SOLUTIONS TO PROBLEMS

PROBLEM 16-1A

(a) 2017

Jan. 1 Debt Investments ……………………………. 2,000,000

Cash ……………………………………….. 2,000,000

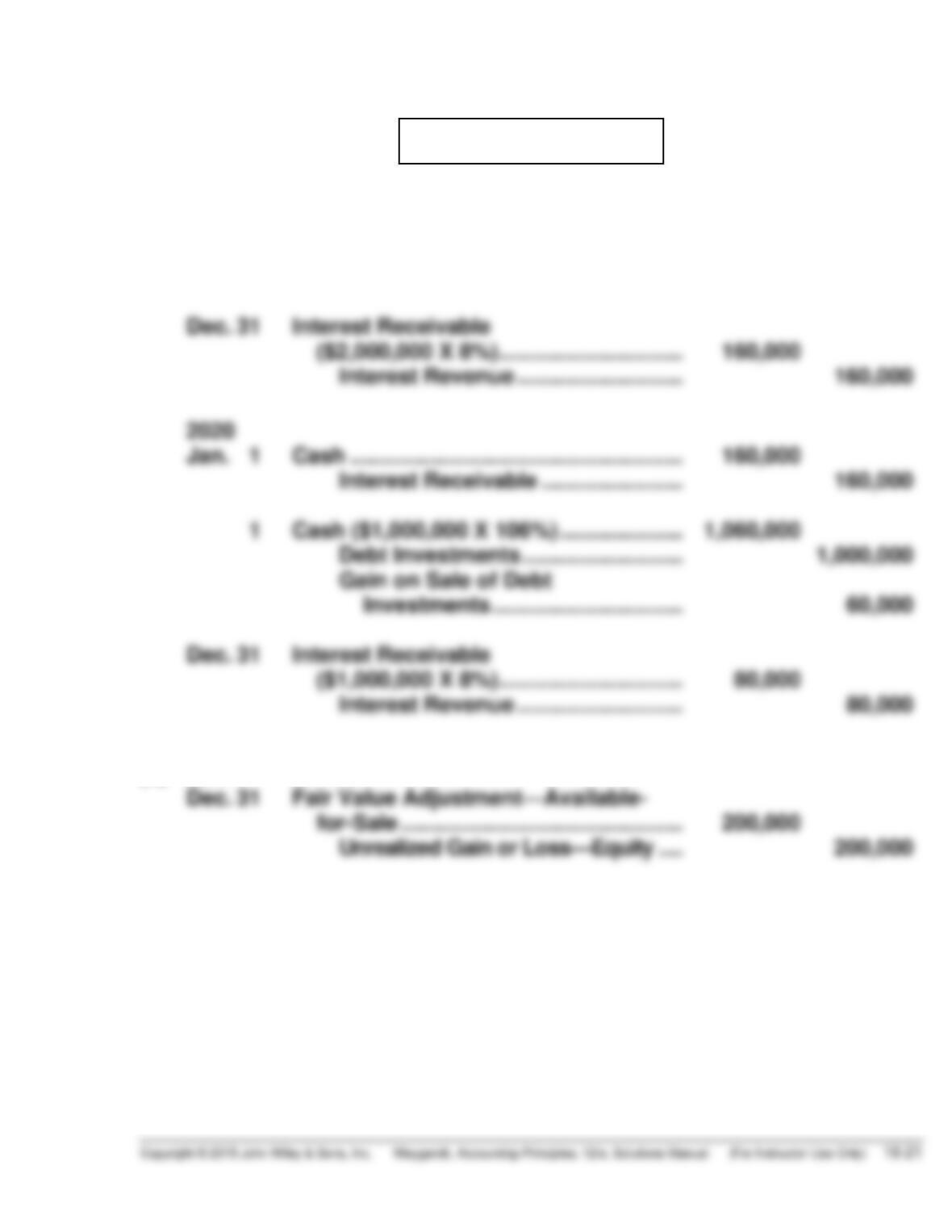

Dec. 31 Interest Receivable

($2,000,000 X 8%) ………………………… 160,000

Interest Revenue ……………………… 160,000

Dec. 31 Interest Receivable

($1,000,000 X 8%) ………………………… 80,000

Interest Revenue ……………………… 80,000

(b) 2017

PROBLEM 16-1A (Continued)

(c) Balance Sheet

Current assets

Interest receivable ………………………………………………. $ 160,000

Investments

PROBLEM 16-2A

(a) Feb. 1 Stock Investments ……………………………… 32,400

Cash …………………………………………… 32,400

Mar. 1 Stock Investments ……………………………… 20,000

Cash …………………………………………… 20,000

Apr. 1 Debt Investments ……………………………….. 50,000

Cash …………………………………………… 50,000

Sept. 1 Cash ($1 X 800) ………………………………….. 800

Dividend Revenue ……………………….. 800

Oct. 1 Cash ($50,000 X 7% X 1/2) …………………… 1,750

Interest Revenue …………………………. 1,750

Stock Investments

Debt Investments

Feb. 1 32,400

Mar. 1 20,000

Aug. 1 10,800

Apr. 1 50,000

Oct. 1 50,000

Dec. 31 Bal. 0

PROBLEM 16-2A (Continued)

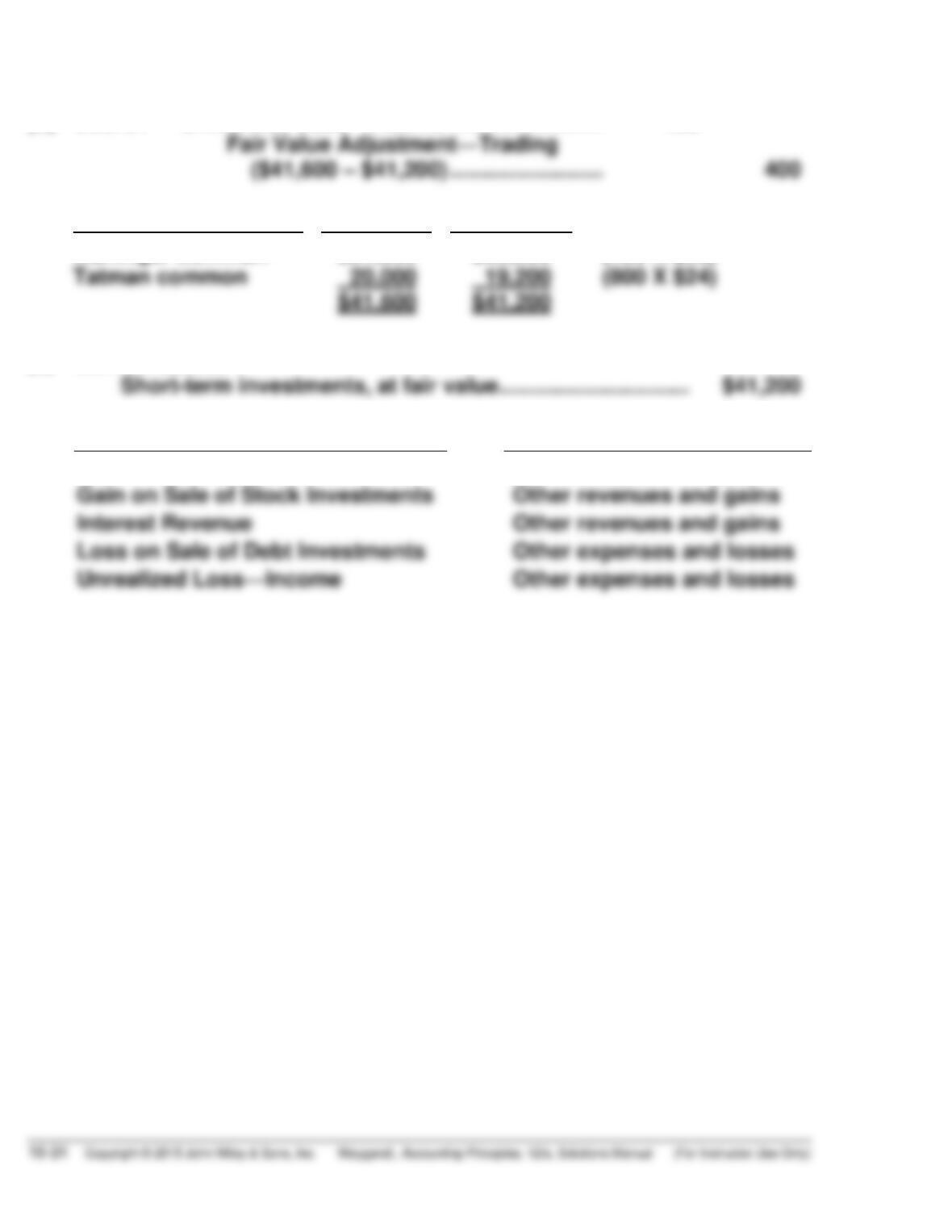

(b) Dec. 31 Unrealized Loss—Income ……………………. 400

Security

Cost

Fair Value

Muninger common

$21,600

$22,000

(400 X $55)

(c) Current assets

Short-term investments, at fair value…………………………. $41,200

(d)

Income Statement Account

Category

Dividend Revenue

Other revenues and gains

Gain on Sale of Stock Investments

Other revenues and gains

Interest Revenue

Other revenues and gains

Loss on Sale of Debt Investments

Other expenses and losses

Other expenses and losses

PROBLEM 16-3A

(a) 2018

Aug. 1 Cash (2,000 X $.50) …………………………….. 1,000

Dividend Revenue ……………………….. 1,000

Nov. 1 Cash (1,500 X $1) ……………………………….. 1,500

Dividend Revenue ……………………….. 1,500

Stock Investments

2018

Jan. 1 Balance 135,000

2018

Sept. 1 13,500

Oct. 1 24,000

PROBLEM 16-3A (Continued)

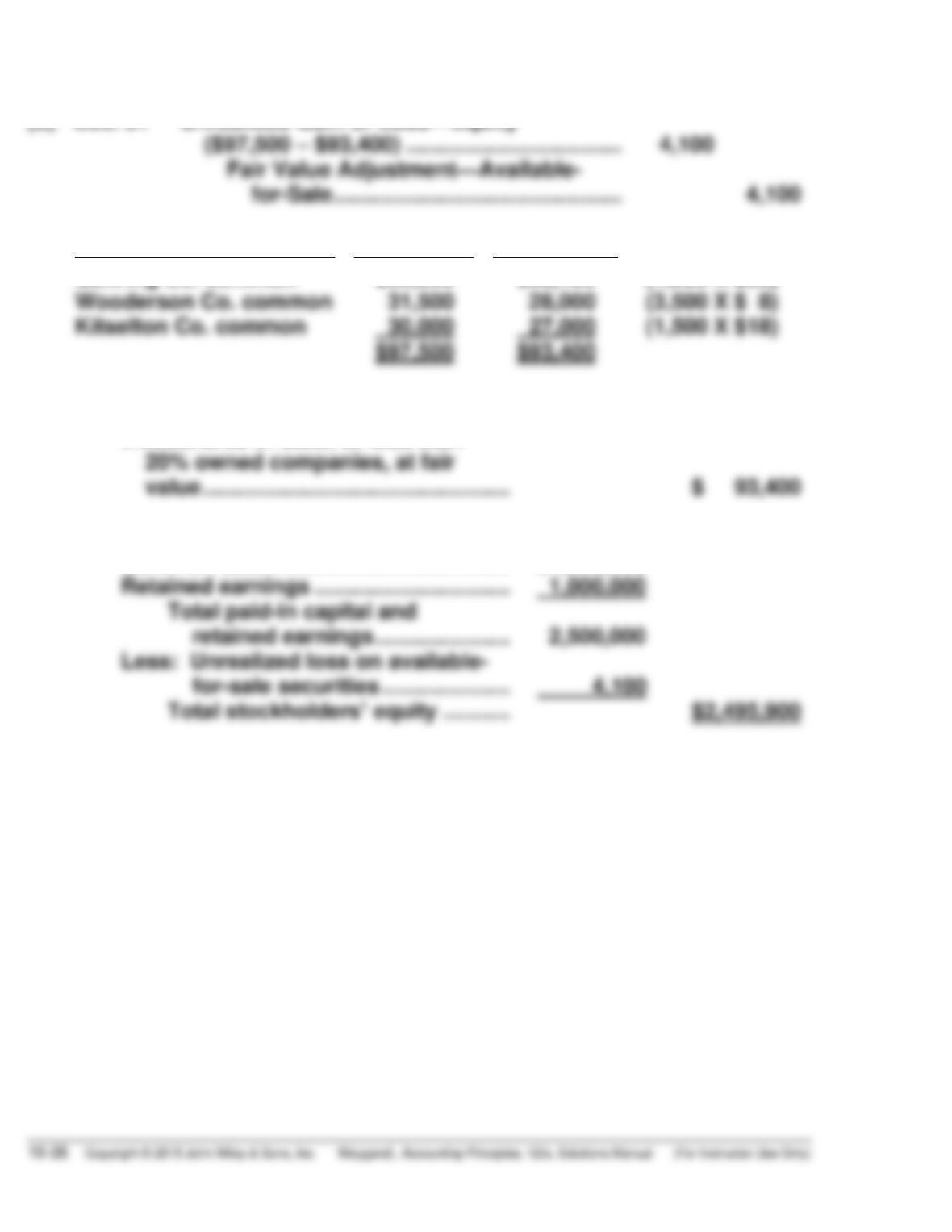

(b) Dec. 31 Unrealized Gain or Loss—Equity

($97,500 – $93,400) …………………………….. 4,100

Security

Cost

Fair Value

Gehring Co. common

Wooderson Co. common

$36,000

31,500

$38,400

28,000

(1,200 X $32)

(3,500 X $ 8)

(c) Investments

Investments in stock of less than

20% owned companies, at fair

value ………………………………………….. $ 93,400

Stockholders’ equity

Common stock ………………………………. $1,500,000)

PROBLEM 16-4A

(a) Jan. 1 Stock Investments ………………………….. 800,000

Cash ……………………………………….. 800,000

Mar. 15 Cash ……………………………………………… 9,000

Dividend Revenue

(30,000 X $.30) ……………………… 9,000

(b) Jan. 1 Stock Investments ………………………….. 800,000

Cash ……………………………………….. 800,000

Mar. 15 Cash ……………………………………………… 9,000

Stock Investments …………………… 9,000

PROBLEM 16-4A (Continued)

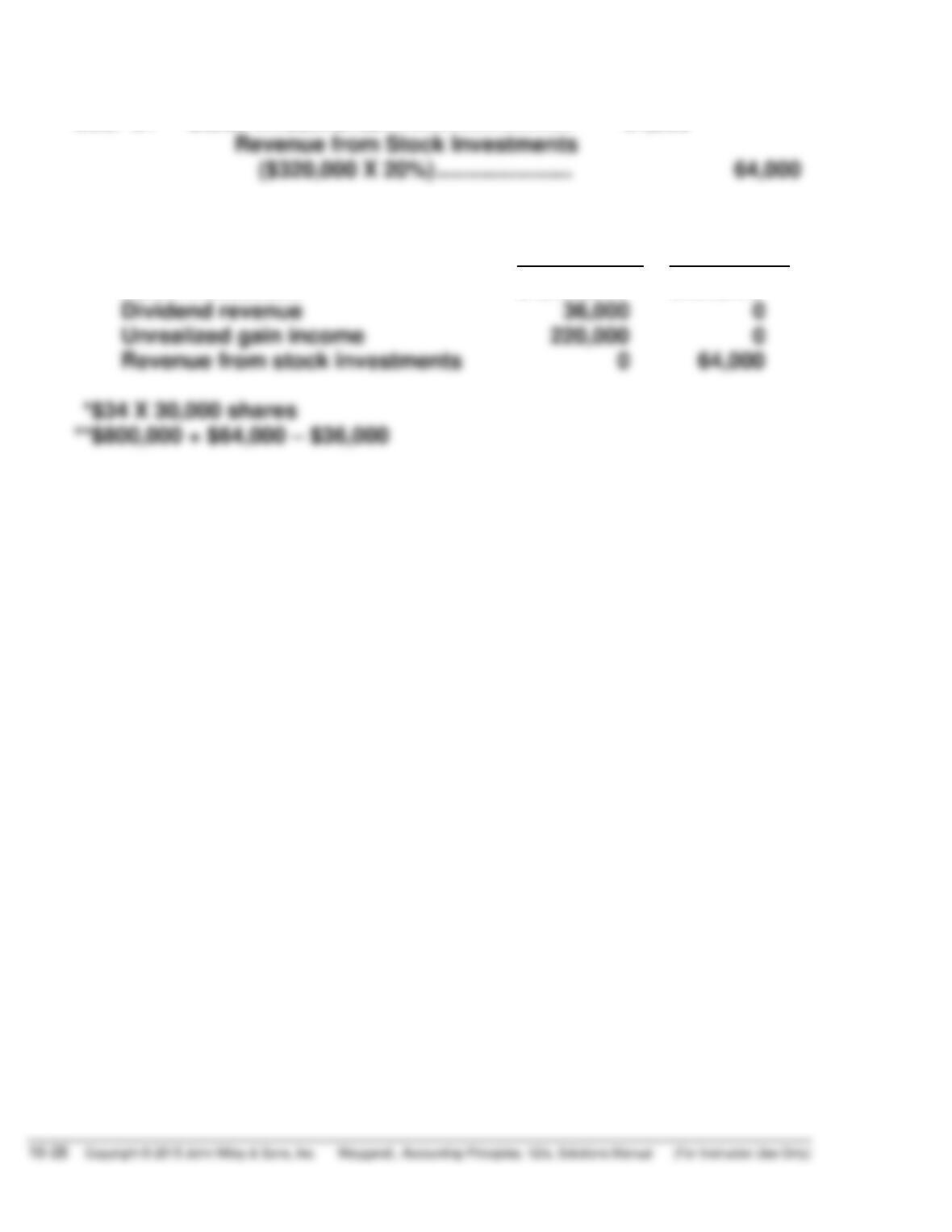

Dec. 31 Stock Investments …………………………. 64,000

(c)

Cost

Method

Equity

Method

Stock Investment

Dividend revenue

$1,020,000*

36,000

$828,000**

0

PROBLEM 16-5A

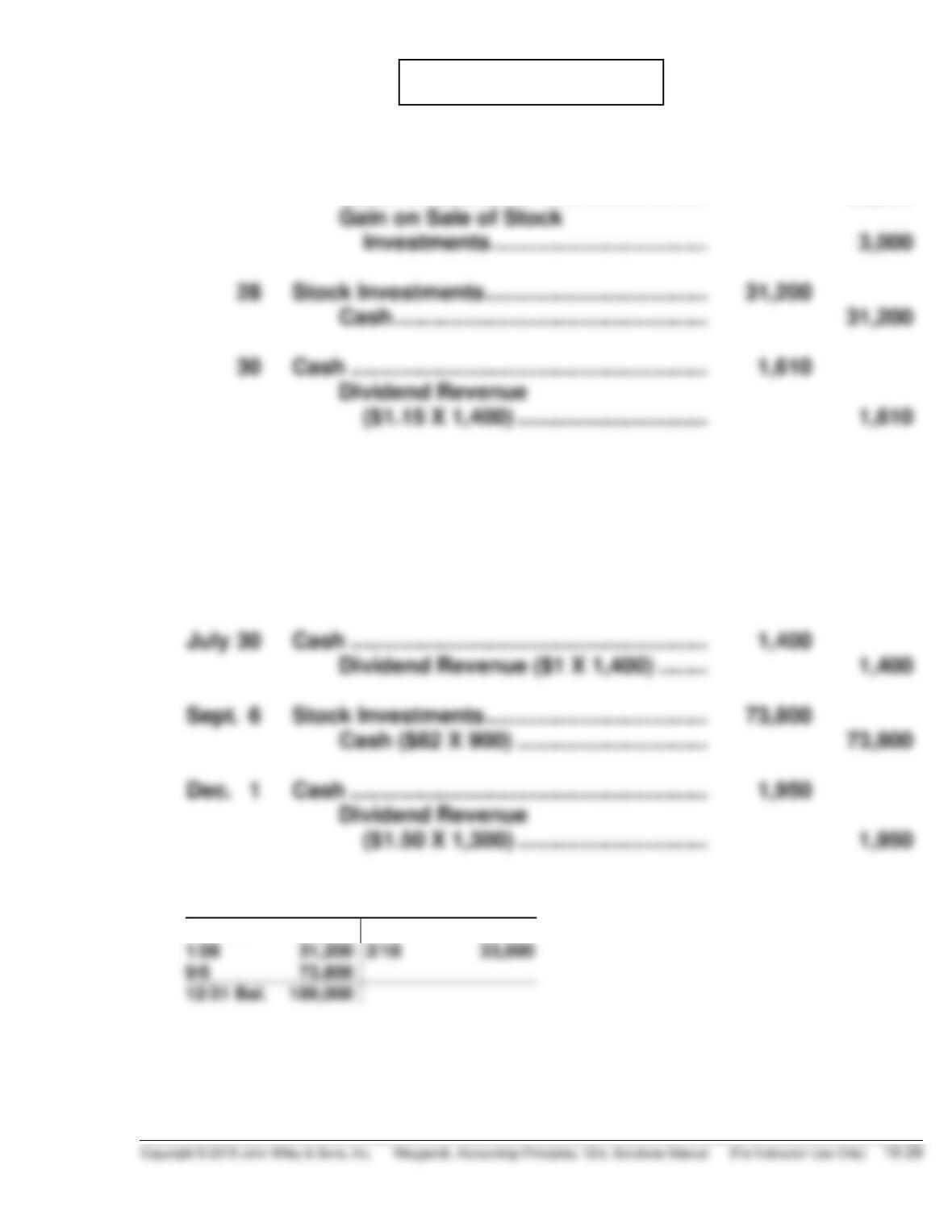

(a) Jan. 20 Cash …………………………………………………. 55,000

Stock Investments ………………………. 52,000

Gain on Sale of Stock

Investments …………………………….. 3,000

Feb. 8 Cash …………………………………………………. 480

Dividend Revenue ($.40 X 1,200) ….. 480

18 Cash ($27 X 1,200) ……………………………… 32,400

Loss on Sale of Stock Investments ……… 1,200

Stock Investments ………………………. 33,600

(b)

Stock Investments

1/1 Bal. 169,600

1/20 52,000

1/28 31,200

2/18 33,600

9/6 73,800

12/31 Bal. 189,000

PROBLEM 16-5A (Continued)

(c) Dec. 31 Unrealized Gain or Loss—Equity ……………. 5,800

Fair Value Adjustment—Available-

(d) Investments

Investments in stock of less than 20% owned

companies, at fair value ……………………………………. $183,200

PROBLEM 16-6A

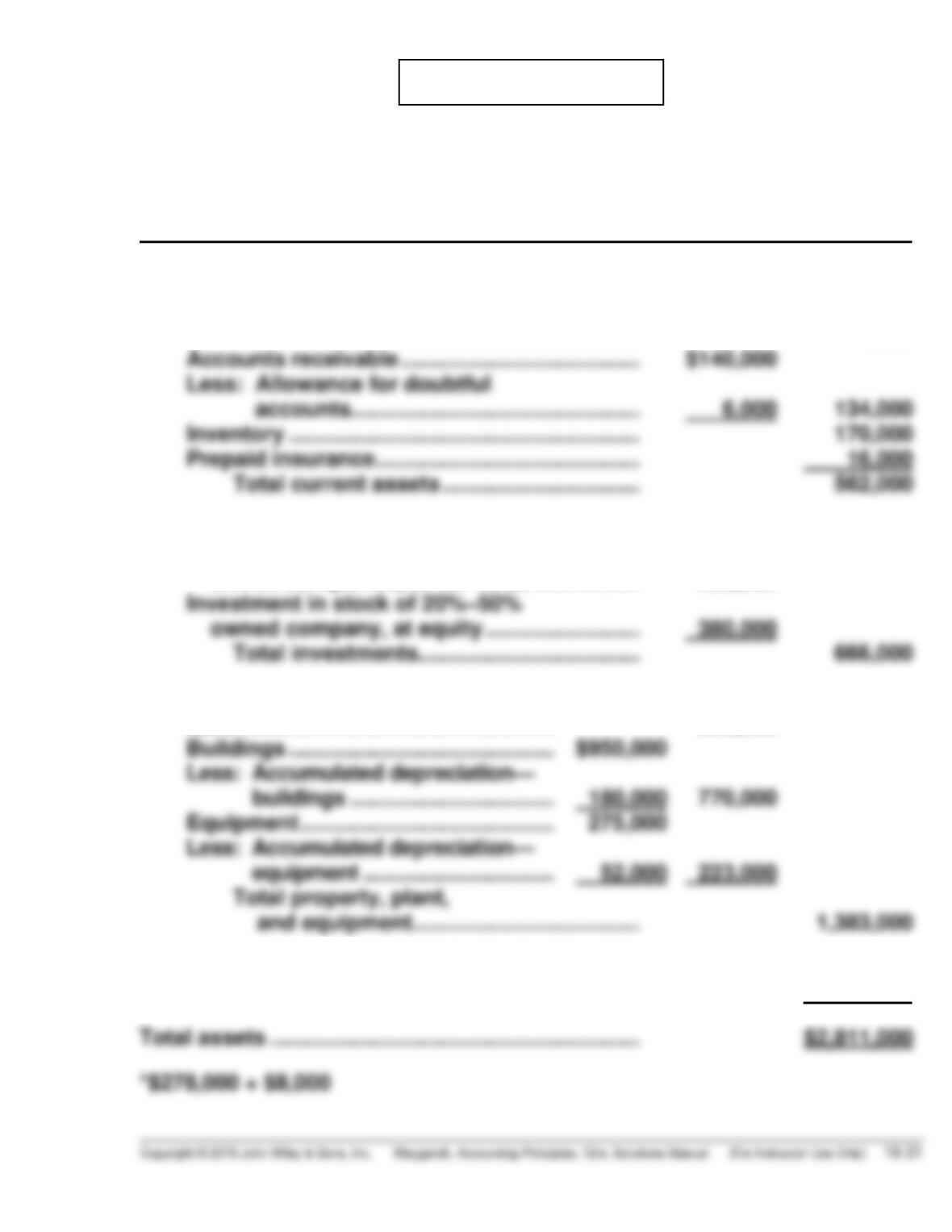

NIETO CORPORATION

Balance Sheet

December 31, 2017

Assets

Current assets

Cash ……………………………………………………….. $ 62,000

Short-term investments, at fair value ………… 180,000

Accounts receivable ………………………………… $140,000

Investments

Investments in stock of less than 20% of

owned companies, at fair value …………….. 286,000*

Property, plant, and equipment

Land …………………………………………… 390,000

Buildings ……………………………………. $950,000

Intangible assets

Goodwill …………………………………………………. 200,000

Total assets …………………………………………………… $2,811,000

PROBLEM 16-6A (Continued)

NIETO CORPORATION

Balance Sheet (Continued)

December 31, 2017

Liabilities and Stockholders’ Equity

Current liabilities

Notes payable ………………………………………….. $ 70,000

Accounts payable …………………………………….. 260,000

Long-term liabilities

Bonds payable, 10%, due 2025 ………………….. $ 500,000

Stockholders’ equity

Paid-in capital

Common stock, $10 par value,

500,000 shares authorized,

Total paid-in capital and retained

earnings ………………………………………… 1,733,000

COMPREHENSIVE PROBLEM: CHAPTERS 12 TO 16

Part I

(a) To: Debby Kauffman, Jamie Hiatt, and Ella Rincon

From: Joe Student

Date: 5/26/2016

Re: Analysis of Partnership vs. Corporate Form of Business

Organization

I have examined your situation regarding the establishment of your business.

Before discussing my recommendations, I would like to briefly review

the advantages and disadvantages of partnerships and corporations.

The primary advantages of a partnership over a corporation are:

1. Partnerships are more easily formed than corporations. Partnerships

can be formed simply by the voluntary agreement of two or more

individuals. Forming a corporation requires preparing and filing docu–

ments with governmental agencies, paying incorporation fees, etc.

2. Income from a partnership is subject to less tax than income from

a corporation. Even though partnerships are required to file information

3. Partnerships have more flexibility in decision making. The decision-

making process used in a partnership is determined by the partners,

whereas some decisions required in corporations must follow formal

procedures described in the bylaws of the corporation.

COMPREHENSIVE PROBLEM (Continued)

The primary advantages of a corporation over a partnership are:

1. Mutual agency does not exist in a corporation. This means that the

owners of a corporation (stockholders) do not have the power to bind

the corporation beyond their authority. For example, a stockholder

2. The owners of a corporation have limited liability. When the

corporation’s assets are not sufficient to pay creditors’ claims, the

personal assets of the stockholders are protected from the

corporation’s creditors. In a partnership, once the assets of the

3. The life of a corporation is unlimited. When ownership changes occur

(e.g., stockholders buy or sell stock), the corporation continues to

exist as a legal entity. When ownership changes occur in a partner-

After examining your situation, I believe that you would be wise to

choose the corporate form of business organization. There are two

reasons for this recommendation. The first reason is that the venture

you are about to undertake will require significant capital and, generally,

COMPREHENSIVE PROBLEM (Continued)

Part II

(b)

Equity financing option:

Positives

Negatives

No fixed interest payments

required

Control of the corporation is lost

Difficulty of finding an interested

investor

Earnings per share are lower

Debt financing option:

Positives

Negatives

Equity Financing

Debt Financing

Income before interest and taxes

$300,000

$300,000

Interest expense

—

126,000

Income before taxes

300,000

174,000

Tax expense

96,000

55,680

$204,000

$118,320

Shares outstanding after financing

Earnings per share

Part III

(c) (1) 6/12/16 Cash ……………………………………… 100,000

COMPREHENSIVE PROBLEM (Continued)

7/21/16 Cash……………………………………….. 900,000

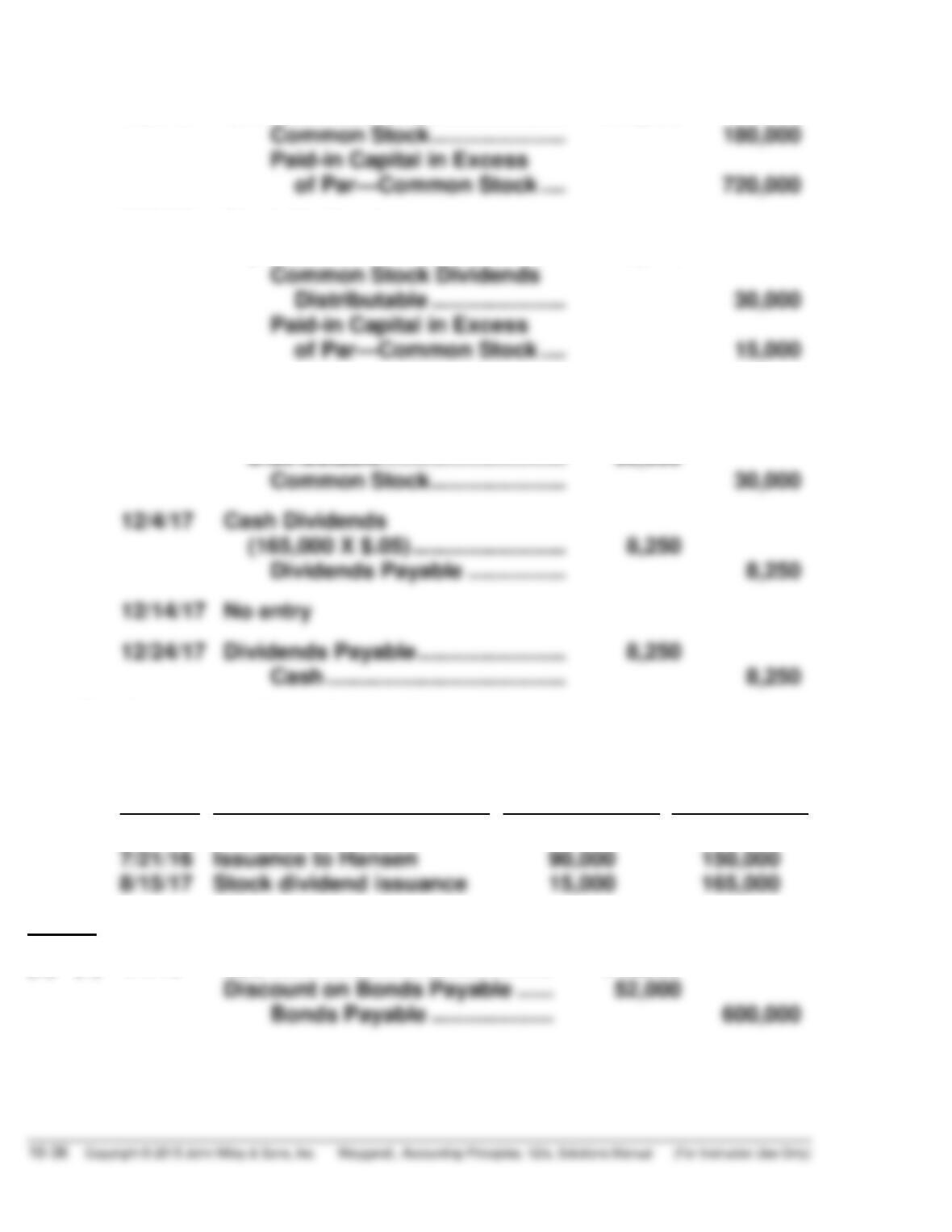

7/27/17 Stock Dividends

(150,000 X .10 X $3) ………………. 45,000

7/31/17 No entry

8/15/17 Common Stock Dividends

Distributable ………………………… 30,000

Common Stock …………………. 30,000

(2) Shares Issued and Outstanding

Date

Event

Number of

Shares Issued

Total Shares

Issued and

Outstanding

6/12/16

Issuance to Incorporators

60,000

60,000

Part IV

(d) (1) 1/1/18 Cash……………………………………… 548,000