Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

CHAPTER 17

UNDERSTANDING THE ISSUES

1. The new reporting model adopts full accrual

accounting for the government-wide statements

for both governmental and business-type activi-

2. Both fund and government-wide financial state-

ments are required in the new model. Fund

statements include (1) the governmental fund

balance sheet and statement of revenues,

expenditures, and changes in fund balances; (2)

the proprietary fund statement of net position,

statement of revenues, expenses, and changes

in net position, and statement of cash flows; and

(3) the fiduciary fund statement of net position

and statement of changes in net position. The

3. Major funds are those funds that management

chooses to disclose in a separate column in the

fund statements either due to their relative size

or because they are of particular interest or con-

vey unique information. The general fund is al-

ways considered a major fund. Funds whose

assets and deferred outflows, liabilities and de-

4. The purpose of the MD&A is to give a concise

overview and analysis of the information in the

government’s financial statements. Required

tions, including impact of important economic

factors; an analysis of individual fund financial

information, including the reasons for significant

changes in fund balances (or net position) and

whether limitations significantly affect the future

use of the resources; an analysis of significant

variations between original and final budget

amounts and between final budget amounts and

actual budget results for the general fund; a de-

original as well as amended budget must be in-

cluded with a comparison of actual results

reported on a budgetary basis.

6. Interfund transactions are recorded separately

from other transactions. Interfund payables and

receivables are eliminated when government-

Ch. 17—Exercises 17–2

EXERCISES

EXERCISE 17-1

Note to Instructor: The 2013 CAFR of the city of Milwaukee needs to be examined to answer

these questions. The general fund is always considered a major fund. Every other governmental

fund from the combining statements must be examined to determine if it is at least 10% of all

the governmental funds and at least 5% of all government and enterprise funds combined.

EXERCISE 17-2

EXERCISE 17-3

(1) Governmental Fund Statement of Revenues, Expenditures, and Changes in Fund Balances

General

Fund

Special

Revenue

Fund C

Capital

Projects

Fund A

Capital

Projects

Fund B

Total

Nonmajor

Funds

Total

Government

Funds

(2) Proprietary Fund Statement of Revenues, Expenses, and Changes in Net Position

Total Enterprise Funds

Enterprise

Fund D

Enterprise

Fund F

Other

Enterprise

Funds

Totals

Total Internal

Service Funds

EXERCISE 17-4

(2) c Both expenditures for debt principal and capital outlays must be eliminated and

converted to expenses. In addition, depreciation expense must be recorded.

(3) a The government-wide statements report internal service funds among the govern-

(4) a All capital assets, including infrastructure, must be included in the government-wide

(5) d The government-wide statements do not include fiduciary funds but do include

(6) c An up-to-date inventory and a current condition assessment are necessary for the

(7) c Revenue that is specific to a particular activity, function, or program, such as fees

(8) d The government-wide statements report internal service funds among the govern-

(9) c The reconciliation is necessary for the governmental funds to convert the modified

accrual fund information to the full accrual government-wide governmental activities

(10) b The statement of cash flows is part of the proprietary fund financial statements but

is not part of the government-wide statements.

EXERCISE 17-5

To convert from the governmental fund balance sheet to the government-wide statement of net

position, the following adjustments are necessary:

• Add general capital assets, including infrastructure, net of accumulated depreciation.

• Add general long-term liabilities.

EXERCISE 17-6

(2) c In the fund statements, proprietary funds are included in the proprietary fund bal-

ance sheet; statement of revenues, expenses, and changes in net position; and

(3) d Account groups are not reported in either the fund or government-wide statements.

(4) b Total columns are not required for combining statements but are quite commonly

(5) a A statement of cash flows is required for all enterprise funds.

(6) d Construction in progress will be reported in the government-wide statements as a

capital asset. Capital assets are not reported in the fund statements.

EXERCISE 17-7

The new reporting model requires that all capital assets, including infrastructure assets, be

included on the financial statements. In addition, these assets must be depreciated. (The rules

are effective three years after the requirement for implementing the new reporting model.) Gov-

ernments may adopt a “modified approach” to depreciation if they have an up-to-date inventory

of their infrastructure assets and have a current condition assessment. As long as the assets

17–5 Ch. 17—Problems

PROBLEMS

PROBLEM 17-1

(1) b The statement of activities is presented using a net program expense format where

(2) d Special purpose governments that provide business-type activities only are permit-

ted to report the financial statements required for enterprise funds. Since these are

(3) d The government-wide financial statements include a statement of net position and a

statement of activities with an economic resources measurement focus and are

(4) b Budgetary comparison may be included as a separate statement or schedule. The

(5) c Combining statements are used to add together nonmajor funds of the same type in

(6) a The three major sections of the comprehensive annual financial statement are the

(7) c The government-wide financial statements include a statement of net position and a

statement of activities with an economic resources measurement focus and are

(8) a The new reporting model requires that all capital assets, including infrastructure, be

recorded and depreciated. Governments have the option of choosing a modified

(9) d Major funds are those funds that management chooses to disclose in a separate

column in the fund statements either due to their relative size or because they are of

Problem 17-1, Concluded

(10) b The Office of Management and Budget (OMB) sets standards for audits of reci-

(11) c OMB Circular A-133 applies to state, local, and not-for-profit organizations that

(12) a The expenditures threshold for having an A-133 single audit (for fiscal years begin-

ning on or after January 1st, 2015) is $750,000.

PROBLEM 17-2

PROBLEM 17-3

The authority is not a component unit but should be disclosed in the notes as a related organi-

zation. The city appoints the authority’s separate governing board but is not financially account-

PROBLEM 17-4

(1) The school district is not legally separate, so it is part of the city and not a component unit.

(2) The authority is legally separate, the city has financial accountability, and so it is a compo-

(3) The mayor appoints all members of the board so it can be assumed that there is control

(5) The water utility is a joint venture and not a component unit. The city’s equity interest will be

presented in the government-wide statements as an asset.

17–7 Ch. 17—Problems

PROBLEM 17-5

The financial reporting entity of a government includes the primary government and all its com-

ponent units. An example of a primary government is a city. An example of a component unit is

PROBLEM 17-6

(1) Budgetary Fund Balance ............................................................ 295,000

Estimated Other Financing Uses ............................................... 15,000

(2) Statement of Revenues, Expenditures, and Changes in Fund Balances

For the Year Ended December 31, 2019

Revenues ..................................................................................................... $ 41,600

Expenditures ................................................................................................ (586,600)

Excess of revenue over expenditures .......................................................... $ (545,000)

Other financing sources ............................................................................... 800,000

(3) Balance Sheet as of December 31, 2019

Cash .................................. $110,000 Contracts payable ...................... $ 110,000

Investments ....................... 250,000 Fund balance—assigned ........... $ 80,000

PROBLEM 17-7

Government-

Fund

Debit Credit Wide

Revenues ..................................... (41,600) (41,600)

Other Financing Sources ............. (800,000) (2) 800,000 0

Expenditures ................................ 586,600 586,600 (1) 0

PROBLEM 17-8

City of Lucas

Statement of Net Position

June 30, 2019

Governmental Business-Type Total Primary

Activities

Activities Government

Assets:

Cash and cash equivalents .................... $ 280,000 $ 75,000 $ 355,000

Receivables ............................................ 36,000 145,000 181,000

Inventories .............................................. 0 56,000 56,000

Capital assets (net) ................................. 1,500,000 1,100,000 2,600,000

17–9 Ch. 17—Problems

PROBLEM 17-9

City of Rose

Statement of Activities

As of June 30, 2019

Program Revenues Net Revenue Change in Net Position

Charges Business-

for Operating Capital Governmental Type

Expenses Services Grants Grants Activities Activities Total

Governmental activities:

General government .................. $ 1,300,000 $ 100,000 $ 0 $(1,200,000) $ 0 $(1,200,000)

Total governmental activities .. $ 3,700,000 $ 575,000 $220,000 $(2,905,000) $ 0 $(2,905,000)

Business-type activities:

Water and sewer system ............ $1,500,000 $ 1,800,000 $ 0 $ 0 $ 300,000 $ 300,000

Parking system ........................... 45,000 40,000 0 0 (5,000) (5,000)

Total business-type activities .. $1,545,000 $ 1,840,000 $ 0 $ 0 $ 295,000 $ 295,000

PROBLEM 17-10

(1) The basic financial statements in the new reporting model include both government-wide

financial statements and fund financial statements. The government-wide financial

statement presents the financial picture of Minneapolis from an economic resources

measurement focus using the full accrual basis of accounting. Governmental and business-

(2) The management’s discussion and analysis is a requirement in the new reporting model. It

provides an overview of the city’s financial activities for the fiscal year and is subject to audit.

The MD&A provides an objective and easily readable analysis of the government’s financial

(3) Budgetary comparison information is reported as required supplementary information. A de-

(4) Minneapolis has four major governmental funds: Community Planning and Economic Devel-

opment, Convention Center, Permanent Improvement, and Special Assessment.

Minneapolis uses the GASB Statement No. 34 criteria for determining major funds—meeting

17–11 Ch. 17—Problems

Problem 17-10, Concluded

(5) Minneapolis capitalizes and depreciates (or amortizes) all capital assets (including infra-

PROBLEM 17-11

(1) The measurement focus for governmental funds is financial resources, and the basis of ac-

counting for governmental funds statements is modified accrual. The proprietary and fidu-

(2) Differences between fund financial statements and government-wide statements:

Fund Statements Government-Wide Statements

Component units Only blended component units Both blended and discretely

are included. presented component units

are included.

(3) The three net asset categories found in the statement of net position:

Invested in capital assets, net of related debt Fixed assets of the government less all fixed

asset-related debt (current and noncurrent)

PROBLEM 17-12

(1) Major programs for the audit will include Programs 1, and 3. These three programs are iden-

tified due to their size (over $750,000 in expenditures) and risk assessment (not classified

as low risk).

PROBLEM 17-13

Packer City

Reconciliation Schedules

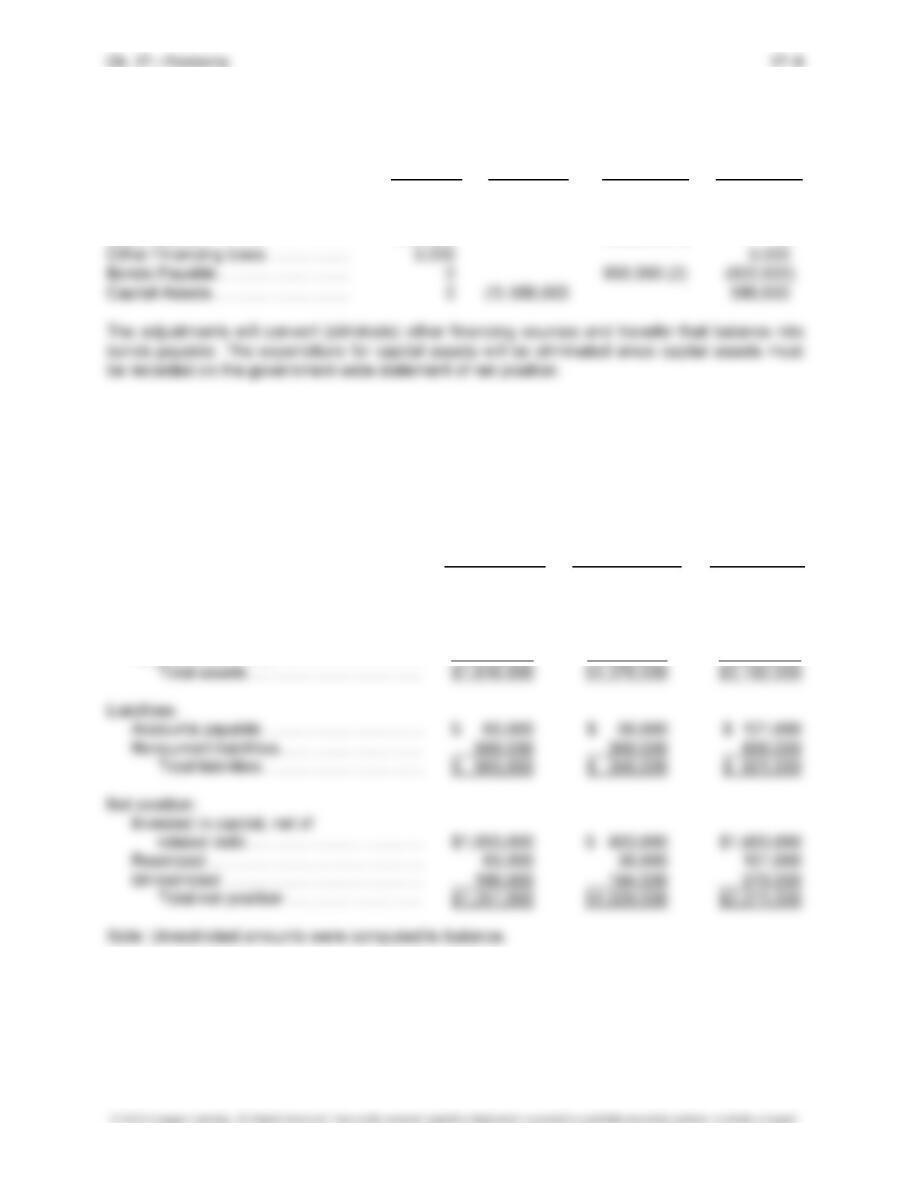

(1) Balance Sheet to Statement of Net Position

Total fund balances for governmental funds ....... $ 15,462,380

Add:

Land .............................................................. $ 3,871,054

Construction in progress ............................... 748,411

Land improvements ....................................... 1,880,024

Buildings........................................................ 10,844,461

Machinery and equipment ............................. 5,968,095

17–13 Ch. 17—Problems

Problem 17-13, Continued

(2) Statement of Revenues, Expenditures, and Changes

in Fund Balances to Statement of Activities

Net change in fund balances—total governmental funds $ (1,326,268)

Changes in capital assets:

Increase in total capital assets* ..................... $ 4,157,074

Book value, assets sold ................................ (76,506)

Depreciation .................................................. (1,291,691) 2,788,877

Principal payments received ......................... (189,417)

Amortization of bond issue cost .................... (12,777)

Add to deferred debits ................................... 6,389

Problem 17-13, Continued

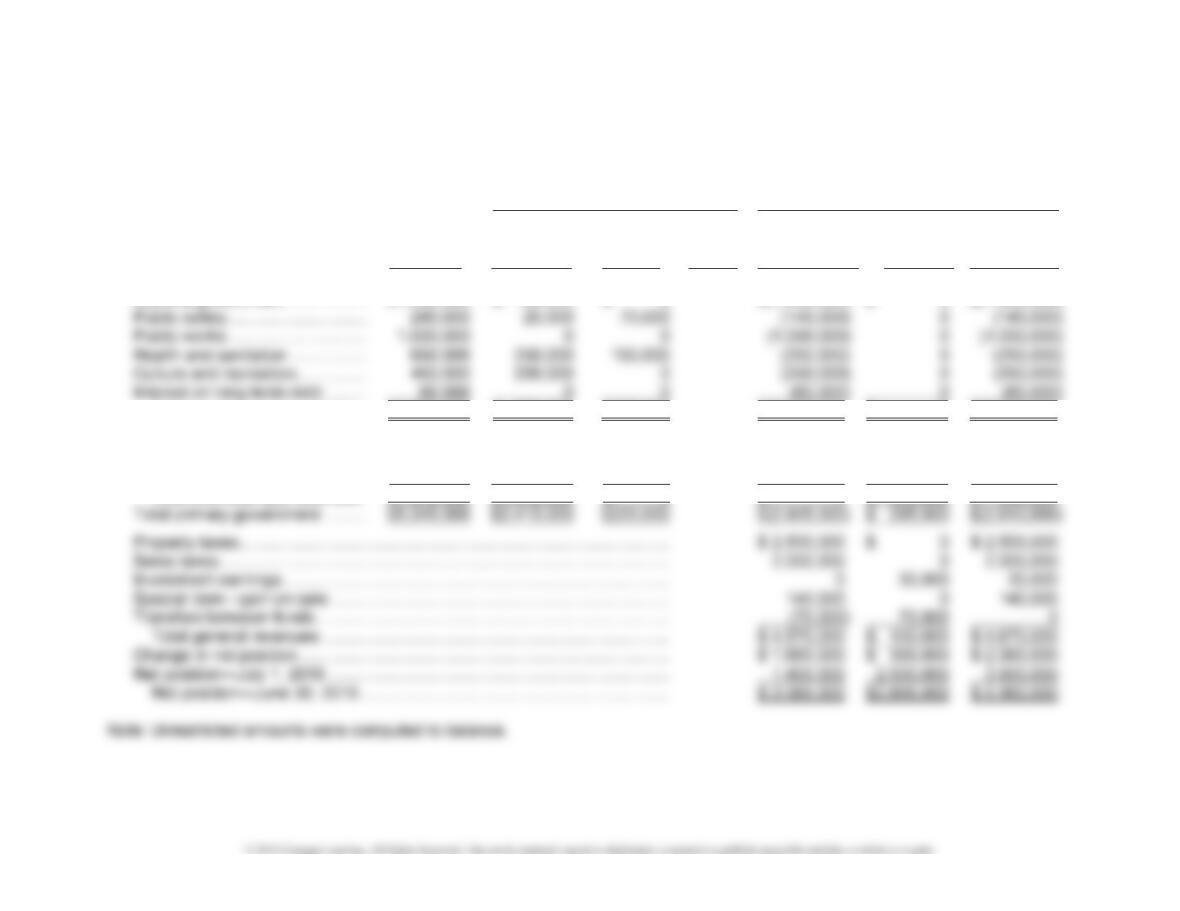

(3) Packer City

Statement of Net Position

Government Activities

December 31, 2019

Governmental

Funds Adjustments Total

Assets:

Cash .............................................................. $16,445,619 $16,445,619

Accounts receivable ...................................... 604,403 604,403

Deferred bond issue cost .............................. 104,357 104,357

Land .............................................................. 3,871,054 3,871,054

Construction in progress ............................... 748,411 748,411

Land improvements ....................................... 1,880,024 1,880,024

Buildings........................................................ 10,844,461 10,844,461

Accrued interest payable ............................... $ 133,627 133,627

General obligation debt ................................. 23,403,178 23,403,178

Community development bonds .................... 2,000,000 2,000,000

Compensated absences ............................... 2,611,738 2,611,738

Total liabilities................................................ $ 1,507,679 $28,148,543 $29,656,222

Problem 17-13, Continued

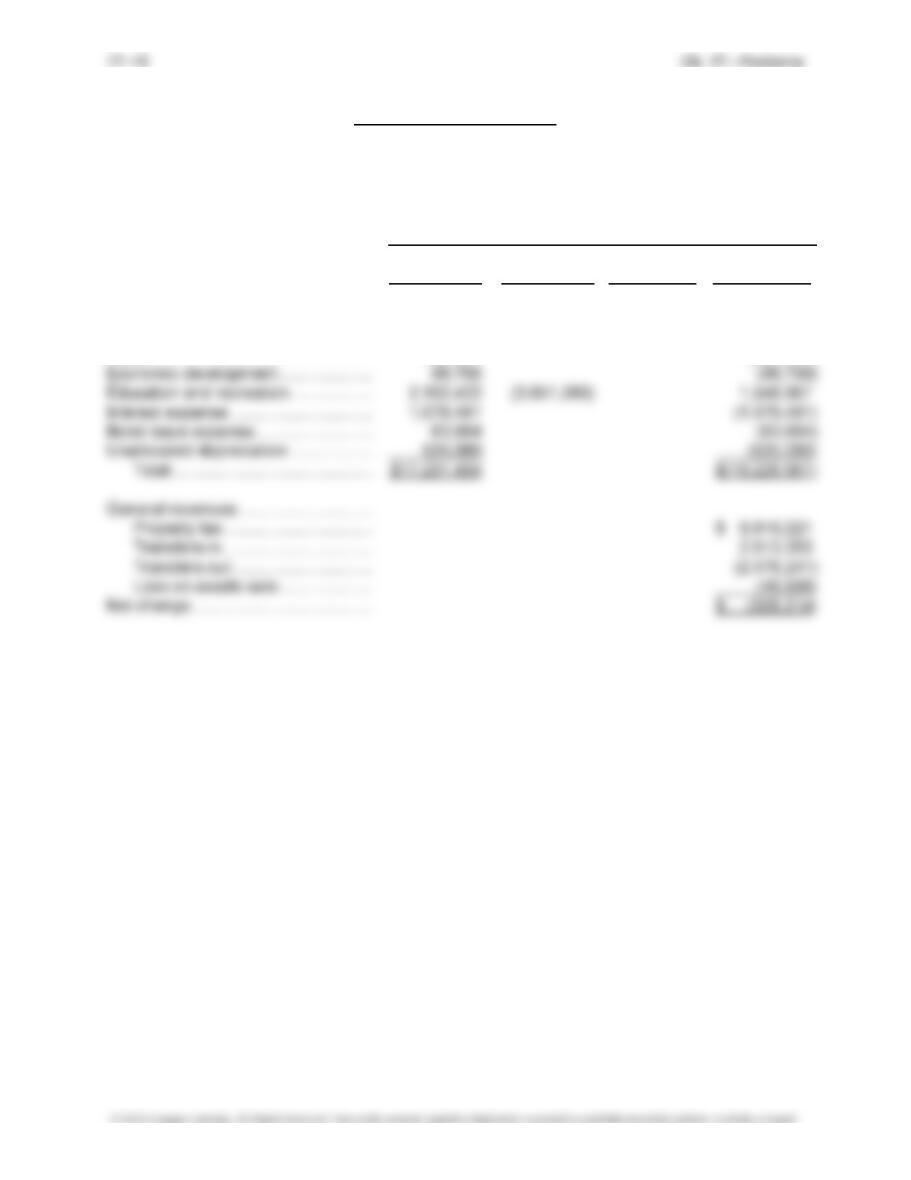

(4) Packer City

Statement of Activities

December 31, 2019

Governmental Funds

Fines, Fees, Operating Net (Expense)

Expenses

Charges Grants Revenue

General government ......................... $ 3,249,306 $ (456,271) $(2,583,307) $ (209,728)

Protection .......................................... 6,161,176 (154,270) (6,006,906)

Highway ............................................ 3,102,827 (159,636) (2,943,191)

Health ................................................ 863,461 (863,461)

Problem 17-13, Concluded

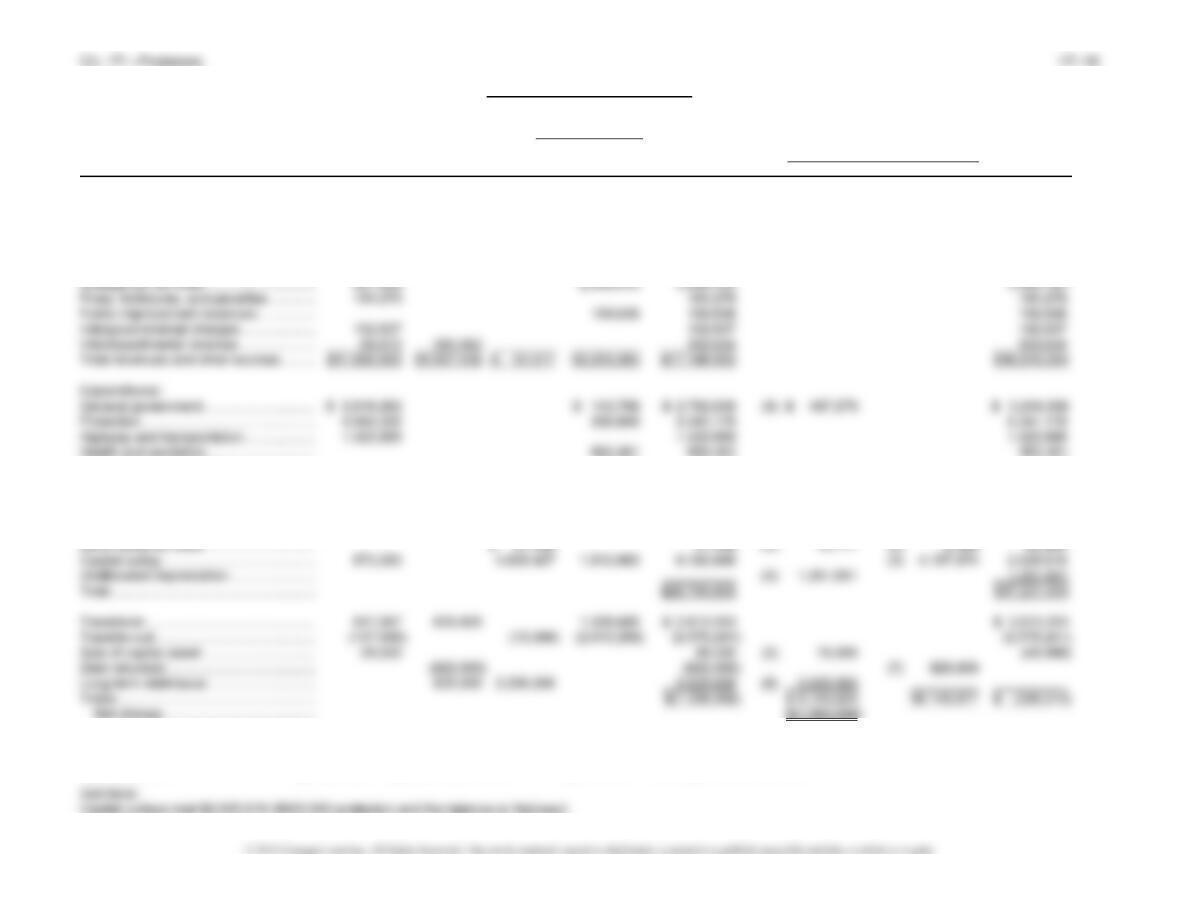

Support Schedule

General Debt Capital Non- Adjustments

Fund Service Project major Total Debit Credit Total

Adjustments:

Property tax ........................................... $ 8,466,838 $1,666,729 $ 10,465 $10,144,032 (6) $ 44,394 $ 9,910,221

(11) 189,417

Intergovernment .................................... 1,530,215 413,989 1,944,204 1,944,204

Commercial revenues ........................... 232,598 6,745 $ 51,217 360,725 651,285 651,285

Licenses and permits ............................ 639,103 639,103 639,103

Economic development ......................... 86,788 86,788 86,788

Education and recreation ...................... 1,768,889 130,257 1,899,146 1,899,146

Debt principal ........................................ $1,157,514 1,157,514 (7) $1,157,514

Debt interest .......................................... 1,057,619 1,057,619 (10) 18,862 1,076,481

(1) Increase capital assets. (4) Bond issue cost amortization. (7) Repayment of bonds. (10) Increase in accrued interest.

(2) Book value of assets sold. (5) New issue cost. (8) New bond issue. (11) Principal payments received in advance.

(3) Depreciation. (6) Decrease in special assessments. (9) Increase in uncompensated absences.