Chapter 16—Management Accounting: A Business Partner

Financial and Managerial Accounting, 18e 16-1

16 MANAGEMENT ACCOUNTING: A BUSINESS PARTNER

Chapter Summary

The introduction to management accounting begins with an overview of the design

requirements of a managerial accounting system. The system must allocate decision-making

authority over a company’s resources. Second, it must furnish the information to support decision

making by managers. Finally, the system must generate the information needed to evaluate and

reward performance.

The chapter then proceeds to analyze the design of a system to account for manufacturing

operations. Manufacturing costs are first classified into direct material, direct labor, and

manufacturing overhead. With these definitions established, we introduce the critical distinction

between product and period costs. This discussion in turn lays the foundation for introducing the

manufacturing inventory accounts: raw materials, work-in-process, and finished goods.

The flow of costs through the inventory accounts is explained with the help of an extended

illustration. The illustration provides examples of the various manufacturing costs and their

associated classifications for a bicycle manufacturer.

The chapter closes with the development of financial statements for a manufacturing

company. The schedule of cost of goods manufactured is introduced as a supplement to the

financial statements intended to assist managers in evaluating the overall costs of manufactured

products.

Learning Objectives

1. Explain the three principles guiding the design of management accounting systems.

2. Describe the three basic types of manufacturing costs.

3. Distinguish between product costs and period costs.

4. Describe how manufacturing costs flow through perpetual inventory accounts.

5. Distinguish between direct and indirect costs.

6. Prepare a schedule of the cost of finished goods manufactured.

Chapter 16—Management Accounting: A Business Partner

16-2 Instructor’s Resource Manual

Brief Topical Outline

A. Management accounting: basic framework

1. Management accounting’s role in assigning decision-making authority

2. Management accounting’s role in decision making

3. Management accounting’s role in performance evaluation and rewards

4. Accounting systems: a business partner

B. Accounting for manufacturing operations

1. Classifications of manufacturing costs

2. Product costs versus period costs—see Ethics, Fraud, & Corporate

Governance (page 729)

3. Product costs and the matching principle

4. Inventories of a manufacturing business—see International Case in Point (page

730)

5. The flow of costs parallels the flow of physical goods

6. Accounting for manufacturing costs: an illustration

7. Direct materials

8. Direct labor

9. Manufacturing overhead

a. Recording overhead costs

10. Direct and indirect manufacturing costs

11. Work in process inventory, finished goods inventory, and the cost of goods

sold—see Your Turn (page 734)

12. The need for per-unit cost data

13. Determining the cost of finished goods manufactured—see Pathways

Connection (page 737)

a. Purpose of the schedule

14. Financial statements of a manufacturing company

C. Concluding remarks

Topical Coverage and Suggested Assignment

Class

Meetings on

Chapter

Topical

Outline

Coverage

Discussion

Questions*

Brief

Exercises*

Exercises*

Problems*

Critical

Thinking

Cases*

1

A

1, 2, 3

1, 5, 10

2, 7

2

2

B

6, 9, 11

3, 6

1, 3, 4

4, 5

1

3

B – C

12, 14, 15

8, 10

6, 9, 13

8

*Homework assignment (to be completed prior to class)

Chapter 16—Management Accounting: A Business Partner

Financial and Managerial Accounting, 18e 16-3

Comments and Observations

Teaching Objectives for Chapter 16

Beginning with this chapter, we shift our focus from financial accounting to managerial

accounting. In presenting this first managerial chapter, our classroom objectives are to:

1. Introduce the design requirements for a management accounting system.

2. Introduce the concept of product costs, and explain how and when product costs ultimately

are deducted from revenue.

3. Describe the three basic types of manufacturing costs; equate manufacturing costs with

product costs.

4. Illustrate and explain the “flow” of manufacturing costs through perpetual inventory records.

5. Identify the three types of inventory that may be held by a manufacturing company. Show

students that the cost of the work in process and finished goods inventories consists of

manufacturing costs (product costs).

6. Identify manufacturing overhead as all manufacturing costs other than direct materials and

direct labor. Give various examples of costs classified as manufacturing overhead.

7. Distinguish between direct and indirect manufacturing costs; explain why manufacturing

overhead is an indirect cost.

8. Explain the purpose, content, and format of a schedule of cost of finished goods

manufactured. Illustrate the preparation of this statement, and explain its relationship to the

Work in Process Inventory account and to the income statement.

9. Explain how the total cost of finished goods manufactured is used to determine unit cost.

Explain the importance of knowing unit cost both to various managerial decisions and to the

preparation of financial statements.

Chapter 16—Management Accounting: A Business Partner

16-4 Instructor’s Resource Manual

General Comments

We cannot overstate the importance of students thoroughly comprehending the flow of

product costs through the perpetual inventory accounts. This concept is the foundation of the

following chapter. For this reason, we review in class the illustration from the chapter, at least one

“flow of costs” homework problem, and often the chapter Demonstration Problem as well.

In our discussion of the flow of costs, we have deliberately omitted transfers of the costs

of indirect materials and indirect labor from the Materials Inventory and Direct Labor accounts

into the Manufacturing Overhead account. We consider these cost flows to be an unnecessary

refinement in an introductory-level discussion. We have found that omitting these “special

treatment” items helps students to more quickly grasp the basic flow of manufacturing costs

through a perpetual inventory system.

We especially like Problems 3 and 4 as means of illustrating the “flow” of manufacturing

costs. These problems may either be assigned as homework or used as an in-class exercise or quiz.

Chapter 16—Management Accounting: A Business Partner

Financial and Managerial Accounting, 18e 16-5

Supplemental Exercises

Group Exercise

You are the chief executive officer of a multinational corporation that operates wholly

owned subsidiaries in several countries. One of the company’s manufacturing plants is located in

Utopia. Utopia provides a corporate income tax break related to the amount of Utopian labor

employed. Specifically, corporate income taxes are reduced by the company’s ratio of labor costs

of Utopian citizens to total manufacturing costs in Utopia. Discuss how management will

appropriately classify costs into the categories of direct material, direct labor, and manufacturing

overhead. Be sure to justify the approach for each cost classification.

Internet Exercise

Visit the website of a manufacturing company of your choice. Access a recent annual report

and review management’s letter to the shareholders. This is sometimes called the “Chairman’s

Message” and will generally begin with “Dear Shareholders.” In the letter find and report on

examples of decision making supported by information from the company’s management

accounting system.

Chapter 16—Management Accounting: A Business Partner

16-6 Instructor’s Resource Manual

CHAPTER 16 NAME #

10-MINUTE QUIZ A SECTION

The manufacturing cost accounts of Varsity Manufacturing Co. provide the following information for the

year ended December 31, 2019:

Direct materials used ………………………………………………………………………… $500,000

Direct materials purchased ……………………………………………………………………… $520,000

Direct labor cost assigned to production …………………………………………………… $130,000

Wages paid to direct workers ………………………………………………………………….. $120,000

Manufacturing overhead costs applied to production …………………………………. $190,000

Cost of finished goods manufactured……………………………………………………….. $850,000

Inventories at the beginning and end of the year were as follows:

Dec. 31 Jan. 1

Materials …………………………………………………………….. $65,000 $ ?

Work in Process …………………………………………………… $15,000 $10,000

Finished Goods ……………………………………………………. $35,000 $65,000

Answer the following questions. If you select answer d, indicate the correct amount.

1. Refer to the above data. The total amount of inventory that should appear in the company’s balance

sheet at December 31, 2019 is:

a $115,000.

b $860,000.

c $85,000.

d Some other amount. $____________

2. Refer to the above data. The total manufacturing costs charged to the Work in Process Inventory

account during 2019 amounted to:

a $850,000.

b $820,000.

c $810,000.

d Some other amount. $____________

3. Refer to the above data. The total manufacturing costs deducted from revenue in 2019: amounted to:

a $890,000.

b $880,000.

c $845,000.

d Some other amount. $____________

4. Refer to the above data. The balance in the Materials Inventory account at the beginning of 2019: was:

a $65,000.

b $85,000.

c $45,000.

d Some other amount. $____________

Chapter 16—Management Accounting: A Business Partner

Financial and Managerial Accounting, 18e 16-7

CHAPTER 16 NAME #

10-MINUTE QUIZ B SECTION

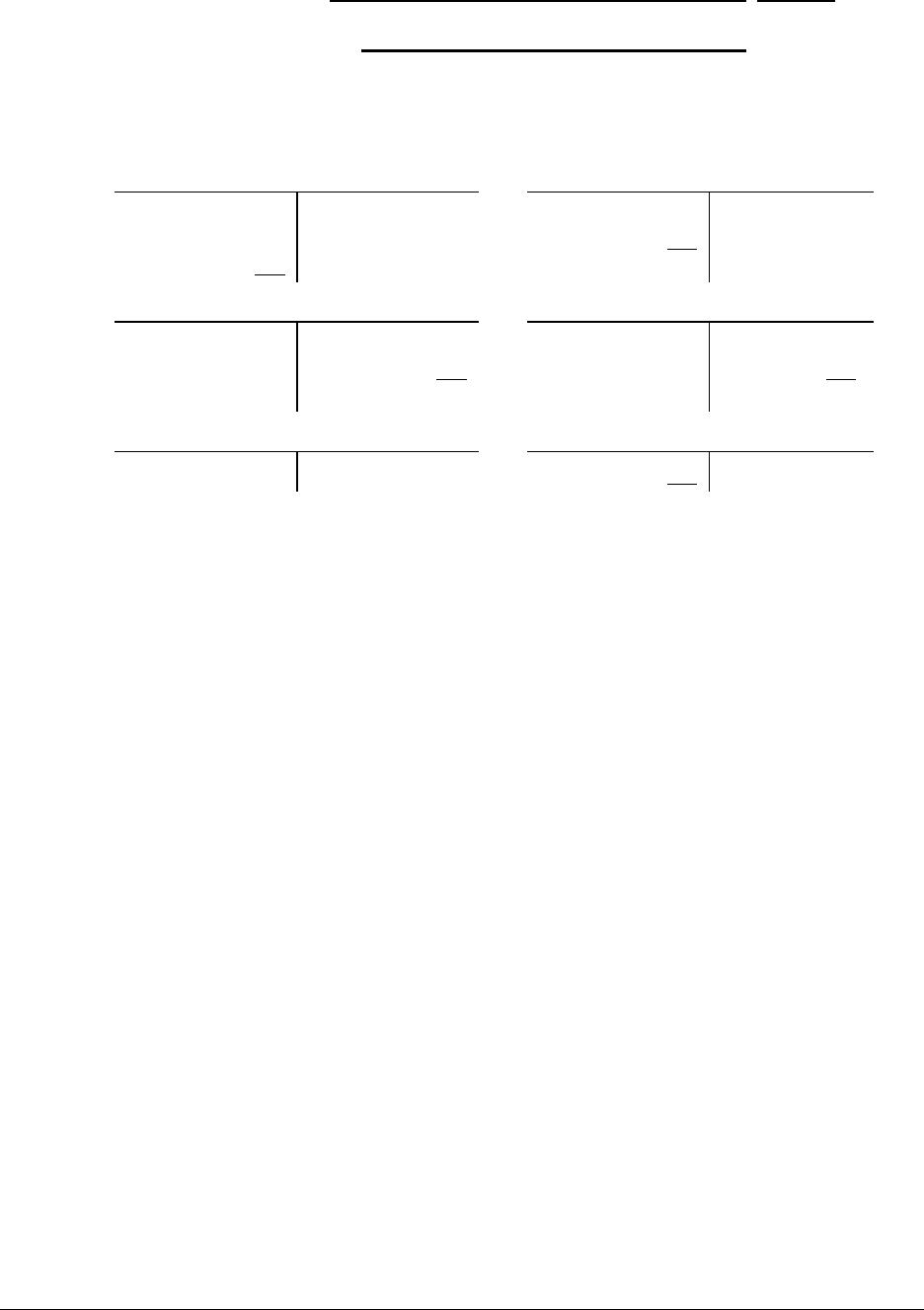

The “flow” of manufacturing costs through the ledger of Able Mfg. Co. during April is summarized in the

following T accounts. Certain amounts have been omitted and are represented by question marks.

Materials Inventory

Work in Process Inventory

Beg. Bal. 32,000

35,000

End. Bal. ?

33,000

Beg. Bal. 3,000

?

End. Bal. 5,000

72,000

Direct Labor

Finished Goods Inventory

13,000

Beg. Bal. 0

?

End. Bal. 1,000

Beg. Bal. 47,000

72,000

End. Bal. 39,000

?

Manufacturing Overhead

Cost of Goods Sold

27,000

27,000

?

Answer the following questions. If you select answer d, indicate the correct amount.

1. Refer to the above data. The total amount of inventory that should appear in the company’s balance

sheet at April 30 is:

a $39,000. c $73,000.

b $82,000. d Some other amount. $____________

2. Refer to the above data. The amount of wages paid to direct workers during April amounted to:

a $14,000. c $13,000.

b $12,000. d Some other amount. $____________

3. Refer to the above data. The total manufacturing costs charged to production during April were:

a $74,000. c $76,000.

b $72,000. d Some other amount. $____________

4. Refer to the above data. The cost of finished goods manufactured in April amounted to:

a $72,000. c $47,000.

b $80,000. d Some other amount. $____________

5. Refer to the above data. The cost of goods sold in April amounted to:

a $72,000. c $39,000.

b $80,000. d Some other amount. $____________

Chapter 16—Management Accounting: A Business Partner

16-8 Instructor’s Resource Manual

CHAPTER 16 NAME #

10-MINUTE QUIZ C SECTION

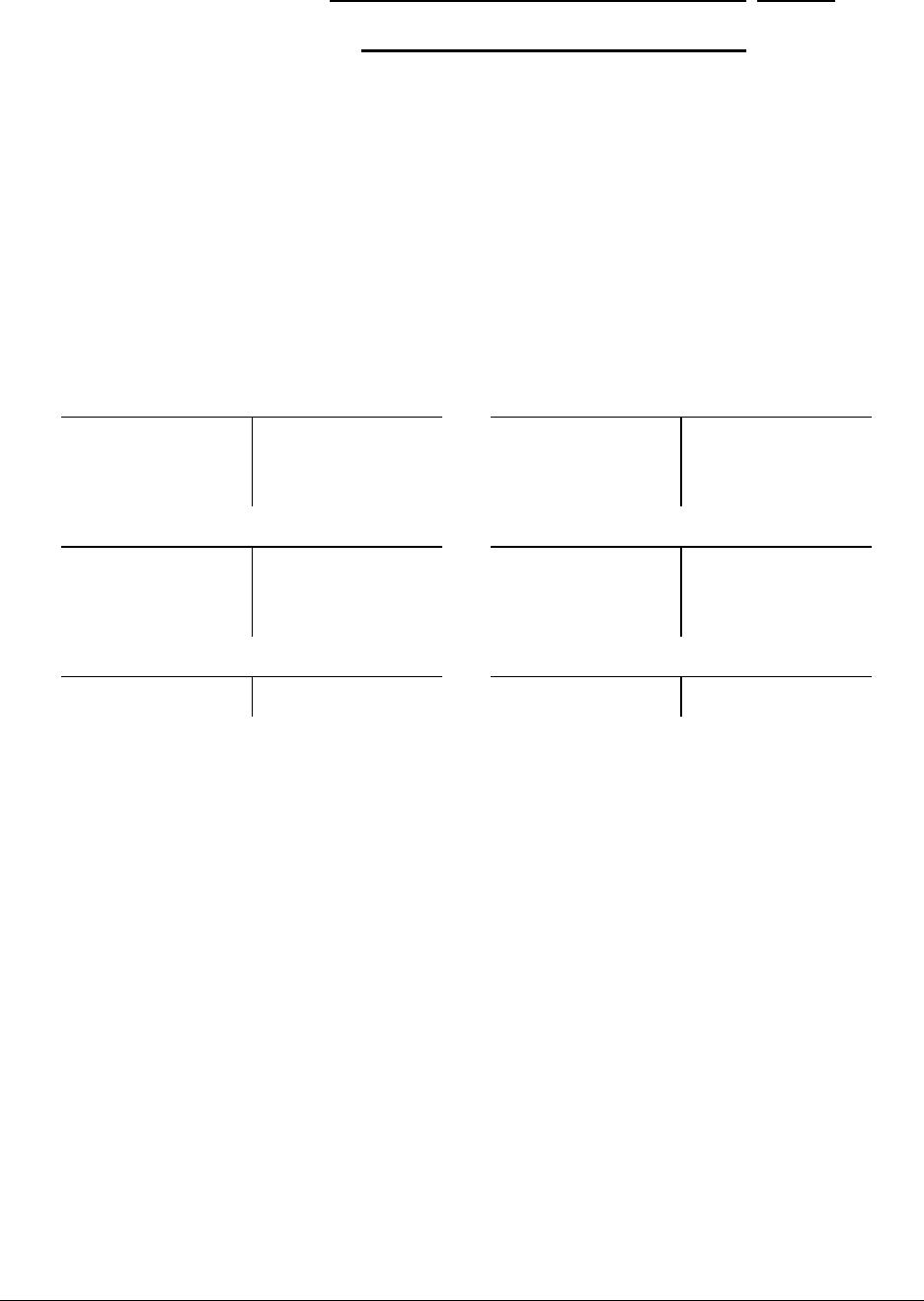

You are to summarize the “flow” of manufacturing costs through the ledger accounts of Berman Mfg. Co.

for the month of June. Complete the following T accounts by entering summary amounts for the month in

each of the blank spaces provided (lettered a through j). In addition to the amounts already shown in the T

accounts, the following information is available:

Direct materials used during June …………………………..………………………………………… $51,000

Wages paid during June to direct labor workers …………………………………………………. $22,000

Cost of finished goods manufactured ………………………………………………………………… $98,000

Total manufacturing costs charged to production (in the Work in

Process account, record this entire amount as

one entry) ………………………………………………………………………………………………………. $94,000

Materials Inventory

Work in Process Inventory

Beg. Bal. 43,000

a

End. Bal. 50,000

b

Beg. Bal. 14,000

f

End. Bal. 10,000

g

Direct Labor

Finished Goods Inventory

c

Beg. Bal. 0

d

End. Bal. 10,000

Beg. Bal. 58,000

h

End. Bal. 52,000

i

Manufacturing Overhead

Cost of Goods Sold

11,000

e

j

Chapter 16—Management Accounting: A Business Partner

Financial and Managerial Accounting, 18e 16-9

CHAPTER 16 NAME #

10-MINUTE QUIZ D SECTION

Information about the manufacturing costs and inventories of Tracy Mfg. Co. in 2011 is shown below:

Manufacturing Costs:

Direct materials used…………………………………………………………………………………………… $655,000

Direct labor charged to production ……………………………………………………………………….. $330,000

Manufacturing overhead ……………………………………………………………………………………… $455,000

Dec. 31, 2019 Jan. 1, 2019

Materials ………………………………………………………………………….. $65,000 $50,000

Work in process ……………………………………………………….………. $27,000 $32,000

Finished goods …………………………………………………………………. $75,000 $83,000

a Using the appropriate data, prepare a Schedule of Cost of Finished Goods Manufactured for the year ended

December 31, 2019

TRACY MFG. CO.

Schedule of Cost of Finished Goods Manufactured

For the Year Ended December 31, 2019

b Compute the cost of goods sold in 2011: $__________

Chapter 16—Management Accounting: A Business Partner

16–10 Instructor’s Resource Manual

SOLUTIONS TO CHAPTER 16 10–MINUTE QUIZZES

QUIZ A

1 A

QUIZ B

QUIZ C

Chapter 16—Management Accounting: A Business Partner

Financial and Managerial Accounting, 18e 16–11

QUIZ D

a

TRACY MFG. CO.

Schedule of Cost of Finished Goods Manufactured

For the Year Ended December 31, 2019

Work in process inventory, Jan. 1, 2019 ……………………………………………….. $ 32,000

Manufacturing costs assigned to production:

Chapter 16—Management Accounting: A Business Partner

16–12 Instructor’s Resource Manual

Assignment Guide to Chapter 16

Brief

Exercises

Exercises

Problems

Cases

Net

Item number

1 – 10

1 – 15

1

2

3

4

5

6

7

8

1

2

4

3

Time estimate (in minutes)

< 15

< 15

20

15

20

20

35

35

25

40

40

40

45

15

Difficulty rating

E

E

E

E

E

E

M

S

M

S

S

S

M

E

Learning Objectives:

1, 7, 8, 11

1. Explain the three principles

guiding the design of

management accounting

systems.

2. Describe the three basic types

of manufacturing costs.

5

1, 2, 13, 14

3. Distinguish between product

costs and period costs.

1, 3, 9, 10

13, 15

manufactured.

5, 9, 10, 12