Ex. 17.10 a. Materials Inventory …….………………………………. 125,000

Accounts Payable ……………………………….

125,000

f.

Accounts Receivable …………..…………………………

600,000

Sales ………………………………………………. 600,000

To record December sales on account.

Cost of Goods Sold ………..………………………………

Selling and Administrative Expenses ……………….….

To record the purchase of direct materials on account.

Work in Process Inventory ………..………………………

Work in Process Inventory ……………………………….

Manufacturing Overhead …………………………………

Ex. 17.10 h.

Cost of Goods Sold …………..……………………………

10,000

(continued)

Manufacturing Overhead ………………………

10,000

Ex. 17.11 a. Actual manufacturing overhead ………………………………………… 200,000$

Debit balance in Manufacturing Overhead account ………………… (40,000)

Direct labor ………………………………………………………………..

e. Beginning Work in Process Inventory …………………………………. 50,000$

Total manufacturing costs charged to production ……………………. 590,000

Gross Profit ………………………………………………………………..

Ex. 17.12 a.

Beginning Materials Inventory ……………………………………….

16,000$

b.

Beginning Work in Process Inventory ……………………………….

34,000$

Direct materials used ………………………………………………….

104,000

Direct labor incurred …………………………………………………..

Manufacturing overhead applied ……………………………………..

Costs transferred to finished goods ………………………………….

Beginning Finished Goods Inventory ………………………………..

Cost of completed goods manufactured …………………………….

Cost of Goods Sold ……………………………………………………

Computations:

3

Cost of finished goods available for sale ……………………………..

450,000$

$500,000 sales × 75% = $375,000 cost of goods sold

Manufacturing overhead = $475,000 × 60% = $285,000

Materials purchased …………………………………………………..

Materials used …………………………………………………………

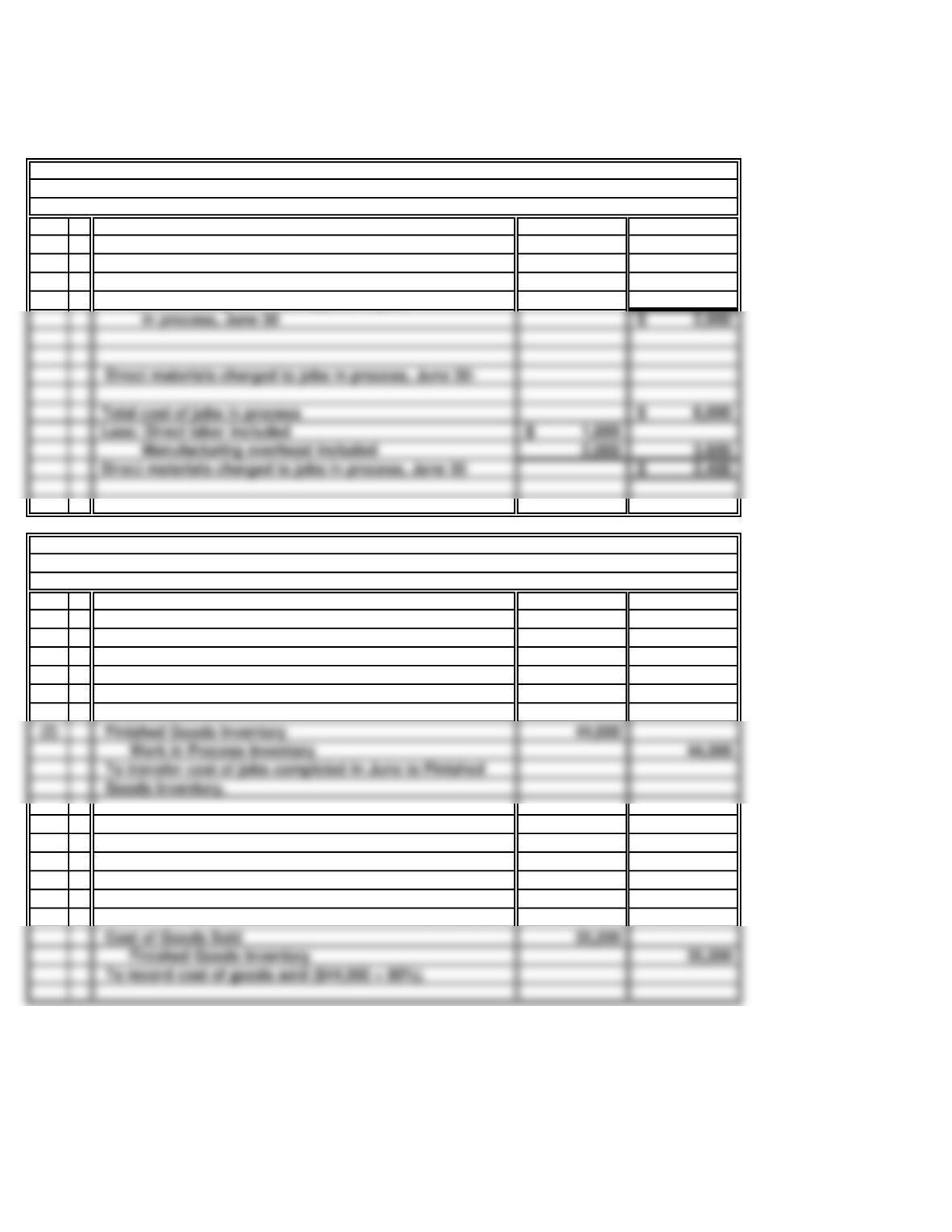

Ex. 17.13 a. Work in Process Inventory:

Job no. 1000 ……………………………………………………………

12,400$

Job no. 1001 …………………………………………………………….

15,000

b. Finished Goods Inventory:

Job no. 1002, February 28 …………………………………………….

2,000$

There is no Finished Goods Inventory balance on March 31.

c.

Sales …………………………………………………………………….

78,750$

Cost of Job no. 1000 ($12,400 + $6,800) ……………………………. 19,200

*

Cost of Job no. 1001 ($15,000 + $7,400 + $1,400) …………………..

Cost of Job no. 1002 …………………………………………………..

Gross Profit ……………………………………………………………..

Ex. 17.14 a.

Power-cost pool: Machine hours

Inspection-cost pool: Number of inspection hours

The most likely cost drivers for each cost pool are:

Work in Process Inventory, February 28 …………………………….

Job no. 1003 ……………………………………………………………

Job no. 1004 …………………………………………………………….

Work in Process Inventory, March 31 ……………………………….

% of total

Machine hours used for machine-made costumes …………

96,000 96%

Step 2:

Allocation of inspection-cost pool to each product line:

Step 1:

% of total

Costs assigned to machine-made costumes ($48,000 × 80%) ……..

Costs assigned to hand-made costumes ($48,000 × 20%) ……….

b.

Machine-

Made

Costumes

Hand-

Made

Costumes

$ 120,000 $ 96,000

30,720 1,280

38,400 9,600

$ 189,120 $ 106,880

$ 3.94 $ 6.68

Manufacturing cost per unit ……………………..

Power (from a)…………………………..

Inspection (from a) ……………………..

Number of units …………………………………..

Total manufacturing costs ……………………….

Allocate $32,000 in power-cost pool to each product line based on the

percentages computed in step 1.

Establish the percent of power-cost pool to be allocated to each product

line using the number of inspection hours as an activity base.

Direct labor and materials ………………………..

Manufacturing overhead costs:

Machine hours used for hand-made costumes………..

Ex. 17.14

(continued)

c.

Machine-

Made

Costumes

Hand-Made

Costumes

$ 240,000 $ 160,000

Ex. 17.15 a.

Direct materials ………………………………………………………….

$ 14,000

Direct labor ……………………………………………………………….

15,000

Maintenance ($40,000 × 60/600 machine hours) ……………………….

4,000

Materials handling ($20,000 × 20/400 moves) ……………………………

1,000

Setups ($10,000 × 4/100 setups) …………………………………………..

400

Quality control ($45,000 × 2/300 inspections) ……………………………..

300

Sales

$ 50,880 $ 53,120

Profit generated by product line

Direct labor and materials

Manufacturing overhead costs:

Number of units

SOLUTIONS TO PROBLEMS SET A

20 Minutes, Easy

PROBLEM 17.1A

JENSEN FENCES

a.

Manufacturing overhead charged to jobs in process,

June 30:

Direct labor charged to jobs in process, June 30 1,600$

Overhead application rate 125%

Manufacturing overhead applied to jobs

b.

(1) Work in Process Inventory 45,000

Materials Inventory 18,000

Direct Labor 12,000

Manufacturing Overhead 15,000

To record costs charged to jobs during June.

(2) Finished Goods Inventory 44,000

Work in Process Inventory 44,000

To transfer cost of jobs completed in June to Finished

Goods Inventory.

(3) Cash 50,000

Sales 50,000

To record cash sale of 80% of goods completed in June.

Cost of Goods Sold 35,200

Finished Goods Inventory 35,200

To record cost of goods sold ($44,000 × 80%).

General Journal

Direct materials charged to jobs in process, June 30:

Manufacturing overhead included 2,000 3,600

15 Minutes, Easy

PROBLEM 17.2A

O’SHAUGHNESSY MFG. CO.

General Journal

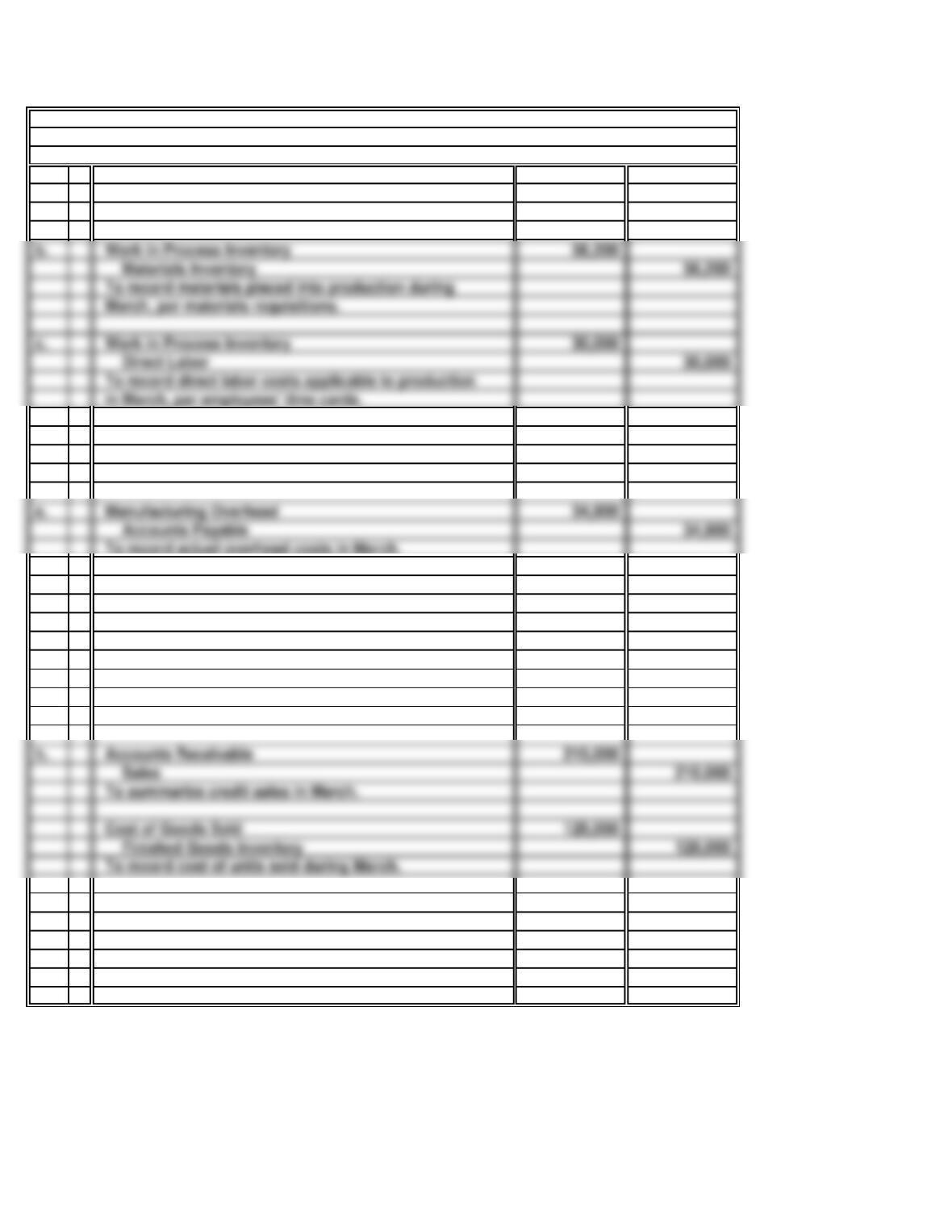

a. Materials Inventory 59,700

Accounts Payable 59,700

To record purchases of direct materials during March.

d. Direct Labor 26,300

Cash 26,300

To record direct labor payrolls paid in March.

e. Manufacturing Overhead 34,900

Accounts Payable 34,900

To record actual overhead costs in March.

f. Work in Process Inventory 36,000

Manufacturing Overhead 36,000

To record overhead applied to production during March

($18 per labor hour × 2,000 hours = $36,000).

g. Finished Goods Inventory 116,000

Work in Process Inventory 116,000

To record cost of completed jobs in March.

h. Accounts Receivable 210,000

To summarize credit sales in March.

Finished Goods Inventory 128,000

To record cost of units sold during March.

b. Work in Process Inventory 56,200

Materials Inventory 56,200

To record materials placed into production during

March, per materials requisitions.

c. Work in Process Inventory 30,000

Direct Labor 30,000

To record direct labor costs applicable to production

30 Minutes, Medium

PROBLEM 17.3A

GEORGIA WOODS, INC.

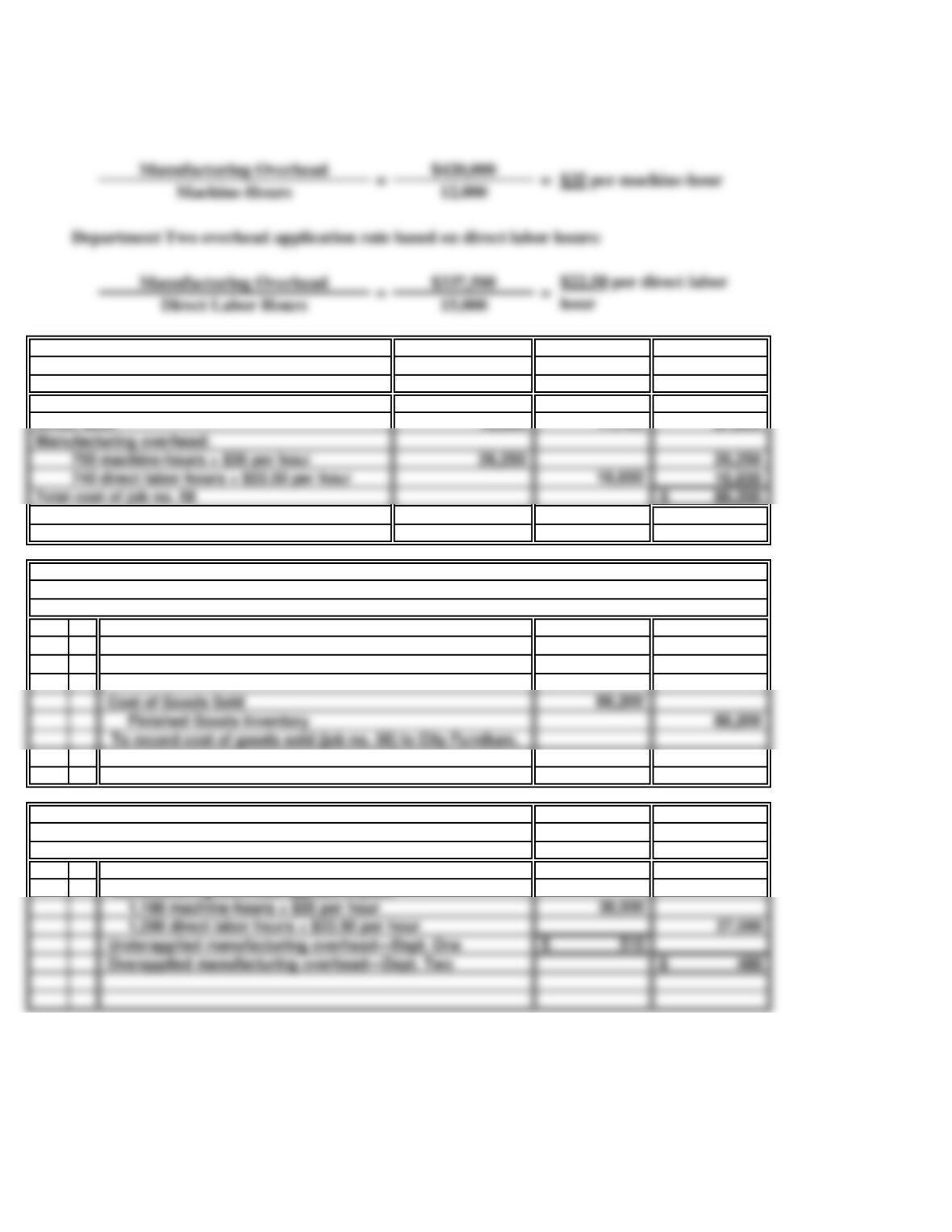

a. Department One overhead application rate based on machine-hours:

b. Job no. 58:

Dept. One Total

Direct materials 10,100$ 17,700$

Direct labor 16,500 27,600

Manufacturing overhead:

Total cost of job no. 58 88,200$

16,650

c.

Accounts Receivable (City Furniture)

Sales 147,000

To record revenue from sale to City Furniture.

Cost of Goods Sold

Finished Goods Inventory 88,200

To record cost of goods sold (job no. 58) to City Furniture.

88,200

d.

Dept. Two

Actual manufacturing overhead for January 26,540$

Manufacturing overhead applied to jobs:

General Journal

39,010$

Dept. One

11,100

147,000

Dept. Two

7,600$

30 Minutes, Medium

PROBLEM 17.4A

PRECISION INSTRUMENTS, INC.

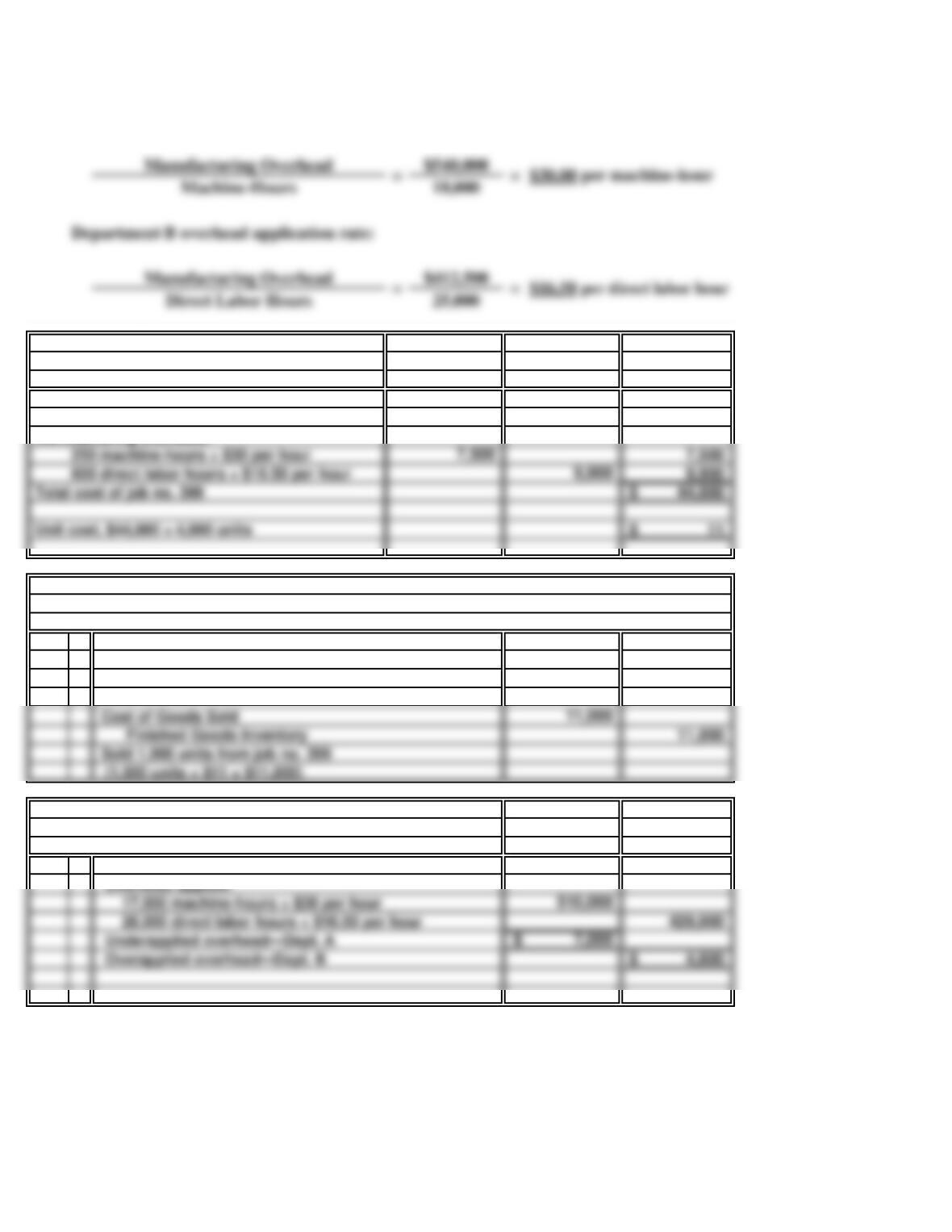

a. Department A overhead application rate:

b. Job no. 399:

Total

Direct materials 11,300$

Direct labor

15,300

Manufacturing overhead:

Total cost of job no. 399 44,000$

Unit cost, $44,000 ÷ 4,000 units 11$

9,900

7,500

c.

Accounts Receivable (SkiCraft Boats)

Sales 19,500

Sale on account to SkiCraft Boats.

Cost of Goods Sold

Finished Goods Inventory 11,000

Sold 1,000 units from job no. 399

(1,000 units × $11 = $11,000)

d.

Dept. B

Actual overhead for the year 424,400$

Overhead applied:

7,000$

Dept. A

517,000$

General Journal

19,500

Dept. A

Dept. B

6,800$

8,100

7,200

4,500$

35 Minutes, Medium

PROBLEM 17.5A

YE OLDE BUMP & GRIND, INC.

a. (1)

123,000$

10,000

12.30$

(2)

b. (1)

25.00$

75.00

61.50

Total cost of Job 1 161.50$

$3,800

3,000

2,460

Total cost of Job 2 9,260$

Direct materials used

Direct labor costs

Overhead applied (200 hr. × $12.30 per hr.)

(2)

25$

Total cost of Job 1 510$

3,800$

3,000

Overhead applied ($410 per job)

Direct materials used

Job 2:

Direct labor

Direct labor costs

Overhead application rate based on direct labor hours:

Estimated total overhead

Estimated direct labor hours

Overhead application rate per direct labor hour ($123,000 ÷ 10,000 hours)

Overhead application rate based upon number of repair jobs:

Job 1:

Overhead applied on a per-job basis:

Job 1:

Direct materials used

Direct labor costs

Overhead applied using direct labor hours:

Overhead applied (5 hr. × $12.30 per hr.)

Job 2:

Direct materials used

123,000$

Estimated number of repair jobs

Estimated total overhead

Overhead application rate per repair job ($123,000 ÷ 300 jobs)

PROBLEM 17.5A

YE OLDE BUMP & GRIND, INC. (concluded)

c.

Comments on the alternative overhead applications:

Allocating overhead based upon the number of jobs assumes that each repair job should be

charged with an equal amount ($410) of overhead. This allocation method ignores the fact

In this business, direct labor hours appear to be the major causal factor in the incurrence of

overhead costs. The use of indirect materials (sandpaper, welding materials, and metal

putty) is likely to be greater on jobs requiring more direct labor hours. As rent is a

percentage of gross revenue, large jobs cause the business to incur higher rent costs than do

30 Minutes, Medium

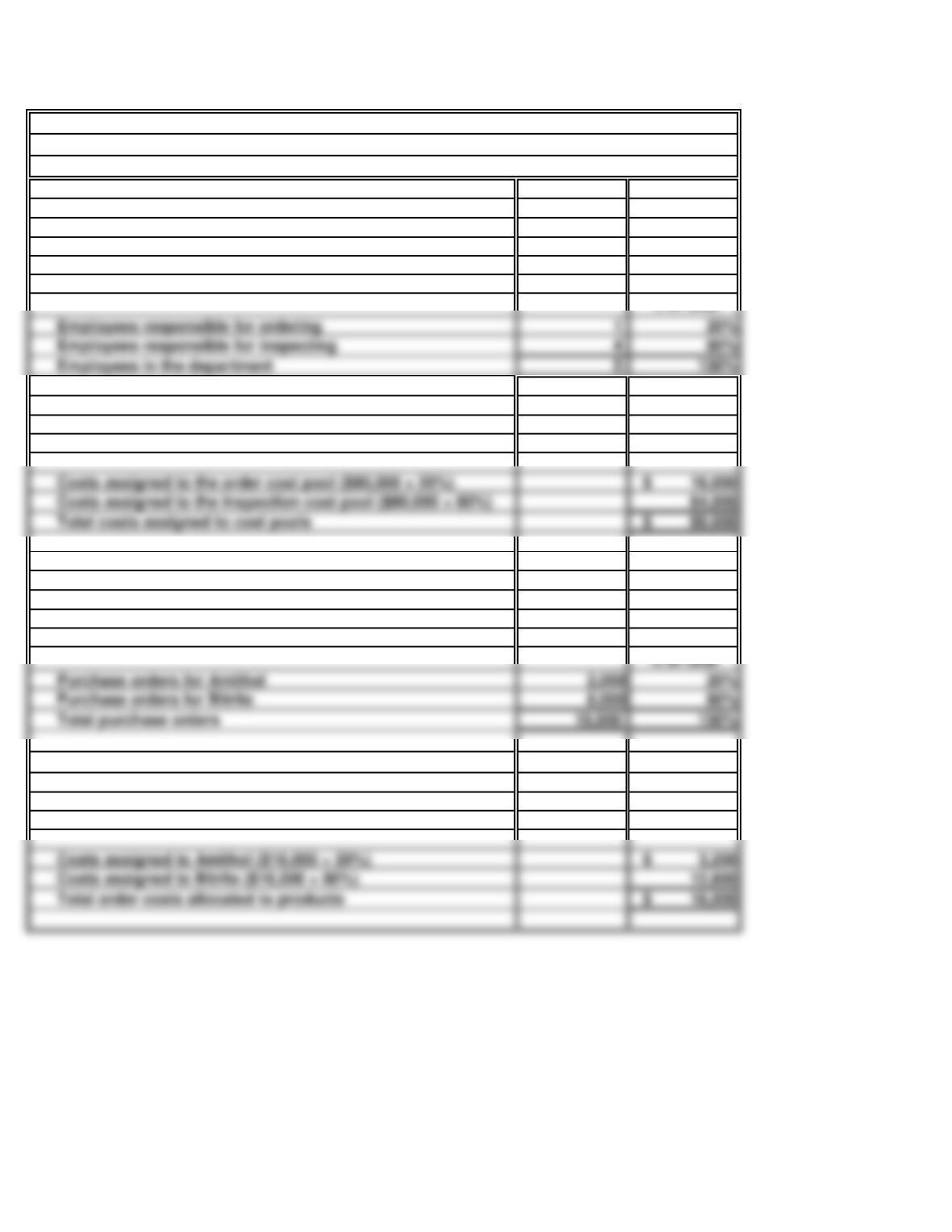

PROBLEM 17.6A

NORTON CHEMICAL COMPANY

a.

base.

% of total

Costs assigned to the order cost pool ($80,000 × 20%)

b.

Purchase orders for Amithol

Costs assigned to Amithol ($16,000 × 20%)

Assign total purchasing department costs of

Establish the percent of order cost pool to be

Allocate $16,000 in the order cost pool to each

$80,000 to each activity cost pool based on the

percentages computed in step 1.

allocated to each product line using the number

of purchase orders as an activity base.

Step 2:

Step 2:

product line based on the percentages computed

in step 1.

Assigning purchasing department costs to activity pools:

Step 1:

Establish the percent of purchasing department

costs to be assigned to each activity cost pool

using the number of employees as an activity

Step 1:

Order cost pool allocated to product lines:

Employees responsible for ordering

PROBLEM 17.6A

NORTON CHEMICAL COMPANY (concluded)

c.

Costs allocated to Bitrite ($64,000 × 25%)

Total inspection costs allocated to products

Costs allocated to Amithol ($64,000 × 75%)

d.

(1)

(2)

If possible, the company needs to consider making larger orders of Bitrite material on a

Step 2:

Norton might control manufacturing overhead costs incurred by the purchasing department

in two ways:

Allocate $64,000 in the inspection cost pool

to each product line based on the percentages

computed in step 1.

The company needs to work more closely with the supplier of materials used to make

of inspections as an activity base.

Inspection cost pool allocated to product lines:

Step 1:

Establish the percent of inspection cost pool to be

allocated to each product line using the number

Inspections for Bitrite

Total inspections

Inspections for Amithol

45 Minutes, Strong

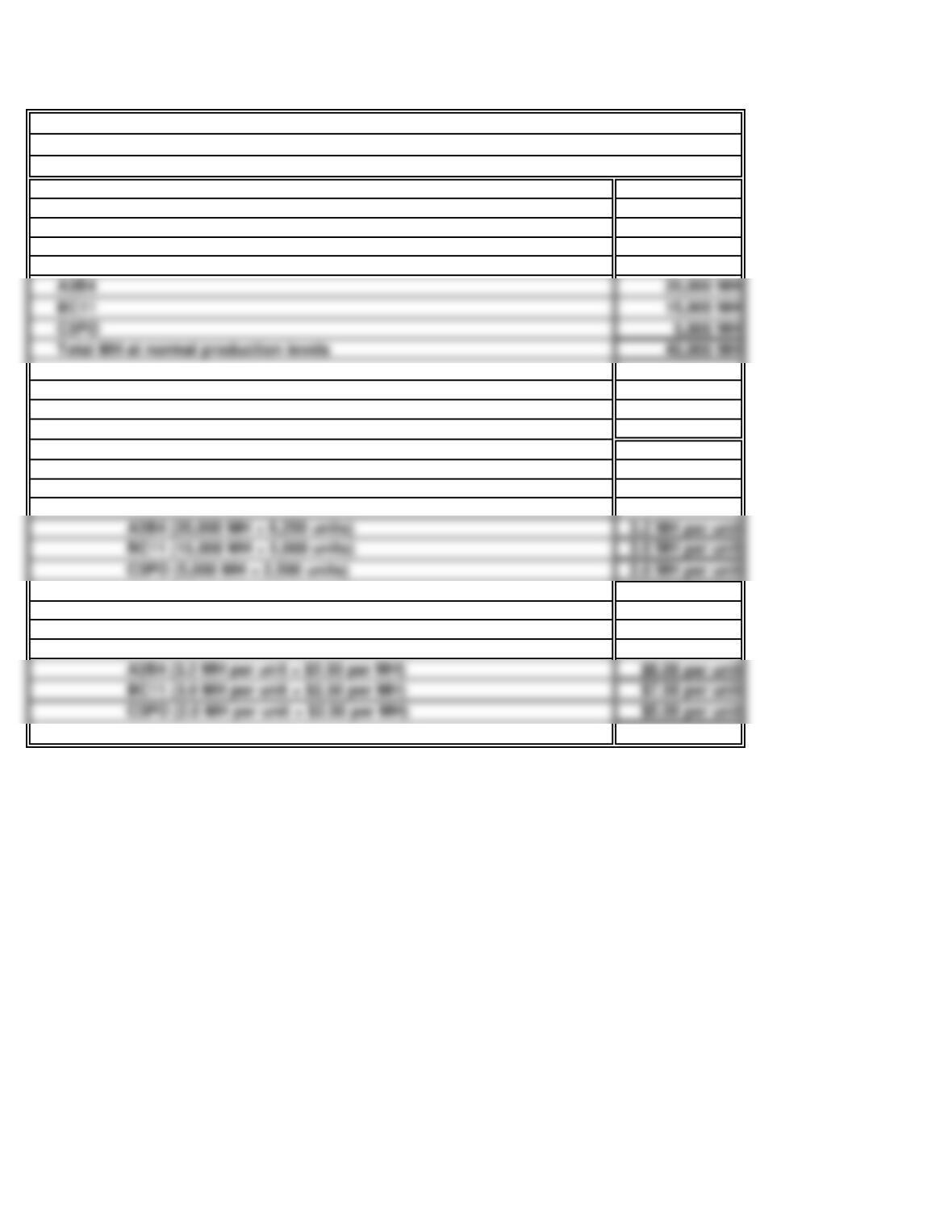

PROBLEM 17.7A

DIXON ROBOTICS

a.

Compute the overhead application rate per MH:

$2.50 per MH

Compute required machine hours on a per-unit basis:

A3B4 (20,000 MH ÷ 6,250 units)

A3B4 (3.2 MH per unit × $2.50 per MH)

Compute maintenance costs allocated to each product

Step 4:

on a per-unit basis:

Maintenance department costs allocated to each product line on a

per-unit basis using machine hours (MH):

Compute total MH at “normal” production levels:

Step 3:

Step 1:

Step 2:

Overhead application rate ($100,000 ÷ 40,000 MH)

Total MH at normal production levels

C3PO

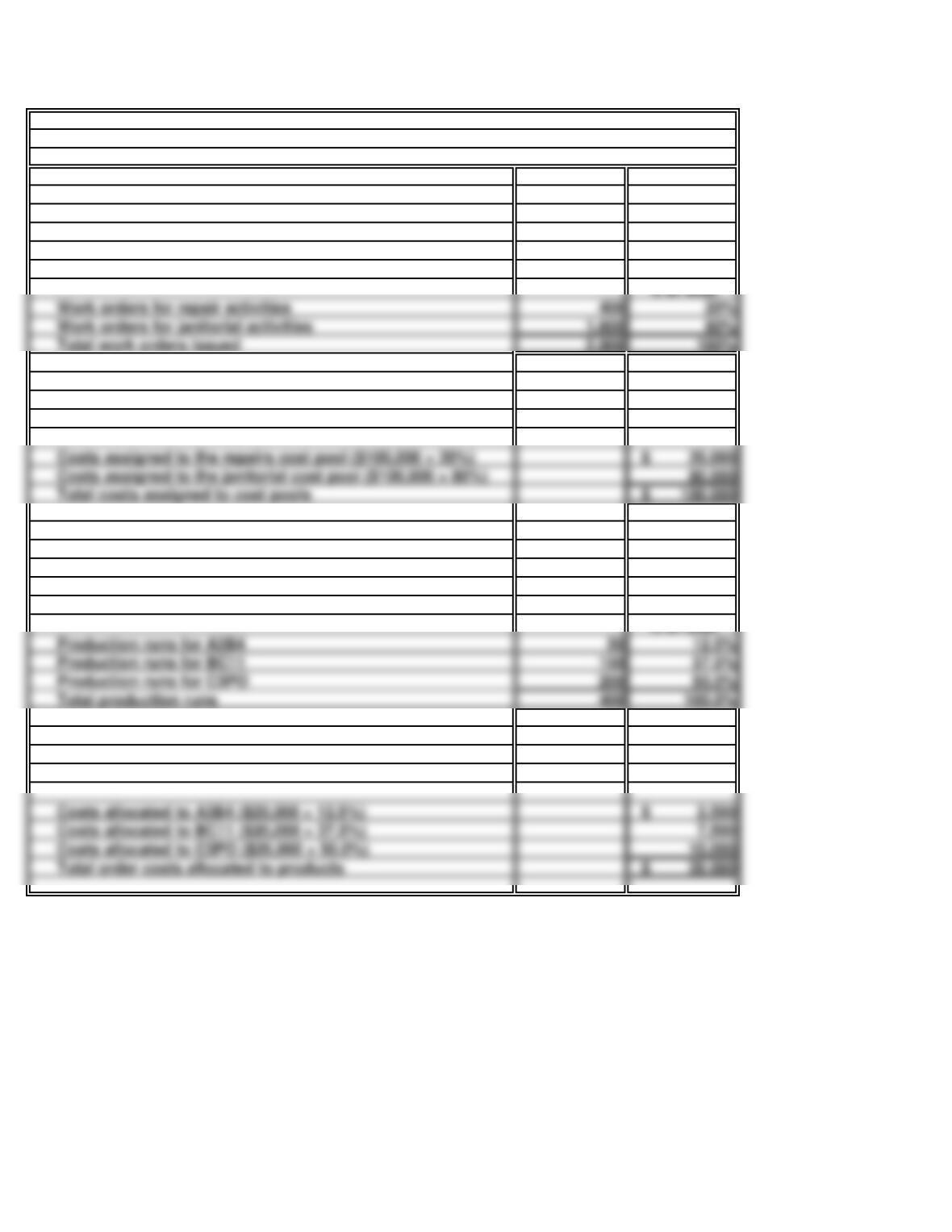

PROBLEM 17.7A

DIXON ROBOTICS (continued)

b.

Costs assigned to the janitorial cost pool ($100,000 × 80%)

Costs assigned to the repairs cost pool ($100,000 × 20%)

Total costs assigned to cost pools

% of total

Production runs for BC11

Production runs for C3PO

Total production runs

in step 1.

Total order costs allocated to products

Costs allocated to BC11 ($20,000 × 37.5%)

Costs allocated to A3B4 ($20,000 × 12.5%)

Costs allocated to C3PO ($20,000 × 50.0%)

Step 1:

Establish the percent of repairs cost pool to be

Assign total maintenance department costs of

$100,000 to each activity cost pool based on the

Step 2:

percentages computed in step 1.

product line based on the percentages computed

Step 2:

Allocate $20,000 in the repairs cost pool to each

allocated to each product line using the

Assigning maintenance department costs to activity pools:

Step 1:

Allocating repairs cost pool to product lines:

number of production runs as an activity base.

Establish the percent of maintenance department

costs to be assigned to each activity cost pool

using the number of work orders as an

activity base.

% of total

Work orders for janitorial activities

Work orders for repair activities

Total work orders issued

PROBLEM 17.7A

DIXON ROBOTICS (concluded)

in step 1.

Costs allocated to C3PO ($80,000 × 62.5%)

Total order costs allocated to products

Costs allocated to A3B4 ($80,000 × 12.5%)

Costs allocated to BC11 ($80,000 × 25.0%)

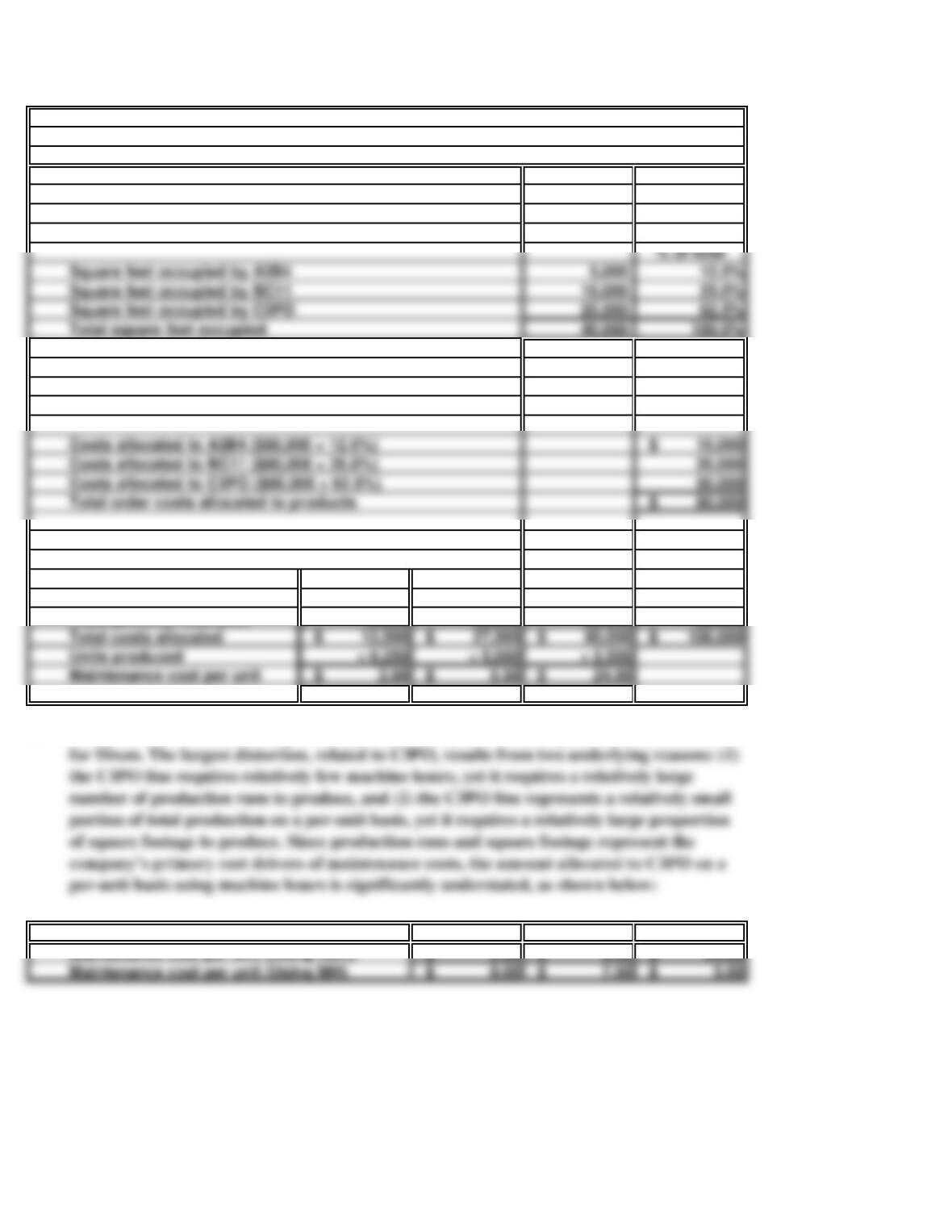

A3B4 BC11 C3PO Total

$ 2,500 $ 7,500 $ 10,000 $ 20,000

10,000 20,000 50,000 80,000

$ 12,500 $ 27,500 $ 60,000 $ 100,000

$ 2.00 $ 5.50 $ 24.00

Maintenance cost per unit

Total costs allocated

Units produced

c.

A3B4 BC11 C3PO

Maintenance cost per unit (Using ABC)

Maintenance cost per unit (Using MH)

Allocating janitorial cost pool to product lines:

Establish the percent of janitorial cost pool to be

allocated to each product line using square

footage occupied as an activity base.

Step 1:

From janitorial cost pool

Allocate $80,000 in the janitorial cost pool to each

product line based on the percentages computed

Determining maintenance costs per unit using ABC:

Using machine hours as a single activity base is likely to result in significant cost distortions

Step 2:

From repairs cost pool

Square feet occupied by BC11

Square feet occupied by A3B4

Total square feet occupied

Square feet occupied by C3PO

45 Minutes, Strong

PROBLEM 17.8A

HEALTHY HOUND, INC.

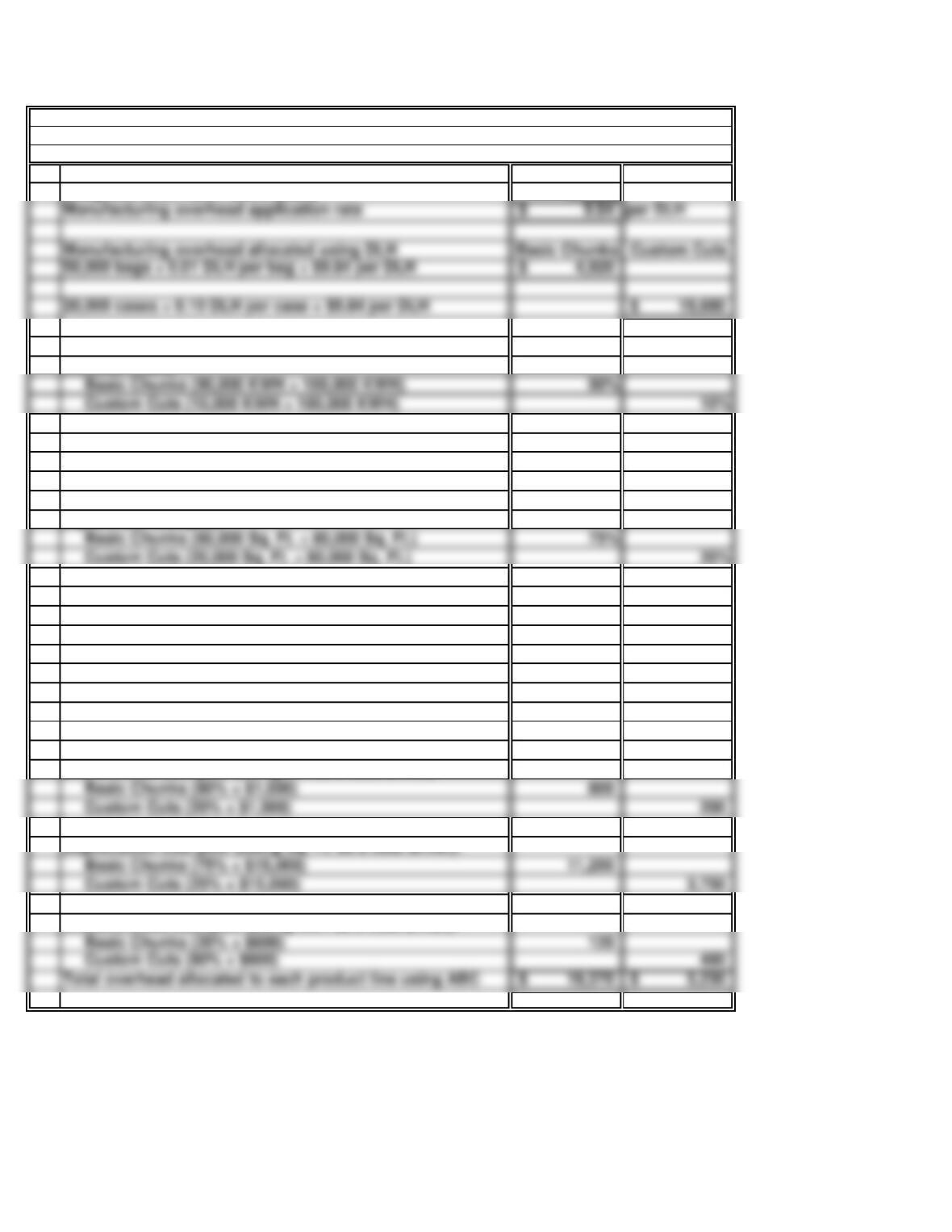

a. Budgeted manufacturing overhead 24,600$

Budgeted direct labor hours (DLH) ÷ 2,500

b. Percent of cost driver assigned to each product line Basic Chunks Custom Cuts

Kilowatt hours:

Custom Cuts (10,000 KWH ÷ 100,000 KWH) 10%

Machine hours:

Basic Chunks (160 MH ÷ 200 MH) 80%

Custom Cuts (40 MH ÷ 200 MH) 20%

Square feet occupied:

Basic Chunks (60,000 Sq. Ft. ÷ 80,000 Sq. Ft.) 75%

Custom Cuts (20,000 Sq. Ft. ÷ 80,000 Sq. Ft.) 25%

Direct labor hours:

Basic Chunks (500 DLH ÷ 2,500 DLH) 20%

Custom Cuts (2,000 DLH ÷ 2,500 DLH) 80%

Manufacturing overhead allocated using ABC Basic Chunks Custom Cuts

Utilities cost pool (using KWH as a cost driver):

Basic Chunks (90% × $8,000) 7,200$

Custom Cuts (10% × $8,000) 800$

Maintenance cost pool (using MH as a cost driver):

Basic Chunks (80% × $1,000) 800

Custom Cuts (20% × $1,000) 200

Depreciation cost pool (using Sq. Ft. as a cost driver):

Basic Chunks (75% × $15,000) 11,250

Custom Cuts (25% × $15,000) 3,750

Miscellaneous cost pool (using DLH as a cost driver):

Basic Chunks (20% × $600) 120

Custom Cuts (80% × $600) 480

Total overhead allocated to each product line using ABC 19,370$ 5,230$

Manufacturing overhead application rate 9.84$ per DLH

Manufacturing overhead allocated using DLH Basic Chunks Custom Cuts

PROBLEM 17.8A

HEALTHY HOUND, INC. (concluded)

c. Total manufacturing costs allocated to each product line Basic Chunks Custom Cuts

Direct Labor:

Basic Chunks (50,000 bags × $12 per DLH × 0.01 DLH) 6,000$

Custom Cuts (20,000 cases × $12 per DLH × 0.10 DLH) 24,000$

d.

e.

The Custom Cuts product line is very labor intensive in comparison to the Basic Chunks

product line. Thus, the company’s current practice of using direct labor hours to allocate

The benefits the company would achieve by implementing an activity-based costing system

Direct Materials:

Basic Chunks (50,000 bags × $2 per bag) 100,000

Custom Cuts (20,000 cases × $4 per case) 80,000

Manufacturing Overhead (allocate using ABC):