1. a. An assembly-type industry using mass production methods, such as TV assembly, would

use the process cost system because the products are somewhat standard and lose their

2. Since all goods produced in a process cost system are identical units, it is not necessary to

3. In a process cost system, the direct labor and factory overhead applied are debited to the

work in process accounts of the individual production departments in which they occur. The

4. The cost per equivalent unit is frequently determined separately for direct materials and

5. The cost per equivalent unit is used to allocate direct materials and conversion costs between

completed and partially completed units.

7. The most important purpose of the cost of production report is to assist in the control of

8. Cost of production reports can provide detailed data about the process. The reports can

CHAPTER 18 (FINMAN); CHAPTER 3 (MAN)

PROCESS COST SYSTEMS

DISCUSSION QUESTIONS

DISCUSSION QUESTIONS (Continued)

9. Yield is a measure of the materials usage efficiency of a process manufacturer. It is

10. Just-in-time processing emphasizes combining process functions into manufacturing cells,

PE 18–1A (FINMAN); PE 3–1A (MAN)

Shipbuilding Job order

Gasoline refining Process

PE 18–1B (FINMAN); PE 3–1B (MAN)

Steel manufacturing Process

Business consulting Job order

PE 18–2A (FINMAN); PE 3–2A (MAN)

PE 18–2B (FINMAN); PE 3–2B (MAN)

PRACTICE EXERCISES

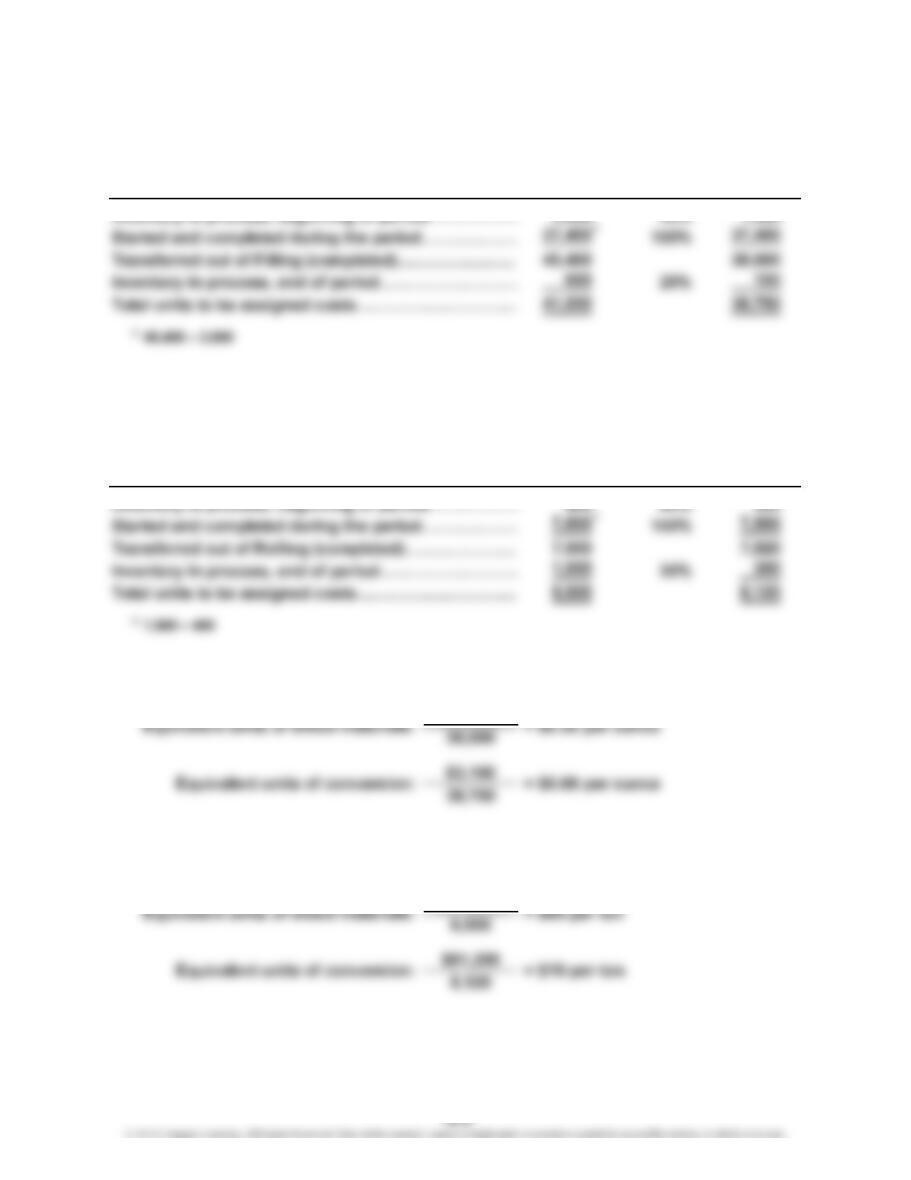

PE 18–3A (FINMAN); PE 3–3A (MAN)

Percent

Total Materials Equivalent

Whole Added In Units for

Units Period Materials

PE 18–3B (FINMAN); PE 3–3B (MAN)

Percent

Total Materials Equivalent

Whole Added In Units for

Units Period Materials

PE 18–4A (FINMAN); PE 3–4A (MAN)

Percent

Total Conversion Equivalent

Whole Completed Units for

Units in Period Conversion

PE 18–4B (FINMAN); PE 3–4B (MAN)

Percent

Total Conversion Equivalent

Whole Completed Units for

Units in Period Conversion

PE 18–5A (FINMAN); PE 3–5A (MAN)

$13,300

PE 18–5B (FINMAN); PE 3–5B (MAN)

$510,000

PE 18–6A (FINMAN); PE 3–6A (MAN)

Direct

Materials Conversion Total

Costs Costs Costs

Inventory in process, balance…………………………

…

$ 1,200

Inventory in process, beginning of period…………

…

0 + 1,200 × $0.08 96

PE 18–6B (FINMAN); PE 3–6B (MAN)

Direct

Materials Conversion Total

Costs Costs Costs

Inventory in process, balance…………………………

…

$ 25,000

Inventory in process, beginning of period…………

…

0 + 320 × $10 3,200

…

…

…

…

…

…

PE 18–7A (FINMAN); PE 3–7A (MAN)

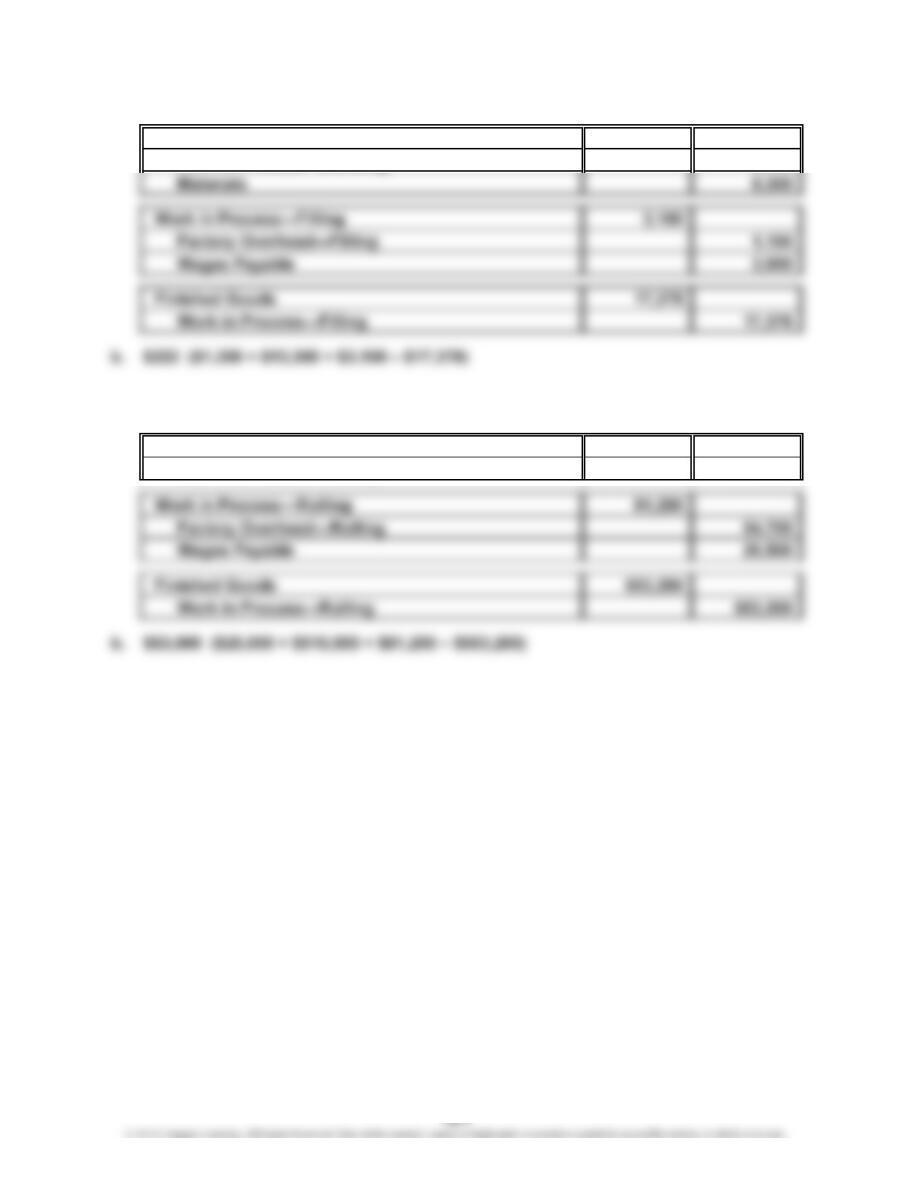

a. Work in Process—Filling 13,300

Work in Process—Blending 5,000

PE 18–7B (FINMAN); PE 3–7B (MAN)

a. Work in Process—Rolling 510,000

Work in Process—Casting 510,000

PE 18–8A (FINMAN); PE 3–8A (MAN)

$14,875

42,500

PE 18–8B (FINMAN); PE 3–8B (MAN)

$76,000

800

Material cost per ton, September: = $95

Energy cost per pound, June: = $0.35

Ex. 18–1 (FINMAN); Ex. 3–1 (MAN)

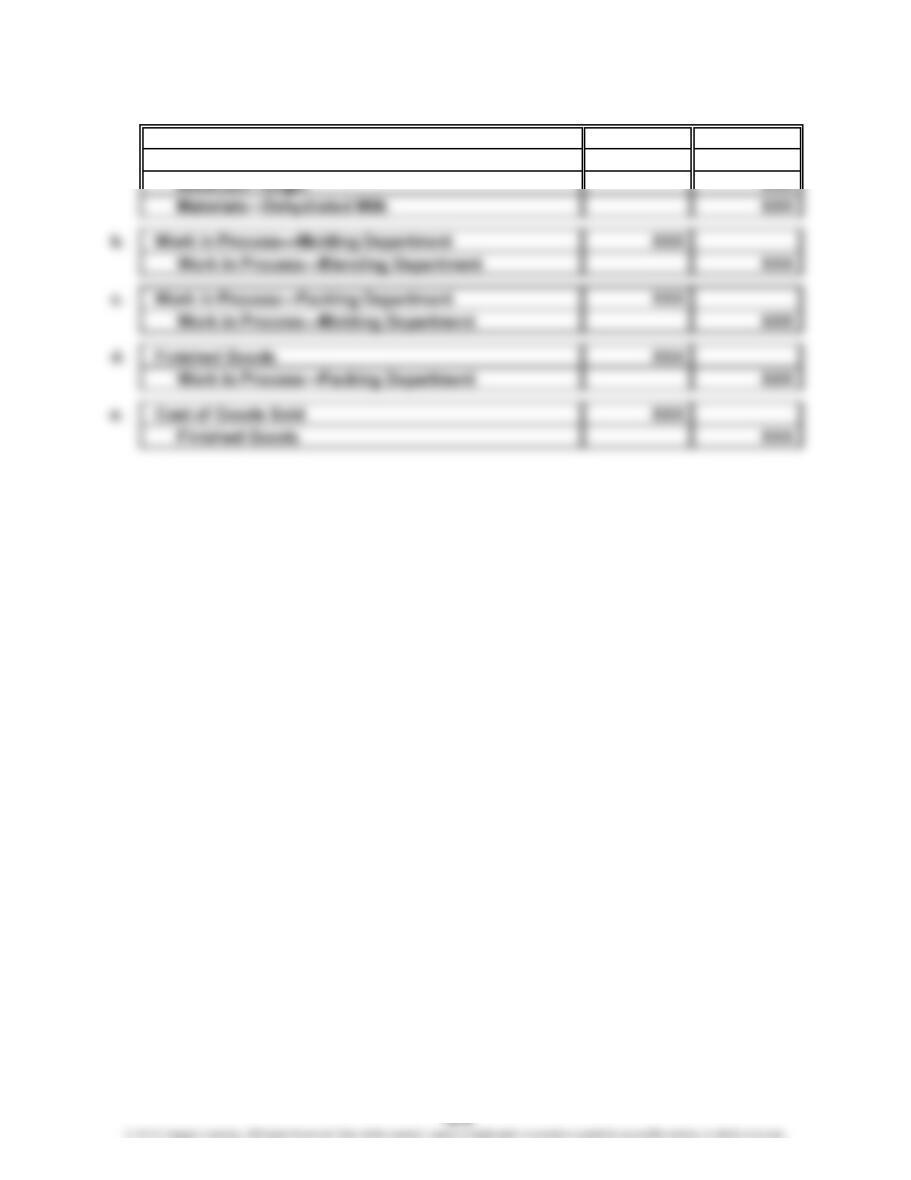

a. Work in Process—Blending Department XXX

Materials—Cocoa XXX

Ex. 18–2 (FINMAN); Ex. 3–2 (MAN)

Materials

Factory Overhead—

Smelting Dept. Smelting Dept.

Work in Process—

Ex. 18–3 (FINMAN); Ex. 3–3 (MAN)

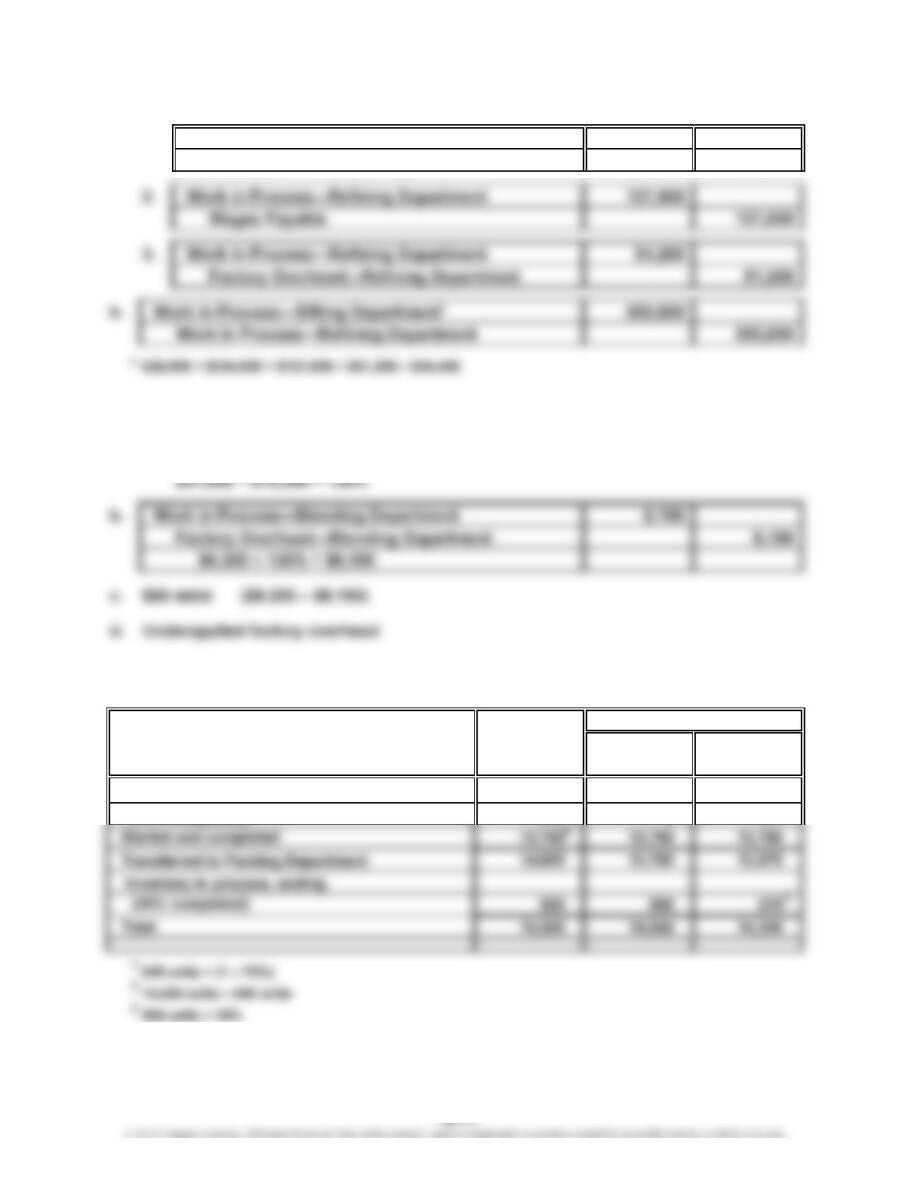

a. 1. Work in Process—Refining Department 335,000

Materials 335,000

Ex. 18–4 (FINMAN); Ex. 3–4 (MAN)

a. Factory overhead rate:

Ex. 18–5 (FINMAN); Ex. 3–5 (MAN)

Whole Direct

Units Materials Conversion

Inventory in process, beginning

(75% completed) 840 0 210

Equivalent Units

1

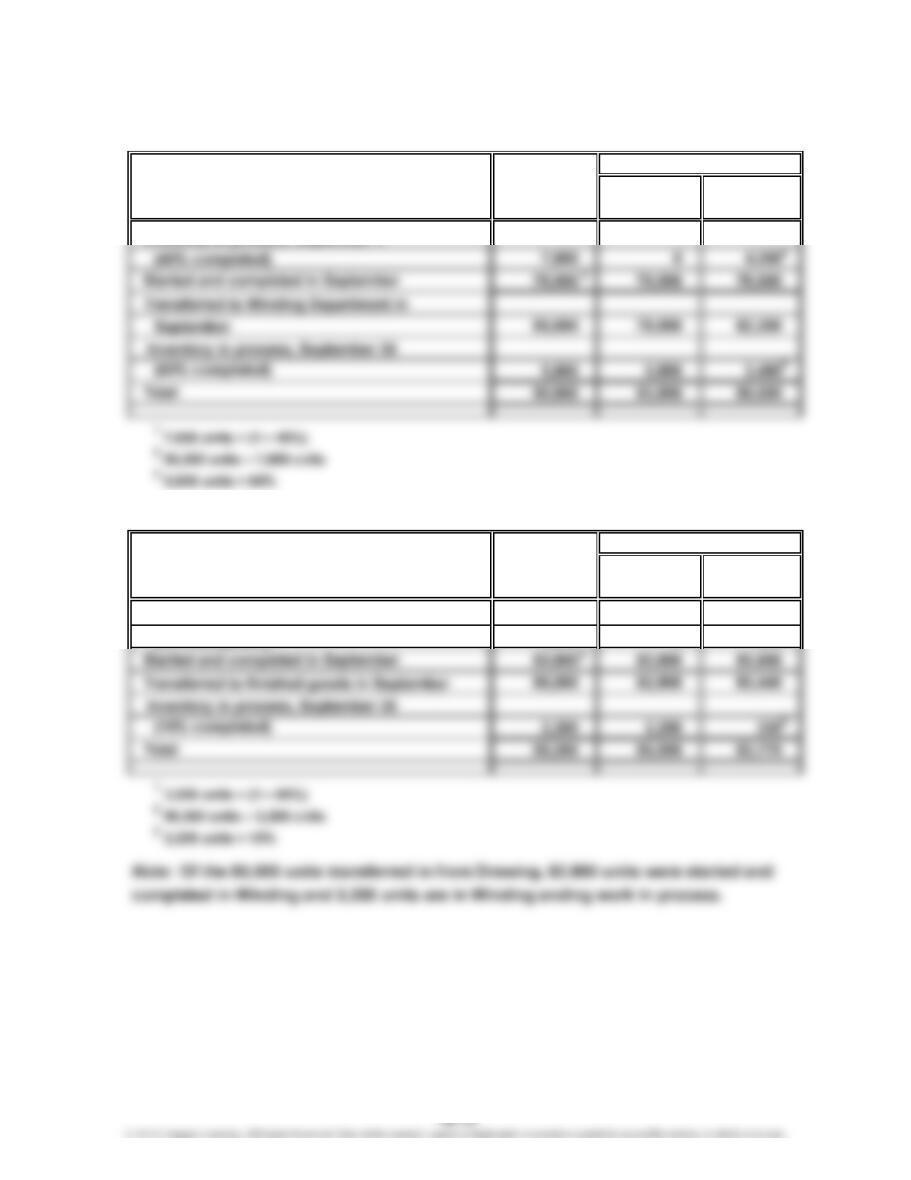

Ex. 18–6 (FINMAN); Ex. 3–6 (MAN)

a. Drawing Department

Whole Direct

Units Materials Conversion

Inventory in process, September 1

b. Winding Department

Whole Direct

Units Materials Conversion

Inventory in process, September 1

(80% completed) 3,200 0 640

Equivalent Units

Equivalent Units

1

Ex. 18–7 (FINMAN); Ex. 3–7 (MAN)

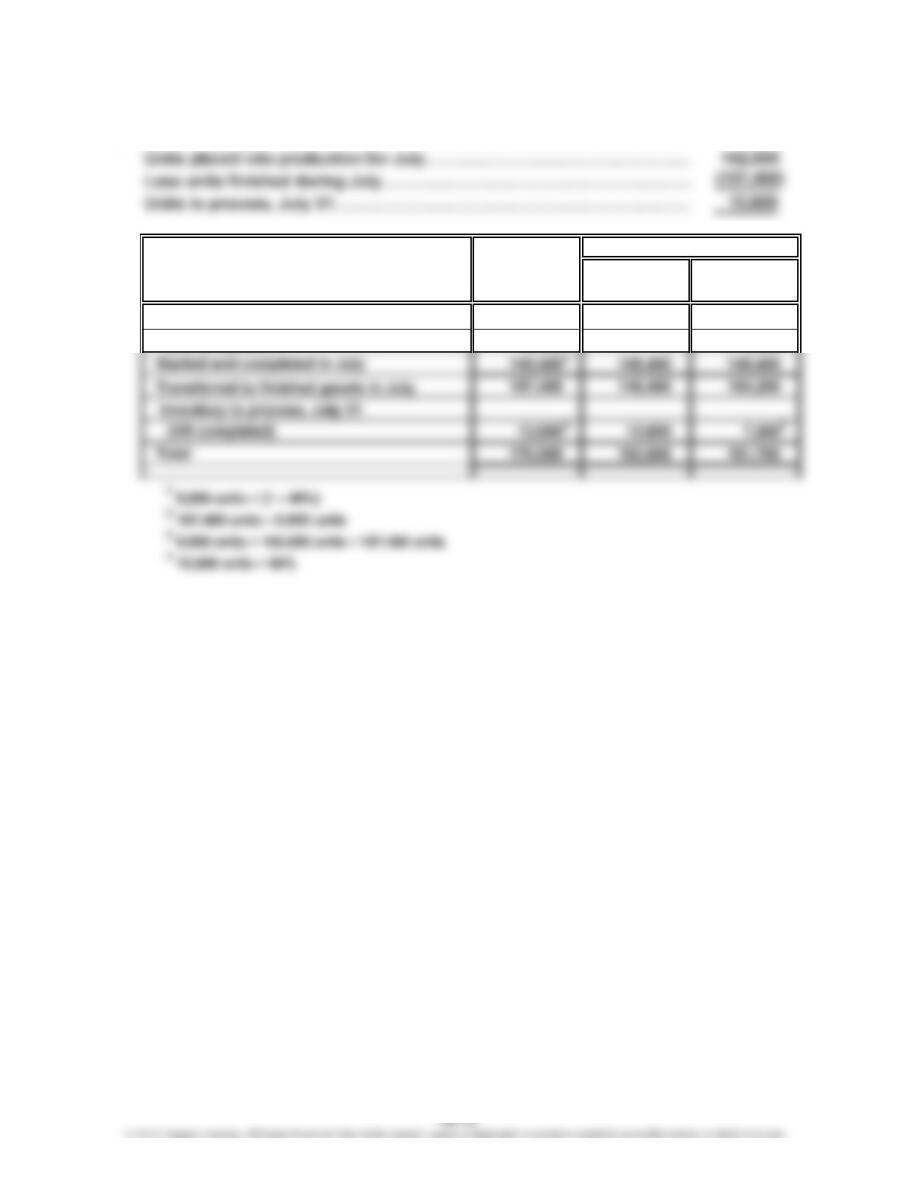

a. Units in process, July 1…………………………………………………………

…

8,000

b.

Whole Direct

Units Materials Conversion

Inventory in process, July 1

(2/5 completed) 8,000 0 4,800

Equivalent Units

1

Ex. 18–8 (FINMAN); Ex. 3–8 (MAN)

a. 1. $1.90 ($307,800 ÷ 162,000 units)

4. $343,620 [($1.90 + $0.40) × 149,400 units]

5. $26,964, determined as follows:

b. The conversion costs in July decreased by $0.03 per equivalent unit,

determined as follows:

Ex. 18–9 (FINMAN); Ex. 3–9 (MAN)

Equivalent units of production:

Conversion

Cereal Boxes Cost

(in pounds) (in boxes) (in boxes)

Inventory in process, March 1……………

…

0 0 600

Supporting explanation:

The whole unit inventory in process on March 1 includes both the cereal in the

hopper and the boxes in the carousel, and thus includes no equivalent units for

Note to Instructors: An actual cereal-filling line begins with the empty box

carousel. The box carousel holds flattened boxes that are fed into a high-speed

…

Ex. 18–10 (FINMAN); Ex. 3–10 (MAN)

a. Direct labor…………………………………………………………………………

…

$36,705

b. Equivalent units of production for conversion costs:

…

Conversion cost per equivalent unit:

c. Equivalent units of production for direct materials costs:

Beginning inventory……………………………………………………………

…

0

Ex. 18–11 (FINMAN); Ex. 3–11 (MAN)

a. Units in process at beginning of period………………………………………

…

900

b.

Whole Direct

Units Materials Conversion

Inventory in process, beginning

c.

Direct

Materials Conversion

Total costs for period in Assembly Department $336,000 $194,796

Equivalent Units

Costs

1

*

…

Ex. 18–12 (FINMAN); Ex. 3–12 (MAN)

a. 1. $29,470; determined as follows:

2. Cost of beginning work in process…………………………………………

…

$ 29,470

3. $16,896; determined as follows:

Direct materials ($21.00 × 640 units)………………………………………… $ 13,440

b. Yes. The production costs per unit increased during the current period. The

c. The conversion cost in the current period increased by $0.73 per equivalent

unit, determined as follows:

…

Ex. 18–13 (FINMAN); Ex. 3–13 (MAN)

1. In computing the equivalent units for conversion costs applicable to the June 1

2. In computing the equivalent units for conversion costs for units started and

completed in June, the June 1 inventory of 6,400 units, rather than the June 30

3. The correct equivalent units for conversion costs should be 53,400, determined

as follows:

To process units in inventory on June 1:

Ex. 18–14 (FINMAN); Ex. 3–14 (MAN)

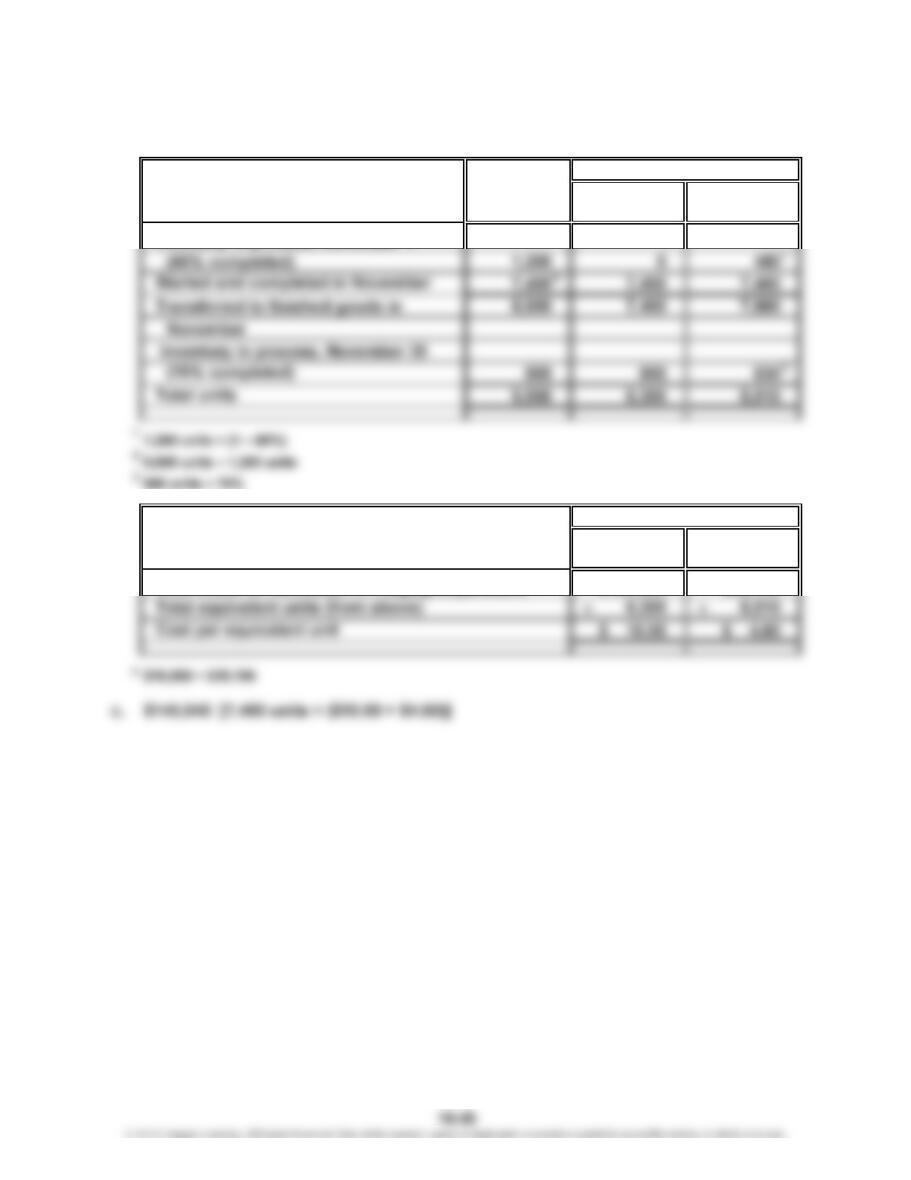

a. 8,600 units (1,200 + 8,300 – 900)

b.

Whole Direct

Units Materials Conversion

Inventory in process, November 1

Direct

Materials Conversion

Total costs for November in Forging Department $124,500 $39,146

Equivalent Units

Costs

*