Chapter 16 – Capital Expenditure Decisions

CHAPTER 16

Capital Expenditure Decisions

ANSWERS TO REVIEW QUESTIONS

16-1 “Time is money” is an apt phrase for the evaluation of capital investment projects. A

16-2 Acceptance-or-rejection decisions involve managers deciding whether they should

undertake a particular capital investment project. In such a decision, the required

16-3 This statement is false. As the discount rate increases, the present value of a future

cash flow decreases. A higher discount rate means a higher return on funds that are

16-4 In a discounted-cash-flow (DCF) analysis, all cash flows over the life of an

investment are discounted to their present value. The discounting process makes

16-5 (1) The decision rule used to accept or reject an investment proposal under the net–

(2) The decision rule used to accept or reject an investment proposal under the

16-6 The return on an investment is equal to the amount of the unrecovered investment

multiplied by rate of return. The cash flow from the investment in a particular time

Chapter 16 – Capital Expenditure Decisions

16-7 Two advantages of the net-present-value method over the internal-rate-of-return

method are as follows:

16-8 Four assumptions underlying discounted-cash-flow analysis are as follows:

(4) A discounted-cash-flow analysis assumes a perfect capital market. In a perfect

16-9 In the total-cost approach, every cash flow for each project under consideration is

16–10 In a postaudit of an investment project, information is gathered about the actual cash

Chapter 16 – Capital Expenditure Decisions

16–11 Depreciation expense is an example of a noncash expense. A noncash expense has

16–13 A depreciation tax shield is the reduction in income taxes that results from the fact

16–14 An example of a cash flow that is not on the income statement is the acquisition cost

16–15 Under an accelerated depreciation method, the depreciation expense for an asset is

higher in the earlier years and lower in the later years than it would be under the

16–16 A gain on disposal of an asset increases income. Therefore, it increases income tax

and will increase the cash outflow for income tax. In a capital-budgeting analysis, the

16–17 The net-present-value method and the internal-rate-of-return method may yield

different rankings for investments with different lives because they make different

16–18 The profitability index (PI) is defined as the present value of cash flows, exclusive of

16–19 A project’s payback period is the number of years required for the cash inflows from

the project to accumulate to an amount equal to the initial acquisition cost for the

16–20 The payback method of evaluating investment proposals fails to consider the time

16–21 There are two ways to define an investment project’s accounting rate of return:

• Accounting rate of return = (average incremental revenue – average incremental

16–22 The chief drawback of the accounting-rate-of-return method as an investment

criterion is that it fails to account for the time value of money. Revenues and

16–23 There are two correct methods of net-present-value analysis in an inflationary

period. (1) The analyst can use real cash flows and discount them at a real discount

Chapter 16 – Capital Expenditure Decisions

SOLUTIONS TO EXERCISES

EXERCISE 16-24 (15 MINUTES)

Acquisition cost of site (time 0) ………………………………………………………………………

$(234,000

)

Preparatory work (time 0) ……………………………………………………………………………….

)

Total cost at time 0 ………………………………………………………………………………………..

$(322,080

)

EXERCISE 16-25 (15 MINUTES)

Acquisition cost of site (time 0) ………………………………………………………………………

$234,000

Preparatory work (time 0) ……………………………………………………………………………….

Find 6.710 in the 10-year row of Table IV in Appendix A. This annuity discount factor falls in

Chapter 16 – Capital Expenditure Decisions

EXERCISE 16-26 (45 MINUTES)

Year

1

2

3

4

5

6

7

8

9

10

(2) Cost savings during year

48,000

48,000

48,000

48,000

48,000

48,000

48,000

48,000

48,000

48,000

25,766

23,988

22,067

19,992

17,751

15,332

12,718

(3) Return on unrecovered

row (3) amount]

22,234

24,012

25,933

28,008

30,249

32,668

35,282

38,104

41,153

44,445

85,590

44,437

(5) Unrecovered investment

at end of year [row (1)

EXERCISE 16-27 (20 MINUTES)

Table III includes three discount rates between 8 and 16 percent. We could begin with 10,

12, or 14 percent. For completeness, the following solution computes the net present value

of the overhaul using all three discount rates.

Present Value at

Year

Repair Costs

Avoided by

Overhaul

10%

12%

14%

1

3,000 euros

3,000 euros .893

2,679 euros

2

5,000 euros

5,000 euros .826

b

4,130 euros

aTable III in Appendix A: r = 10%, n = 1.

EXERCISE 16-28 (30 MINUTES)

Answers will vary widely, depending on the project selected.

EXERCISE 16-29 (15 MINUTES)

1. Net present value calculations:

Discount

Rate

Annuity

Discount

Factor*

Annual

Savings

Present Value

of

Annual

Savings

Acquisition

Cost

Net

Present

Value†

8%

5.747

$27,000

$155,169

$129,750

$25,419

10%

5.335

27,000

144,045

129,750

14,295

12%

4.968

14%

4.639

(4,497

)

Notice that the net present value in the right-hand column declines as the discount rate

increases. A higher discount rate means greater urgency associated with having each cash

flow earlier rather than later.

EXERCISE 16-30 (15 MINUTES)

The annuity discount factor in Table IV of the Appendix (for r = 12% and n = 8) is 4.968. The

theater’s board of directors will be indifferent about replacing the lighting system if its net

present value is zero.

Net present value

=

−

cost

nacquisitio

savings

annual

factor discount

annuity

Therefore, the annual savings associated with the new lighting system could be as low as

$26,117.15 before the board would reject the proposal.

Chapter 16 – Capital Expenditure Decisions

EXERCISE 16-30 (CONTINUED)

Check (not required):

EXERCISE 16-31 (5 MINUTES)

(a) Acquisition cost = $36,000

EXERCISE 16-32 (10 MINUTES)

EXERCISE 16-33 (30 MINUTES)

(1)

Year

(2)

MACRS

Accelerated

Depreciation

(3)

Cash Flow:

Tax Savings

[Col. (2) .30]

(4)

Present Value

of Cash Flow

[Col. (3) Col. (8)]

(5)

MACRS

Straight-Line

Depreciation*

(6)

Cash Flow:

Tax Savings

[Col. (5) .30]

(7)

Present Value

of Cash Flow

[Col. (6) Col. (8)]

(8)

Discount

Factor

(r = .12)†

1

$36,663 (33.33% $110,000)

$10,999

$ 9,822

**

$18,333**

$ 5,500**

$ 4,912

.893

2

**

.797

3

**

.712

4

**

.636

EXERCISE 16-34 (15 MINUTES)

2. Loss on sale = book value – sales proceeds

3.

Reduced cash outflow for taxes ($1,900 .45) ………………………………………

$ 855

EXERCISE 16-35 (15 MINUTES)

Discount Rate

8%

10%

12%

Present value of after-tax savings:

$4,800 6.710*

$32,208

$4,800 5.650*

$27,120

Chapter 16 – Capital Expenditure Decisions

EXERCISE 16-36 (20 MINUTES)

1. Payback period =

flow cash tax–after annual

investment initial

2. Net-present-value analysis:

Discount Rate

10%

12%

14%

Present value of after-tax savings:

$27,000 4.868* ……………………………………….

$131,436

$123,228

$27,000 4.288* ……………………………………….

$115,776

Initial investment …………………………………………

)

)

)

3. Conclusion: The automatic teller machines are a sound economic investment if the

after-tax hurdle rate is 10 percent, but not if it is 12 percent or 14 percent. The pay-

Chapter 16 – Capital Expenditure Decisions

EXERCISE 16-37 (25 MINUTES)

1. The project’s payback period is 2.25 years, calculated as follows:

Year

After-Tax

Cash Flows

1 …………………………………………………………………………………..

$ 50,000

2 …………………………………………………………………………………..

45,000

3 (1st quarter) ………………………………………………………………..

Total …………………………………………………………………………….

$105,000

Initial cost …………………………………………………………………….

$105,000

2. The accounting rate of return is 18.1%, calculated as follows:

Accounting rate of return

=

investment initial

income net average

3. Net present value calculations:

Year

After-Tax

Cash Flow

Discount

Factor*

Present

Value

0

$(105,000)

1.000

$(105,000)

1

50,000

.862

43,100

2

45,000

.743

33,435

3

40,000

.641

25,640

4

35,000

.552

19,320

5

30,000

.476

14,280

EXERCISE 16-38 (20 MINUTES)

1.

Year

Cash Flow

in Real

Dollars

Discount Factor*

(real interest rate = .20)

Present

Value

0

$(150,000)

1.000

$(150,000)

1

45,000

.833

37,485

2

.694

3

.579

4

.482

5

.402

6

.335

7

.279

12,555

8

.233

2. Net present value = $22,665 (See preceding table.)

EXERCISE 16-39 (35 MINUTES)

1.

Nominal interest rate:

Real interest rate ………………………………………………………………….

.20

Inflation rate …………………………………………………………………………

.10

Nominal interest rate …………………………………………………………….

.32

2.

(1)

Year

(2)

Cash Flow

in

Real

Dollars*

(3)

Price

Index

(4)

Cash Flow in

Nominal

Dollars

[Col. (2) Col. (3)]

(5)

Discount

Factor

(nominal interest

rate = .32)†

(6)

Present

Value

[Col. (4)

Col. (5)]

0

$(150,000)

1.0000

$(150,000)

1.000

$(150,000

)

1

45,000

(1.10)1 = 1.1000

49,500

.758

37,521

2

(1.10)2 = 1.2100

54,450

.574

31,254

3

45,000

(1.10)3 = 1.3310

59,895

.435

26,054

4

45,000

(1.10)4 = 1.4641

65,885

.329

21,676

5

(1.10)5 = 1.6105

72,473

.250

18,118

6

45,000

(1.10)6 = 1.7716

79,722

.189

15,067

7

45,000

(1.10)7 = 1.9487

.143

12,540

8

45,000

(1.10)8 = 2.1436

96,462

.108

3. Net present value = $22,648. See the preceding table. The $17 difference between the

Chapter 16 – Capital Expenditure Decisions

SOLUTIONS TO PROBLEMS

PROBLEM 16-40 (30 MINUTES)

1. Yes. This is a long-term decision, with cash flows that occur over a five-year period.

Given that the cash flows have a “value” dependent on when they take place (e.g.,

2. Community Challenges is better off to manufacture the igniters.

Outsource:

$(24,800,000)

Annuity discount factor (Table IV*: r = .14, n = 5)……

x 3.433

$(85,138,400)

Manufacture in-house:

Annual variable manufacturing costs (400,000 units

x $60)…………………………………………………….

$(24,000,000)

(95,000)

$(24,095,000)

x 3.433

$(82,718,135)

(60,000)

Equipment sale: $12,000 x .519 (Table III: r = .14,

6,228

$(82,779,944)

3. The company would be financially indifferent if the net present value (NPV) of the

manufacture alternative equals the NPV of the outsource alternative. Thus:

Let X = purchase price

Chapter 16 – Capital Expenditure Decisions

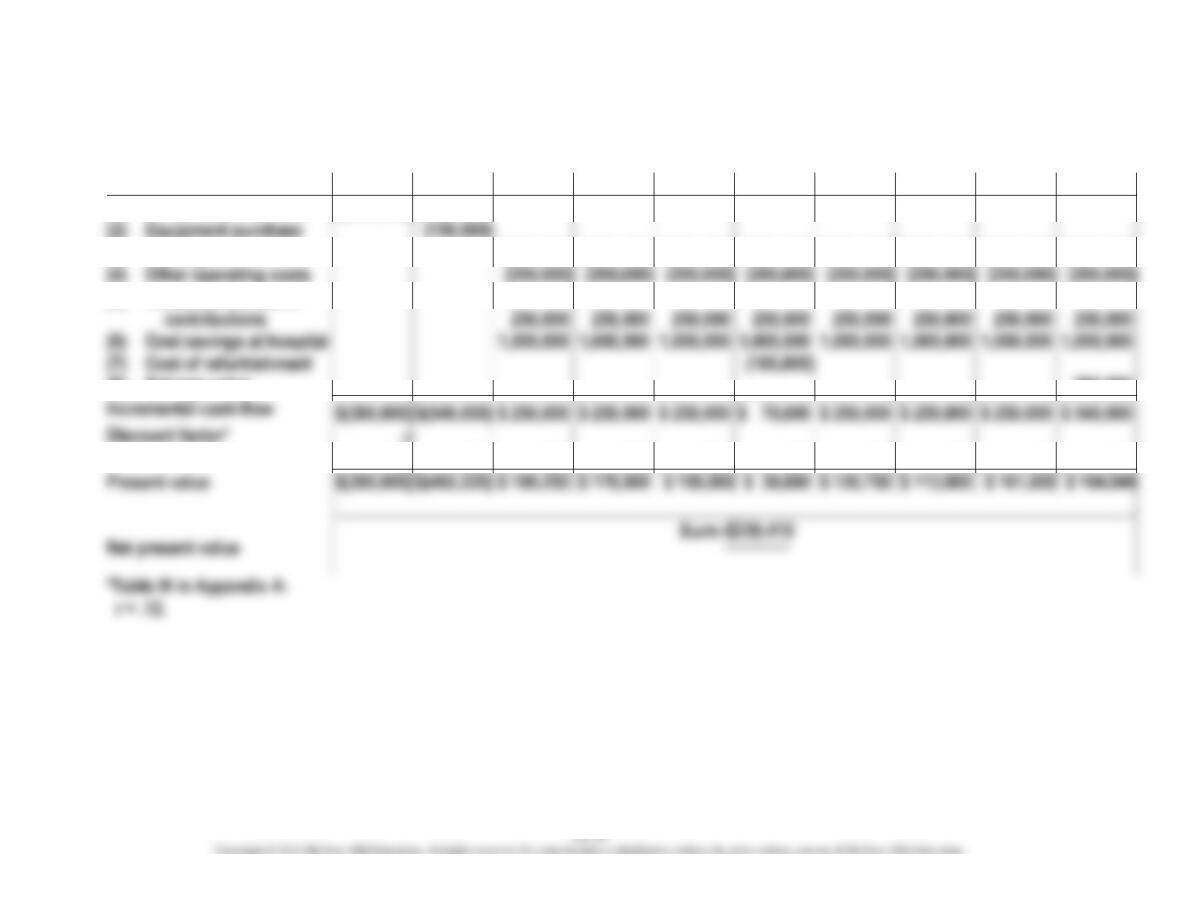

PROBLEM 16-41 (60 MINUTES)

Time 0

Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Year 7

Year 8

Year 9

Year 10

Contract with Diagnostic

Testing Services

Flat fee

$ (80,000)

$ (80,000)

$ (80,000)

$ (80,000)

$ (80,000)

$ (80,000)

$ (80,000)

$ (80,000)

$ (80,000)

$ (80,000)

Total cash flow

Present value

Establish In-House

Testing Lab

Rental of storage space

$ (30,000)

$ (30,000)

$ (30,000)

$ (30,000)

$ (30,000)

$ (30,000)

$ (30,000)

$ (30,000)

$ (30,000)

$ (30,000)

Equipment

Staff

Fixed operating costs

Total cash flow

Present value

PROBLEM 16-42 (45 MINUTES)

The only cash flows listed in the problem that are not annual cash flows are the purchases

of equipment for the proposed lab at time 0 (now) and at the end of year 4. Therefore, the

most efficient way to apply the incremental cost approach is to calculate the incremental

annual cash flows with the proposed lab, and then use the annuity discount factor to

compute the present value.

Incremental annual cash flows associated with proposed diagnostic testing lab:

Rental of storage space …………………………..………………………………….

$ (30,000

)

Staff compensation ……………………………………………………………………..

(200,000

)

Fixed operating costs ………………………………………………………………….

(50,000

)

(250,000

)

100,000

Subtotal ……………………………………………………………………………………..

$(430,000

)

Flat fee ……………………………………………………………………….

400,000

Subtotal ……………………………………………………………………………………..

Add: Contribution margin on cases

currently referred elsewhere ……………………………………………..

100,000

Incremental annual cash flow with proposed lab …………………………..

$ 150,000

Annuity discount factor (Table IV in Appendix A: r = .12, n = 10) ……

5.650

Present value of incremental annual cash flows …………………………...

$ 847,500

Deduct: Present value of equipment purchases:

Net present value of incremental cash flows

*

A tabular presentation of the incremental cost approach, along the lines of Exhibit

16-5, would be more cumbersome than necessary given the equivalent annual cash flows

(excluding the equipment purchases).

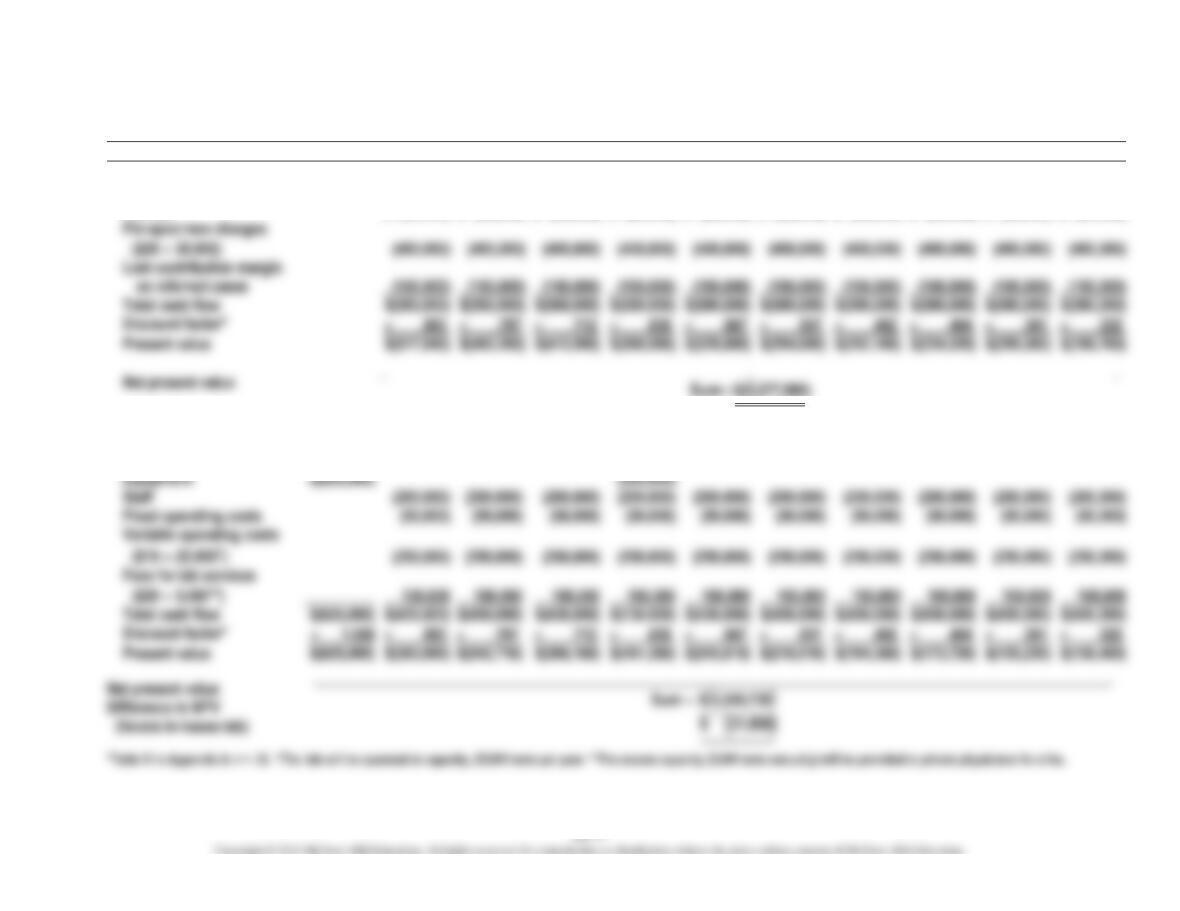

PROBLEM 16-43 (50 MINUTES)

1. See the following table.

2. See the following table.

3. See the following table.

Chapter 16 – Capital Expenditure Decisions

PROBLEM 16-43 (CONTINUED)

Type of Cash Flow

20×0

20×1

20×2

20×3

20×4

20×5

20×6

20×7

20×8

20×9

(1) Construction of clinic

$(390,000)

$(390,000)

(2) Equipment purchase

(3) Staffing

$(800,000)

$(800,000)

$(800,000)

$(800,000)

$(800,000)

$(800,000)

$(800,000)

$(800,000)

(4) Other operating costs

250,000

250,000

250,000

250,000

250,000

250,000

250,000

250,000

(6) Cost savings at hospital

(7) Cost of refurbishment

(5) Increased charitable

(9) Salvage value

290,000

$(390,000)

$(540,000)

$ 70,000

1.000

.893

.797

.712

.636

.567

.507

.452

.404

.361

$(390,000)

$(482,220)