Chapter 17 – Allocation of Support Activity Costs and Joint Costs

CHAPTER 17

Allocation of Support Activity Costs and Joint

Costs

ANSWERS TO REVIEW QUESTIONS

17-1 A service department is a unit in an organization that is not involved directly in

producing the organization’s goods or services. However, a service department does

of these costs are allocated to other service departments.

(b) Under the step-down method, a sequence is first established for allocation of

(c) Under the reciprocal-services method, a system of simultaneous equations is

17-4 The first department in the sequence under the step-down method is the service

department that serves the largest number of other service departments. The second

Chapter 17 – Allocation of Support Activity Costs and Joint Costs

17-5 The dual-allocation approach improves the resulting cost allocations because

17-6 A potential behavioral problem that can result from the dual approach to service

17-7 Budgeted service department costs should be allocated rather than actual service

17-8 Under two-stage allocation with departmental overhead rates, costs first are

distributed to departments; then they are allocated from service departments to

production departments. Finally, they are assigned from production departments to

17-9 (a) Joint-production process: A production process in which the processing of a

17–10 Under the physical-units method of joint cost allocation, joint production costs are

17–11 Under the relative-sales-value method of joint cost allocation, joint production costs

17–12 The net realizable value of a joint product is equal to its ultimate sales value minus

17–13 Joint cost allocations are useful for product-costing purposes. Product costing is

Chapter 17 – Allocation of Support Activity Costs and Joint Costs

SOLUTIONS TO EXERCISES

EXERCISE 17-15 (15 MINUTES)

Direct Customer Service

Departments Using Services

Deposit

Loan

Provider of Service

Cost to Be

Allocated

Proportion

Amount

Proportion

Amount

HR

$ 459,000

(6/9)

$306,000

(3/9)

$153,000

Computing

Total

$1,147,500

$436,500

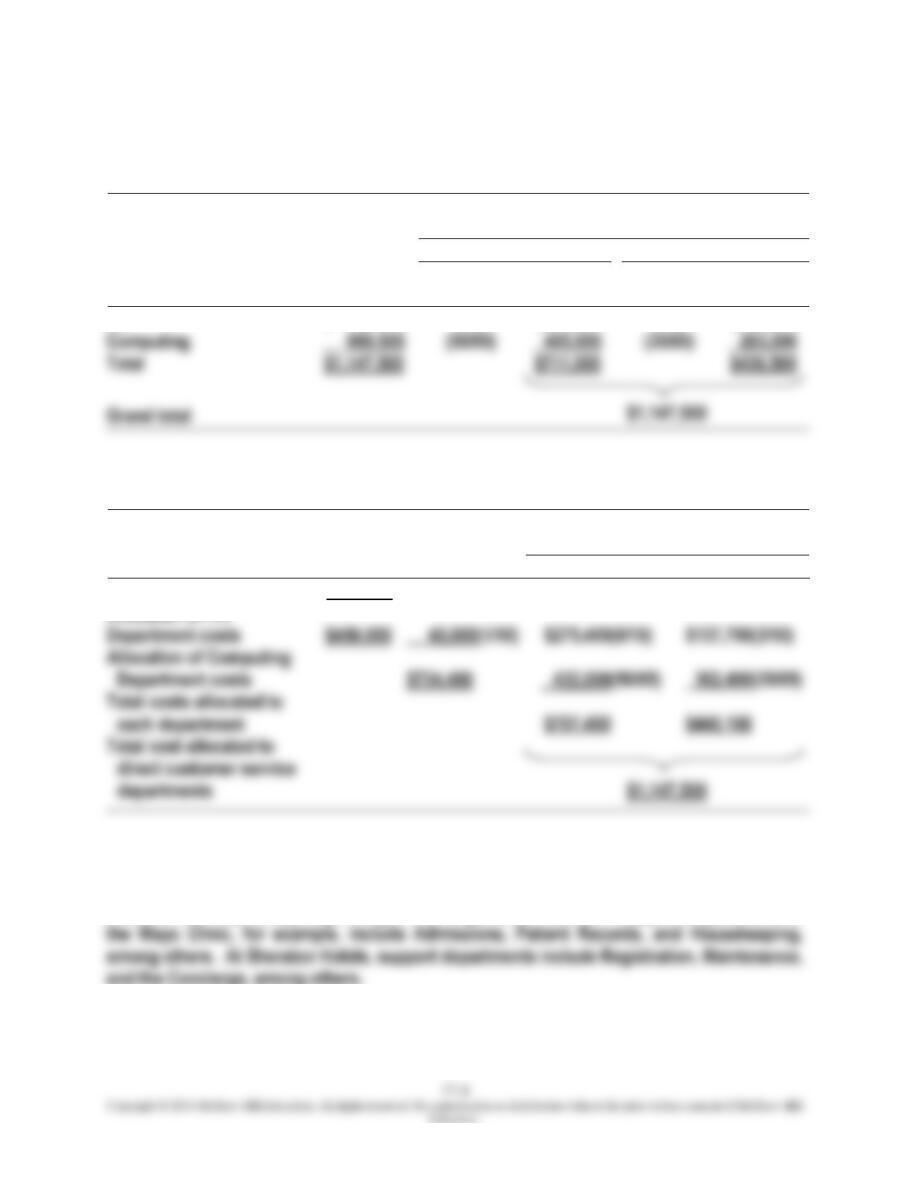

EXERCISE 17-16 (15 MINUTES)

Direct Customer Service

Departments Using Services

HR

Computing

Deposit

Loan

Costs prior to allocation

$459,000

$688,500

Department costs

(6/10)

(3/10)

Allocation of Computing

$734,400

(50/85)

(35/85)

Allocation of HR

EXERCISE 17-17 (30 MINUTES)

Answers will vary widely, depending on the organization chosen. Support departments at

EXERCISE 17-18 (15 MINUTES)

1. Cost allocation using direct method:

Academic Departments Using Services

Liberal Arts

Sciences

Provider of Service

Cost to Be

Allocated

Proportion

Amount

Proportion

Amount

Library

$ 900,000

(3/5)

$540,000

(2/5)

$360,000

Computing Services

(3/8)

(5/8)

Total

$1,260,000

$675,000

$585,000

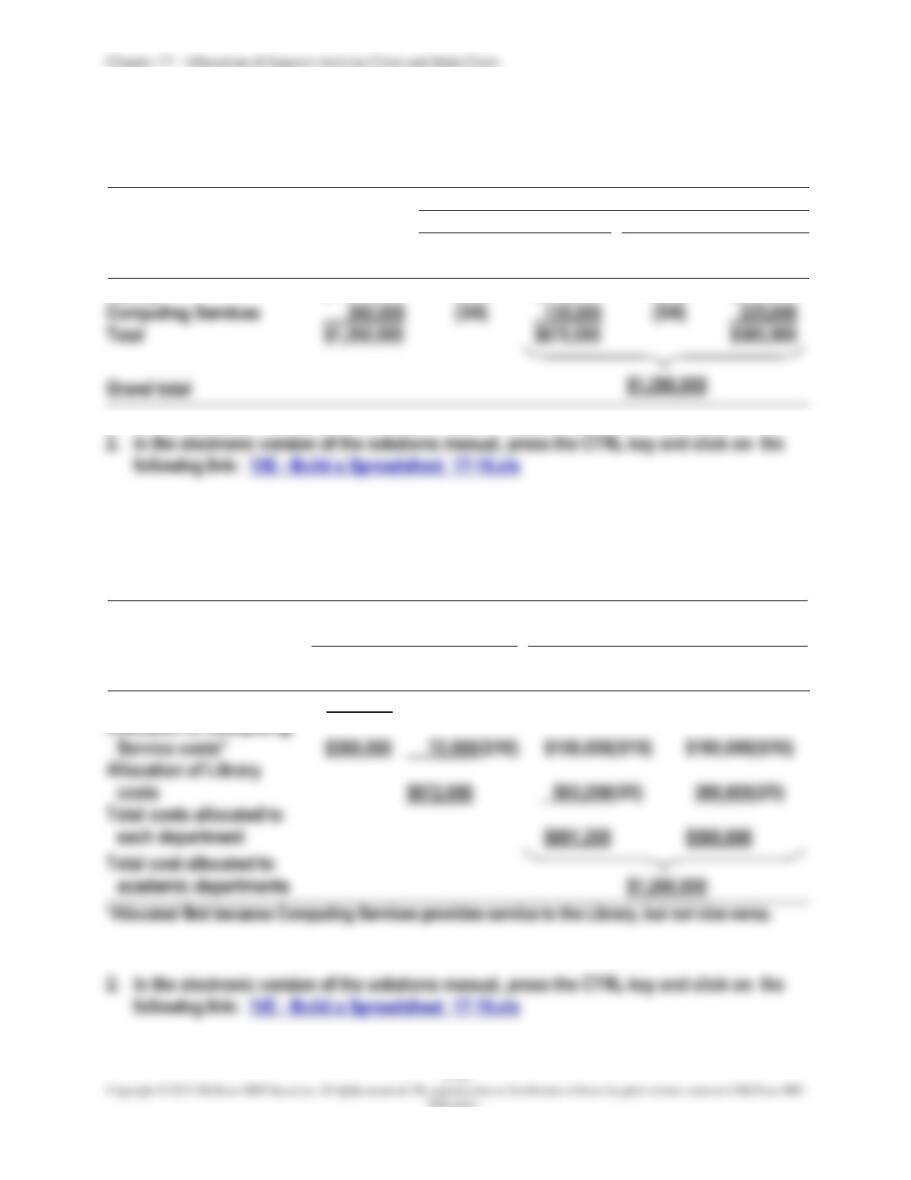

EXERCISE 17-19 (15 MINUTES)

1. Cost allocation using step-down method:

Service Departments

Academic Departments

Using Services

Computing

Services

Library

Liberal

Arts

Sciences

Costs prior to allocation

$360,000

$900,000

$360,000

(3/10)

(5/10)

$972,000

(3/5)

(2/5)

Chapter 17 – Allocation of Support Activity Costs and Joint Costs

EXERCISE 17-20 (10 MINUTES)

Joint

Cost

Joint

Products

Quantity at

Split-Off Point

Relative

Proportion

Allocation

of

Joint Cost

Yummies

12,000 kilograms

.60

$54,000

*

$90,000

Crummies

.40

EXERCISE 17-21 (15 MINUTES)

Joint

Cost

Joint

Products

Quantity at

Split-Off

Sales

Price

Sales Value at

Split-Off Point

Relative

Proportion

Allocation

of

Joint Cost

Yummies

12,000 kg

$6.00

$ 72,000

.545*

$49,050

†

.455*

EXERCISE 17-22 (25 MINUTES)

1. Decision analysis:

Incremental revenue per kilogram:

Sales price of mulch …………………………………………………………

$10.50

Sales price of Crummies …………………………..………………………

Incremental revenue …………………………………………………………

$3.00

Incremental processing cost per kilogram …………………………

Incremental revenue less incremental cost ………………………..

$1.50

Chapter 17 – Allocation of Support Activity Costs and Joint Costs

EXERCISE 17-22 (CONTINUED)

2. Joint cost allocation using net-realizable-value method:

Joint

Cost

Joint

Products

Sales Value of

Final Product

Separable Cost

of Processing

Net

Realizable

Value*

Relative

Proportion

Allocation

of

Joint Cost

Yummies

$72,000 (12,000 $6.00)

-0-

$ 72,000

.50

$45,000

†

.50

†

EXERCISE 17-23 (25 MINUTES)

(a) First, specify equations to express the relationships between the service

departments.

Notation: H denotes the total cost of Human Resources

C denotes the total cost of Computing

Solution of equations: Substitute from equation (2) into equation (1).

H

=

459,000 + .15(688,500 + .10H)

=

562,275

C

=

688,500 + .10(570,838)

Chapter 17 – Allocation of Support Activity Costs and Joint Costs

EXERCISE 17-23 (CONTINUED)

(b) Cost allocation using the reciprocal-services method:

Service Departments

Direct Customer Service

Departments

Human

Resources

(HR)

Computing

Deposit

Loan

Traceable costs

$459,000

$688,500

(570,838)

*(.6)

*(.3)

(745,584)

(.50)

*(.35)

Chapter 17 – Allocation of Support Activity Costs and Joint Costs

SOLUTIONS TO PROBLEMS

PROBLEM 17-24 (40 MINUTES)

1. Direct method:

Production Department

Etching

Finishing

Provider of Service

Cost to Be

Allocated

Proportion

Amount

Proportion

Amount

Maintenance

$ 96,000

(1/9)

$ 10,667*

(8/9)

$ 85,333*

Computing

(7/8)

(1/8)

Total service department costs allocated ………………….

Overhead costs traceable to

640,000

Total overhead cost …………………………………………………

Direct-labor hours (DLH)

(20 2,000) ………………………………………………………….

40,000

(80 2,000) ………………………………………………………….

160,000

Check on allocation procedure:

$448,167

147,833

Overhead rate per hour

Chapter 17 – Allocation of Support Activity Costs and Joint Costs

PROBLEM 17-24 (CONTINUED)

2. Step-down method:

Service Departments

Production Departments

Computing

Maintenance

Etching

Finishing

Costs prior to allocation

$500,000

$ 96,000

$500,000

(2/10)

(7/10)

(1/10)

$196,000

(1/9)

(8/9)

Total service department cost allocated ………………………….

Total overhead cost ……………………………………………………….

Direct-labor hours (DLH)

(20 2,000) ………………………………………………………………..

40,000

(80 2,000) ………………………………………………………………..

160,000

$19.294*

Check on allocation procedure:

Chapter 17 – Allocation of Support Activity Costs and Joint Costs

PROBLEM 17-25 (40 MINUTES)

1. Direct method:

Production Departments

Machining

Finishing

Provider of Service

Cost to Be

Allocated

Proportion

Amount

Proportion

Amount

HR

$250,000

(4/9)

$111,111

*

(5/9)

$138,889

*

Maintenance

*

*

Design

Total

$830,000

$480,944

2. Sequence for step-down method:

Chapter 17 – Allocation of Support Activity Costs and Joint Costs

PROBLEM 17-25 (CONTINUED)

3. Step-down method:

Service Departments

Production Departments

HR

Maintenance

Design

Machining

Finishing

Costs prior to

allocation

$250,000

$230,000

$350,000

Allocation of HR

Department costs

$250,000

(5/100)

(5/100)

$100,000

(40/100)

$242,500

*(5/80)

*(35/80)

(40/80)

Allocation of Design

Department costs

$377,656

(45/60)

(15/60)

$340,664

PROBLEM 17-26 (70 MINUTES)

1. Direct method combined with dual allocation:

(a) Variable costs:

Production Departments

Machining

Finishing

Provider of Service

Cost to Be

Allocated

Proportion*

Amount

Proportion*

Amount

HR

$ 50,000

(4/9)

$ 22,222

†

(5/9)

$ 27,778

†

Maintenance

(35/75)

†

(40/75)

†

Design

(45/60)

(15/60)

(b) Fixed costs:

Production Departments

Machining

Finishing

Provider of Service

Cost to Be

Allocated

Proportion*

Amount

Proportion*

Amount

HR

$200,000

(35/85)

$82,353

†

(50/85)

$117,647

†

Maintenance

(48/72)

100,000

(24/72)

Design

(48/60)

(12/60)

PROBLEM 17-26 (CONTINUED)

(c) Total costs allocated:

Machining

Finishing

Variable costs ………………………………………………………………….

$ 97,055

$ 82,945

Fixed costs ………………………………………………………………………

Total costs ……………………………………………………………………….

2. Step-down method combined with dual allocation:

Chapter 17 – Allocation of Support Activity Costs and Joint Costs

PROBLEM 17-26 (CONTINUED)

(a) Variable costs:

Service Departments

Production Departments

HR

Maintenance

Design

Machining

Finishing

Costs prior to

allocation

$50,000

$80,000

$50,000

Allocation of HR

Department costs

$50,000

(5/100)*

(5/100)

$20,000

(40/100)

(50/100)

$82,500

(40/80)

Allocation of Design

Department costs

$57,656

(45/60)

(15/60)

PROBLEM 17-26 (CONTINUED)

(b) Fixed costs:

Service Departments

Production Departments

HR

Maintenance

Design

Machining

Finishing

Costs prior to

allocation

$200,000

$150,000

$300,000

Allocation of HR

Department costs

$200,000

(5/100)*

(10/100)

(35/100)

(50/100)

$160,000

(8/80)

(48/80)

(24/80)

Allocation of Design

Department costs

$336,000

(48/60)

(12/60)

Chapter 17 – Allocation of Support Activity Costs and Joint Costs

PROBLEM 17-26 (CONTINUED)

(c) Total costs allocated:

Machining

Finishing

Variable costs ………………………………………………………………….

$ 99,336

$ 80,664

Fixed costs ………………………………………………………………………

Total costs ……………………………………………………………………….

PROBLEM 17-27 (50 MINUTES)

1. Plantwide overhead rates:

Departments (numbers in thousands)

Molding

Component

Assembly

Total

Manufacturing departments:

Variable overhead ………………….

$ 7,000

$20,000

$33,000

$ 60,000

Fixed overhead ……………………..

$32,400

$45,200

$119,600

Service departments:

Power ……………………………………

36,800

Maintenance ………………………….

8,000

$164,400

Estimated direct-labor hours (DLH):

Molding …………………………………

500

Component …………………………..

Assembly ……………………………..

=

Chapter 17 – Allocation of Support Activity Costs and Joint Costs

PROBLEM 17-27 (CONTINUED)

2. Departmental overhead rates:

Departments (numbers in thousands)

Service

Manufacturing

Power

Maintenance

Molding

Component

Assembly

Departmental overhead

costs ……………………………..

$36,800

$ 8,000

$42,000

$32,400

$45,200

a. Allocation of mainten-

$65,520

$47,520

$51,360

b. Allocation of power

costs (dual, direct

method)

Fixed costs

($24,000):

c. Cost driver ………………….

875

MH

2,000

DLH

1,500

DLH

Rate (departmental overhead

Chapter 17 – Allocation of Support Activity Costs and Joint Costs

PROBLEM 17-27 (CONTINUED)

3.

Memorandum

Date:

Today

To:

President, Travelcraft, Inc.

From:

I.M. Student

Subject:

Use of departmental overhead rates

Travelcraft should use departmental rates to assign overhead to its products. The

PROBLEM 17-28 (40 MINUTES)

1. Net-realizable-value method of allocation:

Joint

Cost

per Run

Joint

Products

Sales Value of

Final Product*

Additional

Cost of

Processing

Net

Realizable

Value

Relative

Proportion†

Allocation

of Joint

Cost

HTP-3 ………………….

$2,240,000

……………………

$699,200

……

$1,540,800

…………………..

48.15%

…..

$ 654,840

PST-4 ………………….

……………………

652,800

……

…………………..

32.10%

…..

RJ–5 …………………….

……………………

……

…………………..

19.75%

…..