CHAPTER 20 Variable Costing for Management Analysis

Ex. 20–16 (FIN MAN); Ex. 5–16 (MAN)

a. Filmed

Entertainment Networks Publishing

Revenues……………………………

…

$11,784.0 $13,562.0 $6,328.0

b. The Filmed Entertainment and Networks segments sell an information or media

product that has a very small variable cost per unit. For example, the Networks

segment earns revenue monthly from each customer. However, the variable

cost of each customer is rather small. The cost of providing the service is

c. The higher contribution margin ratios of the Filmed Entertainment and Networks

20-21

CHAPTER 20 Variable Costing for Management Analysis

Ex. 20–17 (FIN MAN); Ex. 5–17 (MAN)

a.

Effect of change in sales:

b. The sales will increase by $31,875. If the variable cost per unit were $10, and

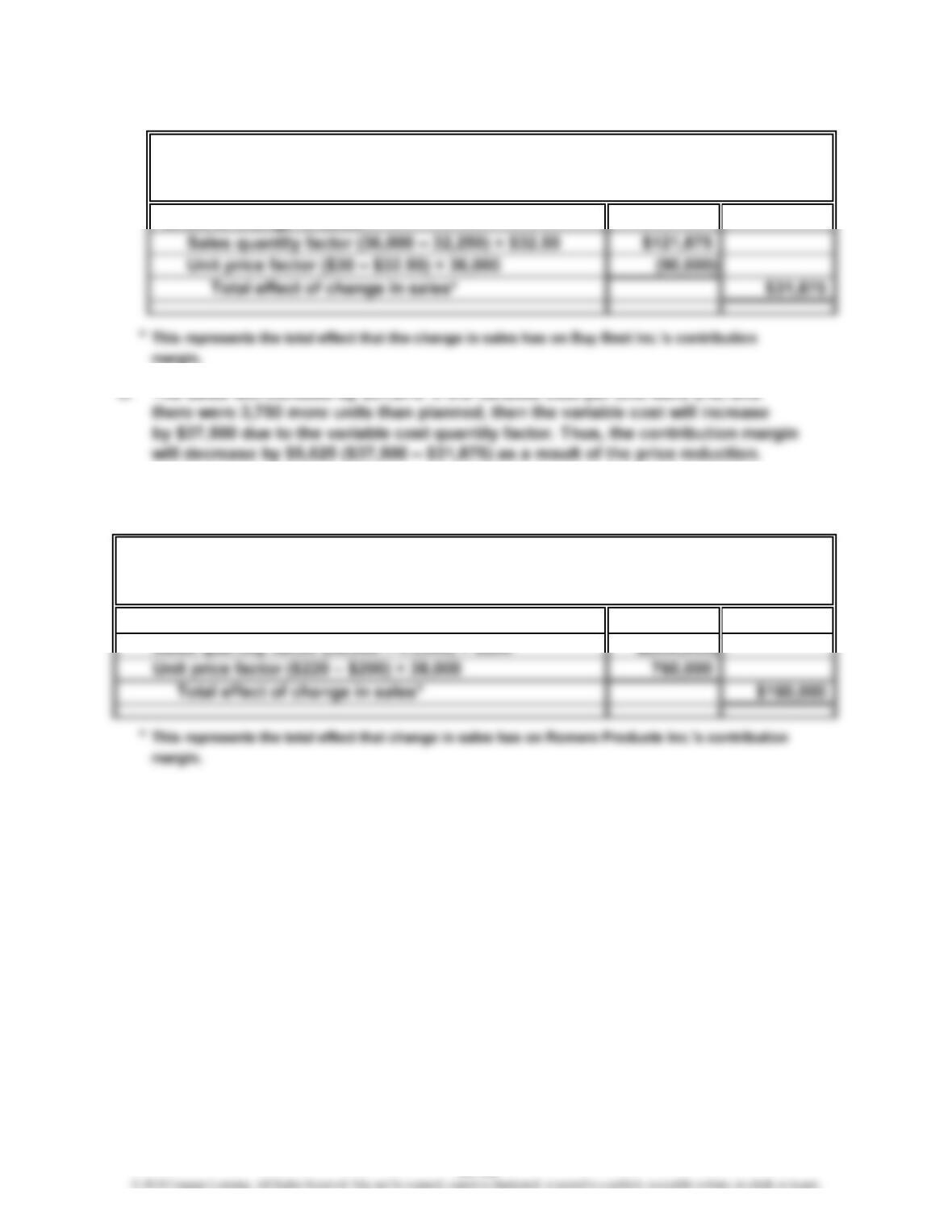

Ex. 20–18 (FIN MAN); Ex. 5–18 (MAN)

Effect of change in sales:

Sales quantity factor (38,000 – 41,000) × $200 $(600,000)

BUY BEST INC.

ROMERO PRODUCTS INC.

Contribution Margin Analysis—Sales

For the Year Ended December 31, 2014

Contribution Margin Analysis—Sales

For the Year Ended December 31, 2015

20-22

CHAPTER 20 Variable Costing for Management Analysis

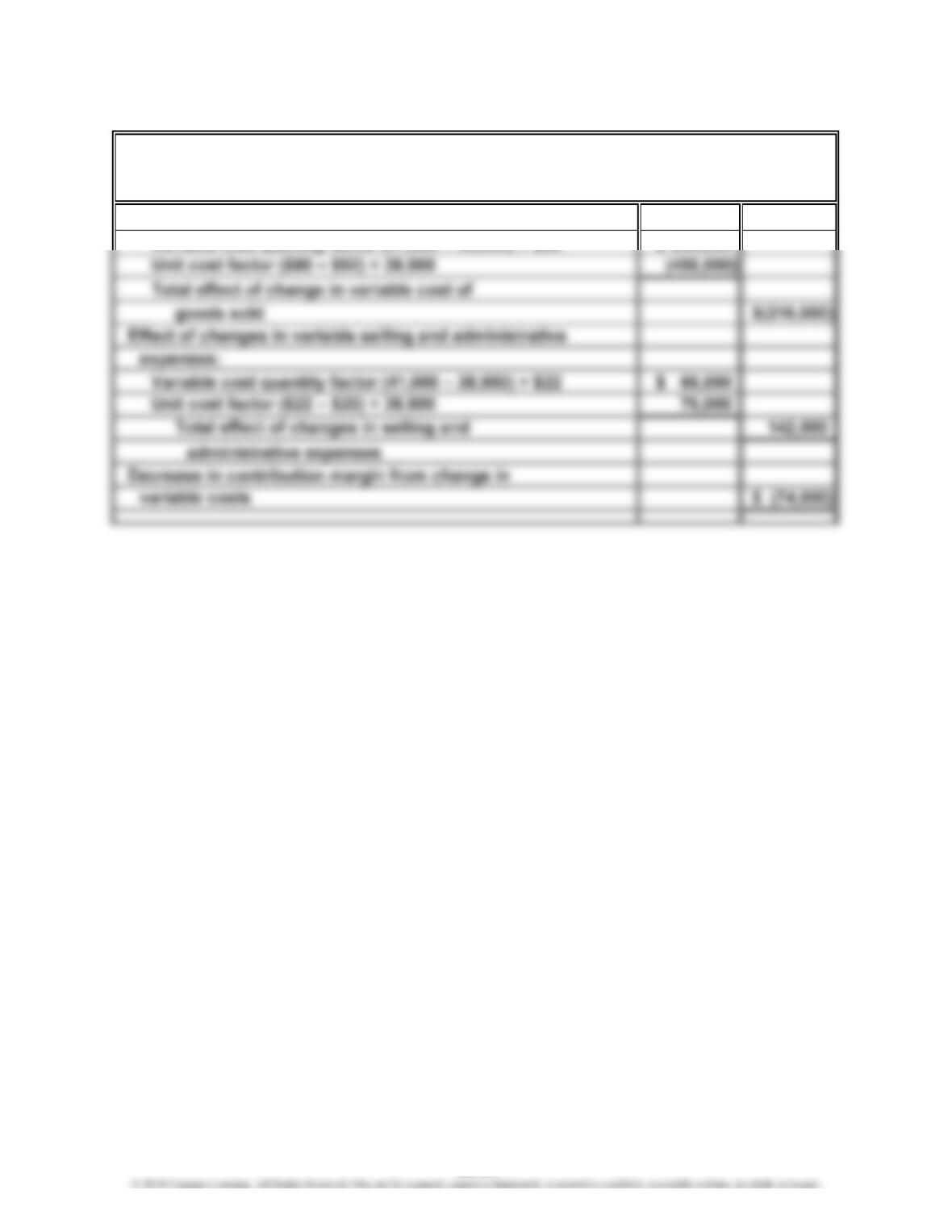

Ex. 20–19 (FIN MAN); Ex. 5–19 (MAN)

Effect of changes in variable costs of goods sold:

Variable cost quantity factor (41,000 – 38,000) × $80 $ 240,000

ROMERO PRODUCTS INC.

Contribution Margin Analysis—Variable Costs

For the Year Ended December 31, 2014

20-23

CHAPTER 20 Variable Costing for Management Analysis

Ex. 20–20 (FIN MAN); Ex. 5–20 (MAN)

a.

Atlanta/ Baltimore/ Pittsburgh/

Baltimore Pittsburgh Atlanta Total

Revenues $255,000 $594,000 $542,080 $1,391,080

Variable costs:

Labor costs for loading

Revenues: Revenue per railcar × Number of railcars

b. The Atlanta/Baltimore route performs significantly worse than do the other two routes.

A close examination of the operating statistics indicates that this route runs very few

EAST COAST RAILROAD

For the Month Ended April 30, 2014

Contribution Margin by Route

20-24

CHAPTER 20 Variable Costing for Management Analysis

Ex. 20–21 (FIN MAN); Ex. 5–21 (MAN)

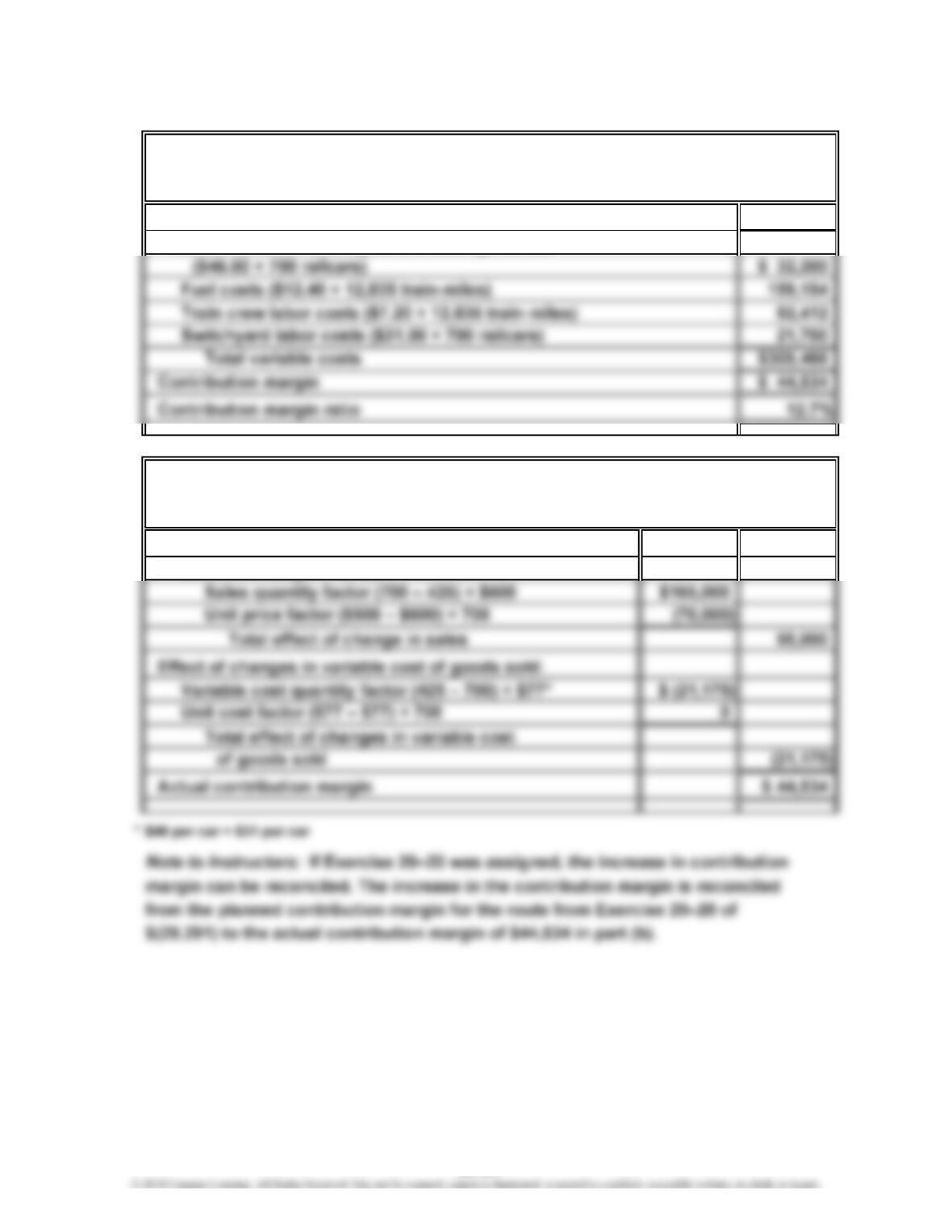

a.

Revenues ($500 × 700 railcars) $350,000

Labor costs for loading and unloading railcars

b.

Planned contribution margin $(29,291)

Effect of change in sales:

Contribution Margin Analysis—Atlanta/Baltimore Route

For the Month Ended May 31, 2014

EAST COAST RAILROAD

Contribution Margin for Atlanta/Baltimore Route

For the Month Ended May 31, 2014

EAST COAST RAILROAD

20-25

CHAPTER 20 Variable Costing for Management Analysis

Ex. 20–22 (FIN MAN); Ex. 5–22 (MAN)

a.

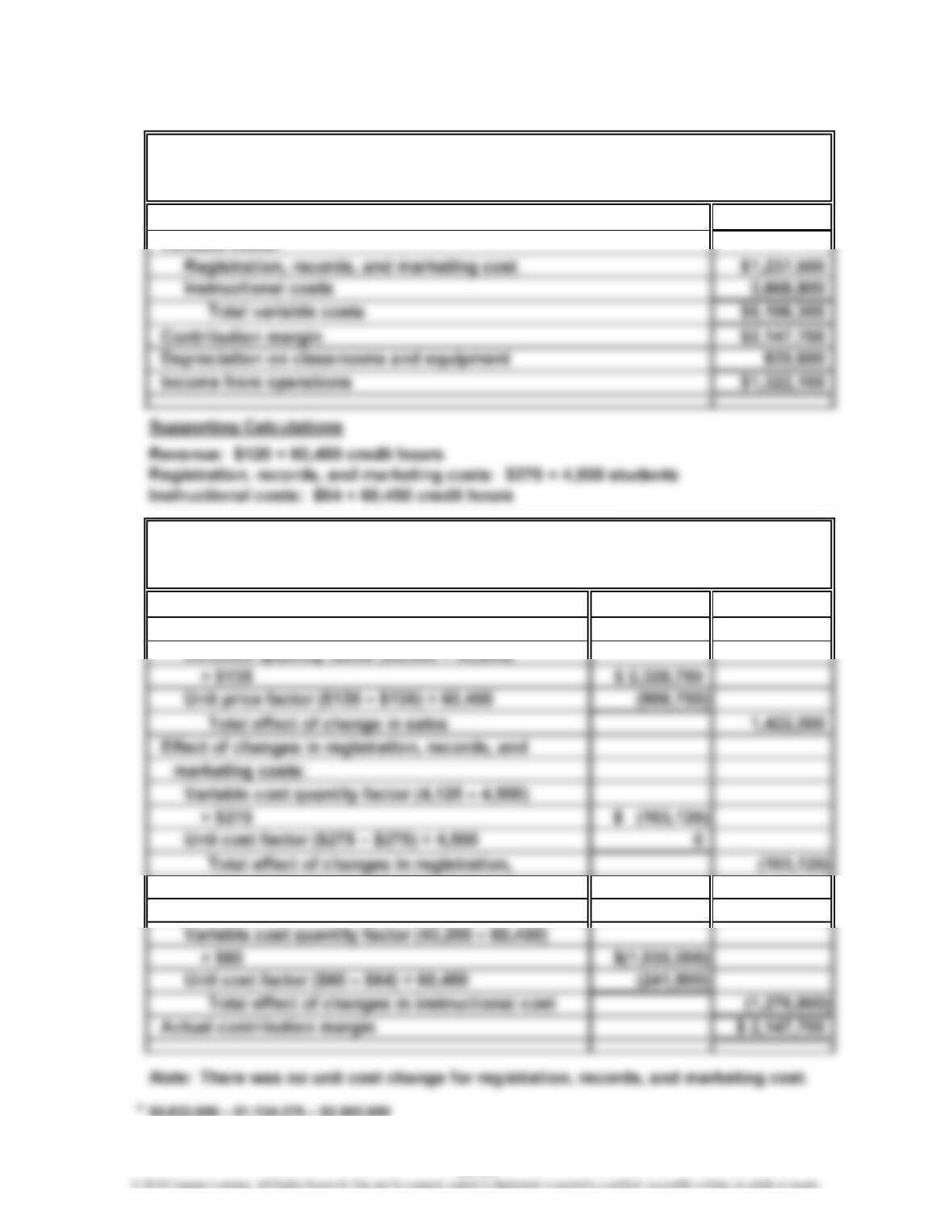

Revenue $7,254,000

Variable costs:

b.

Planned contribution margin* $ 2,105,625

Effect of change in revenue:

records, and marketing costs

Effect of changes in instructional costs:

Contribution Margin Analysis

For the Fall Term 2014

UNDERWATER UNIVERSITY

Variable Costing Income Statement

For the Fall Term 2014

UNDERWATER UNIVERSITY

20-26

CHAPTER 20 Variable Costing for Management Analysis

Prob. 20–1A (FIN MAN); Prob. 5–1A (MAN)

1.

Sales $4,095,000

Cost of goods sold:

2.

Sales $4,095,000

Variable cost of goods sold:

3. The income from operations reported under absorption costing exceeds the

income from operations reported under variable costing by $16,800 ($376,740 –

ICE COLD FRIDGE COMPANY

Variable Costing Income Statement

For the Month Ended May 31, 2014

PROBLEMS

ICE COLD FRIDGE COMPANY

Absorption Costing Income Statement

For the Month Ended May 31, 2014

20-27

CHAPTER 20 Variable Costing for Management Analysis

Prob. 20–2A (FIN MAN); Prob. 5–2A (MAN)

1.

Sales (2,925 units) $315,900

Cost of goods sold:

Direct materials $117,000

2.

Sales (2,925 units) $315,900

Variable cost of goods sold:

Direct materials $117,000

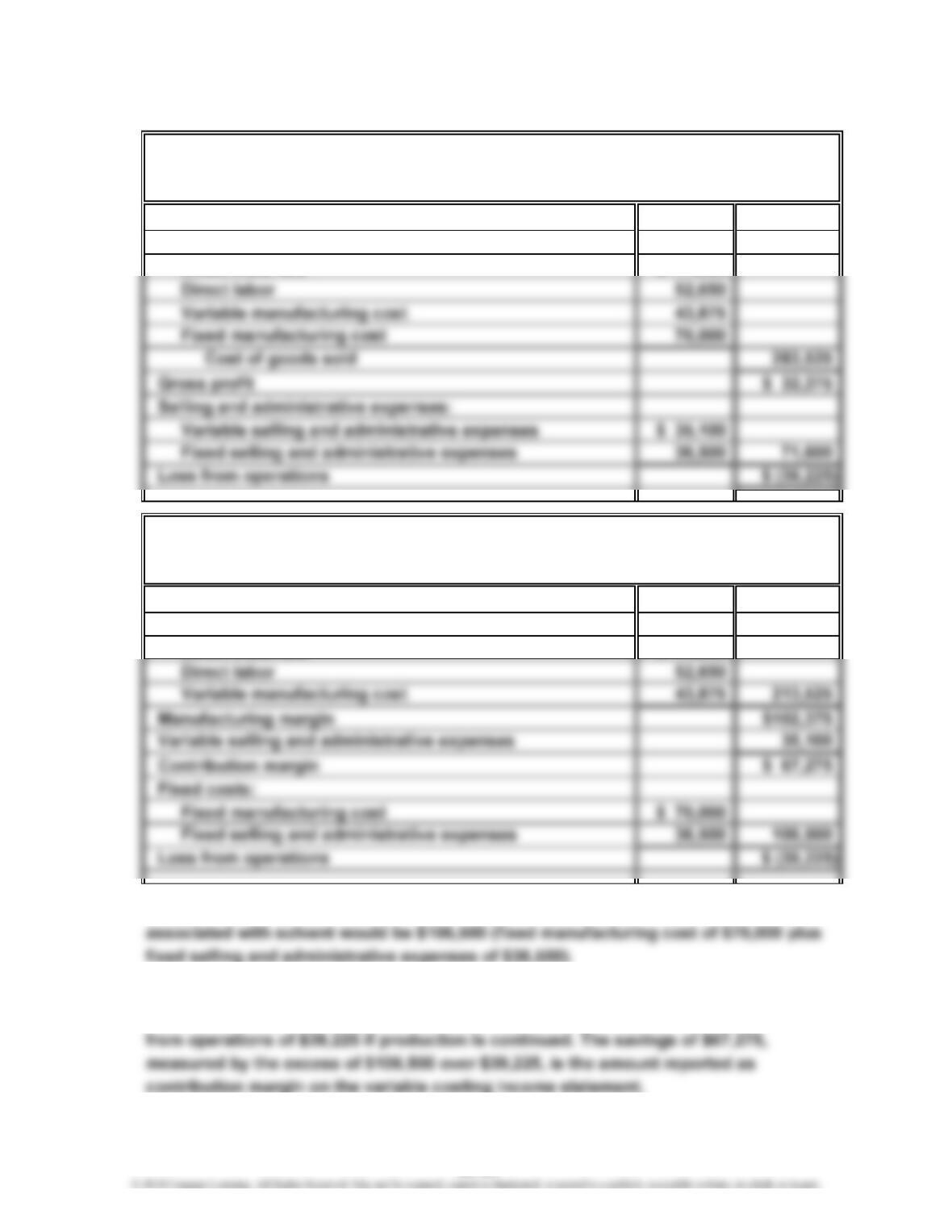

3. $106,500. The loss from operations from temporarily closing the portion of the plant

4. Production of solvent should be continued. Temporary suspension of production

would result in an operating loss of $106,500 [from (3) above], compared with a loss

HEYWARD INDUSTRIES INC.

Estimated Income Statement—Absorption Costing—Solvent

For the Month Ending May 31, 2015

For the Month Ending May 31, 2015

Estimated Income Statement—Variable Costing—Solvent

HEYWARD INDUSTRIES INC.

20-28

CHAPTER 20 Variable Costing for Management Analysis

Prob. 20–3A (FIN MAN); Prob. 5–3A (MAN)

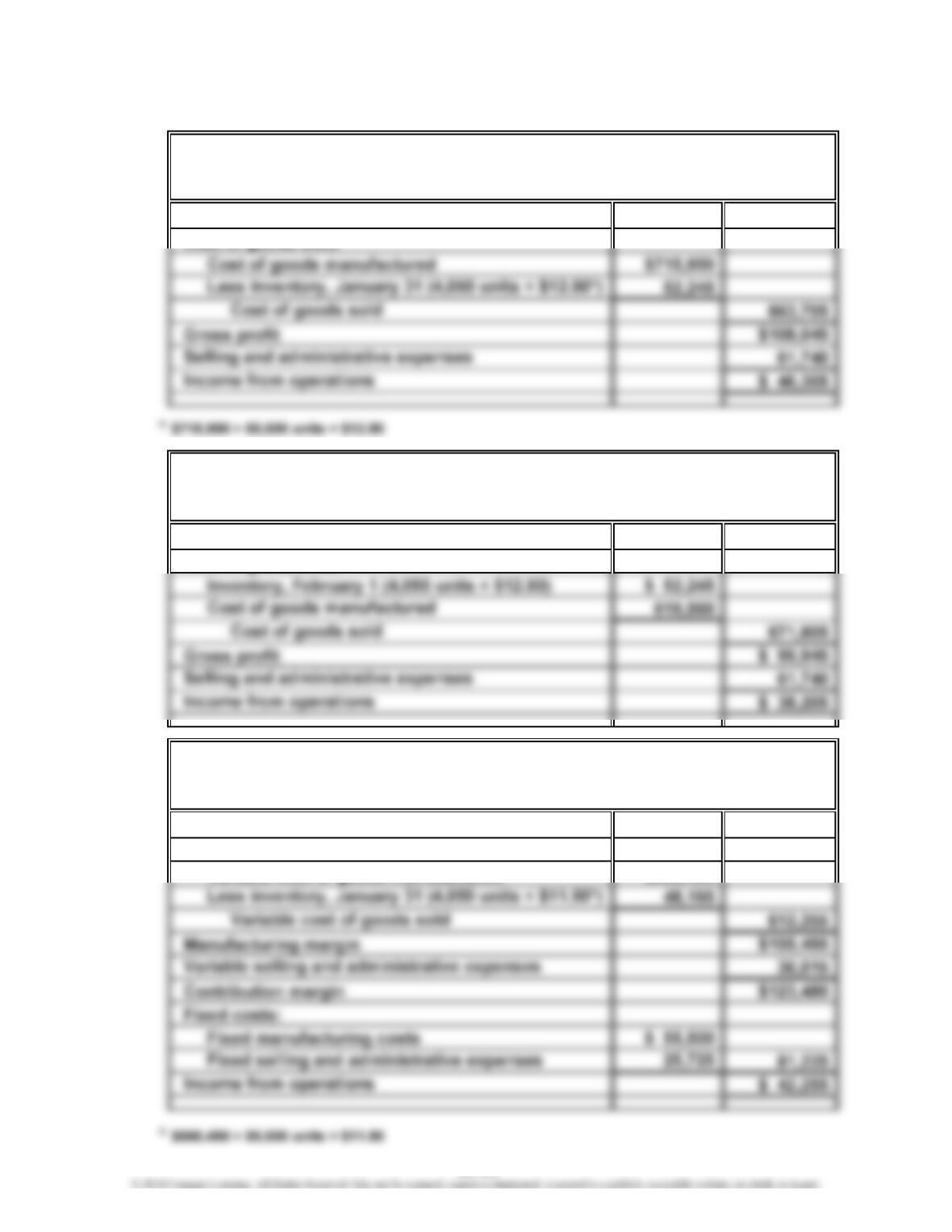

1. a.

Sales $771,750

Cost of goods sold:

b.

Sales $771,750

Cost of goods sold:

2. a.

Sales $771,750

Variable cost of goods sold:

Variable cost of goods manufactured $660,450

For the Month Ended January 31, 2015

HIP AND CONSCIOUS CLOTHING COMPANY

Absorption Costing Income Statement

For the Month Ended February 28, 2015

Variable Costing Income Statement

HIP AND CONSCIOUS CLOTHING COMPANY

Absorption Costing Income Statement

For the Month Ended January 31, 2015

HIP AND CONSCIOUS CLOTHING COMPANY

20-29

CHAPTER 20 Variable Costing for Management Analysis

Prob. 20–3A (FIN MAN); Prob. 5–3A (MAN) (Concluded)

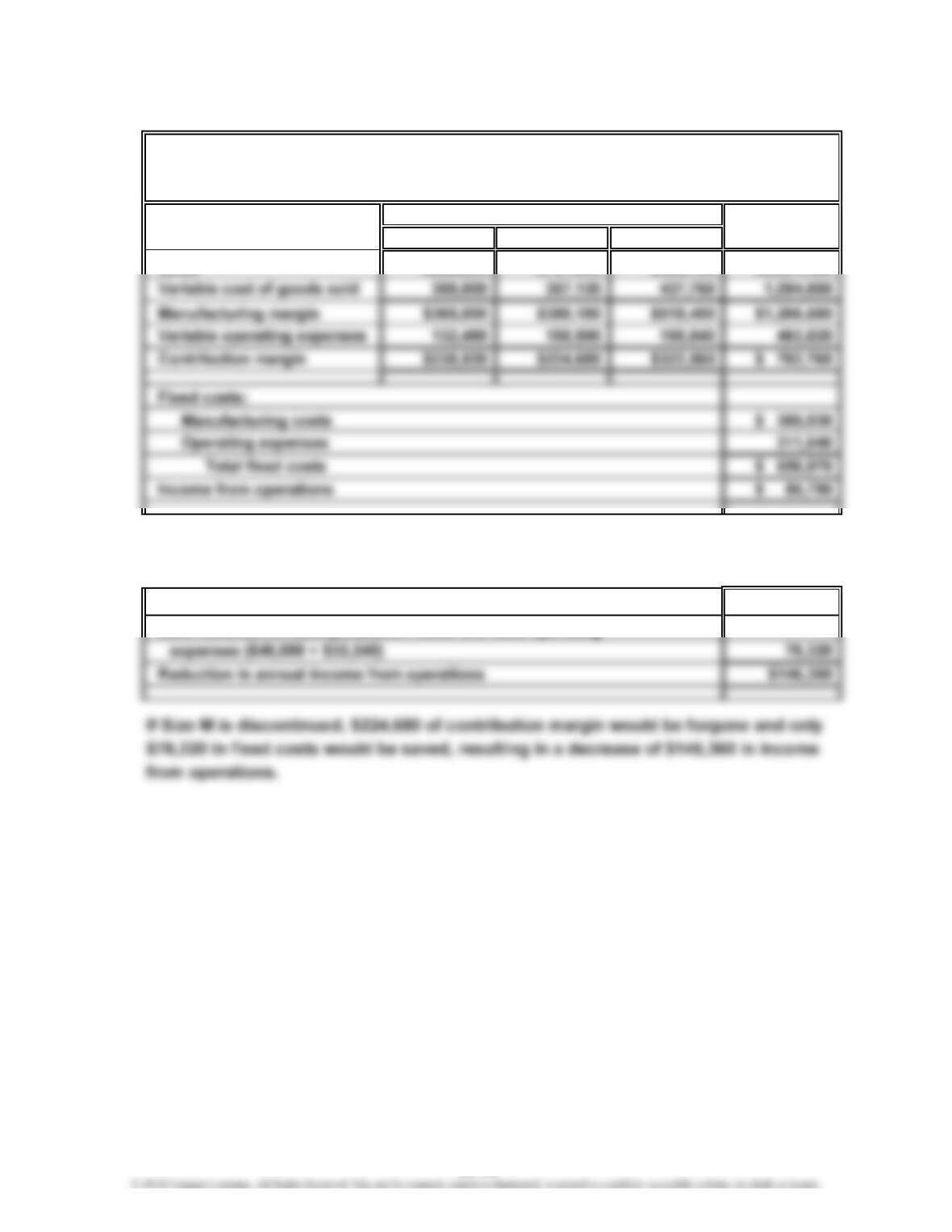

2. b.

Sales $771,750

Variable cost of goods sold:

Inventory, February 1 (4,050 units × $11.90) $ 48,195

3. a. For January, the income from operations reported under absorption costing

exceeds the income from operations reported under variable costing by

b. For February, the income from operations reported under absorption costing

is less than the income from operations reported under variable costing by

4. The Hip and Conscious Clothing Company was equally profitable in January and

February under the variable costing concept. Sales and the variable cost per unit

were the same for both January and February. The difference in income reported

HIP AND CONSCIOUS CLOTHING COMPANY

Variable Costing Income Statement

For the Month Ended February 28, 2015

20-30

CHAPTER 20 Variable Costing for Management Analysis

Prob. 20–4A (FIN MAN); Prob. 5–4A (MAN)

1.

Variable

Variable Cost Selling

of Goods Sold Expenses Contribution

Contribution as a Percent as a Percent Margin

Salesperson Margin of Sales of Sales Ratio

Case $147,560 50.0% 19.0% 31.0%

Dix 139,200 50.0% 21.0% 29.0%

2. Sussman has the highest contribution margin and contribution margin ratio for the

year. This is because of two factors. First, Sussman has the smallest variable cost

3. Other factors that should be considered in evaluating the performance of salespersons

VICTORN INSTRUMENTS COMPANY

Salespersons’ Analysis

For the Year Ended December 31, 2014

20-31

CHAPTER 20 Variable Costing for Management Analysis

Prob. 20–5A (FIN MAN); Prob. 5–5A (MAN)

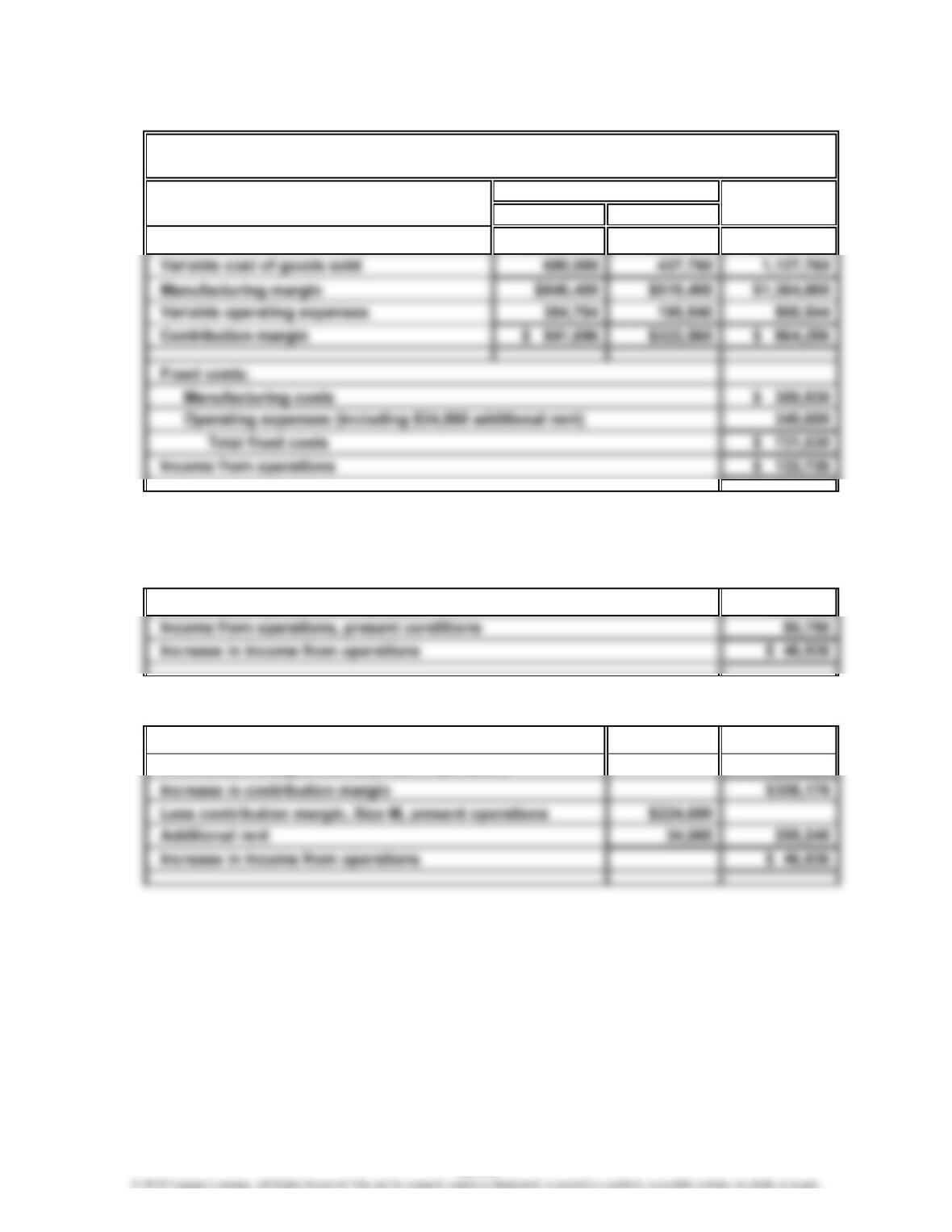

1.

S M L Total

Sales $668,000 $737,300 $956,160 $2,361,460

2. Annual income from operations would be reduced below its present level by $146,360

if Size M were to be discontinued (Proposal 2), as indicated below:

Contribution margin for Size M $224,680

Less reduction in fixed production costs and fixed operating

VALDESPIN COMPANY

For the Year Ended June 30, 2014

Contribution Margin by Size Segment

Size

20-32

CHAPTER 20 Variable Costing for Management Analysis

Prob. 20–5A (FIN MAN); Prob. 5–5A (MAN) (Concluded)

3.

S L Total

Sales $1,536,400 $956,160 $2,492,560

4. $46,936. A comparison of the amount of income from operations under present

conditions, as indicated in (1), and under Proposal 3, as indicated in (3), suggests an

increase of $46,936 if Proposal 3 is accepted, as illustrated below.

Income from operations, Proposal 3 $132,726

Alternatively, the $46,936 increase can be determined as follows:

Contribution margin, Size S, Proposal 3 $541,696

Contribution margin, Size S, present operations 235,520

Size

VALDESPIN COMPANY

Contribution Margin—Proposal 3

20-33

CHAPTER 20 Variable Costing for Management Analysis

Prob. 20–6A (FIN MAN); Prob. 5–6A (MAN)

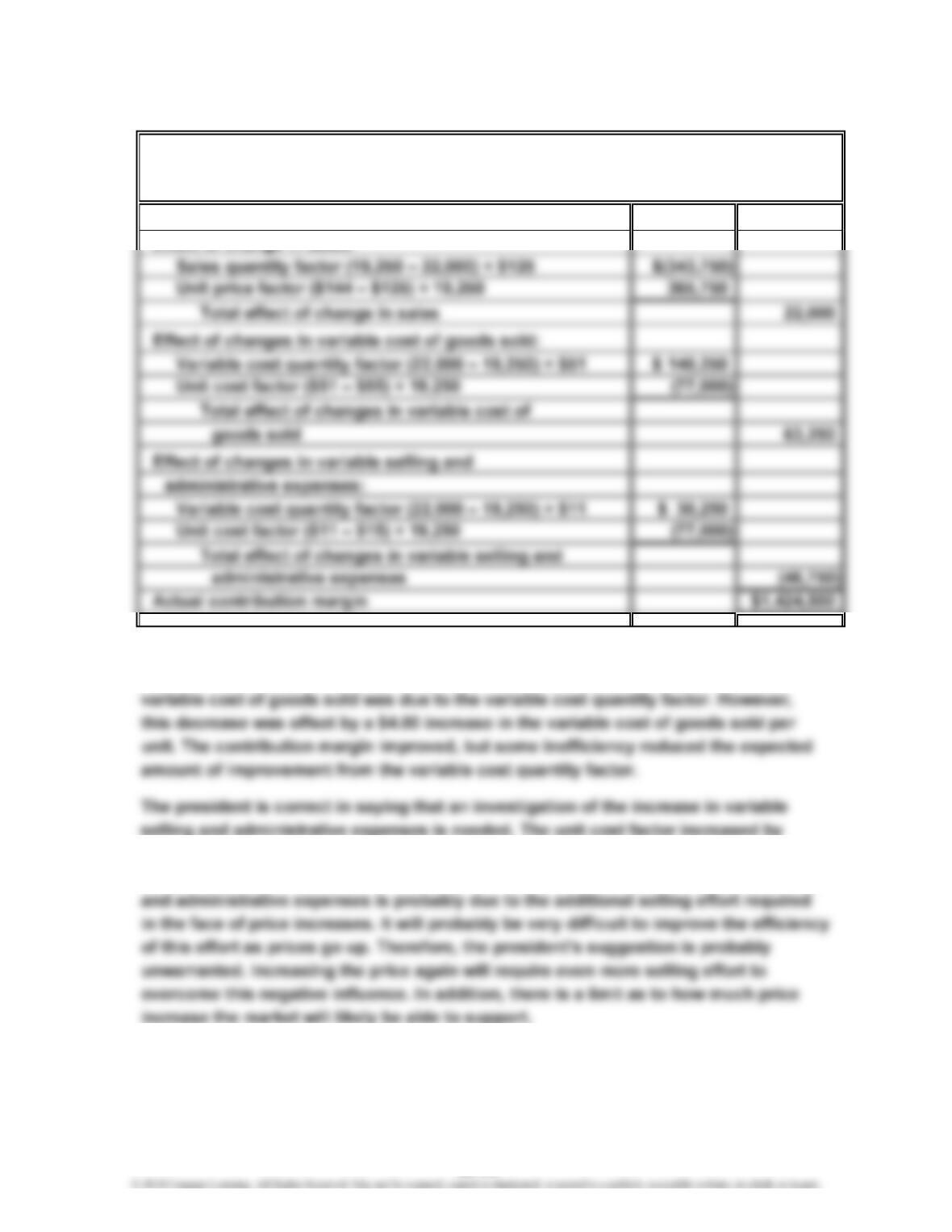

1.

Planned contribution margin $1,386,000

Effect of change in sales:

2. The president’s first statement appears correct taken at face value. The president is

incorrect regarding variable cost of goods sold. The majority of the decrease in the

$4.00, which more than offset the favorable variable cost quantity factor, resulting

in an overall decrease in the contribution margin. The increase in the variable selling

DOZIER INDUSTRIES INC.

Contribution Margin Analysis

For the Year Ended December 31, 2014

20-34