PROBLEM 16-53 (30 MINUTES)

1. Payback period =

inflow cash tax–after annual

investment initial

(a) Mall restaurant:

(b) Downtown restaurant:

2.

Accounting rate of return

=

investment initial

taxes)income

and ondepreciati (including

expenses lincrementa average

revenue

lincrementa

average

−

4. Neither the payback period nor the accounting-rate-of-return method considers the

Chapter 16 – Capital Expenditure Decisions

PROBLEM 16-54 (35 MINUTES)

1. Payback period = 3 years*

2. Accounting rate of return (ARR) using initial investment:

3. Accounting rate of return (ARR) using average investment:

Chapter 16 – Capital Expenditure Decisions

PROBLEM 16-55 (50 MINUTES)

1. Schedule of cash flows in nominal dollars:

(1)

Year

(2)

After-Tax

Incremental

Cash Flow in

Real Dollars

(not including

depreciation shield)

(3)

Price

Index

(4)

After-Tax

Incremental

Cash Flow in

Nominal Dollars

(not including

depreciation shield)**

(5)

MACRS

Depreciation

(6)

Cash Flow:

Tax Savings

(depreciation .40)

(7)

Total

After-Tax

Cash Flow in

Nominal

Dollars

[Col. (4) +

Col.(6)]

20×0

$(188,000

)*

1.0000

$(188,000

)

—

—

$(188,000)

20×1

42,000

†

(1.20)1

=

1.2000

50,400

$200,000 20.00% = $40,000

$16,000

66,400

20×2

42,000

(1.20)2

=

1.4400

60,480

200,000 32.00% = 64,000

25,600

86,080

20×3

42,000

(1.20)3

=

1.7280

72,576

15,360

87,936

20×4

42,000

=

2.0736

87,091

200,000 11.52% = 23,040

96,307

20×5

42,000

(1.20)5

=

2.4883

20×6

42,000

(1.20)6

=

2.9860

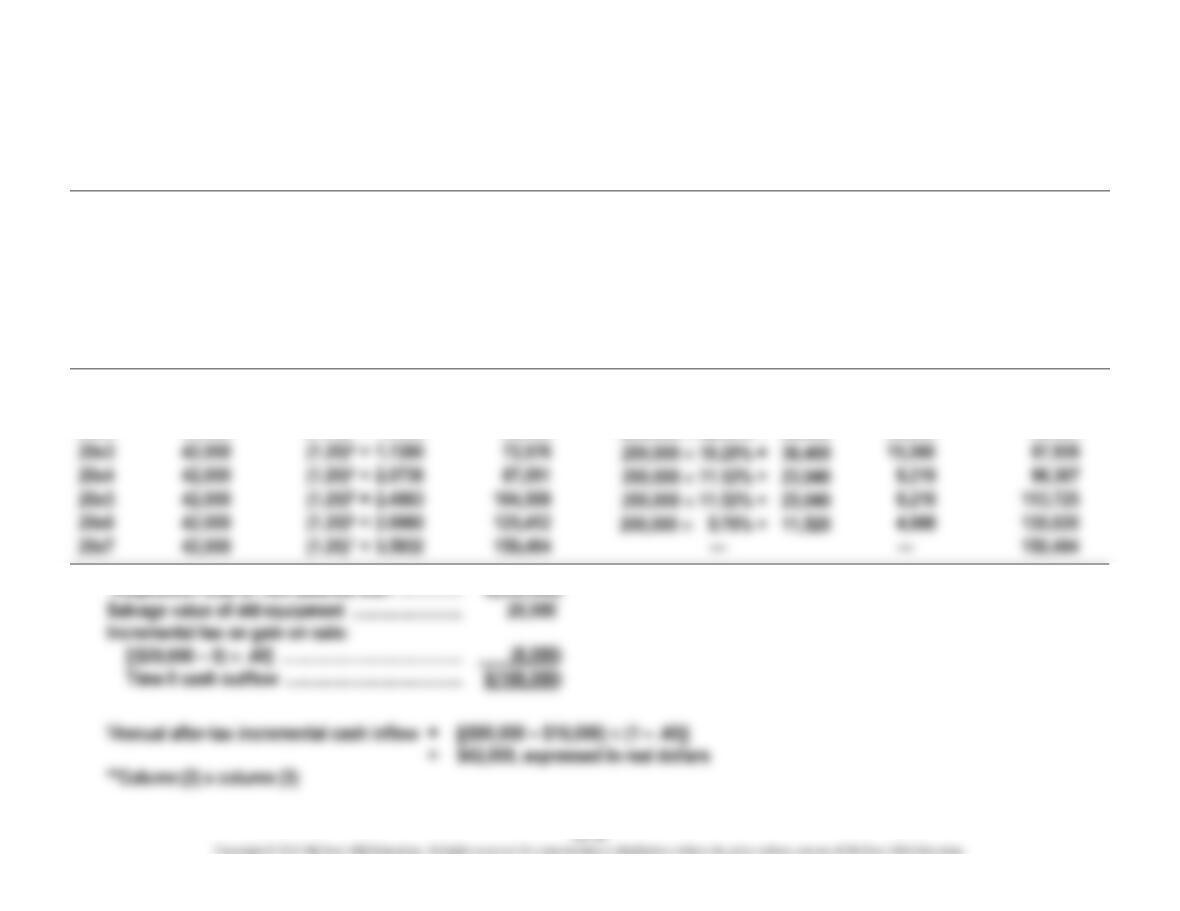

*Acquisition cost of new satellite dish ………………..

)

Salvage value of old equipment …………………………

20,000

Incremental tax on gain on sale:

)

Chapter 16 – Capital Expenditure Decisions

2.

Nominal interest rate:

Real interest rate ………………………………………………………………………………….

.10

Inflation rate ………………………………………………………………………………………..

.20

Nominal interest rate ……………………………………………………………………………

.32

3. Net present value analysis:

Year

After-Tax

Cash Flow in

Nominal Dollars

Discount

Factor*

Present

Value

20×0

$(188,000)

1.000

$(188,000)

20×1

.758

20×2

.574

20×3

.435

20×4

.329

20×5

.250

20×6

.189

20×7

.143

PROBLEM 16-56 (50 MINUTES)

PROBLEM 16-56 (CONTINUED)

(1)

Year

(2)

After-Tax

Incremental

Cash Flow in

Real Dollars

(not including

depreciation shield)

(3)

MACRS

Depreciation

(4)

Cash Flow:

Tax Savings

[Depreciation .40]

(5)

Price

Index

(6)

Depreciation

Tax Shield in

Real Dollars

[Col. (4) ÷ Col. (5)]

(7)

Total

After-Tax

Cash Flow in

Real

Dollars

[Col. (2) + Col.(6)]

20×0

$(188,000

)*

—

—

1.0000

—

$(188,000)

20×1

42,000

†

$200,000 20.00% = $40,000

$16,000

(1.20)1

=

1.2000

$13,333

55,333

20×3

42,000

(1.20)3

=

1.7280

50,889

46,444

20×5

42,000

(1.20)5

=

2.4883

45,704

20×6

42,000

(1.20)6

=

2.9860

43,543

*Acquisition cost of new satellite dish ………………..

$(200,000

)

Salvage value of old equipment …………………………

20,000

Incremental tax on gain on sale:

)

$(188,000

)

Chapter 16 – Capital Expenditure Decisions

PROBLEM 16-56 (CONTINUED)

3. Net present-value analysis:

Year

After-Tax

Cash Flow in

Real Dollars

Discount

Factor*

Present

Value

20×0

$(188,000)

1.000

$(188,000)

20×1

55,333

.909

50,298

20×2

.826

20×3

.751

20×4

.683

20×5

.621

20×6

.564

20×7

.513

Chapter 16 – Capital Expenditure Decisions

SOLUTIONS TO CASES

CASE 16-57 (60 MINUTES)

1. The two main alternatives for the Board of Education are as follows:

2. If the board decides to use minibuses, then there are two options for the full-size

buses:

3. Net-present-value analysis of options for full-size buses:

(a) Sell five full-size buses:

CASE 16-57 (CONTINUED)

4. Net present-value analysis of minibus purchase decision.

In the following incremental cost analysis, parentheses denote cash flows favoring

the full-size bus alternative.

Incremental annual cost of compensation for bus

drivers if minibuses are used

CASE 16-57 (CONTINUED)

5. Internal rate of return on the minibuses:

(a) First, calculate the annual cost savings if the minibuses are used.

Remember that the full-size buses will be kept in reserve.

Annual savings on bus charter fees ($30,000 – $5,000) …………………………..

$25,000

Annual incremental cost of compensation for bus

(54,000

)

Total annual cost savings if minibuses are used …………………………..

$61,000

(b) Second, calculate the initial cost if the minibuses are purchased:

Cost of redesigning bus routes, retraining drivers, etc. …………………………..

)

)

Initial cost ……………………………………………………………………………………

)

Annual incremental maintenance and operating costs

(c) Third, find the internal rate of return:

Annuity discount factor associated

with the internal rate of return

=

savings cost annual

cost initial

6. The cost of purchasing a full-size bus ($90,000) is irrelevant, because the board is

7. Peter Reynolds, the vice president for sales at the automobile dealership, is acting

improperly. First, he should not try to pressure his friend into recommending that the

CASE 16-57 (CONTINUED)

Chapter 16 – Capital Expenditure Decisions

CASE 16-58 (60 MINUTES)

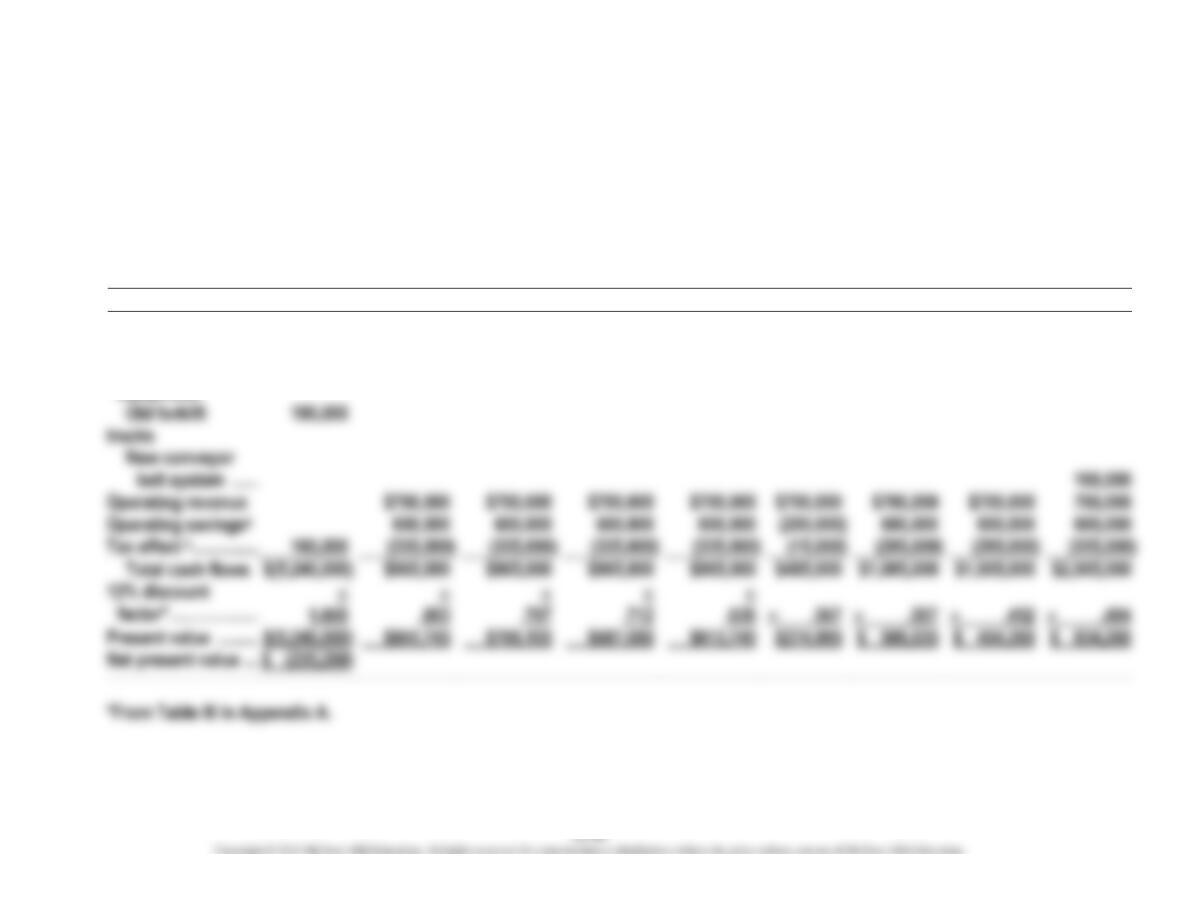

1. The net present value of the proposed investment is $(235,280), calculated as follows:

INSTANT DINNERS, INC.

NET-PRESENT-VALUE ANALYSIS

Time 0

Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Year 7

Year 8

New equipment …………………………..

$(4,500,000

)

Working capital …………………………..

(1,000,000

)

$1,000,000

Disposition of

equipment:

Operating revenue

$700,000

$700,000

Operating savingsa

)

Tax effect b…………………………..

)

)

)

)

(15,000

)

)

)

)

$(5,240,000

)

$1,005,000

$1,005,000

$2,065,000

Present value …………………………..

$(5,240,000

)

Net present value …………………………..

)

Chapter 16 – Capital Expenditure Decisions

CASE 16-58 (CONTINUED)

a

Operating savings for Years 1, 2, 3, 4, 6, 7, 8:

Manufacturing cost reduction ………………………………………………………….

$ 500,000

Maintenance cost reduction …………………………………………………………….

300,000

Less: Increased operating costs ……………………………………………………..

)

$ 600,000

Year 5:

Same as above ……………………………………………………………………………….

$ 600,000

Less: Equipment repairs …………………………………………………………………

)

)

b

Tax effects:

At time 0; disposal of forklifts:

Book value ……………………………………………………………………………………..

$ 500,000

Less: Salvage value …………………………………………………………………………

(100,000

)

Tax loss …………………………………………………………………………………………

$ 400,000

$ 160,000

Years 1 through 4:

Revenue ………………………………………………………………………………………….

$ 700,000

Operating-cost savings ……………………………………………………………………

600,000

Loss of depreciation on forklifts ……………………………………………………..

100,000

*

Depreciation on new equipment ………………………………………………………

Increase in taxable income ………………………………………………………………

)

CASE 16-58 (CONTINUED)

Year 5:

Revenue ………………………………………………………………………………………….

$ 700,000

Operating-costs* ……………………………………………………………………………..

(200,000

)

Loss of depreciation on forklifts ……………………………………………………..

100,000

Depreciation on new equipment ………………………………………………………

)

Increase in taxable income ………………………………………………………………

)

Years 6 and 7:

Revenue ………………………………………………………………………………………….

$ 700,000

Operating-cost savings ……………………………………………………………………

600,000

Depreciation on new equipment ………………………………………………………

)

Increase in taxable income ………………………………………………………………

$ 737,500

)

Year 8:

Revenue ………………………………………………………………………………………….

$ 700,000

Operating-cost savings ……………………………………………………………………

600,000

Depreciation on new equipment ………………………………………………………

(562,500

)

Salvage value of new equipment ……………………………………………………..

Increase in taxable income ………………………………………………………………

$ 837,500

)

2. Referring to the specific ethical standards of competence, confidentiality, integrity,

and credibility, Leland Forrest should evaluate Bill Rolland’s directives as follows:

Competence. Forrest has a responsibility to present complete and clear reports

Chapter 16 – Capital Expenditure Decisions

CASE 16-58 (CONTINUED)

Integrity. Rolland is engaging in activities that could prejudice him from carrying

out his duties ethically. In evaluating Rolland’s directive as it affects Forrest, Forrest

3. Leland Forrest should take the following steps to resolve this situation:

• Forrest should first investigate to see if Instant Dinners, Inc. (IDI) has an

established policy for resolution of ethical conflicts and follow those procedures.

• If this policy does not resolve the ethical conflict, the next step is for Forrest to

discuss the situation with his supervisor, Rolland, and see if he can obtain

Chapter 16 – Capital Expenditure Decisions

FOCUS ON ETHICS (See page 710 in the text.)

2. Marie Fenwar should approve Research Proposal I. It has a higher NPV than

Research Proposal II. Moreover, the NPV of Proposal I is positive, while the NPV of

Proposal II is negative.

Time 0

Year 1

Year 2

Year 3

Year 4

Year 5

Research Proposal I:

Equipment

acquisition ……………………….

$(40,000

)

Contract fee ……………………….

$100,000

$100,000

$100,000

$100,000

$100,000

Operating costs ………………….

(150,000

)

(120,000

)

(75,000

)

(40,000

)

(40,000

)

Total cash flow ……………………

$ (40,000

)

$ (50,000

)

$ (20,000

)

Present value …………………………

$ (40,000

)

$ (46,300

)

$ (17,140

)

Research Proposal II:

Equipment

acquisition ……………………….

$(70,000

)

Contract fee ……………………….

$100,000

$100,000

$100,000

$100,000

$100,000

Operating costs ………………….

(75,000

)

(75,000

)

(95,000

)

(95,000

)

(95,000

)

Total cash flow ……………………

$ (70,000

)

Present value …………………………

$ (70,000

)

3. Marie Fenwar acted unethically in approving Research Proposal II. Proposal I has a

positive NPV, and it is higher than the NPV for Proposal II, which is negative. Fenwar