1.

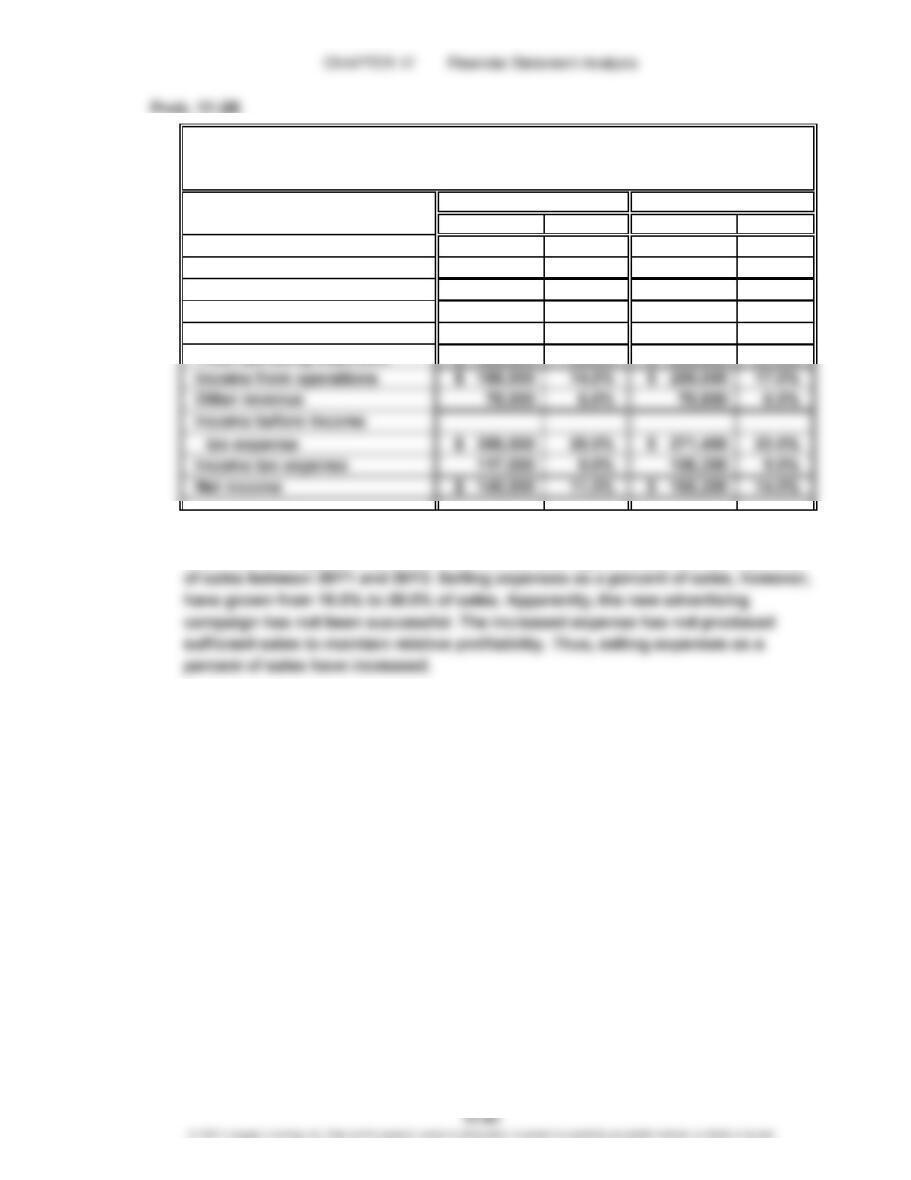

Amount Percent Amount Percent

Sales $1,300,000 100.0% $1,180,000 100.0%

Cost of merchandise sold 682,500 52.5% 613,600 52.0%

Gross profit $ 617,500 47.5% $ 566,400 48.0%

Selling expenses $ 260,000 20.0% $ 188,800 16.0%

Administrative expenses 169,000 13.0% 177,000 15.0%

2. The net income as a percent of sales has declined. All the costs and expenses,

other than selling expenses, have maintained their approximate cost as a percent

20Y2 20Y1

Fielder Industries Inc.

Comparative Income Statement

For the Years Ended December 31, 20Y2 and 20Y1

CHAPTER 17 Financial Statement Analysis

Prob. 17-3B

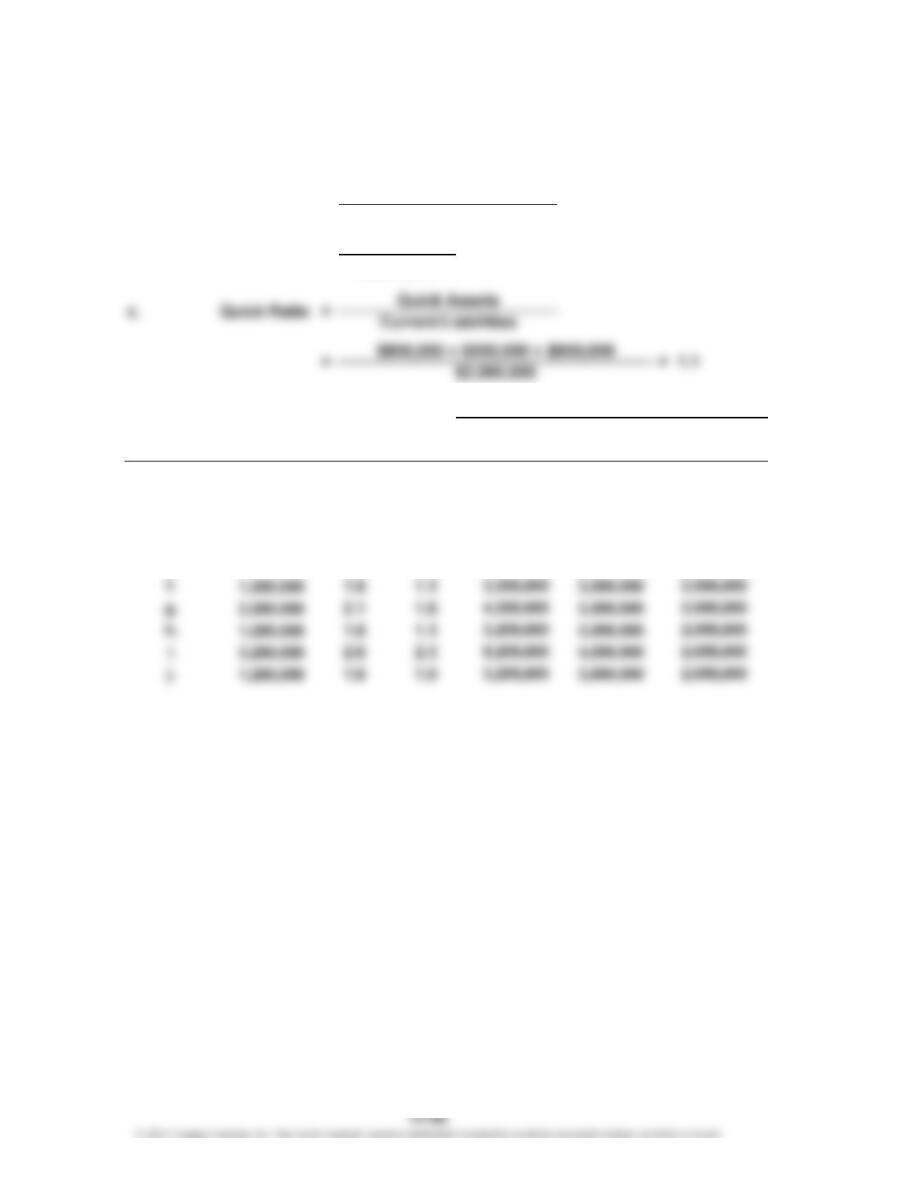

1. a. = Current Assets – Current Liabilities

= $3,200,000 – $2,000,000

2.

Working Quick

Capital Assets

$1,200,000 $2,200,000

1,200,000 1,912,500

1,200,000 2,200,000

1,200,000 2,075,000

875,000 2,200,000

Supporting Data

e.

d.

1.4 0.9 3,200,000

1.5 0.9 3,600,000

1.6 1.1 3,075,000

$3,200,000

1.7 1.1 2,912,500

c.

Current

Ratio

Quick

Ratio

Current

b.

= 1.6

Current Ratio = Current Assets

Current Liabilities

=

$3,200,000

$2,000,000

Working Capital

$1,200,000

Transaction

a.

b.

Current

Liabilities

$2,000,000

1,712,500

2,400,000

1,875,000

2,325,000

Assets

1.6 1.1

CHAPTER 17 Financial Statement Analysis

Prob. 17-4B

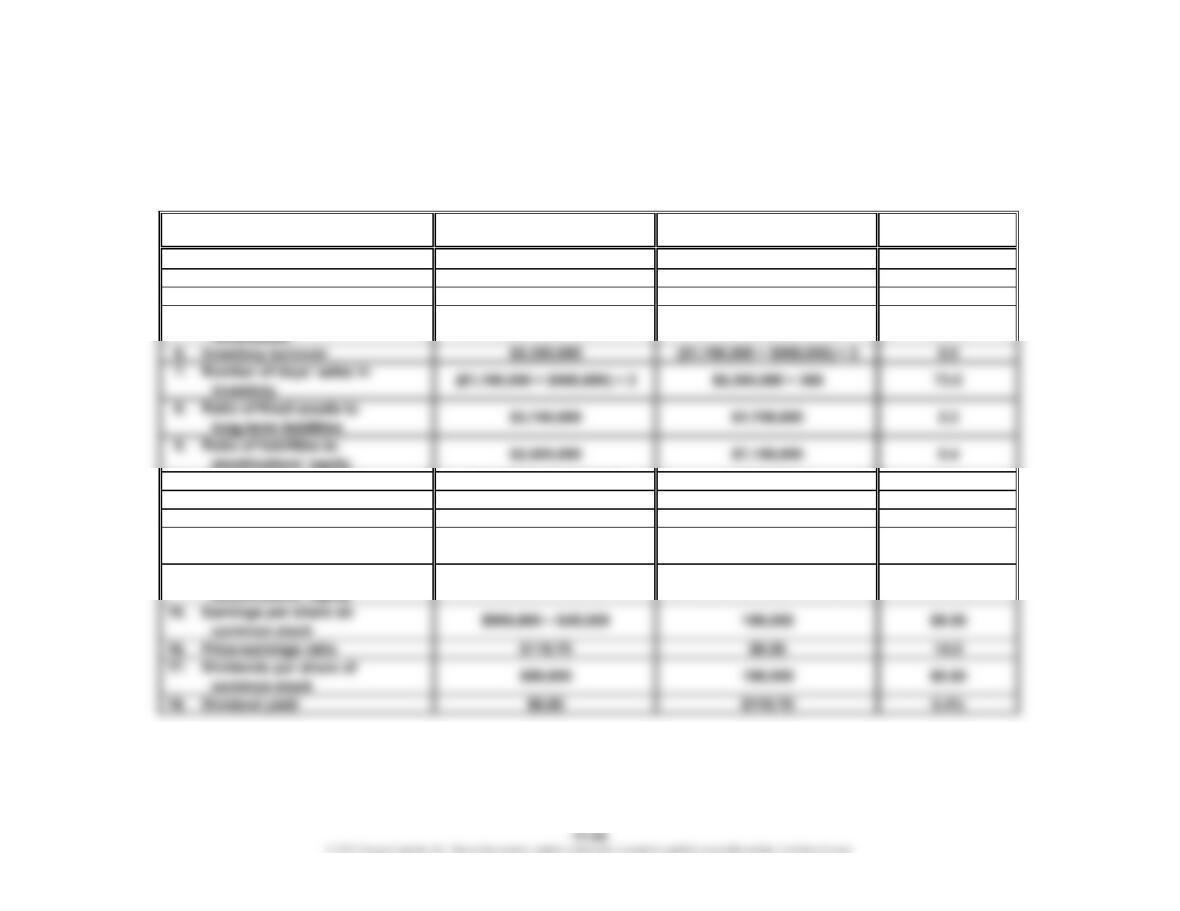

1. Working Capital: $3,690,000 – $900,000 = $2,790,000

Calculated

Numerator Denominator Value

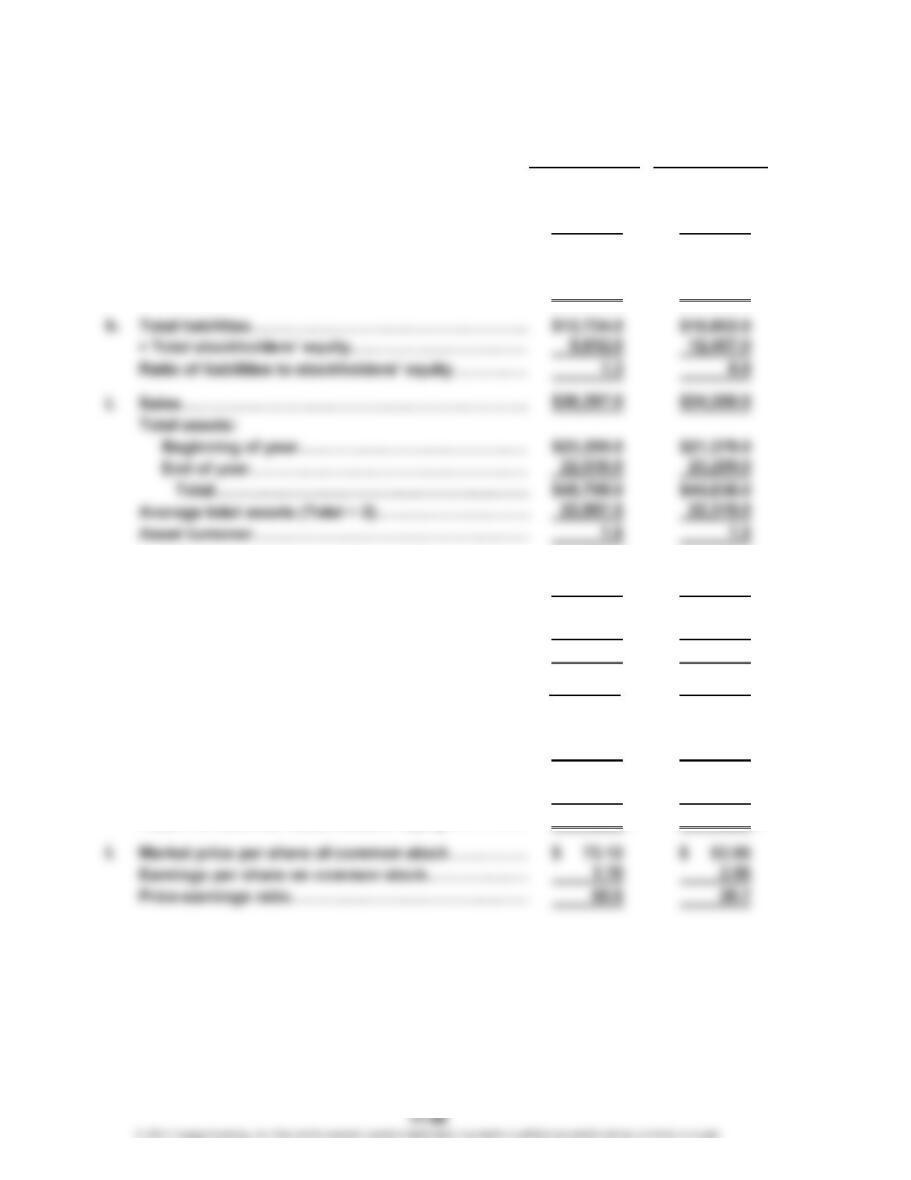

2. Current ratio $3,690,000 $900,000 4.1

3. Quick ratio $2,250,000 $900,000 2.5

4. Accounts receivable turnover $10,000,000 ($740,000 + $510,000) ÷ 2 16.0

5. Number of days’ sales in

stockholders’ equity

10. Times interest earned $1,130,000 + $170,000 $170,000 7.6

11. Asset turnover $10,000,000 ($9,780,000 + $8,755,000) ÷ 2 1.1

12. Return on total assets $900,000 + $170,000 ($9,780,000 + $8,755,000) ÷ 2 11.5%

13. Return on stockholders’

equity

14. Return on common

13.6%

13.3%

($6,680,000 + $5,875,000) ÷ 2

($7,180,000 + $6,375,000) ÷ 2

$900,000 – $45,000

$900,000

22.8

($740,000 + $510,000) ÷ 2 $10,000,000 ÷ 365

Ratio

CHAPTER 17 Financial Statement Analysis

Prob. 17-5B

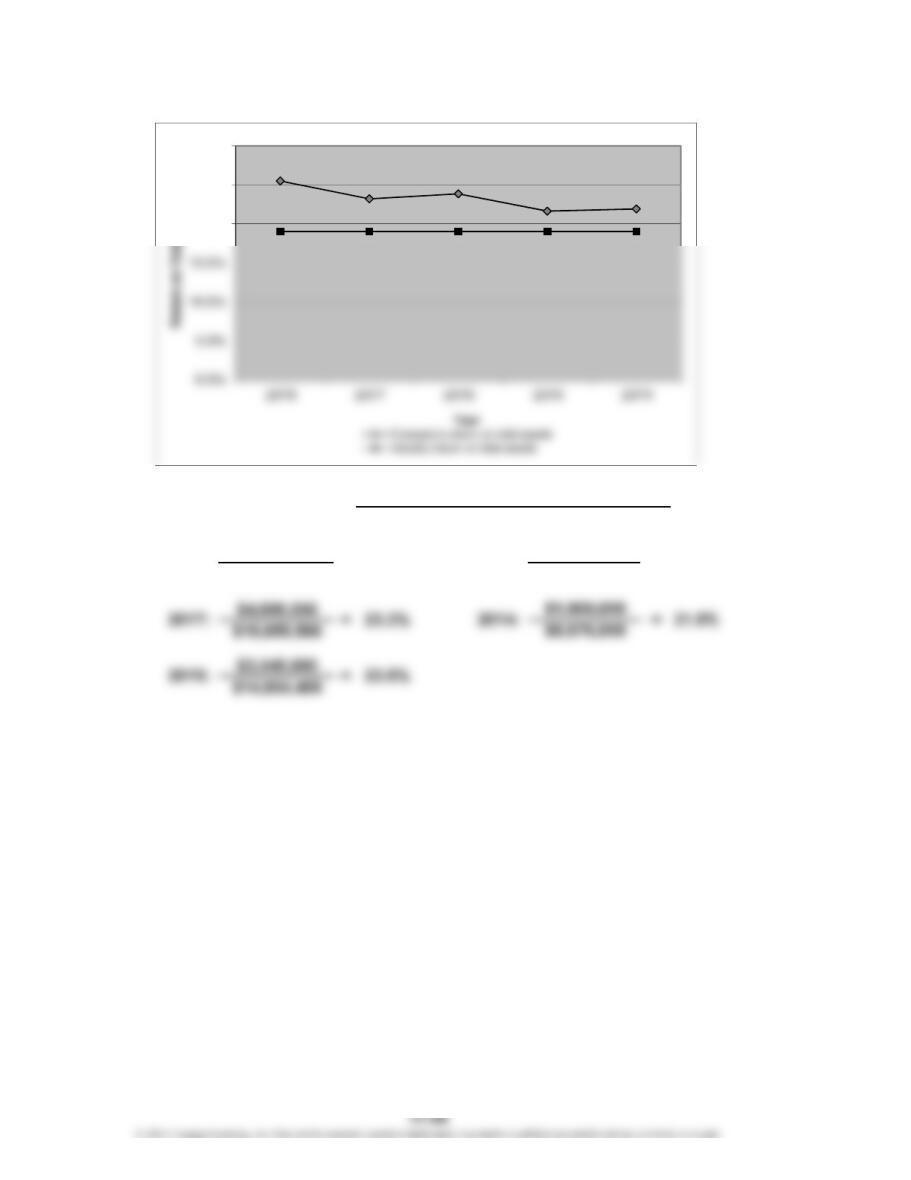

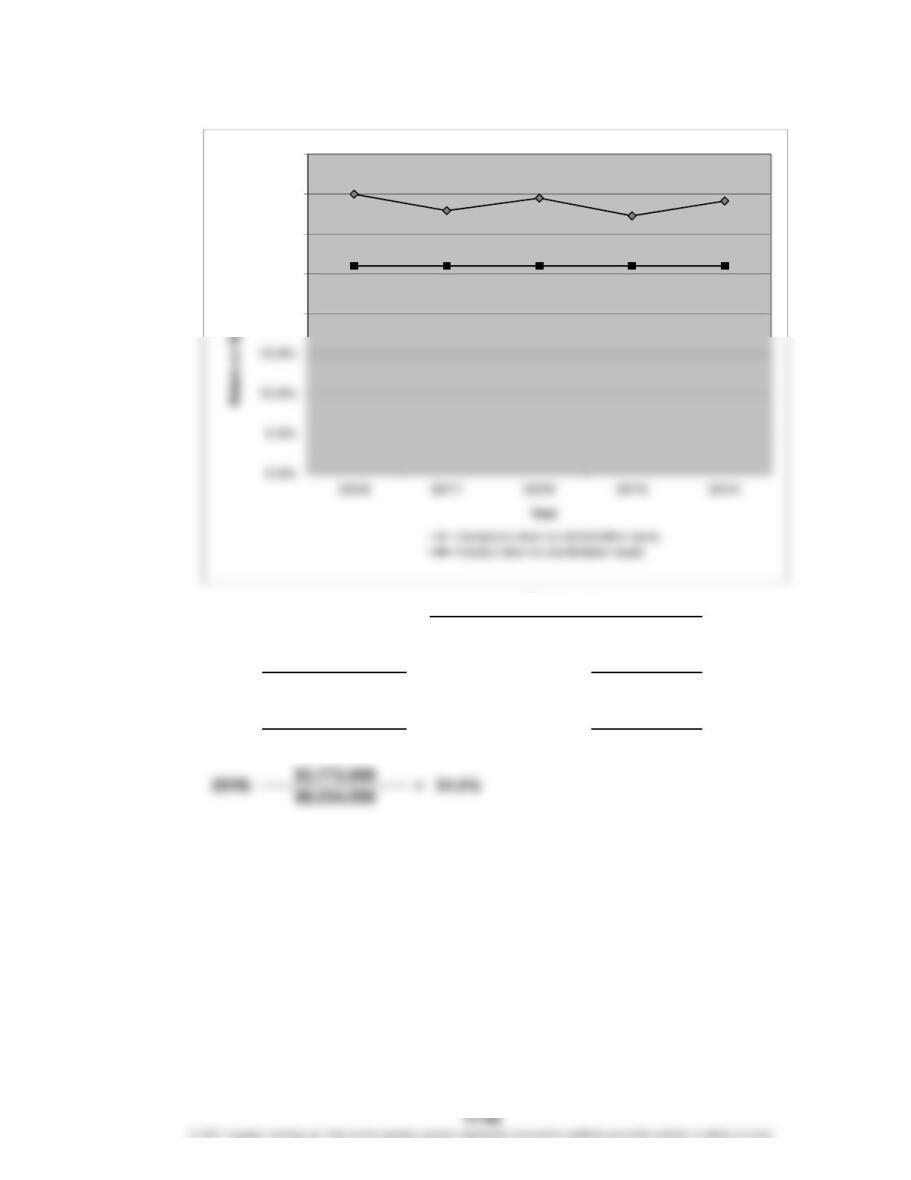

1. a.

$6,623,780

$25,988,665

Return on Total Assets

25.5%

=

=

$11,370,240

Net Income + Interest Expense

Average Total Assets

20Y8: =

20Y5: $2,458,000

21.6%

20.0%

25.0%

30.0%

CHAPTER 17 Financial Statement Analysis

Prob. 17-5B (Continued)

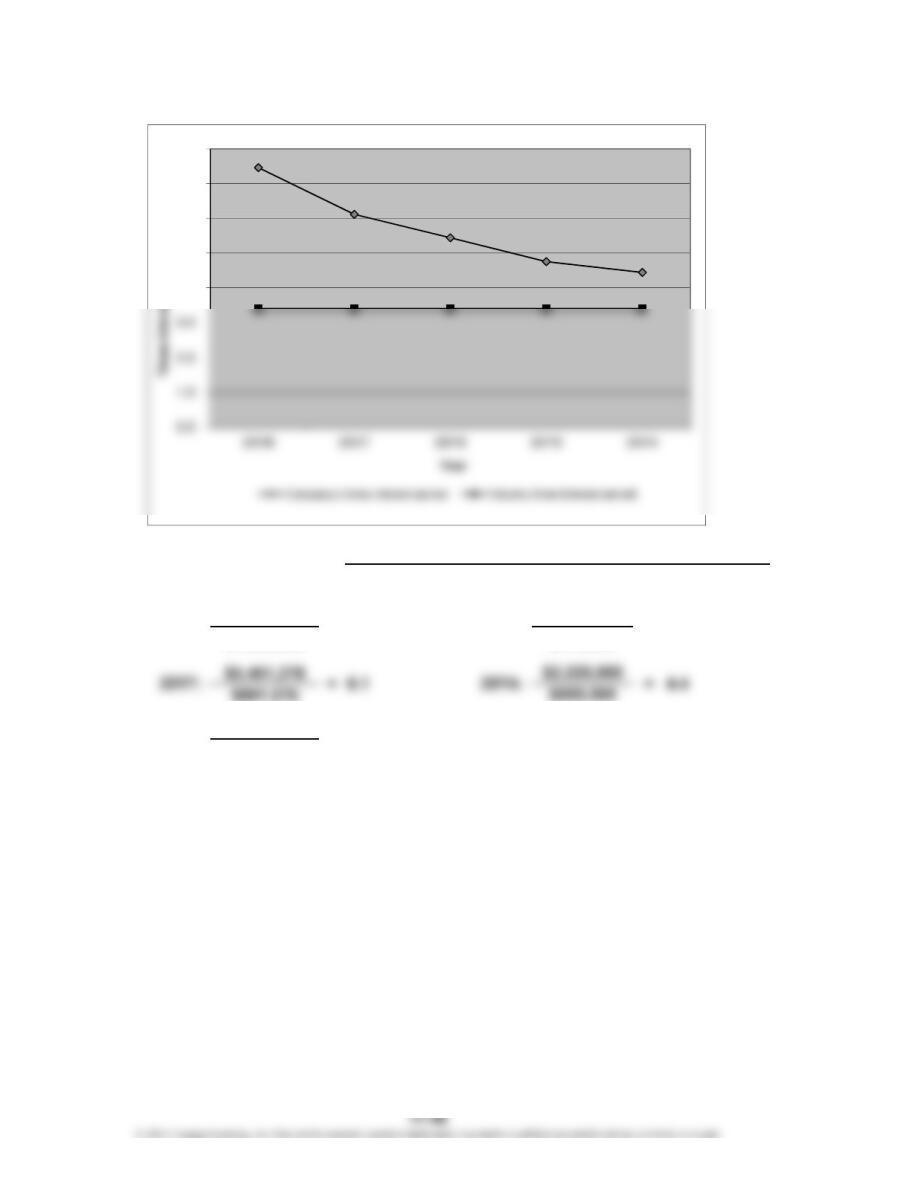

1. b.

$5,571,720

$15,920,340

$3,714,480

$11,277,240

34.1%

20Y8:

$1,400,000 =

=

20Y7: = 20Y4:

32.3%=

$4,100,000

=

35.0%

32.9%

Average Total Stockholders’ Equity

Net Income

Return on Stockholders’ Equity

20Y5: $1,848,000

$5,724,000

20.0%

25.0%

30.0%

35.0%

40.0%

CHAPTER 17 Financial Statement Analysis

Prob. 17-5B (Continued)

1. c.

$7,849,352

$1,052,060

$891,576

$4,180,920

$768,600

$2,899,600

$610,000

20Y6: = 5.4

Times Interest Earned Net Income + Income Tax Expense + Interest Expense

Interest Expense

7.5

=

4.8=20Y5:20Y8: =

4.0

5.0

6.0

7.0

8.0

CHAPTER 17 Financial Statement Analysis

Prob. 17-5B (Continued)

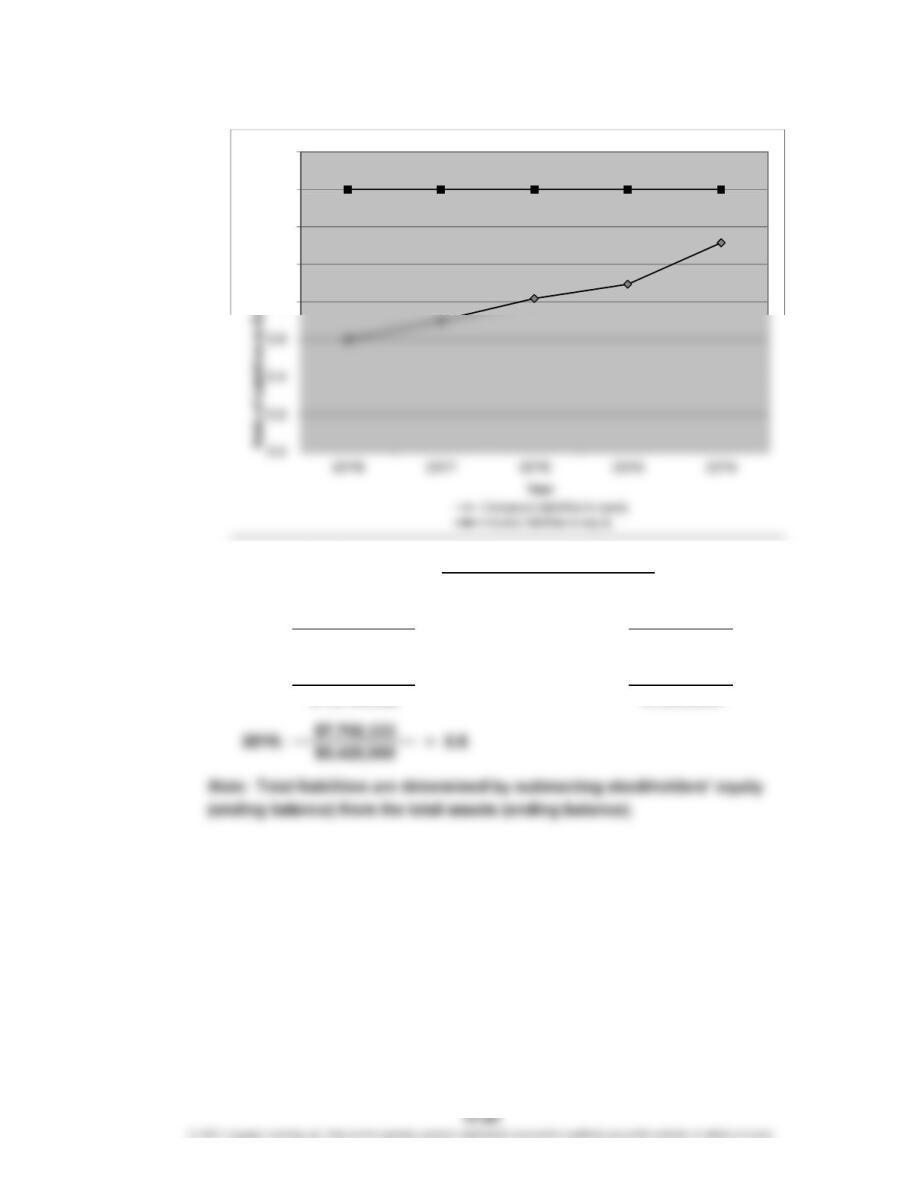

1. d.

$10,672,291

$18,706,200

$9,464,359

1.1

0.9

$5,940,480

$6,648,000

$5,352,000 =

=

=

=

20Y7: = 0.7

Stockholders’ Equity

Ratio of Liabilities to Total Liabilities

Total Stockholders’ Equity

20Y4:

20Y5:

0.620Y8:

0.8

1.0

1.2

1.4

1.6

CHAPTER 17 Financial Statement Analysis

Prob. 17-5B (Concluded)

2. Both the return on total assets and the return on stockholders’ equity are above

the industry average for all five years. The return on total assets is improving

gradually. The return on stockholders’ equity exceeds the return on total assets,

providing evidence of the positive use of leverage. The company is clearly growing

earnings as fast as the asset and equity base. In addition, the ratio of liabilities to

CHAPTER 17 Financial Statement Analysis

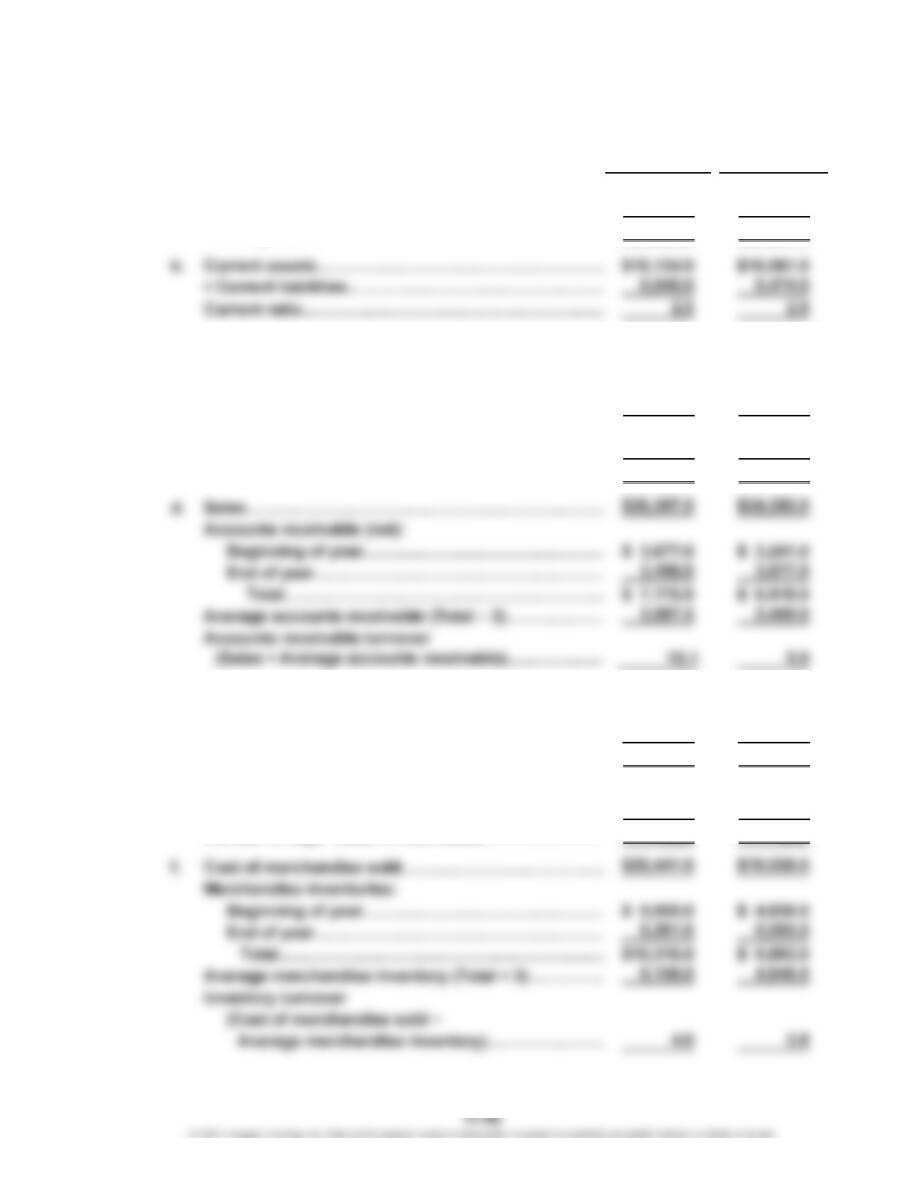

May 31, May 31,

2018 2017

1. a. Current assets……………………………………………

…

$15,134.0 $16,061.0

Current liabilities…………………………………………

…

6,040.0 5,474.0

Working capital……………………………………………

…

$ 9,094.0 $10,587.0

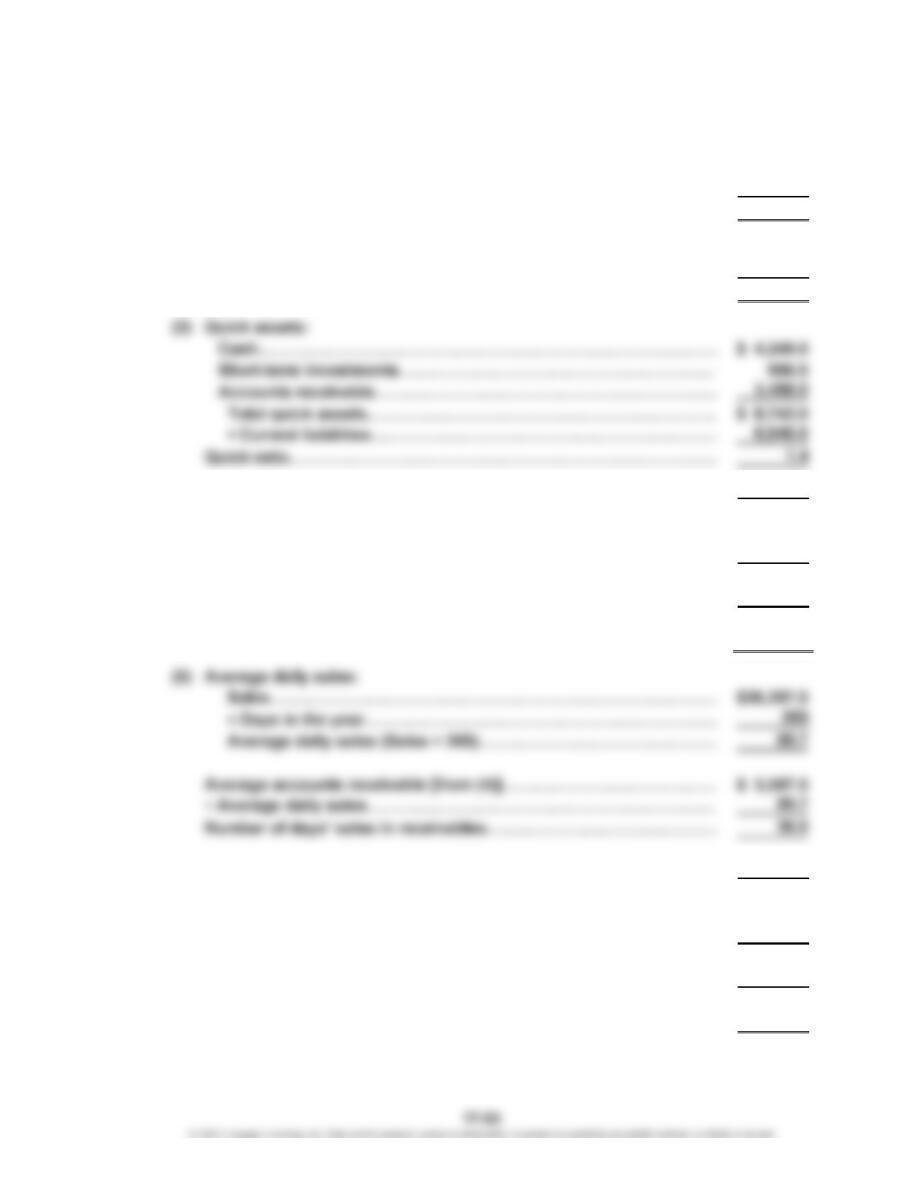

c. Quick assets:

Cash………………………………………………………

…

$ 4,249.0 $ 3,808.0

Short-term investments………………………………

…

996.0 2,371.0

Accounts receivable……………………………………

…

3,498.0 3,677.0

Total quick assets……………………………………

…

$ 8,743.0 $ 9,856.0

÷ Current liabilities………………………………………… 6,040.0 5,474.0

Quick ratio…………………………………………………

…

1.4 1.8

…

e. Average daily sales:

Sales……………………………………………………

…

$36,397.0 $34,350.0

÷ Days in the year……………………………………… 365 365

Average daily sales (Sales ÷ 365)…………………

…

$ 99.7 $ 94.1

Average accounts receivable [from (d)]………………

…

$ 3,587.5 $ 3,459.0

÷ Average daily sales……………………………………

…

99.7 94.1

…

…

…

…

36.0 36.8

NIKE, INC., PROBLEM

…

…

CHAPTER 17 Financial Statement Analysis

May 31, May 31,

2018 2017

g. Average merchandise inventory [from (f)]…………

…

$ 5,158.0 $ 4,946.5

Cost of merchandise sold……………………………… 20,441.0 19,038.0

Average daily cost of merchandise sold (÷ 365)…… 56.0 52.2

Number of days’ sales in inventory (Average

inventory ÷ Average daily cost

of merchandise sold)…………………………………

…

92.1 94.8

j. Net income………………………………………………

…

$ 1,933.0 $ 4,240.0

Interest expense…………………………………………

…

54.0 59.0

Total……………………………………………………

…

$ 1,987.0 $ 4,299.0

÷ Average total assets [from (i)]………………………

…

22,897.5 22,319.0

Return on total assets…………………………………

…

8.7% 19.3%

k. Net income………………………………………………

…

$ 1,933.0 $ 4,240.0

Stockholders’ equity:

Beginning of year……………………………………

…

$12,407.0 $12,258.0

End of year……………………………………………

…

9,812.0 12,407.0

Total…………………………………………………

…

$22,219.0 $24,665.0

Average common stockholders’ equity (Total ÷ 2)

…

11,109.5 12,332.5

Return on common stockholders’ equity…………… 17.4% 34.4%

…

…

NIKE, INC., PROBLEM (Continued)

…

…

…

…

…

CHAPTER 17 Financial Statement Analysis

2. Before reaching definitive conclusions, each measure should be compared with

past years, industry averages, and similar firms in the industry.

a. The working capital decreased between years.

b. and c. The current and quick ratios both decreased during 2018.

f. and g. The results of these two analyses show a very slight increase in

inventory turnover and a decrease in the number of days’ sales in

inventory. Both changes are small. Inventory management is critical to

Nike, so this indicates a favorable change.

h. The margin of protection to creditors declined.

i. These analyses indicate that the effectiveness in the use of assets to generate

l. The price-earnings ratio increased from 2017 to 2018. This increase

was driven by a decrease in Nike’s earnings per share (from $2.56 in

2017 to $1.19 in 2018) combined with a sizable increase in stock price

during the same period.

NIKE, INC., PROBLEM (Concluded)

CHAPTER 17 Financial Statement Analysis

CP 17-1

No. Josh did not behave ethically. The Sarbanes-Oxley Act of 2002 requires a report on

internal control by management. This report acknowledges management’s responsibility

CASES & PROJECTS

CHAPTER 17 Financial Statement Analysis

CP 17-2

Sample solution based on Nike’s 2018 financial statements.

a. (1) Current assets………………………………………………………………

…

$15,134.0

– Current liabilities…………………………………………………………… 6,040.0

Working capital………………………………………………………………

…

$ 9,094.0

(2) Current assets………………………………………………………………

…

$15,134.0

÷ Current liabilities…………………………………………………………… 6,040.0

Current ratio…………………………………………………………………

…

2.5

(4) Sales……………………………………………………………………………

…

$36,397.0

Accounts receivable (net):

Beginning of year………………………………………………………… $ 3,677.0

End of year………………………………………………………………… 3,498.0

Total……………………………………………………………………

…

$ 7,175.0

Average accounts receivable (Total ÷ 2)………………………………… 3,587.5

Accounts receivable turnover

(Sales ÷ Average accounts receivable)………………………………… 10.1

…

…

…

(6) Cost of merchandise sold…………………………………………………

…

$20,441.0

Merchandise inventories:

Beginning of year………………………………………………………… $ 5,055.0

End of year………………………………………………………………… 5,261.0

Total………………………………………………………………………

…

$10,316.0

Average merchandise inventory (Total ÷ 2)……………………………

…

5,158.0

Inventory turnover

(Cost of merchandise sold ÷ Average merchandise inventory)…

…

4.0

…

…

…

…

CHAPTER 17 Financial Statement Analysis

May 31,

2018

(7) Average merchandise inventory [from (6)]…………………………

…

$ 5,158.0

Cost of merchandise sold……………………………………………… 20,441.0

Average daily cost of merchandise sold ……………………………

…

56.0

Number of days’ sales in inventory (Average

merchandise inventory ÷ Average

daily cost of merchandise sold)……………………………………

…

92.1

c. (1) Sales………………………………………………………………………

…

$36,397.0

Total assets:

Beginning of year……………………………………………………

…

$23,259.0

End of year……………………………………………………………

…

22,536.0

Total…………………………………………………………………

…

$45,795.0

Average total assets (Total ÷ 2)………………………………………

…

22,897.5

Asset turnover …………………………………………………………

…

1.6

(2) Net income………………………………………………………………

…

$ 1,933.0

Interest expense…………………………………………………………

…

54.0

Total……………………………………………………………………

…

$ 1,987.0

÷ Average total assets [from (c1)]………………………………… 22,897.5

Return on total assets …………………………………………………

…

8.7%

…

…

…

…

CP 17-2 (Continued)

CHAPTER 17 Financial Statement Analysis

May 31,

2018

(4) Net income………………………………………………………………

…

$1,933.0

÷ Number of shares of common stock………………………………

…

1,624

Earnings per share………………………………………………………

…

$ 1.19

CP 17-3

To: Boss Freeman

From: A+ Student

Re: Debt vs. Equity Financing

I have reviewed your company history and appreciate the challenges your company

has faced in the past during economic downturns. While your conservative approach

to debt financing is commendable, your unwillingness to issue debt could limit your

potential for future success. Financing future growth exclusively through retained

earnings and additional stock sales does not allow the shareholders to take advantage

CP 17-2 (Concluded)

*

CP 17-4

1.

Amazon Best Buy Walmart

Sales……………………………………………………….. 100.0% 100.0% 100.0%

Cost of sales……………………………………………. 59.8% 76.8% 74.9%

Gross profit……………………………………………… 40.2% 23.2% 25.1%

Selling, general, and administrative

expenses……………………………………………….

.

34.9% 18.7% 20.8%

2. Amazon has the highest gross profit on a percentage basis but has the lowest

income from operations on a percentage basis. This is because of the relatively

large percentage of sales that is used for selling, general, and administrative

activities. Walmart has a lower gross profit on a percentage basis but generates

CP 17-5

1.

Year 2: $2,159.1 + $899.5 = 4.9%

$61,852

Year 1: $1,523.9 + $763.7 = 3.9%

$57,933

a. Return on Total Assets = Net Income + Interest Expense

Average Total Assets

Year 3: $2,368.4 + $1,203.6 = 5.3%

$67,947

CHAPTER 17 Financial Statement Analysis

CP 17-5 (Concluded)

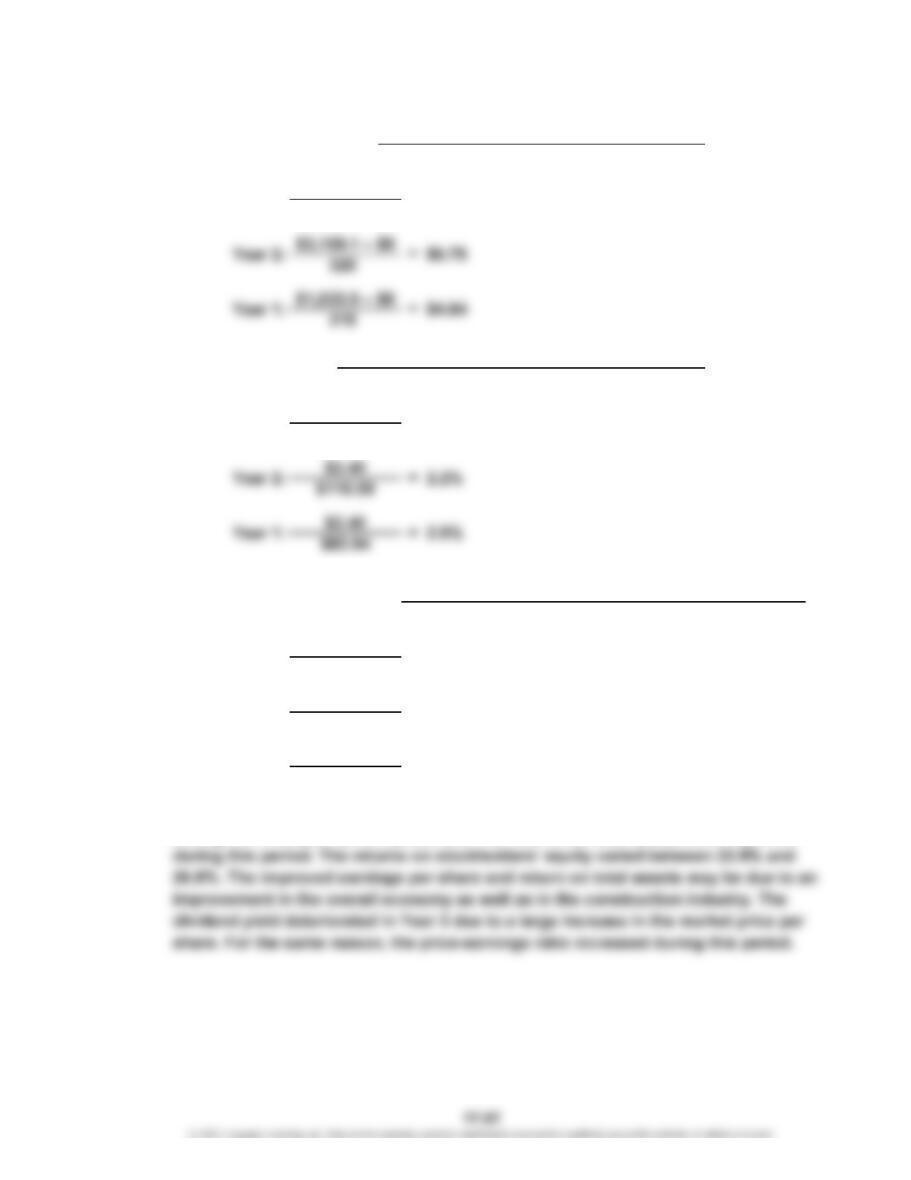

2. Deere’s profitability, as measured by earnings per share, has improved significantly

during the three-year period presented. The returns on total assets also improved

Year 2: $110.59 = 16.4

$6.75

Year 1: $83.94 = 17.3

$4.84

e. Price-Earnings Ratio = Market Price per Share of Common Stock

Earnings per Share

Year 3: $134.16 = 18.3

$7.33

d. Dividend Yield = Dividend per Share of Common Stock

Market Price per Share of Common Stock

Year 3: $2.58 = 1.9%

$134.16

c. Earnings per Share = Net Income – Preferred Dividends

Shares of Common Stock Outstanding

Year 3: $2,368.4 – $0 = $7.33

323

CHAPTER 17 Financial Statement Analysis

CP 17-6

1.

Summary Table:

a. Return on total assets

b. Return on stockholders’ equity

c. Times interest earned

d. Ratio of liabilities to stockholders’ equity

Marriott: $1,907 + $340 = 9.5%

$23,771

a. Return on Total Assets = Net Income + Interest Expense

Average Total Assets

11.1%

$7,608

Hyatt: $769 + $76 =

c. Times Interest Earned = Income Before Income Tax + Interest Expense

Interest Expense

Marriott: $2,345 + $340 = 7.9

$340

Hyatt: $951 + $76 = 13.5

$76

9.6 1.1

Hyatt

9.5% 11.1%

65.7% 20.5%

7.9 13.5

Marriott

CHAPTER 17 Financial Statement Analysis

CP 17-6 (Concluded)

2. Hyatt has a slightly higher return on total assets (11.1% vs. 9.5%), while

Marriott has a significantly higher return on stockholders’ equity (65.7% vs.

20.5%). Hyatt’s weaker performance relative to Marriott’s appears to be due to

its weak earnings relative to its debt level. Hyatt has less leverage than

Marriott. This is confirmed by the ratio of liabilities to stockholders’ equity,