17

Additional Topics in Variance Analysis

Solutions to Review Questions

17–1.

When production is not equal to sales, a portion of the sales comes from inventory or a

17–2.

False. Variances simply represent differences between plans and actual outcomes.

17–3.

Variances are usually “expensed” as a period cost (e.g., charged to Cost of Goods Sold).

17–4.

17–5.

17–6.

17–7.

17–8.

Examples include:

• Steel mills which can process both new steel and recycled scrap

17–9.

The concept of management by exception suggests managers not focus on things that are

Solutions to Critical Analysis and Discussion Questions

17–10.

By recognizing the materials price variance at the time of purchase, management

captures any difference between actual materials cost and the standard costs as reflected

17–11.

17–12.

17–13.

In a hospital, as in other professional firms, billing rates vary with the level of the

17–14.

Salary rates vary according to the classification of the service providers (e.g., nurses’ pay

is higher than nurse practitioners’ pay), and the hospital will budget a certain amount of

17–15.

Disagree. The purpose of variance analysis is to identify items that are different from what

17–16.

Answers will vary. Variance analysis is helpful in any setting where budgets are

calculated, including business schools (and other academic institutions). In addition to the

17–17.

Answers will vary. A company such as Uber with several services (Uber-X, Uber-Black,

and so on), would likely learn something from sales activity and mix. Whether they would

Solutions to Exercises

17–18. (15 min.) Variable Cost Variances: Materials Purchased And Used Are Not

Equal: Gates Corporation.

Actual

Costs

Price

Variance

Actual

Inputs at

Standard

Price

Efficiency

Variance

Flexible

Budget

(Standard

Allowed for

Good Output)

Purchase

Computations

$673,000

$688,000

= $440,000

17–19. (15. Min) Variable Cost Variances: Materials Purchased And Used Are Not

Equal: Mathis, Inc.

Actual

Costs

Price

Variance

Actual

Inputs at

Standard

Price

Efficiency

Variance

Flexible

Budget

(Standard

Allowed for

Good Output)

Computations

= $1,442,000

Purchase

$1,642,800

$1,554,000

17–20. (15 min.) Industry Volume And Market Share Variances: D&B Ice Cream.

Flexible Budget

(SCM x AQ)

Market

Share

Variance

Standard Contribution

Margin Times

Budgeted Market

Share Times Actual

Industry Volume

(SCM x ASQ)

Industry

Volume

Variance

Master Budget

(SCM x SQ)

17–21. (20 min.) Industry Volume And Market Share Variances—Missing Data.

17–22. (20 min.) Industry Volume And Market Share—Missing Data.

17–23. (20 min.) Sales Mix And Quantity Variances: A-Zone Media.

a. and b.

The actual prices are not relevant here. The mix and quantity variances are based on

standard (budgeted) contribution margin per unit.

Flexible Budget

AQ x (SP – SV)

Mix

Variance

ASQ x (SP – SV)

Quantity

Variance

Master Budget

7,500 x ($192 – $80)

11,500 x (10,000/12,500) x ($192 – $80)

17–24. (20 min.) Sales Mix And Quantity Variances: Sara’s Systems.

a. and b.

Flexible Budget

AQ x (SP – SV)

Mix

Variance

ASQ x (SP – SV)

Quantity

Variance

Master Budget

26,400 x ($200 – $80)

33,600 x (22,500/30,000) x ($200 – $80)

22,500 x ($200 – $80)

17–25. (20 min.) Sales Mix And Quantity Variances: Hotel Galaxy.

a. and b.

Flexible Budget

AQ x (SP – SV)

Mix

Variance

ASQ x (SP – SV)

Quantity

Variance

Master Budget

1,350 x ($35 – $15)

2,300 x (1,000/2,500) x ($35 – $15)

1,000 x ($35 – $15)

17–26. (20 min.) Sales Mix And Quantity Variances: Chow-4-Hounds.

a. and b.

Flexible Budget

AQ x (SP – SV)

Mix

Variance

ASQ x (SP – SV)

Quantity

Variance

Master Budget

60,000 x ($12 – $5)

210,000 x (60,000/200,000) x ($12 – $5)

60,000 x ($12 – $5)

17–27. (35 min.) Materials Mix and Yield Variances: Stacy, Inc.

a. and b.

Efficiency Variance

Actual

(AP x AQ)

Purchase

Price

Variance

(SP x AQ)

Mix

Variance

(SP x ASQ)

Yield

Variance

Flexible

Production

Budget (SP

x SQ)

Material:

$4.50 x

= $7.50 x 160,000

Total

17–28. (35 min.) Materials Mix and Yield Variances: John’s Weed-B-Gone.

a. and b.

The actual purchase prices were $9.80 (= $35,280 ÷ 3,600) for Weed-X and $24.00 (=

$72,000 ÷ 3,000) for Pest-O.

Efficiency Variance

Actual

(AP x AQ)

Purchase

Price

Variance

(SP x AQ)

Mix

Variance

(SP x ASQ)

Yield

Variance

Flexible

Production

Budget

(SP x SQ)

Material:

Weed-X

3,600

= $35,280

= $36,000

= $72,000

= $75,000

$10 x (0.005 a

Total

17–29. (35 min.) Labor Mix and Yield Variance: Matt’s Eat ‘N Run.

a. and b.

Efficiency Variance

Actual

(AP x

AQ)

Purchase

Price

Variance

(SP x AQ)

Mix

Variance

(SP x

ASQ)

Yield

Variance

Flexible

Production

Budget

(SP x SQ)

Labor:

Skilled

= $120,000

Unskilled

Total

$270,000

$20 x (0.25 x 21,000)

$20 x (2/60 x 180,000)

17–30. (10 min.) Flexible Budgeting—Service Organization: K&B.

Flexible Budget

(based on

actual of

7,200 hours)

Revenue ………………………….

$648,000a

Costs:

17–31. (20 min.) Sales Activity Variance—Service Organization: K&B.

Flexible Budget

(based on

actual of

7,200 hours)

Sales

Activity

Variance

Master Budget

(based on

budgeted 9,000

hours)

$616,000

17–32. (30 min.) Profit Variance Analysis—Service Organization: K&B.

(1)

(2)

(3)

(4)

(5)

(6)

Actual

(7,200 hrs.)

Cost

Variances

Price

Variances

Flexible

Budget

(7,200 hrs.)

Sales

Activity

Variance

Master

Budget

(9,000 hrs.)

Revenue ……………………….

$670,000

$22,000 F

$648,000

$162,000 U

$810,000

Fixed costs ……………………

17–33. (20 min.) Sales Price and Activity Variances: EZ-Tax.

Actual

(AP x AQ)

Price Variance

Flexible Budget

(SP x AQ)

Partner

$4,264,000

$800 x 5,200 hours

= $4,160,000

$4,510,000

= $4,620,000

Flexible

Budget

Master Budget

AQ x (SP – SV)

Mix Variance

(SP – SV) x ASQ

Quantity

Variance

SQ x (SP – SV)

= $3,925,000

Activity Variance

5,200 x ($800 – $375) +

[$425a x (5,000 ÷ 25,000) x 27,200] +

5,000 x $425 +

17–34. (10 min.) Variable Cost Variances: Harry’s Hotel.

Actual Costs

Price

Variance

Actual Inputs at

Standard Price

Efficiency

Variance

Flexible Budget

(Standard

Allowed)

17–35. (10 min.) Investigating Variances: Harry’s Hotel.

Answers will vary. Clearly, the price variance is much larger than the efficiency variance

Solutions to Problems

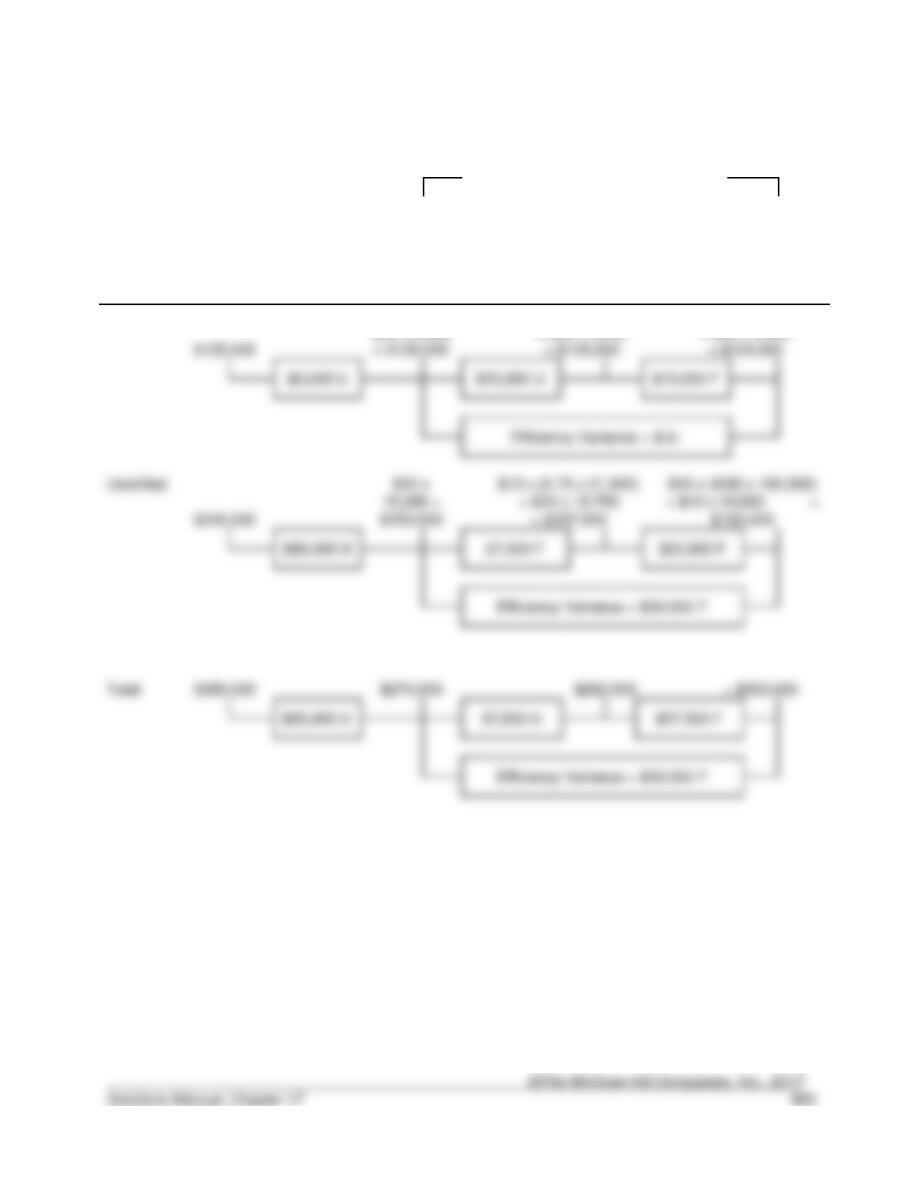

17–36. (20 min.) Variable Cost Variances: Materials Purchased And Used Are Not

Equal: Griffen Company.

Actual Costs

Price

Variance

Actual

Inputs at

Standard

Price

Efficiency

Variance

Flexible Budget

(Standard

Allowed for

Good Output)

($5.30 x

($5.00 x

Notes:

* Given.

a. Material purchase price variance = AQ (purchased) x ($5.30 – $5.00) = $34,590;

17–37. Sales Mix And Quantity Variances: Lake Cellars.

a. Price Variance = (Actual Price − Budgeted Price) x Actual Quantity:

Variety:

Price

Variance

=

(Actual Price − Budgeted Price)

x

Actual Quantity

Flexible Budget

AQ x (SP – SV)

Mix

Variance

ASQ x (SP – SV)

Quantity

Variance

Master Budget

22,000 x ($9.00 – $6.00)

42,000 x (20,000/40,000) x ($9.00 – $6.00)

20,000 x ($9.00 – $6.00)

17–38. (40 min.) Analyze Performance for a Restaurant: Doug’s Diner.

Hint for working the problem: Use sales revenue as the basis for measuring volume.

($000)

Actual

Purchases

Variances

Marketing &

Administrative

Variances

Flexible

Budget

Activity

Variance

Master

Budget

Sales revenuea …………………………………………..

$1,200

$1,200

$200 F

$1,000

Variable costs:

Purchases……………………………………………….

780

$60 U

720

b

120 U

600

Franchise fee …………………………………………..

Utilities ……………………………………………………

e

14 U

Total variable costs ……………………………………..

$60 U

$900

Contribution margin ……………………………………..

$60 U

$300

$ 50 F

Fixed costs: ……………………………………………….

Advertising ………………………………………………

100

100

100

Lease ……………………………………………………..

Salaries…………………………………………………..

Total fixed costs ………………………………………….

17-37. (continued)

a Sales revenue is used as the basis of volume measurement because there are no price changes.

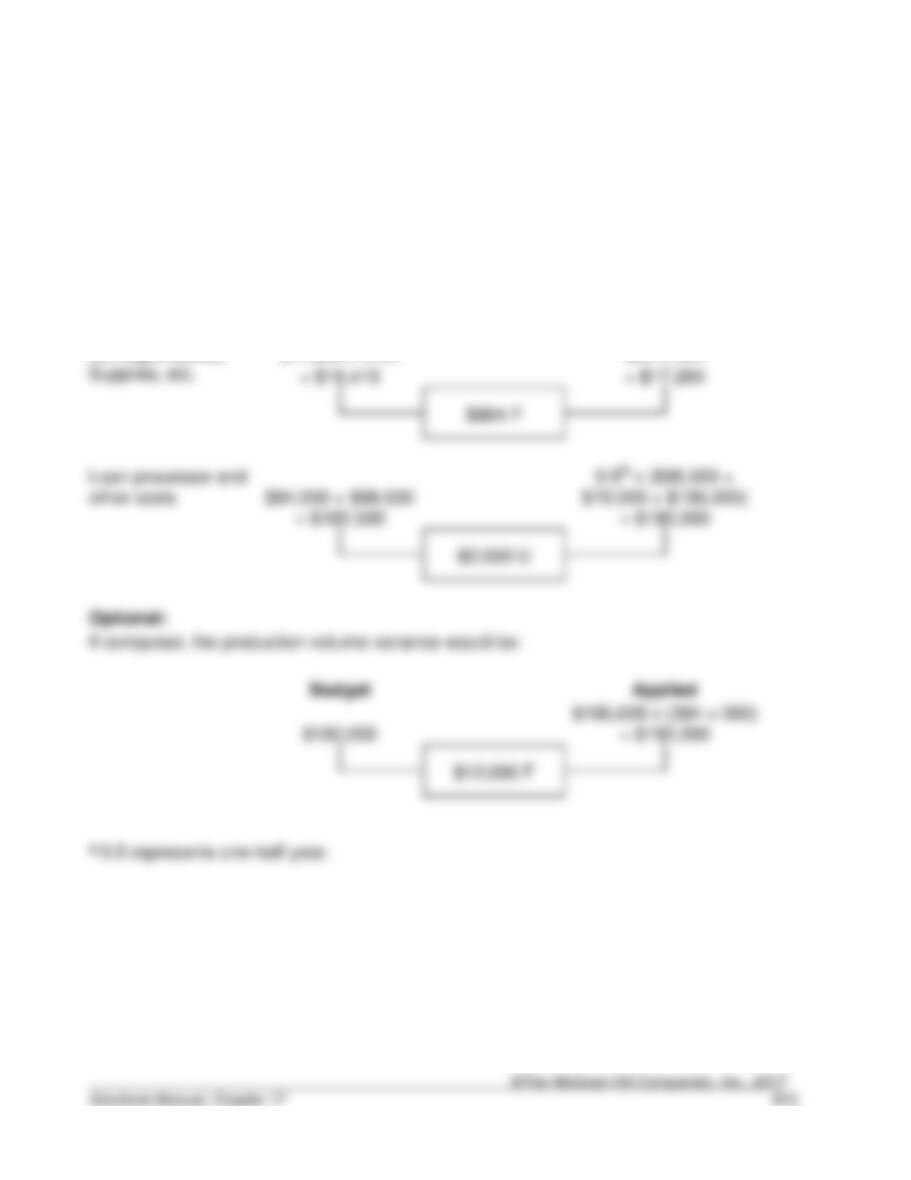

17–39. (30 min.) Nonmanufacturing Cost Variances: FSBCU.

Incidental office costs comprise the variable costs. Salaries and the fixed office costs are

all fixed. Variance analysis for the two classes of overhead is as follows:

Actual Costs

Combined

Price and

Efficiency

Variance

Flexible Budget

(Standard Allowed

for Actual Output)

Correspondence,

$17,280 x 0.95

$45 x 384

17–40. (30 min.) Performance Evaluation In Service Industries: Bay Area Bank.

Actual

Costs

Price

Variance

Actual

Inputs at

Standard

Price

Efficiency

Variance

Flexible

Budget

Activity

Variance

Master

Budget

(Ignored)

$600,000

= $20,250

New

$30 x

$30 x

17–41. (10 min.) Investigating Variances: Bay Area Bank.

Answers will vary. From the variance analysis above, it would be useful to better

17–42. Revenue Analysis Using Industry Data and Multiple Product Lines: Peninsula

Candy Co.

a. Sales price and activity variances.

Flexible

Master

budget

budget

(AP – SV) x AQ

(SP – SV) x AQ

(SP – SV) x SQ

a Unit contribution margins calculated from master budget panel as follows:

b. Two solutions are possible when calculating the market share variance, depending

17-42b. (continued)

Contribution margin variance

Actual Quantities at

Standard Mix and

Industry

Master

Standard Prices

Effect

Budget

$280 x (76,000 ÷ 80,000)

$273a

= $266

$280

$7 F

$14 U

Variance

$7 U

Quantity

Variance

Master Budget

$275

$9 F

$14 U

Activity Variance

The $2 difference in the market share variance is explained by the difference in the mix.

17–43. (20 min.) Sales Mix And Quantity Variances: Peninsula Candy Co.

Flexible Budget

Mix

Variance

Quantity

Variance

Master Budget

(SP – SV) x AQ

(SP – SV) x ASQ

(SP – SV) x SQ

8,000

8,000

8,000

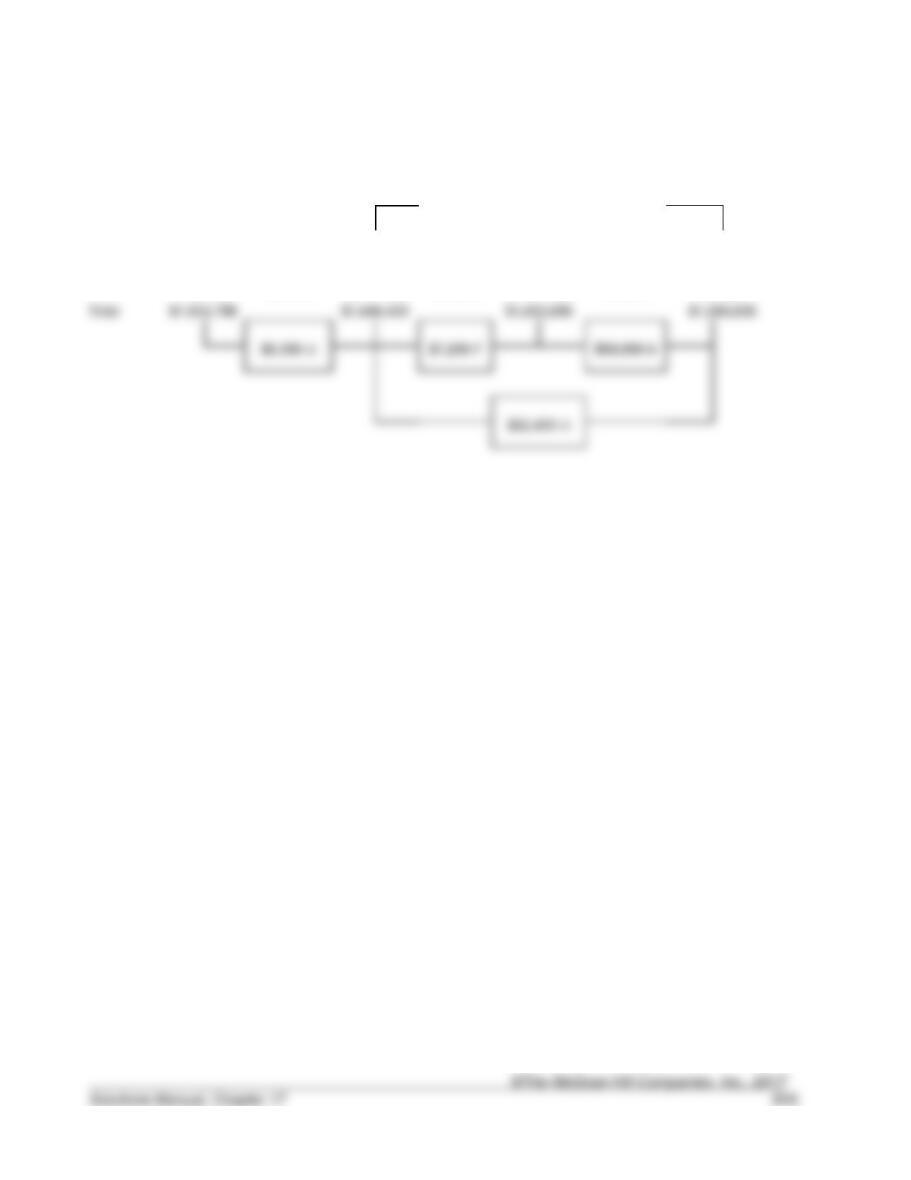

17–44. (45 min.) Materials Mix And Yield Variances: Plano Products.

a. and b.

Efficiency Variance

Material

Actual

(AP x

AQ)

Purchase

Price

Variance

(SP x AQ)

Mix

Variance

(SP x ASQ)

Yield

Variance

Flexible

Production

Budget

Chem-A

$9 x

$9 x (.16a x

104,400) =

$9 x (20 x 800b)

17-44. (continued)

Efficiency Variance

Actual

Purchase

Price

Variance

(SP x AQ)

Mix

Variance

(SP x ASQ)

Yield

Variance

Flexible

Production

Budget

Total

$1,654,788

17–45. (30 min.) Labor Mix and Yield Variances: Matthews & Bros.

a. and b.

Efficiency Variance

Actual

Purchase

Price

Variance

(SP x AQ)

Mix

Variance

(SP x ASQ)

Yield

Variance

Flexible

Production

Budget

17–46. (10 min.) Investigating Variances: Matthews & Bros.

Answers will vary. From the variance analysis above, the purchase price variance is fairly

17–47. (20 min.) Derive Amounts for Profit Variance Analysis: Classics Ltd.

Hint: Use last quarter’s actual as master budget.

Actual (based

on actual

activity of

483

detailings)

Variable

Cost

Variance

Sales

Price

Variance

Flexible Budget

(based on

actual activity

of 483

detailings)

Sales

Activity

Variance

Master Budget

(based on a

prediction of

420 detailings)

Sales revenue …………………………………………….

$68,400

$9,846 U

$78,246

a

$10,206 F

$68,040

Less:

Contribution margin ……………………………………..

$37,080

$558 F

$9,846 U

$46,368

$40,320

17–48. (20 min.) Flexible budget: Oak Hill Township.

Flexible budget is based on actual activity of 94,500 miles for costs that vary per mile.

Solutions to Case

17–49. Comprehensive Overview of Budgets and Variances Racketeer, Inc.

The following solution is based on a report by Tom Terpstra.

Elmo’s problem is that he thinks that the graph and the income statement measure the

same thing. Otto should have told him that they do not. The income statement presents

actual costs in a full-absorption costing format, while the profit graph is based on standard

costs in a variable costing format. These differences account for the difference in the profit

measurement.

The overhead amount differs from the figure on the income statement, because the

income statement overhead variance includes a production volume variance of $470

17-49. (continued)

Now the two results can be reconciled:

Profit per chart …………………………………………….

$20,940

Less:

Profit per Income Statement ………………………….

17-49. (continued)

Exhibit A Comparison of Master Budget to Actual Results.

Actual

Manufacturing

Variance

Selling and

Administrative

Variance

Sales Price

Variance

Flexible

Budget

Activity

Variance

Master

Budget

Sales revenue ……………………..

$90,000

–0–

–0–

$90,000

$18,000

F

$72,000

Less Variable Costs:

19,392

U

U

U

U

Contribution Margin ………………

$31,178

$1,022

U

–0–

–0–

$32,200

$6,440

F

$25,760

Less Fixed Costs:

17-49. (continued)

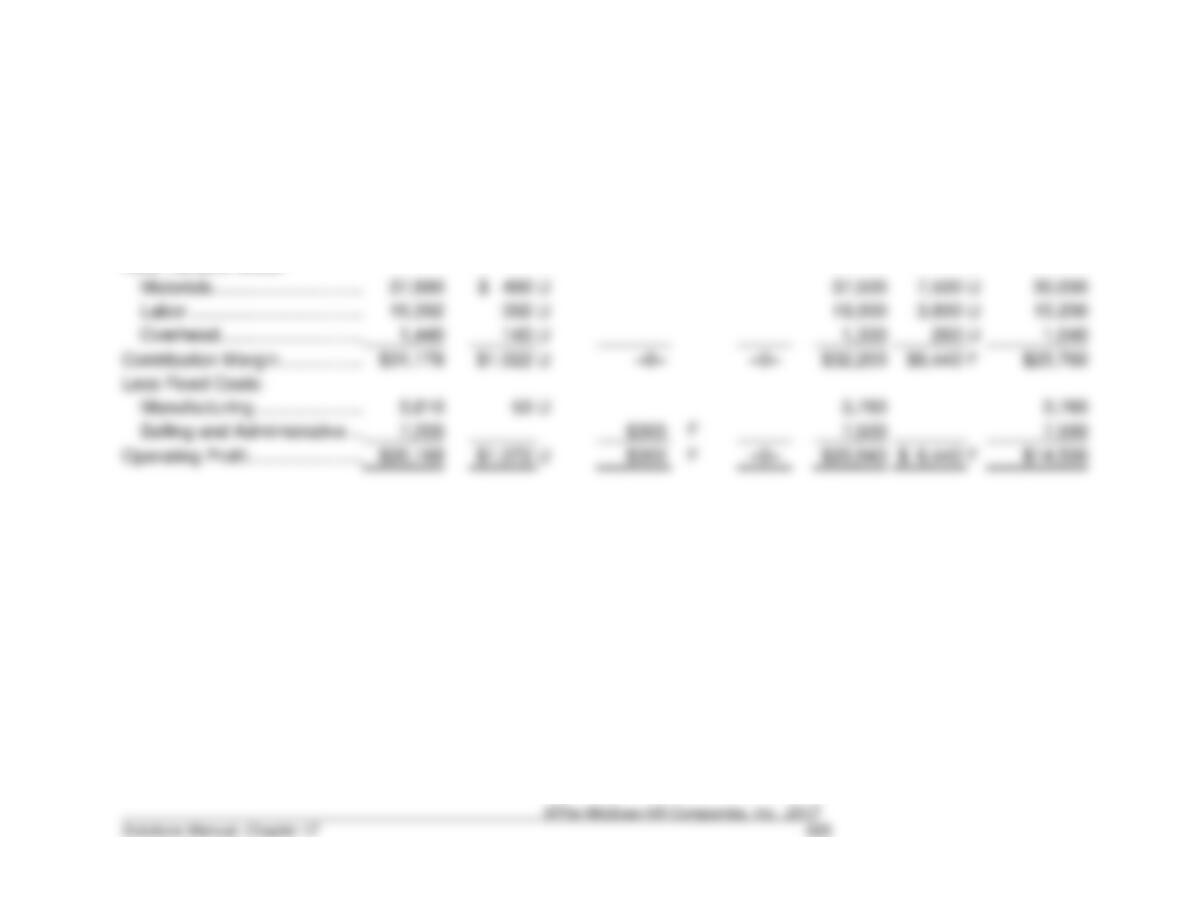

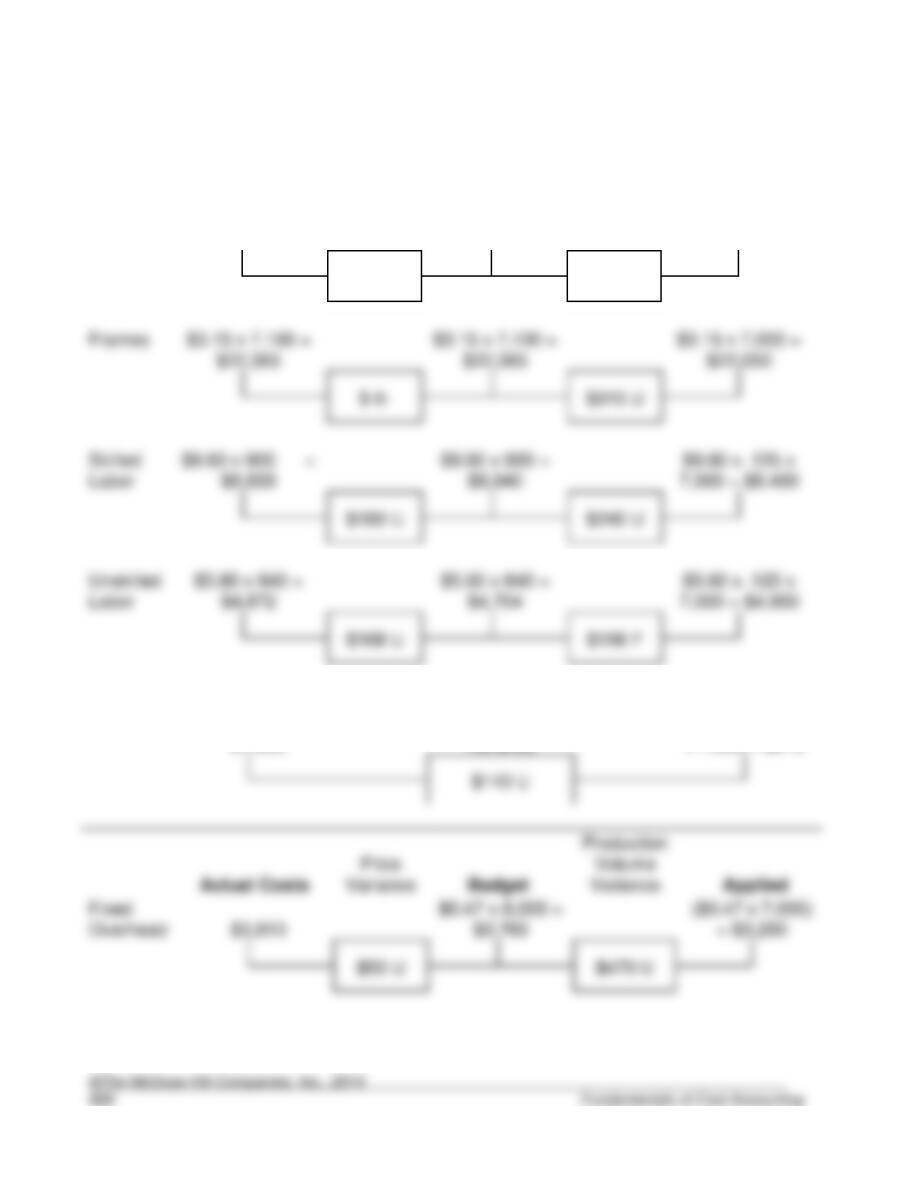

Exhibit B Manufacturing Cost Variances.

Actual Costs

Price

Variance

Actual Inputs

at Standard

Price

Efficiency

Variance

Flexible Budget

String

$0.025 x 175,000

= $4,375

$0.03 x 175,000

= $5,250

$0.03 x 20 x

7,000 = $4,200

$875 F

$1,050 U

Frames

Skilled

Labor

7,000 = $8,400

Unskilled

Labor

7,000 = $4,900

$196 F

Variable

Overhead

$1,050

Total Variable

Overhead

Variance

($0.10 + $.03)

x 7,000 = $910

Actual Costs

Variance

Fixed

Overhead

17-49. (continued)

The variance breakdown in Exhibits A and B highlights the areas that Elmo and Otto

should research. One area involves the strings. Is the combination of a favorable price

variance and unfavorable efficiency variance an indicator that low quality string was