Prob. 18–3B (FINMAN); Prob. 3–3A (MAN)

1.

Whole Direct

UNITS Units Materials Conversion

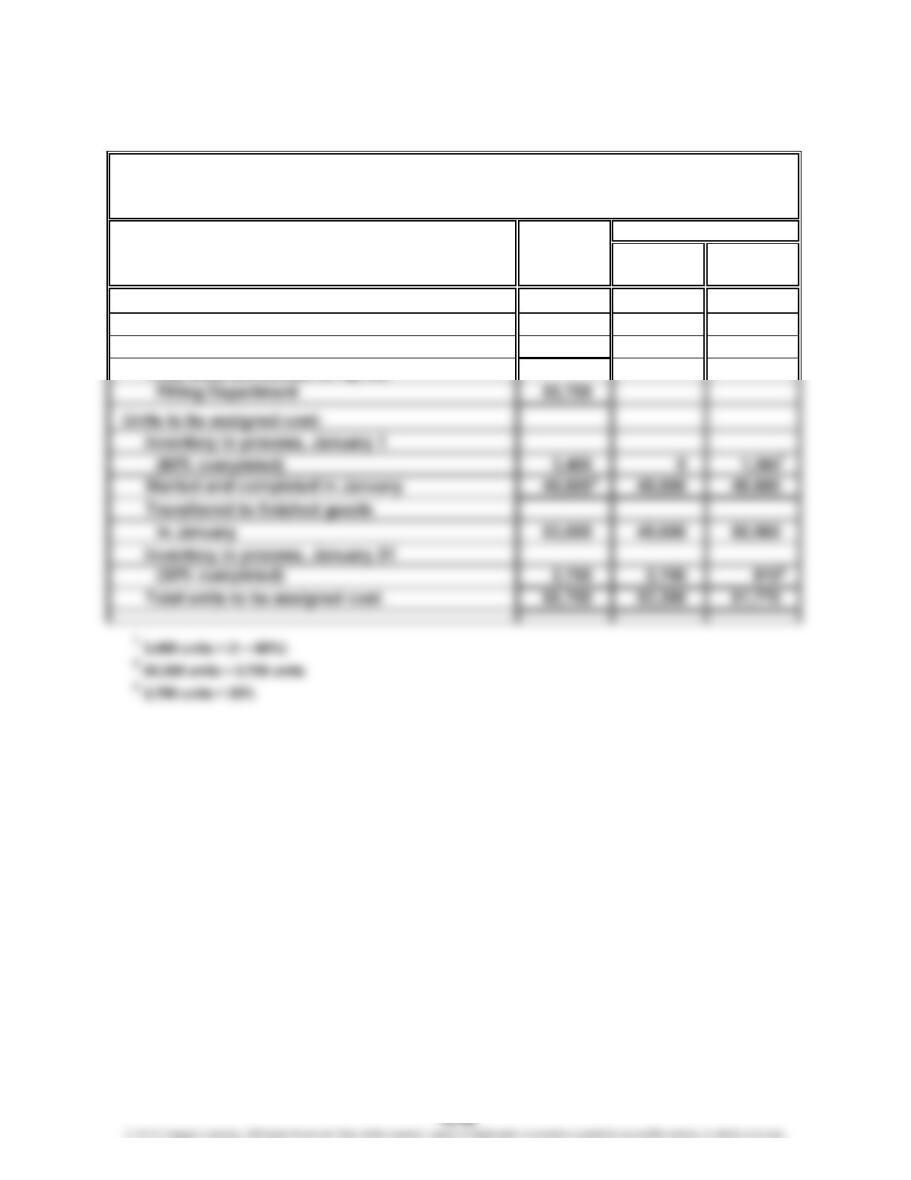

Units charged to production:

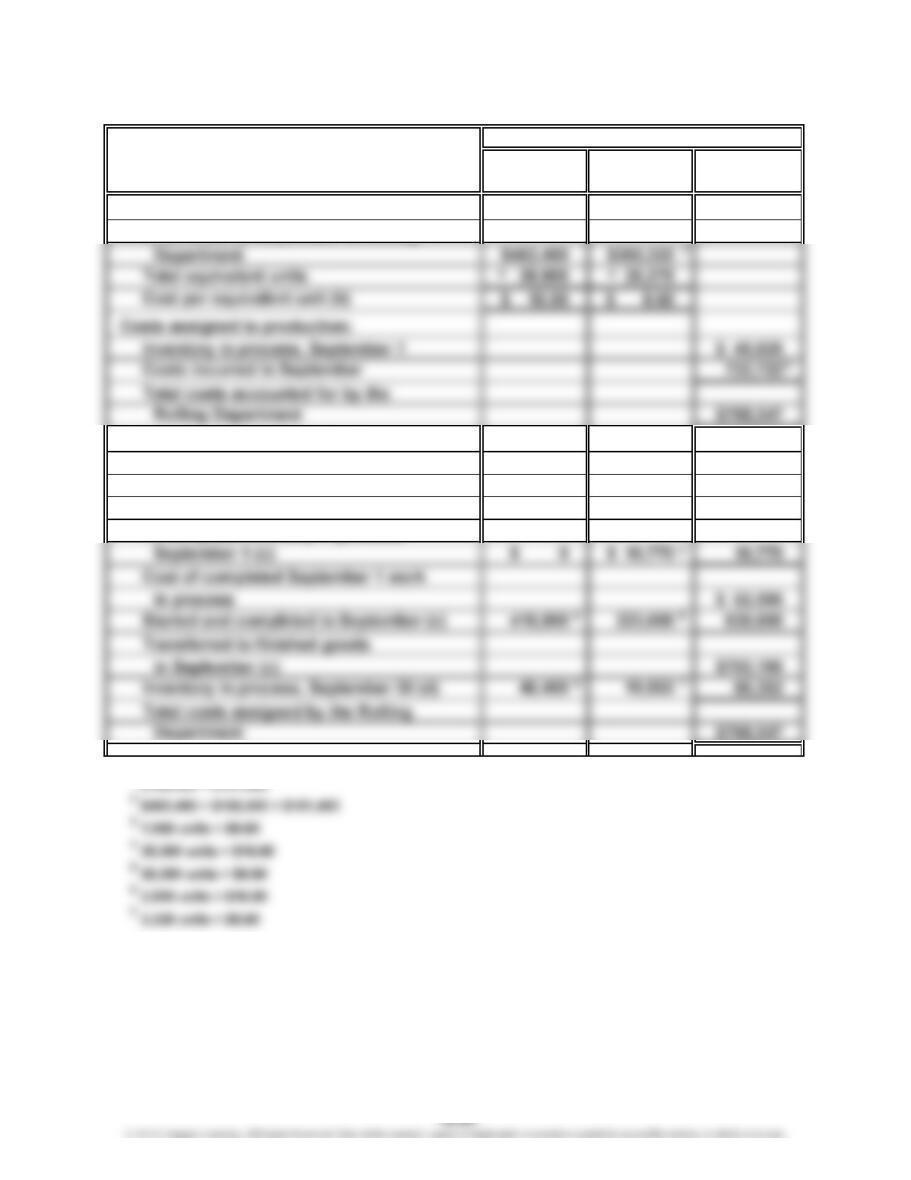

Inventory in process, January 1 3,400

Received from Reaction Department 52,300

Total units accounted for by the

DOVER CHEMICAL COMPANY

Cost of Production Report—Filling Department

For the Month Ended January 31, 2012

Equivalent Units

Prob. 18–3B (FINMAN); Prob. 3–3B (MAN) (Continued)

Direct

COSTS Materials Conversion Total

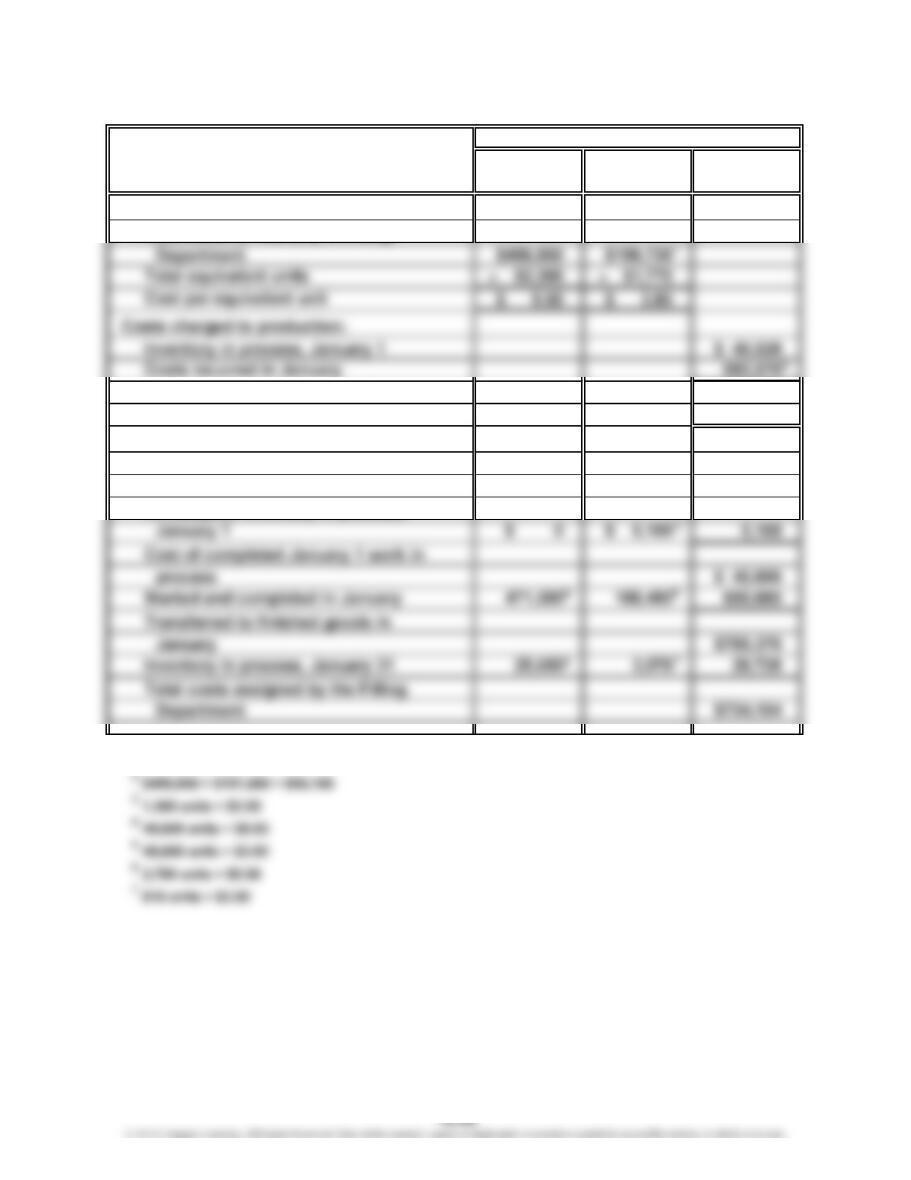

Costs per equivalent unit:

Total costs for January in Filling

Total costs accounted for by the

Filling Department $734,104

Cost allocated to completed and

partially completed units:

Inventory in process, January 1 balance $ 40,528

To complete inventory in process,

1$101,560 + $95,166

Costs

Prob. 18–3B (FINMAN); Prob. 3–3B (MAN) (Concluded)

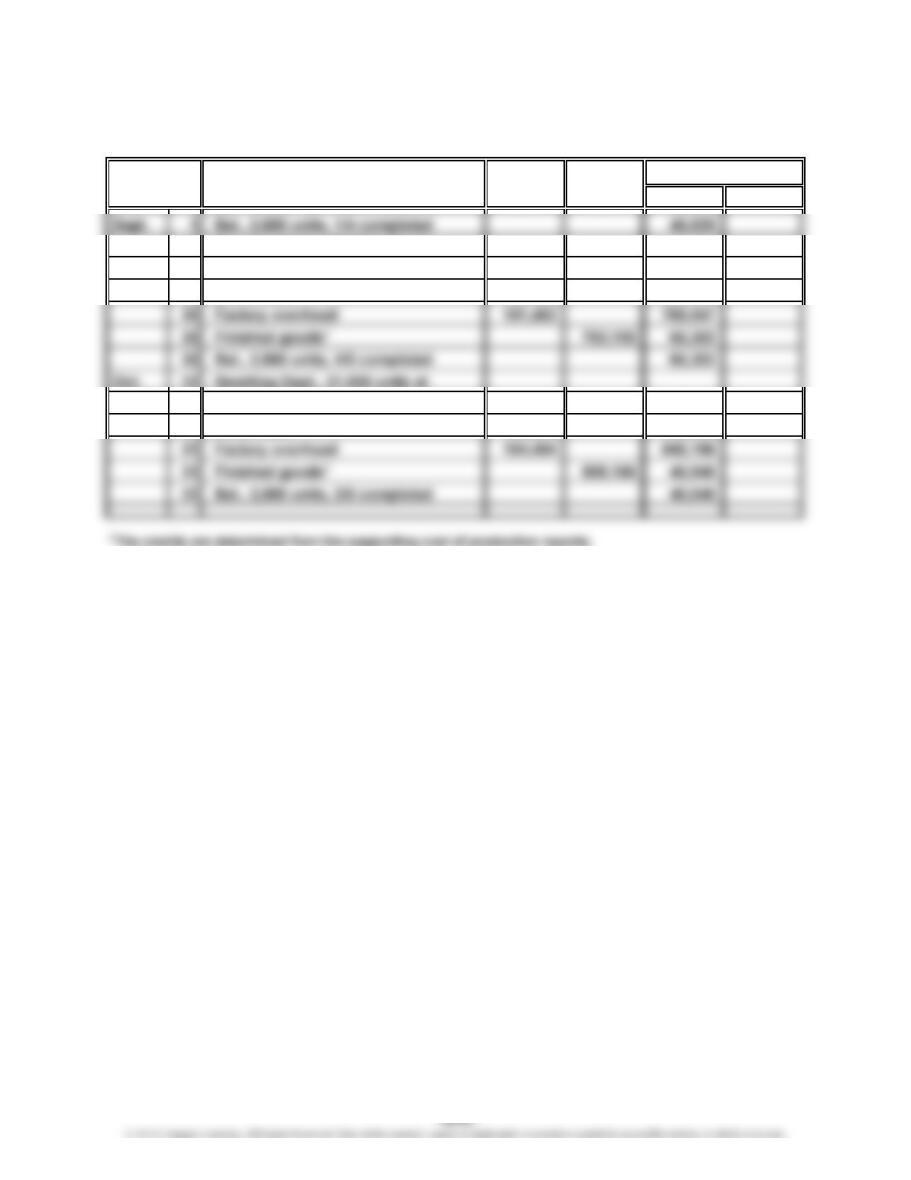

2. Work in Process—Filling Department 496,850

Work in Process—Reaction Department 496,850

4. The cost of production report may be used as the basis for allocating product

costs between Work in Process and Finished Goods. The report can also be

Prob. 18–4B (FINMAN); Prob. 3–4B (MAN)

1. and 2.

Item Dr. Cr. Dr. Cr.

30 Smelting Dept., 28,900 units at

$16.00/unit 462,400 508,225

30 Direct labor 158,920 667,145

$16.50/unit 511,500 577,852

31 Direct labor 162,850 740,702

Date

Balance

Work in Process—Rolling

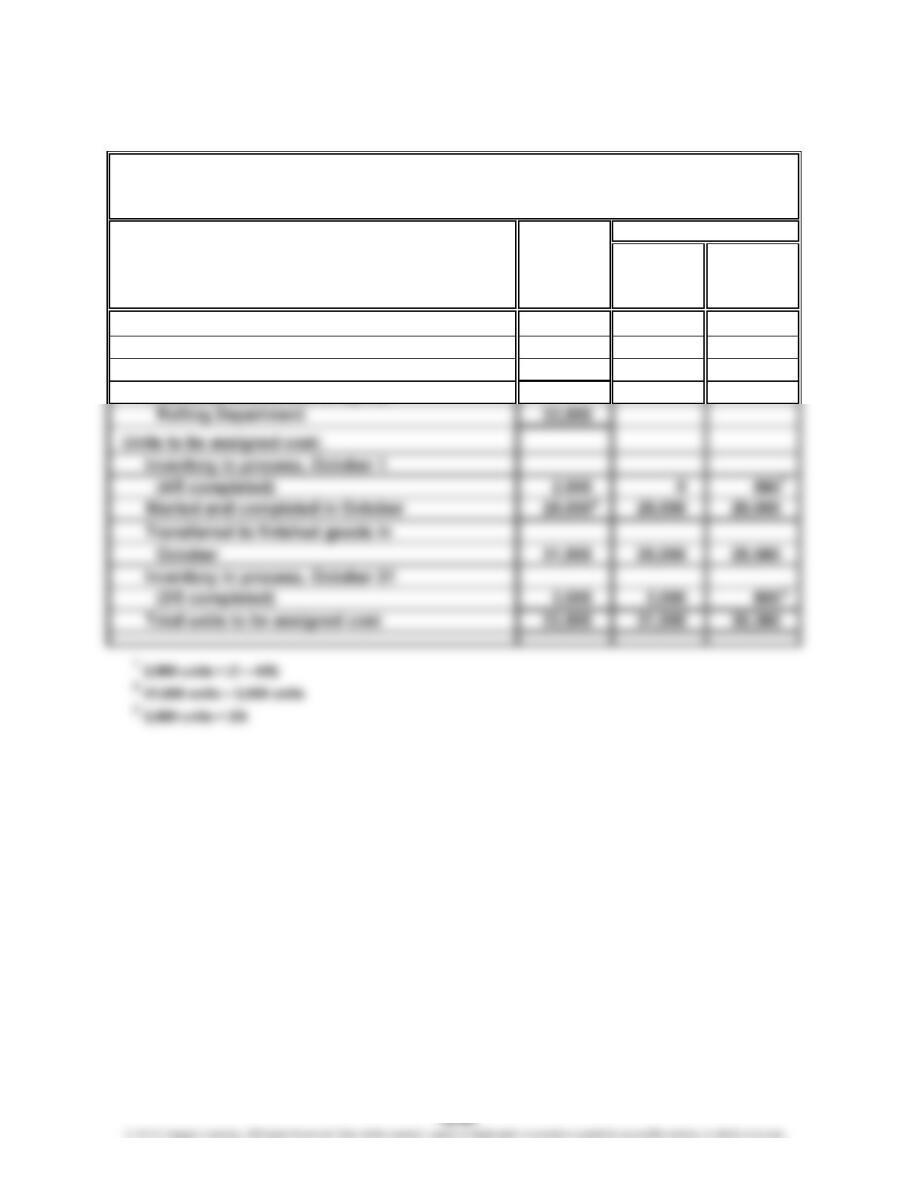

Prob. 18–4B (FINMAN); Prob. 3–4B (MAN) (Continued)

Whole Direct

UNITS Units Materials Conversion

(a) (a)

Units charged to production:

Total units accounted for by the

Rolling Department 31,500

Units to be assigned cost:

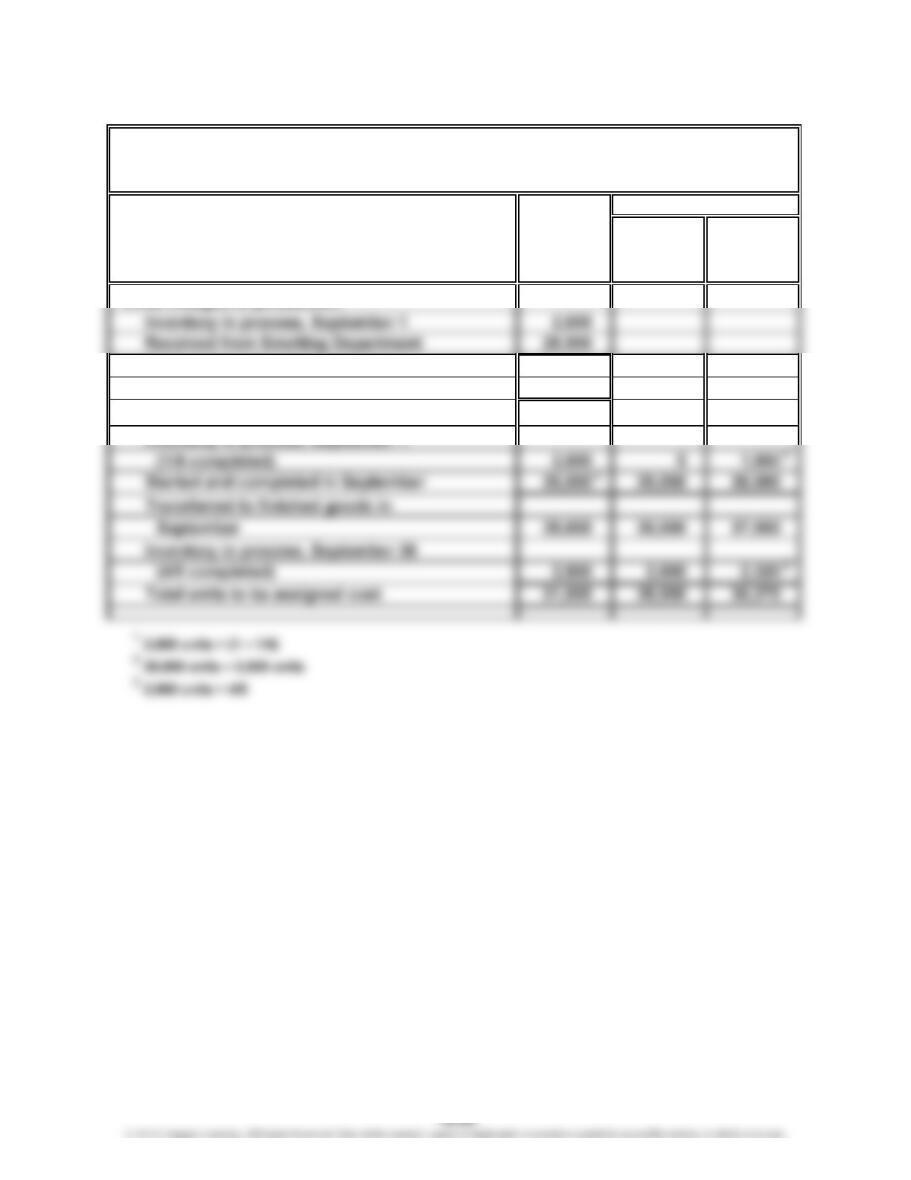

Inventory in process, September 1

PITTSBURGH ALUMINUM COMPANY

Cost of Production Report—Rolling Department

For the Month Ended September 30, 2014

Equivalent Units

Prob. 18–4B (FINMAN); Prob. 3–4B (MAN) (Continued)

Direct

COSTS Materials Conversion Total

Costs per equivalent unit:

Total costs for September in Rolling

Cost allocated to completed and

partially completed units:

Inventory in process, September 1

balance (c) $ 45,825

To complete inventory in process,

1$158,920 + $101,402

Costs

Prob. 18–4B (FINMAN); Prob. 3–4B (MAN) (Continued)

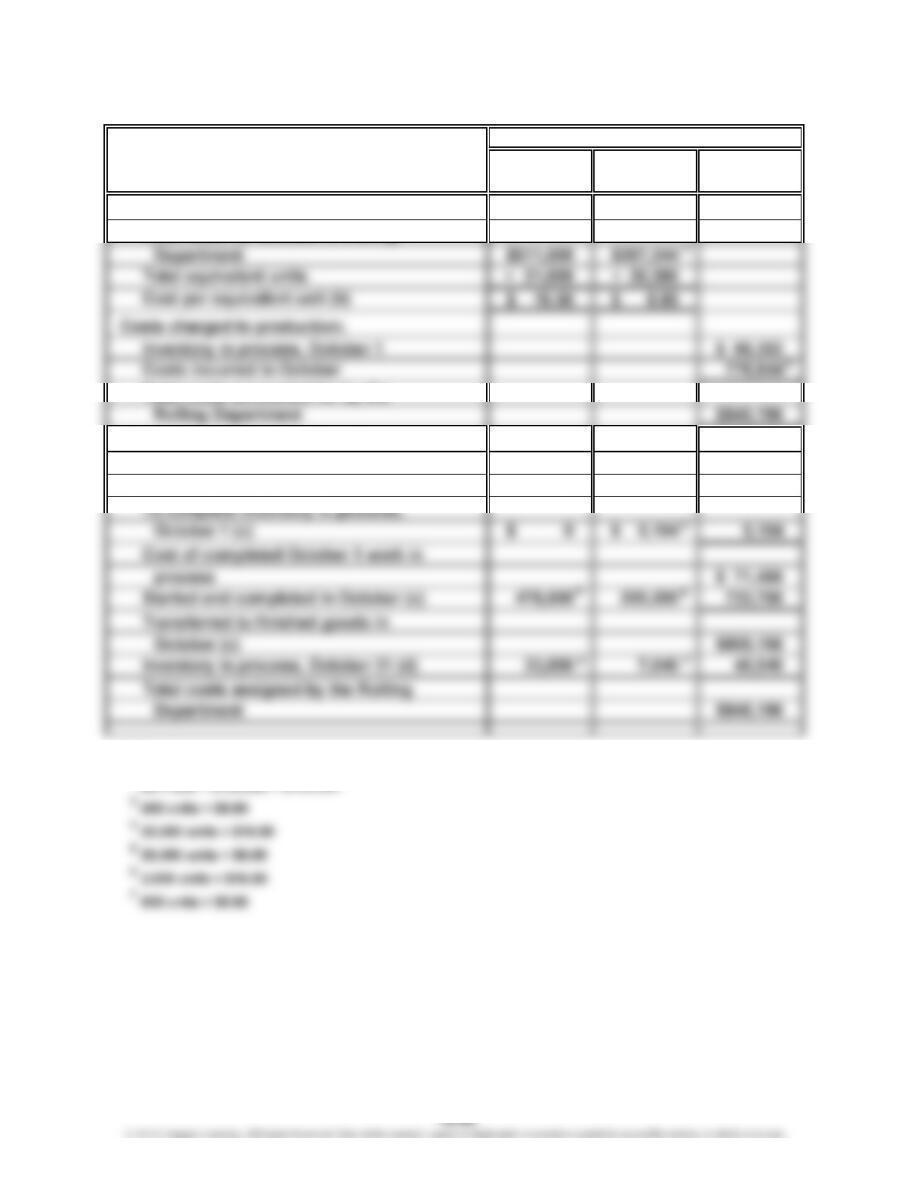

2.

Whole Direct

UNITS Units Materials Conversion

(a) (a)

Units charged to production:

Inventory in process, October 1 2,900

Received from Smelting Department 31,000

Total units accounted for by the

PITTSBURGH ALUMINUM COMPANY

Cost of Production Report—Rolling Department

For the Month Ended October 31, 2014

Equivalent Units

Prob. 18–4B (FINMAN); Prob. 3–4B (MAN) (Concluded)

Direct

COSTS Materials Conversion Total

Costs per equivalent unit:

Total costs for October in Rolling

Total costs accounted for by the

Cost allocated to completed and

partially completed units:

Inventory in process, October 1 balance (c) $ 66,352

1$162,850 + $104,494

2$511,500 + $162,850 + $104,494

Costs

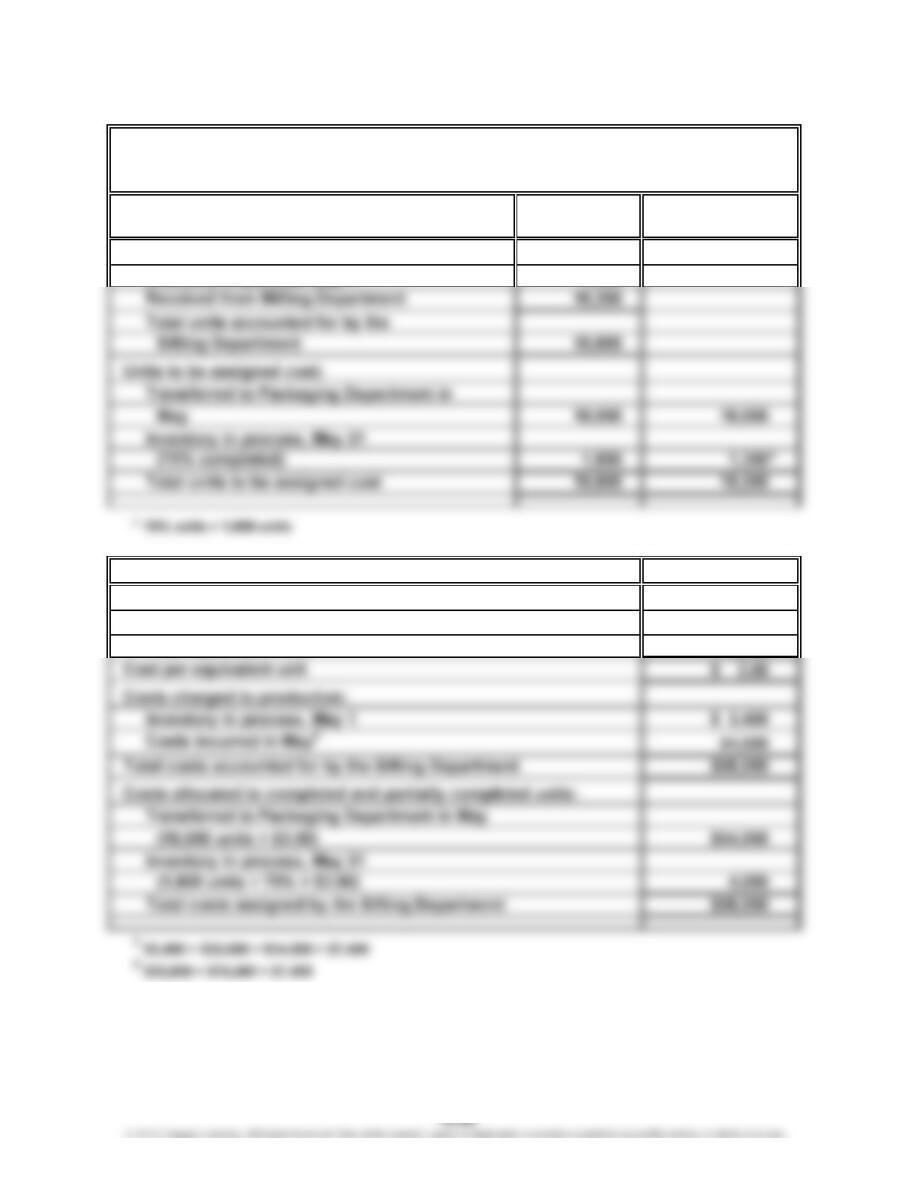

Appendix Prob. 18–5B (FINMAN); Appendix Prob. 3–5B (MAN)

Whole Equivalent Units

UNITS Units of Production

Units charged to production:

Inventory in process, May 1 1,500

COSTS Costs

Unit costs:

Total costs for May in Sifting Department1$58,050

Total equivalent units 19,350

BLUE RIBBON FLOUR COMPANY

Cost of Production Report—Sifting Department

For the Month Ended May 31, 2014

÷

CP 18–1 (FINMAN); CP 3–1 (MAN)

This case comes from a real story. In the real story, the first reduction in chips had

no impact on the marketplace. The manager was promoted, and the next manager

attempted the same strategy—reduce chips by 10%. Again, it worked. The next

manager did the same thing. All of a sudden, the market demand dropped for the

cookie. A threshold was reached, and the cookie was in trouble in the marketplace.

The current cookie was nothing like the original recipe. The cookie’s integrity was

slowly eroded until it wasn’t “Full of Chips.” Senior management had no idea this was

happening, since it occurred slowly over a period of many years. Now, with respect

to the controller, there are a number of options.

a. Do nothing. This is a safe strategy. It would be highly unlikely that failing to

reveal this information to anybody would ever be discovered or “pinned” on

b. Talk to Bishop. You can have a conversation with Bishop. This is also a

reasonably safe strategy and probably the best start. For example, you may

without any risk through a personal conversation with Bishop.

c. Talk to the vice president. You could also go right over Bishop’s head to the

vice president. This strategy might label you as “not a team player,” so some

care is in order here. You might get Bishop in trouble, or you may get yourself

CASES & PROJECTS

CP 18–2 (FINMAN); CP 3–2 (MAN)

a. This accounting procedure has the effect of rewarding the production of

broke. In essence, the procedure communicates to operating personnel that

broke is a normal part of doing business. In fact, not only is broke a normal

b. The accounting for broke that is typical in the industry fails to account for the

total impact of broke. It is true that the use of recycled materials may reduce the

direct materials cost to the operation. However, such a view is very limited. For

example, the production of broke has a cost. Machine capacity was used to

CP 18–3 (FINMAN); CP 3–3 (MAN)

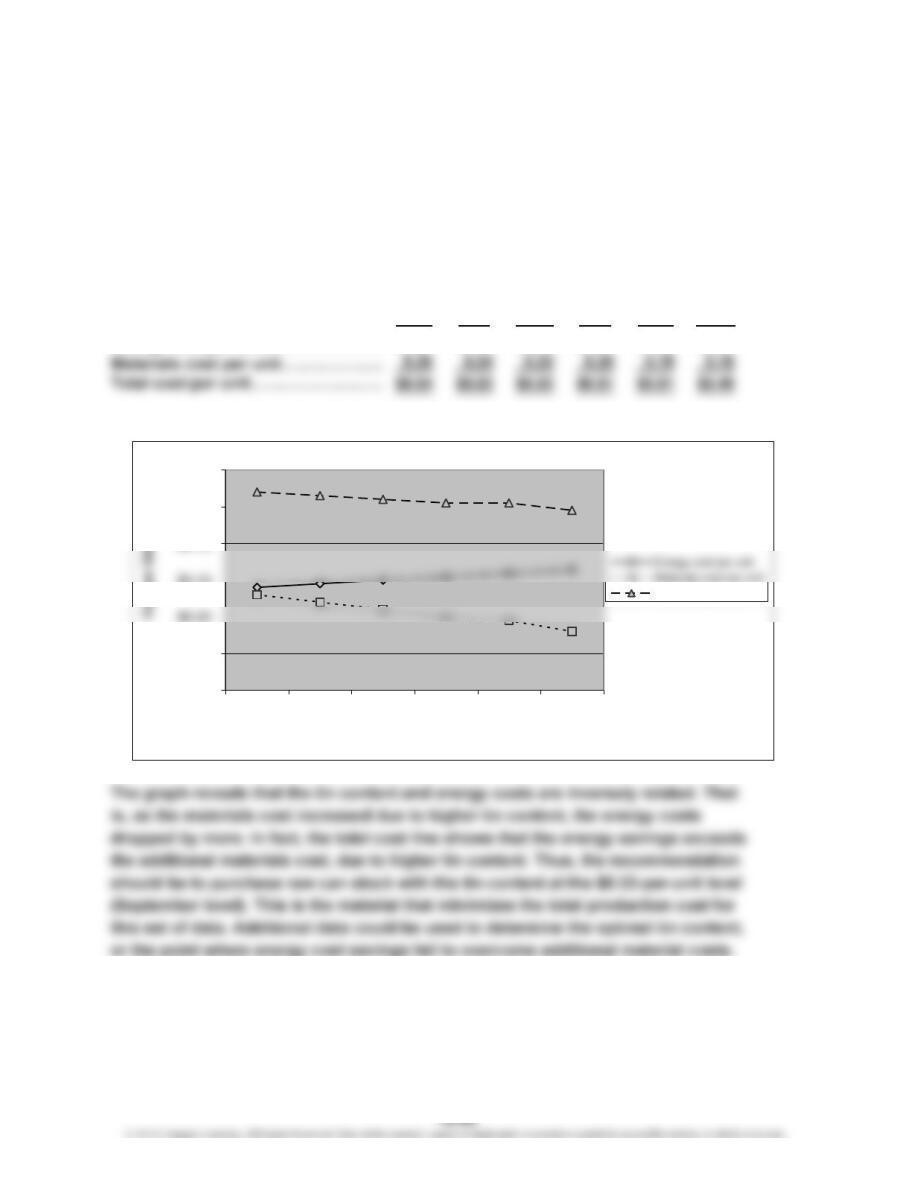

This case is abstracted from a real situation, where higher raw materials costs due

to tin content were more than offset by lower energy costs. The cost system used

in the real situation was a sophisticated “real-time” expense tracking system. The

subtlety of this trade-off analysis is impressive.

The first step is to translate the monthly materials and energy costs into their

respective costs per unit of monthly production. In this way, the costs can be

compared across the months.

April May June July Aug. Sept.

Energy cost per unit…………………

…

$0.28 $0.29 $0.30 $0.31 $0.32 $0.33

The graph below shows the total unit cost data for each month.

$0.00

$0.10

$0.30

$0.40

$0.50

$0.60

April May June July Aug. Sept.

Month

Total cost per unit

…

…

CP 18–4 (FINMAN); CP 3–4 (MAN)

To: Jamarcus Bradshaw

From: Leann Brunswick

Re: Analysis of August Increase in Unit Costs for Papermaking Department

July August

Materials cost per ton……………………………………

…

$246.33 $269.12

…

An analysis was done to isolate the cause of the increased cost per ton. My

interviews indicated that there were two possible causes. First, we changed the

specification of the green paper in early August. This may have altered the way

the paper machines process the green paper. Thus, it is possible that the paper

Fortunately, we run both colors on paper machine No. 1. Thus, we can separate

the analysis between these two possible explanations. I have provided the

following cost per ton data for the two paper machines and the two product

colors:

Paper machine analysis:

Materials Conversion

Cost per Ton Cost per Ton Total

Paper Machine No. 1…………………

…

$290.54 $143.04 $433.58

…

…

Product color analysis:

Materials Conversion

Cost per Ton Cost per Ton Total

Green……………………………………

…

$269.15 $132.37 $401.52

…

CP 18–4 (FINMAN); CP 3–4 (MAN) (Concluded)

The results are clear. Paper machine 1 has a much higher materials and conversion

cost per ton in August. Apparently, the paper machine is overapplying pulp. This is

resulting in an increase in both the materials and conversion cost per ton. Paper

machine No. 2 is running at a cost near our historical cost per ton. There is no

Average materials cost per ton for paper machine No. 1:

($40,300 + $41,700 + $44,600 + $36,100) ÷ (150 + 140 + 150 + 120) = $290.54

Average conversion cost per ton for paper machine No. 1:

($18,300 + $21,200 + $22,500 + $18,100) ÷ (150 + 140 + 150 + 120) = $143.04

Average materials cost per ton for paper machine No. 2:

CP 18–5 (FINMAN); CP 3–5 (MAN)

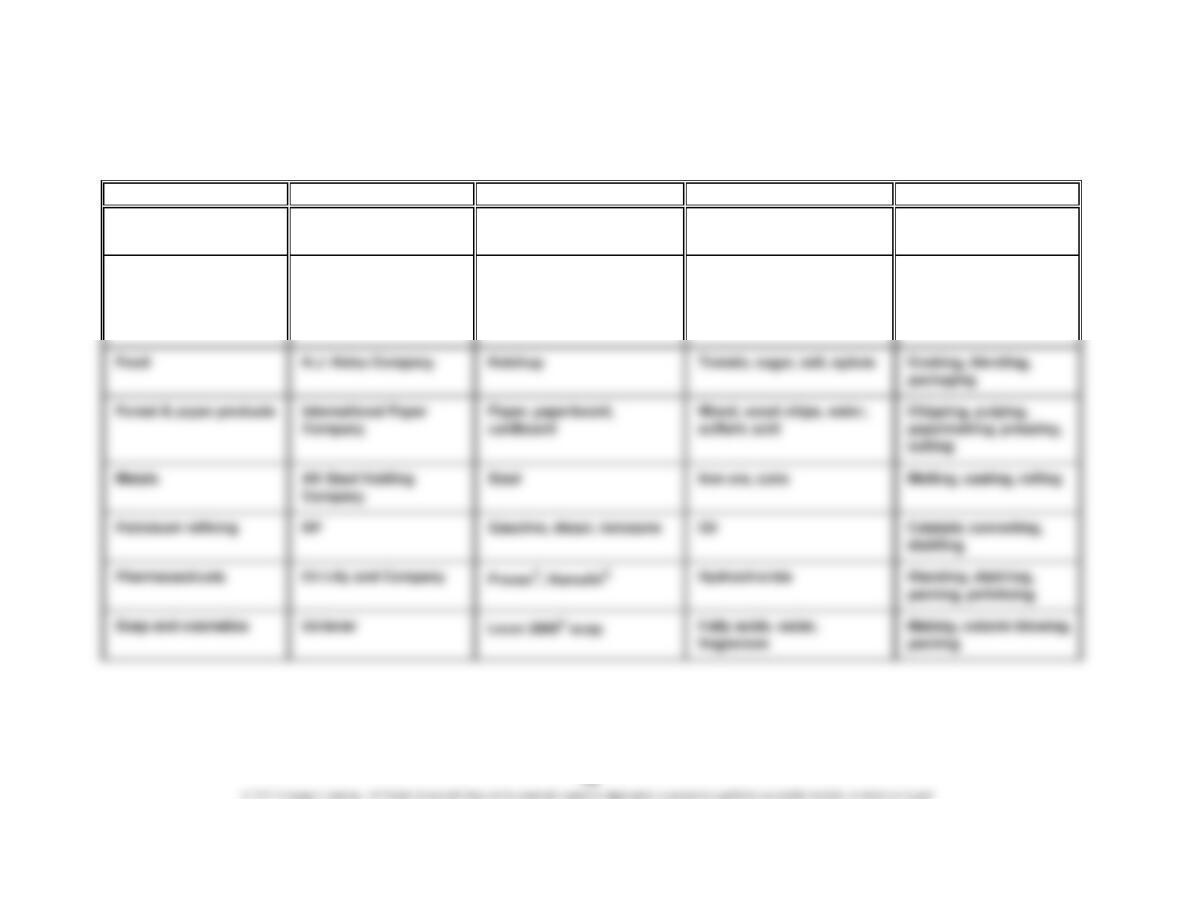

This activity can be accomplished with multiple groups assigned to one or more

of the industry categories. Assign at least one group to each industry category

(some are easier than others, so some groups may be assigned multiple

CP 18–5 (FINMAN); CP 3–5 (MAN) (Concluded)

Industry Category Example Company Products Materials Processes

Beverages PepsiCo, Inc. Pepsi, Diet Pepsi Sugar, carbonated water,

concentrate

Mixing, bottling

Chemicals E. I. du Pont de Nemours

and Company

Stainmaster®, Kevlar®,

Lycra®, Teflon®, refrigerants,

electronic materials

Petroleum and petroleum-

based intermediates

(esters and olefins)

Reaction, blending,

distilling, extruding