Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

Prob. 19–3B (FIN MAN); Prob. 4–3B (MAN)

*$150 unit selling price – $110 unit variable cost

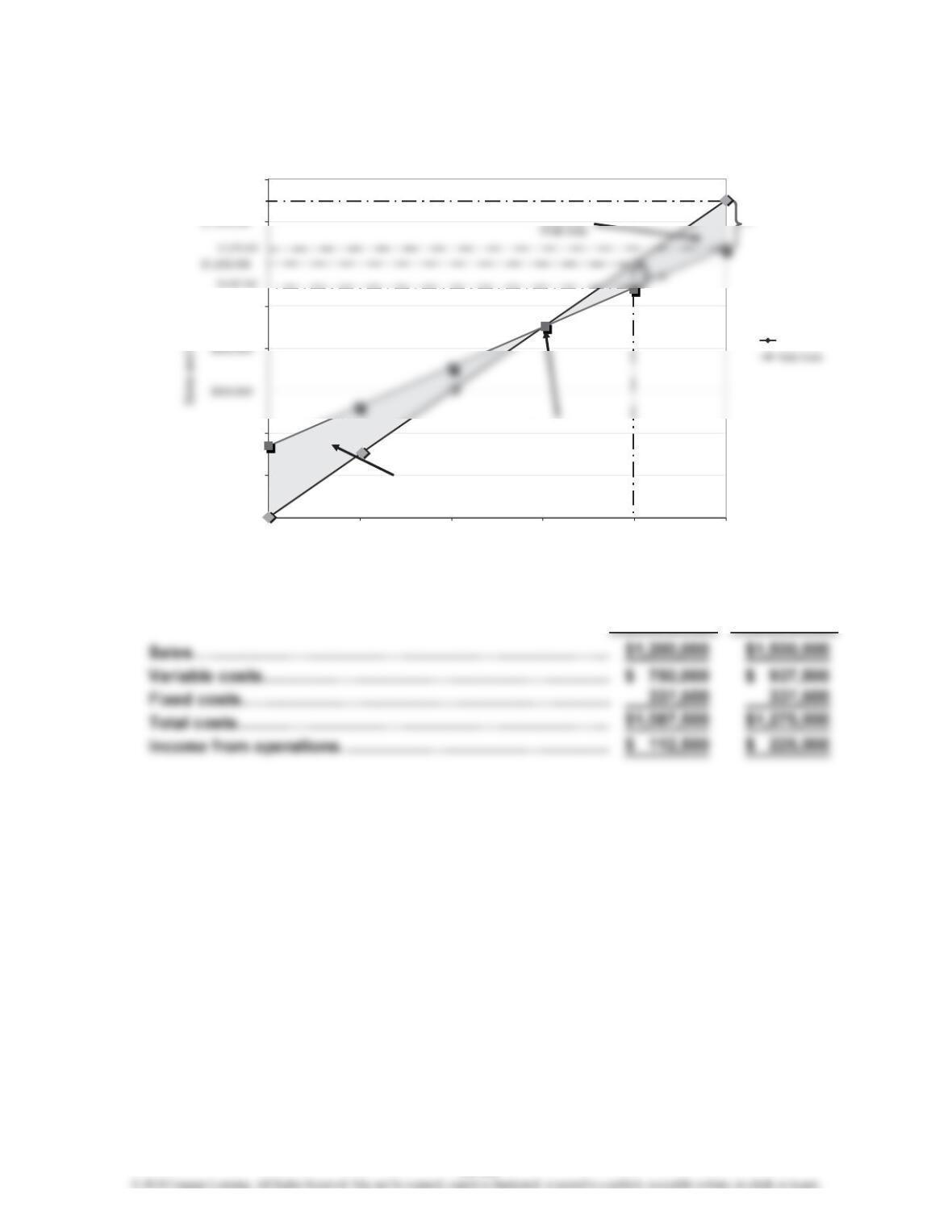

3.

4. Sales (32,000 × $150)…………………………

…

$4,800,000

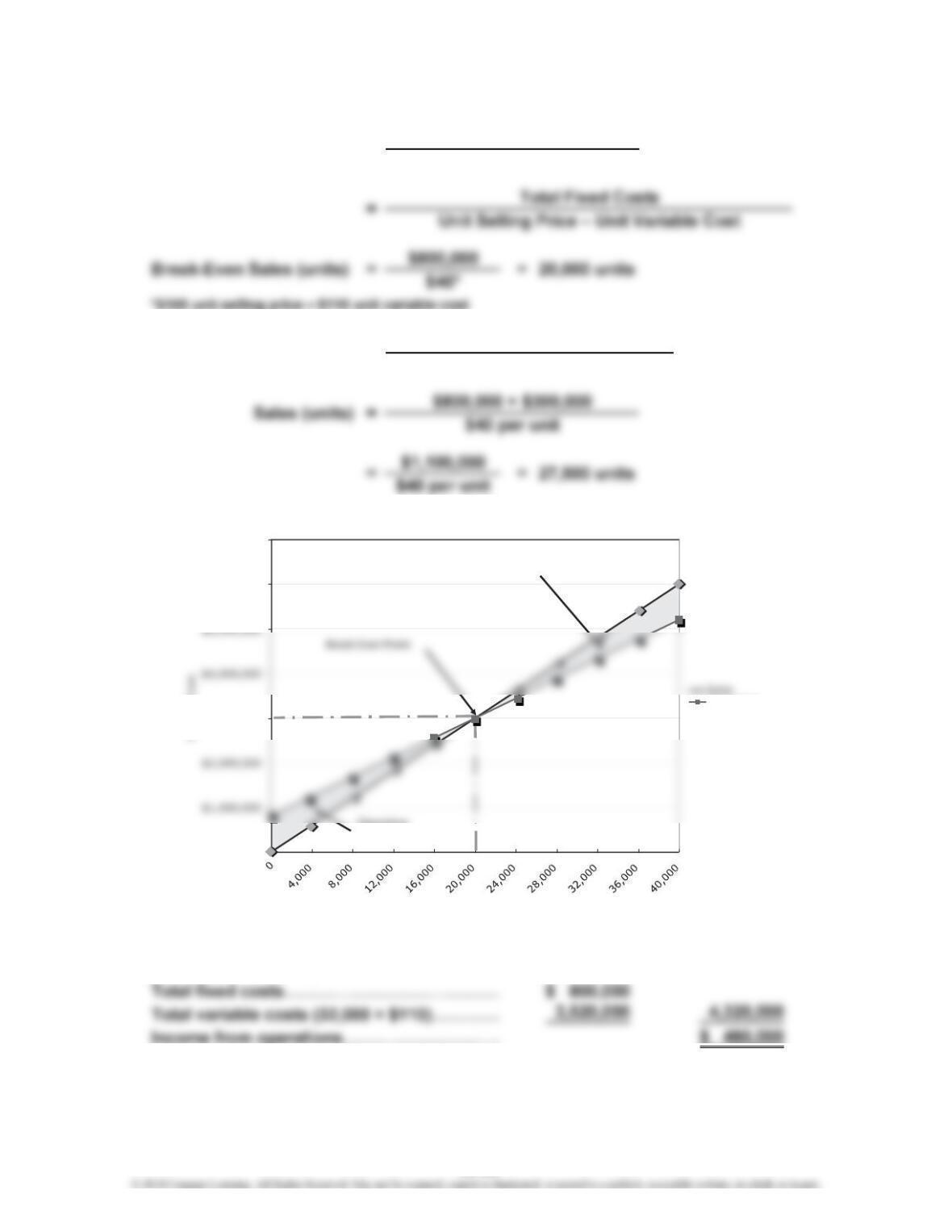

1. Break-Even Sales (units) = Total Fixed Costs

Unit Contribution Margin

2. Sales (units) = Total Fixed Costs + Target Profit

Unit Contribution Margin

$0

$3,000,000

$6,000,000

$7,000,000

Sales and Costs

Units of Sales

Total C ost s

Operating

Loss Area

Operating Profit Area

19-35

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

Prob. 19–4B (FIN MAN); Prob. 4–4B (MAN)

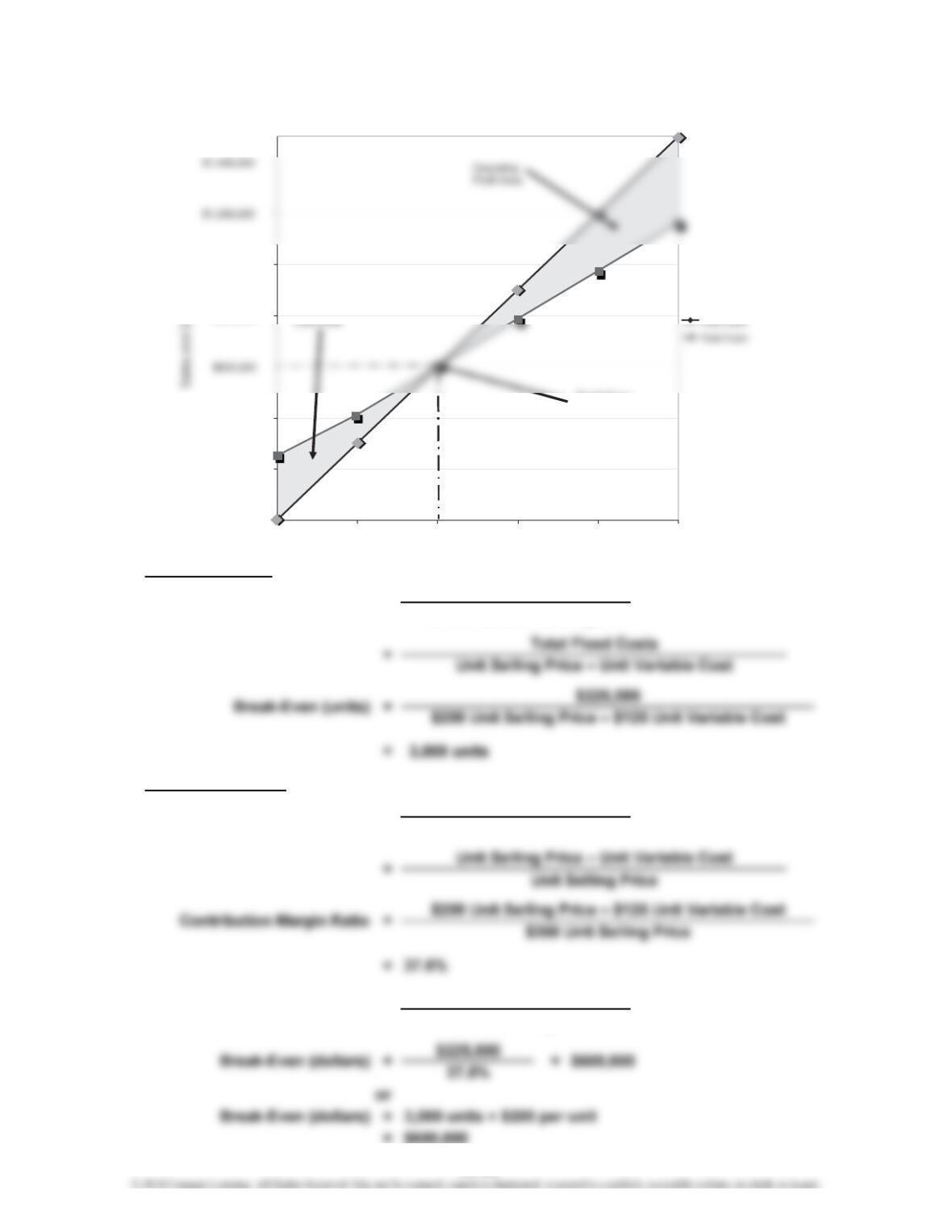

Break-Even Units:

Break-Even Dollars:

Unit Selling Price

Contribution Margin Ratio = Unit Contribution Margin

Break-Even (dollars) = Total Fixed Costs

Contribution Margin Ratio

1.

Unit Contribution Margin

Break-Even Sales (units) = Total Fixed Costs

$0

$200,000

$400,000

$800,000

$1,000,000

0 1,500 3,000 4,500 6,000 7,500

Units of Sales

Break-Even

Point

Operating

$225,000

19-36

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

Prob. 19–4B (FIN MAN); Prob. 4–4B (MAN) (Continued)

2.

a. b.

4,500 units 7,500 units

$0

$600,000

$1,400,000

$1,600,000

0 1,500 3,000 4,500 6,000 7,500

Sales and Costs

Units of Sales

Break-Even

Point

$1,500,000

19-37

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

Prob. 19–4B (FIN MAN); Prob. 4–4B (MAN) (Continued)

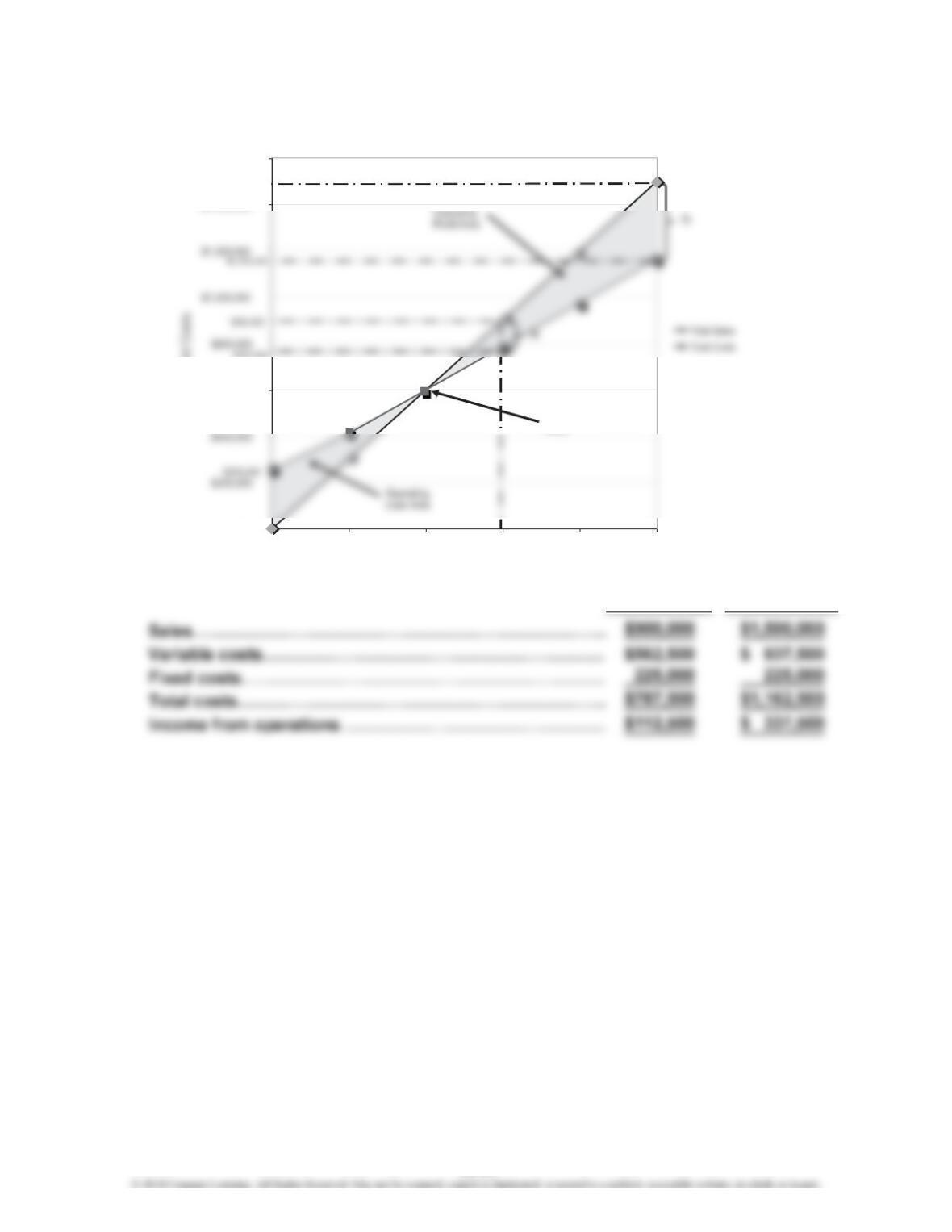

3.

Unit Contribution Margin

Unit Contribution Margin

Unit Selling Price

=Total Fixed Costs

=

Break-Even (dollars)

=

Total Fixed Costs

Contribution Margin Ratio

Contribution Margin Ratio

Break-Even Dollars:

Break-Even Units:

Break-Even Sales (units)

$0

$200,000

$1,400,000

$1,600,000

0 1,500 3,000 4,500 6,000 7,500

Units of Sales

Operating

Operating

Loss Area

$337,500

19-38

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

Prob. 19–4B (FIN MAN); Prob. 4–4B (MAN) (Concluded)

4.

a. b.

6,000 units 7,500 units

$0

$200,000

$400,000

$1,000,000

$1,400,000

$1,600,000

0 1,500 3,000 4,500 6,000 7,500

Units of Sales

Total Sales

b.

Operating

Break-Even

Point

Operating

Loss Area

$1,500,000

$337,500

19-39

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

Prob. 19–5B (FIN MAN); Prob. 4–5B (MAN)

(Overall product is labeled E.)

1. Unit Selling Price of E [($12 × 30%) + ($15 × 70%)]…………………………………

…

$14.10

3. Unit selling price of E [($12 × 50%) + ($15 × 50%)]…………………………………

…

$13.50

Break-Even Sales (units)

=Fixed Costs

Unit Contribution Margin

19-40

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

Prob. 19–6B (FIN MAN); Prob. 4–6B (MAN)

1.

Sales (12,000 × $240) $2,880,000

Cost of goods sold:

Expenses:

Selling expenses:

Sales salaries and commissions

[$340,000 + (12,000 × $4)] $388,000

Advertising 116,000

BELMAIN CO.

Estimated Income Statement

For the Year Ended December 31, 2014

19-41

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

Prob. 19–6B (FIN MAN); Prob. 4–6B (MAN) (Continued)

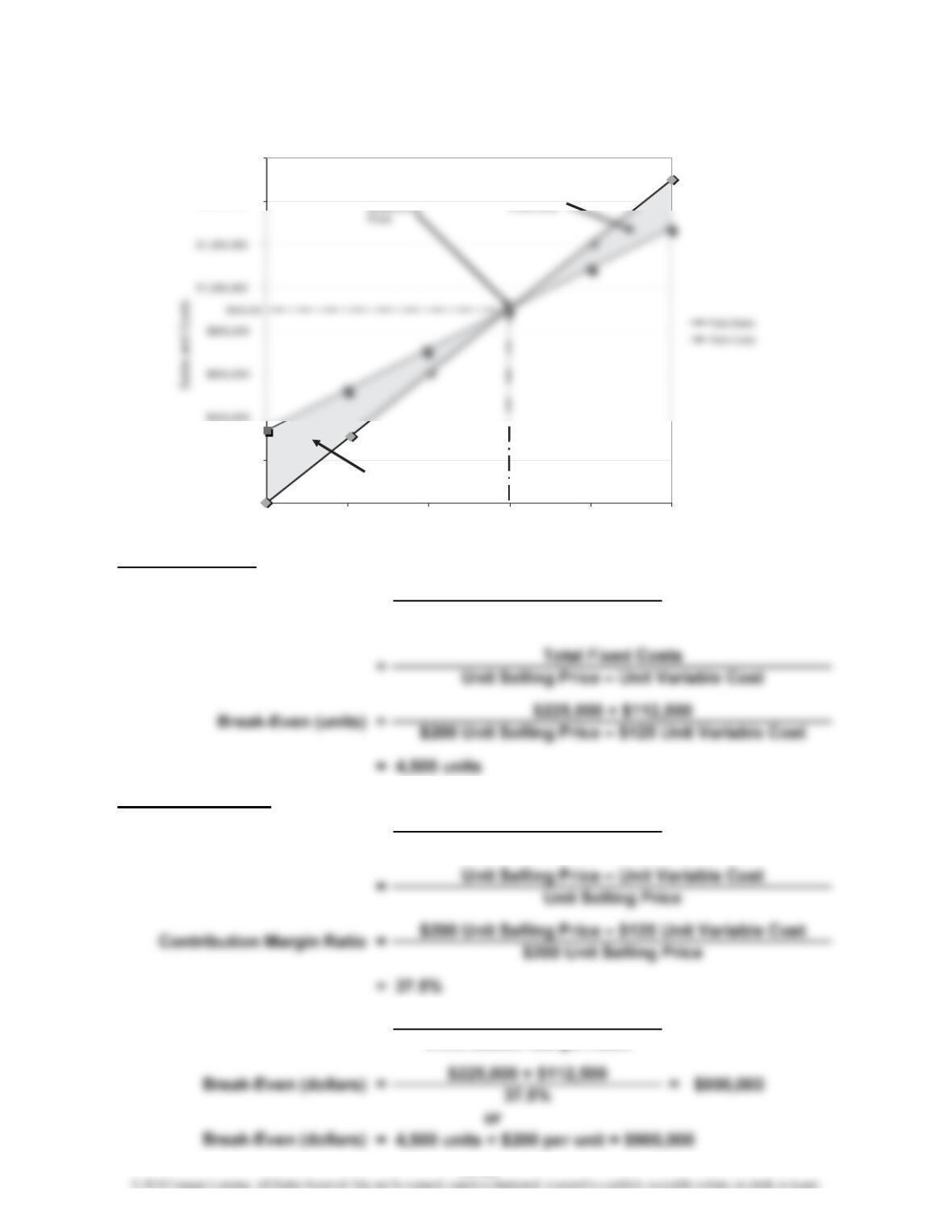

3. Break-Even Sales (units) = Fixed Costs

Unit Contribution Margin

2. Contribution Margin Ratio = Sales – Variable Costs

Sales

19-42

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

Prob. 19–6B (FIN MAN); Prob. 4–6B (MAN) (Concluded)

4.

5. Margin of safety:

In dollars:

Expected sales (12,000 units × $240)………………………

…

$2,880,000

As a percentage of sales:

=Margin of Safety Sales – Sales at Break-Even Point

Sales

$0

$500,000

$2,000,000

$2,500,000

$4,000,000

$4,500,000

0 2,000 4,000 6,000 8,000 10,000 12,000 14,000 16,000 18,000

Sales and Costs

Units

Sales

Total Co sts

Operating

Profit Area

Area

$1,920,000

19-43

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

CP 19–1 (FIN MAN); CP 4–1 (MAN)

In an absolute sense, Edward’s actions are devious. He is clearly attempting

to use the first four-year scenario, which is favorable, as a way to market the

partnerships. They are really longer-term investments. After the first four

CASES & PROJECTS

19-44

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

CP 19–2 (FIN MAN); CP 4–2 (MAN)

The airline industry has a high operating leverage. This means that fixed costs

are a large part of the cost structure. The break-even volume is apparently around

65% of capacity. When the volume falls below 65%, the industry loses money. As

the percentage increases above 65%, the industry becomes very profitable. There

change in passenger volume. However, this is unlikely. The revenue from price

increases would need to increase faster than the lost revenue from lower traffic

volume for a price increase to lower break-even. To raise ticket prices, the airline

would have to minimize the impact on lost volume. This might be possible for fare

increases targeted to business travelers that need to fly, regardless of ticket price.

scale. For example, an airline could consolidate three flights departing in the

morning from Tulsa to Dallas into just two flights departing in the morning. This

would reduce the airline’s costs but would increase the airline passengers’

inconvenience. This strategy works only if there is little loss in revenue by going

to two flights, meaning that the people bumped from the third flight go to the other

19-45

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

CP 19–3 (FIN MAN); CP 4–3 (MAN)

Do-Nothing Strategy:

Revenue – Variable Costs – Fixed Costs = Profit

Thomas’s Strategy:

Revenue – Variable Costs – Fixed Costs = Profit

CP 19–4 (FIN MAN); CP 4–4 (MAN)

The direct labor costs are not variable to the increase in unit volume. The unit

volume is the wrong activity base for direct labor costs. The “number of

impressions” is a more accurate reflection of the direct labor cost. An impression

is a separate printing color application on the banners. Thus, the analysis should

be done as follows:

One Three

Color Color Total

Number of banners 212 616 1,800

Two

Color

274

Color

Four

698

19-46

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

CP 19–5 (FIN MAN); CP 4–5 (MAN)

The Shipping Department manager should respond by pointing out that the

activities performed by his department are not related to sales volume but to

CP 19–6 (FIN MAN); CP 4–6 (MAN)

There are many possible applications of break-even analysis in a school

environment. Below are just a few possible ideas.

Revenue Fixed Costs Variable Costs

1 Break-even number Student tuition Faculty salary, space Supplies, copying

of students in a class for a class costs

2 Break-even sales Book sales Manager’s salary, Cashier salaries,

in the bookstore space costs cost of books

Break-Even Analysis

19-47