PROBLEM 16.5B

VALLEYVIEW MANUFACTURING (concluded)

b.

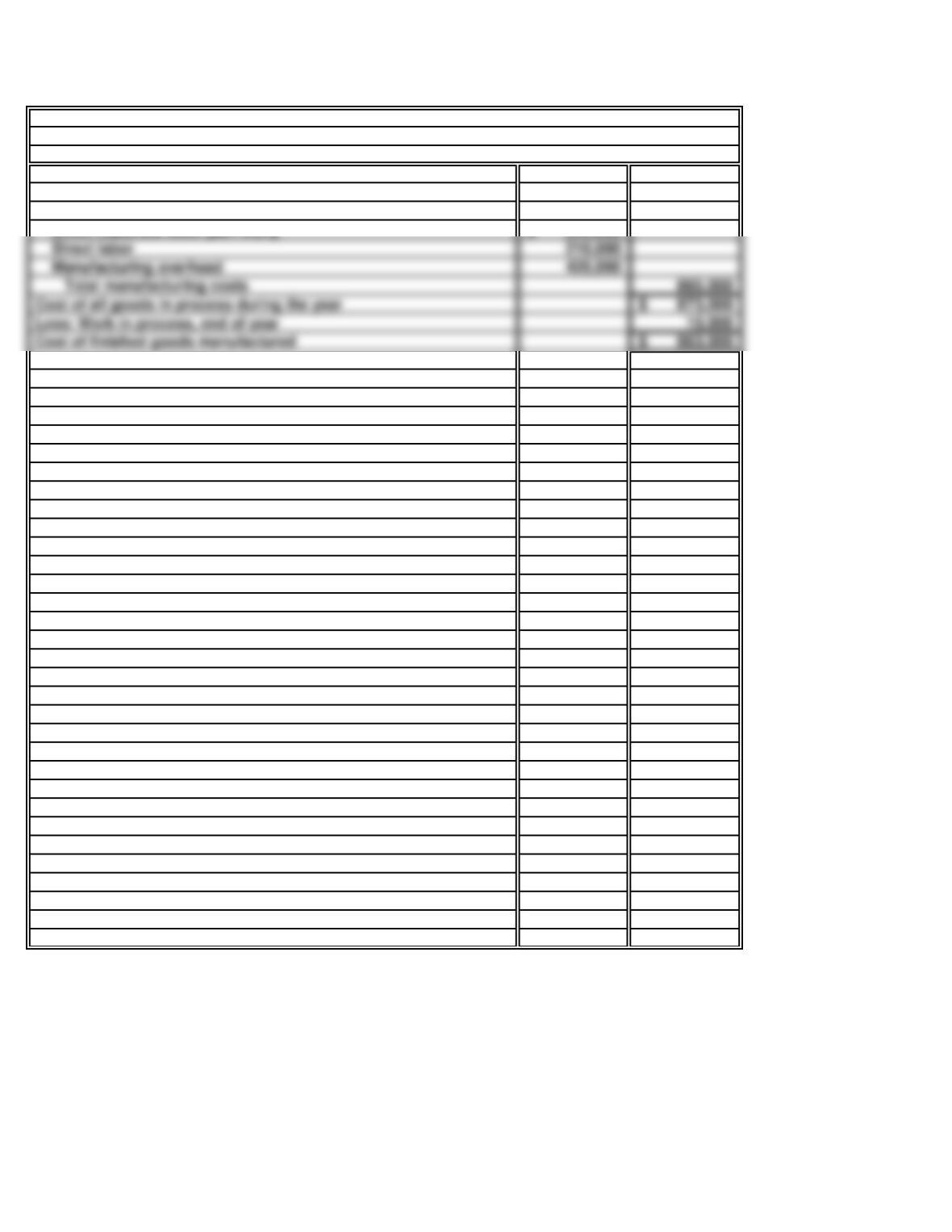

Work in process inventory, beginning of year 8,000$

Add: Manufacturing costs assigned to production:

Direct materials used [part a(2)] 235,000$

VALLEYVIEW MANUFACTURING CORP.

Schedule of the Cost of Finished Goods Manufactured

For the Year Ended December 31

Cost of all goods in process during the year 873,000$

Less: Work in process, end of year 10,000

Cost of finished goods manufactured 863,000$

35 Minutes, Strong

PROBLEM 16.6B

COLUMBUS TOY CO.

a.

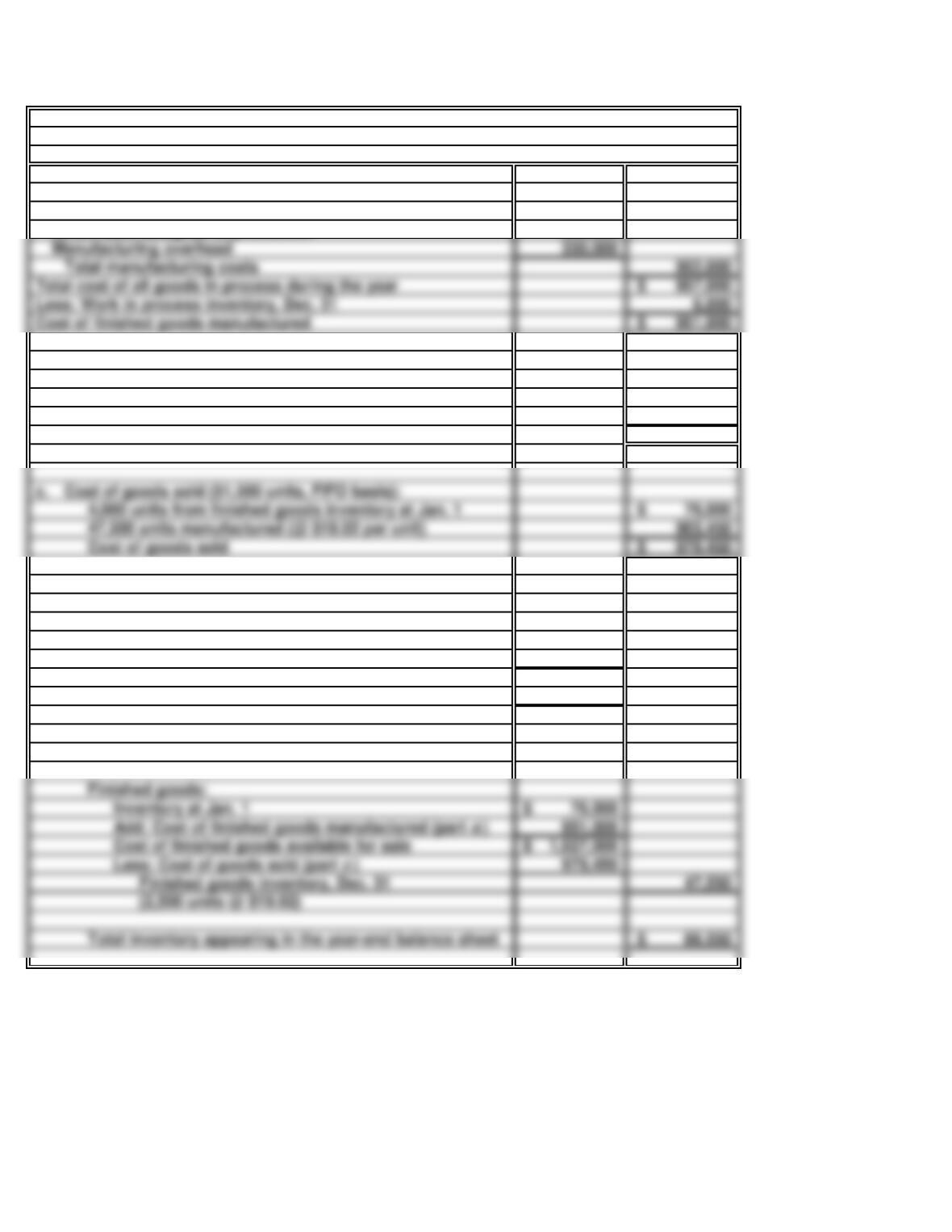

Work in process inventory, Jan. 1 5,000$

Add: Manufacturing costs assigned to production:

Direct materials used 402,000$

Direct labor assigned to production 220,000

b. Unit cost of goods finished:

Cost of finished goods manufactured (part a)951,000$

Units manufactured 50,000

Unit cost ($951,000 ÷ 50,000 units) 19.02$

4,000 units from finished goods inventory at Jan. 1 76,000$

Cost of goods sold 979,450$

d. Inventory at December 31:

Materials:

Inventory at Jan. 1 15,000$

Add: Purchases of direct materials 400,000

Total direct materials available during the year 415,000$

Less: Direct materials used 402,000

Materials inventory at Dec. 31 13,000$

Work in process inventory, Dec. 31 (given) 6,000

Finished goods:

Inventory at Jan. 1 76,000$

Cost of finished goods available for sale 1,027,000$

Total inventory appearing in the year-end balance sheet 66,550$

COLUMBUS TOY CO.

Schedule of the Cost of Finished Goods Manufactured—Old Joe

For the Year Ended December 31

Manufacturing overhead 330,000

Total cost of all goods in process during the year 957,000$

Less: Work in process inventory, Dec. 31 6,000

Cost of finished goods manufactured 951,000$

PROBLEM 16.6B

COLUMBUS TOY CO. (concluded)

e.

Direct labor is a product cost, and therefore, it becomes “attached” to the products

manufactured. To the extent that units manufactured during the year were sold in that

25 Minutes, Medium

PROBLEM 16.7B

CEDAR COMPANY

a.

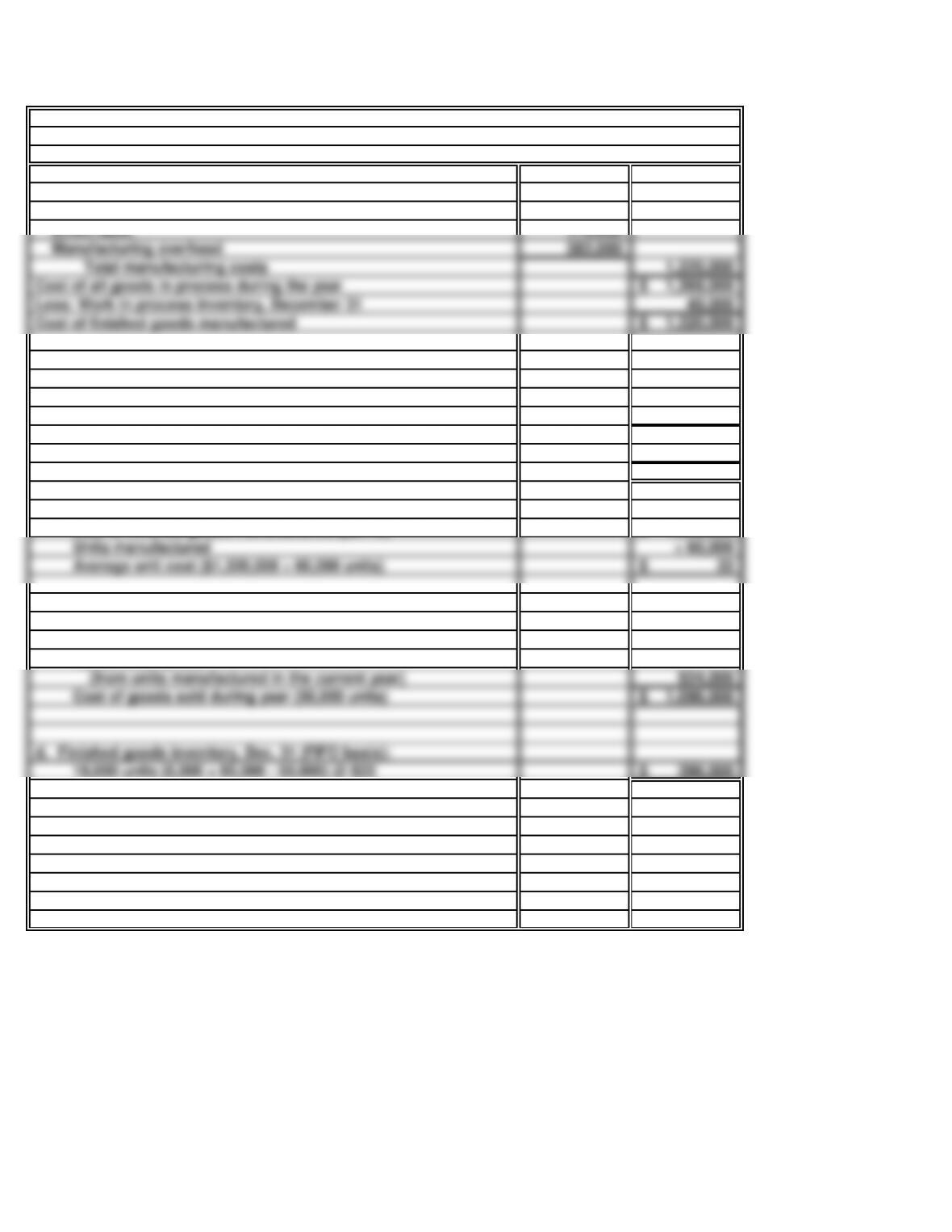

Work in process inventory, January 1 49,000$

Add: Manufacturing costs assigned to production:

Direct materials used (1)328,000$

(1)

Cost of direct materials used:

Materials inventory, January 1 40,000$

Purchases of direct materials 310,000

Cost of direct materials available for use 350,000$

Less: Materials inventory, December 31 22,000

Cost of direct materials used 328,000$

b. Average unit costs:

Cost of finished goods manufactured (part a)1,320,000$

Units manufactured ÷ 60,000

Average unit cost ($1,320,000 ÷ 60,000 units) 22$

c. Cost of goods sold (FIFO basis):

8,000 units @ $21.50 (beginning inventory of finished goods) 172,000$

42,000 units @ $22

Cost of goods sold during year (50,000 units) 1,096,000$

d. Finished goods inventory, Dec. 31 (FIFO basis):

CEDAR COMPANY

Schedule of the Cost of Finished Goods Manufactured

For the Year Ended December 31

Cost of all goods in process during the year 1,369,000$

Less: Work in process inventory, December 31 49,000

Cost of finished goods manufactured 1,320,000$

40 Minutes, Strong

PROBLEM 16.8B

JACKSON ENGINEERING CO.

a.

Manufacturing costs assigned to production:

Direct materials used (1) 137,000$

Direct labor 113,000

(1)

Computation of cost of direct materials used:

Purchases of direct materials 188,000$

Less: Materials inventory, end of year 51,000

Direct materials used 137,000$

c.

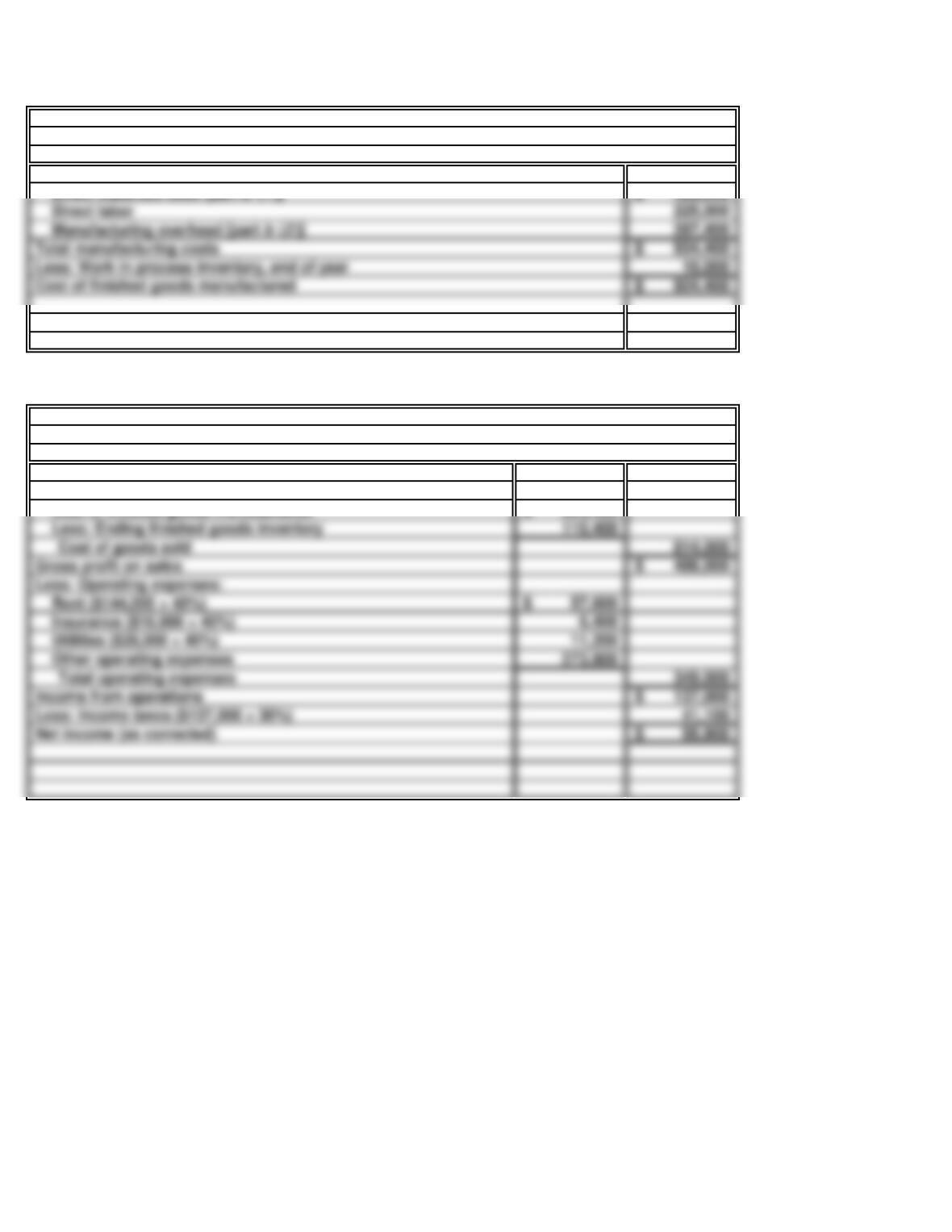

Net sales 625,000$

Add: Cost of goods sold:

Cost of finished goods manufactured (part a)378,000$

Cost of goods sold 270,000

Gross profit on sales 355,000$

Operating expenses:

Operating income 145,000

Less: Income taxes expense ($145,000 × 20%) 29,000

Net income 116,000$

JACKSON ENGINEERING CO.

Income Statement

For the Year Ended December 31

JACKSON ENGINEERING CO.

Schedule of the Cost of Finished Goods Manufactured

For the Year Ended December 31

PROBLEM 16.8B

JACKSON ENGINEERING CO. (concluded)

d.

(46,000)$

191,000

Evaluation of Jackson’s conclusions:

Jackson is in error about the $67.10 unit cost of production and the overall unprofitability

of the business. In concluding that the business sustained a net loss, Jackson treated

product costs as if they were period costs to be offset against the revenue of the year.

Net loss calculated by Jackson

Jackson has made three errors in computing the cost of production. First, he included

selling and administrative expenses in his calculations. These costs do not relate to the

Add: Product costs erroneously deducted as expense

Actual operating income

Less: Income taxes (ignored)

Actual net income (see part c)

40 Minutes, Strong CASE 16.1

WEST TEXAS GUITAR COMPANY

a.

(2)

(3)

b. (1) Cost of direct materials used:

Purchases of direct materials 460,000$

The errors and shortcomings in the illustrated income statement include the following:

Dividends declared on common stock have been offset against revenue in measuring

As a result of deduction from revenue of dividends declared and of manufacturing costs

relating to ending inventories of raw materials, goods in process, and finished goods, it is

reasonable to conclude that the company’s actual net income is higher than the amount

shown in the income statement.

Period expenses are improperly included in the cost of goods sold. As a result, the

CASE 16.1

WEST TEXAS GUITAR COMPANY (concluded)

c.

Manufacturing costs assigned to production:

Direct materials used [part b (1)] 422,000$

d.

Net sales 1,300,000$

Add: Cost of goods sold:

Cost of finished goods manufactured 924,400$

Less: Ending finished goods inventory 110,400

Gross profit on sales 486,000$

Less: Operating expenses:

Rent ($144,000 × 40%) 57,600$

Insurance ($16,000 × 40%) 6,400

Utilities ($28,000 × 40%) 11,200

Other operating expenses 273,800

Income from operations 137,000$

Less: Income taxes ($137,000 × 30%) 41,100

Net income (as corrected) 95,900$

WEST TEXAS GUITAR COMPANY

Income Statement

For the Year Ended December 31

WEST TEXAS GUITAR COMPANY

Schedule of the Cost of Finished Goods Manufactured

For the Year Ended December 31

Direct labor 225,000

Manufacturing overhead [part b (2)] 287,400

Total manufacturing costs 934,400$

Less: Work in process inventory, end of year 10,000

Cost of finished goods manufactured 924,400$

40 Minutes, Strong

CASE 16.2

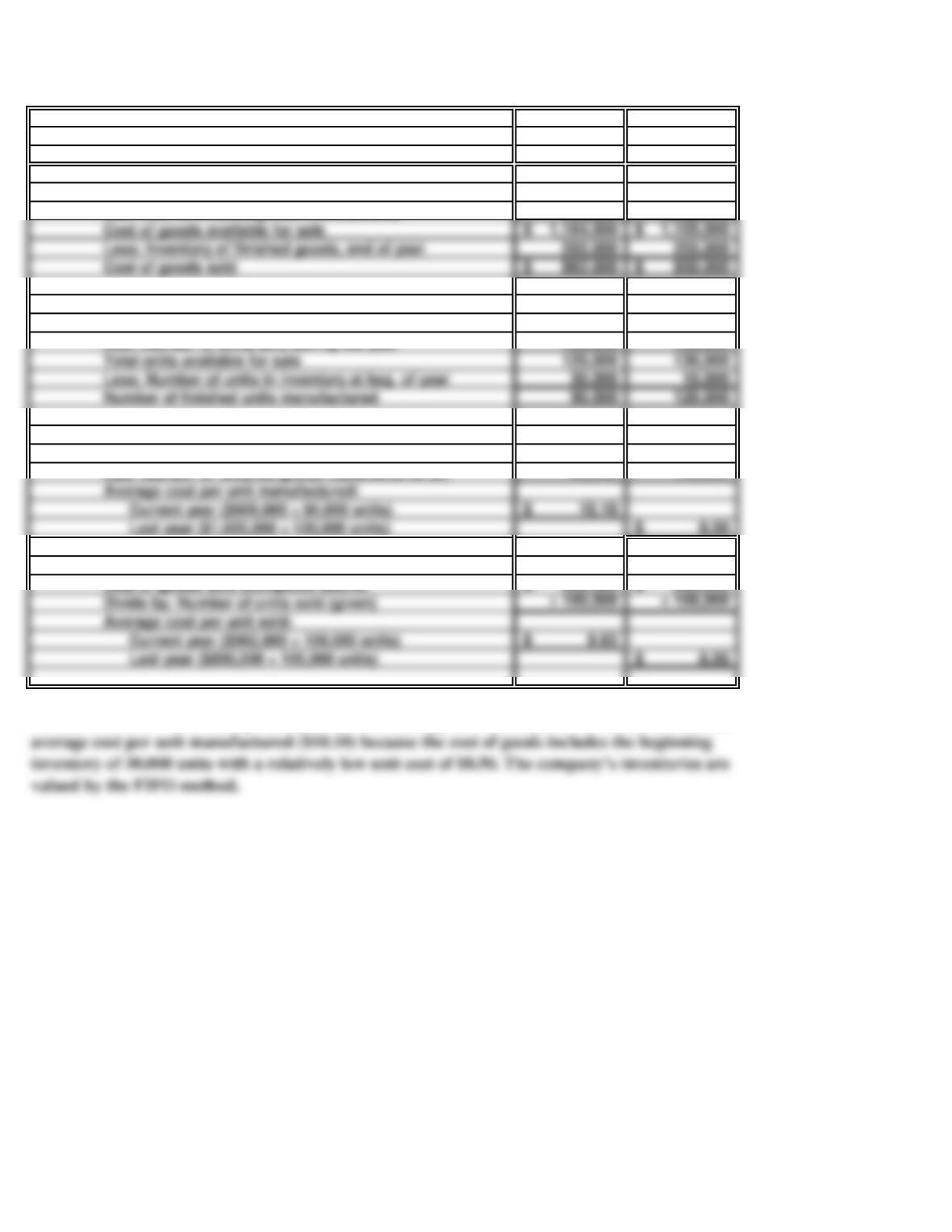

PRESCOTT MANUFACTURING

Current Last

Year Year

a. (1)

Inventory of finished goods, beginning of year 255,000$ 85,000$

Add: Cost of finished goods manufactured 909,000 1,020,000

(2)

Number of units in inventory at year-end 20,000 30,000

Add: Number of units sold during the year 100,000 100,000

Total units available for sale 120,000 130,000

Number of finished units manufactured 90,000 120,000

(3)

Cost of finished goods manufactured (given) 909,000$ 1,020,000$

Add: Number of finished goods manufactured (2) 90,000 120,000

(4)

Cost of goods sold (computed above) 962,000$ 850,000$

Divide by: Number of units sold (given) ÷ 100,000 ÷ 100,000

Note to instructor: The average cost per unit sold during the current year ($9.62) is less than the

Cost of goods sold:

Average cost of goods manufactured:

Average cost per unit sold:

Number of finished units manufactured:

Cost of goods available for sale 1,164,000$ 1,105,000$

Less: Inventory of finished goods, end of year 202,000 255,000

Cost of goods sold 962,000$ 850,000$

CASE 16.2

PRESCOTT MANUFACTURING (concluded)

b.

Note to instructor: The increase in the unit cost of finished goods manufactured (from $8.50 to

$10.10—an increase of approximately 19%) does not necessarily indicate poor performance. In

Evaluation of Walker’s statements:

Walker’s statements are misleading. He claims that his plant “has made real gains” in

Walker improperly computed the “manufacturing cost per unit sold.” He divided the cost of

CASE 16.3

PFIZER, INC.

INTERNET

a.

b.

c.

There are usually very few details regarding overhead contained in an annual report. One

of the more consistently reported overhead items is depreciation. Other overhead items

15 Minutes, Easy

Pfizer’s Inventories footnote shows the three typical categories of inventory—finished

By using the current and previous years’ Finished Goods balance sheet data and the

calculate the cost of finished goods manufactured:

CASE 16.4

CODE OF CONDUCT AT COCA-COLA

ETHICS, FRAUD & CORPORATE GOVERNANCE

a. T

b.

c. Th

45 Minutes, Medium

Potential concerns identified by the company that pertain to human rights violations

Potential concerns identified by the company that pertain to conflicts of interest include:

Potential concerns identified by the company that pertain to auditing, accounting, and