PROBLEM 17-28 (CONTINUED)

2. October production cost per gallon:

Product

HTP-3

PST-4

RJ-5

Joint cost allocation …………………………...

$ 654,840

$ 436,560

$268,600

Additional processing costs ………………..

699,200

652,800

48,000

Total cost

$1,089,360

$316,600

Quantity produced (gallons) ………………..

Inventory valuation:

Product

HTP-3

PST-4

RJ-5

October 1 inventory (gallons) ……………….

18,000

52,000

3,000

October production (gallons) ……………….

Quantity available (gallons) ………………….

October sales (gallons) ………………………..

October 31 inventory (gallons) ……………..

23,000

3. LeMonde Company should sell PST-4 at the split-off point. The incremental revenue

of sales beyond the split-off point is less than the incremental cost of further

processing.

Per gallon sales value beyond the split-off point …………………………..

$4.80

Per gallon sales value at the split-off point ……………………………………………………..

Incremental sales value ………………………………………………………………………………….

$1.76

Per gallon gain (loss) of further processing …………………………..

$ (.11

)

PROBLEM 17-29 (35 MINUTES)

1. Joint cost allocations using the relative-sales-value method:

Gamma: joint cost allocation

=

off–splitat valuesales total

off–splitat valuesales sGamma’

joint cost

=

$78,000 – $46,800 – $11,700 = $19,500

Summary of joint cost allocations:

Alpha …………………………………………………………………………………………………………….

$46,800

(given)

Beta ………………………………………………………………………………………………………………

19,500

Gamma ……………………………………………………………………………………

Total ……………………………………………………………………………………………………………..

$78,000

2.

Alpha’s joint cost allocation

=

off–splitat valuesales total

off–splitat valuesales sAlpha’

joint cost

=

$78,000

=

$78,000

PROBLEM 17-29 (CONTINUED)

3. Joint cost allocation using the net-realizable-value method:

Joint

Cost

Joint

Products

Sales Value of

Final Product

Separable

Cost of

Processing

Net

Realizable

Value

Relative

Proportion

Allocation

of Joint

Cost

PROBLEM 17-30 (30 MINUTES)

1. Physical-units method of allocation:

Joint

Joint

Quantity at

Relative

Allocation of

2. Relative-sales-value method of allocation:

Joint

Joint

Sales Value at

Relative

Allocation of

Chapter 17 – Allocation of Support Activity Costs and Joint Costs

PROBLEM 17-30 (CONTINUED)

3. Net-realizable-value method of allocation:

$750,000

Sales

Additional

Net

Allocation

*$12.50 60,000

†$25 (90,000 – 10,000)

Joint cost allocation …………………………………………………………

$ 500,000

Additional processing costs ……………………………………………..

Total cost ……………………………………………………….………………..

$1,500,000

Quantity (good units) ………………………………………………………..

Cost per unit ($1,500,000 ÷ 80,000) …………………………………….

4.

Sales value if coated (60,000 $12.50) ………………………………

$ 750,000

Additional cost of coating …………………………………………………

250,000

Incremental contribution if coated …………………………………….

$ 500,000

300,000

Decline in contribution if uncoated ……………………………………

5. The allocation of joint costs is irrelevant to the decision about coating the mine

Chapter 17 – Allocation of Support Activity Costs and Joint Costs

PROBLEM 17-31 (40 MINUTES)

1. Joint costs arise from the simultaneous processing or manufacturing of two or more

products made from the same process. These joint costs are not traceable to any

2. The dollar value of the finished-goods inventories on November 30 for products MJ-4

and HD–10 are calculated as follows:

MJ-4 HD–10

November production (in gallons) ……………………… 600,000 320,000

Final sales value per gallon ………………………………. $8.00 $12.75

Chapter 17 – Allocation of Support Activity Costs and Joint Costs

PROBLEM 17-31 (CONTINUED)

Inventory values on November 30:

MJ-4 HD–10

Joint cost allocation …………………………………………. $1,800,000 $1,200,000

3. Wyalusing Chemicals should continue to process HD-10 beyond the split-off point,

since the incremental revenue is $1.00 greater per gallon than the incremental cost.

The joint cost is irrelevant to the decision because it will not change regardless of

Chapter 17 – Allocation of Support Activity Costs and Joint Costs

PROBLEM 17-32 (45 MINUTES)

1. Physical-units method:

Joint Cost

Joint

Cost

Joint

Quantity at

Relative

Allocation of

2. Relative-sales-value method:

Cost

Joint

Relative

Allocation of

Joint

3. Now there are additional processing costs beyond the split-off point.

b. Net-realizable-value method:

Joint

Cost

per Run

Joint

Products

Sales Value of

Final Product

Separable Cost

of Processing

Net

Realizable

Value

Relative

Proportion

Allocation

of Joint

Cost

Chapter 17 – Allocation of Support Activity Costs and Joint Costs

PROBLEM 17-32 (CONTINUED)

4.

Incremental revenue per gallon from further processing

into Compodalene ($7.80 – $6.00) …………………………………………………………………

$1.80

Incremental cost per gallon from further processing:

$1.20

Incremental loss per gallon from further processing

5. The director of research, Jack Turner, acted improperly in asking the assistant

controller to alter her analysis in favor of producing Compodalene. If he believes the

further processing of Compod is in Chemco’s best interests, he should try to back

up his claim with some projected cost reductions and the potential impact on the

Chapter 17 – Allocation of Support Activity Costs and Joint Costs

PROBLEM 17-32 (CONTINUED)

6. It is preferable to sell Compod than to sell Compodalene, as the solution to

requirement (4) showed. Nevertheless, it is preferable to sell Compodalene than to

sell nothing, since each gallon of Compodalene makes a positive contribution

toward covering the joint production cost, fixed costs, and profit.

PROBLEM 17-33 (30 MINUTES)

1. Reciprocal-services method:

Equations: M = 96,000 + .2C

PROBLEM 17-33 (CONTINUED)

Solution of equations:

Allocation:

Service Departments

Production Departments

Maintenance

Computing

Etching

Finishing

Traceable costs …………………..

$ 96,000

$500,000

Allocation of Maintenance

Department costs ……………..

(200,000

)

20,000

(.1)

$ 20,000

(.1)

$160,000

(.8)

Department costs ……………..

(.2)

(520,000

)

(.7)

(.1)

Total service department costs allocated ………………………..

$384,000

$212,000

Overhead costs traceable to production departments ……..

Total overhead cost ……………………………………………………….

$784,000

Direct-labor hours (DLH)

40,000

Overhead rate per hour (total overhead ÷ DLH) ……………….

$19.60

$5.325

Check on allocation procedure:

Allocation of Computing

2. The direct allocation method ignores any service rendered by one service

department to another. Allocation of each service department’s total cost is made

Chapter 17 – Allocation of Support Activity Costs and Joint Costs

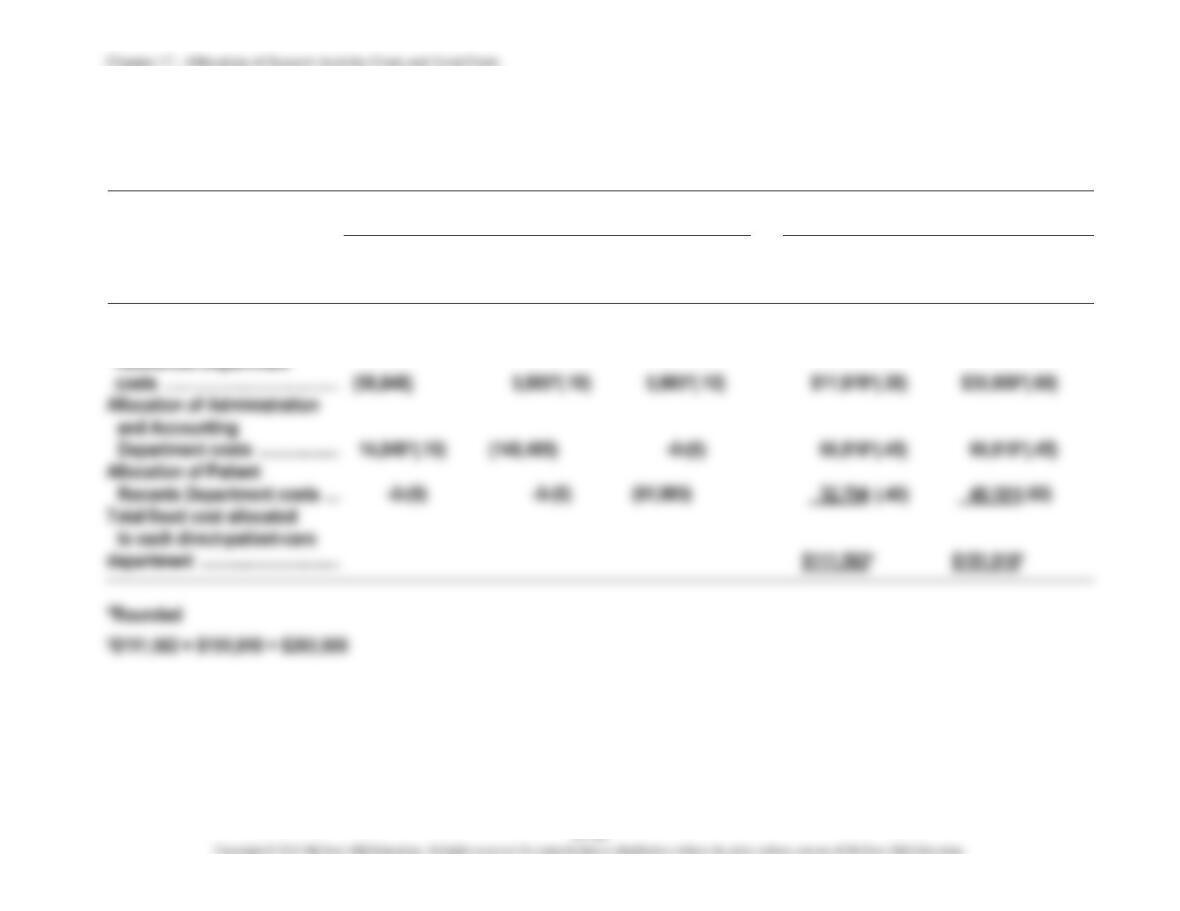

PROBLEM 17-34 (55 MINUTES)

1. Variable costs:

Notation: R denotes the total variable cost of Patient Records

H denotes the total variable cost of Human Resources

A denotes the total variable cost of Administration and Accounting

Chapter 17 – Allocation of Support Activity Costs and Joint Costs

PROBLEM 17-34 (CONTINUED)

Allocation of variable costs:

Service Departments

Direct-Patient-Care

Departments

Human

Resources

Administration

and

Accounting

Patient

Records

Orthopedics

Internal Medicine

Traceable costs ……………………

$15,000

$47,500

$24,000

)

(.20)

*(.05)

*(.25)

*(.50)

Allocation of Administration

*(.05)

(51,010

)

(0)

*(.35)

(.60)

(0)

(0)

)

*(.30)

*(.70)

Allocation of Human

PROBLEM 17-34 (CONTINUED)

2. Fixed costs:

Notation: R denotes the total fixed cost of Patient Records

H denotes the total fixed cost of Human Resources

A denotes the total fixed cost of Administration and Accounting

PROBLEM 17-34 (CONTINUED)

Allocation of fixed costs:

Service Departments

Direct-Patient-Care

Departments

Human

Resources

Administration

and

Accounting

Patient

Records

Orthopedics

Internal Medicine

Traceable costs ……………………

$45,000

$142,500

$76,000

)

*(.10)

*(.10)

$11,970

*(.20)

*(.60)

Allocation of Administration

14,849

*(.10)

)

(0)

*(.45)

*(.45)

(0)

(0)

)

(.60)

Allocation of Human

Resources Department

Chapter 17 – Allocation of Support Activity Costs and Joint Costs

PROBLEM 17-34 (CONTINUED)

Total costs allocated:

Orthopedics

Internal

Medicine

Variable costs ………………………………………………………………….

$ 29,705

$ 56,797

Fixed costs ……………………………………………………….……………..

Total costs ……………………………………………………………………….

Chapter 17 – Allocation of Support Activity Costs and Joint Costs

SOLUTIONS TO CASES

CASE 17-35 (40 MINUTES)

1. Product output in pounds:

Product

Proportion

Total

Pounds

Pounds

Lost in

Processing

Net

Pounds

Slices

.35

189,000

—

189,000

Crushed

.28

151,200

—

151,200

Juice

.27

145,800

135,000

Animal feed

.10

*Evaporation loss is 8% of the remaining good output. Let X denote the remaining

quantity of juice:

145,800 – .08X

=

X

=

2. Net realizable value at the split-off point:

Product

Pounds of

Production

Selling

Price

Sales

Revenue

Separable

Cost

Net Realizable Value

Amount

Percent

Slices

189,000

1.20

$226,800

$18,800

$208,000

52%

Crushed

151,200

1.10

31%

Juice

135,000

17%

Chapter 17 – Allocation of Support Activity Costs and Joint Costs

CASE 17-35 (CONTINUED)

3. Allocation of joint costs:

Cutting department costs …………………………………………………

$240,000

Less net realizable value of by-product

)

$232,000

Allocation of joint cost:

52% …………………………..……………………

$120,640

31% …………………………..……………………

17% …………………………..……………………

Total ………………………………………………………………………………..

$232,000

Chapter 17 – Allocation of Support Activity Costs and Joint Costs

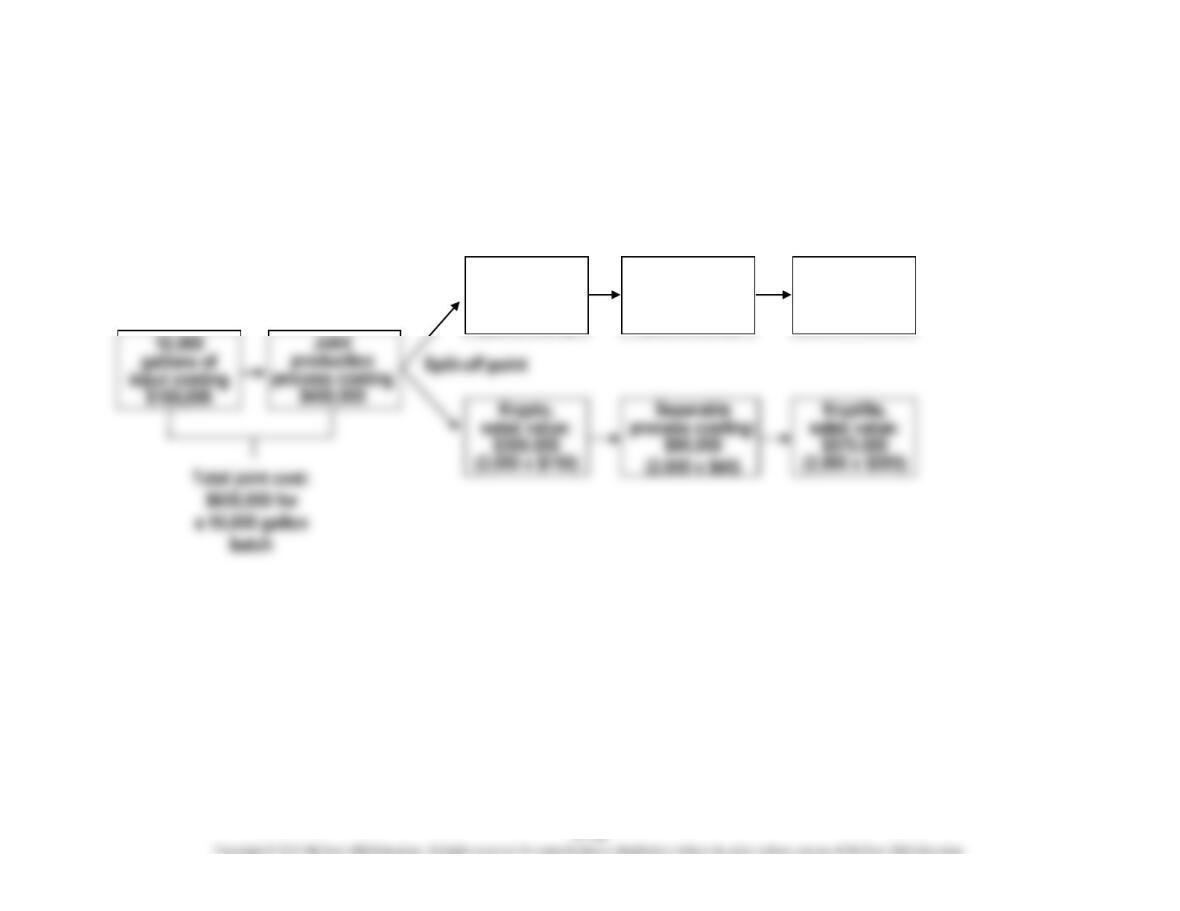

CASE 17-36 (50 MINUTES)

1. Diagram of joint production process:

Resoline,

sales value:

$600,000

(8,000 x $75)

Separable

process costing:

$120,000

(8,000 x $15)

Resolite,

sales value:

$840,000

(8,000 x $105)

Chapter 17 – Allocation of Support Activity Costs and Joint Costs

CASE 17-36 (CONTINUED)

2. Allocation of joint costs:

a. Physical-units method:

Joint

Cost

Joint

Products

Quantity at

Split-Off Point

Relative

Proportion

Allocation of

Joint Cost

$630,000

Resoline

8,000 pounds

8/10

$504,000

2/10

b. Relative-sales-value method:

Joint

Cost

Joint

Products

Sales Value at

Split-Off Point

Relative

Proportion

Allocation of

Joint Cost

$630,000

Resoline

$420,000

c. Net-realizable-value method:

Joint

Cost

Joint

Products

Sales

Value of

Final Product

Separable

Cost of

Processing

Net

Realizable

Value

Relative

Proportion

Allocation

of Joint

Cost

Resolite

$840,000

$120,000

$ 720,000

.60

$378,000

Chapter 17 – Allocation of Support Activity Costs and Joint Costs

CASE 17-36 (CONTINUED)

3. Decision analysis:

Incremental revenue per pound:

Sales price of Omega ……………………………………………………

$390

Sales price of Kryptite …………………………………………………..

285

Incremental revenue ……………………………………………………..

$105

Incremental cost per pound:*

Separable processing …………………………..………………………

$120

Packaging ……………………………………………………………………

Incremental cost …………………………………………………………..

138

Incremental loss per pound ………………………………………………

)