CHAPTER 16

FINANCIAL STATEMENT ANALYSIS

DISCUSSION QUESTIONS

1. Liquidity is the ability of a company to convert assets into cash. Short-term creditors such as banks and

2. Comparative statements provide information about changes between dates or periods. Trends indicated by

comparisons may be far more significant than the data for a single date or period.

3. Before this question can be answered, the increase in net income should be compared with changes in

sales, expenses, and assets for the current year. The return on total assets for both periods should also be

compared. If these comparisons indicate favorable trends, the operating performance has improved. If not,

the apparent favorable increase in net income may be offset by unfavorable trends in other areas.

4. Generally, the two ratios would be very close because most service businesses sell services and hold very

little inventory.

6. The ratio of fixed assets to long-term liabilities increased from 3.4 ($1,360,000 ÷ $400,000) in the

preceding year to 4.2 ($1,260,000 ÷ $300,000) in the current year. This indicates that the company is in a

stronger position this year to borrow additional long-term debt.

7. a. The return on total assets measures the profitability of the total assets, without regard for how the

assets are financed. The return on stockholders’ equity measures the profitability of the stockholders’

CHAPTER 16 Financial Statement Analysis

DISCUSSION QUESTIONS (Concluded)

8. The price-earnings ratio measures the market’s expectations of a company’s future earnings prospects.

Kroger’s low price-earnings ratio compared to the industry average suggests that the market has low

expectations about the company’s future earnings.

9. The dividend yield measures the return common stockholders receive from a cash dividend. The high

CHAPTER 16 Financial Statement Analysis

BASIC EXERCISES

BE 16–1

Accounts payable ……………………………….. $12,240 increase ($114,240 – $102,000), or 12%

Long-term debt …………………………………… $7,200 increase ($127,200 – $120,000), or 6%

BE 16–2

Amount

Percentage

Sales ………………………………………………….. $1,500,000

100% ($1,500,000 ÷ $1,500,000)

Cost of goods sold. ……………………………. 900,000

BE 16–3

= 2.5

b. Quick Ratio = Quick Assets ÷ Current Liabilities

= ($225,000 + $115,000 + $112,000) ÷ $244,000

= 1.9

BE 16–4

= 12.0

= 30.4 days

BE 16–5

a. Inventory Turnover = Cost of Goods Sold ÷ Average Inventory

= $500,000 ÷ $62,500

= 8.0

= 45.6 days

BE 16–6

= 3.5

b.

= $800,000 ÷ $320,000

= 2.5

BE 16–7

Equity rs’Stockholde Total

sLiabilitie Total

Equity rs’Stockholde to sLiabilitie of Ratio =

CHAPTER 16 Financial Statement Analysis

BE 16–8

Asset Turnover = Sales ÷ Average Total Assets

= $6,750,000 ÷ $2,500,000

= 2.7

BE 16–9

BE 16–10

a.

BE 16–11

a.

b.

14.0%

$8,750,000 $1,225,000

Equity rs’Stockholde Common Average

IncomeNet

Equity rs’Stockholde on Return

=

=

=

21.8%

=

Dividends Preferred – IncomeNet

Share per Earnings =

$6.40=

5.0

$6.40 $32.00

Stock Common on Share per Earnings

Stock Common of Share per PriceMarket

Ratio EarningsPrice

=

=

=–

CHAPTER 16 Financial Statement Analysis

EXERCISES

Ex. 16–1

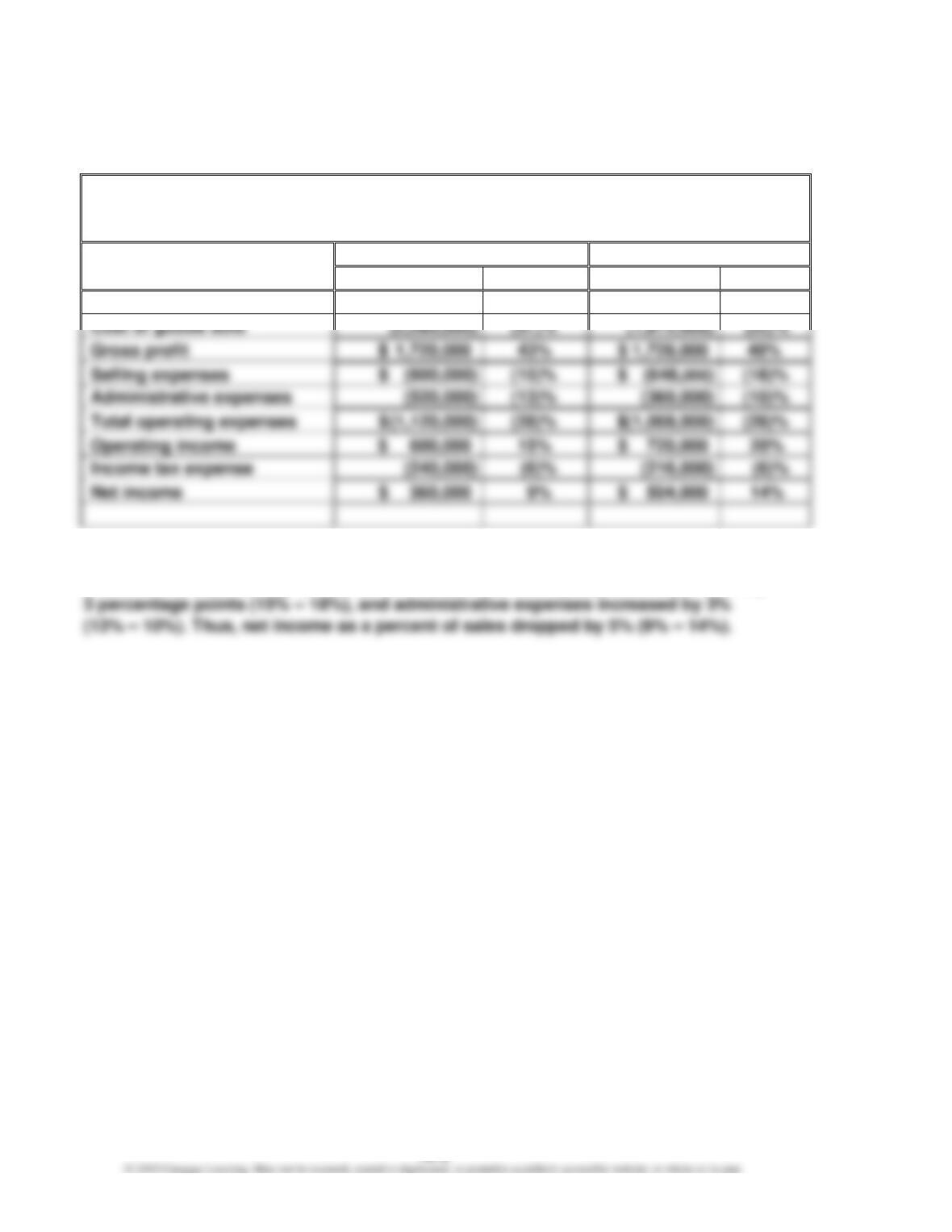

a.

Innovation Quarter Inc.

Comparative Income Statement

For the Years Ended December 31

Current Year

Previous Year

Amount

Percent

Amount

Percent

Sales

$ 4,000,000

100%

$ 3,600,000

100%

Cost of goods sold

(57)%

Gross profit

Administrative expenses

(13)%

Total operating expenses

(28)%

$(1,008,000)

Operating income

$ 720,000

Income tax expense

Net income

$ 504,000

b. The vertical analysis indicates that the cost of goods sold as a percent of sales

increased by 5 percentage points (57% – 52%), while selling expenses decreased by

CHAPTER 16 Financial Statement Analysis

Ex. 16–2

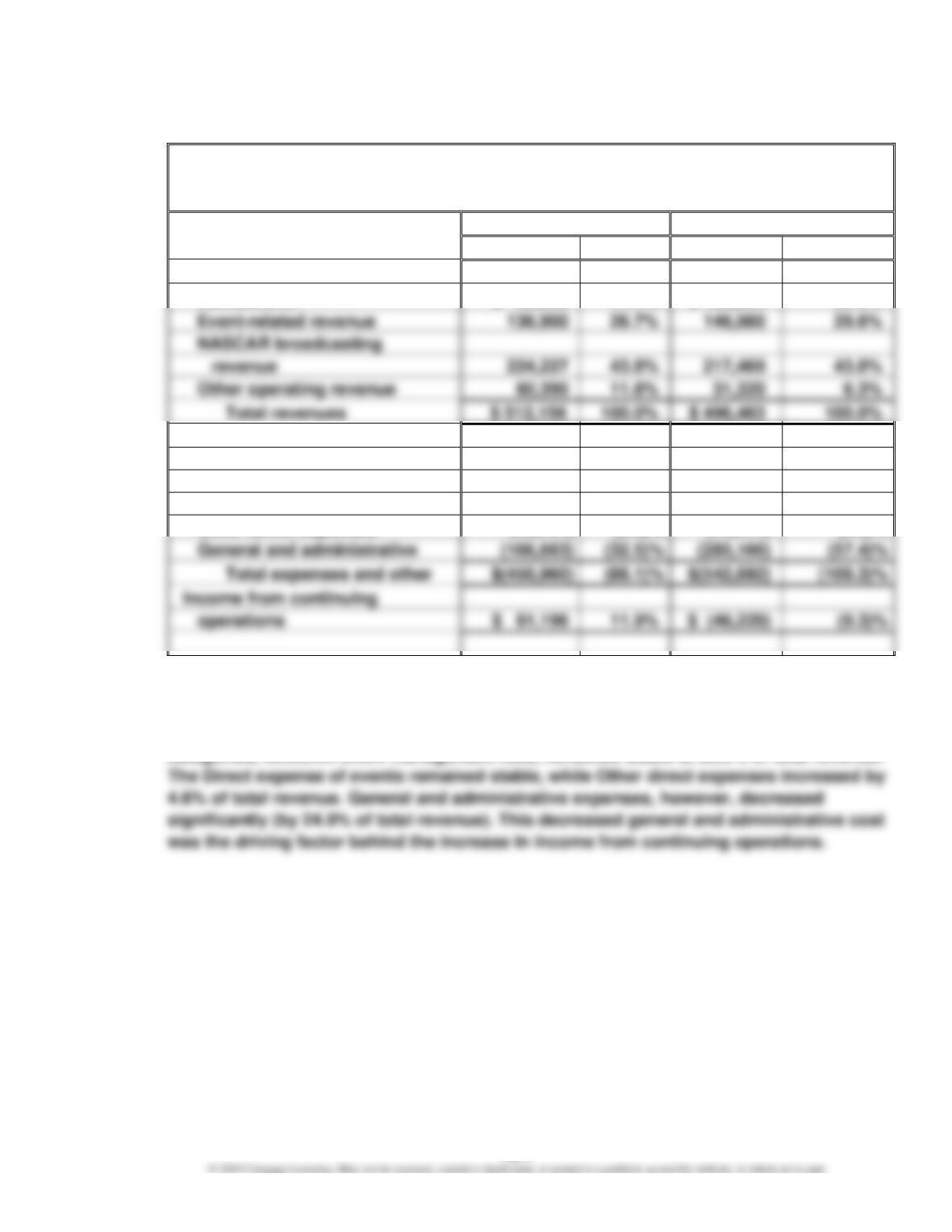

a.

Speedway Motorsports, Inc.

Comparative Income Statement (in thousands of dollars)

For the Years Ended December 31

Current Year

Prior Year

Amount

Percent

Amount

Percent

Revenues:

Admissions

$ 90,639

17.7%

$ 100,694

20.3%

Event-related revenue

136,900

26.7%

29.6%

NASCAR broadcasting

224,227

43.8%

43.8%

Other operating revenue

Total revenues

$ 512,156

$ 496,463

Expenses and other:

Direct expense of events

$(102,786)

(20.1)%

$(104,303)

(21.0)%

NASCAR event

management fees

(137,727)

(26.9)%

(133,682)

(26.9)%

Other direct expenses

General and administrative

(32.5)%

(285,166)

(57.4)%

Total expenses and other

$(450,960)

(88.1)%

$(542,692)

Income from continuing

operations

11.9%

$ (46,229)

b. Overall revenue increased between the two years, with changes in the mix of revenue

sources. The NASCAR broadcasting revenue remained stable (43.8% of total revenue),

while admissions revenue decreased by 2.6% of total revenue. One of the major expense

CHAPTER 16 Financial Statement Analysis

Ex. 16–3

a.

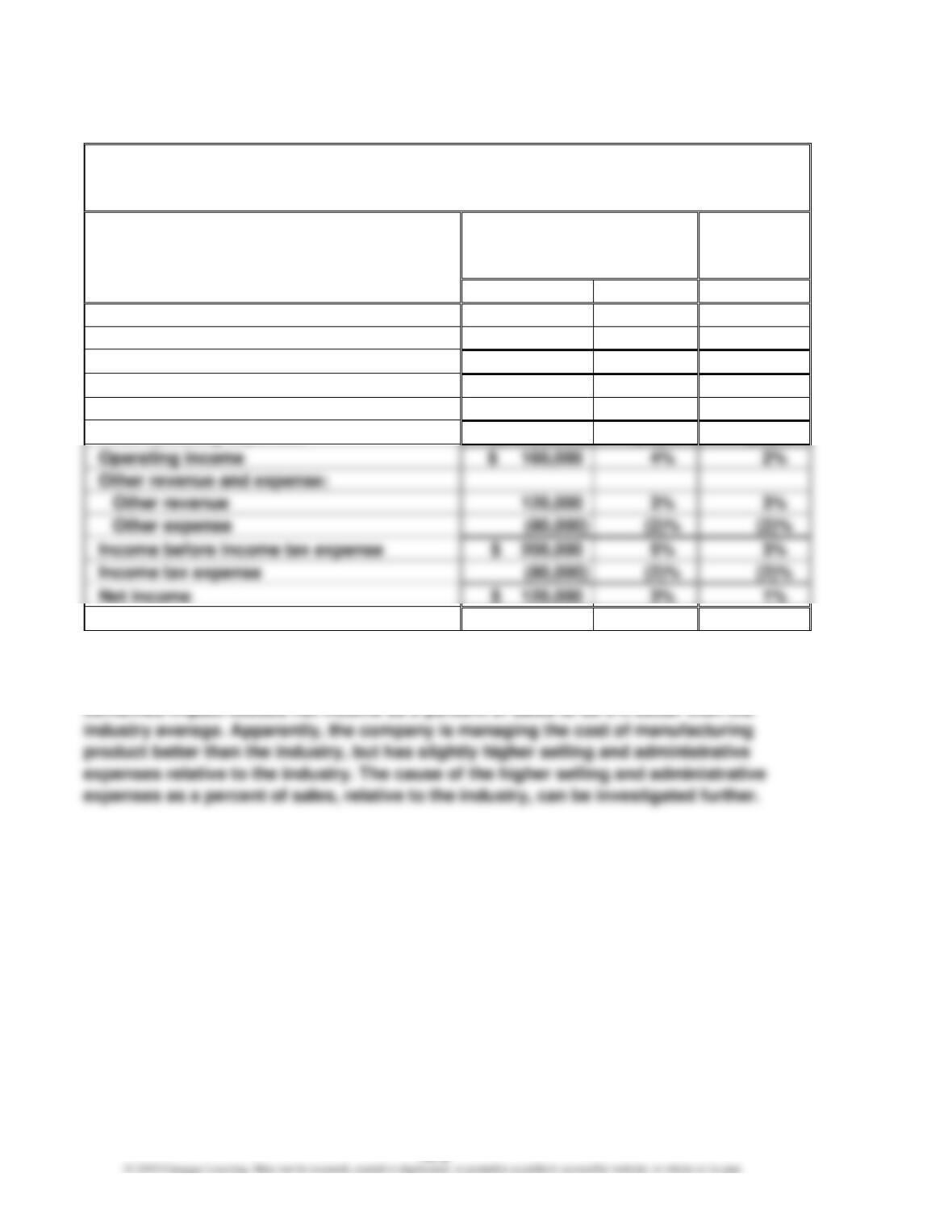

Tannenhill Company

Common-Sized Income Statement

For the Year Ended December 31

Tannenhill

Company

Electronics

Industry

Average

Amount

Percent

Sales

$ 4,000,000

100%

100%

Cost of goods sold

(2,120,000)

(53)%

(60)%

Gross profit

$ 1,880,000

47%

40%

Selling expenses

$(1,080,000)

(27)%

(24)%

Administrative expenses

(640,000)

(16)%

(14)%

Total operating expenses

$(1,720,000)

(43)%

(38)%

Operating income

Other revenue and expense:

Income before income tax expense

Income tax expense

Net income

b. The cost of goods sold is 7% lower than the industry average, but the selling expenses

and administrative expenses are 3% and 2% higher than the industry average. The

CHAPTER 16 Financial Statement Analysis

Ex. 16–4

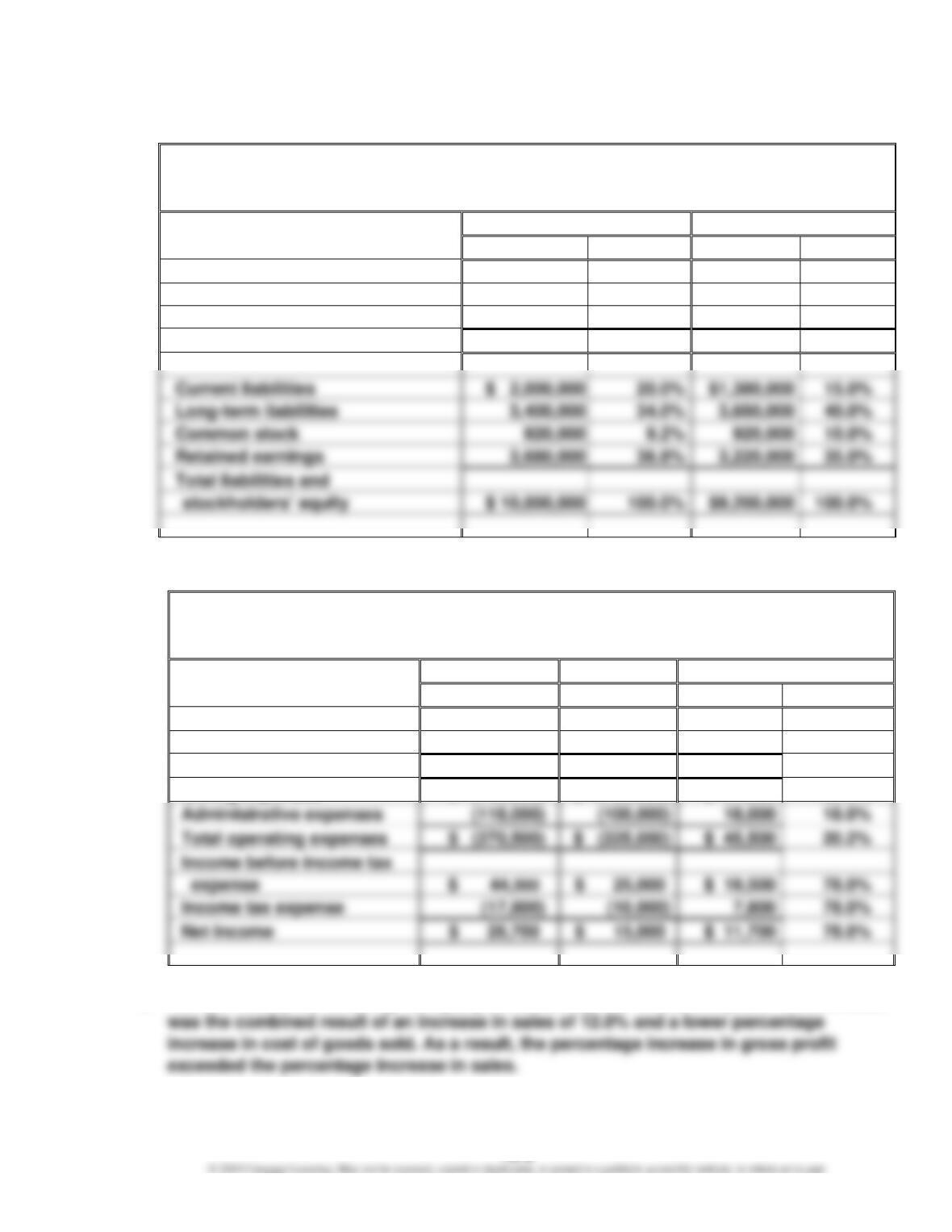

Alvarez Company

Comparative Balance Sheet

For the Years Ended December 31

Current Year

Previous Year

Amount

Percent

Amount

Percent

Current assets

$ 2,500,000

25.0%

$1,840,000

20.0%

Property, plant, and equipment

5,600,000

56.0%

6,072,000

66.0%

Intangible assets

1,900,000

19.0%

1,288,000

14.0%

Total assets

$ 10,000,000

100.0%

$9,200,000

100.0%

Current liabilities

$ 2,000,000

$1,380,000

15.0%

3,400,000

34.0%

3,680,000

40.0%

Common stock

920,000

10.0%

Retained earnings

3,680,000

36.8%

3,220,000

35.0%

Total liabilities and

$ 10,000,000

100.0%

$9,200,000

100.0%

Ex. 16–5

a.

Winthrop Company

Comparative Income Statement

For the Years Ended December 31

Current Year

Previous Year

Increase/(Decrease)

Amount

Amount

Amount

Percent

Sales

$ 2,240,000

$ 2,000,000

$240,000

12.0%

Cost of goods sold

(1,925,000)

(1,750,000)

175,000

10.0%

Gross profit

$ 315,000

$ 250,000

$ 65,000

26.0%

Selling expenses

$ (152,500)

$ (125,000)

$ 27,500

22.0%

Administrative expenses

18.0%

Total operating expenses

$ (270,500)

$ 45,500

20.2%

Income before income tax

expense

$ 44,500

$ 19,500

78.0%

Income tax expense

78.0%

Net income

$ 26,700

$ 15,000

$ 11,700

78.0%

b. The net income for Winthrop Company increased by 78.0% between years. This increase

CHAPTER 16 Financial Statement Analysis

Ex. 16–6

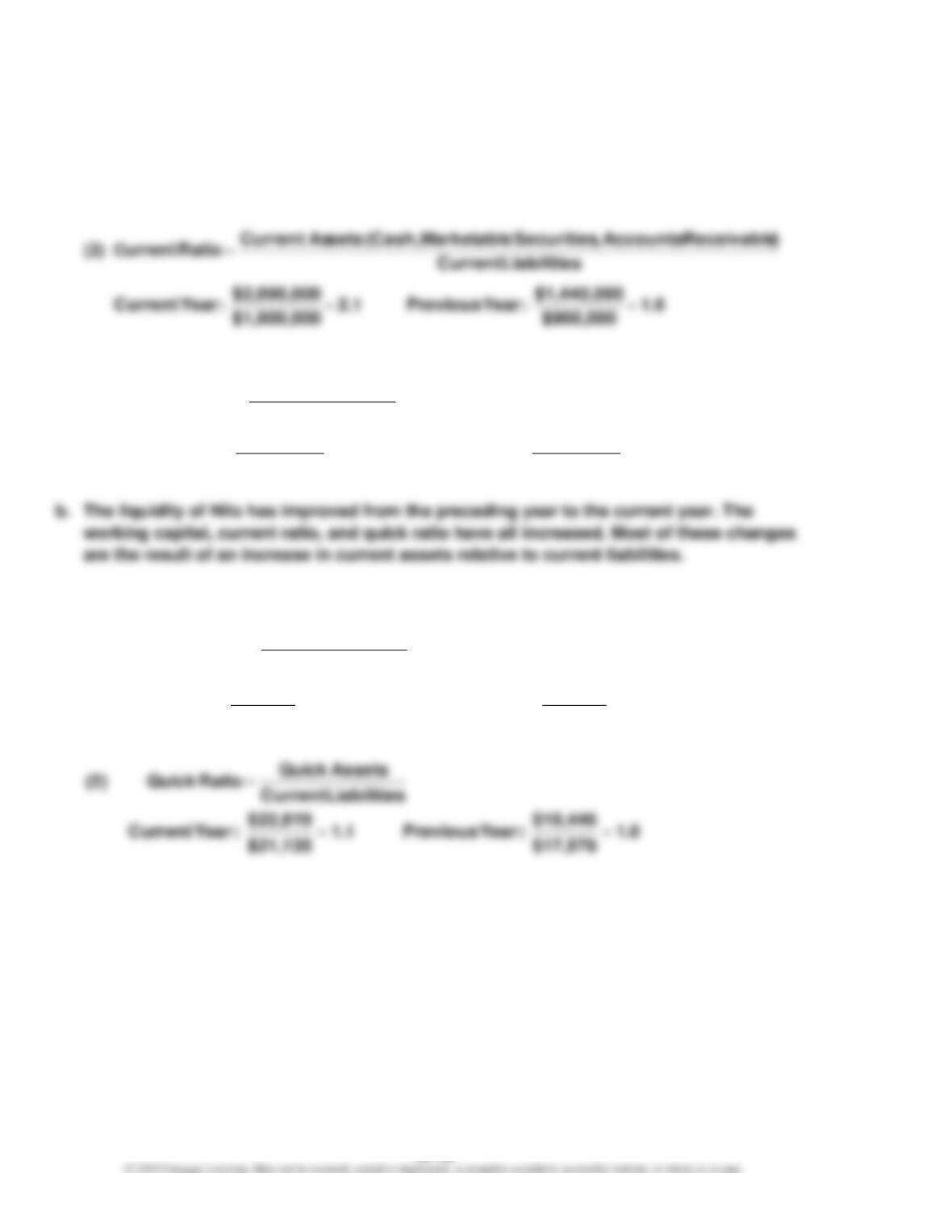

a. (1) Working Capital = Current Assets – Current Liabilities

Current year: $1,090,000 = $2,090,000 – $1,000,000

Previous year: $540,000 = $1,440,000 – $900,000

Ex. 16–7

a. (1)

b. The liquidity of PepsiCo has increased slightly over this time period. The current ratio

has remained stable at 1.3, and the quick ratio has increased by 0.1. PepsiCo appears to

have ample resources to meet its short-term obligations, and these resources have

remained constant during this time period.

1.2

$900,000

$1,080,000

:Year Previous1.5

$1,000,000

$1,540,000

:YearCurrent

sLiabilitieCurrent

AssetsQuick

Ratio Quick(3)

==

=

1.3

$17,578

$23,031

:Year Previous1.3

$21,135

$27,089

:YearCurrent

sLiabilitieCurrent

setsCurrent As

RatioCurrent

==

=

CHAPTER 16 Financial Statement Analysis

Ex. 16–8

a. The working capital, current ratio, and quick ratio are calculated incorrectly. The working

capital and current ratio incorrectly include intangible assets and property, plant, and

The correct calculations are as follows:

Working Capital = Current Assets – Current Liabilities

$30,000 = $330,000 – $300,000

b. Unfortunately, the working capital, current ratio, and quick ratio are below the minimum

threshold required by the bond indenture. This may require the company to renegotiate

the bond contract, including a possible unfavorable change in the interest rate.

CHAPTER 16 Financial Statement Analysis

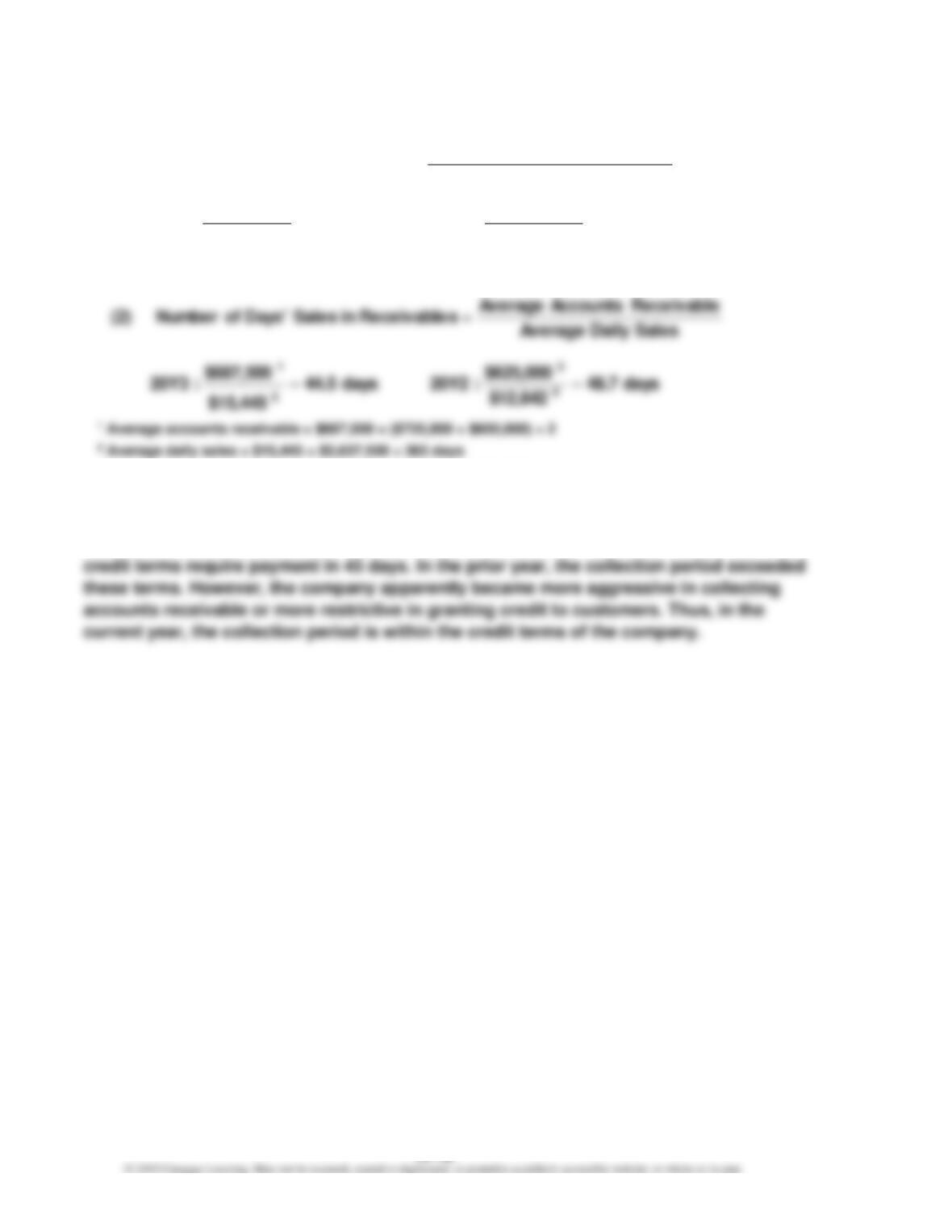

Ex. 16–9

a.

3 Average accounts receivable = $625,000 = ($650,000 + $600,000) ÷ 2

4 Average daily sales = $12,842 = $4,687,500 ÷ 365 days

b. The collection of accounts receivable has improved. This can be seen in both the

increase in accounts receivable turnover and the reduction in the collection period. The

7.5

**$625,00

0$4,687,500

:20Y28.2

*$687,500

$5,637,500

:20Y3

Receivable AccountsAverage

Sales

Turnover Receivable Accounts(1)

2 $600,000) ($650,000 $625,000 **2 $650,000) ($725,000 $687,500*

==

=

+=+=

CHAPTER 16 Financial Statement Analysis

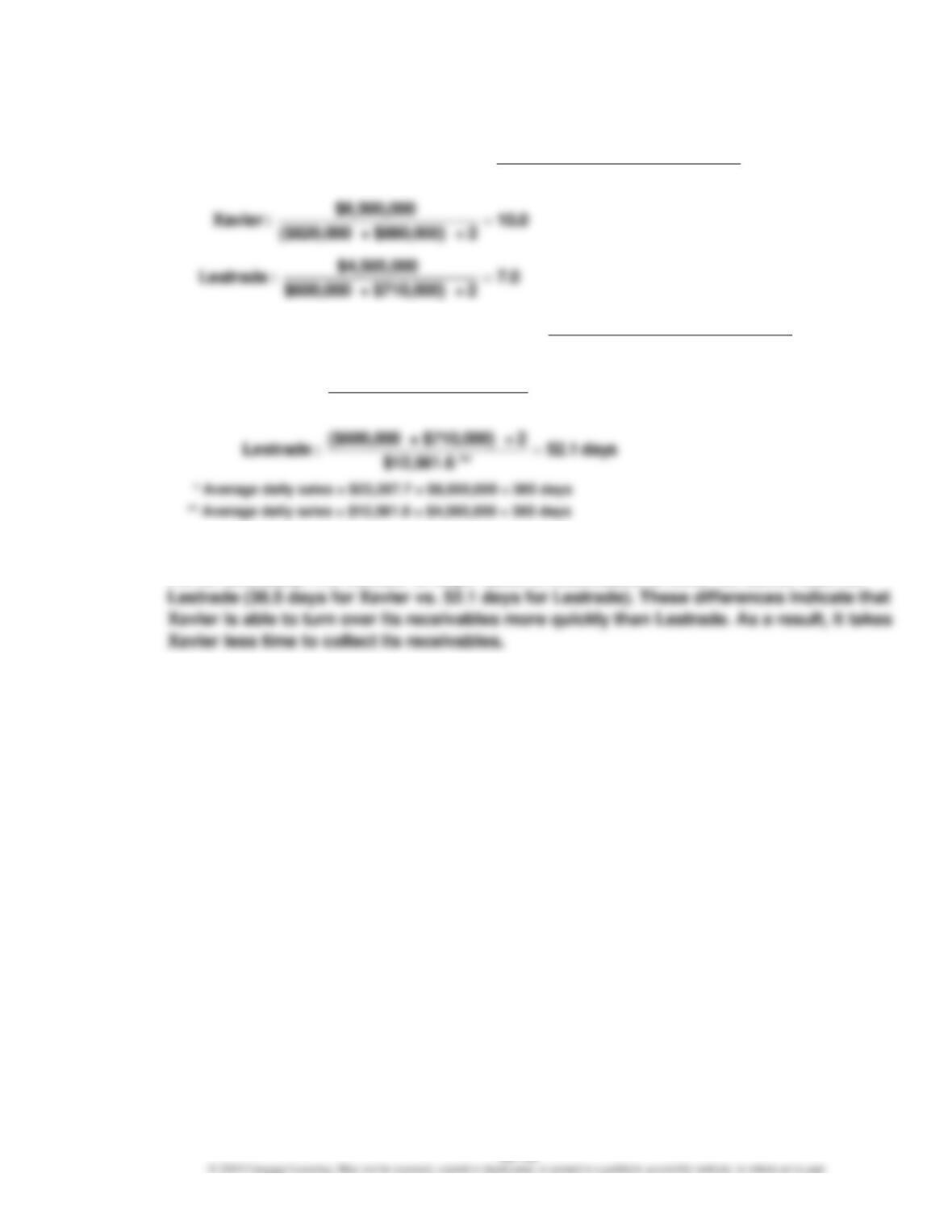

Ex. 16–10

a.

b. Xavier’s accounts receivable turnover is much higher than Lestrade’s (10.0 for Xavier vs.

7.0 for Lestrade). The number of days’ sales in receivables is lower for Xavier than for

days 36.5

*$23,287.7

2 ÷ $880,000) + ($820,000

:Xavier

Sales Daily Average

Receivable AccountsAverage

=sReceivable in Sales Days’ of Number(2)

Receivable AccountsAverage

Sales

=Turnover Receivable Accounts(1)

=

CHAPTER 16 Financial Statement Analysis

Ex. 16–11

a.

b. The inventory position of the business has deteriorated. The inventory turnover has

decreased, while the number of days’ sales in inventory has increased. The sales volume

days 40.6

*$25,397

2 ÷ $940,000) + 0($1,120,00

:YearCurrent

Sold Goods ofCost Daily Average

Inventory Average

Inventory in Sales Days’ of Number(2)

InventoryAverage

Sold Goods ofCost

=Turnover Inventory(1)

=

=

CHAPTER 16 Financial Statement Analysis

Ex. 16–12

a.

b. QT has a much higher inventory turnover ratio than does Elppa (32.1 vs. 13.4).

Likewise, QT has a much smaller number of days’ sales in inventory (11.4 days vs.

27.3 days). These significant differences are a result of QT’s make-to-order strategy.

QT has successfully developed a manufacturing process that is able to fill a customer

13.4

2 ÷ $7,490) + ($6,317

$92,385

:Elppa

32.1

2 ÷ $1,404) + ($1,382

$44,754

:QT

InventoryAverage

Sold Goods ofCost

=Turnover Inventory(1)

=

=

CHAPTER 16 Financial Statement Analysis

Ex. 16–13

a.

b.

c. Both the ratio of liabilities to stockholders’ equity and the number of times bond

interest charges were earned have improved from the previous year. These results

Equity rs’Stockholde Total

sLiabilitie Total

=Equity rs’Stockholde to sLiabilitie of Ratio

5.0

$120,000

*$120,000 + $480,000

:arCurrent ye

ExpenseInterest

ExpenseInterest + Expense Tax Income Before Income

=EarnedInterest Times

=

CHAPTER 16 Financial Statement Analysis

Ex. 16–14

b.

c. Hasbro carries the same proportion of debt to stockholders’ equity as Mattel (1.7

$2,407,782

5.3

$95,118

$95,118 + $409,472

:Inc. Mattel,

8.1

$97,405

$97,405 + $692,489

:Inc. Hasbro,

ExpenseInterest

ExpenseInterest + Expense Tax Income Before Income

=EarnedInterest Times

=

=

CHAPTER 16 Financial Statement Analysis

Ex. 16–15

a.

b.

c. Hershey’s total liabilities to stockholders’ equity ratio is higher than Mondelez’s (5.7 vs.

1.4), meaning Hershey uses more debt than Mondelez. Mondelez has a lower ratio of

fixed assets to long-term liabilities than Hershey. This ratio divides the property, plant,

and equipment (net) by the long-term debt. The ratio for Mondelez is aggressive, with

Equity rs’Stockholde Total

sLiabilitie Total

Equity rs’Stockholde to sLiabilitie of Ratio

=

0.8

$2,787,203

$2,177,248

:Hershey

0.4

0$21,906,00

$8,229,000

:Mondelez

sLiabilitie Term–Long

(net) AssetsFixed

sLiabilitie Term–Long to AssetsFixed of Ratio

=

=

=

CHAPTER 16 Financial Statement Analysis

Ex. 16–16

a.

b. The asset turnover ratio measures the number of sales dollars earned for each dollar of

assets. The greater the number of sales dollars earned for every dollar of assets, the

more efficient a firm is in using assets. Thus, the ratio is a measure of each company’s

asset efficiency. Union Pacific earns only 40 cents for every dollar of assets. This is

because railroads are very asset intensive. The company must invest in locomotives,

Note to Instructors: Students may wonder how asset-intensive companies overcome their

asset efficiency disadvantages to competitors with better asset efficiencies, as in the case

between railroads and motor carriers. Asset efficiency is part of the financial equation; the

AssetsTotal Average

Sales

TurnoverAsset

=

CHAPTER 16 Financial Statement Analysis

Ex. 16–17

a.

3 Interest expense = $2,250,000 8%

4 Average total assets = ($4,400,000 + $4,000,000) ÷ 2

3 Preferred dividends = $500,000 4%

4 Average common stockholders’ equity = ($1,472,000 + $1,000,000) ÷ 2

b. The profitability ratios indicate that the company’s profitability has deteriorated. Most of

this change is from net income falling from $492,000 in 20Y6 to $372,000 in 20Y7.

AssetsTotal Average

ExpenseInterest + IncomeNet

AssetsTotal on Return

=

Equity rs’Stockholde Total Average

IncomeNet

Equity rs’Stockholde on Return

=

21.4%

$1,648,000

$20,000 – $372,000

:20Y7

Equity rs’Stockholde Common Average

Dividends Preferred – IncomeNet

Equity rs’Stockholde

Common on Return

2

1

=

=