Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

16-1

CHAPTER 16

REPORTING THE STATEMENT OF CASH FLOWS

Related Assignment Materials

Student Learning Objectives

Questions

Quick

Studies*

Exercises*

Problems*

Beyond the

Numbers

Conceptual objectives:

C1. Distinguish between operating,

investing, and financing

activities, and describe how

noncash investing and financing

activities are disclosed

1, 2, 3, 5, 7,

8, 9,14

16-1, 16-20

16-1, 16-14

16-3, 16-4,

16-6, 16-8,

16-7, 16-8,

16-9, 16-10

Analytical objectives:

A1. Analyze the statement

of cash flows and apply the

cash flow on total assets ratio.

1, 9, 12, 13

16-17

16-10, 16-11

16-3,

GL 16-1

16-1, 16-2,

16-3, 16-5,

16-6, 16-7,

16-8

Procedural objectives:

P1. Prepare a statement of cash

flows.

16-2, 16-9,

16-19

16-9, 16-11,

16-12, 16-17,

16-3, 16-4,

16-5, 16-6,

GL16-3, ES

P2. Compute cash flows from

operating activities using

the indirect method.

6, 10, 11

16-3, 16-4,

16-5, 16-6,

16-11, 16-19

16-2, 16-3,

16-4, 16-5,

16-6, 16-11

GL 16-3

16-1, 16-3,

16-4, 16-6,

16-7, SP,

GL 16-1,

GL 16-2,

16-6

P3. Determine cash flows from

both investing and financing

activities.

2, 3, 7, 8, 9,

15

16-7, 16-8,

16-9, 16-10,

16-12, 16-13,

16-19

16-7, 16-8,

16-11, 16-12,

16-17, 16-18

16-3, 16-4,

16-5, 16-6,

16-7, 16-8,

SP,GL16-1,

GL 16-3

P4A.Illustrate use of a spreadsheet to

prepare a statement of

cash flows (Appendix 16A)

16-18

16-13

16-4, 16-7

P5B.Compute cash flows from

operating activities using

the direct method.

(Appendix 16B)

4, 5

16-14, 16-15,

16-16

16-12, 16-14,

16-15, 16-16,

16-17, 16-18

16-2, 16-5,

16-8

16-6

*See additional information on next page that pertains to these quick studies, exercises and problems.

SP refers to the Serial Problem

GL refers to the General Ledger Problems

ES refers to the Excel Simulations

SP, GL16-1,

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

16-2

Additional Information on Related Assignment Material

Connect

Available on the instructor’s course-specific website) repeats all numerical Quick Studies, all Exercises and

Problems Set A. Connect also provides algorithmic versions for Quick Study, Exercises and Problems. It allows

instructors to monitor, promote, and assess student learning. It can be used in practice, homework, or exam mode.

Connect Insight

The first and only analytics tool of its kind, Connect Insight is a series of visual data displays that are each framed

The Serial Problem for Success Systems continues in this chapter.

General Ledger

Assignable within Connect, General Ledger (GL) problems offer students the ability to see how transactions post

from the general journal all the way through the financial statements. Critical thinking and analysis components are

added to each GL problem to ensure understanding of the entire process. GL problems are auto-graded and provide

instant feedback to the student.

Excel Simulations

Assignable within Connect, Excel Simulations allow students to practice their Excel skills—such as basic formulas

and formatting—within the context of accounting. These questions feature animated, narrated Help and Show Me

tutorials (when enabled). Excel Simulations are auto-graded and provide instant feedback to the student.

Synopsis of Chapter Revisions

NEW opener—Amazon and entrepreneurial assignment.

Continued infographics on examples of operating, investing, and financing cash flows.

Kept 5-step process for preparing statement of cash flows.

New graphic on use of Indirect vs Direct methods.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

16-3

Chapter Outline

Notes

I. Basics of Cash Flow Reporting

A. Purpose of a Statement of Cash Flows

To report all major cash receipts (inflows) and cash payments

(outflows) during a period. This report classifies cash flows into

operating, investing, and financing activities. It answers important

questions such as:

1. How does a company obtain its cash?

2. Where does a company spend its cash?

3. What explains the change in the cash balance?

4. How much is paid in cash dividends?

B. Importance of Cash Flows

Information about cash flows, and its sources and uses, can

influence decision makers in important ways.

C. Measurement of Cash Flows

The phrase, cash flows refers to both cash and cash equivalents. A

cash equivalent must satisfy two criteria:

2. Be sufficiently close to its maturity date so its market value is

unaffected by interest rate changes.

D. Classifications of Cash Flows

Cash receipts and cash payments are classified and reported in one

of three categories:

1. Operating activities include transactions and events that

determine net income (with some exceptions such as unusual

gains and losses). Specific examples:

a. Cash inflows from cash sales, collections on credit sales,

receipts of dividends and interest, sale of trading

securities, and settlements of lawsuits.

b. Cash outflows for payments to suppliers for goods and

services, to employees for wages, to lenders for interest, to

government for taxes, to charities, and to purchase trading

securities.

2. Investing activities include transactions and events that affect

long-term assets, namely the purchase or sale of these assets.

Specific examples:

a. Cash inflows from selling long-term productive assets,

selling available-for-sale securities, notes and held-to–

maturity securities, and collecting principal on loans to

assets, purchasing available for sale securities and held-to–

maturity securities, and making loans to others.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

16-4

Chapter Outline

Notes

3. Financing activities include transactions and events that affect

long-term liabilities and equity:

a. Cash inflows from owner contributions, from issuing

company’s own stock, from issuing bonds and notes and

from issuing short and long-term debt.

b. Cash outflows from repaying cash loans, owner’s

withdrawals, paying shareholder’s cash dividend and

purchasing treasury stock.

E. Noncash Investing and Financing Activities

Activities that do not affect cash receipts or payments but because

of their importance and the full disclosure principle they are

disclosed at the bottom of the statement of cash flows or in a note

to the statement.

F. Format of the Statement of Cash Flows

1. Lists cash flows by categories (operating, financing and

2. Combines the net cash flow in each of the three categories and

identifies the net change in cash for the period.

4. Contains a separate schedule or note disclosure of any noncash

financing and investing activities.

G. Preparing the Statement of Cash Flow

1. Five steps:

a. Compute the net increase or decrease in cash (bottom line

or target number).

b. Compute and report net cash provided (used) by operating

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

16-5

Chapter Outline

Notes

2. Sources of information for preparing the statement of cash

flows

3. Alternative approaches to preparing the statement:

a. Analyzing the cash account.

b. Analyzing noncash accounts.

II. Cash Flows from Operating Activities

A. Indirect and Direct Methods of Reporting—Two ways of reporting

that apply only to the operating activities section.

1. Direct Method—separately lists each major item of operating

2. Indirect Method—reports net income and then adjusts it for

3. Note that the net cash provided (used) by operating activities

is identical under both the direct and indirect method.

B. Applying the Indirect Method

provided (used) by operating activities.

1. Reports net income using accrual accounting, and then adjusts

2. The types of adjustments are:

a. to income statement items involving operating activities

that do not affect

i. Revenues and gains are deducted from net income.

ii. Expenses and losses are added back to net income.

b. for changes in current assets (other than cash) and current

liabilities

i.Decreases in noncash current assets are added to net

income.

C. Summary Adjustments for the Indirect method—see Exhibit

16-12 in text.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

16-6

Chapter Outline

Notes

III. Cash Flows from Investing—identical under direct and indirect

methods. Three-stage process of analysis to determine cash provided

(used) by investing activities:

A. Identify changes in investing-related accounts (all non-current

assets, and the current accounts for both notes receivable and

investments in securities—excluding trading securities).

IV. Cash Flows from Financing— identical under direct and indirect

methods. Three-stage process of analysis to determine cash provided

(used) by financing activities:

A. Identify changes in financing-related accounts (all non-current

liabilities—including current portion of any notes and bonds, and

the equity accounts).

B. Explain these changes to identify their cash flows effects using

reconstruction analysis (reconstructed entries—not the actual

entries by the preparer).

C. Report their cash flow effects.

V. Proving Cash Balances

Last step in preparing the statement is to report the beginning and

ending cash balances and provide that the net change in cash is

explained by operating, investing and financing cash flows. Exhibit

16-13 in text.

VI. Decision Analysis—Cash Flow Analysis

A. Analyzing Cash Sources and Uses

2. Creditor and investor decisions are also based on a company’s

cash flow evaluations.

3. Operating cash flows are generally considered to be most

reconstruction analysis (reconstructed entries—not the actual

entries by the preparer).

C. Report their cash flow effects.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

16-7

Chapter Outline

Notes

B. Cash Flow on Total Assets

2. Computed by dividing cash flow from operations by average

total assets.

VIII. Spreadsheet Preparation of the Statement of Cash Flows

(Appendix 16A)

A spreadsheet approach may be used to organize and analyze the

information to prepare a statement of cash flows by the indirect

method, including the supplemental disclosures of noncash investing

and financing activities.

A. The spreadsheet has four columns containing dollar amounts.

1. Columns one and four contain the beginning and ending

balances of each balance sheet account.

2. Columns two and three are for reconciling the changes in

each balance sheet account.

B. Separate sections on the working paper present (a) balance

sheet items with debit balances; (b) balance sheet items with

credit balances; (c) cash flows from operating activities,

starting with net income; (d) cash flows from investing

activities; (e) cash flows from financing activities; and (f)

noncash investing and financing activities.

C. Information for sections (c) – (f) is developed in four steps in

the Analysis of Changes columns:

1. By adjusting net income for the changes in all noncash

2. By eliminating from net income the effects of all noncash

3. By eliminating from net income any gains or losses from

investing and financing activities. This involves the

4. By entering any remaining items, such as dividend

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

16-8

Chapter Outline

Notes

IX. Direct Method of Reporting Operating Cash Flows (Appendix

16B)

A. Separately list each major item or class of operating cash

receipts and cash payments.

B. Classes of operating cash receipts include cash received from

customers, renters, interest, and dividends.

C. Classes of operating cash payments include cash paid to

suppliers, to employees and other operating expense, interest,

and income taxes.

D. Subtract the cash payments from cash receipts to determine

the net cash provided (used) by operating activities.

E. The items to be listed are determined by adjusting individual

F. Exhibit 16B.6 summarizes the common adjustments for the

items making up net income to arrive at net cash provided

(used) by operating activities under the direct method.

G. This is the method recommended (but not required) by the

FASB.

H. When the direct method is used, the FASB requires a

reconciliation of net income to net cash provided (used) by

operating activities. This is operating cash flows computed

using the indirect method.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

16-9

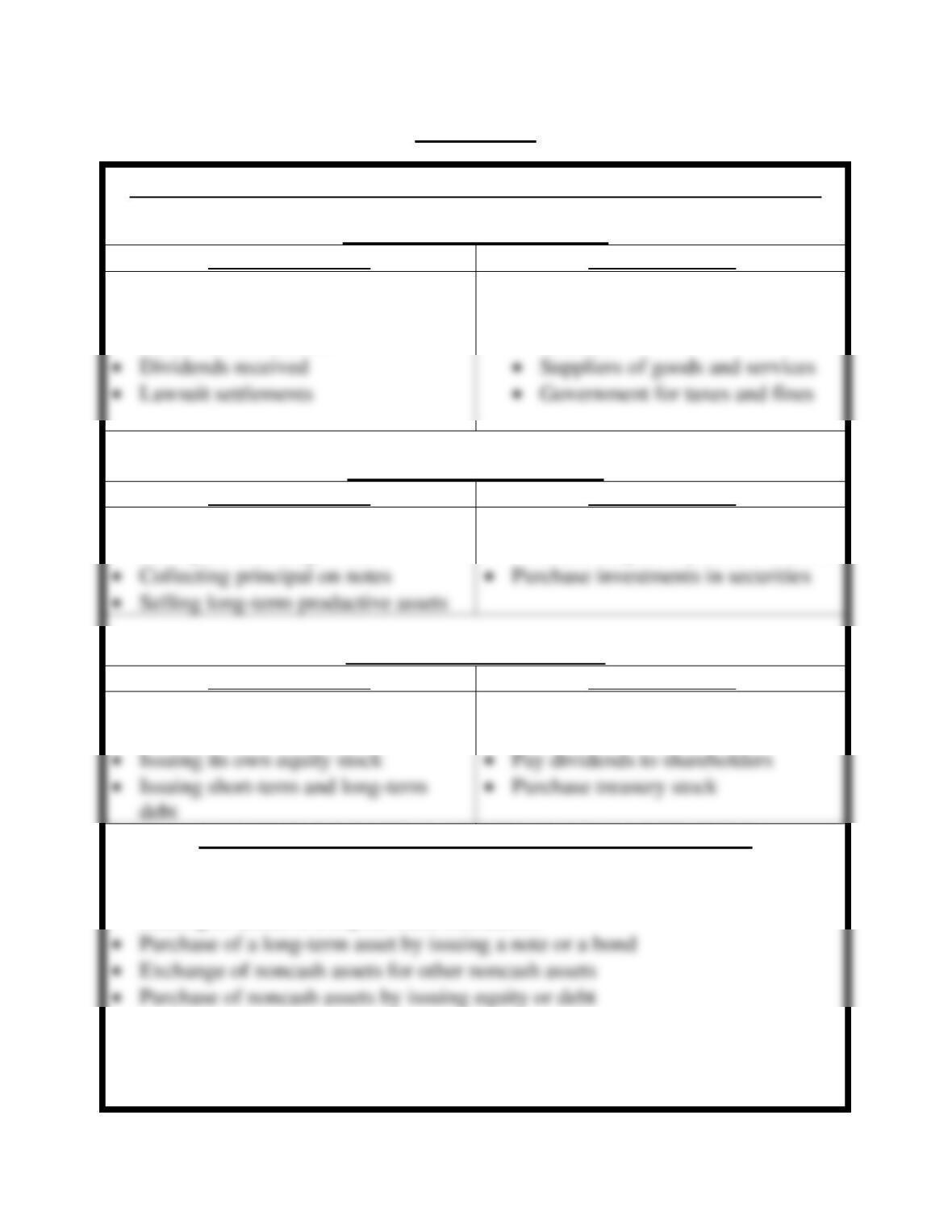

VISUAL #16-1

CLASSIFYING ACTIVITIES IN THE STATEMENT OF CASH FLOWS

OPERATING ACTIVITIES

Cash inflows from

Cash outflows to

• Customers for cash sales

• Collections on credit sales

• Borrowers for interest

• Salaries and wages

• Lenders for interest

• Charities

INVESTING ACTIVITIES

Cash inflows from

Cash outflows to

• Selling investments in securities

• Selling (discounting) notes

• Make loans to others

• Purchase long-term productive assets

FINANCING ACTIVITIES

Cash inflows from

Cash outflows to

• Contributions by owners

• Issuing notes and bonds

• Repay cash loans

• Pay withdrawals by owners

NONCASH INVESTING AND FINANCING ACTIVITIES

• Retirement of debt by issuing equity stock

• Conversion of preferred stock to common stock

• Leasing of assets in a capital lease transaction

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

16-10

VISUAL #16-2

STEPS TO DETERMINE INFORMATION

STATEMENT OF CASH FLOWS

1. Find change in Cash—This is the target number.

2. Find cash flow from operations

(Using direct or indirect method)

3. Find Cash Flow from A. Financing and

B. Investing

Procedure:

4. Combine cash flows from all three activities (from 2 and 3) to find

net cash flow and prove change in cash. (Target number

determined in Step 1).

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

16-11

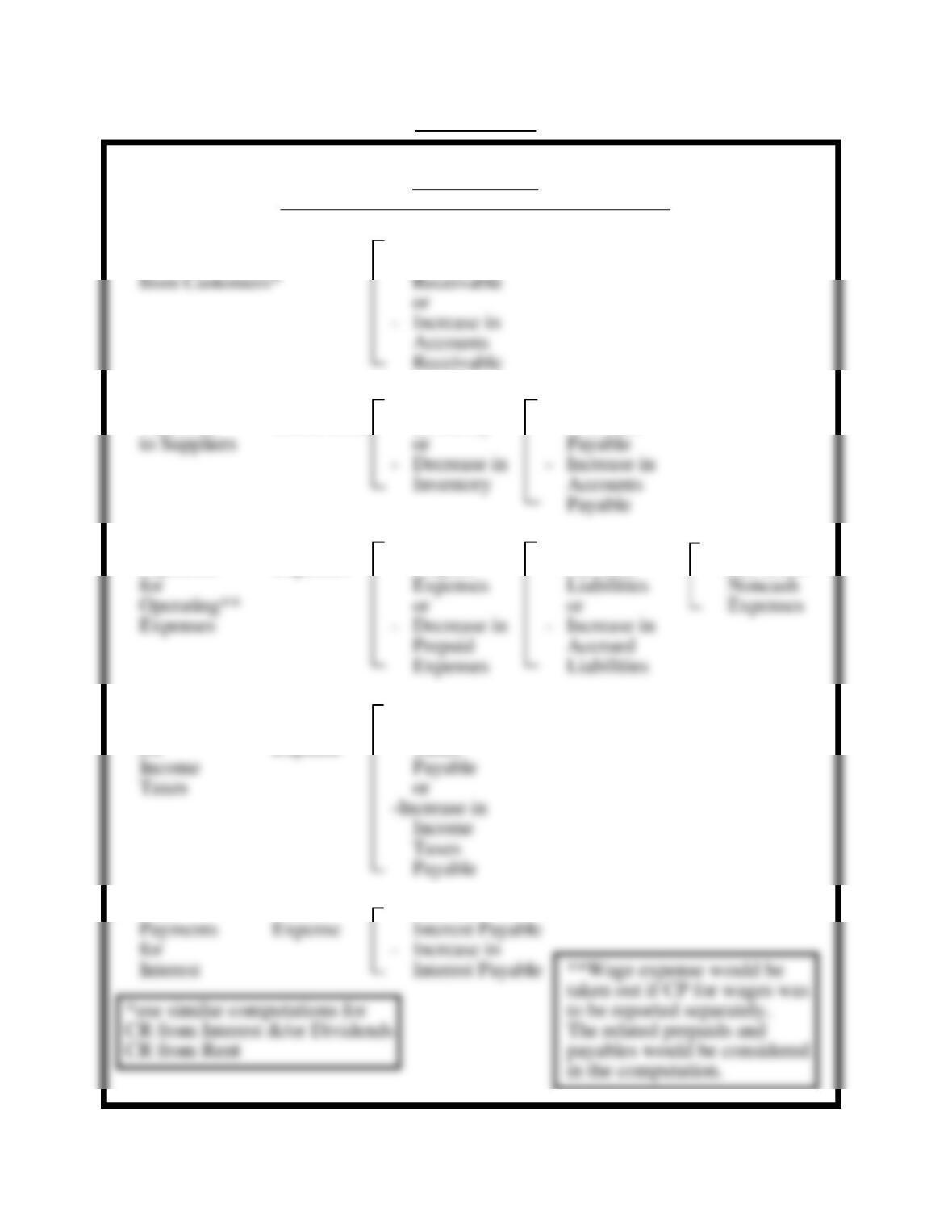

VISUAL #16-3

Determining Cash Flows from Operating Activities

Direct Method

(Need income statement and balance sheet data)

1. Cash = Sales + Decrease in

Receipts Accounts

2. Cash = Cost of + Increase in + Decrease in

Payments Goods Sold Inventory Accounts

3. Cash = Operating + Increase in + Decrease in – Depreciation

Payments Expenses Prepaid Accrued and Other

4. Cash = Income + Decrease in

Payments Taxes Income

for Expense Taxes

5. Cash = Interest + Decreases in

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

16-12

VISUAL #16-4

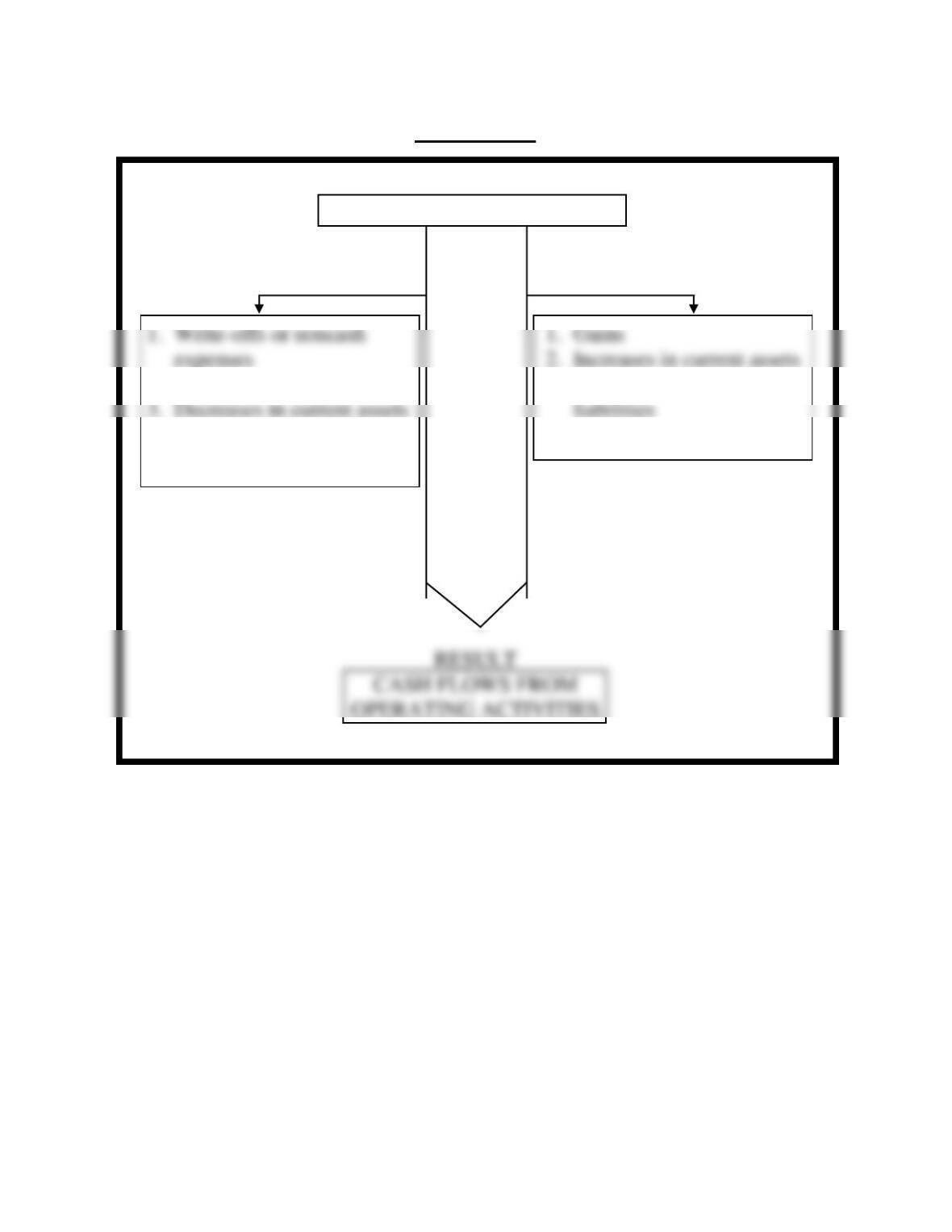

START WITH

NET INCOME OR (NET LOSS)

Add Subtract

2. Losses 3. Decreases in current

4. Increases in current

liabilities.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

16-13

Chapter 16 Alternate Demonstration Problem

The Carpet Company’s 2017 and 2018 balance sheets included the

following items:

December 31

2018

2017

Debits

Credits

Accumulated depreciation, equipment ………………….

$ 4,000

$ 3,000

Accounts payable …………………………………………………

Taxes payable ………………………………………………………

Common stock, $10 par value ……………………………….

Retained earnings ………………………………………………..

Totals ………………………………………………………….

$57,500

$46,000

The Carpet Company’s income statement was as follows:

CARPET COMPANY

Income Statement

For the Year Ended December 31, 2018

Sales ……………………………………………………………………

$61,000

$40,000

Wages and other operating expenses……………………

Depreciation expense …………………………………………..

$ 9,000

$10,500

$ 4,000

Accounts receivable …………………………………………….

Merchandise inventory …………………………………………

Equipment ……………………………………………………………

Totals ………………………………………………………….

$57,500

$46,000

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

16-14

Required:

Prepare the statement of cash flows under both the direct method and the

indirect method for the year ended December 31, 2018. Additional

information includes the following:

a. Equipment costing $3,500 was purchased during the year.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

16-15

Chapter 16 Solution: Alternate Demonstration Problem

Direct Method:

CARPET COMPANY

Statement of Cash Flows

For Year Ended December 31, 2018

Cash flows from operating activities:

Cash received from customers ………………………….

$ 62,000

Cash paid for merchandise ……………………………….

)

expenses ………………………………………………………

)

Cash paid for taxes …………………………………………..

)

Net cash provided by operating activities ………….

Cash flows from investing activities:

Cash paid for purchase of plant assets ……………..

)

Net cash used by investing activities ………………..

)

Cash flows from financing activities:

Cash received from issuing stock ……………………..

Cash paid for dividends …………………………………….

)

Net cash provided by financing activities ………….

Net increase in cash ……………………………………………….

Cash balance at end of 2017 …………………………………..

Cash balance at end of 2018 …………………………………..

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

16-16

Indirect Method:

CARPET COMPANY

Statement of Cash Flows

For Year Ended December 31, 2018

Cash flows from operating activities:

Net income …………………………………………………………….

$ 9,000

Adjustments to reconcile net income to net cash

provided by operating activities:

Decrease in accounts receivable ……………………….

Increase in merchandise inventory ……………………

)

Increase in accounts payable …………………………...

Decrease in taxes payable …………………………………

)

Net cash provided by operating activities ………….

Cash flows from investing activities:

Net cash used by investing activities ………………..

)

Cash flows from financing activities:

Cash received from issuing stock ……………………..

Cash paid for dividends …………………………………….

)

Net cash provided by financing activities ………….

Net increase in cash ……………………………………………….

Cash balance at end of 2017 …………………………………..