CHAPTER 20 Variable Costing for Management Analysis

Prob. 20–1B (FIN MAN); Prob. 5–1B (MAN)

1.

Sales $2,150,000

Cost of goods sold:

2.

Sales $2,150,000

Variable cost of goods sold:

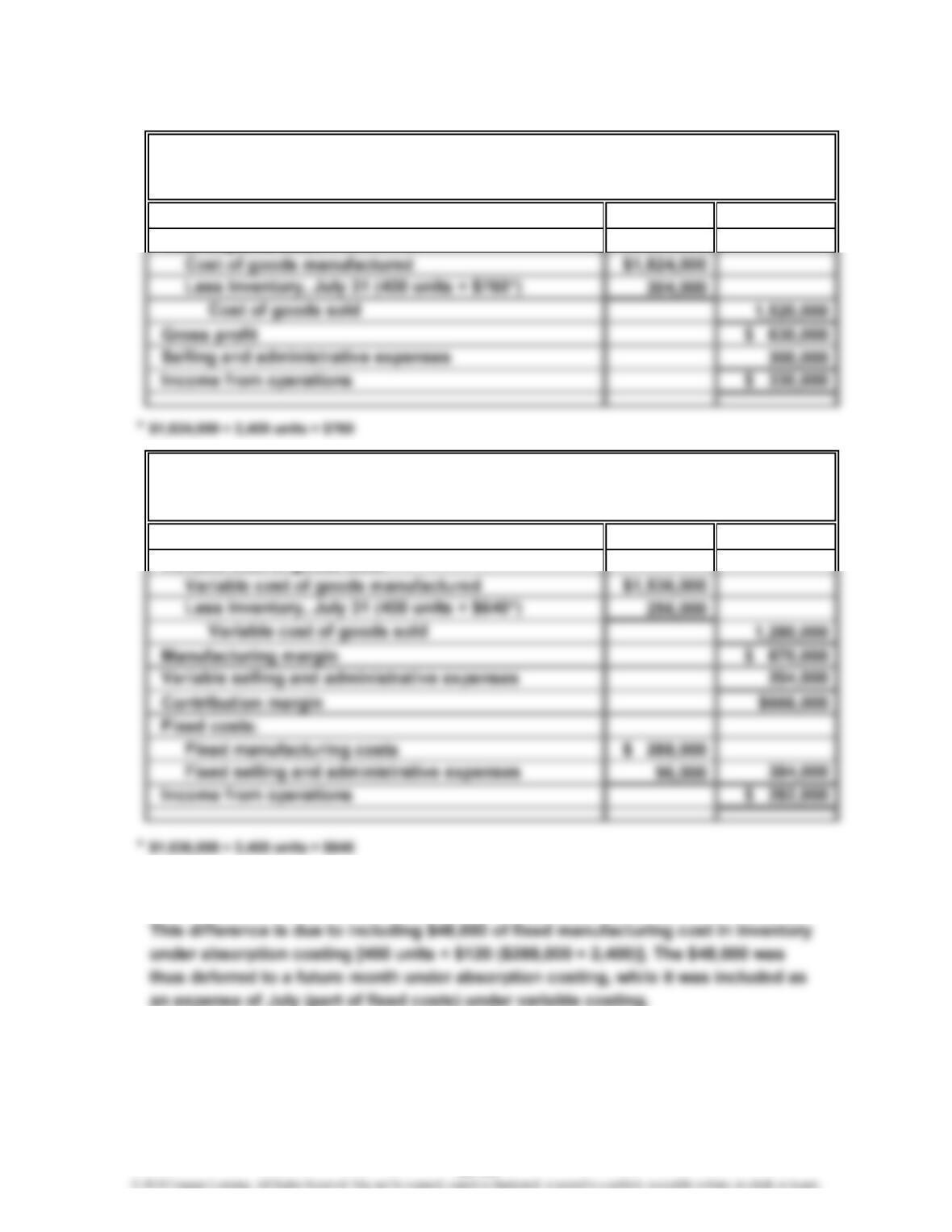

3. The income from operations reported under absorption costing exceeds the income

from operations reported under variable costing by $48,000 ($330,000 – $282,000).

YOSAN INC.

Variable Costing Income Statement

For the Month Ended July 31, 2014

YOSAN INC.

Absorption Costing Income Statement

For the Month Ended July 31, 2014

20-35

CHAPTER 20 Variable Costing for Management Analysis

Prob. 20–2B (FIN MAN); Prob. 5–2B (MAN)

1.

Sales (320,000 units) $25,600,000

Cost of goods sold:

2.

Sales (320,000 units) $25,600,000

Variable cost of goods sold:

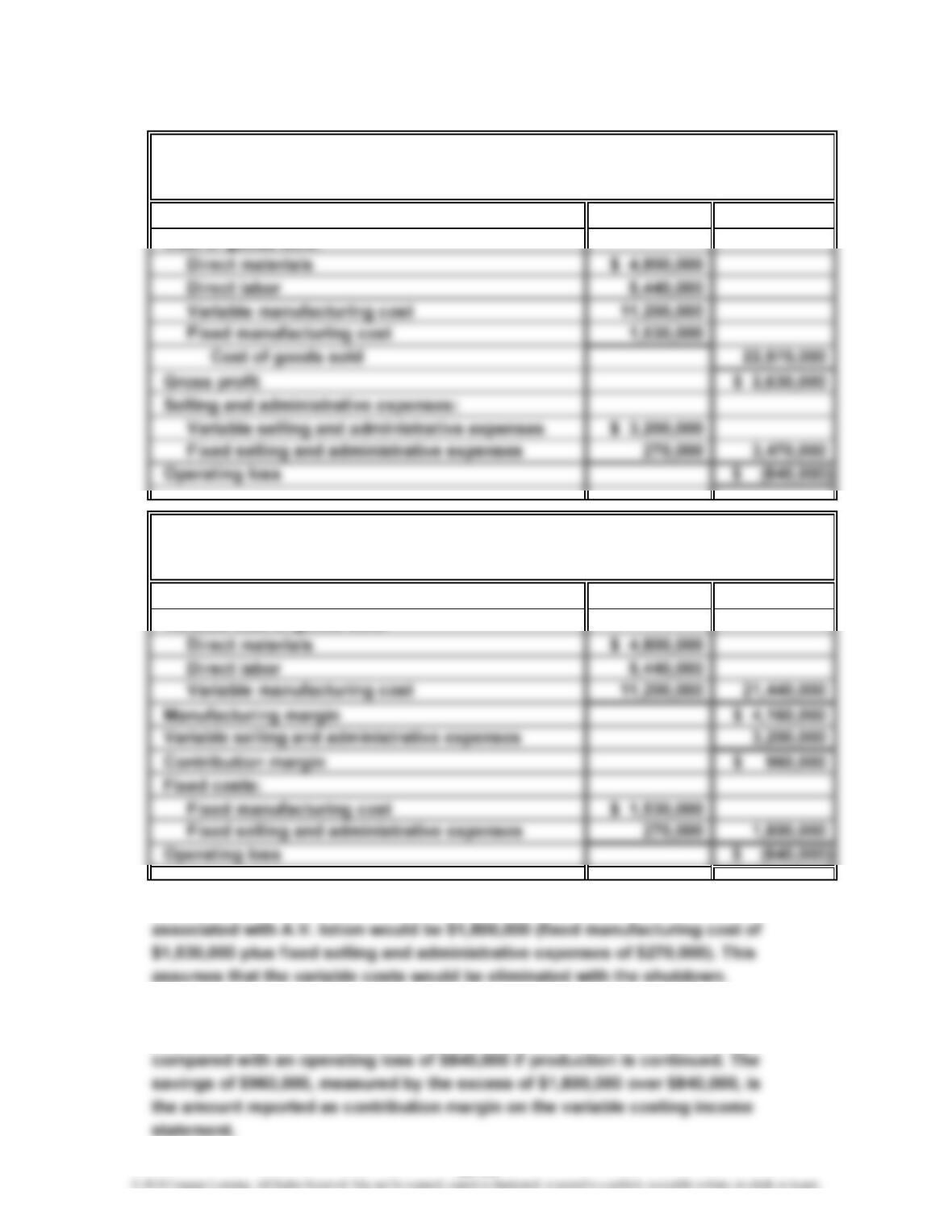

3. $1,800,000. The operating loss from temporarily closing the portion of the plant

4. Production of A.V. lotion should be continued. Temporary suspension of

production would result in an operating loss of $1,800,000 [from (3) above],

SMOOTH SKIN CARE PRODUCTS INC.

Estimated Income Statement—Absorption Costing—Aloe Vera Hand Lotion

For the Month Ending February 28, 2014

For the Month Ending February 28, 2014

Estimated Income Statement—Variable Costing—Aloe Vera Hand Lotion

SMOOTH SKIN CARE PRODUCTS INC.

20-36

CHAPTER 20 Variable Costing for Management Analysis

Prob. 20–3B (FIN MAN); Prob. 5–3B (MAN)

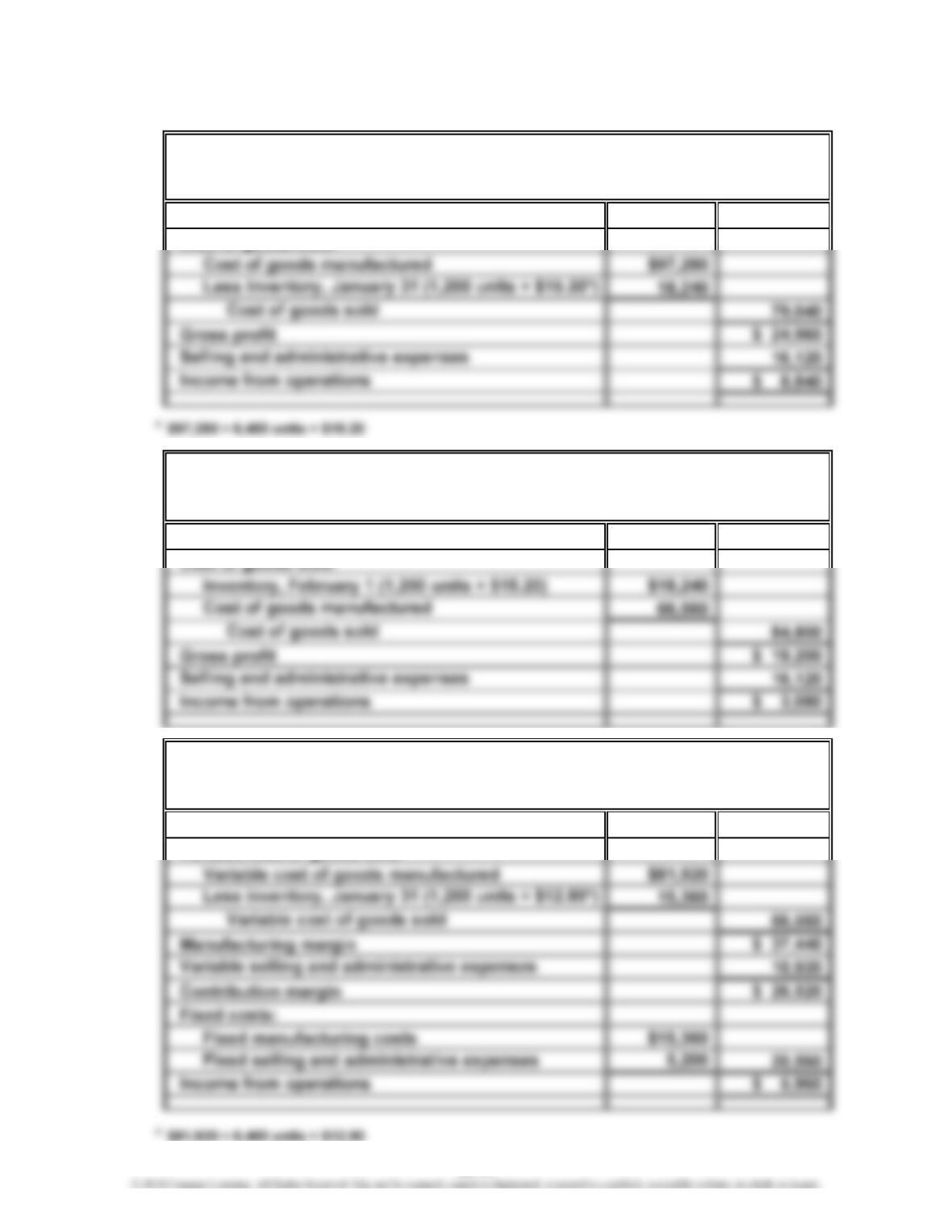

1. a.

Sales $104,000

Cost of goods sold:

b.

Sales $104,000

2. a.

Sales $104,000

Variable cost of goods sold:

For the Month Ended January 31, 2014

HEAD GEAR INC.

Absorption Costing Income Statement

For the Month Ended February 28, 2014

Variable Costing Income Statement

HEAD GEAR INC.

Absorption Costing Income Statement

For the Month Ended January 31, 2014

HEAD GEAR INC.

20-37

CHAPTER 20 Variable Costing for Management Analysis

Prob. 20–3B (FIN MAN); Prob. 5–3B (MAN) (Concluded)

2. b.

Sales $104,000

Variable cost of goods sold:

3. a. For January, the income from operations reported under absorption costing

exceeds the income from operations reported under variable costing by

b. For February, the income from operations reported under absorption costing

4. Head Gear Inc. was equally profitable in January and in February under the variable

costing concept. Sales and the variable cost per unit were the same for both January

and February. The difference in income reported under the absorption costing

HEAD GEAR INC.

Variable Costing Income Statement

For the Month Ended February 28, 2014

20-38

CHAPTER 20 Variable Costing for Management Analysis

Prob. 20–4B (FIN MAN); Prob. 5–4B (MAN)

1.

Variable

Variable Cost Selling

of Goods Sold Expenses Contribution

Contribution as a Percent as a Percent Margin

Salesperson Margin of Sales of Sales Ratio

Asarenka $157,500 45.0% 19.0% 36.0%

2. Crowell has the highest contribution margin and contribution margin ratio for

the year. This is because of two factors. First, Crowell had the smallest variable

3. Other factors that should be considered in evaluating the performance of

PACHEC INC.

Salespersons’ Analysis

For the Year Ended June 30, 2014

20-39

CHAPTER 20 Variable Costing for Management Analysis

Prob. 20–5B (FIN MAN); Prob. 5–5B (MAN)

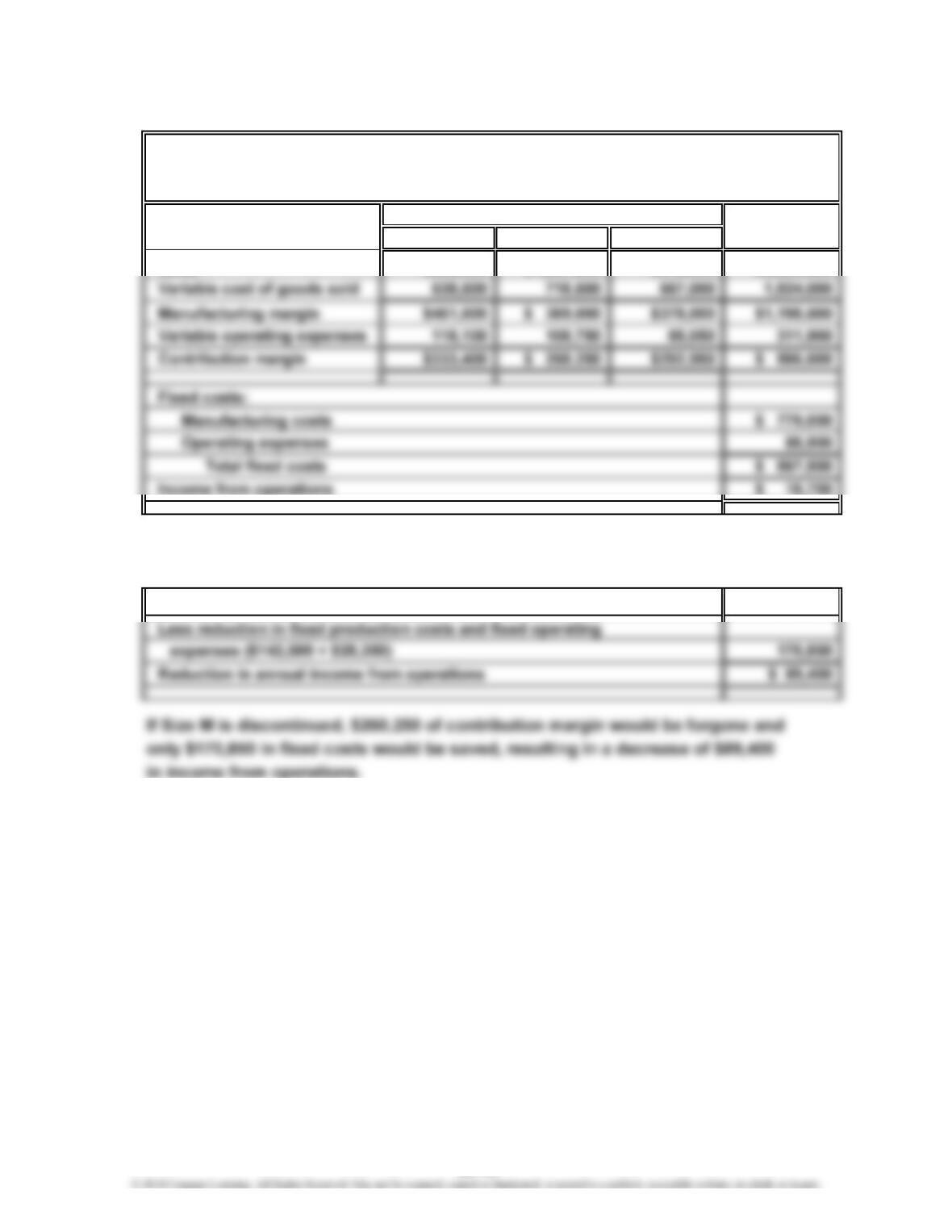

1.

S M L Total

Sales $990,000 $1,087,500 $945,000 $3,022,500

2. Annual income from operations would be reduced below its present level by

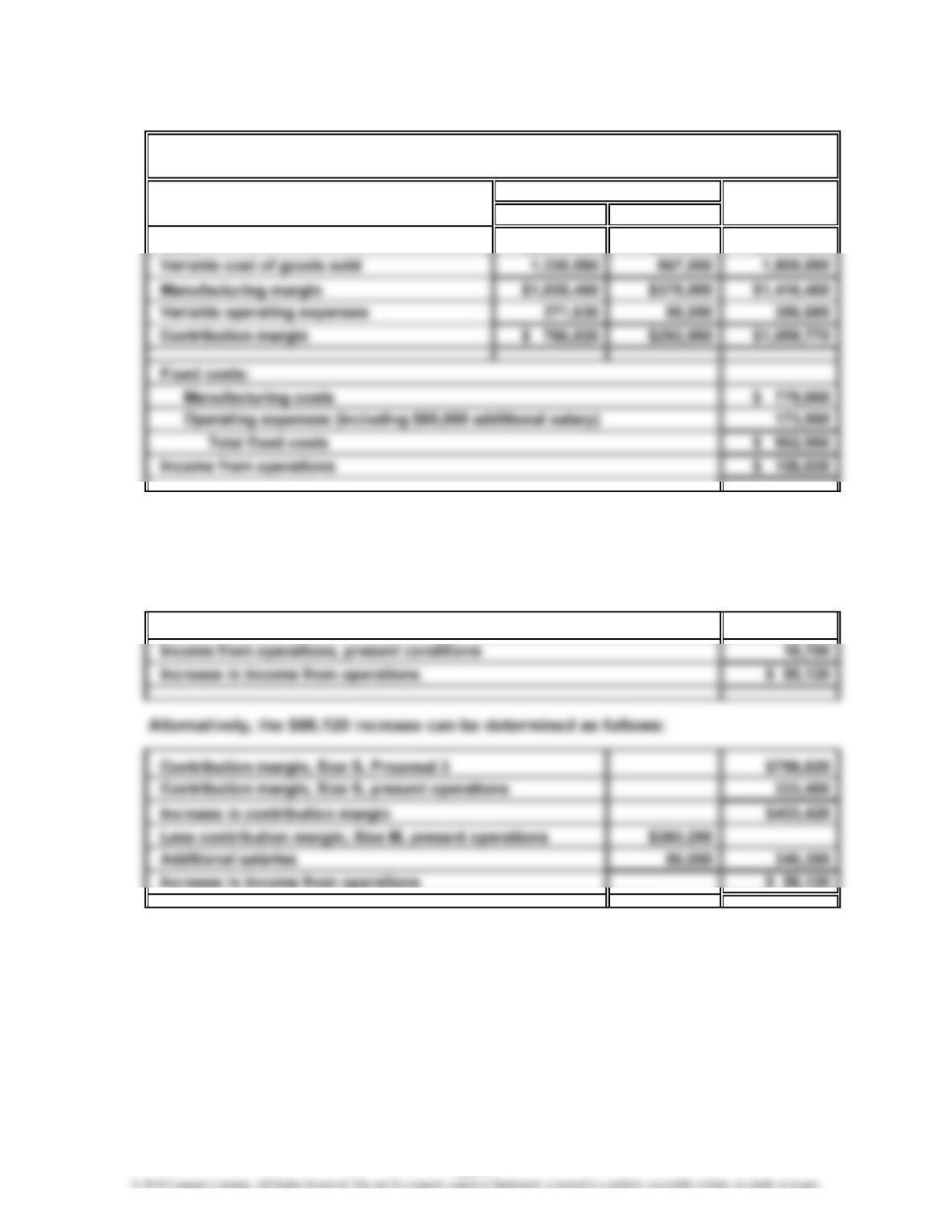

$89,400 if Size M were to be discontinued (Proposal 2), as indicated below.

Contribution margin for Size M $260,250

KIMBRELL, INC.

For the Year Ended January 31, 2015

Contribution Margin by Size Segment

Size

20-40

CHAPTER 20 Variable Costing for Management Analysis

Prob. 20–5B (FIN MAN); Prob. 5–5B (MAN) (Concluded)

3.

S L Total

Sales $2,277,000 $945,000 $3,222,000

4. $88,120. A comparison of the amount of income from operations under

present conditions, as indicated in (1), and under Proposal 3, as indicated in

(3), suggests an increase of $88,120 if Proposal 3 is accepted, as illustrated

below.

Income from operations, Proposal 3 $106,820

Size

KIMBRELL, INC.

Contribution Margin—Proposal 3

20-41

CHAPTER 20 Variable Costing for Management Analysis

Prob. 20–6B (FIN MAN); Prob. 5–6B (MAN)

1.

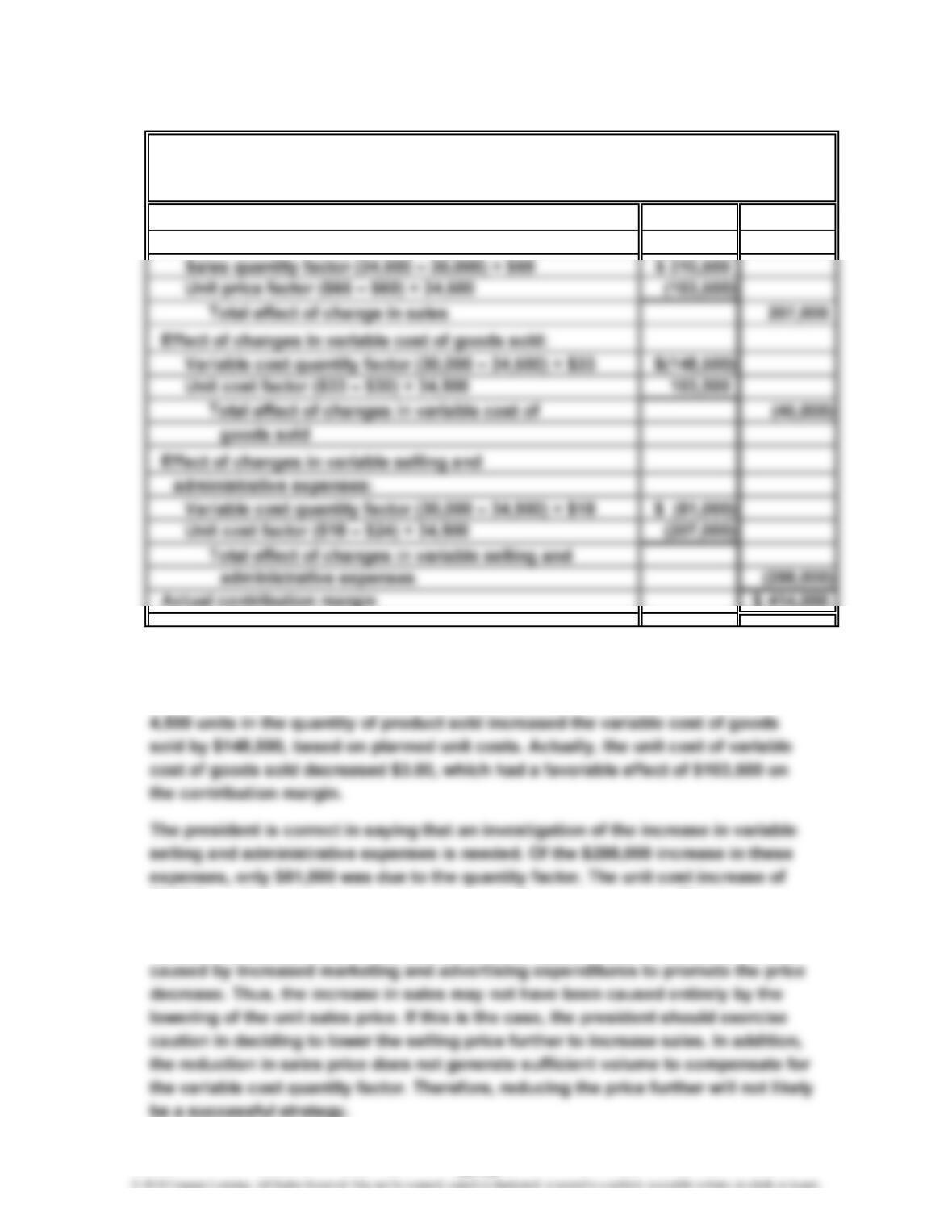

Planned contribution margin $540,000

Effect of change in sales:

2. No, the president is not correct in saying that the variable cost of goods sold got

out of control in 2014. The majority of the increase in the variable cost of goods

sold was due to the variable cost quantity factor. Specifically, the increase of

$6.00 for selling and administrative expenses does raise concern. This increase

may have been caused by additional selling expenses associated with the increased

sales. The increase in selling and administrative expenses also could have been

MATHEWS COMPANY

Contribution Margin Analysis

For the Year Ended December 31, 2014

20-42

CHAPTER 20 Variable Costing for Management Analysis

CP 20–1 (FIN MAN); CP 5–1 (MAN)

Aston Melon has performed the task requested by the division manager. However,

Aston Melon has not exercised good judgment, to the point of bordering on

unethical behavior. Aston Melon should question the wisdom of manipulating

the amount of inventory solely for purposes of meeting numerical profit targets.

CASES & PROJECTS

CHAPTER 20 Variable Costing for Management Analysis

CP 20–2 (FIN MAN); CP 5–2 (MAN)

1. Absorption costing is required under generally accepted accounting principles.

Under this approach, the fixed manufacturing costs are allocated to sold and

inventoried units. Thus, if production exceeds sales, a portion of the fixed

2. Gordon is incorrect in implying that nothing can be done because of generally

accepted accounting principles (GAAP). GAAP is required for external financial

reporting. However, the income reports used to guide management may be

20-44

CP 20–3 (FIN MAN); CP 5–3 (MAN)

Martin is earning more contribution margin than Dean; however, both salespersons

are earning the same contribution margin ratio. Dean’s total sales are less than

Martin’s. However, the manufacturing margin ratio is much different between the

two salespersons. Dean is selling products with a much higher manufacturing

CP 20–4 (FIN MAN); CP 5–4 (MAN)

1. Danica Kyle Richard Tom

2. Danica has the highest contribution margin and contribution margin ratio of the

four salespersons, even though Danica’s sales level is ranked third. There are

two reasons for Danica’s superior performance. First, Danica sells products that

20-45

CP 20–5 (FIN MAN); CP 5–5 (MAN)

1.

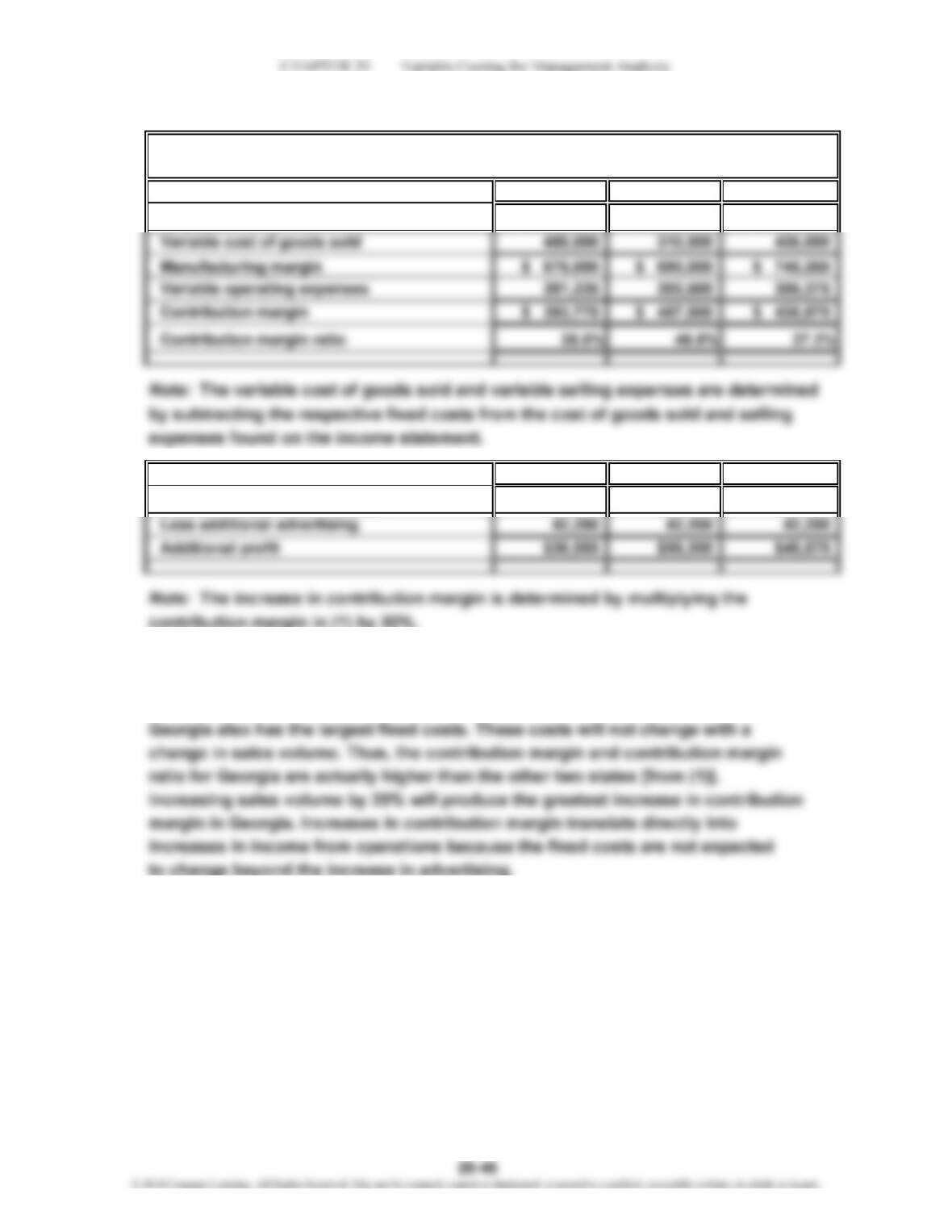

Florida Georgia Tennessee

Revenue $1,125,000 $1,000,000 $1,181,250

2. Florida Georgia Tennessee

Increase in contribution margin $78,755 $97,500 $87,775

3. Georgia will generate the greatest profit increase for an additional $42,200

in advertising. This may seem surprising, because the profit report indicates

that Georgia is the least profitable on an absorption costing basis. However,

TRANS SPORT COMPANY

Contribution Margin by State

CP 20–6 (FIN MAN); CP 5–6 (MAN)

1.

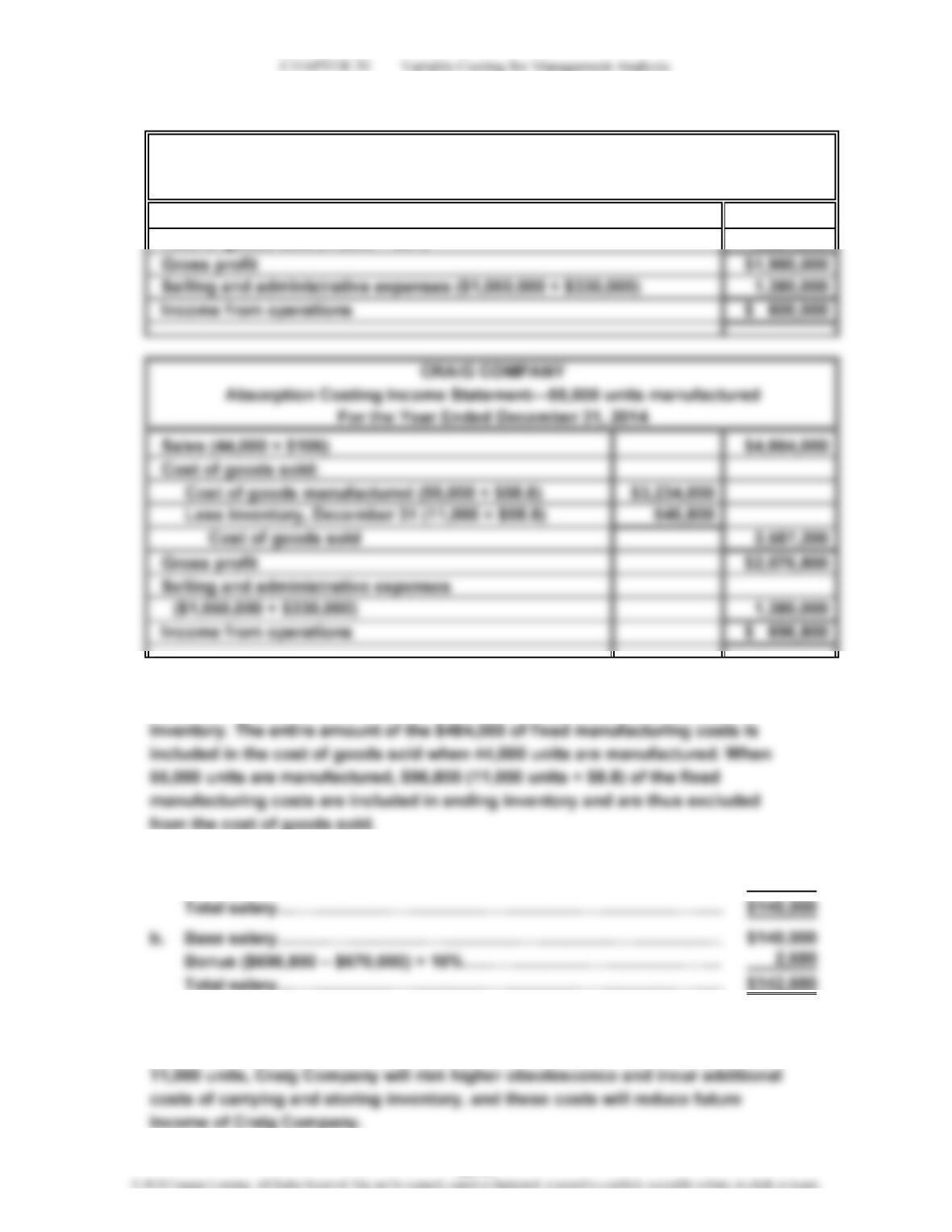

Sales (44,000 × $106) $4,664,000

Cost of goods sold (44,000 × $61) 2,684,000

2. The $96,800 difference in the amount of income from operations ($696,800 –

$600,000) is due to the allocation of fixed manufacturing costs to ending

3. a. Base salary……………………………………………………………………

…

$140,000

Bonus ($600,000 – $670,000) × 10%………………………………………

…

—

…

…

…

…

4. By manufacturing 55,000 units, Pinder increased his salary by $2,680.

Note: Instructors may also point out that by increasing the ending inventory by

CRAIG COMPANY

Absorption Costing Income Statement—44,000 units manufactured

For the Year Ended December 31, 2014

20-47

CP 20–6 (FIN MAN); CP 5–6 (MAN) (Concluded)

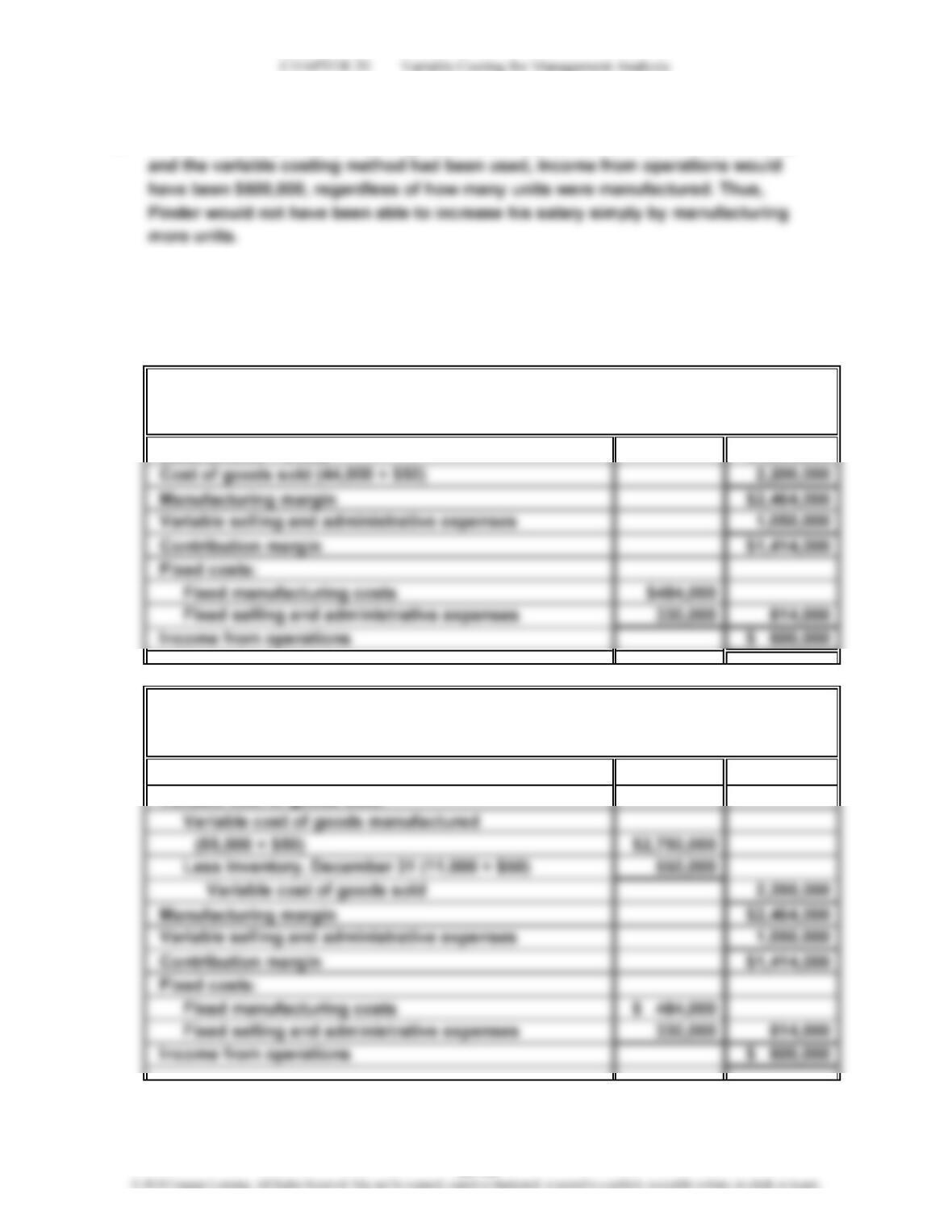

5. If Pinder’s salary were $140,000 (plus a bonus based on income from operations)

Note: Instructors may ask students to verify that income from operations, using

the variable costing method, would be $600,000 regardless of whether 44,000 or

55,000 units are manufactured. The variable costing income statements are as

follows:

Sales (44,000 × $106) $4,664,000

Sales (44,000 × $106) $4,664,000

Variable cost of goods sold:

CRAIG COMPANY

Variable Costing Income Statement—55,000 units manufactured

For the Year Ended December 31, 2014

CRAIG COMPANY

Variable Costing Income Statement—44,000 Units Manufactured

For the Year Ended December 31, 2014

20-48