16–1

Chapter 16

Fundamentals of Variance Analysis

Learning Objectives

1. Use budgets for performance evaluation.

2. Develop and use flexible budgets.

3. Compute and interpret the sales activity variance.

4. Prepare and use a profit variance analysis.

5. Compute and use variable cost variances.

6. Compute and use fixed cost variances.

7. (Appendix) Understand how to record costs in a standard costing system.

16–2

Chapter Overview

I. USING BUDGETS FOR PERFORMANCE EVALUATION

II. PROFIT VARIANCE

• Why are Actual and Budgeted Results Different?

III. FLEXIBLE BUDGETING

IV. COMPARING BUDGETS AND RESULTS

• Sales Activity Variance

o Interpreting Variances

V. PROFIT VARIANCE ANALYSIS AS A KEY TOOL FOR MANAGERS

• Sales Price Variance

VI. PERFORMANCE MEASUREMENT AND CONTROL IN A COST CENTER

• Variable Production Costs

o Direct Materials

o Direct Labor

o Variable Production Overhead

VII. VARIABLE COST VARIANCE ANALYSIS

• General Model

• Direct Materials

o Responsibility for Direct Materials Variances

• Direct Labor

o Direct Labor Price Variance

o Labor Efficiency Variance

• Variable Production Overhead

o Variable Production Overhead Price Variance

o Variable Overhead Efficiency Variance

• Variable Cost Variances Summarized in Graphic Form

VIII. FIXED COST VARIANCES

• Fixed Cost Variances with Variable Costing

IX. SUMMARY OF OVERHEAD VARIANCES

• Key Points

16–3

Chapter Overview, continued

X. APPENDIX: RECORDING COSTS IN A STANDARD COST SYSTEM

• Direct Materials

• Direct Labor

• Variable Manufacturing Overhead

• Fixed Manufacturing Overhead

• Transfer To Finished Goods Inventory and to Cost of Goods Sold

• Close Out Variance Accounts to Cost of Goods Sold

16–4

Chapter Outline

LO 16-1 Use budgets for performance evaluation.

USING BUDGETS FOR PERFORMANCE EVALUATION

• The development of the master budget is the first step in the budgetary planning and control

cycle.

o The budgeting process provides a means to coordinate activities among units of the

organization, to communicate the organization’s goals to individual units, and to ensure

o The budget is management’s plan for financial performance.

• The master budget includes:

o Operating budgets (such as the budgeted income statement, production budget,

budgeted cost of goods sold, and supporting budgets)

• Variance is the difference between planned result and actual outcome. That is:

Variance = Actual result – Budgeted performance.

o Variance analysis is used to:

16–5

PROFIT VARIANCE

• The simplest measure of performance is the variance between actual income and budgeted

income.

o A favorable variance is the variance that, taken alone, results in an addition to operating

profit.

o An unfavorable variance is the variance that, taken alone, reduces operating profit.

o The labels “favorable” and “unfavorable” should not be considered as evaluations of

performance without additional investigation. (See Business Application box “When a

Favorable Variance Might Not Mean “Good” News.”)

▪ Although a simple comparison of planned and actual profit suggests that performance

was better (or worse) than planned, the additional data (such as those in Exhibit 16.2)

provide information on the impact on profit performance from each of the revenue

and cost line items.

▪ The additional information is useful for two reasons:

• Why are Actual and Budgeted Results Different?

o An important part of variance analysis is to understand:

▪ What might cause a difference between actual and budgeted results.

16–6

o The following table summarizes the variance analysis between actual results and the

master budget for line items comprising the operating profit:

(1)

Actual

(3) = (1) – (2)

Variancea

(2)

Master Budget

Units

xxx

xxx F or U

xxx

Sales revenue

$ xxx

$xxx F or U

$ xxx

=

+

Unit Variable

×

See Demonstration Problem 1

LO 16-2 Develop and use flexible budgets.

FLEXIBLE BUDGETING

• One obvious reason that actual results might differ from budgeted results is that the actual

activity itself differed from the budgeted or expected activity.

o A static budget is developed in detail for one level of anticipated activity, such as a

master budget.

o A flexible budget indicates budgeted revenues, costs, and profits for virtually all feasible

levels of activities.

▪ Because variable costs and revenues change with changes in activity levels, these

amounts are budgeted to be different at each activity level in the flexible budget.

▪ Flexible budget line is the expected costs at different output levels and can be

represented by the following formula:

Contribution margin

$xxx

$xxx F or U

Operating profit

$ xxx

$xxx F or U

$ xxx

16–7

LO 16-3 Compute and interpret the sales activity variance.

COMPARING BUDGETS AND RESULTS

• A comparison of the master budget with the flexible budget and with actual results is the

basis for analyzing differences between plans and actual performance.

• Sales Activity Variance

o Sales activity variance (also known as sales volume variance) is the difference between

operating profit in the master budget and operating profit in flexible budget that arises

because the actual number of units sold is different from the budgeted number.

▪ That is:

o The sales activity variance, as shown in Exhibit 16.4, is useful for management because:

16–8

o Interpreting Variances

▪ Holding everything else constant, a decrease in sales creates an unfavorable sales

activity variance as shown in Exhibit 16.4. Does this indicate poor performance?

LO 16-4 Prepare and use a profit variance analysis.

PROFIT VARIANCE ANALYSIS AS A KEY TOOL FOR MANAGERS

• Profit variance analysis shows the causes of differences between budgeted profits and the

actual profits earned.

o The actual results can be compared with both the flexible budget and the master budget in

a profit variance analysis, as shown in Exhibit 16.5.

(1)

(2)

(3)

(4)

(5)

(6)

(7)

Actual

(Based on

Actual

Activity)

Manufacturing

Variances

Marketing And

Administrative

Variance

Sales Price

Variance

Flexible

Budget

(Based on

Actual

Activity)

Sales

Activity

Variance

Master

Budget

(Based on

Planned

Activity)

Sales revenue

$xxx

$xx U or F

$xxx

$xxx U or F

$xxx

Less:

Variable costs

Variable manufacturing cost

administrative cost

Contribution margin

$xxx

$xxx U or F

Less:

Fixed costs

Fixed manufacturing cost

administrative cost

16–9

o Cost variances result from deviations in costs and efficiencies in operating the company.

They are important for measuring productivity and for helping to control costs.

• Sales Price Variance

o Column (4) shows the sales price variance as derived from the difference between the

actual revenue and budgeted selling price multiplied by the actual number of units sold.

▪ That is:

Sales Price

Variance

=

Actual

Revenue

–

Budgeted

Selling Price

×

Actual

Units Sold

=

Selling Price

–

Budgeted

×

Actual

Units Sold

• Variable Production Cost Variances

o Variable costs in Column (5) represent what should have been spent given the actual

sales volume.

• Fixed Production Cost Variance

See Demonstration Problem 2

PERFORMANCE MEASUREMENT AND CONTROL IN A COST CENTER

• For cost centers whose production managers typically do not control what they are asked to

produce, the actual unit production (not sales) should be used as a baseline.

• Variable Production Costs

o For any unit variable cost (such as direct materials), the variable cost in the budget is

determined by multiplying the budgeted amount of the direct material in each unit of

output by the expected price of each unit of direct material.

o Direct Materials

o Direct Labor

o Variable Production Overhead

▪ The overhead “quantity” is expressed in terms of the units of the cost driver chosen

(such as direct labor hours) because that is what is being used to apply the overhead.

16–11

LO 16-5 Compute and use variable cost variances.

VARIABLE COST VARIANCE ANALYSIS

• General Model

o Comparing the budget (based on standard costing) to actual results identifies production

cost variances.

o Both the actual and standard input quantities are for the actual output attained.

▪ A price variance is the difference between actual costs and budgeted costs arising

from changes in the cost of inputs to a production process or other activity.

o Managers who are responsible for price variances would not be held responsible for

efficiency variances and vice versa.

16–12

▪ That is,

Actual Costs =

Actual Input Quantity

at Actual Input Price

(AP X AQ)

Actual Input

Quantity at Standard

Input Price

(SP X AQ)

Flexible Production Budget =

Standard Input Quantity Allowed

For Actual Output at Standard

Input Price

(SP X SQ)

Price (Rate, or Spending) Quantity (Usage, or Efficiency)

Variance Variance

• Direct Materials

o A flexible production budget is calculated as standard input price times standard

quantity of input allowed for actual good output. It is based on actual production volume.

▪ An alternative way to view these variances graphically is shown below. Quantities are

16–13

▪ Exhibit 16.8 applies the general model to direct materials variances.

o Responsibility for Direct Materials Variances

▪ Responsibility for the direct materials price variance is usually assigned to the

purchasing department.

See Demonstration Problem 3

• Direct Labor

o Exhibit 16.9 applies the general model to direct labor variances.

o Direct Labor Price Variance

o Labor Efficiency Variance

▪ The labor efficiency variance is a measure of labor productivity and is usually

controlled by production managers.

See Demonstration Problem 4

• Variable Production Overhead

o Exhibit 16.10 applies the general model to variable overhead variances. The variable

overhead standard rate is derived from a two-stage estimation of:

o Variable Production Overhead Price Variance

▪ The variable overhead price variance could have occurred because

o Variable Overhead Efficiency Variance

▪ The variable overhead price variance actually contains some efficiency items as well

as price items. Some companies separate those components.

See Demonstration Problem 5

• Variable Cost Variances Summarized in Graphic Form

o Exhibit 16.11 summarizes the variable production cost variances.

▪ A summary of this nature is useful for reporting variances to high-level managers. It

provides both an overview of variances and their sources.

16–15

LO 16-6 Compute and use fixed cost variances.

FIXED COST VARIANCES

• It is usually assumed that fixed costs are unchanged when volume changes within the

relevant range, so the amount budgeted for fixed overhead is the same in both the master and

flexible budgets.

• Fixed Cost Variances with Variable Costing

o When the income statement is prepared using variable costing, there is no absorption of

the fixed costs by units of production. All the fixed manufacturing overhead is charged to

income in the period incurred.

o Exhibit 16.12 shows a variance analysis for fixed overhead.

▪ That is:

Actual

Flexible Production

Budget

Price (Spending) Variance

(Efficiency Variance is not Applicable)

16–16

o Developing the Standard Unit Cost for Fixed Production Costs

▪ The fixed manufacturing standard cost is determined before the start of the production

period using the following formula from Chapter 7:

Standard (or Predetermined)

Fixed Production Overhead Cost

=

Budgeted Fixed Manufacturing Overhead

Budgeted Activity Level

o Compare with the Fixed Production Cost Price Variance

▪ Exhibit 16.13 demonstrates the variance analysis for fixed overhead under absorption

costing.

• That is:

▪ An alternative way to present fixed overhead variances graphically is shown below

16–17

• Since fixed overhead is unitized through the calculation of predetermined fixed

overhead rate, fixed overhead is applied as if it were variable cost, as seen in the

application line.

▪ The production volume variance applies only to fixed costs as a result of allocating a

fixed period cost to units on a predetermined basis. It does not represent resources

spent or saved, and is unique to full-absorption costing.

See Demonstration Problem 6

SUMMARY OF OVERHEAD VARIANCES

• The method of computing overhead variances described is known as the four-way analysis of

overhead variances because it computes the following four variances:

• Key Points

o Exhibit 16.15 summarizes the four-way analysis of variable and fixed overhead variances.

16–18

LO 16-7 (Appendix) Understand how to record costs in a standard costing

system.

APPENDIX: RECORDING COSTS IN A STANDARD COST SYSTEM

• When using standard costing, costs are transferred through the production process at their

standard costs.

o Standard costing is an accounting method that assigns costs to cost objects at

predetermined amounts.

• Direct Materials

Work-in-Process Inventory

xxx

Materials Price Variancea

xxx

Materials Efficiency Variancea

xxx

xxx

16–19

• Direct Labor

Work-in-Process Inventory

xxx

Direct Labor Price Variancea

xxx

• Variable Manufacturing Overhead

Work-in-Process Inventory

xxx

Variable Overhead (Applied)

xxx

(To record the application of Variable overhead to Work-in–Process on

the basis of standard input allowed)

Variable Overhead (Actual)

xxx

Miscellaneous Payables and Inventory Accounts

xxx

(To record actual variable overhead costs)

Variable Overhead (Applied)

xxx

Variable Overhead Efficiency Variancea

xxx

Variable Overhead (Actual)

xxx

(To record variable overhead variances and close the applied and

actual accounts)

Work-in-Process Inventory

xxx

Fixed Overhead (Applied)

xxx

(To record the application of fixed overhead to Work-in-Process on the

basis of standard input allowed)

Fixed Overhead (Actual)

xxx

Miscellaneous Payables and Inventory Accounts

xxx

(To record actual fixed overhead costs)

a Favorable variances should be credited; unfavorable variances should be debited. The

variances are debited here for illustration only.

• Fixed Manufacturing Overhead

Direct Labor Efficiency Variancea

xxx

Wages Payable

xxx

(To record the purchase and use of direct labor at actual cost and the

transfer to Work-in-Process at standard cost)

16–20

• Transfer to Finished Goods Inventory and to Cost of Goods Sold

Finished Goods Inventory

xxx

Work-in-Process Inventory

xxx

(To record the transfer to Finished Goods Inventory at standard cost)

Accounts Receivable

xxx

Sales Revenue

xxx

Cost of Goods Sold

xxx

Finished Goods Inventory

xxx

(To record the sale and the standard cost per unit sold)

• Close out variance accounts to Cost of Goods Sold

Cost of Goods Sold

xxx

Materials Price Variancea

xxx

Materials Efficiency Variancea

xxx

Direct Labor Price Variancea

xxx

Direct Labor Efficiency Variancea

xxx

Variable Overhead Price Variancea

xxx

Variable Overhead Efficiency Variancea

xxx

Fixed Overhead Price Variancea

xxx

Fixed Overhead Production Volume Variancea

xxx

(To close the variance accounts to Cost of Goods Sold)

Fixed Overhead (Applied)

xxx

Fixed Overhead Price Variancea

xxx

Fixed Overhead Production Volume Variancea

xxx

Fixed Overhead (Actual)

xxx

actual accounts)

16–21

Matching

A.

Cost variance analysis

K.

Profit variance analysis

B.

Efficiency variance

L.

Sales activity variance

C.

Favorable variance

M.

Sales price variance

D.

Financial budgets

N.

Spending (or budget) variance

E.

Flexible budget

O.

Standard cost sheet

F.

Flexible budget line

P.

Standard costing

G.

Flexible production budget

Q.

Static budget

H.

Operating budgets

R.

Total cost variance

I.

Price variance

S.

Unfavorable variance

J.

Production volume variance

T.

Variance

_____ 1. Budgeted income statement, production budget, budgeted cost of goods sold, and

supporting budgets.

_____ 2. Budgets of financial resources—for example, the cash budget and the budgeted

balance sheet.

_____ 3. Variance that, taken alone, results in an addition to operating profit.

_____ 4. Budget for a single activity level; usually the master budget.

_____ 5. Difference between operating profit in the master budget and operating profit in the

flexible budget that arises because the actual number of units sold is different from

the budgeted number.

_____ 6. Comparison of actual input amounts and prices with standard input amounts and

prices.

_____ 7. Difference between actual costs and budgeted costs arising from changes in the cost

of inputs to a production process or other activity.

_____ 8. Price variance for fixed overhead.

_____ 9. Difference between planned result and actual outcome.

_____ 10. Budget that indicates revenues, costs, and profits for different levels of activity.

_____ 11. Accounting method that assigns costs to cost objects at predetermined amounts.

_____ 12. Difference between budgeted and actual results arising from differences between the

inputs that were budgeted per unit of output and the inputs actually used.

_____ 13. Expected monthly costs at different output levels.

_____ 14. Analysis of the causes of differences between budgeted profits and the actual profits

earned

_____ 15. Standard input price times standard quantity of input allowed for actual good output.

_____ 16. Variance that, taken alone, reduces operating profit.

_____ 17. Variance that arises because the volume used to apply fixed overhead differs from the

estimated volume used to estimate fixed costs per unit.

_____ 18. Difference between budgeted and actual results (equal to the sum of the price and

efficiency variances).

_____ 19. Difference between actual revenue and actual units sold multiplied by budgeted

selling price.

_____ 20. Form providing standard quantities of inputs used to produce a unit of output and the

standard prices for the inputs.

Matching Answers

1. H

16–23

Multiple Choice

1. Which of the following statements is not correct?

a. Unfavorable variance occurs when actual costs are lower than budgeted costs.

b. The labels “favorable” and “unfavorable” should not be considered as evaluations of

performance without additional investigation.

c. An important part of variance analysis is to understand what might cause a difference

between actual and budgeted results.

d. Variance = Actual result – Budgeted performance.

2. With a planned volume of 15,000 units, the master budget includes variable costs of

$450,000 and fixed costs of $350,000. If the actual volume is 12,000 units, what is the

amount of the total costs in the flexible budget?

a. $490,000

b. $560,000

c. $650,000

d. $710,000

3. Which of the following is correct regarding sales activity variance?

a. Sales activity variance is driven by the volume difference between actual results and

flexible budget.

b. Variable costs are expected to decrease when volume is higher than planned.

c. Sales activity variance is the difference between operating profit in the master budget and

operating profit in flexible budget.

d. Sales activity variance can be seen on the master budget’s profit-volume line.

4. Which of the following statements is correct?

a. Marketing and administrative cost variances are treated differently from production cost

variances.

b. The fixed production cost variance is the difference between flexible budget and master

budget costs.

c. Variable cost variances are output variances.

d. Profit variance analysis shows the causes of differences between budgeted profits and the

actual profits earned.

16–24

Use the following information to answer questions 5 through 8:

Actual results

Budget data

20,000 units produced and sold

19,000 units planned

Direct materials: 62,300 units of

input purchased and used @

$29 per input unit

$1,806,700

Direct materials: 3 units of input

allowed per output unit @ $30

per input unit

$90

Direct labor: 51,500 hours used

per output unit @ $21.50 per

hour

1,107,250

Direct labor: 2.5 hours of input

allowed per output unit @ $20

per hour

50

5. What is the materials price variance?

a. $62,300 Unfavorable

b. $62,300 Favorable

c. $69,000 Favorable

d. $77,250 Favorable

6. What is the materials total cost variance?

a. $7,500 Unfavorable

b. $11,250 Unfavorable

c. $7,500 Favorable

d. $6,700 Unfavorable

7. What is the labor price variance?

a. $77,250 Unfavorable

b. $30,000 Unfavorable

c. $62,300 Favorable

d. $69,000 Unfavorable

8. What is the labor efficiency variance?

a. $77,250 Unfavorable

b. $30,000 Unfavorable

c. $62,300 Favorable

d. $69,000 Unfavorable

9. Which of the following statements regarding variable overhead variances is correct?

a. The variable overhead price variance could have occurred because actual costs are

different from those expected.

b. The relationship between variable production overhead costs and the basis chosen is

perfect.

c. The variable overhead price variance usually contains only the efficiency items.

d. The variable overhead efficiency variance is related to the use of variable costs.

16–25

10. Which of the following statements regarding fixed overhead is correct?

a. Production volume variance is the difference between the actual and applied fixed

overhead.

b. When the income statement is prepared using variable costing, there is no absorption of

the fixed costs by units of production.

c. Production volume variance applies only to fixed costs.

d. Both b and c are correct.

11. A company purchased and used 10,000 pounds of materials while incurring $2,000

unfavorable price variance. The standard cost for materials is $4.80 per pound. What was the

actual price of materials per pound?

a. $5.00.

b. $4.90.

c. $5.10.

d. $5.20.

12. Which of the following statements regarding standard costing system is incorrect?

a. The difference between actual costs assigned and the standard costs of the work done

determines the variance.

b. Favorable variances should be credited.

c. The use of standard costs contributes to management control.

d. Standard costing system complicates the costing of inventories.

16–26

Multiple Choice Answers

16–27

16–28

Demonstration Problem 1

The accountant at EZ Toys, Inc. is analyzing the production and cost data for its Trucks Division.

For October, the actual results and the master budget data are presented below.

Actual Results:

Budget Data:

10,000 Trucks Produced and Sold

12,000 Trucks Planned

Unit selling price

$15

Unit selling price

$14

Variable costs:

Unit variable cost:

Direct materials

$ 52,800

Direct materials

$ 5

Direct labor

51,000

Direct labor

4

Variable overhead

23,000

Variable overhead

2

Total variable costs

$126,800

Total unit variable costs

$11

Fixed overhead

$9,000

Fixed overhead

$9,600

Required:

Prepare a variance analysis to compare actual results and the master budget.

16–29

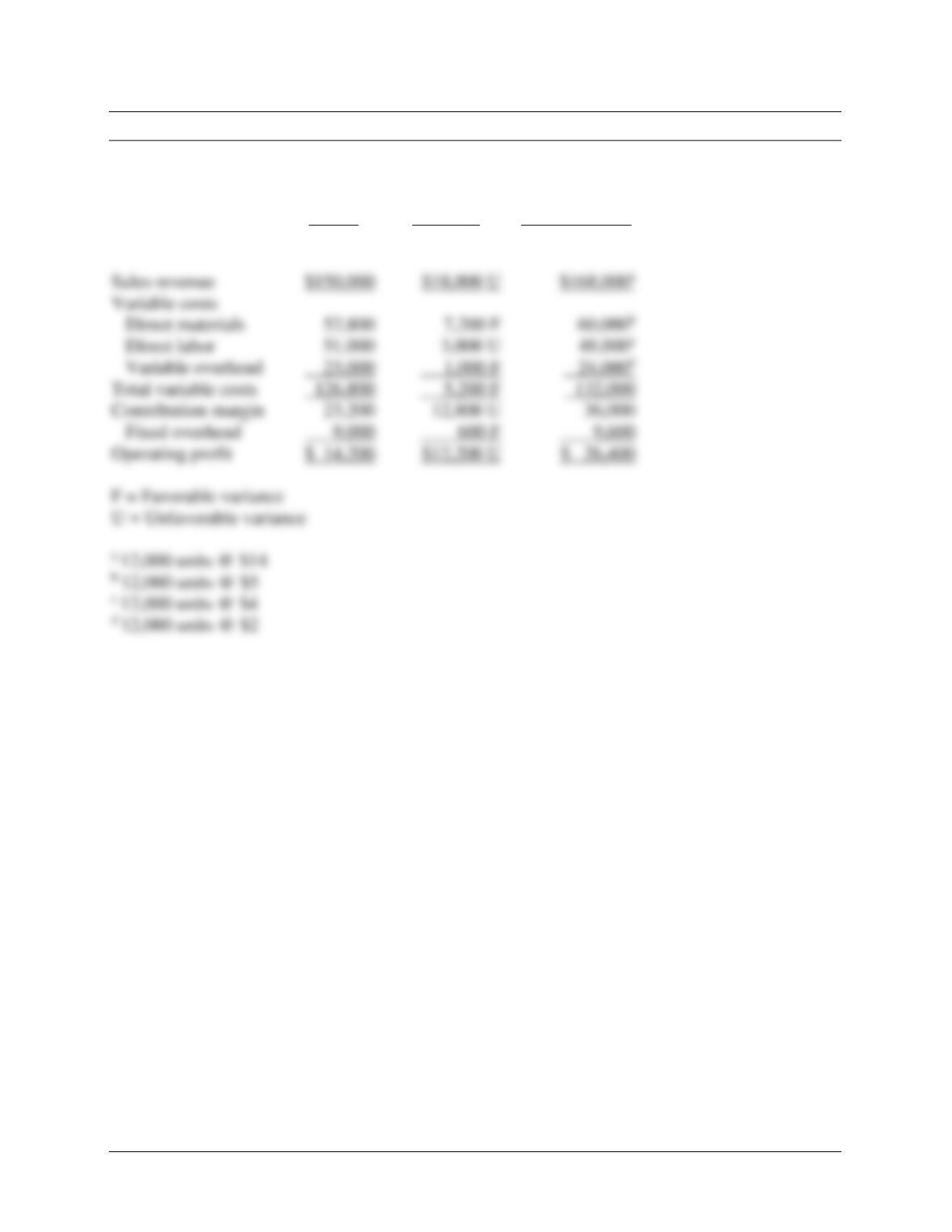

Demonstration Problem 1 – Solution

(1)

Actual

(3) = (1) – (2)

Variance

(2)

Master Budget

Units

10,000

2,000 U

12,000

Sales revenue

$18,000 U

Variable costs

Direct materials

52,800

Direct labor

51,000

3,000 U

Variable overhead

Total variable costs

Contribution margin

23,200

36,000

Fixed overhead

Operating profit

$12,200 U

16–30

Demonstration Problem 2 – Solution

(Continued from Demonstration Problem 1)

Required:

Prepare a profit variance analysis.

Demonstration Problem 2 – Solution

Actual

(Based on

Actual

Activity

of 10,000

Units

Sold)

Manufacturing

Variances

Sales

Price

Variance

Flexible

Budget

(Based on

Actual

Activity of

10,000

Units Sold)

Sales

Activity

Variance

Master

Budget

(Based

on 12,000

Units

Planned)

Sales revenue

$150,000

$10,000 F

$140,000a

$28,000 U

$168,000

Variable costs

Direct

10,000 F

Direct labor

Variable

Total variable

126,800

22,000 F

132,000

Contribution

Fixed

9,000

0

$ 14,200

$10,000 F

$ 6,000 U

$ 26,400

16–32

Demonstration Problem 3

(Continued from Demonstration Problem 1)

Information about the use of direct materials at EZ Toys’ Trucks Division for October follows:

Standard costs:

2 units per truck @ $2.50 per unit

=

$5 per truck

Trucks produced in October

=

10,000

Actual materials purchased and used:

22,000 units @ $2.40 per unit

=

$52,800

There was no beginning inventory on October 1.

Required:

Prepare the Truck Division’s direct materials variances for October.

16–33

Demonstration Problem 3 – Solution

Actual Costs =

Actual Input Quantity

Actual Input Quantity

Flexible Production Budget =

Standard Input Quantity Allowed

for Actual Output

16–34

Demonstration Problem 4

(Continued from Demonstration Problem 1)

Information about the use of direct labor at EZ Toys’ Trucks Division for October follows:

Standard costs:

0.4 hour per truck @ $10 per hour

=

$4 per truck

Trucks produced in October

=

10,000

Actual direct labor costs:

Actual hours worked

=

5,000

Total actual labor cost

=

$51,000

Average cost per hour

=

$10.20

Required:

Prepare the Truck Division’s direct labor variances for October.

Demonstration Problem 4 – Solution

Actual Costs =

Actual Input Quantity

Actual Input Quantity

Flexible Production Budget =

Standard Input Quantity Allowed

for Actual Output

16–36

Demonstration Problem 5

(Continued from Demonstration Problem 1)

Information about the use of variable overhead at EZ Toys’ Trucks Division for October follows:

Standard costs:

0.4 hour per truck @ $5 per hour

=

$2 per truck

Trucks produced in October

=

10,000

Actual variable overhead cost

=

$23,000

Required:

Prepare the Truck Division’s variable overhead variances for October.

16–37

Demonstration Problem 5 – Solution

Actual Costs =

Sum of Actual Variable

Actual Input Quantity

Flexible Production Budget =

Standard Input Quantity Allowed

for Actual Output

16–38

Demonstration Problem 6

(Continued from Demonstration Problem 1)

Information about the use of fixed overhead at EZ Toys’ Trucks Division follows:

Annual budget data:

Fixed overhead

=

$115,200

Direct labor hours

=

57,600

Standard fixed overhead rate

=

$2 per hour

Standard costs:

0.4 hour per truck @ $2 per hour

=

$0.80 per truck

Trucks produced in October

=

10,000

Actual variable overhead cost

=

$9,000

Required:

Prepare Truck Division’s fixed overhead variances for October.

Demonstration Problem 6 – Solution