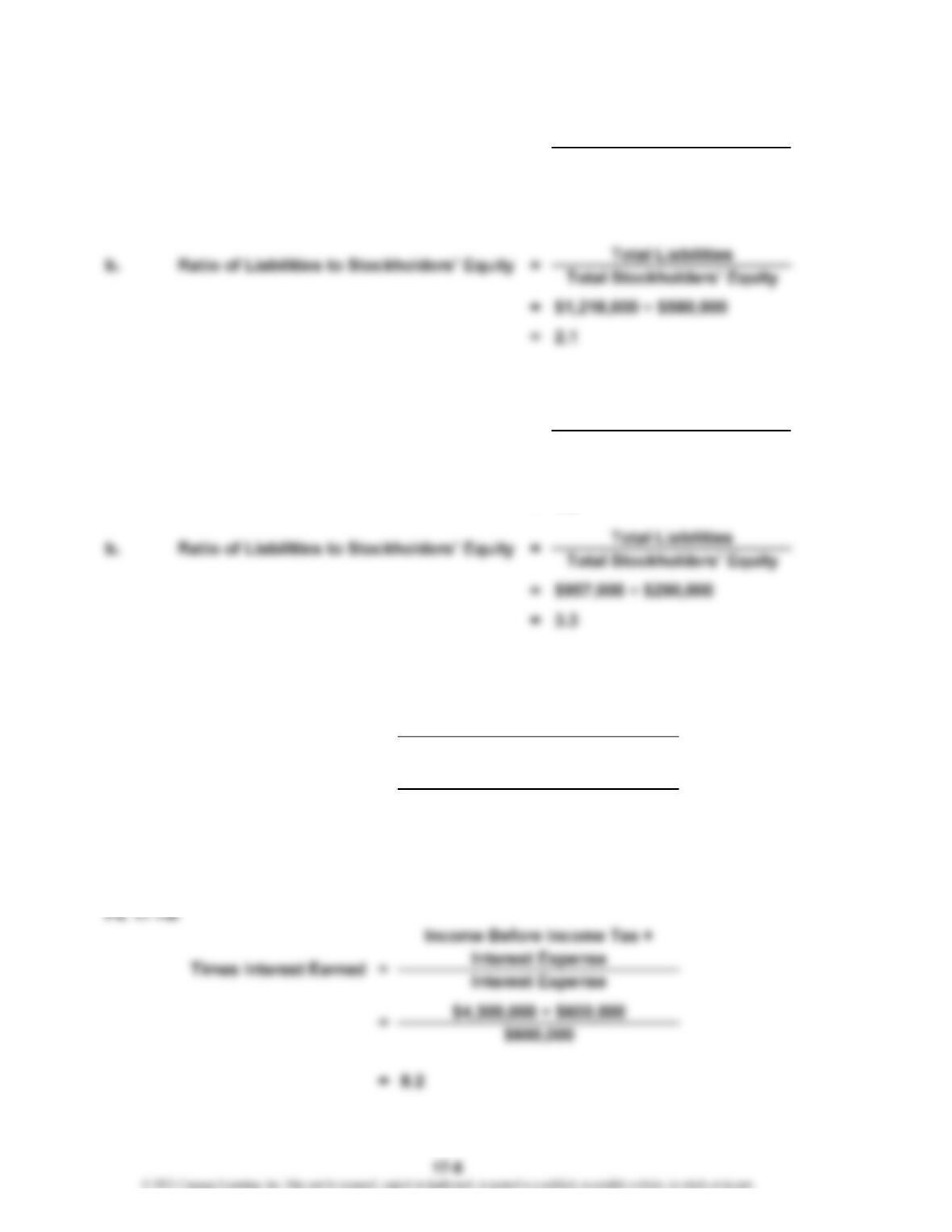

5.0Current Year:

$140,000

=

=

Total Liabilities

Total Stockholders’ Equity

=

4.0

=

a.

b.

Times Interest Earned Income Before Income Tax + Interest Expense

Interest Expense

Ratio of Liabilities to Stockholders’ Equity

*

**