PROBLEM 16.5A

ANDITON MANUFACTURING (concluded)

b.

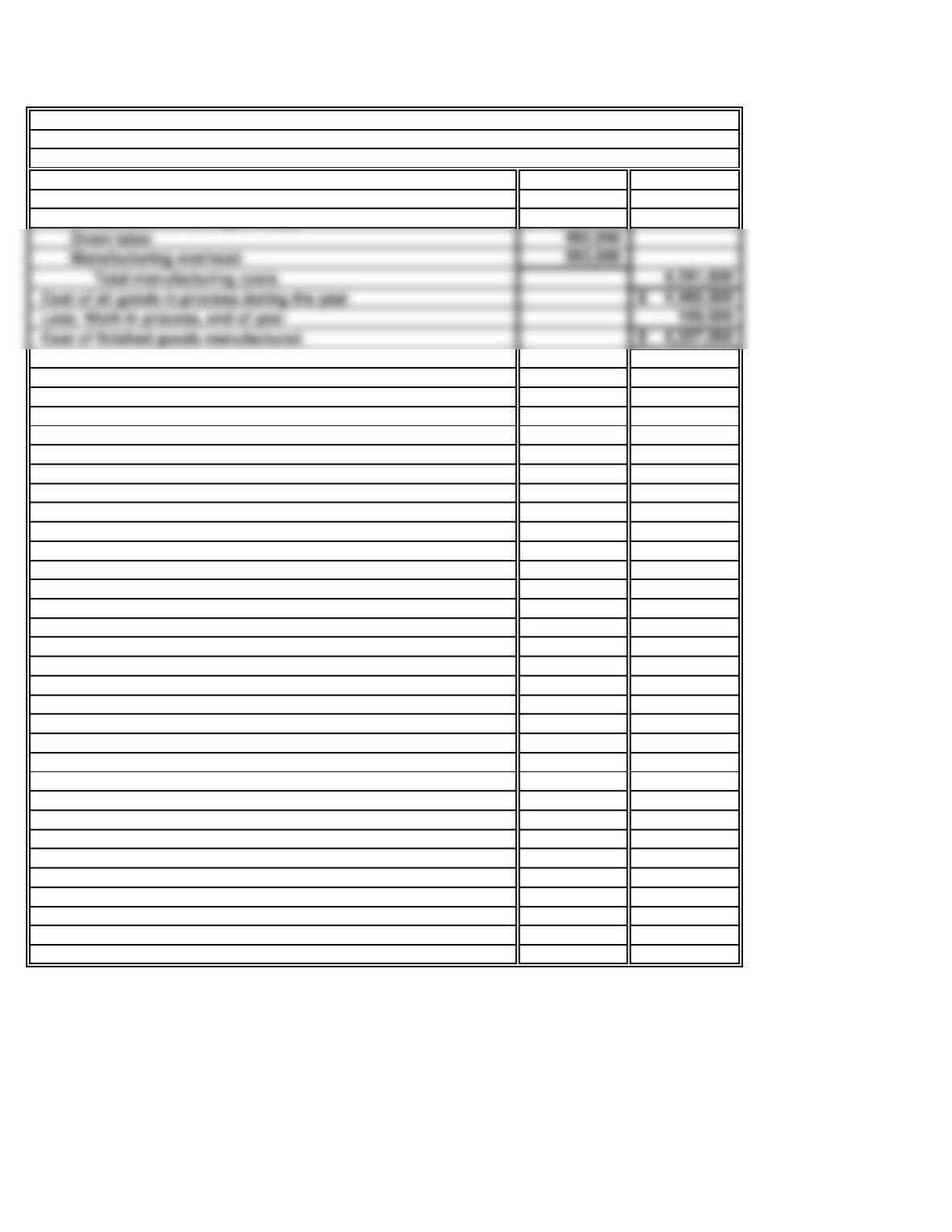

Work in process inventory, beginning of year 75,000$

Add: Manufacturing costs assigned to production:

Direct materials used [part a (2) ]2,506,000$

ANDITON MANUFACTURING CORP.

Schedule of the Cost of Finished Goods Manufactured

For the Year Ended December 31

35 Minutes, Strong

PROBLEM 16.6A

KITCHEN GADGET CO.

a.

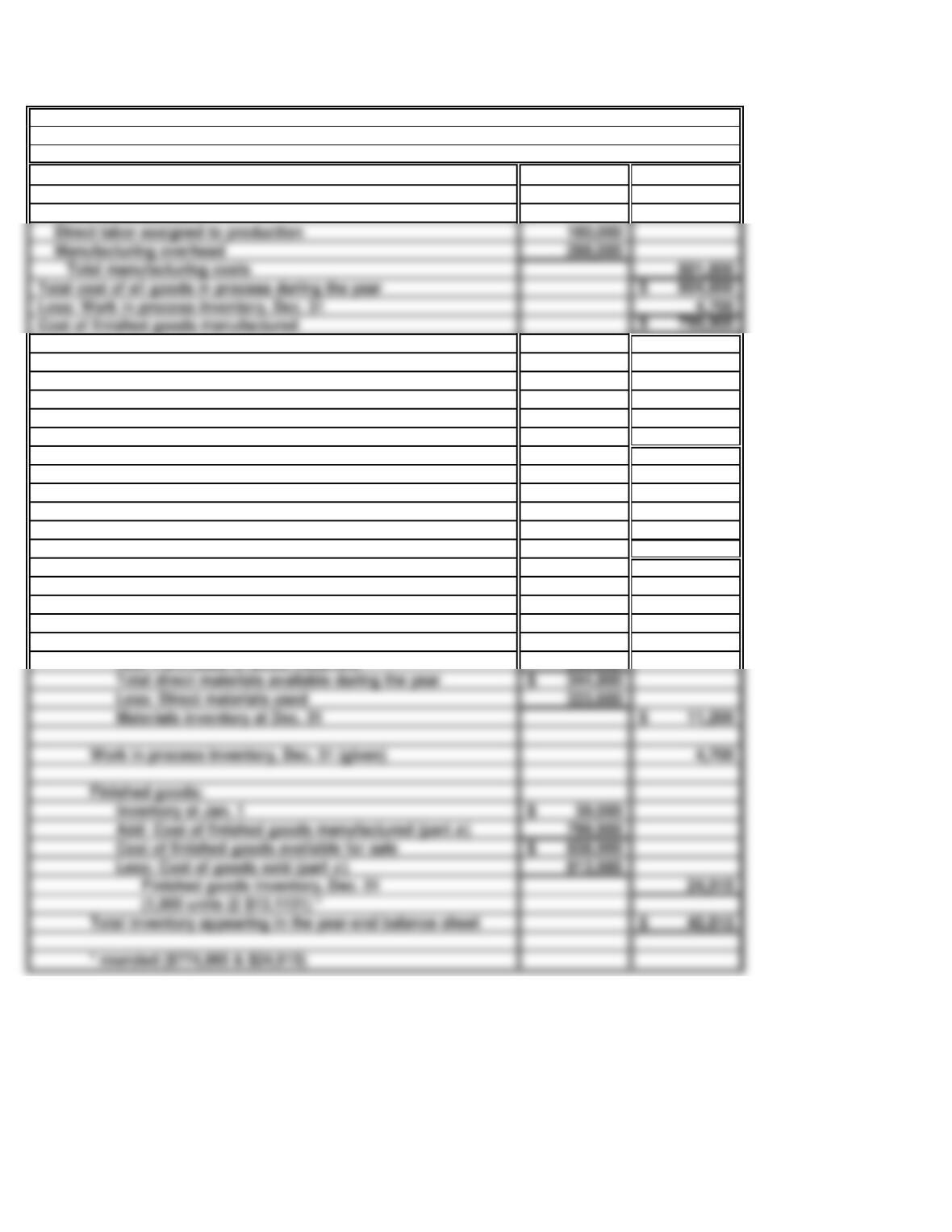

Work in process inventory, Jan. 1 3,000$

Add: Manufacturing costs assigned to production:

Direct materials used 333,600$

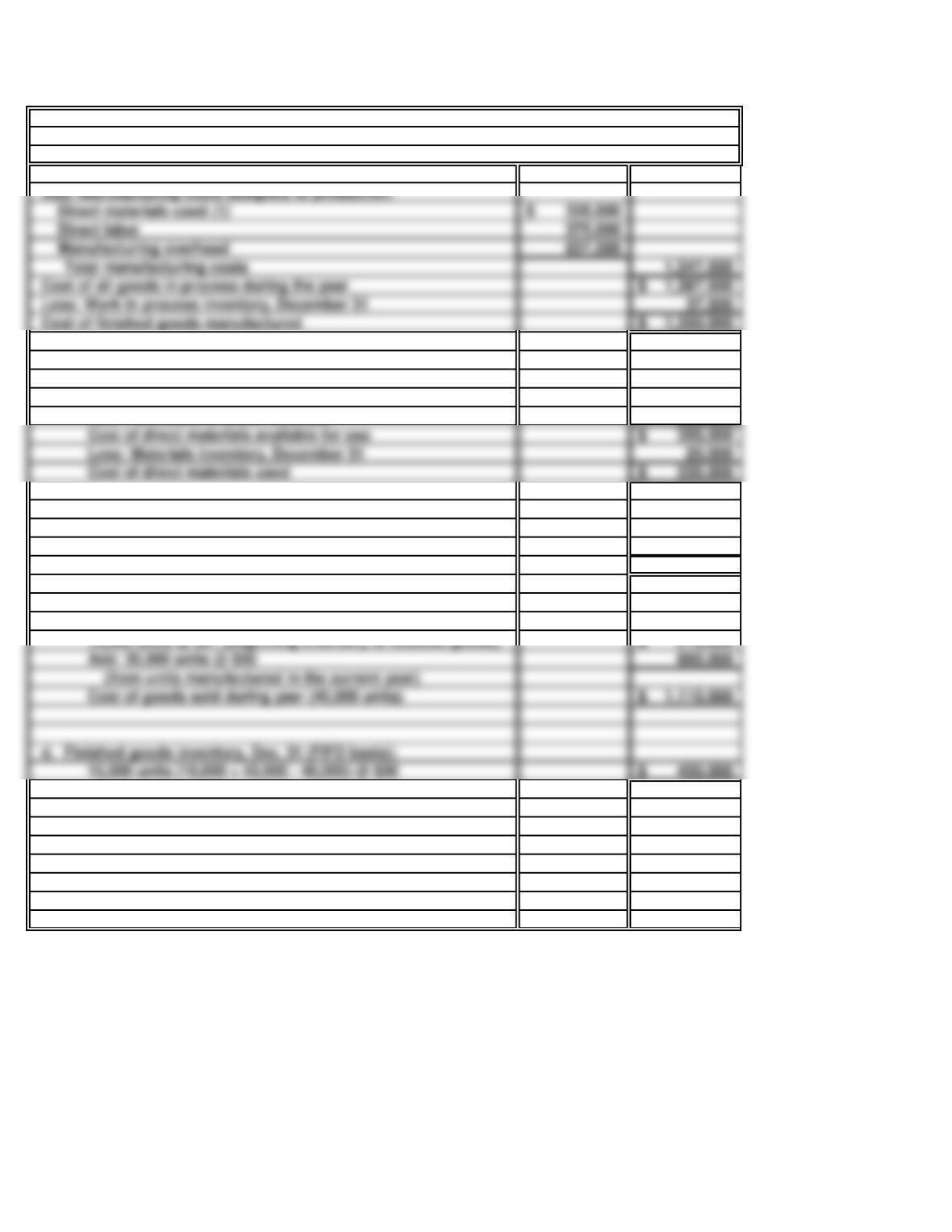

b. Unit cost of goods finished:

Cost of finished goods manufactured (part a)799,900$

Units manufactured 61,000

Unit cost ($799,900 ÷ 61,000 units) 13.1131$

c. Cost of goods sold (62,100 units, FIFO basis):

3,000 units from finished goods inventory at Jan. 1 39,000$

Add: 59,100 units manufactured (@ $13.1131 per unit) * 774,985

Cost of goods sold 813,985$

d. Inventory at December 31:

Materials:

Inventory at Jan. 1 12,800$

Add: Purchases of direct materials 332,000

Total direct materials available during the year 344,800$

Less: Direct materials used 333,600

Materials inventory at Dec. 31 11,200$

Inventory at Jan. 1 39,000$

Cost of finished goods available for sale 838,900$

Total inventory appearing in the year-end balance sheet 40,815$

KITCHEN GADGET CO.

Schedule of the Cost of Finished Goods Manufactured—Dicer Ricer

December 31

PROBLEM 16.6A

KITCHEN GADGET CO. (concluded)

e.

Direct labor is a product cost, and therefore, it becomes “attached” to the products

manufactured. To the extent that units manufactured were sold in the same year, the

25 Minutes, Medium

PROBLEM 16.7A

IDAHO PAPER COMPANY

a.

Work in process inventory, January 1 40,000$

(1)

Cost of direct materials used:

Materials inventory, January 1 25,000$

Add: Purchases of direct materials 330,000

Cost of direct materials available for use 355,000$

Less: Materials inventory, December 31 20,000

Cost of direct materials used 335,000$

b. Average unit costs:

Cost of finished goods manufactured (part a)1,350,000$

Units manufactured 45,000

Average unit cost ($1,350,000 ÷ 45,000 units) 30$

c. Cost of goods sold (FIFO basis):

Add: 30,000 units @ $30 900,000

Cost of goods sold during year (40,000 units) 1,110,000$

d. Finished goods inventory, Dec. 31 (FIFO basis):

IDAHO PAPER CO.

Schedule of the Cost of Finished Goods Manufactured

For the Year Ended December 31

Add: Manufacturing costs assigned to production:

Cost of all goods in process during the year 1,387,500$

Less: Work in process inventory, December 31 37,500

Cost of finished goods manufactured 1,350,000$

40 Minutes, Strong

PROBLEM 16.8A

RAYMOND ENGINEERING CO.

a.

Manufacturing costs assigned to production:

Direct materials used (1) 135,000$

Direct labor 110,000

(1)

Computation of cost of direct materials used:

Purchases of direct materials 181,000$

Less: Materials inventory, end of year 46,000$

Direct materials used 135,000$

c.

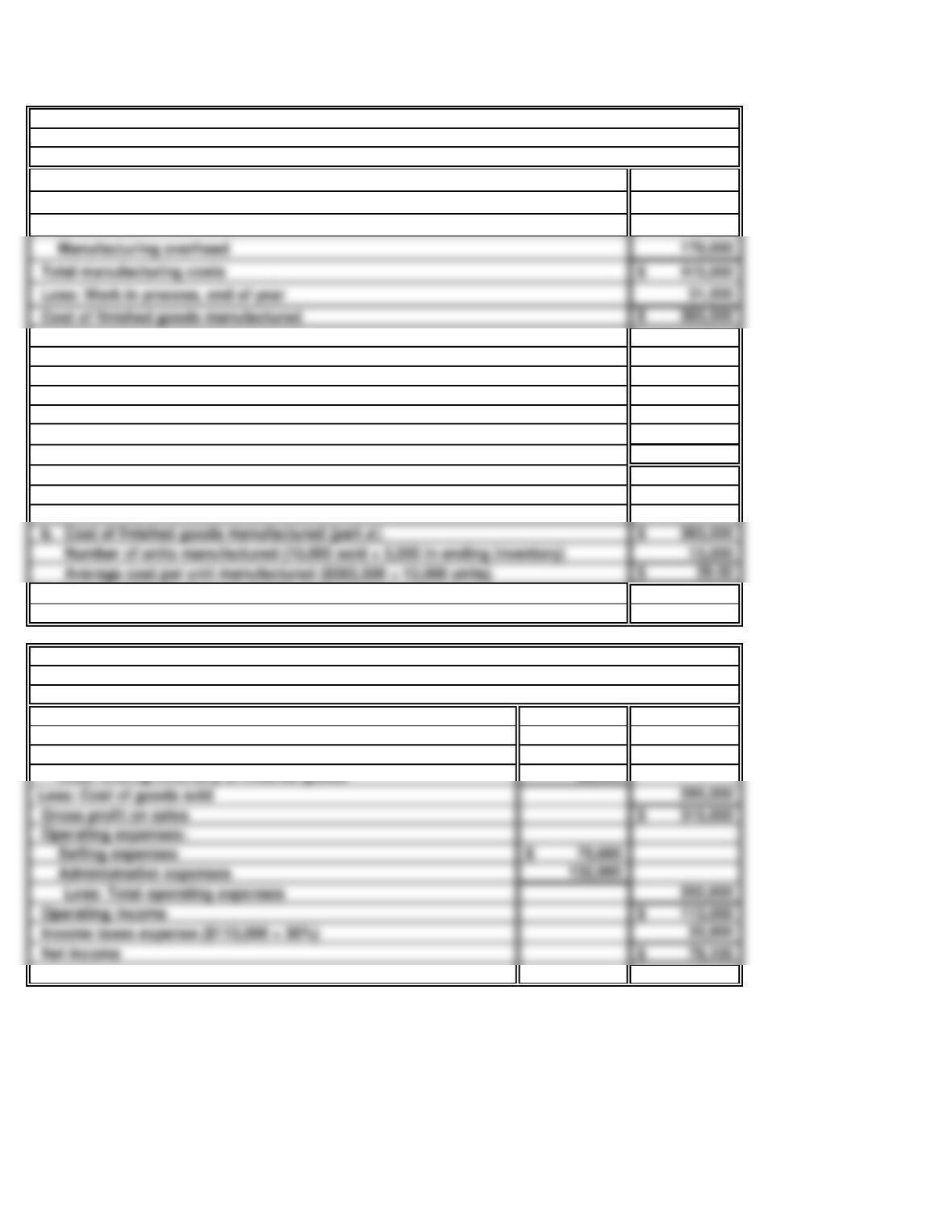

Net sales 610,600$

Cost of goods sold:

Cost of finished goods manufactured (part a)383,500$

Less: Ending inventory of finished goods 88,500

Administrative expenses 132,000

RAYMOND ENGINEERING CO.

Income Statement

For the Year Ended December 31

RAYMOND ENGINEERING CO.

Schedule of the Cost of Finished Goods Manufactured

For the Year Ended December 31

PROBLEM 16.8A

RAYMOND ENGINEERING CO. (concluded)

d.

(53,000)$

166,000

Evaluation of Raymond’s conclusions:

Raymond is in error about the $66.36 unit cost of production and the overall

unprofitability of the business. In concluding that the business sustained a net loss,

Net loss calculated by Raymond

Raymond has made three errors in computing the cost of production. First, he included

selling and administrative expenses in his calculations. These costs do not relate to the

manufacturing process and, therefore, are not part of the cost to manufacture the valves.

Add: Product costs erroneously deducted as expense

Actual operating income

Less: Income taxes (ignored by Raymond)

Actual net income (see part c)

SOLUTIONS TO PROBLEMS SET B

20 Minutes, Easy

PROBLEM 16.1B

PINNING, INC.

a. Computations of amounts:

(1) Average per-unit manufacturing cost:

Cost of finished goods manufactured 880,000$

Number of completed units manufactured 110

Average cost per unit ($880,000 ÷ 110 units) 8,000$

Ending finished goods inventory:

Average per-unit manufacturing cost [part (1) ]8,000$

Number of finished goods in inventory

(110 manufactured, less 90 sold) 20

Ending inventory of finished goods

(20 units × $8,000 per unit) 160,000$

(3) Cost of goods sold:

Cost of goods sold (90 units × $8,000 per unit) 720,000$

Alternative computation:

Cost of finished goods manufactured 880,000$

(2) Ending materials inventory:

Direct materials purchased 415,000$

Less: Direct materials used in production 385,000

Materials inventory, end of year 30,000$

Ending work in process inventory:

Manufacturing costs charged to work in process:

Direct materials used 385,000$

Direct labor assigned to production 335,000

Manufacturing overhead 430,000

PROBLEM 16.1B

PINNING, INC. (concluded)

b.

1,180,000$

The disposition of the $1,180,000 in manufacturing costs “incurred” during the year is

summarized below:

Comments on deducting manufacturing costs from revenue:

No—the entire $1,180,000 in manufacturing costs is not deducted from the revenue of the

Total manufacturing costs “incurred” during the year

15 Minutes, Easy

PROBLEM 16.2B

RIVER QUEEN CORPORATION

a. Total manufacturing costs assigned to work in process:

Direct materials used 800,000$

Direct labor applied to production 1,000,000

Manufacturing overhead 2,000,000

Total manufacturing costs assigned to work in process 3,800,000$

b. Cost of finished goods manufactured:

d. Gross profit on sales:

Sales ($130,000 average sales price × 30 units sold) 3,900,000$

Less: Cost of goods sold (c)2,400,000

Gross profit on sales 1,500,000$

e.

Cost per completed boat 80,000$

Number of boats completed during the year 40

Cost of finished goods manufactured (40 units × $80,000 per unit) 3,200,000$

c.

Cost of goods sold:

Cost per completed boat 80,000$

Number of completed boats sold 30

Cost of goods sold (30 units × $80,000 per unit) 2,400,000$

20 Minutes, Easy

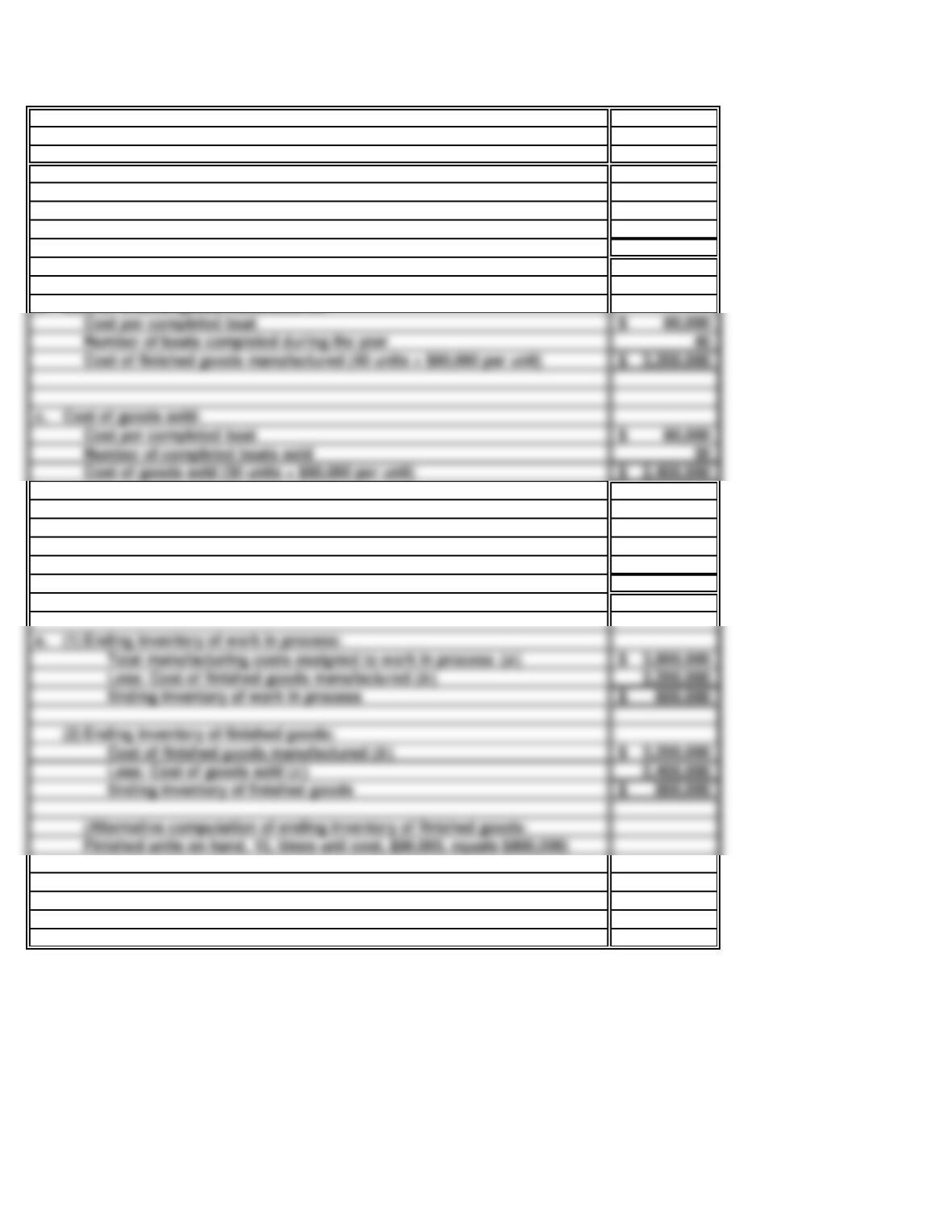

PROBLEM 16.3B

ISP, INC.

a. Purchases of direct materials 260,000$

b. Cost of direct materials used:

e. Overhead rate:

Overhead assigned during the year 210,000$

Direct labor costs assigned to production 140,000$

Overhead rate, stated as a percentage of direct labor cost

($210,000 ÷ $140,000) 150%

f. Total Manufacturing costs:

Direct materials used (part b)255,000$

Direct labor costs 140,000

Manufacturing overhead 210,000

Total manufacturing costs 605,000$

Work in process inventory, beginning of year 20,000$

Add: Total manufacturing costs (part f)605,000

Cost of all goods in process during the year 625,000$

Less: Cost of finished goods manufactured 608,000

Work in process inventory, end of year 17,000$

i. Cost of goods sold:

Beginning inventory of finished goods 45,000$

Add: Cost of finished goods manufactured 608,000

Cost of goods available for sale 653,000$

Less: Ending inventory of finished goods 50,000

Cost of goods sold 603,000$

Materials inventory, beginning of year 10,000$

Add: Purchases of direct materials 260,000

Cost of materials available for use 270,000$

Less: Materials inventory, end of year 15,000

Cost of direct materials used 255,000$

c. Direct labor costs assigned to production 140,000$

PROBLEM 16.3B

ISP, INC. (concluded)

j. Total inventory at year-end:

20 Minutes, Easy

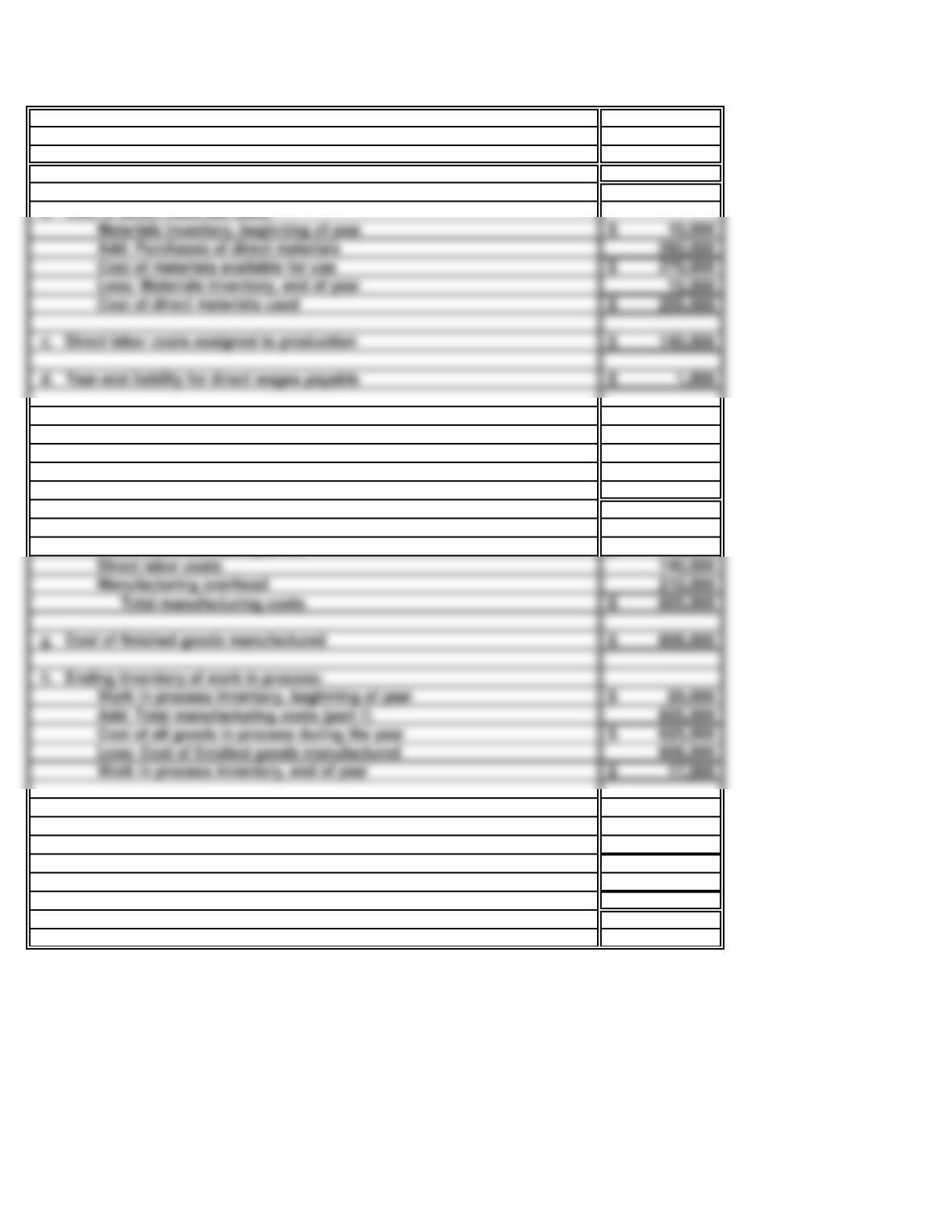

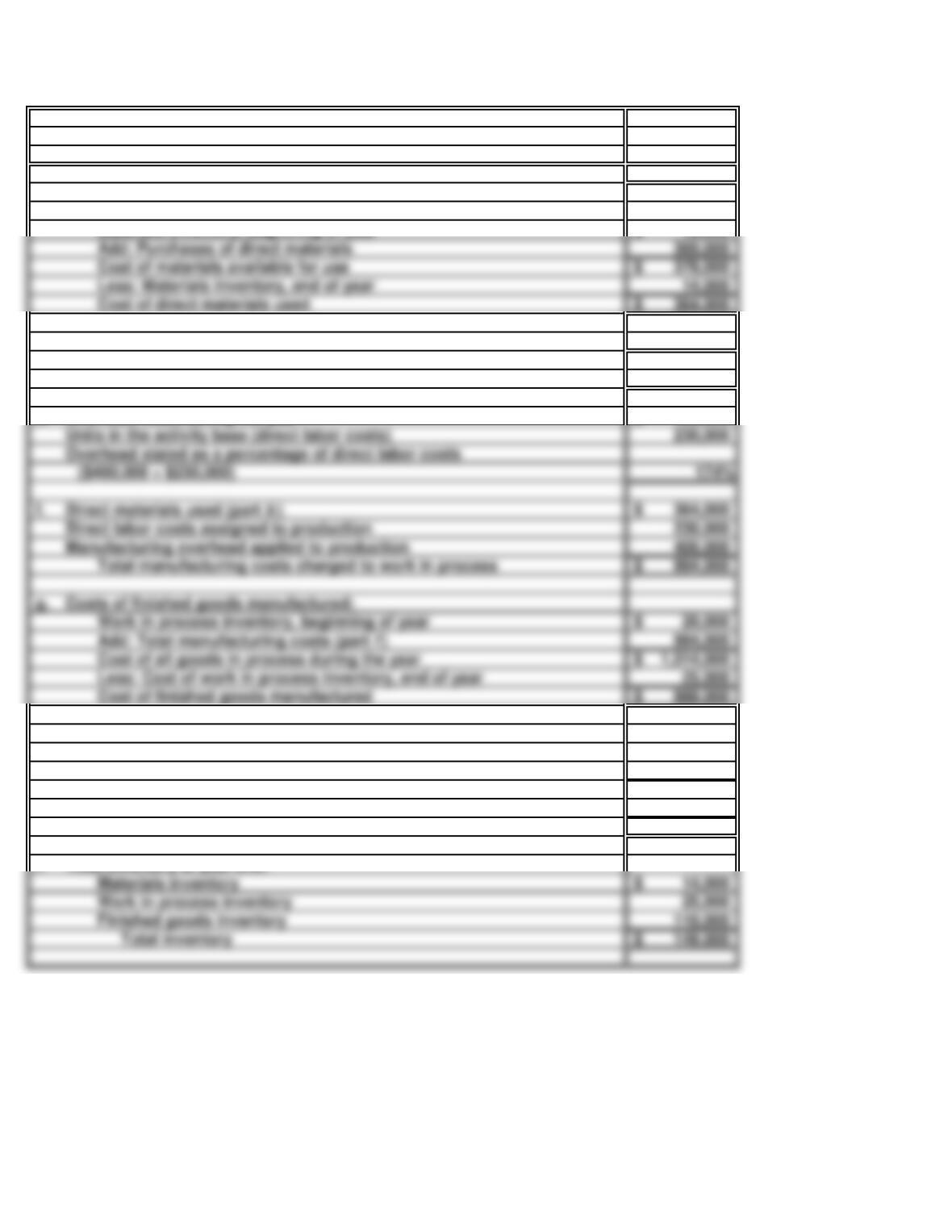

PROBLEM 16.4B

PAYBACK CORPORATION

a. Purchases of direct materials 360,000$

b. Cost of direct materials used:

Materials inventory, beginning of year 18,000$

c. Direct labor payrolls paid during the year 225,000$

d. Direct labor costs assigned to production 230,000$

e. Overhead costs during the year 400,000$

f. Direct materials used (part b)364,000$

Total manufacturing costs charged to work in process 994,000$

g. Costs of finished goods manufactured:

Work in process inventory, beginning of year 20,000$

Add: Total manufacturing costs (part f)994,000

Cost of all goods in process during the year 1,014,000$

Less: Cost of work in process inventory, end of year 25,000

Cost of finished goods manufactured 989,000$

h. Cost of goods sold:

Beginning inventory of finished goods 98,000$

Add: Cost of finished goods manufactured (part g)989,000

Cost of goods available for sale 1,087,000$

Less: Ending inventory of finished goods 110,000

Cost of goods sold 977,000$

i. Total inventory at year-end:

Materials inventory 14,000$

Work in process inventory 25,000

Finished goods inventory 110,000

Add: Purchases of direct materials 360,000

Cost of materials available for use 378,000$

Less: Materials inventory, end of year 14,000

Cost of direct materials used 364,000$

35 Minutes, Medium

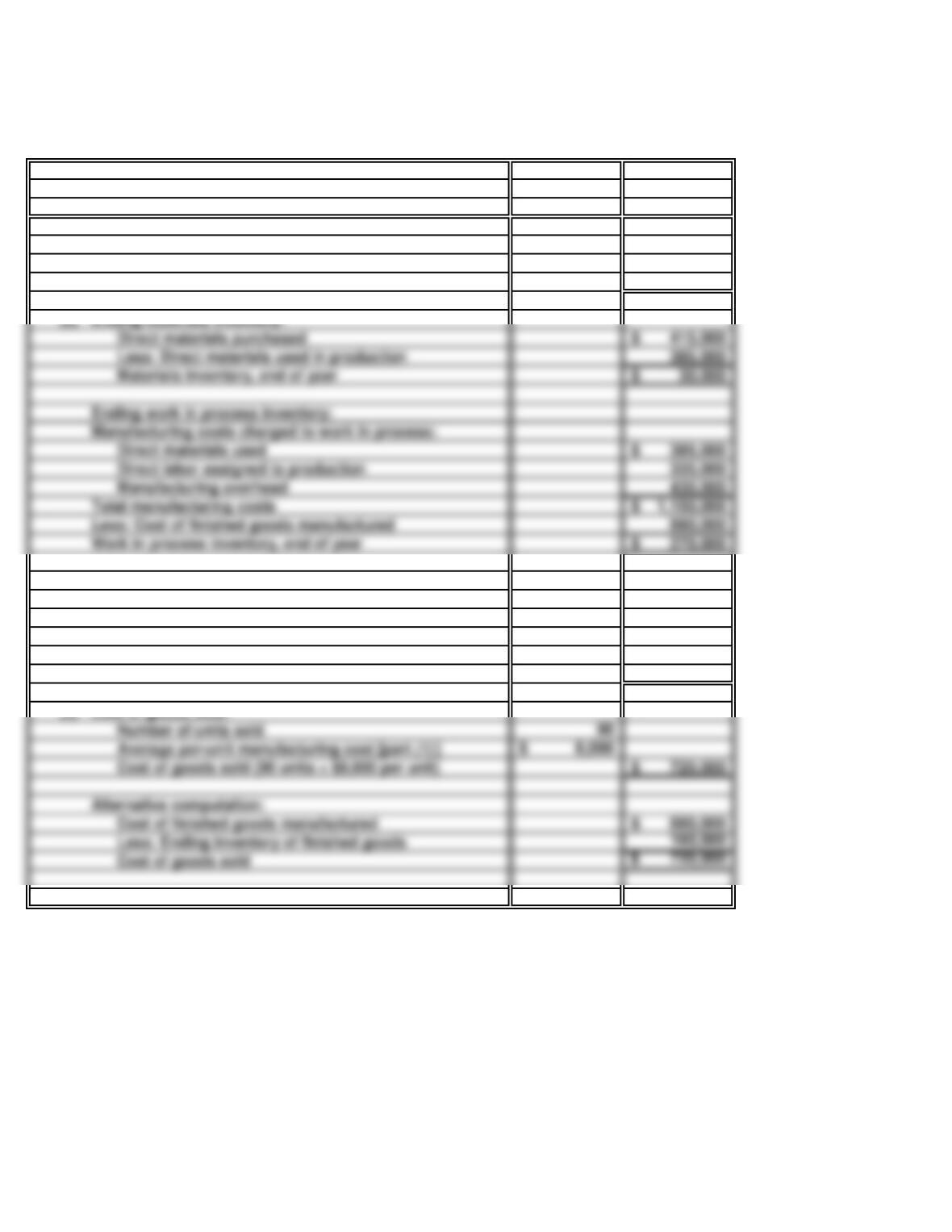

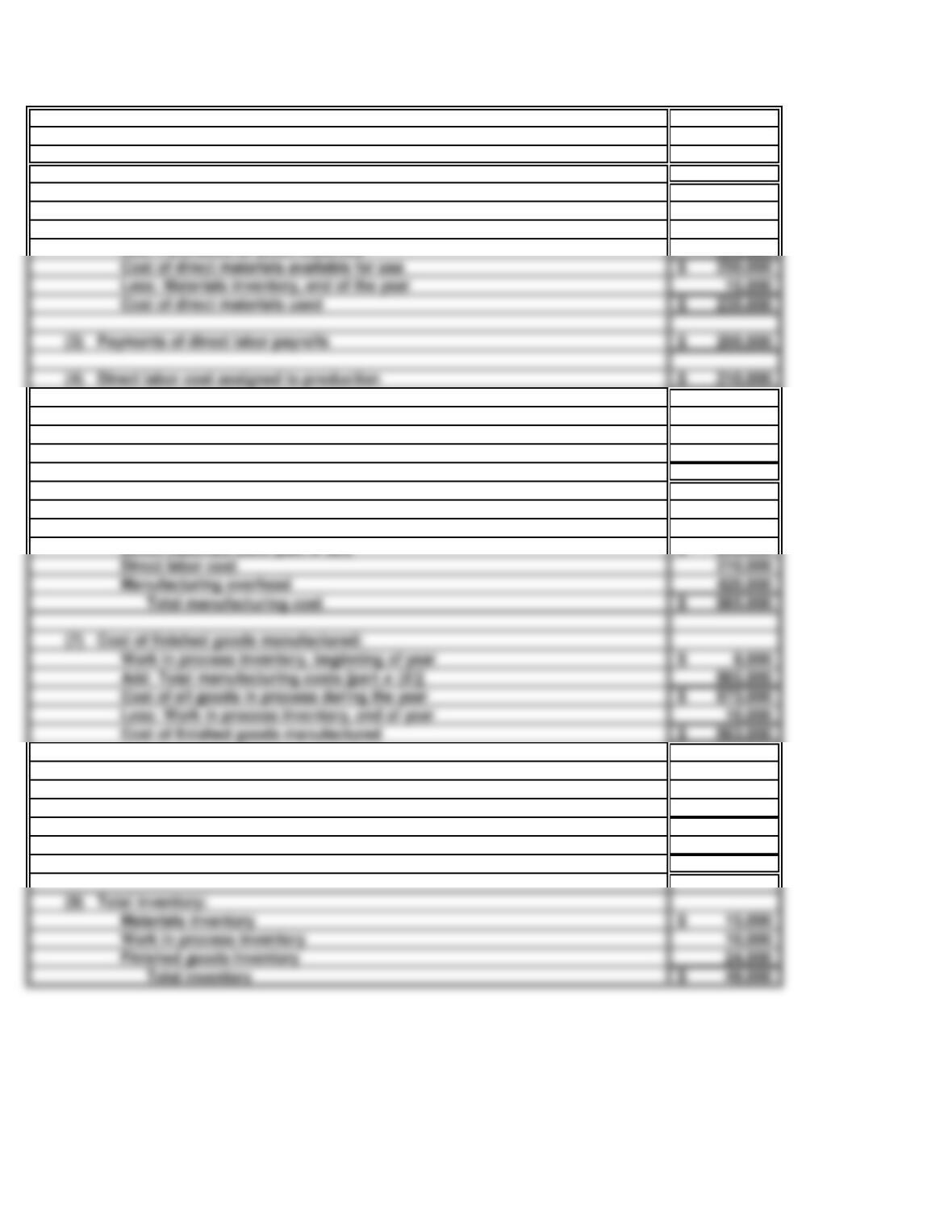

PROBLEM 16.5B

VALLEYVIEW MANUFACTURING

a. (1) Direct materials purchased 225,000$

(2) Direct materials used:

Materials inventory, beginning of year 25,000$

Add: Purchases of direct materials 225,000

(5) Overhead:

Overhead assigned to production 420,000$

Direct labor cost assigned to production 210,000

Overhead stated as a percentage of direct labor cost ($420,000 ÷ $210,000) 200%

($420,000 ÷ $210,000)

(6) Total manufacturing costs:

Direct materials used [part a (2) ]235,000$

Direct labor cost 210,000

Manufacturing overhead 420,000

(7) Cost of finished goods manufactured:

Work in process inventory, beginning of year 8,000$

Add: Total manufacturing costs [part a (6)] 865,000

Cost of all goods in process during the year 873,000$

Less: Work in process inventory, end of year 10,000

Cost of finished goods manufactured 863,000$

(8) Cost of goods sold:

Beginning inventory of finished goods 30,000$

Add: Cost of finished goods manufactured [part a (7)] 863,000

Cost goods available for sale 893,000$

Less: Ending inventory of finished goods 24,000

Cost of goods sold 869,000$

(9) Total inventory:

Materials inventory 15,000$

Work in process inventory 10,000

Finished goods Inventory 24,000

Cost of direct materials available for use 250,000$

Less: Materials inventory, end of the year 15,000

Cost of direct materials used 235,000$