PROBLEM 16-44 (40 MINUTES)

1. Net present-value analysis:

Old machine:

Annual costs:

Variable 300,000 $.38 ……………………………………………………….

$(114,000

)

Fixed ……………………………………………………………………………………

(21,000

)

$(135,000

)

Annuity discount factor (r = 16%; n = 6) …………………………..

Present value of annual costs ……………………………………………………….

$(497,475

)

Salvage value, December 31, 20×6 ……………………………………………………….

Present value of salvage value ……………………………………………………….

Net present value ……………………………………………………………………………………

$(494,605

)

New machine:

Annual costs:

Variable 300,000 $.29 ……………………………………………………….

$(87,000

)

)

)

Present value of annual costs ……………………………………………………….

$(361,130

)

Salvage value of new machine, December 31, 20×6 …………………………..

Salvage value of old machine, December 31, 20×0 …………………………..

Acquisition cost of new machine ……………………………………………………….

)

$(432,930

)

PROBLEM 16-44 (CONTINUED)

2.

Memorandum

Date:

Today

To:

President, Special People Industries

From:

I.M. Student

Subject:

Cookie machine replacement decision

The nonquantitative factors that are important to the decision include the following:

• The lower operating costs (variable and fixed) of the new machine would enable

Special People Industries to meet future competitive or inflationary pressures to

a greater degree than the old machine.

PROBLEM 16-45 (25 MINUTES)

1. Initial cost of investment in a longer runway:

Land acquisition ……………………………………………………………………………………

$ (70,000

)

Runway construction ……………………………………………………………………………………

)

Extension of perimeter fence ……………………………………………………….

)

Runway lights ……………………………………………………………………………………

)

New snow plow ……………………………………………………………………………………

)

Salvage value of old snow plow ……………………………………………………….

Initial cost of investment ……………………………………………………….

)

2. Annual net incremental benefit from runway:

Runway maintenance ……………………………………………………………………………………

$ (28,000

)

Incremental revenue from landing fees ……………………………………………………….

Incremental operating costs for new snow plow …………………………..

)

Additional tax revenue ……………………………………………………….

Annual incremental benefit ……………………………………………………….

3. Internal rate of return:

Annuity discount factor associated

with the internal rate of return

=

benefit lincrementa annual

investment ofcost initial

Find 6.710 in the 10-year row of Table IV of Appendix A. It falls in the 8 percent

Chapter 16 – Capital Expenditure Decisions

PROBLEM 16-46 (45 MINUTES)

1. Net present-value analysis:

Runway maintenance ……………………………………………………………………………………

$ (28,000

)

Incremental revenue from landing fees ……………………………………………………….

40,000

Incremental operating costs for new snow plow …………………………..

)

Additional tax revenue ……………………………………………………….

Annual incremental benefit ……………………………………………………….

Present value of annual benefits ……………………………………………………….

Less: Initial costs:

Land acquisition ……………………………………………………….

)

Runway construction ……………………………………………………….

)

Extension of perimeter fence ……………………………………………………….

)

Runway lights ……………………………………………………………………………………

)

New snow plow ……………………………………………………….

)

Salvage value of old snow plow ……………………………………………………….

Net present value ……………………………………………………………………………………

$ (67,840

)

2. From a purely economic perspective, the board should not approve the runway,

3. (a) Data that are likely to be most uncertain include the following:

Chapter 16 – Capital Expenditure Decisions

PROBLEM 16-46 (CONTINUED)

(b) The least uncertain data would likely include the following:

• Cost of acquiring land

PROBLEM 16-47 (30 MINUTES)

Annuity discount factor associated

with the internal rate of return

=

benefit lincrementa annual

investment ofcost initial

For the internal rate of return to be 12 percent, the annuity discount factor must be 5.650

(Table IV in Appendix A: r = .12, n = 10). Therefore:

benefit lincrementa annual

benefit lincrementa annual

PROBLEM 16-47 (CONTINUED)

We calculate the required increase in annual tax revenue as follows:

Required incremental benefit ……………………………………………………….

$ 76,007

Add: Annual costs to cover:

Promotional campaign ……………………………………………………….

Runway maintenance ……………………………………………………….

Incremental operating costs of new snow plow …………………………..

Total annual costs ……………………………………………………….……………………..

Subtotal ……………………………………………………………………………………

Deduct: Incremental revenue from landing fees …………………………..

)

Required increase in tax revenue ……………………………………………………….

$ 96,007

Chapter 16 – Capital Expenditure Decisions

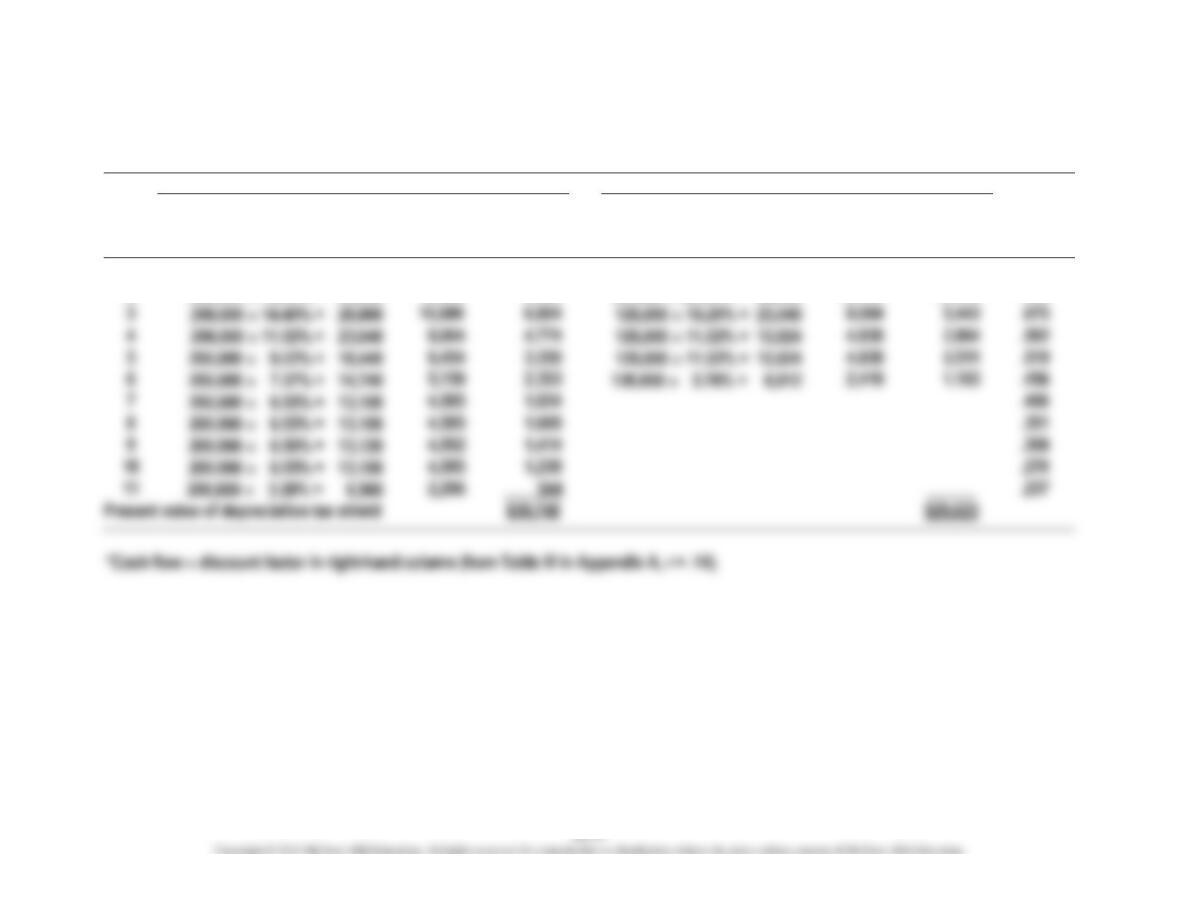

PROBLEM 16-48 (45 MINUTES)

Storage Racks

Forklift

Year

MACRS

Depreciation

Cash Flow:

Tax Savings

(Depr. .35)

Present

Value*

MACRS

Depreciation

Cash Flow:

Tax Savings

(Depr. .35)

Present

Value*

Discount

Factor

1

$200,000 10.00% = $20,000

$ 7,000

$ 6,139

$120,000 20.00% = $24,000

$ 8,400

$ 7,367

.877

2

200,000 18.00% = 36,000

12,600

9,689

120,000 32.00% = 38,400

13,440

10,335

.769

3

200,000 14.40% = 28,800

10,080

6,804

5,443

.675

4

200,000 11.52% = 23,040

4,774

2,864

.592

5

3,350

2,511

.519

6

2,353

1,103

.456

7

1,834

.400

8

1,609

.351

9

1,414

.308

1,238

.270

544

.237

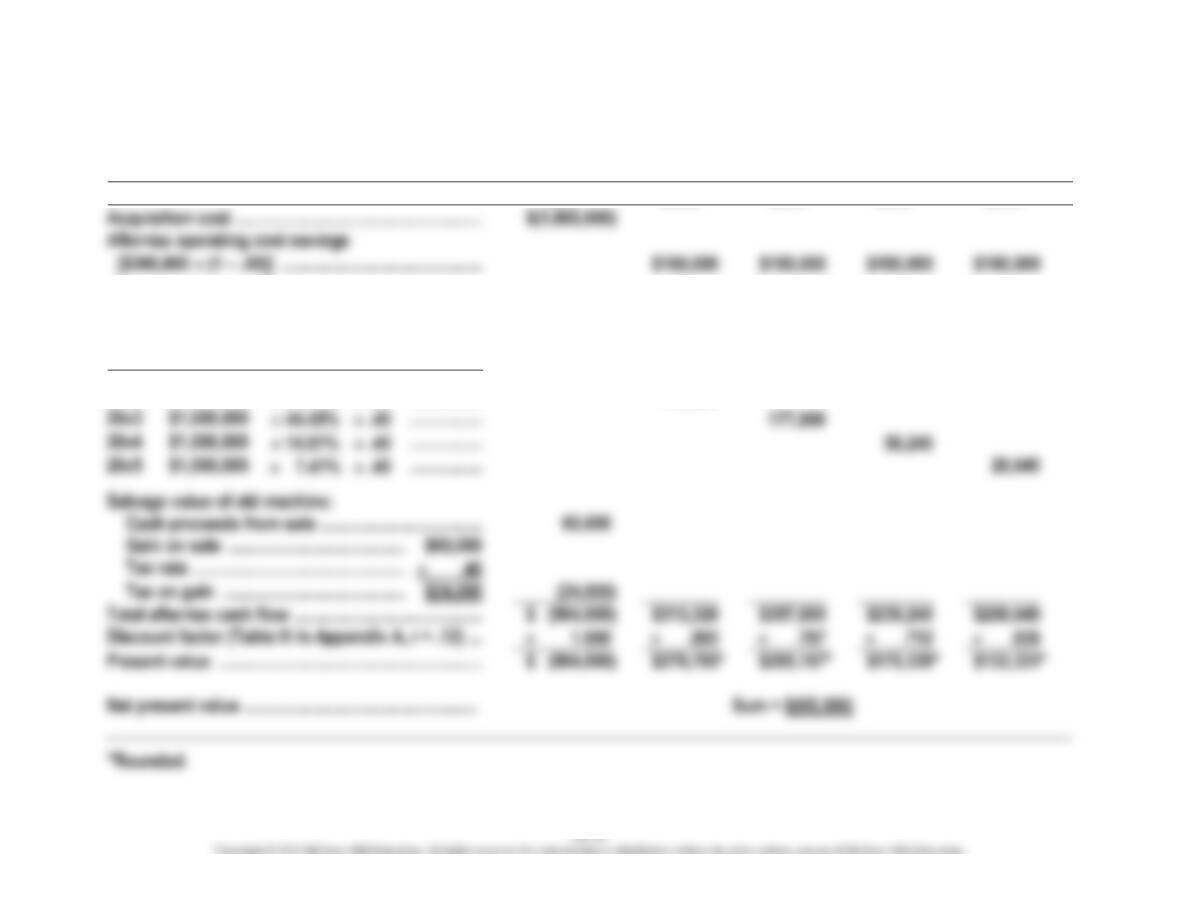

PROBLEM 16-49 (40 MINUTES)

1. MicroTest Technology, Inc. should not purchase the new pump because the net

present value is a negative amount, $(70,547), as calculated in the following table:

20×2

20×3

20×4

20×5

20×6

Equipment cost …………………..

$(608,000

)

Installation cost ………………….

)

Sale of old pump

[$50,000 (1 – .4)] …………….

30,000

Depreciation tax shield* ………

$ 82,658

$110,236

$ 36,729

$ 18,377

Annual savings† …………………..

75,000

75,000

75,000

75,000

Incremental savings** ………….

21,600

36,000

36,000

50,400

Salvage value of new pump

[$80,000 (1 – .4)] …………….

________

________

________

After-tax cash flow ………………

$(590,000

)

$ 179,258

$221,236

$ 147,729

$191,777

Present value ………………………

$(590,000

)

$ 154,520

$ 164,378

$105,861

PROBLEM 16-49 (CONTINUED)

Explanatory notes:

*20×3: $620,000 33.33% .4 = $82,658

20×4: $620,000 44.45% .4 = $110,236

2. Factors other than the net present value that management should consider before

making the pump replacement decision include the following:

• Availability of any necessary financing

Chapter 16 – Capital Expenditure Decisions

PROBLEM 16-50 (45 MINUTES)

1. Net-present-value analysis:

(a) Cost savings from manufacturing pressure fittings:

Per

Unit

Total

Cost to purchase pressure fittings from outside supplier ……………………….

$20.00

$1,600,000

Incremental costs of manufacturing the pressure fittings*

Total incremental costs ……………………………………………………….

Cost savings from manufacturing pressure fittings …………………………..

$11.70

Taxes (40%) ……………………………………………………………………………………

Chapter 16 – Capital Expenditure Decisions

PROBLEM 16-50 (CONTINUED)

(b) Discounted-cash-flow analysis:

Cash

Flow

Discount

Factor

Present

Value

Annual cost savings

$561,600

3.605

$2,024,568

MACRS depreciation tax shield:

Year

MACRS

Percentage

MACRS

Depreciation

Tax

Rate

Tax

Shield

1

33.33%

$ 833,250

40%

$333,300

.893

297,637

2

44.45%

40%

.797

354,267

3

14.81%

40%

.712

105,447

4

40%

.636

47,128

Salvage Value of Tools

Cash

Flow

Cash proceeds

from sale

$100,000

.567

56,700

$ 100,000

40%

.567

)

Initial investment

)

2. Factors that LifeLine Corporation’s management should consider in addition to the

discounted-cash-flow analysis before a decision is made to replace the tools or

purchase the pressure fittings from an outside supplier include:

• the possibility of negotiating a lower price for the pressure fittings.

Chapter 16 – Capital Expenditure Decisions

PROBLEM 16-51 (45 MINUTES)

1. Net-present value analysis of the machine replacement:

20×1

20×2

20×3

20×4

20×5

Acquisition cost ……………………………………………….

)

Depreciation tax shield:

Year

Acquisition

Cost

MACRS

Percentage

Tax

Rate

20×2:

$1,000,000

33.33%

.40

…………………………..

133,320

20×3

$1,000,000

…………………………..

20×4

$1,000,000

14.81%

.40

…………………………..

.40

Salvage value of old machine:

60,000

)

Total after-tax cash flow ……………………………………

)

Discount factor (Table III in Appendix A, r = .12) …

Present value …………………………………………………..

)

*

*

*

*

Chapter 16 – Capital Expenditure Decisions

PROBLEM 16-51 (CONTINUED)

2. The machine replacement’s internal rate of return is between 6% and 8%. The

project’s net present value is positive if a 6% discount rate is used, but it is negative

if an 8% discount rate is used.

Year

Total After-Tax

Cash Flow

(from

requirement 1)

6%

Discount

Factor

Present

Value

(using 6%)

8%

Discount

Factor

Present

Value

(using 8%)

20×1 ……………..

$(964,000

)

1.000

$(964,000

)

1.000

$(964,000

)

20×2 ……………..

20×3 ……………..

20×4 ……………..

20×5 ……………..

3. The payback period on the machine replacement is between three and four years.

Year

Total After-Tax

Cash Inflow

(from requirement 1)

20×2 …………………………………..

$ 313,320

20×3 …………………………………..

357,800

20×5 …………………………………..

Chapter 16 – Capital Expenditure Decisions

PROBLEM 16-51 (CONTINUED)

4. With a salvage value of zero on the new machine, the machine replacement’s net

present value is $(95,368). Thus, the after-tax discounted cash flow from the salvage

X – .40X

=

$149,950

=

$249,917 (rounded)

Chapter 16 – Capital Expenditure Decisions

PROBLEM 16-52 (35 MINUTES)

1. (a) Mall restaurant:

Net after-tax cash inflows ……………………………………………………………………..

$ 50,000

Present value of annual cash flows ……………………………………………………….

Cash outflow at time 0 ………………………………………………………………………….

(b) Downtown restaurant:

Net after-tax cash inflows ……………………………………………………………………..

$ 35,800

Present value of annual cash flows ……………………………………………………….

Cash outflow at time 0 ………………………………………………………………………….

2. Profitability index =

investment initial

investment initial of exclusive flows, cash of valuepresent

(a) Mall restaurant:

4. The two proposed restaurant projects have different lives, which makes it