An asterisk (*) will appear to the right of an incorrect entry. The essay answer will not be graded.

Enter a zero in cells you would otherwise leave blank.

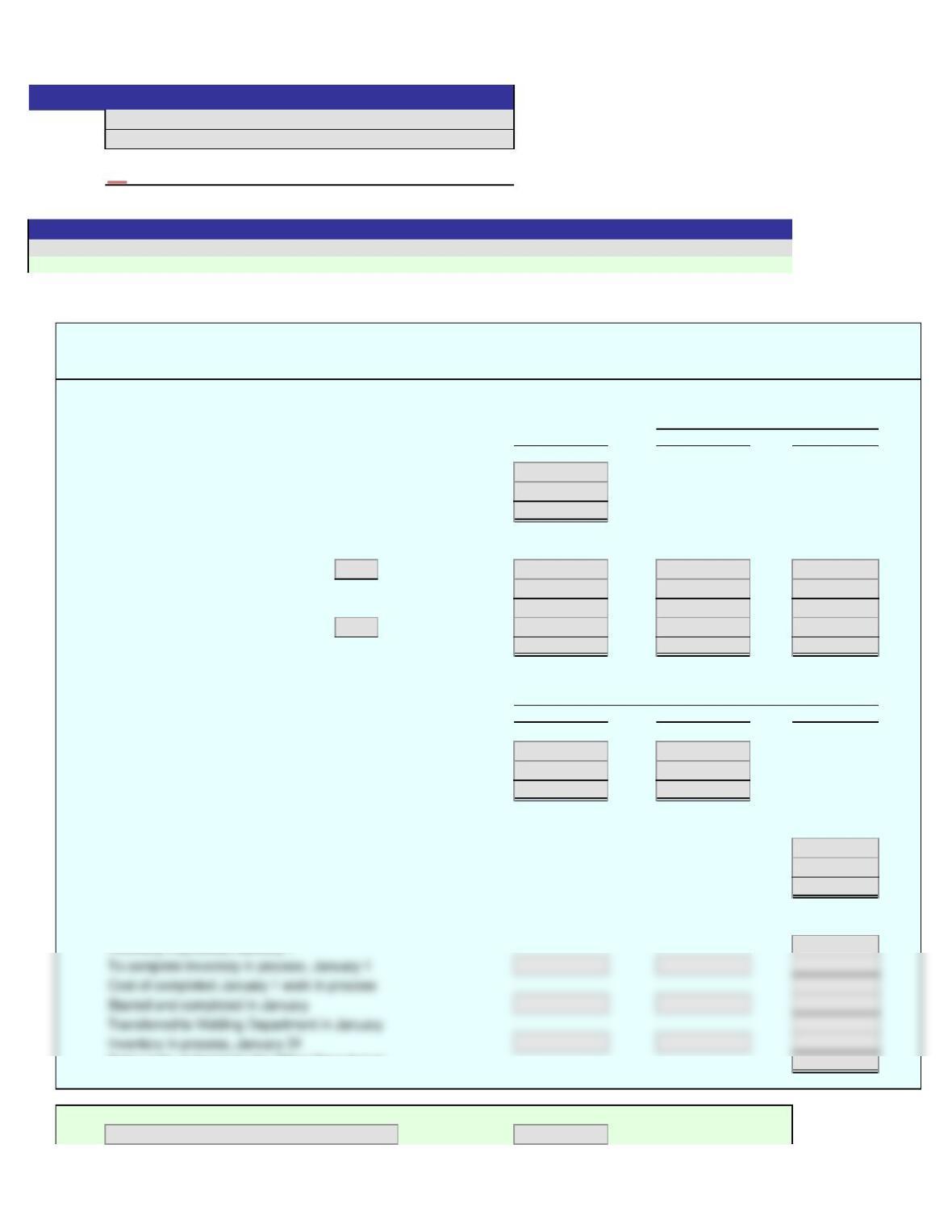

1.

UNITS

Whole Units Direct Materials Conversion

Units charged to production:

Inventory in process, January 1

Received from Reaction Department

Total units accounted for by the Filling Department

Units to be assigned cost:

Inventory in process, January 1 ( complete)

Started and completed in January

Transferred to finished goods in January

Inventory in process, January 31 ( complete)

Total units to be assigned cost

COSTS

Direct Materials Conversion Total

Costs per equivalent unit:

Total costs for January in Filling Department

Total equivalent units

Cost per equivalent unit

Costs assigned to production:

Inventory in process, January 1

Costs incurred in January

Total costs accounted for by the Filling Department

Costs allocated to completed and partially completed units:

Total costs assigned by the Filling Department

2.

Problem 17(3)-3B

Name:

Section:

Equivalent Units

Costs

0%

[Key code here]

Answers are entered in the cells with gray backgrounds.

Score:

Key Code:

Instructions

Cells with non-gray backgrounds are protected and cannot be edited.

Dover Chemical Company

Cost of Production Report – Filling Department

For the Month Ended January 31

3.

Direct Materials Conversion

Cost per equivalent unit:

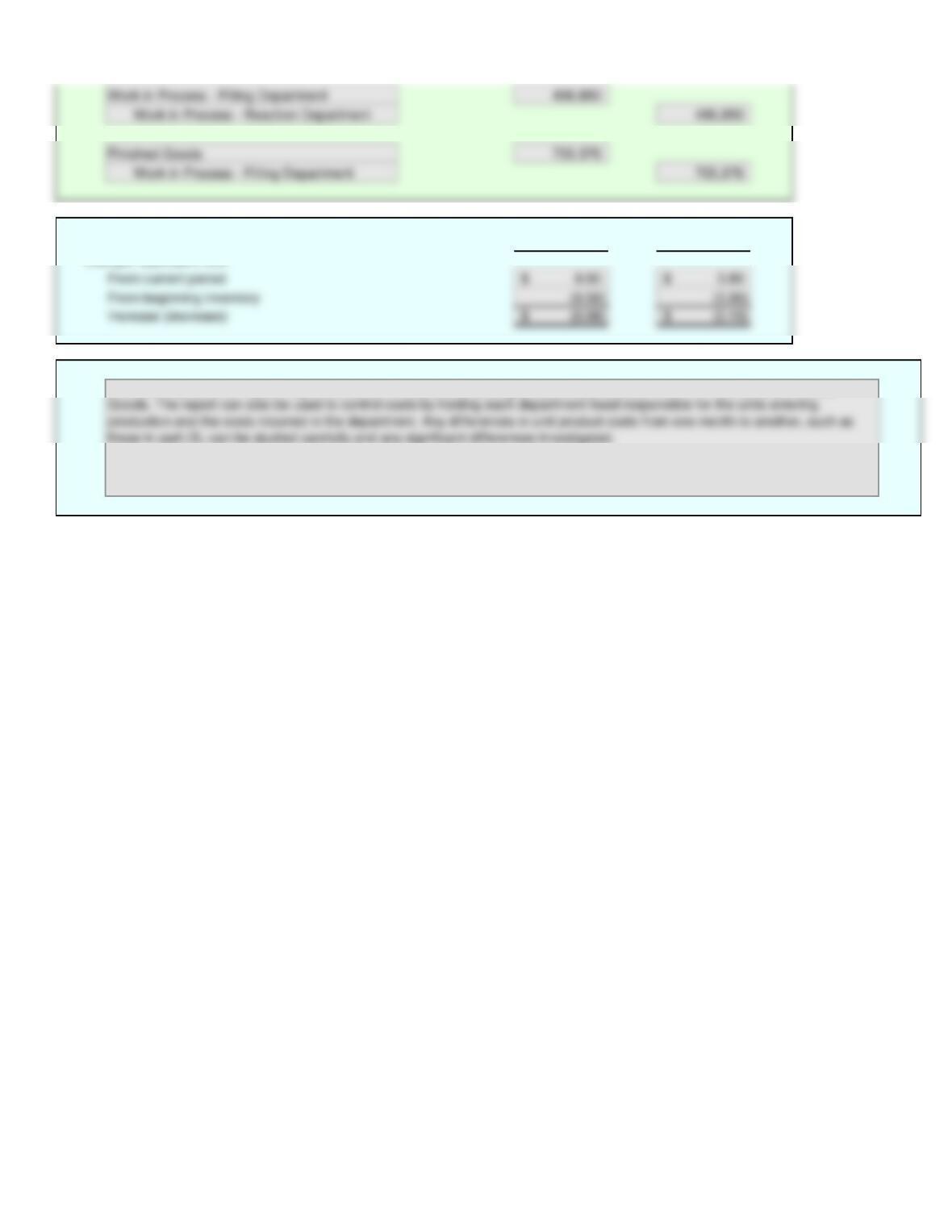

From current period

From beginning inventory

Increase (decrease)

An asterisk (*) will appear to the right of an incorrect entry. The essay answer will not be graded.

Enter a zero in cells you would otherwise leave blank.

1.

UNITS

Whole Units Direct Materials Conversion

COSTS

Direct Materials Conversion Total

2.

Dover Chemical Company

Cost of Production Report – Filling Department

For the Month Ended January 31

Problem 17(3)-3B

Name:

Solution

Section:

Score:

Instructions

Cells with non-gray backgrounds are protected and cannot be edited.

Answers are entered in the cells with gray backgrounds.

ON

Equivalent Units

Costs

3.

Direct Materials Conversion

4.

The cost of production report may be used as the basis for allocating product costs between Work in Process and Finished