Problem 16-3B (Continued)

Part 2

Gazelle Corporation’s dividend payments of $53,600 represent 34% of the

$158,100 net income for the year, and 41% of cash inflow provided by

978

Problem 16-4BA (60 minutes)

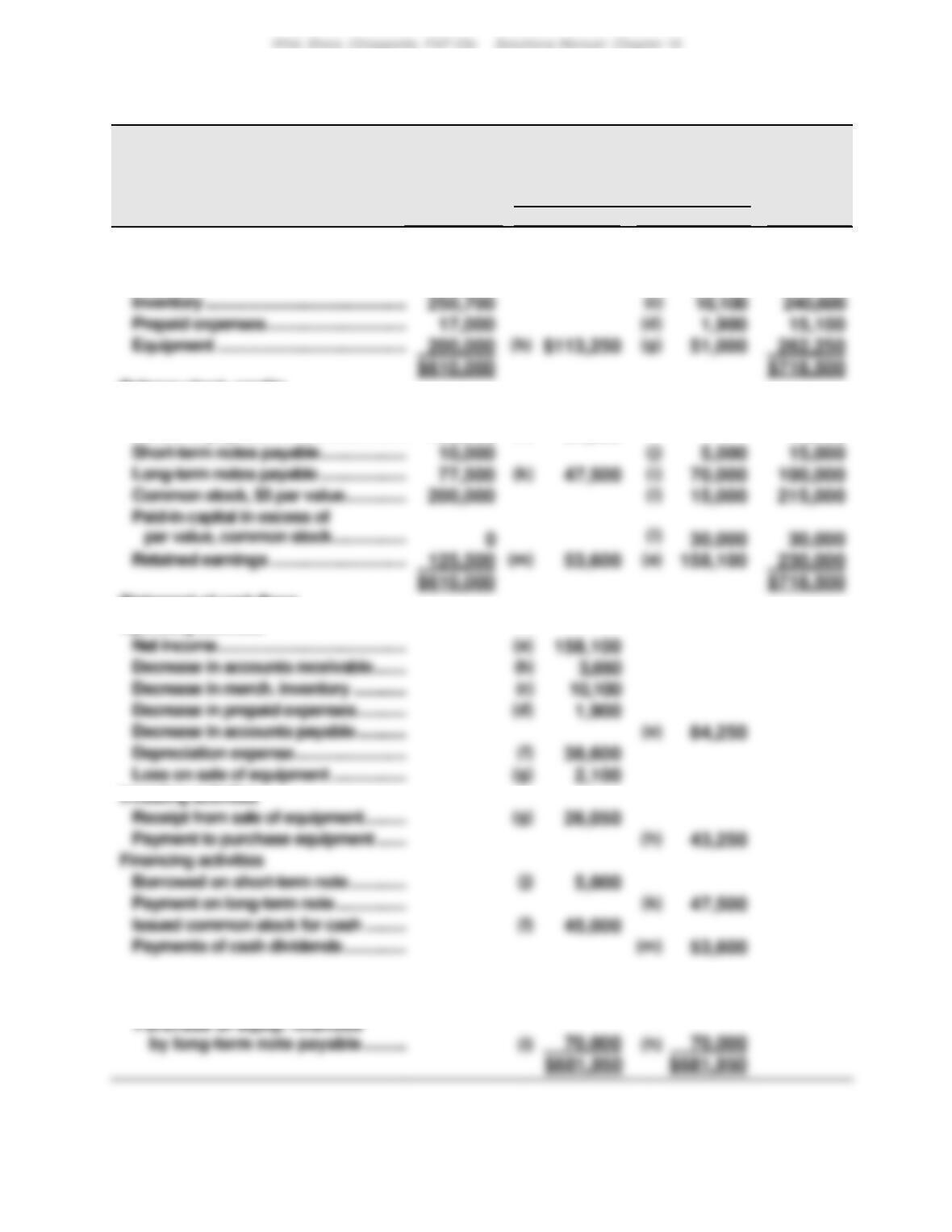

GAZELLE CORPORATION

Spreadsheet for Statement of Cash Flows

For Year Ended December 31, 2017

December

31, 2016

Analysis of Changes

December

31, 2017

Debit

Credit

Balance sheet—debits

Cash ………………………………………………….

$ 61,550

$123,450

Accounts receivable …………………………

80,750

(b)

$ 3,650

77,100

Inventory …………………………………………..

250,700

Prepaid expenses ……………………………..

17,000

15,100

Equipment ………………………………………..

51,000

$610,000

$718,500

Balance sheet—credits

Accum. depreciation—Equip. …………..

$ 95,000

(g)

22,850

(f)

38,600

$110,750

Accounts payable ……………………………..

102,000

(e)

84,250

17,750

Short–term notes payable ………………….

10,000

15,000

Long–term notes payable ………………….

77,500

(k)

47,500

70,000

Common stock, $5 par value …………….

200,000

15,000

0

30,000

30,000

Retained earnings …………………………….

53,600

$610,000

$718,500

Statement of cash flows

Operating activities

Net income ………………………………………..

(a)

Decrease in accounts receivable ………

Decrease in merch. inventory …………..

Decrease in prepaid expenses ………….

(d)

1,900

Decrease in accounts payable ………….

84,250

Depreciation expense ……………………….

38,600

Loss on sale of equipment ……………….

(g)

2,100

Investing activities

Receipt from sale of equipment ………..

(g)

26,050

Payment to purchase equipment ……..

43,250

Financing activities

Borrowed on short–term note ……………

5,000

Issued common stock for cash ………..

45,000

Payments of cash dividends …………….

53,600

Noncash investing and financing

activities

979

Problem 16-4BA (Concluded)

GAZELLE CORPORATION

Statement of Cash Flows

For Year Ended December 31, 2017

Cash flows from operating activities

Net income ………………………………………………………………………………

Adjustments to reconcile net income to net

cash provided by operating activities

Income statement items not affecting cash

Depreciation expense ……………………………………………………….

38,600

Loss on disposal of equipment …………………………………………..

Changes in current assets and current liabilities

Decrease in accounts receivable ($80,750 – $77,100) …………….

Decrease in inventory ($250,700 – $240,600) ……………………

10,100

Decrease in prepaid expenses ($17,000 – $15,100) ………………..

Decrease in accounts payable ($102,000 – $17,750) ………………

Net cash provided by operating activities …………………………..

Cash flows from investing activities

Cash received from sale of equipment …………………………..………

26,050

Cash paid for equipment ……………………………………………………….

Net cash used in investing activities ………………………………………

Cash flows from financing activities

Cash borrowed on short–term note ………………………………………..

Cash paid on long–term note …………………………………………………..

Cash received from issuing stock (3,000 x $15) ……………………….

45,000

Cash paid for dividends ……………………………………………………….

Net increase in cash…………………………………………………………………..

980

Problem 16-5BB (40 minutes)

GAZELLE CORPORATION

Statement of Cash Flows

For Year Ended December 31, 2017

Cash flows from operating activities

Cash received from customers (Note 1) …………………

$1,188,650

Cash paid for inventory (Note 2) …………………………..

Cash paid for other expenses (Note 3) …………………..

Cash paid for income taxes ………………………………….

Net cash provided by operating activities ……………..

Cash flows from investing activities

Cash received from sale of equipment ………………….

Cash paid for equipment ………………………………………

Net cash used in investing activities …………………….

Cash flows from financing activities

Cash borrowed on short-term note ……………………….

Cash paid on long-term note ………………………………..

Cash received from issuing stock (3,000 x $15) ………

Net increase in cash ……………………………………………….

Noncash investing and financing activities

Supporting calculations

981

Problem 16-6B (35 minutes)

SATU COMPANY

Statement of Cash Flows

For Year Ended December 31, 2017

Cash flows from operating activities

Net income ……………………………………………………………………..

$202,767

Adjustments to reconcile net income to net

cash provided by operating activities

Income statement items not affecting cash

Changes in current assets and current liabilities

Decrease in accounts receivable ($25,860 – $20,222) ……

Increase in inventory ($165,667 – $140,320) …………………..

Decrease in accounts payable ($157,530 – $20,372) ……..

Decrease in taxes payable ($6,100 – $2,100) …………………

Net cash provided by operating activities …………………….

Cash flows from investing activities

Cash paid for equipment ……………………………………………….

Cash received from issuing stock (3,000 x $21) ……………..

Cash paid for dividends ………………………………………………..

Problem 16-7BA (50 minutes)

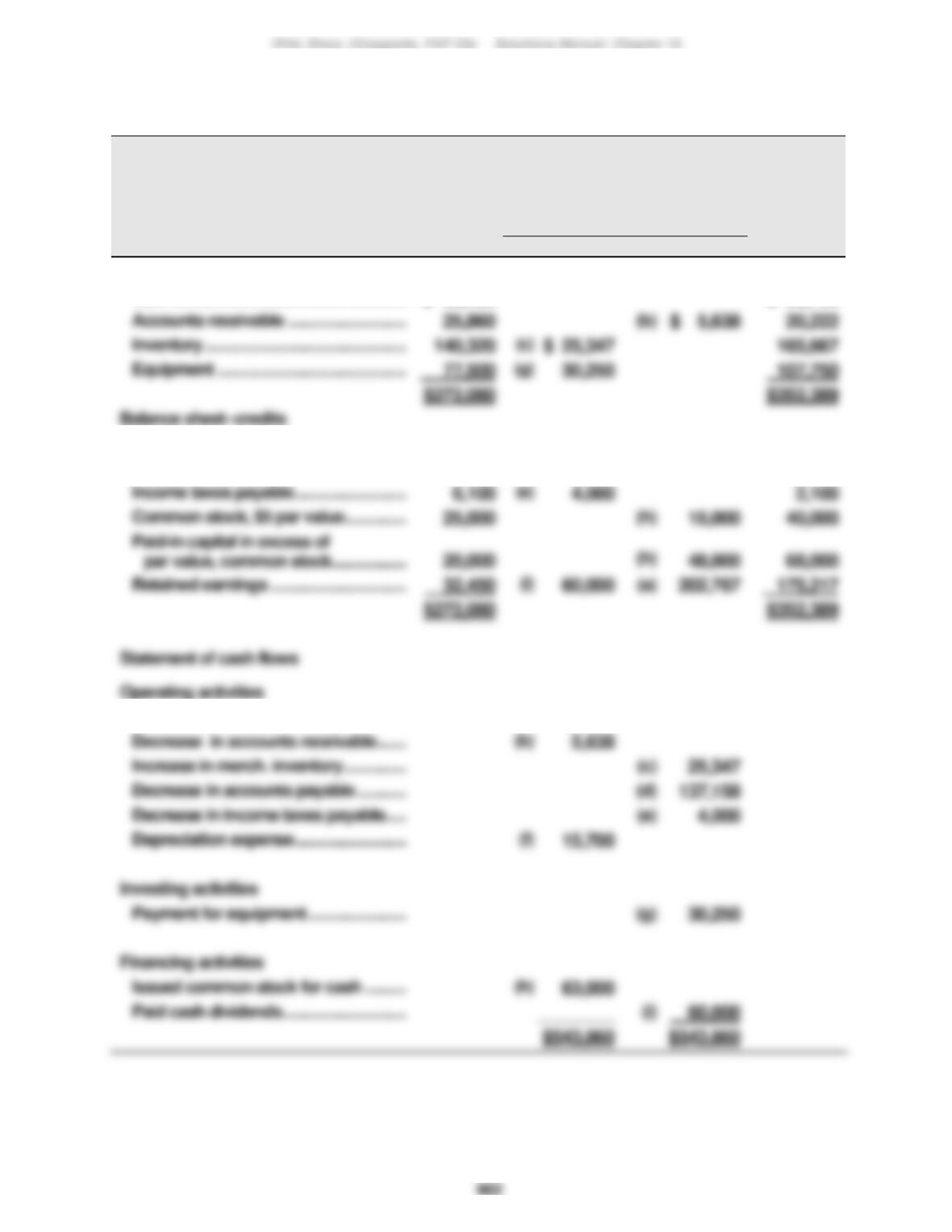

SATU COMPANY

Spreadsheet for Statement of Cash Flows

For Year Ended December 31, 2017

December

31, 2016

Analysis of Changes

December

31, 2017

Debit

Credit

Balance sheet—debits

Cash ………………………………………………….

$ 28,400

$ 58,750

Accounts receivable …………………………

25,860

20,222

Inventory …………………………………………..

140,320

(c)

165,667

Equipment ………………………………………..

(g)

$272,080

$352,389

Balance sheet—credits

Accum. depreciation—Equip. …………..

$ 31,000

(f)

15,700

$ 46,700

Accounts payable ……………………………..

157,530

(d)

137,158

20,372

Income taxes payable ……………………….

(e)

Common stock, $5 par value …………….

25,000

15,000

40,000

20,000

48,000

68,000

Retained earnings …………………………….

$272,080

$352,389

Statement of cash flows

Operating activities

Net income ………………………………………..

(a)

202,767

Decrease in accounts receivable ……..

(b)

Increase in merch. inventory …………….

25,347

Decrease in accounts payable ………….

Decrease in income taxes payable ……

Depreciation expense ……………………….

Investing activities

Payment for equipment …………………….

30,250

Financing activities

Issued common stock for cash ………..

(h)

Paid cash dividends ………………………….

983

Problem 16-7BA (concluded)

SATU COMPANY

Statement of Cash Flows

For Year Ended December 31, 2017

Cash flows from operating activities

Net income ……………………………………………………………………..

$202,767

Adjustments to reconcile net income to net

cash provided by operating activities

Income statement items not affecting cash

Changes in current assets and current liabilities

Net cash provided by operating activities …………………….

Cash paid for equipment ……………………………………………….

Cash received from issuing stock (3,000 x $21) ……………..

Cash paid for dividends ………………………………………………..

984

Problem 16-8BB (35 minutes)

SATU COMPANY

Statement of Cash Flows

For Year Ended December 31, 2017

Cash flows from operating activities

Cash received from customers (Note 1) ………………

$756,438

Cash paid for inventory (Note 2) …………………………

Cash paid for other operating expenses ……………..

Cash paid for income taxes (Note 3) ……………………

Net cash provided by operating activities ……………

Cash flows from investing activities

Cash paid for equipment …………………………………….

Cash flows from financing activities

Cash received from issuing stock (3,000 x $21) ……

Cash paid for cash dividends ……………………………..

Net cash provided by financing activities ……………

Net increase in cash ………………………………………………

Supporting calculations

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 16

985

SERIAL PROBLEM — SP 16

Serial Problem — SP 16, Business Solutions (45 minutes)

BUSINESS SOLUTIONS

Statement of Cash Flows (Indirect)

For Quarter Ended March 31, 2018

Cash flows from operating activities

Net income ………………………………………………………………………………

$ 18,833

Adjustments to reconcile net income to net

cash provided by operating activities

Income statement items not affecting cash

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 16

986

Reporting in Action — BTN 16-1

1. Apple uses the indirect method of reporting operating cash flows. We

2. In all three fiscal years, Apple’s cash flows from operating activities

markedly exceed its cash dividends paid, as shown in the table below:

3. In fiscal 2015, the largest item in reconciling the difference between net

income and cash flow from operations was depreciation and amortization

4. In fiscal 2015, the largest cash inflow from investing activities was $107,447

million from proceeds from sales of marketable securities. The largest cash

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 16

987

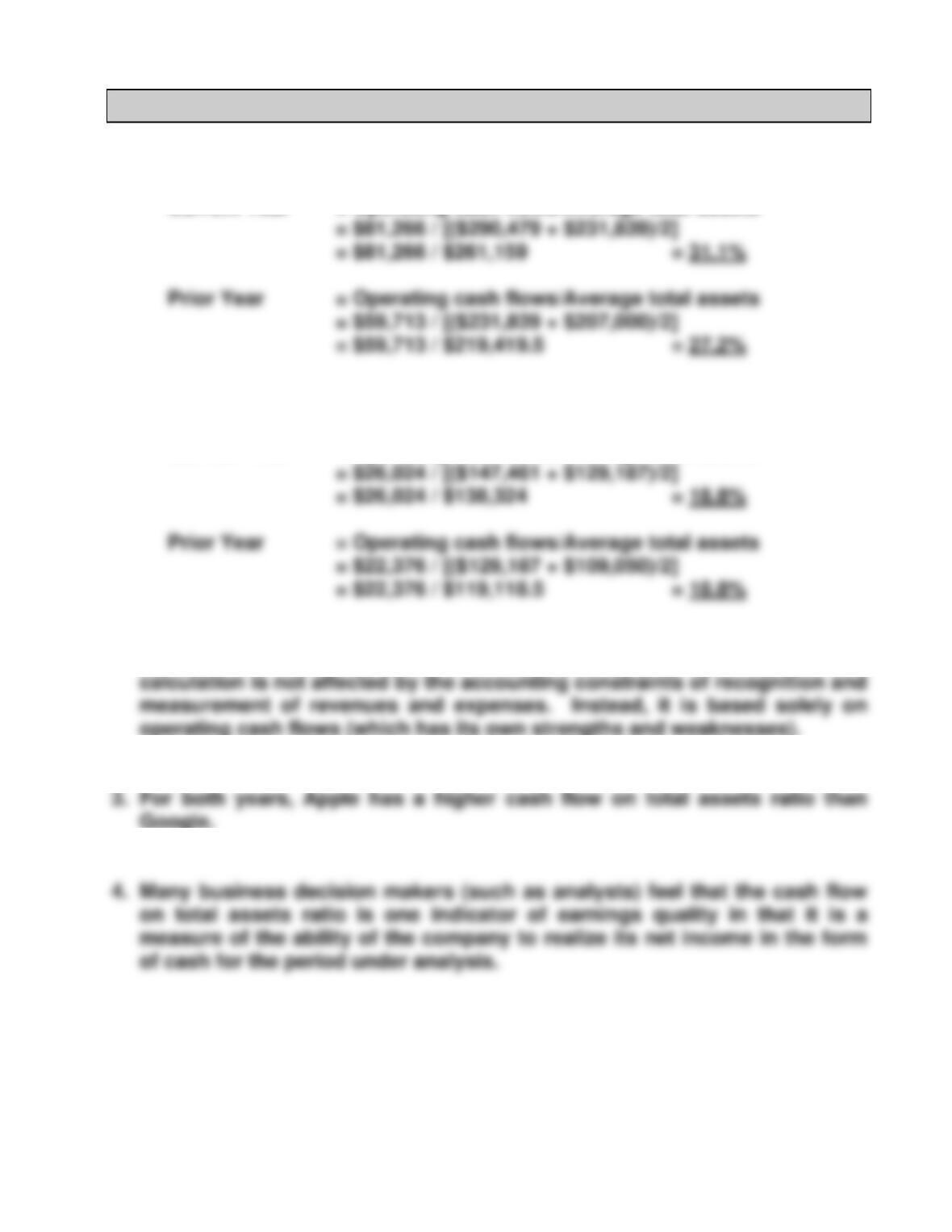

Comparative Analysis — BTN 16-2

1. Apple’s cash flow on total assets ratio ($ millions)

Current Year = Operating cash flows/Average total assets

Google’s cash flow on total assets ratio ($ millions)

Current Year = Operating cash flows/Average total assets

2. The cash flow on total assets ratio reflects the return on average assets by

using actual operating cash flows instead of net income. This return

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 16

988

Ethics Challenge — BTN 16-3

1. The business actions available include

2. As a business owner, Katie Murphy certainly can exercise discretion over

business actions. However, the underlying economic realities should

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 16

989

Communicating in Practice — BTN 16-4

Here is a sample of what the body of the memorandum might include:

TO: Diana Wood

FROM: (Your Name)

SUBJECT: Statement of Cash Flows

DATE: _________________

I am pleased to hear your business is more profitable this year than last.

However, I have been thinking about what you said regarding the statement of

cash flows and have some thoughts as to why you found it confusing.

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 16

990

Taking It to the Net — BTN 16-5

3. The following table shows the net income (or net loss) and the cash flows

from operations for Mendocino Brewing for 2014 and 2015. Over this two–

year period, Mendocino has generated consistently positive cash flows

4. For the recent period, the largest cash outflow for investing was $642,400

for purchases of property, equipment and leasehold improvements.

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 16

991

Teamwork in Action — BTN 16-6

Part 1

a. The reporting objective of the statement of cash flows is to provide

information about important cash inflows and outflows for business

decision makers. It answers specific questions such as:

• How does a company obtain its cash?

• Where does a company spend its cash?

• What is the change in the cash balance?

b. The statement can be prepared using the direct method or the indirect

method for reporting cash flows from operating activities.

Similarities

• Both methods report the same net cash flow from operating activities.

• Both methods classify cash flows into operating, financing, and

investing categories.

Differences

• Cash flow from operating activities is determined differently. The direct

method determines all operating cash inflows and outflows, and then

subtracts total operating outflows from inflows. The indirect method

starts with net income and applies a series of adjustments to reconcile

this accrual basis number to a cash basis number.

• The direct method requires an extra section reconciling net income to

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 16

992

Teamwork in Action (Continued)

c. Steps to prepare the statement of cash flows:

(i) Compute the net increase or decrease in cash using comparative

balance sheet data. This is the target number or the number the

statement will explain and prove.

d. Common analyses made from information in the statement of cash flows

include assessing a company’s:

• Ability to generate future cash flows.

• Ability to pay dividends.

Part 2

Adjusting Net Income to Cash Flow from Operating Activities

Items to Add

Items to Subtract

a.

Noncash expenses

Noncash revenues

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 16

993

Teamwork in Action (Concluded)

Part 3

a. Cash receipts from customers = Sales – Increase in Accounts Receivable,

or, + Decrease in Accounts Receivable.

b. Cash paid for inventory requires a two-step computation.

c. Cash paid for wages and operating expenses = Wages and other operating

d. Cash paid for interest and taxes = Interest and tax expense + Decrease in

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 16

994

Entrepreneurial Decision — BTN 16-7

1. It is common that small businesses must pay cash in advance for items such

as rent, advertising, supplies, and facilities expansion. Consequently, those

2. As a privately owned company, it can potentially raise cash financing for

Entrepreneurial Decision — BTN 16-8

Memorandum

To: Jenna and Matt Wilder

From: Your name

Subject: Performance evaluation of Mountain High

Date: Current Date

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 16

995

Hitting the Road — BTN 16-9

1. The Motley Fool’s Website defines cash flow as earnings before interest,

taxes, depreciation, and amortization (EBITDA). The school’s justification

for this definition includes: “Interest income and expense, as well as taxes, are

all tossed aside because cash flow is designed to focus on the operating business

2. Some analysts tend to focus on this particular earnings definition

(earnings before interest and taxes or EBIT) as it purportedly allows a

3. Answer depends on the links visited and chosen for the report.

Global Decision — BTN 16-10

1. Samsung’s cash flow on total assets ratio follows (in KRW millions):

Current Year = Operating cash flows / Average total assets

2. For the current and prior years, Samsung’s ratios (17.0% and 16.6%,