Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

16–19 Ch. 16—Problems

PROBLEM 16-7

(1) b, f

(3) d, b

PROBLEM 16-8

(1) Entries in the Internal Service Fund:

Expenses—Claims and Judgments ................................................ 4,000,000

Cash ......................................................................................... 2,300,000

(2) Entries in General Fund:

Expenditures ................................................................................... 3,200,000

Cash ......................................................................................... 3,200,000

To record premium transferred to insurance internal

service fund.

(3) If the county elects to use a general fund for its self-insurance activity, revenue can be rec-

ognized from other funds up to the amount of actual losses incurred ($4,000,000) or 80% of

PROBLEM 16-9

(1) General Fixed Assets Account Group (6) Private-Purpose Trust

(3) General Long-Term Debt Account Group (8) Agency Fund

(5) General Long-Term Debt Account Group (10) Special Revenue Fund

Ch. 16—Problems 16–20

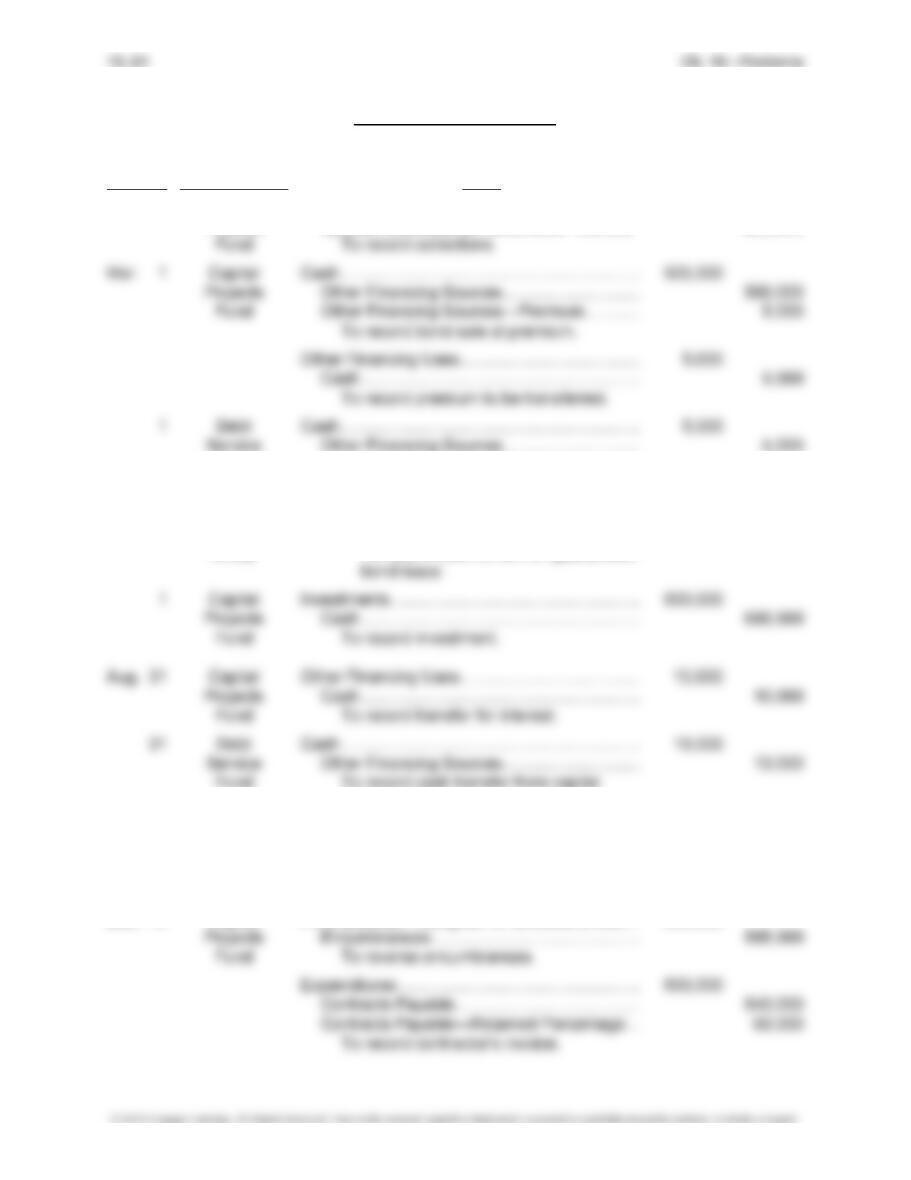

PROBLEM 16-10

Fund or

Date Account Group Entry

Jan. 2 Capital Estimated Revenues ......................................... 350,000

Projects Estimated Other Financing Sources .................. 550,000

Projects Due from General Fund ..................................... 50,000

Fund Revenues ...................................................... 100,000

Other Financing Sources .............................. 50,000

To record amounts receivable.

General Other Financing Uses ........................................ 50,000

Fund Due from General Fund ................................ 50,000

To record amounts received.

General Due to Capital Projects Fund ............................ 50,000

Fund Cash .............................................................. 50,000

To record cash transfer.

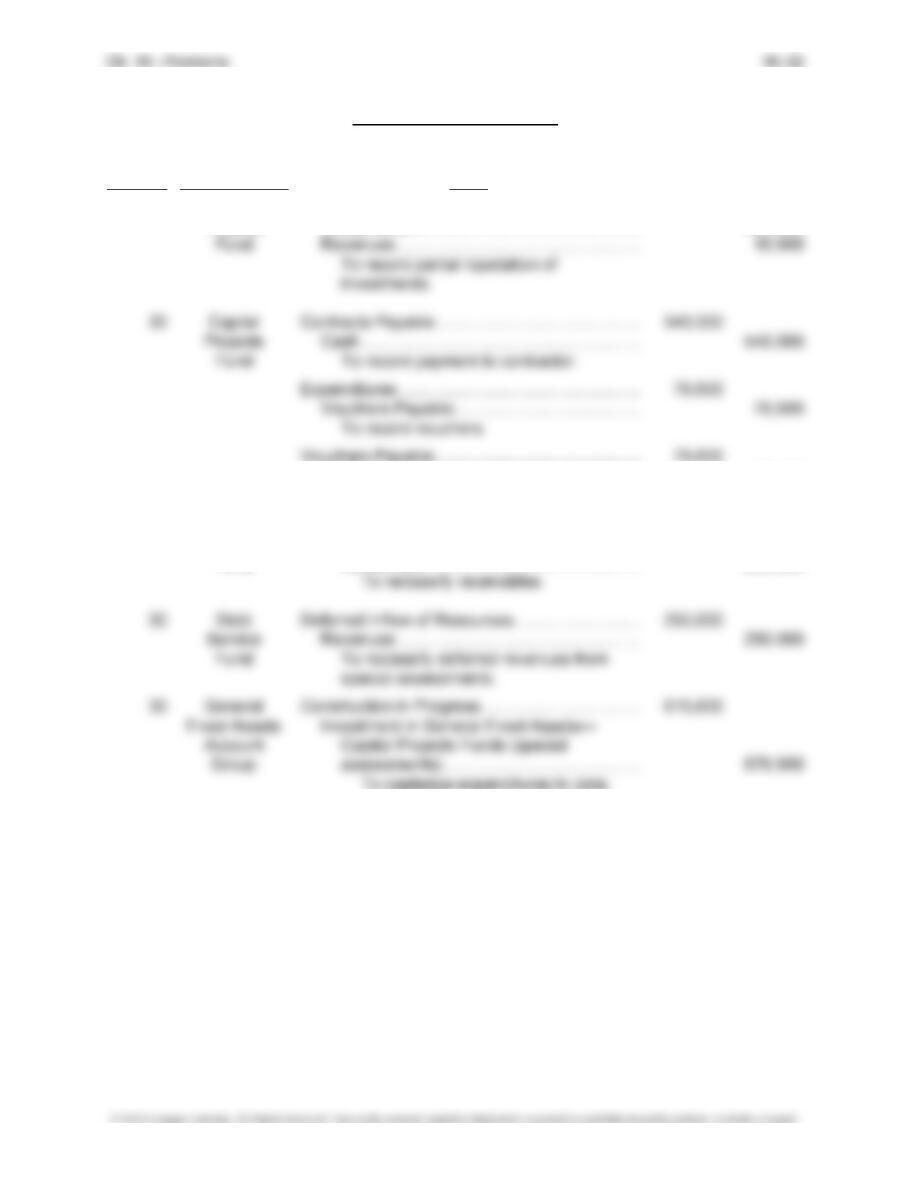

Problem 16-10, Continued

Fund or

Date Account Group Entry

Feb. 1 Capital Cash .................................................................. 250,000

Projects Special Assessments Receivable—Current 250,000

Fund To record premium due.

1 General Amount to Be Provided for Payment of Special

Long-Term Assessment Serial Bonds ............................. 500,000

Debt Account Special Assessment Bonds Payable ........ 500,000

Group To record commitment on guaranteed

projects fund.

Sept. 1 Debt Expenditures ..................................................... 15,000

Service Cash .............................................................. 15,000

Fund To record interest payment.

Dec. 15 Capital Fund Balance—Assigned for Encumbrances .... 595,000

Problem 16-10, Concluded

Fund or

Date Account Group Entry

Dec. 29 Capital Cash .................................................................. 416,600

Projects Investments ................................................... 400,000

Cash .............................................................. 76,600

To record voucher payment.

30 Debt Special Assessments Receivable—Current ...... 250,000

Service Special Assessments Receivable—

Fund Noncurrent ................................................ 250,000

16–23 Ch. 16—Problems

PROBLEM 16-11

City of Boniville Internal Service Fund

Statement of Cash Flows

Cash flows from operating activities:

Collections (for services) from other funds ................................................... $ 6,000

Wages and salaries paid .............................................................................. (3,100)

Purchase of supplies .................................................................................... (1,650)

Net cash provided by operating activities ..................................................... $ 1,250

Cash flows from capital and related financing activities:

Proceeds of revenue bonds ......................................................................... $ 900

Proceeds from sale of capital assets ........................................................... 23

Purchase of capital assets ........................................................................... (900)

Interest paid on long-term debt .................................................................... (150)

Net cash used for capital and related financing activities ............................ $ (127)

Cash flows from investing activities:

Net increase in cash .......................................................................................... $ 781

Cash on hand beginning of year .................................................................. 122

Cash on hand end of year ............................................................................ $ 903

PROBLEM 16-12

(1) (a) Inventory of Materials and Supplies .......................................... 72,000

Vouchers Payable ............................................................... 72,000

To record purchases on account.

Problem 16-12, Concluded

(d) Operating Expenses ................................................................. 40,000

Cash ................................................................................... 40,000

To record payment of utility charge.

(e) Operating Expenses ................................................................. 139,500

Allowance for Depreciation—Building ................................. 6,500

Allowance for Depreciation—Computer Equipment ............ 133,000

To record depreciation.

(g) Cash ......................................................................................... 506,000

Due from General Fund

($140,000 + $392,000 – $136,000)............................... 396,000

Due from Water and Sewer Fund ....................................... 84,000

Due from Special Revenue Fund ($42,000 – $16,000) ...... 26,000

To record collections.

(2) Closing Entries:

Operating Revenues ................................................................. 518,000

Operating Expenses

16–25 Ch. 16—Problems

PROBLEM 16-13

(1) Landfill Expense ............................................................................. 500,000

Landfill Closure and Post-Closure Care Liability ........................ 500,000

(2) Landfill Expense ............................................................................. 555,172

Landfill Closure and Post-Closure Care Liability ...................... 555,172

(3) If the landfill is accounted for in the general fund, then the liability would be recognized in

PROBLEM 16-14

Bedrock City’s Employees’ Retirement System Fund

Statement of Plan Net Position

As of June 30, 2018

Assets

Cash and short-term investments .......................................................... $ 38,000

Receivables:

Employer .......................................................................................... $4,000

Liabilities

Refunds payable .................................................................................... $1,000

Annuities payable ................................................................................... 3,000

Total liabilities................................................................................... $ 4,000

Net position held in trust for pension benefits ........................................ $540,000

Problem 16-14, Concluded

Bedrock City’s Employees’ Retirement System Fund

Statement of Changes in Plan Net Position

For Year Ended June 30, 2018

Additions

Contributions:

Employer ($16,000 + $4,000) .......................................................... $20,000

Plan members .................................................................................. 32,000

Total contributions ...................................................................... $ 52,000

Investment income:

Net appreciation (depreciation) in fair value ..................................... $13,500

Interest and dividend income ($30,000 + $5,000) ............................ 35,000

Net investment income ..................................................................... 48,500

Total additions ............................................................................ $100,500

16–27 Ch. 16—Problems

PROBLEM 16-15

Tilburg County Tilburg County Reed City Newport Township

Accounts Tax Agency Fund General Fund General Fund General Fund

Dr.

Cr. Dr. Cr. Dr. Cr. Dr. Cr.

Taxes Receivable—Current ............................... ............... ................ 3,600,000 ............... 1,800,000 ............... 600,000 ............

To record taxes to be collected.

Cash ................................................................... 1,440,000 ................ ................ ............... ............... ............... ............ ............

Taxes Receivable for Other Funds ............... ............... 1,440,000 ................ ............... ............... ............... ............ ............

To record tax collection.

Due to Other Governmental Units ...................... 1,440,000 ................ ................ ............... ............... ............... ............ ............

Cash .............................................................. ............... 1,440,000 ................ ............... ............... ............... ............ ............

To record cash distribution.

Expenditures ...................................................... ............... ................ ................ ............... 8,640 ............... 2,880 ............

Cash ................................................................... ............... ................ 875,520* ............... 423,360* ............... 141,120* ............

Taxes Receivable—Current .......................... ............... ................ ................ 864,000 ............... 432,000 ............ 144,000

Revenues ...................................................... ............... ................ ................ 11,520 ............... ............... ............ ............

To record cash received by general funds.

*Calculation of cash distribution:

Tilburg County Reed City Newport Township

General Fund

General Fund General Fund

Cash collected ................................................... $1,440,000 $1,440,000 $1,440,000

PROBLEM 16-16

Fund or

Account Group Journal Entry

(1) General Estimated Revenues ............................................. 4,500,000

(2) Special Estimated Revenues ............................................. 264,500

(3) General Taxes Receivable—Current .................................. 3,000,000

(4) Capital Cash ...................................................................... 985,000

Projects Expenditures .......................................................... 5,000

Fund Other Financing Uses ............................................ 10,000

(5) Capital Encumbrances ....................................................... 1,000,000

Problem 16-16, Concluded

Fund or

Account Group Journal Entry

(6) Capital Fund Balance—Assigned for Encumbrances ........ 1,000,000

Projects Encumbrances .................................................. 1,000,000

Fund To liquidate encumbrances.

(7) General Other Financing Uses ............................................ 100,000

Fund Cash .................................................................. 100,000

(8) General Land ....................................................................... 500,000

(9) Special Cash ...................................................................... 205,000

(10) Special Expenditures .......................................................... 410,000

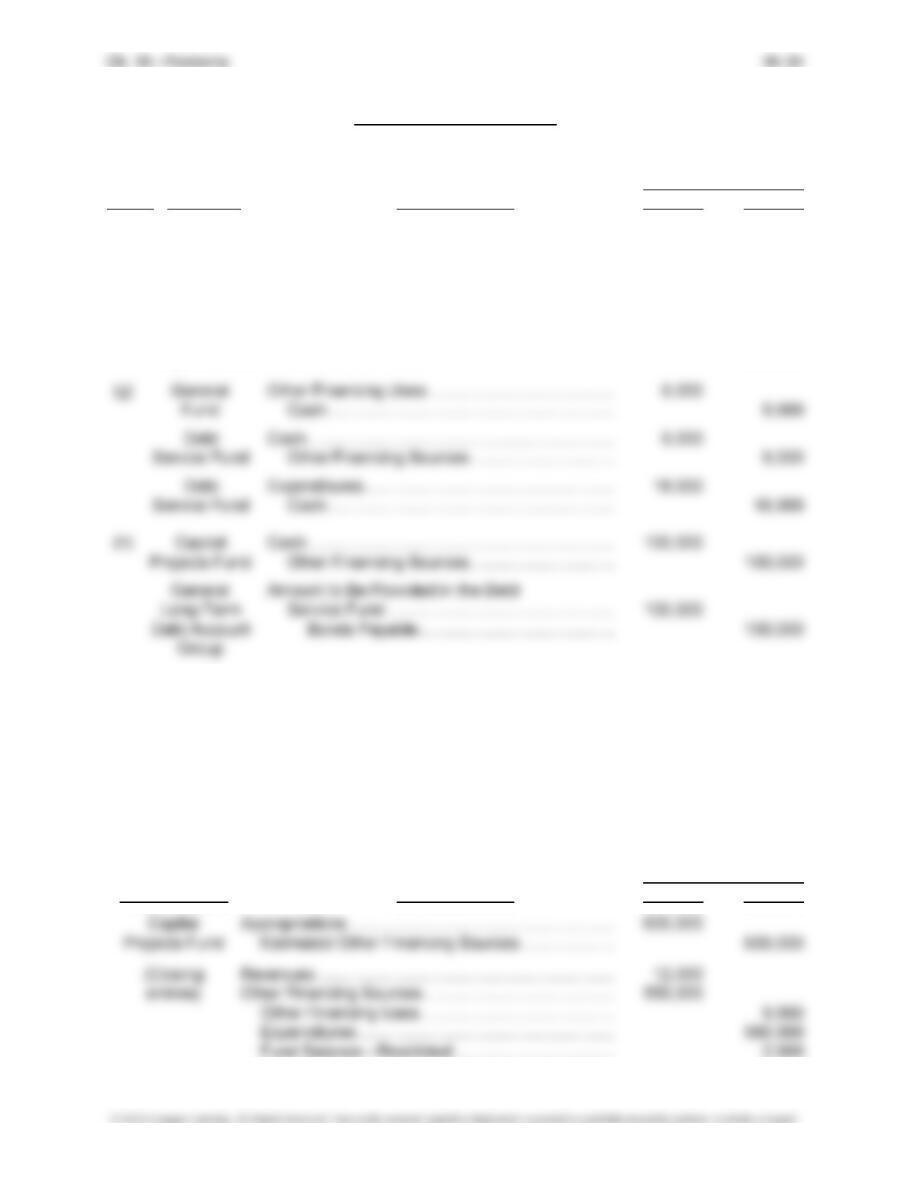

PROBLEM 16-17

Village of Fay

Transactions for Fiscal Year Ended June 30, 2019

Trans- Fund or

action Account Account Title Amount

No. Group and Explanation Debit Credit

(1) General Estimated Revenues ........................................... 400,000

(2) General Taxes Receivable—Current ................................ 390,000

Fund Allowance for Uncollectible Current

Taxes ......................................................... 7,800

Revenues ....................................................... 382,200

(5) Capital Estimated Other Financing Sources ................... 3,000

Projects Estimated Revenues ........................................... 72,000

16–31 Ch. 16—Problems

Problem 16-17, Continued

Trans- Fund or

action Account Account Title Amount

No. Group and Explanation Debit Credit

(6b) Capital Cash ................................................................... 75,000

Projects Special Assessments Receivable .................. 72,000

Fund Due from General Fund .................................. 3,000

(6c) General Other Financing Uses ......................................... 3,000

Fund Due to Capital Projects Fund ......................... 3,000

(7c) General Improvements Other than Buildings ................... 75,000

Fixed Assets Investments in General Fixed Assets—

Account Capital Projects Fund ................................ 75,000

Group To record improvements.

(8) Internal Inventory ............................................................. 1,900

Service Cash or Vouchers Payable............................. 1,900

Fund To record purchase of supplies.

Problem 16-17, Concluded

Trans- Fund or

action Account Account Title Amount

No. Group and Explanation Debit Credit

(10a) Capital Cash ................................................................... 500,000

Projects Other Financing Sources................................ 500,000

Fund To record issuance of bonds.

(10b) General Amount to Be Provided for Payment

Long-Term of Bonds ......................................................... 500,000

Debt Account General Obligation Bonds Payable ............ 500,000

Group To record liability.

PROBLEM 16-18

(1) $104,500 (6) $104,500

(2) $30,000 (7) $386,000 ($364,000 + $22,000)

(4) $236,000 (9) $181,000

16–33 Ch. 16—Problems

PROBLEM 16-19

(1) N (9) Y (16) $5,600,000

(3) Y (11) Y (18) $1,000,000

(6) N (14) N (21) $800,000

(7) N (15) Y (22) $2,032,000 ($900,000 + $52,000 + $1,080,000)

PROBLEM 16-20

(1)

Trans- Fund or

action Account Account Title Amount

No. Group and Explanation Debit Credit

(a) Capital Estimated Other Financing Sources ................... 600,000

Projects Fund Appropriations ................................................ 600,000

(b) Capital Expenditures ....................................................... 150,000

Projects Fund Cash ............................................................... 50,000

Vouchers Payable .......................................... 100,000

Problem 16-20, Continued

Trans- Fund or

action Account Account Title Amount

No. Group and Explanation Debit Credit

(e) Capital Encumbrances .................................................... 400,000

Projects Fund Fund Balance—Assigned for Encumbrances . 400,000

(f) Capital Fund Balance—Assigned for Encumbrances ..... 200,000

Projects Fund Encumbrances ............................................... 200,000

Capital Expenditures ....................................................... 200,000

Projects Fund Cash ............................................................... 200,000

(i) Capital Fund Balance—Assigned for Encumbrances ..... 200,000

Projects Fund Encumbrances ............................................... 200,000

Capital Expenditures ....................................................... 210,000

Projects Fund Cash ............................................................... 210,000

(j) Capital Cash ................................................................... 12,000

Projects Fund Revenues ....................................................... 12,000

(2) Closing and Adjusting Entries:

Fund or Account Title Amount

Account Group and Explanation Debit Credit

Problem 16-20, Concluded

Fund or Account Title Amount

Account Group and Explanation Debit Credit

(Transfer Interfund Transfers-Out ............................................ 2,000

residual equity Cash ..................................................................... 2,000

to debt Fund Balance—Restricted ........................................ 2,000

(3) Mountain View

Statement of Revenues, Expenditures,

and Changes in Fund Balance

For Year Ended December 31, 2018

Library Construction Project

Revenues ..................................................................................................... $ 12,000

Expenditures ................................................................................................ 560,000

Excess (deficiency) of revenues over expenditures ............................... $(548,000)

Other financing sources (uses):