1. In a centralized operation, all major planning and operating decisions are made by top management

In a decentralized operation, managers of separate divisions or units are delegated operating

2. The department manager of a profit center has responsibility for and authority over costs and

3. Payroll: Number of checks issued. Accounts payable: Number of invoices paid. Accounts

4. The major shortcoming of using income from operations as a measure of investment center

p

5. A division of a decentralized company could be considered the least profitable, even though

7. A balanced scorecard can indicate the underlying causes of financial performance from

innovation and learning, customer, internal, and financial perspectives. In addition, a

b

8. The objective of transfer pricing is to encourage each division manager to work in the best

b

9. When unused capacity exists in the supplying division, the negotiated price approach is

p

referred over the market price approach.

CHAPTER 23 (FIN MAN); CHAPTER 8 (MAN)

PERFORMANCE EVALUATION

DISCUSSION QUESTIONS

FOR DECENTRALIZED OPERATIONS

23-1

CHAPTER 23 Performance Evaluation for Decentralized Operations

PE 23–1A (FIN MAN); PE 8–1A (MAN)

PE 23–1B (FIN MAN); PE 8–1B (MAN)

PE 23–2A (FIN MAN); PE 8–2A (MAN)

Northeast Division Service Charge for Travel Department:

PE 23–2B (FIN MAN); PE 8–2B (MAN)

Retail Division Service Charge for Computer Technology Department:

PE 23–3A (FIN MAN); PE 8–3A (MAN)

Northeast Pacific

Division Division

Sales……………………………………………………

…

$1,155,000 $1,204,000

Cost of goods sold…………………………………… 590,800 658,000

PRACTICE EXERCISES

23-2

CHAPTER 23 Performance Evaluation for Decentralized Operations

PE 23–3B (FIN MAN); PE 8–3B (MAN)

Retail Commercial

Division Division

Sales……………………………………………………

…

$945,000 $966,000

PE 23–4A (FIN MAN); PE 8–4A (MAN)

PE 23–4B (FIN MAN); PE 8–4B (MAN)

PE 23–5A (FIN MAN); PE 8–5A (MAN)

Income from operations…………………………………………………………………… $90,000

PE 23–5B (FIN MAN); PE 8–5B (MAN)

Income from operations…………………………………………………………………… $420,000

PE 23–6A (FIN MAN); PE 8–6A (MAN)

PE 23–6B (FIN MAN); PE 8–6B (MAN)

Increase in Pembroke (Supplying)

Division’s Income from Operations =(Transfer Price – Variable Cost per Unit)

× Units Transferred

Increase in South (Supplying)

Division’s Income from Operations =(Transfer Price – Variable Cost per Unit)

× Units Transferred

23-4

CHAPTER 23 Performance Evaluation for Decentralized Operations

Ex. 23–1 (FIN MAN); Ex. 8–1 (MAN)

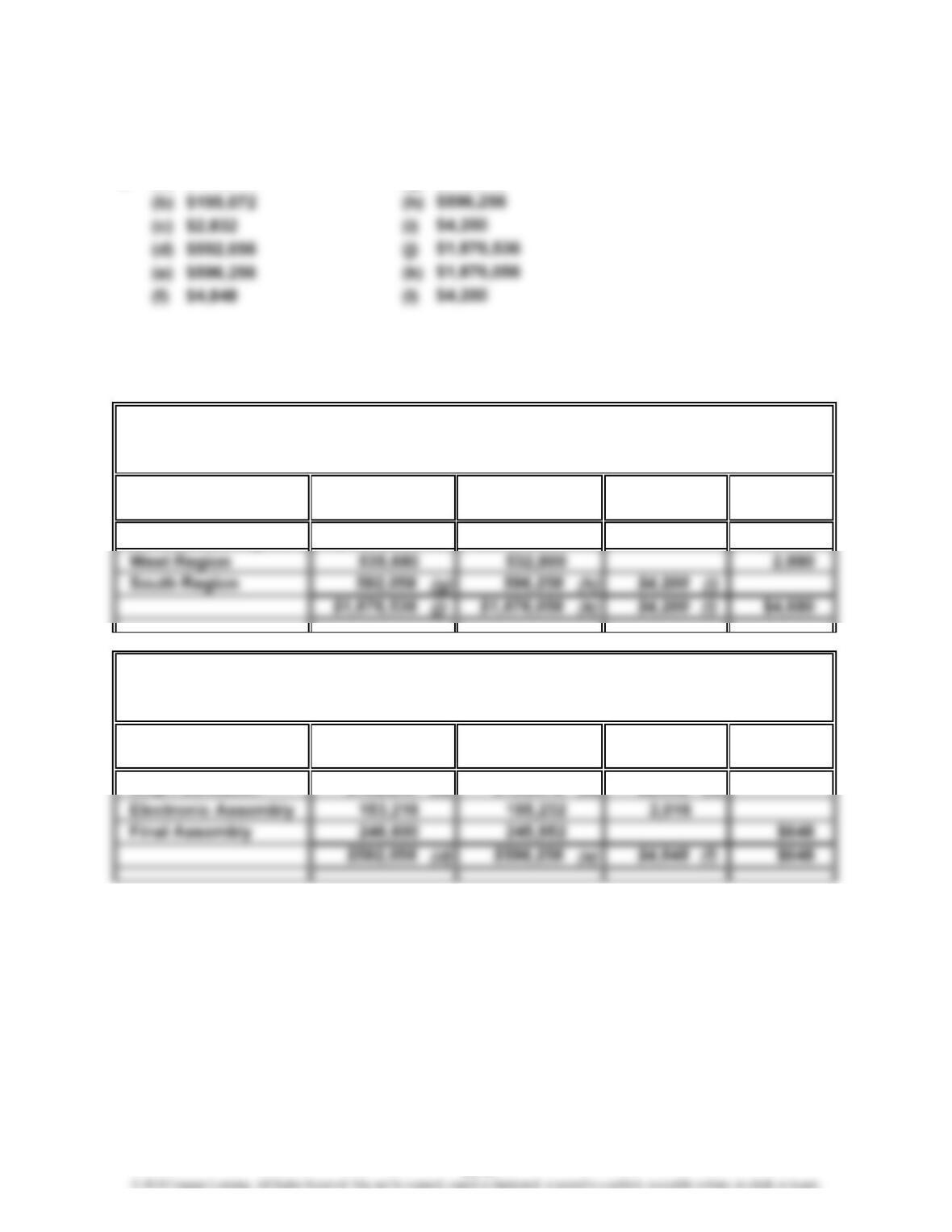

a. (a) $192,240 (g)

Schedules of supporting calculations (answers in italics; the solution requires

working from the department level, up to the plant level, then to the vice president

of production level):

Under

Budget

Mid-Atlantic Region $ 747,000 $1,800

Under

Budget

Chip Fabrication (a) $195,072 (b) $2,832 (c)

BudgetPlant

$192,240

Department

Actual

Over

Over

MAQUIRE COMPANY

Budget Performance Report—Manager, South Region Plant

For the Month Ended May 31, 2014

Budget

Budget Actual

Budget

$ 748,800

EXERCISES

MAQUIRE COMPANY

Budget Performance Report—Vice President, Production

For the Month Ended May 31, 2014

$592,056

23-5

CHAPTER 23 Performance Evaluation for Decentralized Operations

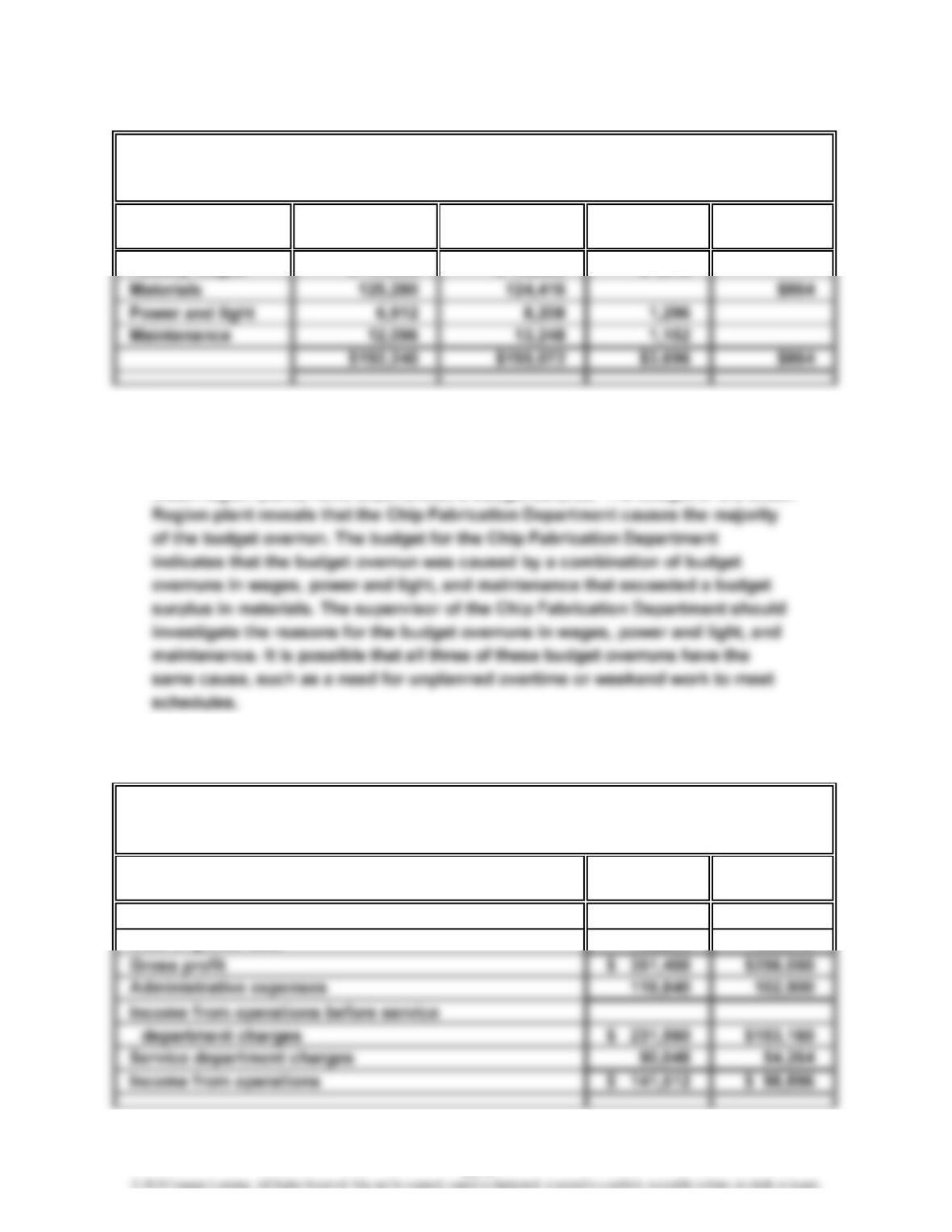

Ex. 23–1 (FIN MAN); Ex. 8–1 (MAN) (Concluded)

Under

Budget

Factory wages

b. MEMO

To: Holly Keller, Vice President of Production

The South Region plant has experienced a budget overrun, while the Mid-Atlantic and

West Region plants have experienced a budget surplus. The budget of the South

Ex. 23–2 (FIN MAN); Ex. 8–2 (MAN)

Residential

Division

Net sales $595,000

Cost of goods sold 338,940

$1,083,600

732,200

For the Year Ended June 30, 2014

Commercial

Division

ENDLESS RIVER CONSTRUCTION COMPANY

Divisional Income Statements

$ 47,952 $1,248

Over

MAQUIRE COMPANY

Budget Performance Report—Supervisor, Chip Fabrication

For the Month Ended May 31, 2014

Cost BudgetBudget Actual

$ 49,200

23-6

CHAPTER 23 Performance Evaluation for Decentralized Operations

Ex. 23–3 (FIN MAN); Ex. 8–3 (MAN)

Expense Activity Bases

a. Legal Number of hours

b. Duplication services Number of pages

Ex. 23–4 (FIN MAN); Ex. 8–4 (MAN)

23-7

CHAPTER 23 Performance Evaluation for Decentralized Operations

Ex. 23–5 (FIN MAN); Ex. 8–5 (MAN)

Government

a. Residential Commercial Contract Total

Number of payroll checks:

Service Activity Charge

b. Dept. Cost ÷ Base = Rate

Service department charge rates:

Government

Residential Commercial Contract Total

Service department charges:

c. Residential’s service department charge is higher than the other two divisions

because Residential is a heavy user of service department services. Residential

3

21

23-8

CHAPTER 23 Performance Evaluation for Decentralized Operations

Ex. 23–6 (FIN MAN); Ex. 8–6 (MAN)

$160,000

3,200 calls

b. October charges to the COMM sector:

Help desk charge:

(5,200 employees × 25% × 96% × 1.5) × $50/call = $93,600

Network center charge:

= $50 per call

a. Help desk:

23-9

CHAPTER 23 Performance Evaluation for Decentralized Operations

Ex. 23–7 (FIN MAN); Ex. 8–7 (MAN)

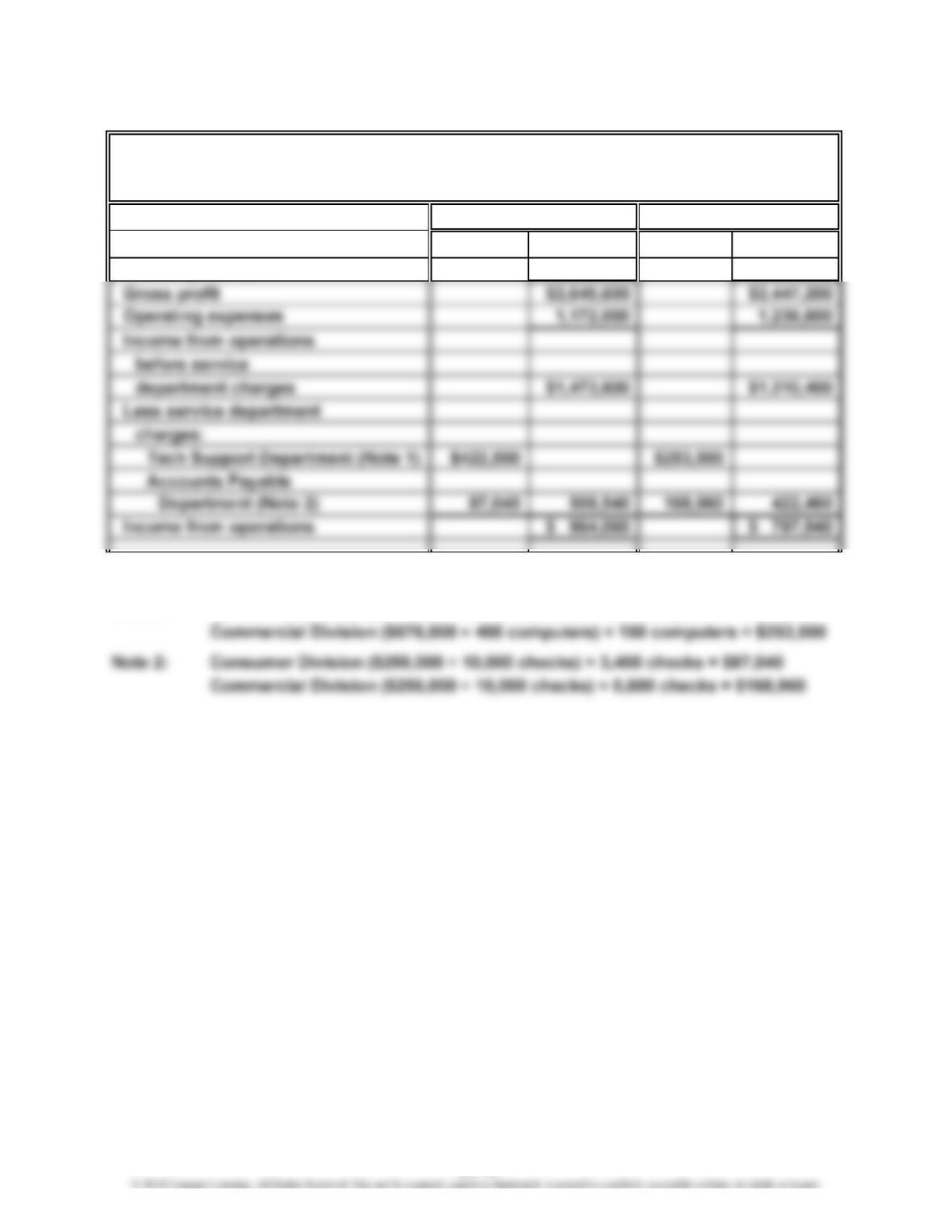

Revenues $5,944,000 $4,947,200

Cost of goods sold 3,298,400 2,500,000

Supporting calculations for controllable service department charges:

Note 1: Consumer Division ($676,000 ÷ 400 computers) × 250 computers = $422,500

VAN EMBURGH TECHNOLOGY

Divisional Income Statements

For the Year Ended December 31, 2014

Consumer Division Commercial Division

23-10

CHAPTER 23 Performance Evaluation for Decentralized Operations

Ex. 23–8 (FIN MAN); Ex. 8–8 (MAN)

a. The reported income from operations does not accurately measure performance

because the service department charges are based on revenues. Revenues are

b.

Revenues $3,025,000 $3,025,000

Operating expenses 2,450,000 2,736,000

Income from operations

before service department

Supporting calculations for controllable service department charges:

Training: Passenger Division, ($250,000 ÷ 500 personnel trained)

× 350 personnel trained

WILD SUN AIRLINES INC.

Divisional Income Statements

For the Year Ended December 31, 2014

Passenger Division Cargo Division

23-11

CHAPTER 23 Performance Evaluation for Decentralized Operations

Ex. 23–9 (FIN MAN); Ex. 8–9 (MAN)

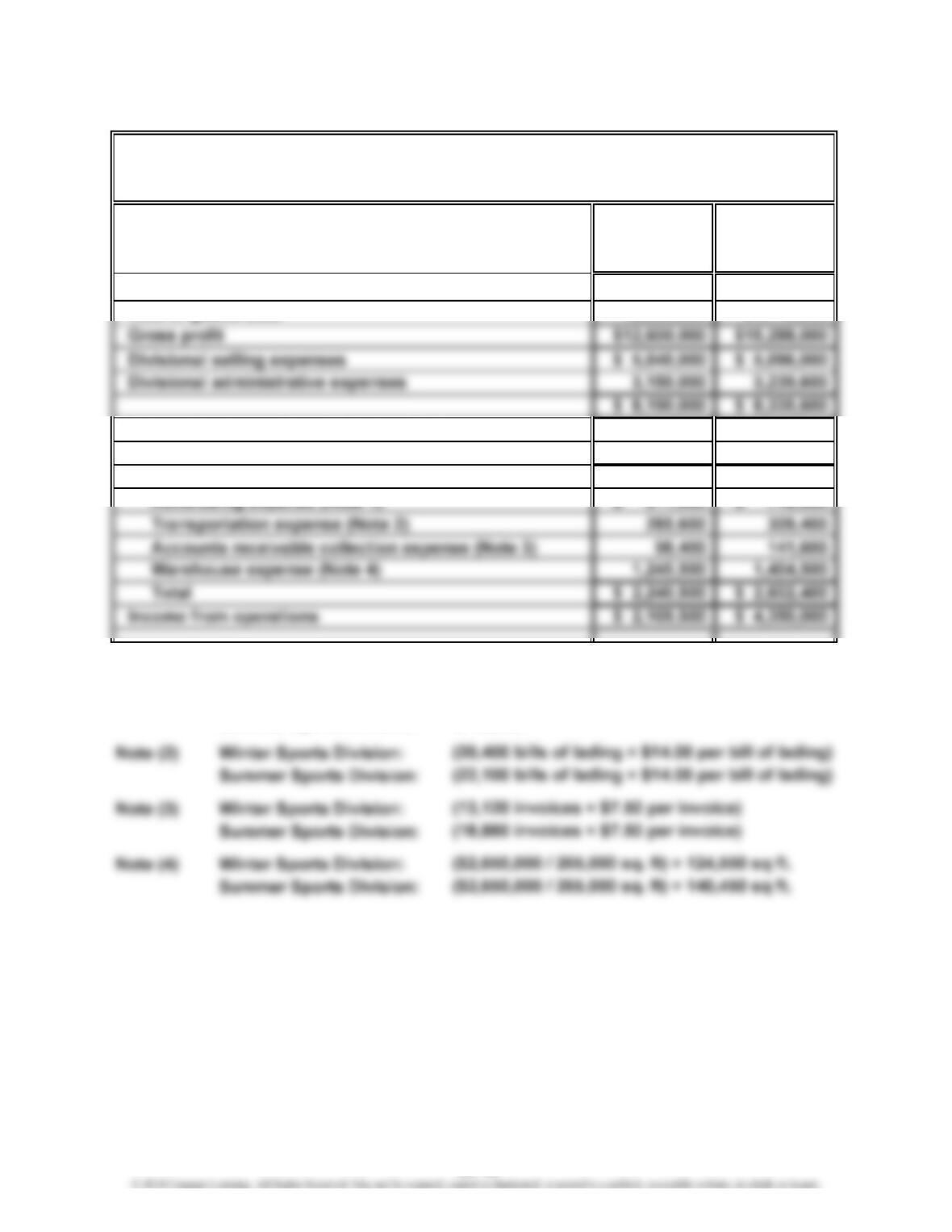

Winter Summer

Sports Sports

Division Division

Sales $31,500,000 $36,400,000

Cost of goods sold 18,900,000 21,112,000

Income from operations before service

department charges $ 4,410,000 $ 6,952,400

Less service department charges:

Supporting Schedule:

Note (1) Winter Sports Division: $611,000

Summer Sports Division: $746,900

FULL THROTTLE SPORTING GOODS CO.

Divisional Income Statements

For the Year Ended December 31, 2014

23-12

CHAPTER 23 Performance Evaluation for Decentralized Operations

Ex. 23–10 (FIN MAN); Ex. 8–10 (MAN)

a. Retail Division: 20% ($130,000 ÷ $650,000)

Ex. 23–11 (FIN MAN); Ex. 8–11 (MAN)

a. Retail Commercial Internet

Division Division Division

Income from operations………………………

…

$130,000 $72,000 $137,500

Minimum amount of income from

operations:

b. Internet Division

Ex. 23–12 (FIN MAN); Ex. 8–12 (MAN)

a. 2.40 = 12% ÷ 5%

23-13

CHAPTER 23 Performance Evaluation for Decentralized Operations

Ex. 23–13 (FIN MAN); Ex. 8–13 (MAN)

Sales

Invested Assets

b. The profit margin would increase from 25% to 30%, the investment turnover

would remain unchanged, and the rate of return on investment would increase

from 35% to 42%, as shown below.

Sales

Invested Assets

a. Rate of Return

on Investment = Profit Margin × Investment Turnover

×

=

Rate of Return

on Investment Sales

Income from Operations

Rate of Return

on Investment = Profit Margin × Investment Turnover

Rate of Return

on Investment =Income from Operations ×

Sales

23-14

CHAPTER 23 Performance Evaluation for Decentralized Operations

Ex. 23–14 (FIN MAN); Ex. 8–14 (MAN)

Revenues

Invested Assets

$6,146 $18,714

$18,714 $27,244

$1,553 $11,797

$11,797 $19,530

$618 $6,351

$6,351 $12,221

$816 $3,049

$3,049 $4,992

b. The four sectors are different from each other. Media Networks combines a good

profit margin with a very low investment turnover. Media Networks is sensitive to

Income from Operations

Consumer Products: ×

× Parks and Resorts:

Studio Entertainment: ×

=

Rate of Return

on Investment

a. ×

Media Networks: ×

Revenues

23-15

CHAPTER 23 Performance Evaluation for Decentralized Operations

Ex. 23–15 (FIN MAN); Ex. 8–15 (MAN)

a. 25.0% ($215,000 ÷ $860,000) g. $64,000 ($320,000 × 20%)

Ex. 23–16 (FIN MAN); Ex. 8–16 (MAN)

a. (a) $60,000 ($750,000 × 8%)

(b) $300,000 ($60,000 ÷ 20%)

23-16

CHAPTER 23 Performance Evaluation for Decentralized Operations

Ex. 23–17 (FIN MAN); Ex. 8–17 (MAN)

Revenues

Invested Assets

$105 $688

$688 $2,139

b. Vacation

Ownership

c. The Vacation Ownership (VO) segment has the weakest return on investment,

which is mainly the result of a weak investment turnover. The VO segment earns

profit margins that are higher than the profit margins in the Hotel Ownership (HO)

Revenues

Ownership

Hotel

Income from Operations

a.

Vacation Ownership: ×

× =

Rate of Return

on Investment

23-17

CHAPTER 23 Performance Evaluation for Decentralized Operations

Ex. 23–18 (FIN MAN); Ex. 8–18 (MAN)

Although there is some judgment in classifying each of these measures, the following

represents the author’s assessment with explanations:

Average card member spending Customer—demonstrates the usefulness of

the card to the customer.

23-18

CHAPTER 23 Performance Evaluation for Decentralized Operations

Ex. 23–19 (FIN MAN); Ex. 8–19 (MAN)

a. UPS wanted a performance measurement system that would focus more on

the underlying drivers, or levers, of financial success. It believed that focusing on

the financial numbers by themselves would not reveal how financial objectives

b. The employee sentiment number is common in service businesses. The

employees are the face of the company to the customer. If employees feel poorly

Ex. 23–20 (FIN MAN); Ex. 8–20 (MAN)

a. Increase in Dart Industries’ Market Variable Cost Unit

Income from Operations = Price – per Unit × Transferred

$2,200,000 =($180 –$125) × 40,000

23-19

CHAPTER 23 Performance Evaluation for Decentralized Operations

Ex. 23–21 (FIN MAN); Ex. 8–21 (MAN)

a. Increase in Dart Industries’ Market Variable Cost Units

Income from Operations = Price – per Unit × Transferred

This amount is the same amount by which Dart Industries’ income from operations

increased in Ex. 23–20 (FIN MAN); Ex 8–20 (MAN), when a transfer price of $145 was

used.

b. Increase in the Instrument Division’s Market Transfer Units

Income from Operations = Price – Price × Transferred

This is the amount the Instrument Division saves by purchasing from the

Components Division at an internal price that is lower than the market price.

c. Increase in the Components Division’s Transfer Variable Cost Units

Income from Operations = Price – per Unit × Transferred

d. Any transfer price will cause the total income of the company to increase,