CHAPTER 27 Cost Management for Just-in-Time Environments

Ex. 27–19 (FIN MAN); Ex. 12–19 (MAN)

Pareto Chart of Quality Activities

120,000

140,000

CHAPTER 27 Cost Management for Just-in-Time Environments

Ex. 27–20 (FIN MAN); Ex. 12–20 (MAN)

a.

Prevention $260,000 52% 13.0%

Appraisal 70,000 14% 3.5%

b.

Value-added 66%

The following classifications were used to develop the reports:

Activity

Cost

Billing error correction………………

…

$ 50,000

Cable signal testing…………………

…

70,000

Reinstalling service (installed

Quality Cost

Non-value-added

Value-added

DIGITAL LIGHT INC.

Cost of Quality Report

Cost Summary

Percent of

VA/NVA

Category

Value-Added/Non-Value-Added Activity Analysis

Quality Cost Classification

Amount

DIGITAL LIGHT INC.

Quality Activities

External failure

Appraisal

Classification

Percent

of Total

Sales

Percent

Quality

Cost

Total

Quality Cost

$330,000

21

CHAPTER 27 Cost Management for Just-in-Time Environments

Ex. 27–20 (FIN MAN); Ex. 12–20 (MAN) (Concluded)

c. The reports indicate that Digital Light Inc.’s total costs of quality are 25% of total sales.

CHAPTER 27 Cost Management for Just-in-Time Environments

Ex. 27–21 (FIN MAN); Ex. 12–21 (MAN)

b. In this improvement scenario there will 237,000 (300,000 – 63,000) additional cans

processed through the packaging operation. The same number of cans still will be

processed by the mixing and filling activities.

Additional cost to packaging activity from improved process:

c. Expected activity cost per can after improvement:

a. =Activity Cost per Can

Activity Cost per Can =

Number of Completed Cans

Activity Cost

Activity Cost

Number of Completed Cans

CHAPTER 27 Cost Management for Just-in-Time Environments

Ex. 27–22 (FIN MAN); Ex. 12–22 (MAN)

a.

Cost

Receiving claim……………………………………………… $ 80,000 20%

b. Average process cost per paid claim:

c. Activity Cost Activity Cost

Prior to After

Activity Improvement Improvement

Receiving claim…………………………

…

$ 80,000 $ 92,000

d. Average process cost per paid claim:

Percent of

Activity Total Process

Activity Cost

(Cost)

Savings

$ (12,000)

*

CHAPTER 27 Cost Management for Just-in-Time Environments

Ex. 27–23 (FIN MAN); Ex. 12–23 (MAN)

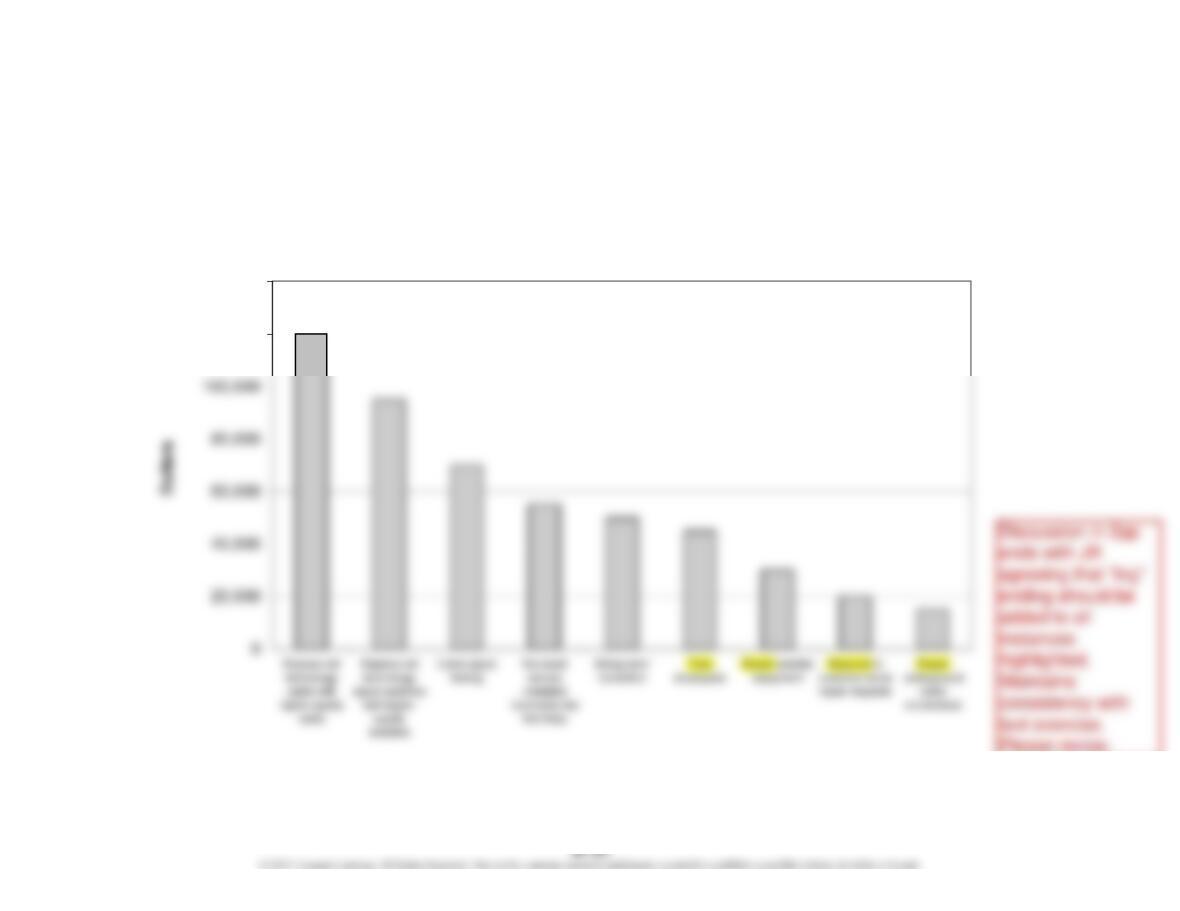

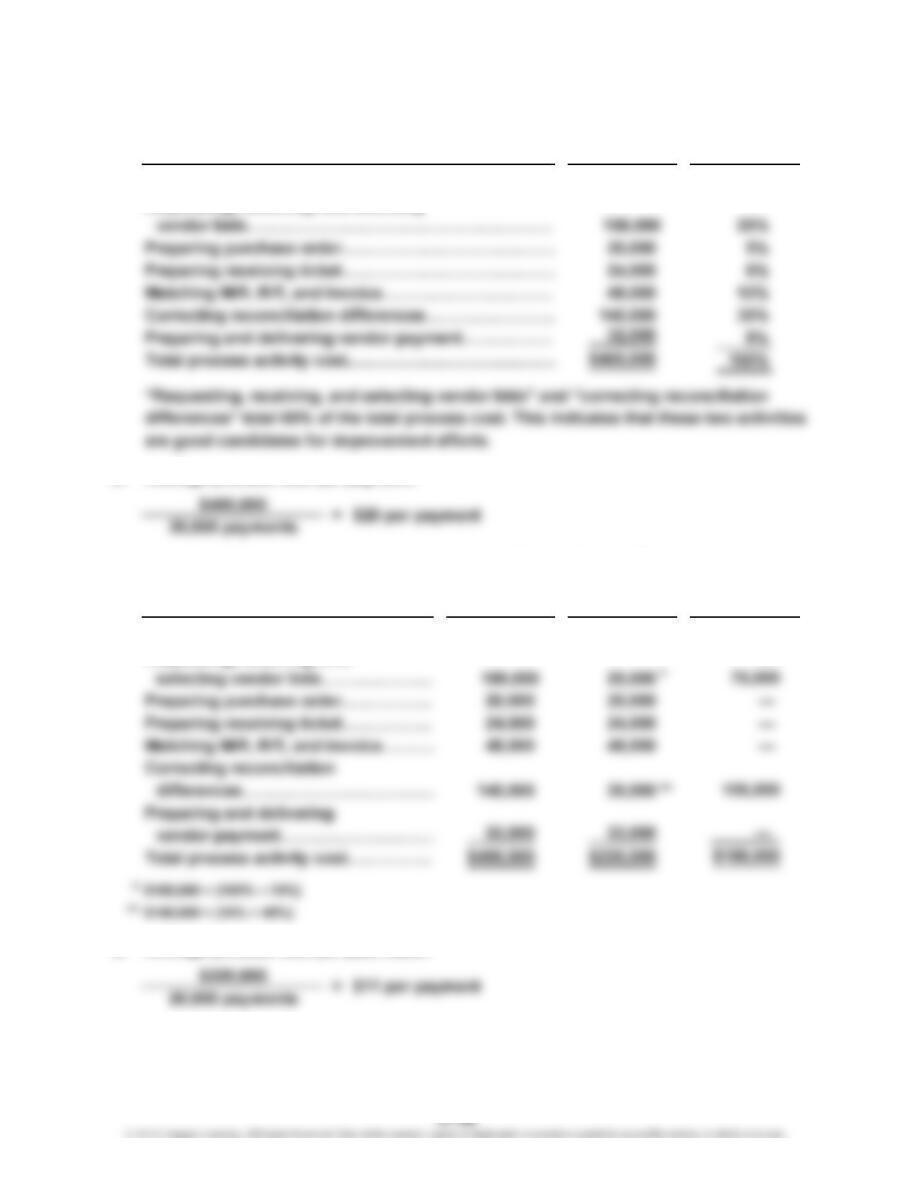

a.

Cost

Preparing materials request………………………………

…

$ 36,000 9%

Requesting, receiving, and selecting

b. Average process cost per payment:

c. Activity Cost Activity Cost

Prior to After

Activity Improvement Improvement

Preparing materials request…………

…

$ 36,000 $ 36,000

Requesting, receiving, and

…

…

d. Average process cost per paid claim:

Savings

Activity Cost

$—

—

Percent of

Activity Total Process

…

…

CHAPTER 27 Cost Management for Just-in-Time Environments

Prob. 27–1A (FIN MAN); Prob. 12–1A (MAN)

1. Brite Lite’s purchasing policy is very short-sighted. It does not involve developing

partnerships with suppliers. Brite Lite should consider changing its arm’s length

policy and work on building a long-term supply chain strategy with its suppliers. With

2. The hidden costs beyond the price include the costs associated with the higher

inventory required by Mid-State’s delivery schedule. These inventory costs include

additional space, handling, obsolescence, financing, and materials management

3. If the financing costs are 10%, then the additional cost of the inventory could be

determined as follows:

At the beginning of July, the new shipment of 45,000 pounds arrives. Assuming that

PROBLEMS

CHAPTER 27 Cost Management for Just-in-Time Environments

Prob. 27–1A (FIN MAN); Prob. 12–1A (MAN) (Concluded)

The inventory carrying cost can be estimated as follows:

Average pounds in inventory for the quarter…………………………………

…

22,500

…

CHAPTER 27 Cost Management for Just-in-Time Environments

Prob. 27–2A (FIN MAN); Prob. 12–2A (MAN)

1. Value-added time:

Assembly of PC board……………………………………………

…

5min.

Stereo assembly…………………………………………………… 18

Time to inspect one unit…………………………………………

…

9

Non-value-added time:

Wait time:

Within-batch wait time—PC board assembly

(59 × 5 min.)………………………………………………………

…

295 min.

Within-batch wait time—final assembly

Move time:

Move from PC board assembly to final assembly…………

…

10 min.

Move from final assembly to testing…………………………

…

20

2. The existing process is very wasteful. The company could improve the process by

changing the layout from a process orientation to a product orientation. Each

stereo model could be formed into a production cell. Each cell would have PC

CHAPTER 27 Cost Management for Just-in-Time Environments

Prob. 27–3A (FIN MAN); Prob. 12–3A (MAN)

3. a. Raw and In Process Inventory*

Accounts Payable 730,000

*7,300 units × $100 per unit

b. Raw and In Process Inventory*

4. Raw and In Process Inventory:

$730,000 + $756,000 – $1,465,750 = $20,250

730,000

756,000

CHAPTER 27 Cost Management for Just-in-Time Environments

Prob. 27–3A (FIN MAN); Prob. 12–3A (MAN) (Concluded)

5. JIT accounting is different from traditional accounting in a number of respects. Most

importantly, JIT accounting is simplified and uses minimal control. As a result, the

number of transactions are reduced, and the control intervals between adjacent

work in process transaction points are widened. In many JIT operations, there are

CHAPTER 27 Cost Management for Just-in-Time Environments

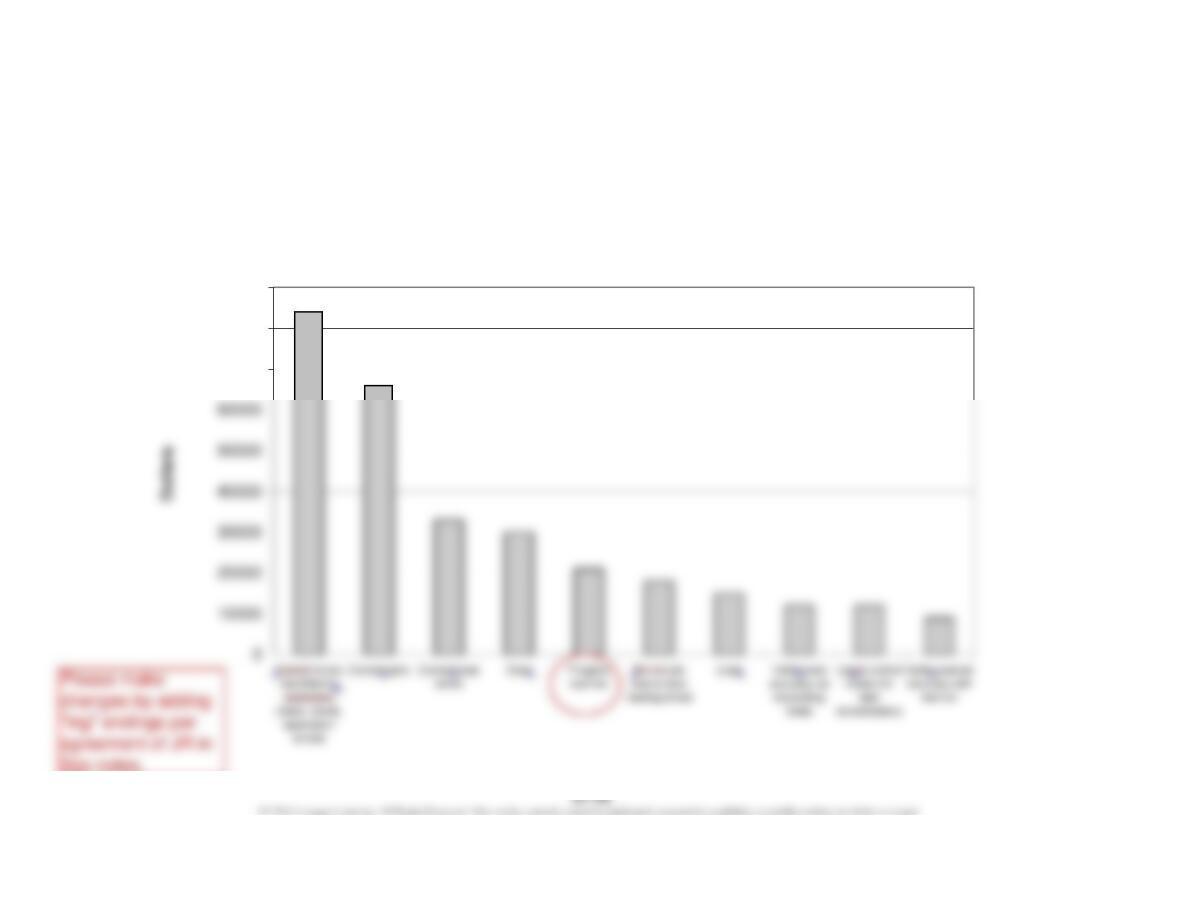

Prob. 27–4A (FIN MAN); Prob. 12–4A (MAN)

1.

Pareto Chart-Quality Activities

70000

80000

90000

CHAPTER 27 Cost Management for Just-in-Time Environments

Prob. 27–4A (FIN MAN); Prob. 12–4A (MAN) (Continued)

The following classifications are used in answering (2) and (3):

Activity

Cost

Correcting errors identified

by election commission………

…

$ 84,000

Correcting jams……………………

…

66,000

2. Percent of total activity cost for each quality cost (and nonquality cost)

classification:

Prevention…………………………………………… 3%

Appraisal……………………………………………

…

8%

…

External failure

Internal failure

Activity ClassificationClassification

Value-Added/

Quality Cost Classification

Cost of Quality Non-Value-Added

Non-value-added

Non-value-added

Percent of Total

Department Cost

Activity

Cost

$ 9,000

24,000

…