Brief

Exercises Topic Skills

B. Ex. 16.1 Product vs. period costs Analysis, communication

B. Ex. 16.2 Direct material used Analysis

B. Ex. 16.3 Cost of goods sold Analysis

B. Ex. 16.4 Materials inventory Analysis

B. Ex. 16.5 Direct labor journal entries Analysis

B. Ex. 16.6 Manufacturing overhead assigned Analysis

B. Ex. 16.7 Inventory balances Analysis

B. Ex. 16.8 Work in process balances Analysis

B. Ex. 16.9 Prime vs. conversion costs Analysis

B. Ex. 16.10 Partial balance sheet 16-3 Analysis

Exercises Topic Skills

16.1 Accounting terminology Analysis

16.2 Basic types of manufacturing costs Analysis

16.3 Product and period costs Analysis

16.4

Flow of costs through manufacturing

accounts

Analysis

16.5

Schedule of cost of finished goods

manufactured

Analysis

16.6

Flow of costs through manufacturing

accounts

16-3, 16-4, 16-

5

Analysis

16.7 Manipulating accounting figures

Analysis, communication,

judgment

16.8 Design of management accounting systems Analysis, judgment

16.9

Preparing an income statement using the cost

of finished goods manufactured

Analysis

16.10

Preparing an income statement using the cost

of finished goods manufactured

Analysis

16.11 Real World: General Electric Company 16-1 Analysis, judgment

Management accounting system design

16.12 Costs at Hobart Industries

16-3, 16-4, 16-

6

Analysis

16.13

Real World: Classifying costs at misc.

companies

Analysis

16-1

16-1

16-4, 16-6

16-4, 16-6

16-2, 16-3, 16-

5

16-4

16-3, 16-5

16-1–16-5

16-4

16-6

16-2

16-4

16-3, 16-4, 16-

5

16-4

16-2, 16-4

16-4

16-3, 16-4

Learning

Objectives

16-4, 16-5

CHAPTER 16

MANAGEMENT ACCOUNTING: A BUSINESS PARTNER

Learning

Objectives

OVERVIEW OF BRIEF EXERCISES, EXERCISES, PROBLEMS, AND CRITICAL

THINKING CASES

16-3

Exercises Topic Skills

16.14 Real World: Coca-Cola Company 16-2, 16-5 Analysis, judgment

Manufacturing costs at Coca-Cola

16.15 Real World: Home Depot 16-3 Analysis, research

Home Depot product vs. period costs

Sets A, B Skills

16.1 A,B An introduction to product costs 16-3, 16-4 Analysis, communication

16.2 A,B An introduction to product costs

16-2, 16-3,

16-4

Analysis

16.3 A,B

The flow of manufacturing costs through

ledger accounts

16-4 Analysis

16.4 A,B

The flow of manufacturing costs through

perpetual inventory records

16-4 Analysis

16.5 A,B

The flow of manufacturing costs: A

comprehensive problem

16-3, 16-4,

16-6

Analysis, communication

16.6 A,B

Determining and reporting product cost

information

16-4, 16-6 Analysis, communication

16.7 A,B

Determining unit costs using the cost of

finished goods manufactured

16-4, 16-6 Analysis

16.8 A,B Measuring unit costs

16-3, 16-4,

16-6

Analysis, communication,

judgment

16.1

Effects on income statement of errors in

handling manufacturing costs

16-3, 16-4,

16-6

Analysis, communication,

judgment

16.2 The Meadowbrooke miracle

16-2, 16-3,

16-4, 16-6

Analysis, communication,

judgment

16.3 Real World: Pfizer, Inc. 16-4, 16-6 Analysis, research,

(Internet)

technology

16.4 Real World: Coca-Cola Company 16-1, 16-3 Analysis, research,

Code of conduct at Coca-Cola

communication

(Ethics, fraud and corporate governance)

Critical Thinking Cases

Learning

Objectives

Problems

Topic

DESCRIPTIONS OF PROBLEMS AND CRITICAL THINKING CASES

Problems (Sets A and B)

16.1 A,B Aqua-Marine/Pinning, Inc. 20 Easy

A short introduction to the nature of product costs. In addition to

computing manufacturing costs, inventories, and the cost of good

sold, students are asked to explain how and when product costs are

deducted from revenue.

16.2 A,B

Road Warrior Corporation/River Queen Corporation 15 Easy

A short problem illustrating the flow of product costs through the

financial statements of a manufacturing company.

16.3 A,B Superior Locks, Inc./ISP, Inc. 20 Easy

Presented with an illustration of T accounts for a manufacturing

company, students are asked to identify important cost flows and

make computations illustrating key relationships. An excellent first

si

16.4 A,B Double Bar Corporation/Payback Corporation 20 Easy

A short problem that effectively acquaints students with the flow of

manufacturing costs through perpetual inventory accounts.

16.5 A,B Anditon Manufacturing/Valleyview Manufacturing 35 Medium

A short but comprehensive problem on the flow of manufacturing

costs through perpetual inventory records. Also requires

preparation of a schedule of the cost of finished goods

16.6 A,B Kitchen Gadget Co./Columbus Toy Co. 35 Strong

Prepare a schedule of the cost of finished goods manufactured,

determine the cost of goods sold and ending inventory, and explain

the “flow” of product costs.

16.7 A,B Idaho Paper Co./Cedar Company 25 Medium

Prepare a schedule of the cost of finished goods manufactured and

determine the manufacturing cost per unit. Use the unit cost

information to determine the ending inventory of finished goods

and cost of goods sold on a FIFO basis.

16.8 A,B

Raymond Engineering Co./Jackson Engineering Co. 40 Strong

Owner of a company in its first year of operations confuses

manufacturing costs with period costs, which leads him/her to think

that the business is failing. Student is asked to assign costs to

inventories, determine the unit cost of production, prepare a revised

income statement, and explain the shortcomings in the owner’s

original analysis.

Below are brief descriptions of each problem, case, and the first Internet assignment. These

descriptions are accompanied by the estimated time (in minutes) required for completion and by

a difficulty rating. The time estimates assume use of the partially filled-in working papers.

Critical Thinking Cases

16.1

West Texas Guitar Company 40 Strong

Student is presented with a poorly prepared income statement in

which inventories are ignored and all manufacturing costs and

operating expenses are included in the cost of goods sold.

Student is to identify the shortcomings in this income statement

and prepare a schedule of the cost of finished goods

manufactured and a corrected income statement.

16.2

Prescott Manufacturing 40 Strong

In a presentation to the board of directors, a plant manager

attributes the decline in the cost of finished goods manufactured

to increased efficiency. Students are asked to make several unit

cost computations and then to evaluate the manager’s claims.

Pfizer, Inc. 15 Easy

16.3

Internet

The student is asked to examine the notes to the financial

statements and describe the categories of inventories shown.

Information from the financial statements is then used to

calculate the cost of goods manufactured.

16.4

Code of Conduct at Coca-Cola 45 Medium

Ethics, Fraud, and Corporate Governance

Students research how the code of conduct at Coca-Cola helps

employees report ethics, fraud, or governance violations.

SUGGESTED ANSWERS TO DISCUSSION QUESTIONS

1. a.

Managerial accounting information is intended for use by managers of the business

b.

Managerial accounting information is intended to assist managers in planning and

2.

3.

4.

6.

7.

8.

9.

Benchmark studies show comparisons of companies within the same industry. They are

The Direct Labor account is debited for the cost of the direct labor payroll at each payroll date

and is credited as direct labor costs are assigned to products being manufactured. As

Three inventory control accounts that might be used by a manufacturing firm are materials

The three principles guiding the design of management accounting systems are: 1) to help

Since management accounting information is developed for use primarily by a company’s

Employees are made aware of their decision-making authority through various means such as

job descriptions, verbal instructions from supervisors, and management accounting system

The Materials Inventory account is debited for the cost of purchasing direct materials and

credited for the cost of materials used in the production process. As it is not possible to use

10.

11.

12.

13.

14.

(1)

The starting point is the beginning inventory of work in process, representing

15. a.

Management accountants need per-unit manufacturing information to assist managers in

The Work in Process Inventory account is debited for the costs of (1) direct materials used, (2)

direct labor costs assigned to production, and (3) manufacturing overhead costs assigned to

The Finished Goods Inventory account is debited for the cost of finished goods manufactured

The computation of the cost of finished goods manufactured in a schedule of the cost of finished

goods manufactured involves three steps:

No. Direct materials are those raw materials and parts that can be traced directly and

Five of the six accounts often have balances that appear in financial statements: the three

inventory accounts (Materials, Work in Process, and Finished Goods), the Direct Labor account,

and the Cost of Goods Sold account. Over the year, all overhead costs should be assigned to

production. Therefore, the Manufacturing Overhead account has a zero balance at year-end and

SOLUTIONS TO BRIEF EXERCISES

B. Ex. 16.1

B. Ex. 16.4

Balance, 1/1 $ 320,000

Purchases of

Balance, 12/31 $ 270,000

B. Ex. 16.6

Indirect labor payroll 370,000

Overhead costs

assigned to production

548,000

Indirect material costs 15,000

Direct Materials Inventory

CF Manufacturing Co. — Manufacturing Overhead

Coronado Boat Yard should not recognize any of the manufacturing costs on

B. Ex. 16.6

B. Ex. 16.8

Beginning Bal. 4/1 16,200$

Transferred to

Finished Goods

523,500$

Accounts Receivable ……………………………………………………..

B. Ex. 16.10

Current assets:

$540,000

Only product costs are debited to the Manufacturing Overhead account

Eskola Manufacturing

Work in Process Inventory

Partial Balance Sheet

At December 31

Cash and Cash Equivalents …………………………………………….

SOLUTIONS TO EXERCISES

Ex. 16.2

a.

g.

Manufacturing overhead

Direct materials

Direct product cost

Manufacturing overhead

Manufacturing overhead

Manufacturing overhead

Direct labor

Period cost

Period cost

Period cost

Period cost

Ex. 16.4 $ 35,000

Direct materials

Manufacturing costs applied to production:

Work in process inventory, beginning of the year ………………………..

a.

g.

Work in Process Inventory

Management accounting

Manufacturing overhead

None (These are prime costs.)

None (The statement describes direct manufacturing costs.)

Cost of finished goods manufactured

Period costs

Ex. 16.5 a.

$ 12,000

Manufacturing costs assigned to production:

Work in process inventory, Jan. 1 ………………………………………..

Direct materials used …………………………………………………

Direct labor used …………………………………………………

Less: Finished goods transferred out ………………………………….

Cost of finished goods transferred in ………………………………………….

Less: Cost of goods sold …………………………………………………………….

Manufacturing overhead assigned …………………………………….

Supervisor salaries ………………………………………………………………

Indirect labor costs ……………………………………………………………

Depreciation ……………………………………………………………………….

Less: Manufacturing overhead assigned …………………………………………

Factory utilities ……………………………………………………………..

Factory insurance ……………………………………………………………

Property taxes on factory ………………………………………………….

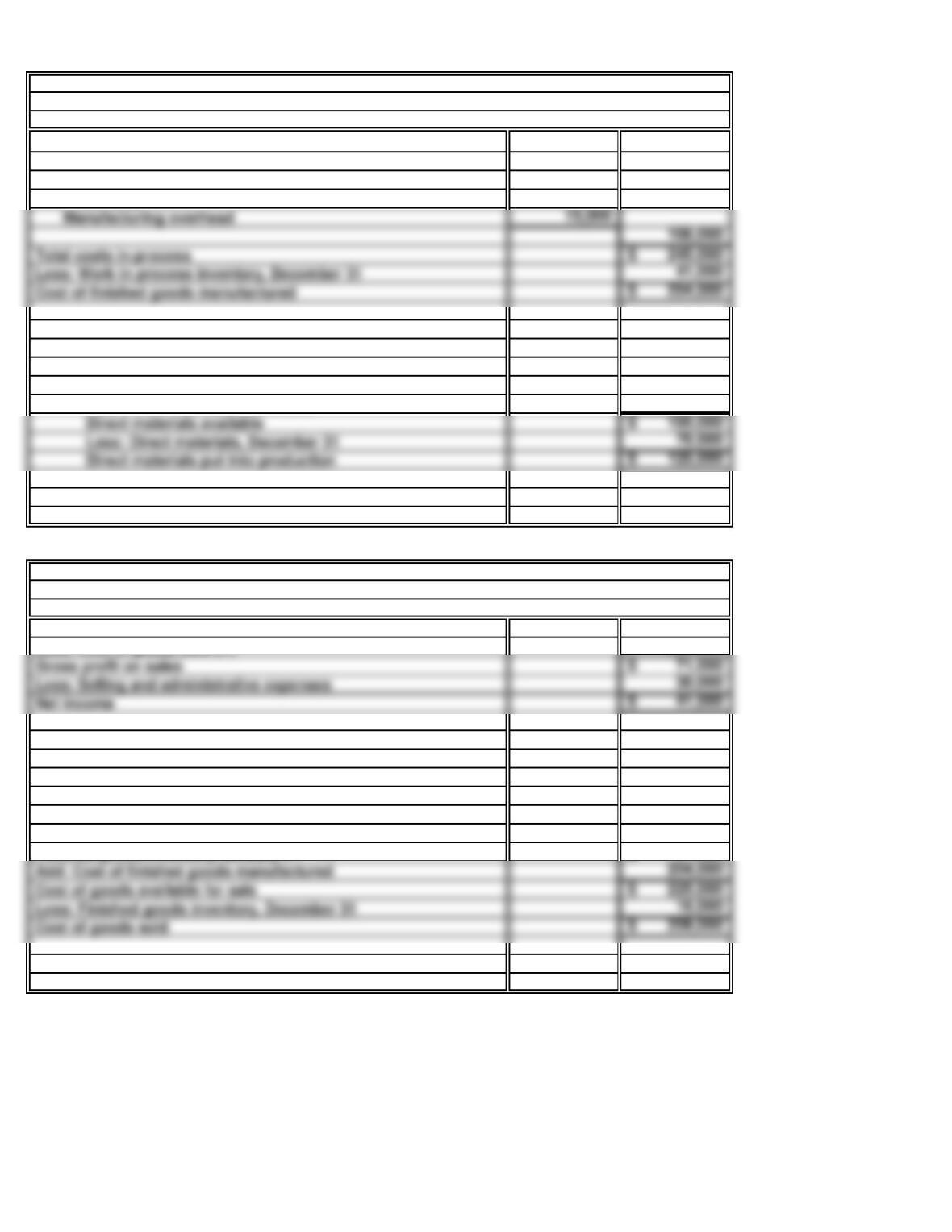

Ex. 16.6 a. 89,200$

335,750

(326,000)

b. $ 0

13,500

Manufacturing overhead, Jan. 1 ……………………………………….

Indirect materials purchased …………………………………………………….

NuTronics, Inc.

Schedule of the Cost of Finished Goods Manufactured

Direct materials inventory, Jan. 1 ………………………………………

Work in process, January 1 ………………………………….

Less: Direct materials used in production …………………………..

For the Year Ended December 31

Direct materials purchased …………………………………….

Cost of finished goods manufactured …………………………………

Ex. 16.6 c.

(continued)

$ 1,550,000

Ex. 16.7

Ex. 16.8

1.

The answer to this question depends upon one’s interpretation of the word

The decision-making authority for incurring costs at the plant level is not

under the complete control of Sheila. Thus, even though Sheila is held

The Bastile Furniture Company’s management accounting system has these

three problems:

Operating income for the month of January:

Revenues ……………………………………………………………………….

$ 208,200

Cost of goods sold ………………………………………………………

Gross profit …………………………………………………………….

Ex. 16.9

a.

Work in process inventory, January 1 60,000$

Add: Manufacturing costs assigned to production:

(1) Computation of direct materials used:

Direct materials, January 1 40,000$

Add: Direct materials purchased 40,000

Less: Direct materials, December 31 10,000

Direct materials put into production 70,000$

b.

Sales 250,000$

(1) The company’s cost of goods sold figure is based

on the following flow of costs through production

to finished goods:

Finished goods inventory, January 1 42,000$

Add: Cost of finished goods manufactured 140,000

Income Statement

For the Year Ended December 31

ANTHONY COMPANY

Schedule of the Cost of Finished Goods Manufactured

For the Year Ended December 31

ANTHONY COMPANY

Ex. 16.10

a.

Work in process inventory, January 1 79,000$

Add: Manufacturing costs assigned to production:

Direct materials used (1)125,000$

Direct labor 22,000

(1) Computation of direct materials used:

Direct materials, January 1 60,000$

Add: Direct materials purchased 135,000

Direct materials available 195,000$

Less: Direct materials, December 31 70,000

Direct materials put into production 125,000$

b.

Sales 280,000$

Less: Cost of goods sold (1)209,000

Gross profit on sales 71,000$

(1) The company’s cost of goods sold figure is based

on the following flow of costs through production

to finished goods:

Finished goods inventory, January 1 21,000$

Cost of goods available for sale 225,000$

Income Statement

For the Year Ended December 31

RANDOLPH COMPANY

Schedule of the Cost of Finished Goods Manufactured

For the Year Ended December 31

RANDOLPH COMPANY

Total costs in process 245,000$

Ex. 16.11

Ex. 16.15

General Electric’s actions reflect the three design principles of management

Cost of Sales includes the actual cost of merchandise sold and services performed,

the cost of transportation of merchandise from vendors to the Company’s stores,

locations or customers, shipping and handling costs from the Company’s stores,

SOLUTIONS TO PROBLEMS SET A

20 Minutes, Easy

PROBLEM 16.1A

AQUA-MARINE

a. Computations of amounts:

(1) Average per-unit manufacturing cost:

Cost of finished goods manufactured 728,000$

Number of completed units manufactured 112

Average cost per unit ($728,000 ÷ 112 units) 6,500$

Ending finished goods inventory:

Average per-unit manufacturing cost [part (1) ]6,500$

Number of finished goods in inventory

(112 manufactured, less 100 sold) 12

Ending inventory of finished goods

(12 units × $6,500 per unit) 78,000$

(3) Cost of goods sold:

Average per-unit manufacturing cost [part (1) ]6,500$

Alternative computation:

(2) Ending materials inventory:

Ending work in process inventory:

Manufacturing costs charged to work in process:

Direct materials used 216,000$

Direct labor assigned to production 200,000

PROBLEM 16.1A

AQUA-MARINE (concluded)

b.

775,000$

The disposition of the $775,000 in manufacturing costs “incurred” during the year is

summarized below:

Comments on deducting manufacturing costs from revenue:

Total manufacturing costs “incurred” during the year

Less: Amounts representing inventory at year-end:

15 Minutes, Easy

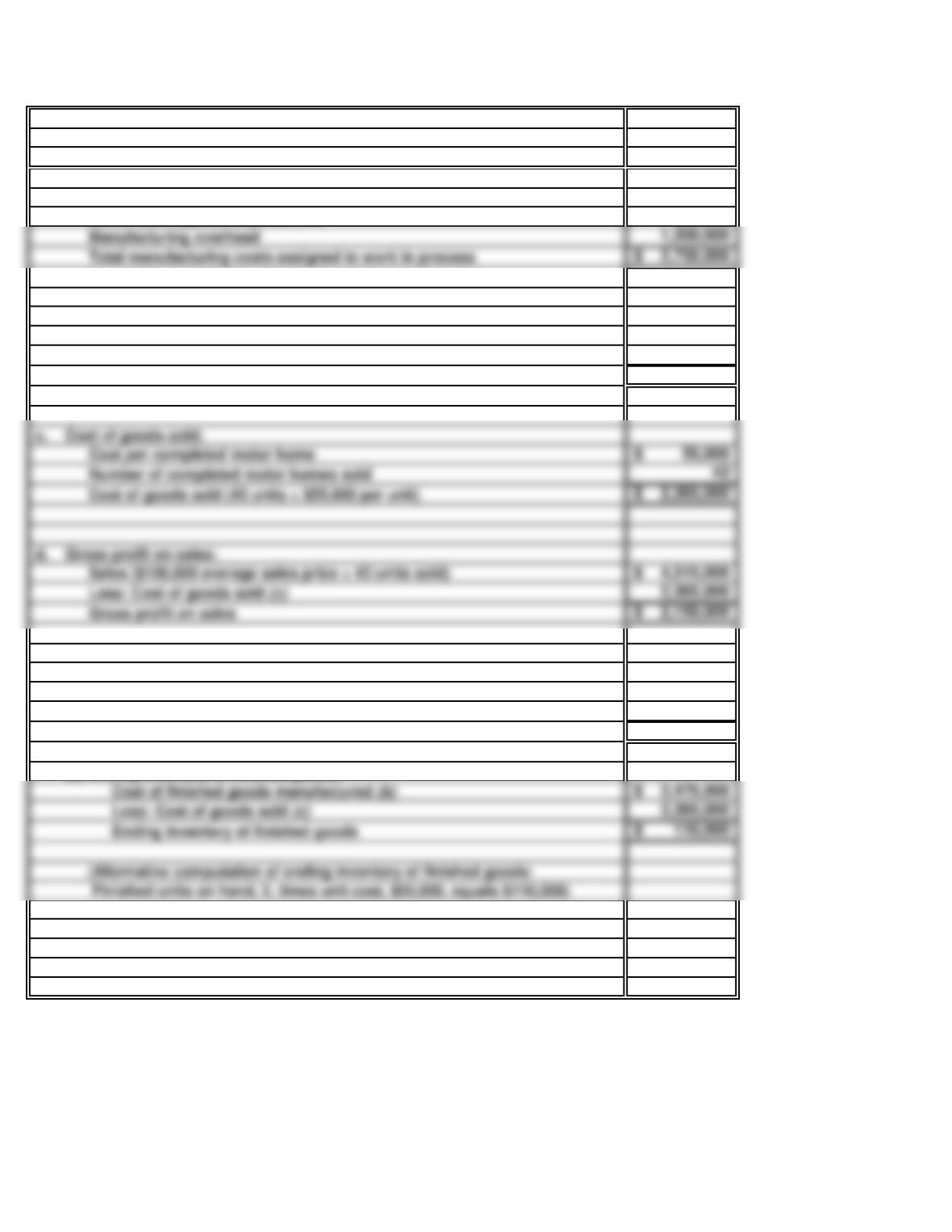

PROBLEM 16.2A

ROAD WARRIOR CORPORATION

a. Total manufacturing costs assigned to work in process:

Direct materials used

750,000$

Direct labor applied to production 800,000

b. Cost of finished goods manufactured:

Cost per completed motor home

55,000$

Number of motor homes completed during the year 45

Cost of finished goods manufactured (45 units × $55,000 per unit) 2,475,000$

55,000$

Number of completed motor homes sold 43

Cost of goods sold (43 units × $55,000 per unit) 2,365,000$

Gross profit on sales 2,150,000$

e. (1) Ending inventory of work in process:

Total manufacturing costs assigned to work in process (a) 2,750,000$

Less: Cost of finished goods manufactured (b) 2,475,000

Ending inventory of work in process 275,000$

(2) Ending inventory of finished goods:

Less: Cost of goods sold (c) 2,365,000

15 Minutes, Easy

PROBLEM 16.3A

SUPERIOR LOCKS, INC.

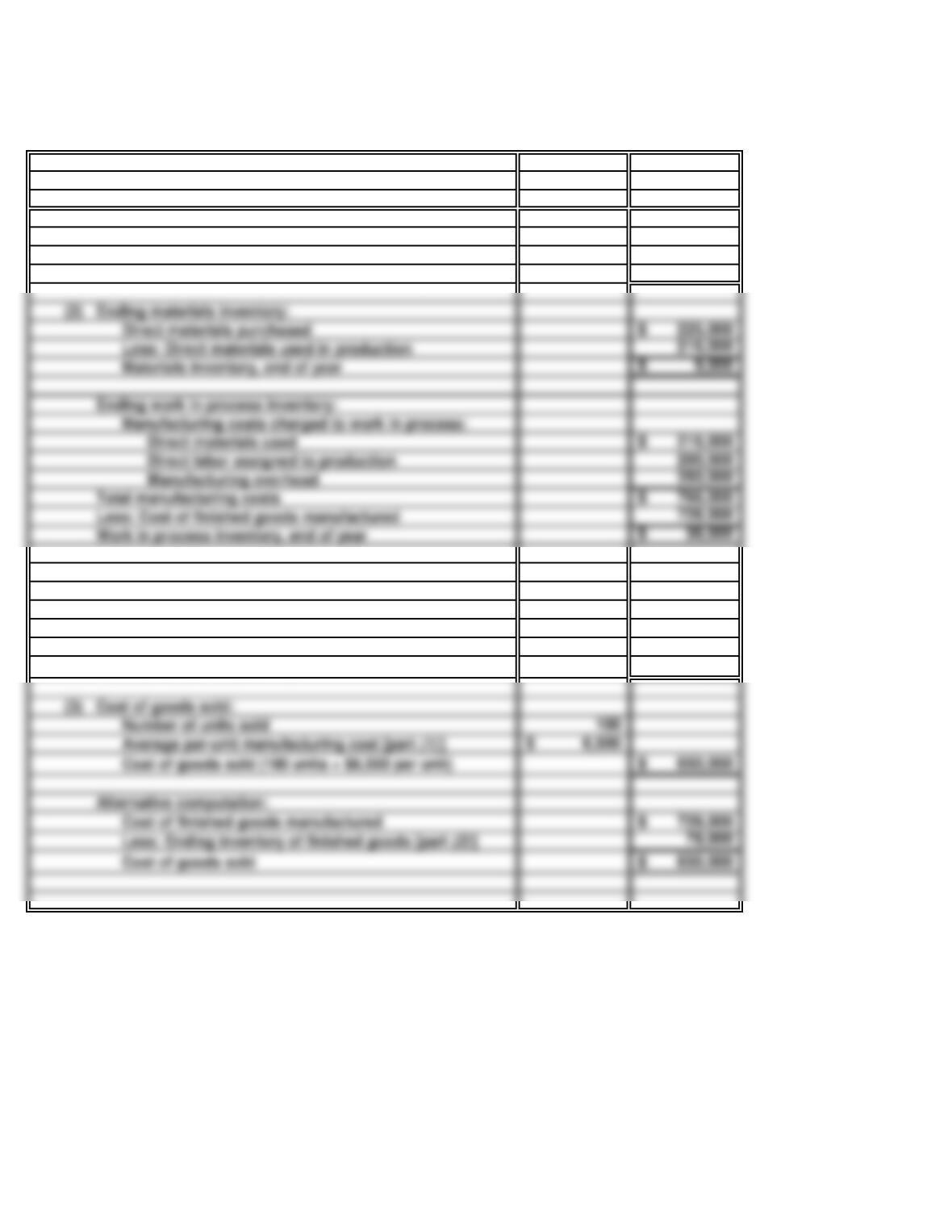

a. Purchases of direct materials 269,000$

b. Cost of direct materials used:

Materials inventory, beginning of year 13,000$

Add: Purchases of direct materials 269,000

e. Total manufacturing costs:

Direct materials used (part b)265,000$

Direct labor costs 134,000

Manufacturing overhead 214,400

Total manufacturing costs 613,400$

f. Cost of finished goods manufactured 614,400$

g. Ending inventory of work in process:

Work in process inventory, beginning of year 19,000$

Cost of all goods in process during the year 632,400$

Work in process inventory, end of year 18,000$

h. Cost of goods sold:

Beginning inventory of finished goods 46,000$

Add: Cost of finished goods manufactured 614,400

Cost of goods available for sale 660,400$

Less: Ending inventory of finished goods 53,400

Cost of goods sold 607,000$

i. Total inventory at year-end:

Work in process (part g)18,000

Finished goods 53,400

Cost of materials available for use 282,000$

Less: Materials inventory, end of year 17,000

Cost of direct materials used 265,000$

20 Minutes, Easy

PROBLEM 16.4A

DOUBLE BAR CORPORATION

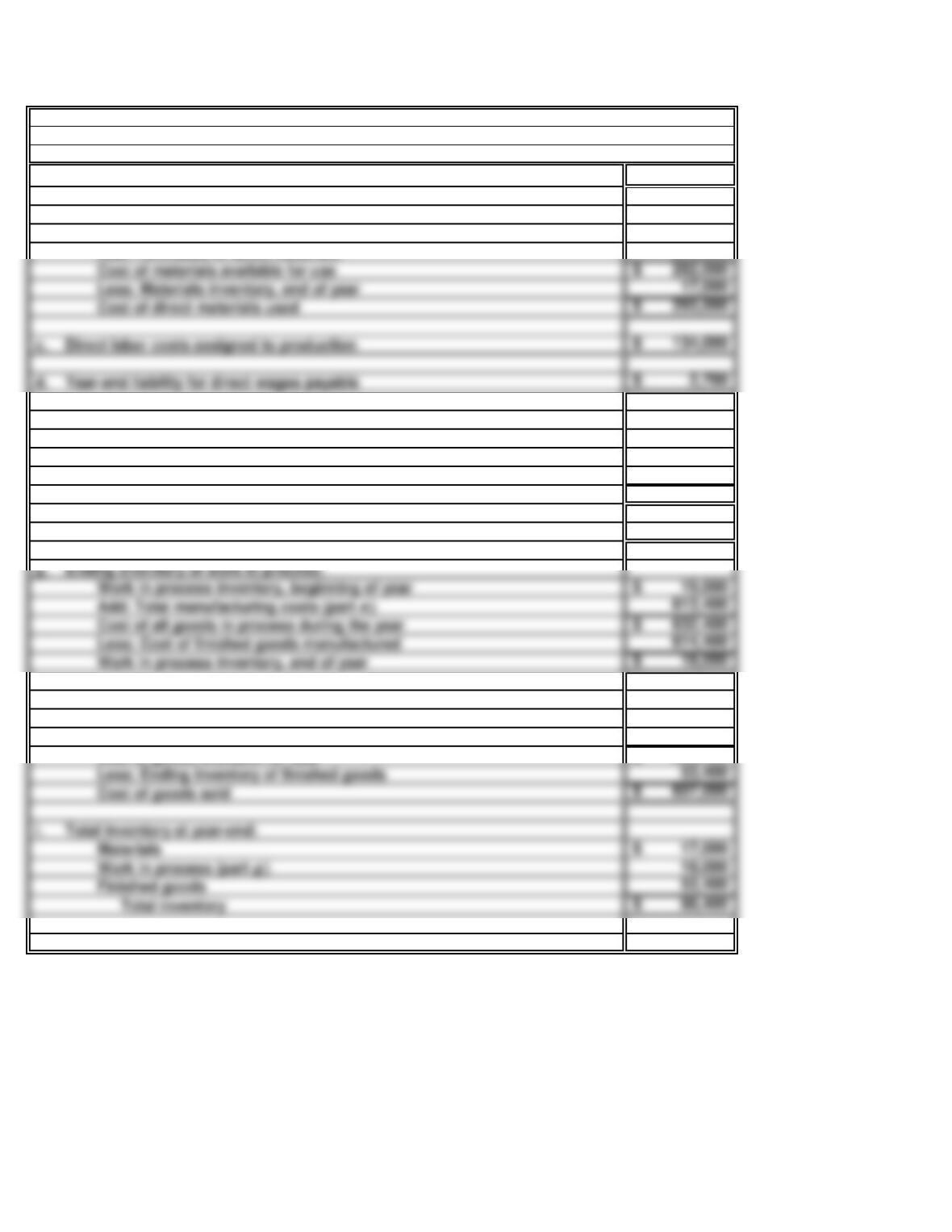

a. Purchases of direct materials 355,000$

b. Direct materials used:

Materials inventory, beginning of year 16,000$

Add: Purchases of direct materials 355,000

Cost of direct materials available for use 371,000$

Less: Materials inventory, end of year 13,000

Cost of direct materials used 358,000$

f. Cost of finished goods manufactured:

Work in process inventory, beginning of year 21,000$

Add: Total manufacturing costs (part e)958,000

Cost of all goods in process during the year 979,000$

Less: Work in process inventory, end of year 25,000

Cost of finished goods manufactured 954,000$

g. Cost of goods sold:

Beginning inventory of finished goods 106,000$

Add: Cost of finished goods manufactured (part f)954,000

Cost of goods available for sale 1,060,000$

Less: Ending inventory of finished goods 118,000

Cost of goods sold 942,000$

h. Total inventory at year-end:

Finished goods inventory 118,000

Total manufacturing costs charged to work in process 958,000$

35 Minutes, Medium

PROBLEM 16.5A

ANDITON MANUFACTURING

a. (1) Direct materials purchased 2,410,000$

(2) Direct materials used:

Materials inventory, beginning of year

222,000$

Add: Purchases of direct materials 2,410,000

(5) Total manufacturing costs:

Direct materials used [part a (2) ]2,506,000$

Direct labor cost 992,000

Manufacturing overhead 893,600

Total manufacturing costs 4,391,600$

(6) Cost of finished goods manufactured:

Work in process inventory, beginning of year

75,000$

Add: Total manufacturing costs [part a (5) ]4,391,600

Cost of all goods in process during the year 4,466,600$

Less: Work in process inventory, end of year 109,000

Cost of finished goods manufactured 4,357,600$

(7) Cost of goods sold:

238,000$

Add: Cost of finished goods manufactured [part a (6) ]4,357,600

Cost of goods available for sale 4,595,600$

Less: Ending inventory of finished goods 325,000

Cost of goods sold 4,270,600$

(8) Total inventory:

Materials inventory

126,000$

Work in process inventory 109,000

Finished goods inventory 325,000

Total inventory 560,000$

Cost of direct materials available for use 2,632,000$

Less: Materials inventory, end of year 126,000

Cost of direct materials used 2,506,000$